Singapore HDB Inheritance and Transfer Guide 2026: Joint Tenancy, CPF Rules and Who Can Inherit

Quick Answer: Singapore HDB Inheritance & Transfer Guide 2026

- HDB flats held under Joint Tenancy (JT) pass automatically to the surviving owner by right of survivorship — no probate required and no Will can override this.

- Flats held under Tenancy-in-Common (TIC) pass according to the deceased’s Will or, if there is no Will, the Intestate Succession Act (ISA). Muslim estates are governed by the Administration of Muslim Law Act (AMLA) and Faraid rules.

- The deceased owner’s CPF principal and accrued interest used for the flat is refunded to their CPF account — not to the estate — and distributed to CPF nominees or the CPF Public Trustee.

- Any outstanding HDB loan on the flat must be assumed by the inheriting owner (subject to HDB approval) or discharged; the flat cannot be retained if the inheritor cannot service the loan.

- The inheritor must meet HDB eligibility criteria to retain the flat. Ineligible inheritors (including foreigners) must sell within 6 months or HDB may compulsorily acquire the flat.

- Singapore Citizens generally have the widest inheritance eligibility; SPRs and family members in non-standard situations require case-by-case HDB assessment.

- The Minimum Occupation Period (MOP) typically restarts from the date of the transfer for the new owner when the flat is transferred (other than via JT survivorship).

- Making a Will and CPF nomination while alive is the single most important step HDB owners can take to ensure their wishes are carried out on death.

Introduction: When a HDB Owner Passes Away

The death of a Housing & Development Board (HDB) flat owner raises a series of consequential legal and practical questions: Who takes over the flat? What happens to the outstanding mortgage? Are there CPF refunds? How long does the process take? For the 1.1 million HDB households in Singapore, understanding the inheritance and transfer rules is not just academic — it is part of responsible property ownership and estate planning.

Singapore’s framework for HDB flat inheritance is governed by several bodies of law operating concurrently: HDB’s own eligibility and transfer rules, the Conveyancing and Law of Property Act which recognises the right of survivorship for Joint Tenancy, the Intestate Succession Act (ISA) which distributes estates without Wills, and — for Muslim Singaporeans — the Administration of Muslim Law Act (AMLA) and the principles of Faraid Islamic inheritance. The CPF Board administers the refund of CPF monies on death separately from the flat transfer.

