by Lovelyhomes Editorial Team | Apr 24, 2026 | Investment Analysis, Market News, Price Trends, Property News, Property Trends

Singapore’s private residential property market began 2026 on a note of careful consolidation. The Urban Redevelopment Authority’s flash estimate for Q1 2026, released on 1 April, recorded a 0.3% quarter-on-quarter increase in the overall private residential price index — the softest quarterly growth in six quarters and a meaningful deceleration from the 0.6% gain seen in Q4 2025. Yet beneath this headline restraint lie important divergences across segments and regions that tell a more nuanced story.

Key Market Signals — Q1 2026

- Overall private residential prices: +0.3% q-o-q (slowest growth in 6 quarters)

- Non-landed segment: +1.0% q-o-q — strong rebound from Q4 2025’s slight dip

- OCR leads: +1.3% q-o-q — suburban condos remain the demand driver

- CCR recovery: +0.4% q-o-q — reverses the -3.5% slide of Q4 2025

- Transactions: ~4,041 units — down 39.7% q-o-q from a high Q4 2025 base

- New launch take-up: Several Q1 launches sold over 90% on launch weekend

Singapore Private Residential Market — Q1 2026

Flash estimate figures released 1 April 2026 by the Urban Redevelopment Authority

| Overall Price Change (q-o-q) |

+0.3% — slowest growth in 6 quarters |

| Non-Landed Prices (q-o-q) |

+1.0% — rebound from -0.2% in Q4 2025 |

| Landed Prices (q-o-q) |

-1.8% — reversal from +3.4% in Q4 2025 |

| Core Central Region (CCR) |

+0.4% — reversal from -3.5% decline in Q4 2025 |

| Rest of Central Region (RCR) |

+0.9% — after +0.7% in Q4 2025 |

| Outside Central Region (OCR) |

+1.3% — strongest regional performer |

| Total Transactions (Q1 2026) |

~4,041 units — down 39.7% q-o-q from 6,699 in Q4 2025 |

| New Launch Take-up Highlight |

Several Q1 launches achieved >90% take-up at launch weekend |

| 2026 Launch Pipeline |

~17 projects / ~8,100 units — approx. 30% fewer than 2025 |

Key Takeaway

Private residential prices in Singapore remain in positive territory in Q1 2026, with non-landed homes leading a modest recovery. Transaction volumes fell sharply from a high Q4 2025 base but demand at quality new launches remained resilient.

Source: URA flash estimate — ura.gov.sg — 1 April 2026

lovelyhomes.com.sg

lovelyhomes.com.sg

Non-Landed Segment Rebounds; Landed Dips

The Q1 2026 data reveals a clear bifurcation between the non-landed and landed segments. Non-landed private homes (condominiums and apartments) posted a 1.0% quarter-on-quarter price gain — a healthy rebound from the marginal 0.2% decline recorded in Q4 2025. Landed homes, in contrast, retreated 1.8% after a strong 3.4% surge in the preceding quarter. The landed pullback is consistent with the typical volatility in that segment, which trades on thin volumes and is sensitive to single large transactions.

For most buyers and investors focused on the condominium market, the non-landed rebound is the more relevant signal. The data suggests that underlying demand for well-located private apartments remains positive, supported by a constrained 2026 launch pipeline and steady household formation among Singapore’s resident population.

OCR Leads; CCR Stages a Recovery

The Outside Central Region (OCR) — Singapore’s suburban heartland comprising districts such as Tampines, Jurong, Tengah, Sengkang, Upper Thomson, and Woodlands — delivered the strongest price performance of any region in Q1 2026 at +1.3% quarter-on-quarter. This reflects sustained demand from HDB upgraders, first-time private buyers, and families attracted to the OCR’s larger unit sizes and more accessible price quantum. Several OCR launches in late 2025 and early 2026 recorded impressive sales velocity; with the 2026 pipeline lean in this segment, competition for quality suburban new launches is likely to remain brisk.

The Rest of Central Region (RCR), covering districts like Bishan, Toa Payoh, Queenstown, River Valley, and parts of Novena, posted a 0.9% gain — a tick up from the 0.7% seen in Q4 2025, suggesting mid-market city-fringe product continues to attract steady demand from owner-occupiers and investors seeking a balance of accessibility and price growth.

The Core Central Region (CCR) — comprising the prime districts of Sentosa, Orchard, Holland, Tanglin, Marina Bay, and the financial district — staged a notable recovery with a +0.4% quarter-on-quarter gain, directly reversing the -3.5% decline of Q4 2025. The Q4 2025 weakness was largely attributed to a normalisation after a period of elevated prime-market activity and the impact of the 60% foreign buyer ABSD, which has materially suppressed international demand since April 2023. The Q1 2026 recovery suggests domestic CCR demand — led by Singapore Citizens, PRs, and Free Trade Agreement-eligible nationals including US citizens and Swiss nationals — is stabilising the top end of the market.

Transaction Volume Down on a High Base

Total private home transactions fell to approximately 4,041 units in Q1 2026, a 39.7% decline from the 6,699 units transacted in Q4 2025. The sharp percentage drop sounds alarming but should be read with important context: Q4 2025 was an unusually active quarter, boosted by a high concentration of new project launches in the second half of 2025 (including multiple large OCR and RCR projects that sold strongly). The Q1 2026 volume is closer to a normalised quarterly run-rate rather than an indication of distress.

Of the six developments launched in Q1 2026, several achieved take-up rates exceeding 90% on their respective launch weekends — a clear signal that buyer demand remains calibrated to the right product at the right price point. The cautionary note, however, is that with only approximately 17 projects and 8,100 units anticipated in the 2026 full-year pipeline (a 30% reduction on 2025’s approximately 11,000+ units), the aggregate transaction volume for 2026 is expected to be structurally lower than in prior years — not because demand has collapsed, but because supply is meaningfully constrained.

What This Means for Buyers in 2026

For prospective buyers, the Q1 2026 data paints a picture of a market in consolidation rather than in correction. Prices are neither accelerating dangerously nor sliding materially. The government has signalled no intention to introduce additional cooling measures in the near term, with the existing 60% foreign buyer ABSD and 55% TDSR cap continuing to provide structural support for affordability among genuine owner-occupiers.

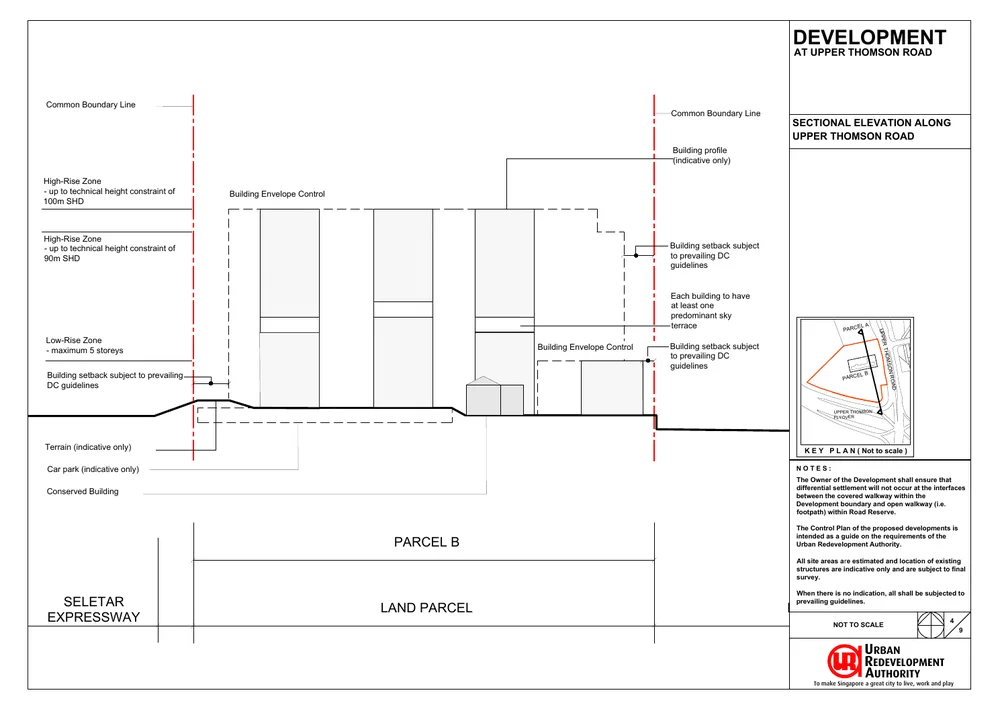

For buyers considering the OCR, the combination of +1.3% price growth and a thin 2026 pipeline suggests that well-located suburban launches — particularly those with MRT proximity — are likely to see sustained demand. Projects such as Springleaf Residence (Upper Thomson, TEL, 941 units) and Pinery Residences (Tampines) illustrate the kind of connected suburban product that has been absorbing the bulk of OCR demand in early 2026. For CCR buyers, the segment’s Q1 recovery after a period of weakness opens a potential re-entry window for domestic buyers who have been waiting on the sidelines.

The full Q1 2026 URA report (incorporating complete sales data beyond the preliminary caveat cut-off) is expected in late April 2026. Buyers and investors should monitor the final figures alongside the HDB Resale Price Index, which is released in the same cycle, for a complete picture of how the private-public residential market relationship is evolving.

Related Guides

Disclaimer: Market data in this article is drawn from the URA flash estimate released 1 April 2026. Final figures will be published in the full URA quarterly release (typically 3–4 weeks after flash estimate). This article is for informational purposes only and does not constitute investment or financial advice.

by Lovelyhomes Editorial Team | Apr 24, 2026 | Market News, Property News, Property Trends

If you have been waiting for the right moment to enter Singapore’s private residential market, the numbers in 2026 are telling a story worth paying attention to. This year is shaping up to be the quietest year for new private condo launches in at least three years — with an estimated 17 projects and approximately 8,100 units entering the market, compared with roughly 23 projects and over 11,000 units in 2025. A 30% reduction in new supply is not a footnote; it is the defining market dynamic that every prospective buyer and investor needs to factor into their planning.