HDB Flat Ownership Structures: Joint Tenancy vs Tenancy-in-Common

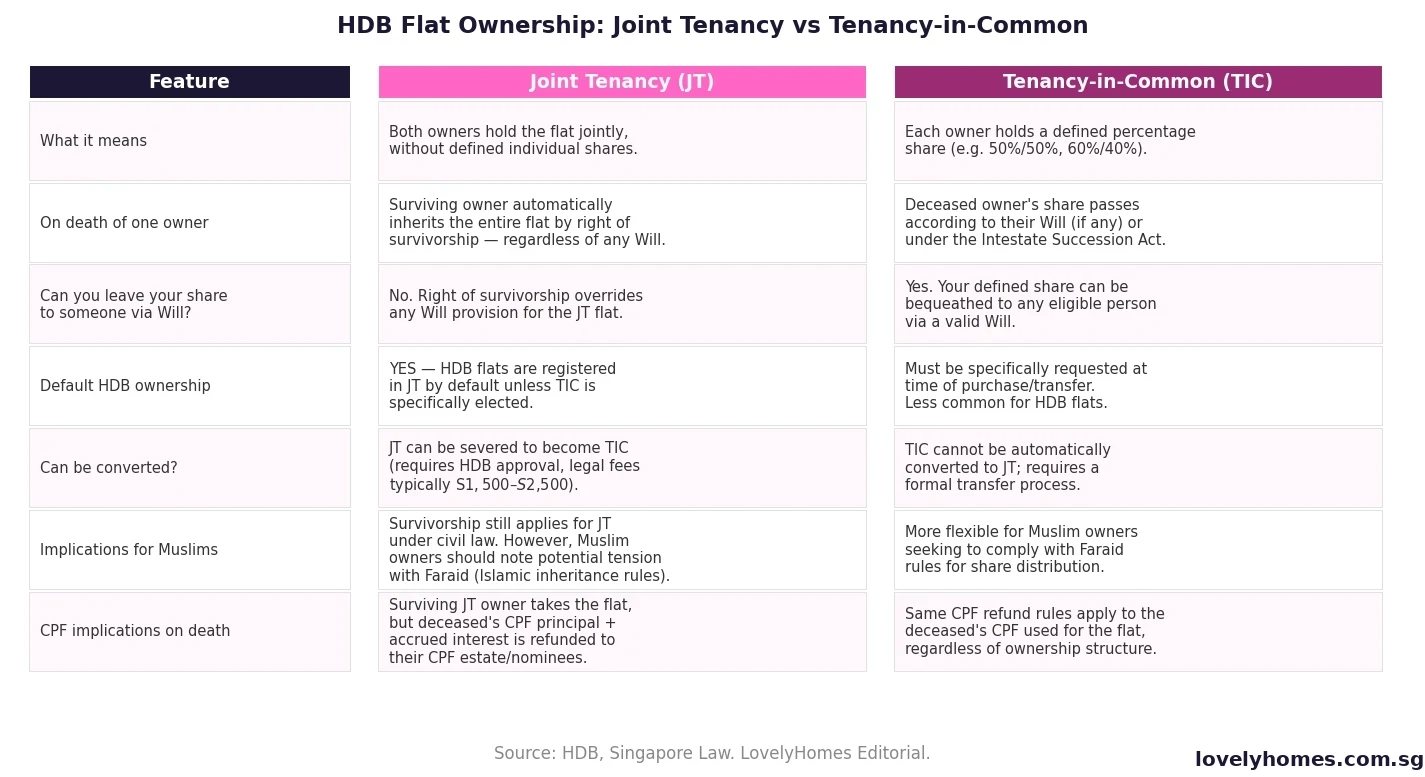

When two or more people purchase an HDB flat together, they must choose between two forms of co-ownership: Joint Tenancy (JT) or Tenancy-in-Common (TIC). The choice made at purchase has profound consequences on what happens to the flat when one owner dies.

Under Joint Tenancy, all owners hold the flat jointly without defined individual shares. The central legal feature of JT is the right of survivorship: on the death of any one joint tenant, that person’s interest in the flat automatically vests in the surviving joint tenant(s). No probate or letters of administration are required; no Will can override this automatic transfer. HDB flats purchased by couples are registered in Joint Tenancy by default.

Under Tenancy-in-Common, each owner holds a specified, separate share — for example, 50%/50% or 60%/40%. On the death of a TIC owner, their share forms part of their estate and is distributed according to their Will, or the ISA if they die intestate (without a Will). TIC must be specifically elected at the time of purchase or during ownership via a legal severance of the JT arrangement.