2026 New Launch Pipeline at a Glance

- Approximately 17 private residential projects (18 including ECs) expected in 2026

- Total unit supply: ~8,100 units — roughly 30% below 2025’s ~11,000+

- OCR suburban projects dominate the pipeline — more than half of all units

- Several early 2026 launches already recording 90%+ take-up at launch weekend

- Key launches still to come: Springleaf Residence, UPPERHOUSE, W Residences Marina View, and others in D1, D9, D10, D26

- EC pipeline: ~5 projects expected, catering to the HDB upgrader segment

Singapore New Launch Condo Pipeline 2026

Estimated supply vs prior years — as at April 2026

| 2026 New Launch Estimate |

~17 private residential projects / ~8,100 units |

| 2025 Launches (actual) |

~23 projects / ~11,000+ units |

| Year-on-Year Change |

Approximately -30% in unit supply |

| 2024 Launches (actual) |

~8,000–9,000 units (comparable to 2026) |

| OCR Share (2026 pipeline) |

Majority — over 50% of units in suburban locations |

| CCR Share (2026 pipeline) |

Smaller share — constrained by 60% foreign ABSD, GLS scarcity |

| Key OCR Projects (2026) |

Springleaf Residence, Pinery Residences, Rivelle Tampines EC |

| Key CCR/RCR Projects (2026) |

UPPERHOUSE Orchard Blvd, W Residences Marina View, 21 Anderson |

| Strong Take-Up Threshold |

Several 2026 launches recording >90% on launch weekend |

Key Takeaway

With roughly 30% fewer new units launching in 2026 versus 2025, well-located projects are experiencing strong buyer interest. Buyers who wait too long risk limited availability at quality launches.

Source: Industry data, URA pipeline reports — April 2026

lovelyhomes.com.sg

Why is 2026 Supply so Constrained?

The 2026 supply tightness is largely a function of the Government Land Sales (GLS) programme cycle and the typical 3–5 year development period between site award and launch. Many of the sites sold during the 2019–2020 period have already launched (contributing to the busy 2023–2025 pipeline), while the sites awarded in 2022–2023 are still under construction and will not be market-ready until 2027 or beyond in many cases. The result is a natural valley in the launch calendar during 2026.

Compounding the GLS timing effect, Singapore’s construction costs and labour constraints have added 6–12 months to typical development timelines for several projects originally slated for 2025 launches that have slipped into 2026 or later. Meanwhile, the government has been measured in its GLS supply releases — calibrating site offerings against market conditions to avoid both over-supply and price spikes — meaning the pipeline for the near-term is already largely set.

OCR Dominates, CCR Gets Premium Boutique Projects

The geographic distribution of the 2026 pipeline skews heavily toward the OCR. More than half of the anticipated new units are in suburban locations, reflecting the GLS programme’s allocation of residential sites in growth areas such as Tengah, Tampines North, Jurong Lake District, Canberra, and Upper Thomson. This is broadly consistent with the government’s stated objective of providing well-served housing near employment hubs and public transport nodes.