The Right of Survivorship: How Joint Tenancy Works on Death

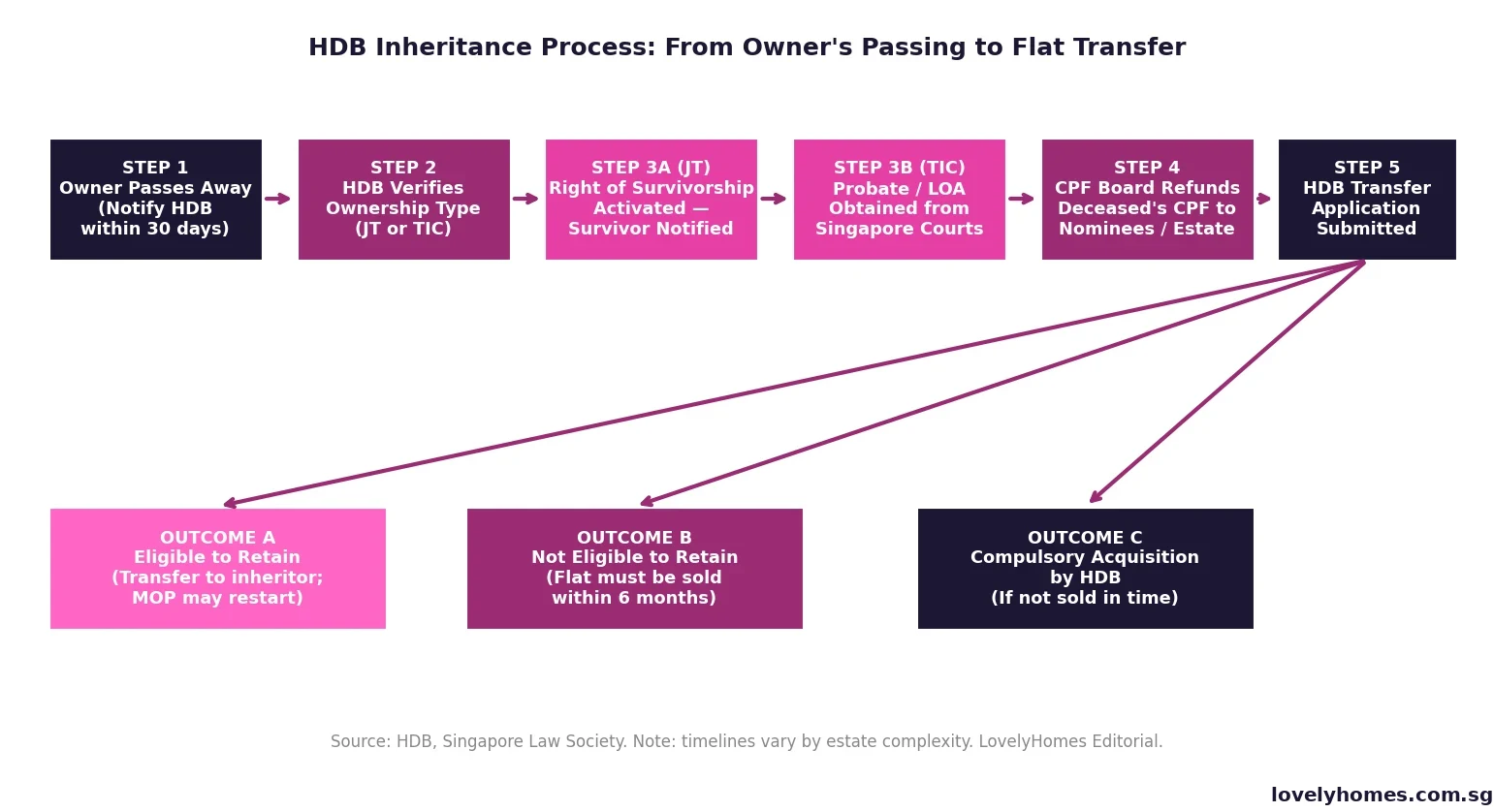

The right of survivorship is a powerful legal mechanism that simplifies the transfer of HDB flats in the common scenario where a married couple owns a flat and one spouse passes away. When the first spouse dies, the surviving spouse automatically becomes the sole owner of the flat — there is no need to go through the courts, apply for probate, or even instruct a solicitor for the transfer itself (though an application must be made to HDB to update the records).

The process involves notifying HDB within 30 days of the death, submitting the death certificate, the original title deeds or relevant HDB documentation, and completing HDB’s survivorship transfer form. HDB will then update its records to reflect the surviving owner as the sole registered proprietor. The entire administrative process typically takes 3–6 weeks once documents are submitted.

The surviving JT owner inherits the flat subject to any outstanding HDB or bank loan. If the deceased was the primary borrower and the surviving spouse does not meet the bank’s income criteria to assume the sole loan, they may need to make other arrangements — including partial repayment, sourcing a guarantor, or selling the flat. It is advisable for couples to ensure both spouses are listed as co-borrowers on any mortgage to avoid this complication.

Tenancy-in-Common and the Intestate Succession Act

For flat owners holding the property under Tenancy-in-Common, the death of one owner requires a formal estate administration process before the flat can be transferred to the inheritor. If the deceased left a valid Will, executors named in the Will apply for a Grant of Probate from the Singapore High Court. If there is no Will, the next-of-kin applies for Letters of Administration. Both processes take 3–6 months on average for uncontested estates, though complex cases can take longer.

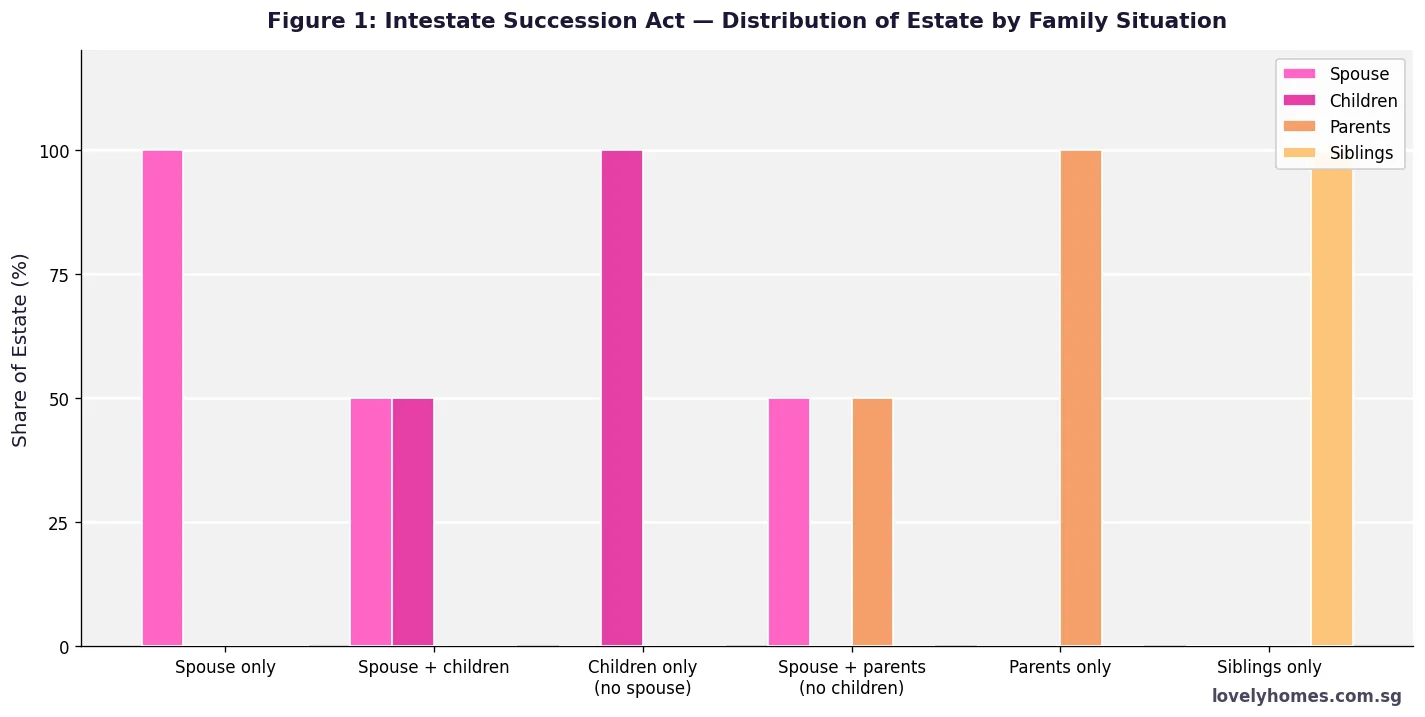

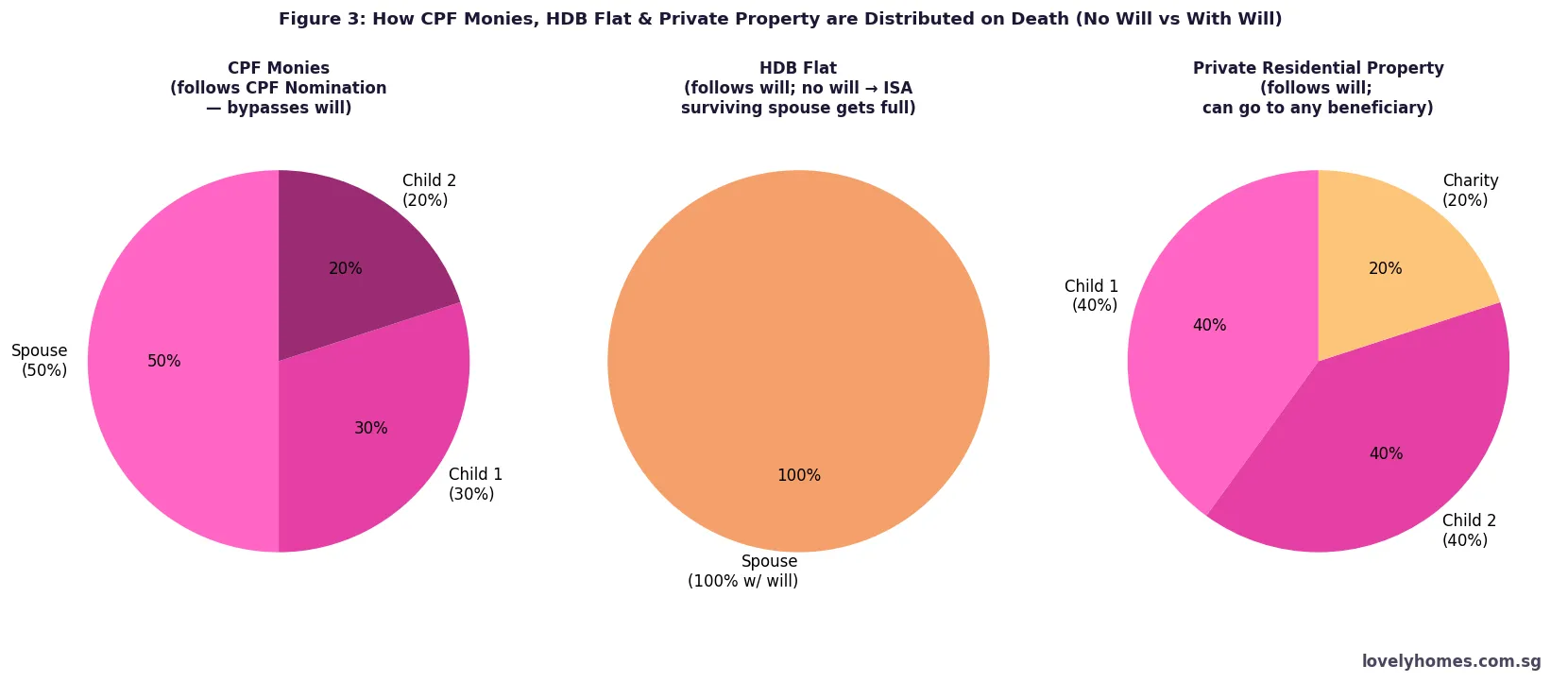

Where there is no Will, the ISA prescribes how the estate is distributed based on the family structure. For example, if the deceased leaves a spouse and children, the spouse receives 50% of the estate and the children share the remaining 50% equally. If only a spouse survives (no children, no living parents), the spouse receives the entire estate. The ISA does not apply to Muslim Singaporeans, whose estates are governed by Faraid rules under AMLA, administered through the Syariah Court for distribution certificates.

CPF and HDB on the Death of an Owner

CPF monies used to purchase an HDB flat do not form part of the flat’s transfer on death — they are handled separately by the CPF Board. When an owner dies, all CPF funds used to purchase the flat — including both the original principal withdrawn and the accrued interest at 2.5% p.a. compounded — must be refunded to the deceased’s CPF account. These funds are then distributed to CPF nominees (designated by the deceased via a CPF nomination form before death), or — if there is no nomination — to the Public Trustee for distribution under the Intestate Succession Act.

This CPF refund is separate from the flat’s ownership transfer. The inheritor who takes over the flat does not receive the deceased’s CPF monies as part of the flat — they receive only the flat itself, potentially subject to an outstanding mortgage. The CPF refund may significantly reduce the equity available in the flat if the loan is outstanding, as the CPF monies do not offset the mortgage on death.

If the flat has an outstanding HDB concessionary loan at the time of death, the surviving owner or inheritor must arrange with HDB to either assume the loan (if they qualify) or repay it. In some cases where the deceased had Home Protection Scheme (HPS) insurance (a mortgage-reducing insurance administered by CPF Board), the outstanding HDB loan may be discharged on death, passing the flat to the inheritor debt-free. All HDB flat owners with an outstanding HDB loan are required to maintain HPS cover, making this a meaningful protection for families.

Who Can Retain an Inherited HDB Flat?