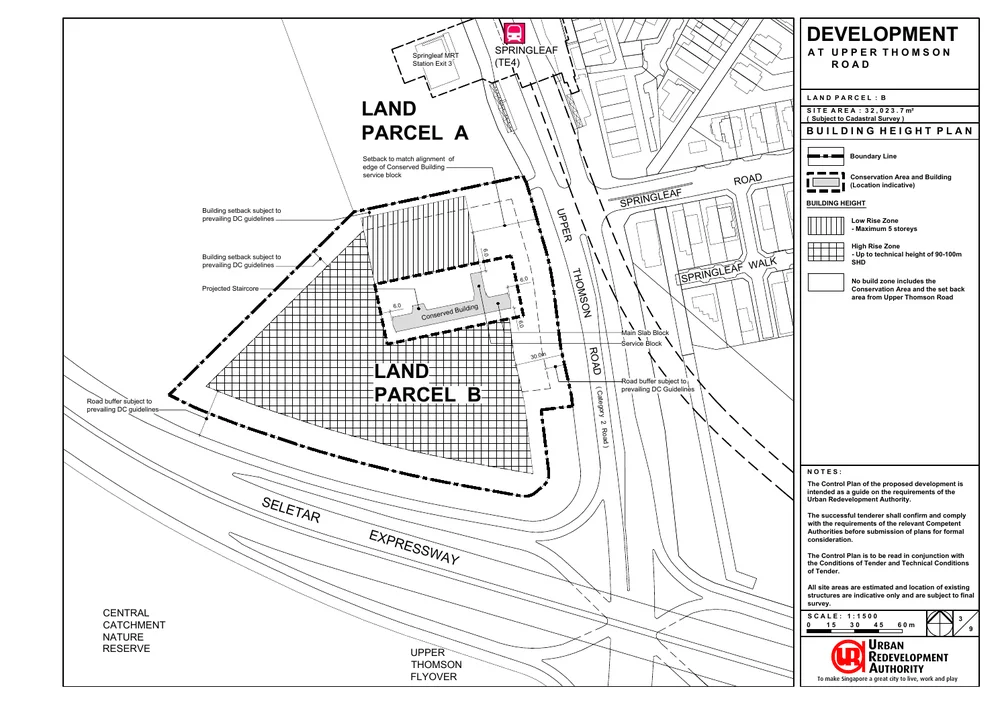

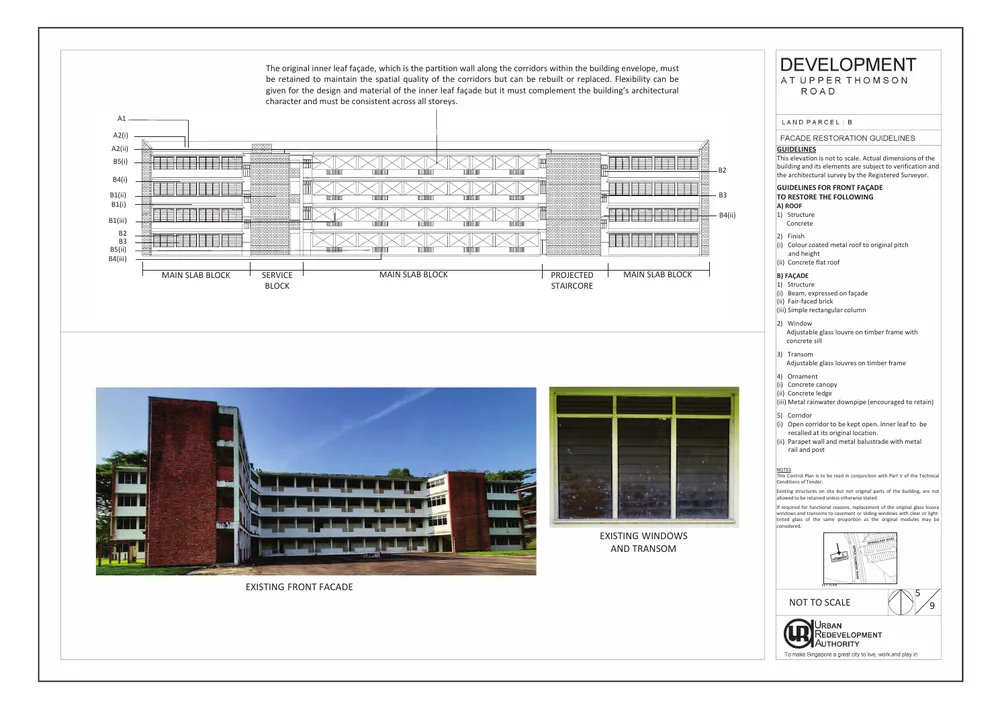

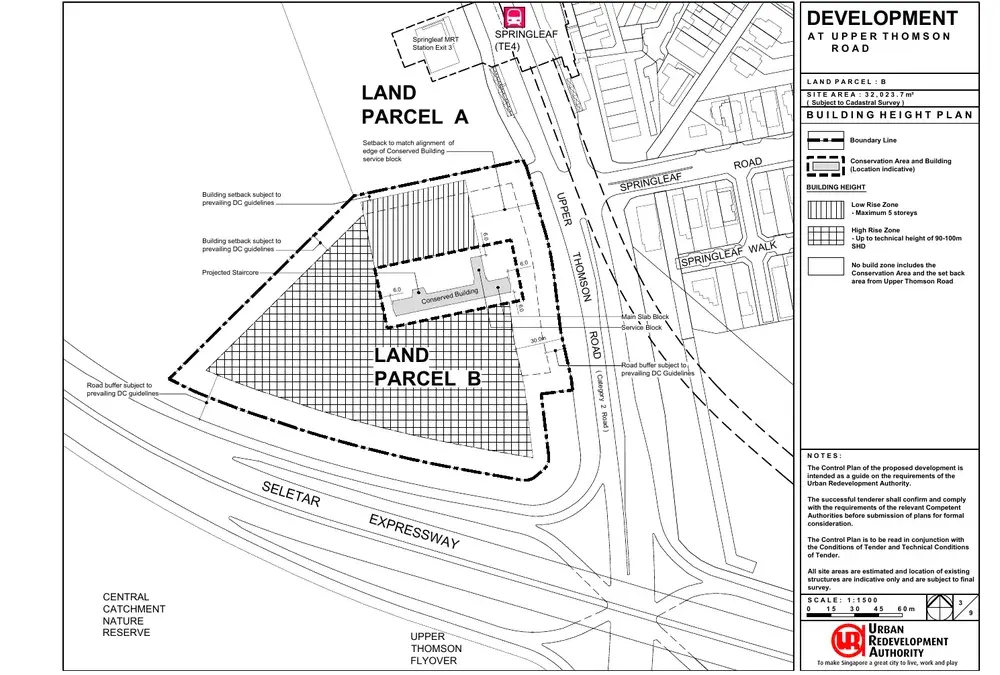

In the OCR, the standout offering this year is Springleaf Residence — GuocoLand’s 941-unit nature-integrated development at Upper Thomson Road, just 110 metres from Springleaf MRT on the Thomson-East Coast Line. The project’s biodiversity-conservation design concept and a conserved heritage building make it architecturally unlike anything else in the suburban pipeline. At this stage, the Upper Thomson corridor is also set to benefit from the broader Springleaf new town development planned by URA, which will add community amenities, green corridors, and township infrastructure around the site over the coming decade.

In the CCR and RCR, the 2026 picture is one of boutique quality over quantity. UPPERHOUSE at Orchard Boulevard — the 301-unit UOL Group and Singapore Land Group collaboration at 22 Orchard Boulevard — is among the most keenly anticipated CCR launches of the year, offering a genuinely rare Orchard Boulevard address with low unit density and Swiss-Italian material specifications. W Residences Marina View, a 683-unit branded residence by IOI Properties atop a 360-room W Hotels property in Marina Bay District 1, represents an entirely new product category for Singapore: a luxury branded residence tower that brings five-star hotel services into an owner-occupied residential framework. At 237 metres, it is also set to be among the tallest residential towers in the republic.

Strong Demand Meets Leaner Supply: What Happens to Prices?

Early 2026 market data suggests that the combination of constrained new supply and sustained demand from domestic buyers is creating a productive tension in the new launch segment. The Q1 2026 URA flash estimate recorded a 0.3% quarter-on-quarter price increase overall, with the OCR leading at +1.3% q-o-q. This is a market in measured growth, not a speculative spike — the structural constraints of the ABSD framework and the TDSR limit mean Singapore’s residential market cannot achieve the kind of runaway appreciation seen in some other global cities.

For buyers, the implication of a lean 2026 pipeline is straightforward: there are fewer opportunities to choose from, and the best-positioned units (MRT-proximate stacks, larger configurations, view-facing orientations) are likely to be absorbed quickly at launch. The pattern seen at Pinery Residences — a 588-unit Tampines West project that sold 92.5% of units at an average of S$2,546 per square foot at its launch weekend in early 2026 — indicates buyers are prepared to commit decisively when the product offering is right.

The Executive Condo Opportunity in 2026

For eligible HDB upgraders, the 2026 EC pipeline presents a compelling alternative to private condos. Five EC projects are expected in 2026, including Rivelle Tampines EC and projects near Sembawang and the Plantation Close area. ECs are sold at prices typically 20–30% below comparable private condos in the same location, and first-timer HDB upgraders who purchase directly from the developer are not required to pay ABSD even if they still own their HDB flat. The income ceiling for EC applications is S$16,000 in combined gross monthly household income.

As EC projects privatise after 10 years from their TOP, they typically achieve capital appreciation comparable to private condos in the same district. For value-conscious upgraders who can qualify, the 2026 EC pipeline deserves serious attention — particularly given the tighter supply of private OCR launches this year.

Looking Ahead: What to Expect from H2 2026

The majority of the 2026 new launches are expected in the second half of the year. Buyers who have done their research, secured their In-Principle Approval, and identified their preferred district and project type are best placed to act quickly when launches are announced. With limited inventory in both OCR and CCR segments, waiting for conditions to “improve” is a strategy that carries its own risks in a supply-constrained year.

The government’s consistent message has been that there are no plans for additional cooling measures unless private home prices show an unsustainable spike exceeding 10% year-on-year. With Q1 2026 growth at 0.3% for the quarter, the current trajectory does not suggest intervention is imminent. The next data checkpoint will be the full Q1 2026 URA report expected later in April, followed by the Q2 2026 flash estimate in July.

Related Guides

Disclaimer: Pipeline estimates in this article are based on publicly available project information, GLS award records, and industry data as at April 2026. Actual launch dates and unit counts are subject to change at developer’s discretion. This article is for informational purposes only and does not constitute investment advice. Source: URA — ura.gov.sg.