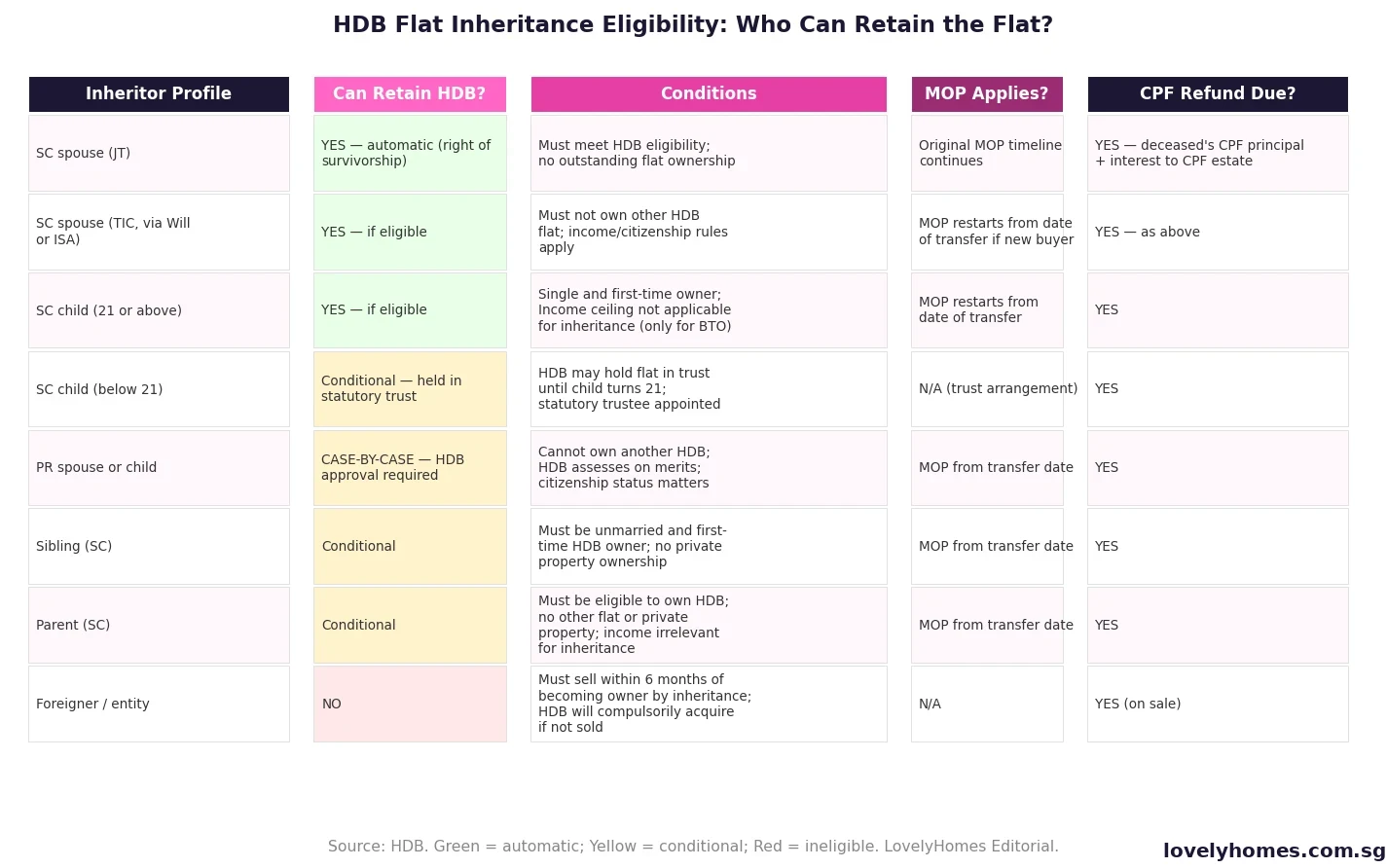

The right to retain an inherited HDB flat is subject to HDB’s standard eligibility criteria. The core principle is that HDB flats are public housing meant for Singapore citizens and permanent residents who meet the relevant conditions. Simply inheriting a flat does not guarantee the right to keep it if the inheritor does not meet HDB’s eligibility framework.

Singapore Citizen beneficiaries in a nuclear family context — such as a surviving SC spouse or adult SC children — generally have the widest eligibility to retain an HDB flat. However, they must not already own another HDB flat (subject to the non-concurrent ownership rule) and must not hold any private residential property at the time of inheritance (or must dispose of private property within 6 months). Singapore Permanent Resident inheritors are assessed on a case-by-case basis by HDB and face more restrictions. Foreigners (non-PRs) are not eligible to own HDB flats and must sell any inherited flat within 6 months; failure to do so can result in HDB compulsorily acquiring the flat.

Where a flat is inherited by a minor (below 21), HDB typically holds the flat in a statutory trust arrangement until the child reaches majority. A statutory trustee (often a parent or guardian) is appointed to manage the flat in the interim.

Applying to Transfer or Retain the HDB Flat

The formal process of applying to retain or transfer an HDB flat after a death involves several steps that typically span 3–9 months depending on the estate complexity, whether probate is required, and HDB’s processing time. The beneficiary or executor must submit an application to HDB with the death certificate, identity documents, Grant of Probate or Letters of Administration (if TIC), and supporting documents evidencing eligibility (e.g. income documents, CPF statement, private property declaration).

HDB will assess the application, verify eligibility, check for any outstanding charges or HDB loans on the flat, and — where the inheritor is taking over a loan — require the inheritor to meet the relevant debt servicing criteria. If approved, the transfer is completed via a legal instrument lodged with the Singapore Land Authority (SLA), and the Land Register is updated to reflect the new owner.

Selling an Inherited HDB Flat

Where the inheritor is ineligible to retain the HDB flat — either because they do not meet HDB’s eligibility criteria or because they choose to liquidate the asset — the flat must be sold on the open HDB resale market. The 6-month timeline begins from when ownership is formally transferred to the ineligible inheritor (not from the date of death), giving families some breathing room to arrange the estate and marketing process.