by Lovelyhomes Editorial Team | Apr 24, 2026 | Condo New Launches, New Launches

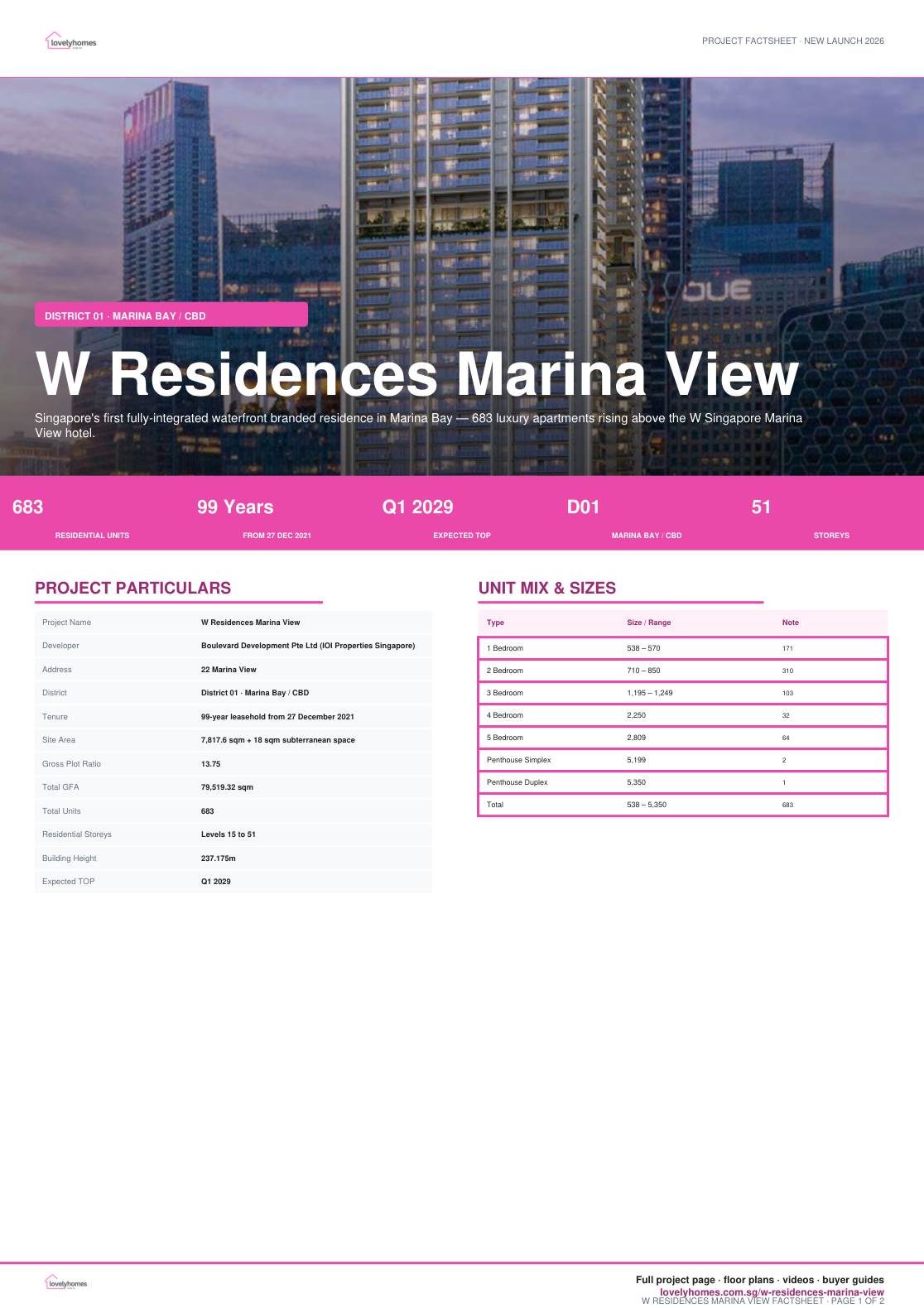

Marina View · District 01

W Residences Marina View

Singapore’s first fully-integrated waterfront branded residence in Marina Bay — 683 luxury apartments rising above the W Singapore Marina View hotel.

99 Years

From 27 Dec 2021

Why W Residences Marina View

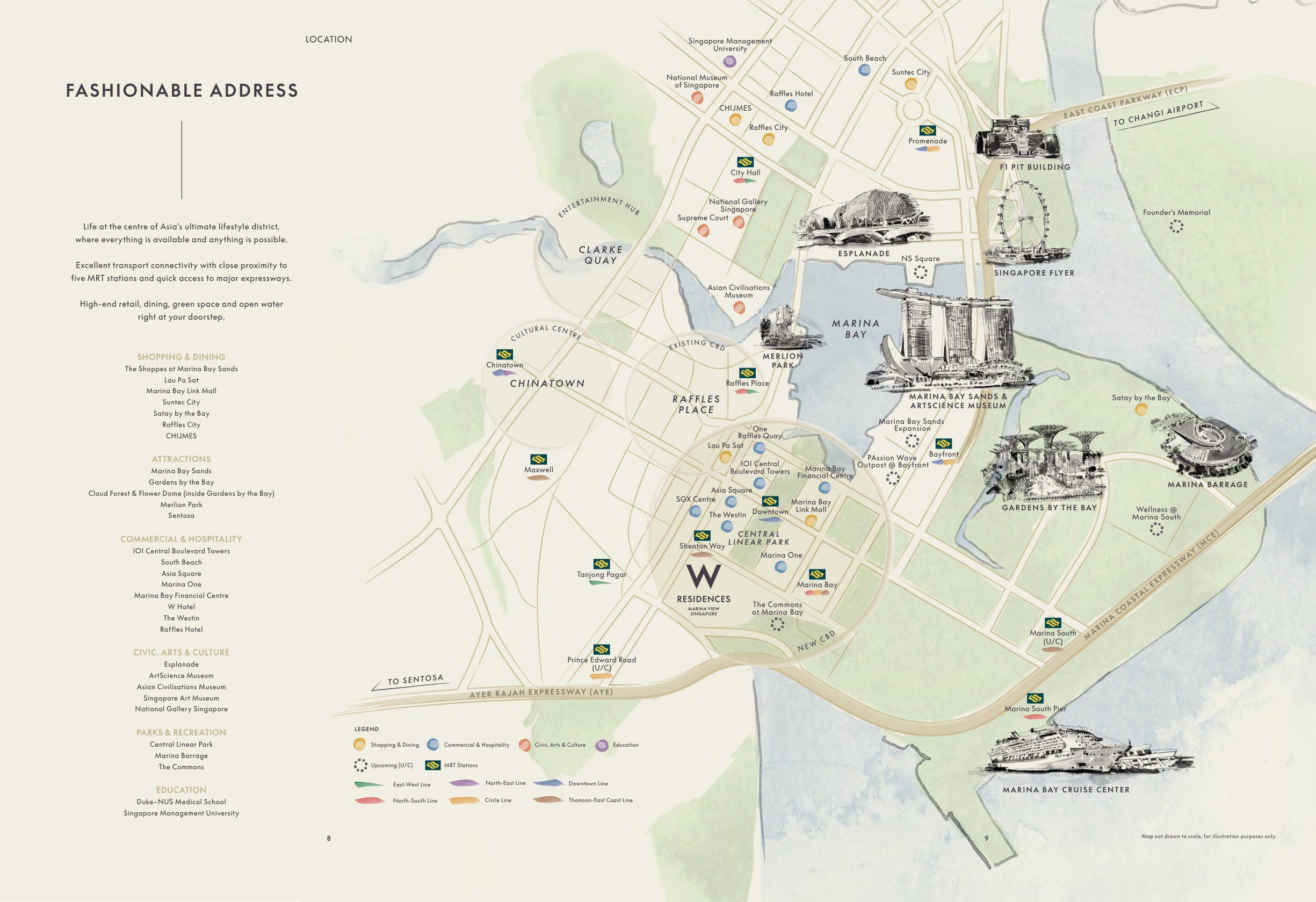

W Residences Marina View is a 99-year leasehold branded residence at 22 Marina View, developed by Boulevard Development Pte Ltd under IOI Properties Singapore. Project documents describe it as the first integrated development in Singapore with 683 residences sitting above a 360-room W Singapore hotel.

The key appeal is the combination of a Marina Bay address, managed branded-residence services, a large 683-unit amenity base, and the long-term transformation of Marina Bay / Greater Southern Waterfront.

01 · Address

Marina Bay new downtown

Located at the junction of Union Street and Marina View, within walking reach of Shenton Way, Downtown, Marina Bay, Raffles Place and Tanjong Pagar MRT stations.

02 · Branded Living

W hotel-managed lifestyle

Developer buyer notes position the residence around W’s hotel-style services, concierge support and branded hospitality environment.

03 · Scale

683 luxury units

Unit sizes span 1-bedroom suites through 5-bedroom apartments and three penthouses, supporting multiple sky and club facilities.