The sale proceeds are handled as follows: the outstanding HDB loan (if any) is repaid first from the sale price; CPF monies used by all owners over the flat’s ownership history are refunded (with accrued interest) to each respective owner’s CPF account or estate; legal and agent costs are deducted; and the net cash proceeds form part of the estate for distribution. If the flat was sold at the prevailing resale market price, the estate may receive a meaningful cash sum — particularly for flats in mature estates with substantial appreciation.

| Scenario | Ownership Type | Legal Process Required | Timeline (est.) | MOP Reset? |

|---|---|---|---|---|

| SC surviving spouse (JT) | Joint Tenancy | Notify HDB; submit death cert + survivorship docs | 3–6 weeks admin | No (continuity) |

| SC child inheriting via Will (TIC) | Tenancy-in-Common | Grant of Probate + HDB transfer application | 4–8 months | Yes (from transfer date) |

| SC child inheriting — intestate (TIC) | Tenancy-in-Common | Letters of Administration + HDB transfer application | 5–10 months | Yes |

| PR beneficiary (TIC or JT estate) | Either | Probate/LOA + HDB case-by-case assessment | 6–12 months | Yes |

| Ineligible beneficiary — must sell | Either | Transfer to ineligible owner + list for HDB resale | Must sell within 6 months of transfer | N/A (sold) |

| Minor inheritor (below 21) | Either | Statutory trust arrangement via HDB; trustee appointed | Until majority | Assessed at age 21 |

Worked Example: The Lim Family — SC Widow Inheriting Under Joint Tenancy

David and Susan Lim are Singapore Citizens who purchased a 4-room HDB flat in Ang Mo Kio in 2015 under Joint Tenancy at S$450,000, financed by an HDB concessionary loan. Their outstanding HDB loan as at June 2026 is S$210,000. David passes away unexpectedly in June 2026 at age 58.

Step 1 — Survivorship: As the flat was held in JT, Susan automatically becomes the sole owner of the flat by right of survivorship. No probate is required. Susan notifies HDB within 30 days and submits the death certificate and survivorship transfer form.

Step 2 — CPF refund: David had used S$180,000 in CPF OA (principal) towards the flat purchase and monthly instalments over 11 years. Accrued interest on these CPF withdrawals at 2.5% p.a. amounts to approximately S$61,000. The total CPF refund of S$241,000 is credited back to David’s CPF account. As David made a CPF nomination naming Susan and their two adult children, the S$241,000 in David’s CPF is distributed per the nomination — not as part of the flat’s transfer.

Step 3 — Mortgage: David maintained Home Protection Scheme (HPS) insurance on the HDB loan. On his death, the outstanding S$210,000 HDB loan is discharged by HPS, passing the flat to Susan debt-free.

Outcome: Susan now owns the flat in sole name, free of mortgage, with the flat’s estimated resale value at ~S$620,000 (based on comparable resale transactions in the area in 2026). The net equity in the flat for Susan is approximately S$620,000 (since the CPF refund went to David’s CPF estate, not reducing the flat’s market value). The HDB admin process took approximately 5 weeks from death notification to registration of Susan as sole owner.

Key lesson: The combination of JT ownership, HPS insurance, and CPF nomination meant that the inheritance process was administratively simple and economically optimal for Susan. Had David not maintained HPS, Susan would have needed to service the S$210,000 loan herself from retirement savings or a new bank loan — a significant burden at age 56.

What This Means for HDB Flat Owners

Estate planning for HDB flat owners in Singapore is not a complex exercise, but it does require deliberate action rather than relying on defaults. The most important steps any HDB owner can take are: first, confirm the current ownership structure of their flat (JT or TIC) and whether it reflects their actual wishes; second, maintain a valid and up-to-date CPF nomination so that CPF monies reach the intended beneficiaries; third, consider making a Will to address any TIC share and other non-CPF assets; and fourth, ensure adequate HPS cover is maintained on any outstanding HDB loan to protect the family from the mortgage burden on death.

Joint Tenancy works well for most married couples as a default — it is simple, automatic, and avoids probate delays. However, for blended families, second marriages, business partners owning flats together, or Muslim families seeking Faraid-compliant distributions, Tenancy-in-Common provides greater flexibility and should be considered with legal advice.

What Might Come Next

There are no announced changes to Singapore’s HDB inheritance framework as at June 2026. The Law Reform Commission has previously considered but not implemented recommendations on simplifying intestate succession for HDB flats, and the Ministry of Law continues to review options for making probate processes faster and less costly for estates with modest assets. The digitisation of the Probate Court and HDB’s integrated estate management platform (accessible via MyHDBPage) has already reduced administrative timelines in recent years. HDB owners and estate practitioners should monitor any future legislative changes to the Probate and Administration Act, the Intestate Succession Act, and HDB’s Housing Policy as Singapore’s population ages and inheritance scenarios become more common.

Frequently Asked Questions: HDB Inheritance & Transfer

Can I change my HDB flat from Joint Tenancy to Tenancy-in-Common?

Yes. A Joint Tenancy in an HDB flat can be severed to become a Tenancy-in-Common through a legal process called a severance of joint tenancy. This involves instructing a solicitor to prepare and lodge the relevant instrument at the Singapore Land Authority. Both owners must consent to the severance. The legal costs typically range from S$1,500 to S$2,500 depending on the complexity. Once severed, each owner’s defined share (usually 50%/50% unless otherwise specified) can be bequeathed to beneficiaries via a Will, bypassing the right of survivorship. HDB’s approval may be required in some cases.

What if the deceased HDB owner did not leave a CPF nomination?

If the deceased did not make a CPF nomination, the CPF Board will transfer the CPF savings (including the refunded flat-related CPF monies) to the Public Trustee’s Office. The Public Trustee distributes these funds according to the Intestate Succession Act — meaning they follow the same intestate distribution rules as other estate assets (e.g., 50% to spouse, 50% to children). This process adds time and cost to the estate administration. It is strongly advisable to make a CPF nomination and to update it whenever family circumstances change.

Does the Minimum Occupation Period (MOP) restart when I inherit an HDB flat?

Generally yes, when a flat is transferred to a new owner via inheritance (other than a Joint Tenancy survivorship transfer, where the surviving owner continues the original MOP timeline), the MOP is assessed from the date the new owner takes legal title of the flat. For example, if you inherit a flat in June 2026, your 5-year MOP (or 10-year MOP for Plus/Prime flats purchased under the new classification rules) begins from June 2026. You must continue to occupy the flat and cannot sublet the whole flat or purchase any other residential property during the MOP period. Always confirm the specific MOP conditions with HDB when applying for the transfer.

What is the Home Protection Scheme (HPS) and is it compulsory?

HPS is a mortgage-reducing insurance administered by CPF Board that covers the outstanding HDB home loan in the event of the insured owner’s death, terminal illness, or total permanent disability. It is compulsory for all HDB flat owners with outstanding HDB concessionary loans who have CPF OA savings. For HDB flat owners with bank loans, HPS cover is not mandatory but CPF Board strongly recommends it. HPS premiums are payable from CPF OA and are relatively affordable. On the insured event (e.g., death), HPS discharges the outstanding loan balance up to the insured amount, passing the flat to the family debt-free. Reviewing your HPS coverage amount (especially if you have refinanced to a bank loan) is an important part of property ownership in Singapore.

Can a Muslim Singaporean’s HDB flat be distributed via Faraid rules?

Under Singapore law, a Muslim person’s estate — including any HDB flat held under Tenancy-in-Common — is governed by Faraid (Islamic inheritance law) as applied by the Syariah Court under the Administration of Muslim Law Act (AMLA), rather than the civil Intestate Succession Act. The Syariah Court issues an Inheritance Certificate specifying the Faraid shares to each beneficiary. For HDB flats under Joint Tenancy, however, the civil right of survivorship technically applies — a tension between civil and religious law that some Muslim families resolve by electing Tenancy-in-Common and making a Will consistent with Faraid requirements. Muslim HDB owners are strongly advised to consult both a Syariah lawyer and HDB to ensure their ownership structure and estate plans align with their religious obligations.

How long does the HDB inheritance transfer process typically take?

The timeline varies significantly by case type. For Joint Tenancy survivorship transfers — the simplest scenario — the HDB administrative process typically takes 3 to 6 weeks once all required documents are submitted. For Tenancy-in-Common cases where probate is needed, the Grant of Probate or Letters of Administration alone typically takes 3–6 months, after which the HDB transfer application takes a further 4–8 weeks. Complex estates involving disputes, overseas beneficiaries, or unusual eligibility circumstances can take 12–24 months or more. Throughout this period, the flat can generally continue to be occupied by eligible family members, though it cannot be sold or rented out until the transfer is completed and any applicable MOP is met.

Click anywhere outside to close