Project At-a-Glance

| Project Name |

W Residences Marina View |

| Developer |

Boulevard Development Pte Ltd (IOI Properties Singapore) |

| Address |

22 Marina View |

| District |

District 01 · Marina Bay / CBD |

| Tenure |

99-year leasehold from 27 December 2021 |

| Site Area |

7,817.6 sqm + 18 sqm subterranean space |

| Gross Plot Ratio |

13.75 |

| Total GFA |

79,519.32 sqm |

| Total Units |

683 |

| Residential Storeys |

Levels 15 to 51 |

| Building Height |

237.175m |

| Expected TOP |

Q1 2029 |

| Carpark |

342 lots + 4 accessible lots; EV provision |

| Bicycle Lots |

171 residential bicycle lots |

| Architect |

Architects61 Pte Ltd |

| Landscape Architect |

Coen Design International Pte Ltd |

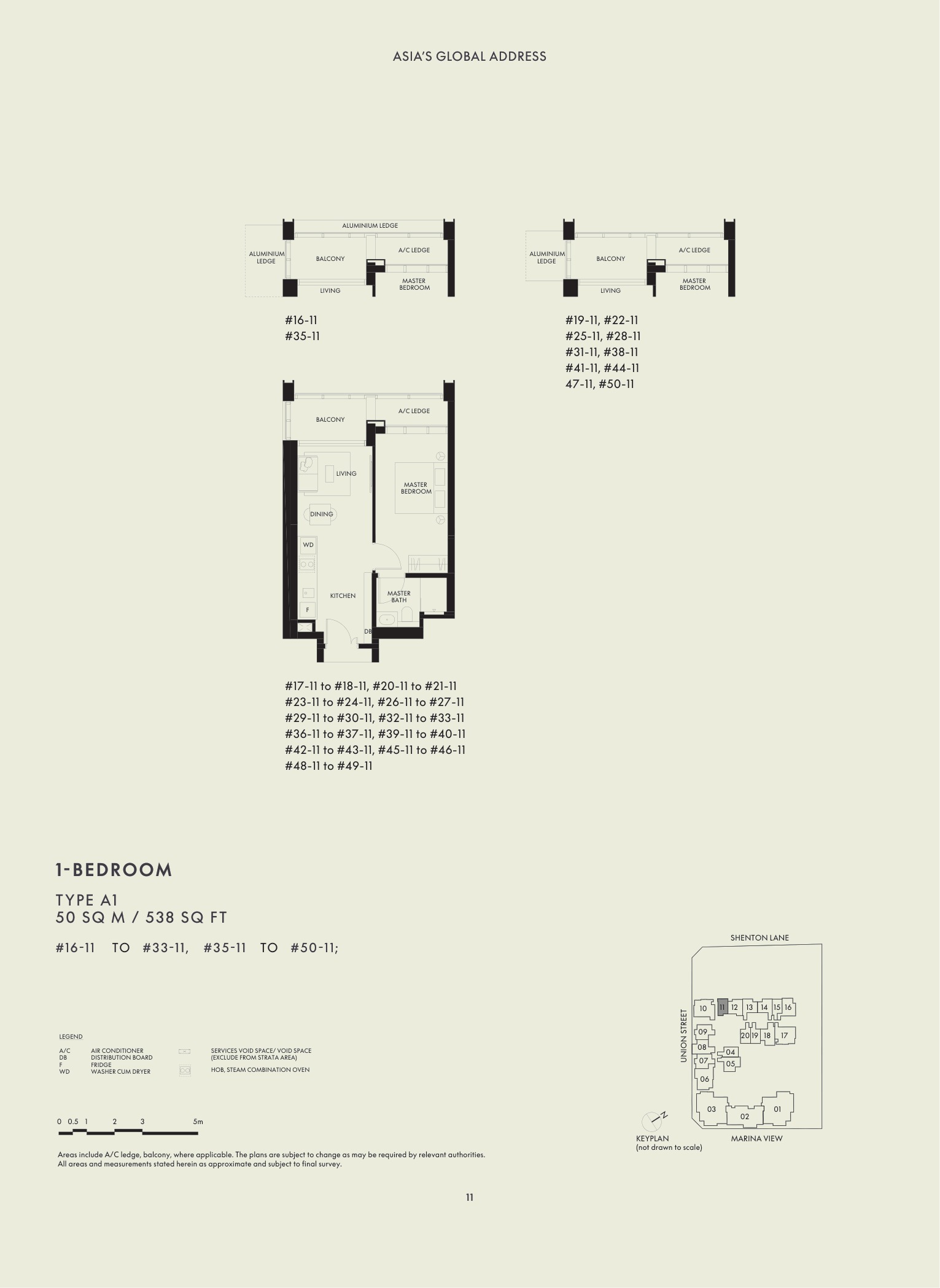

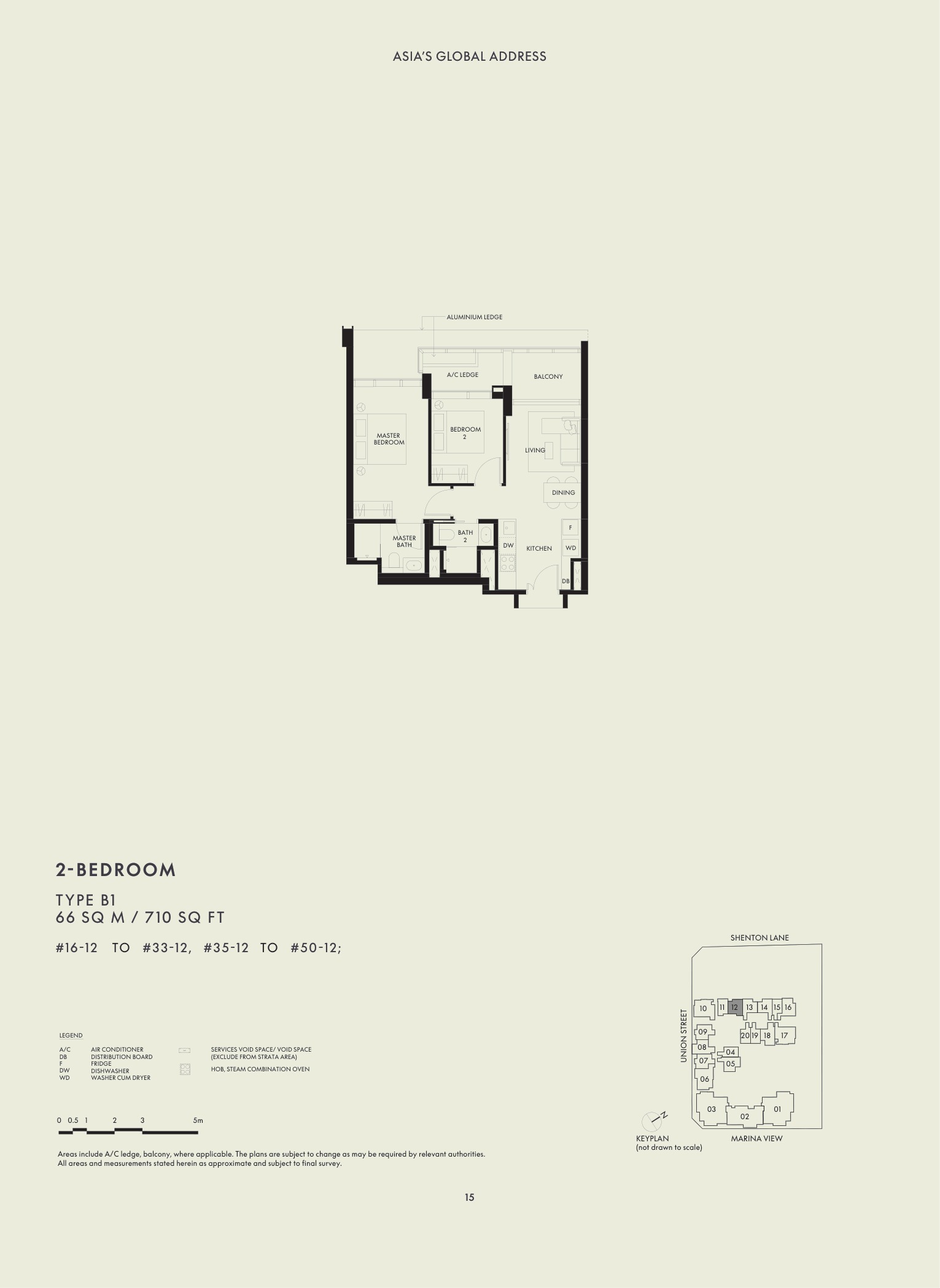

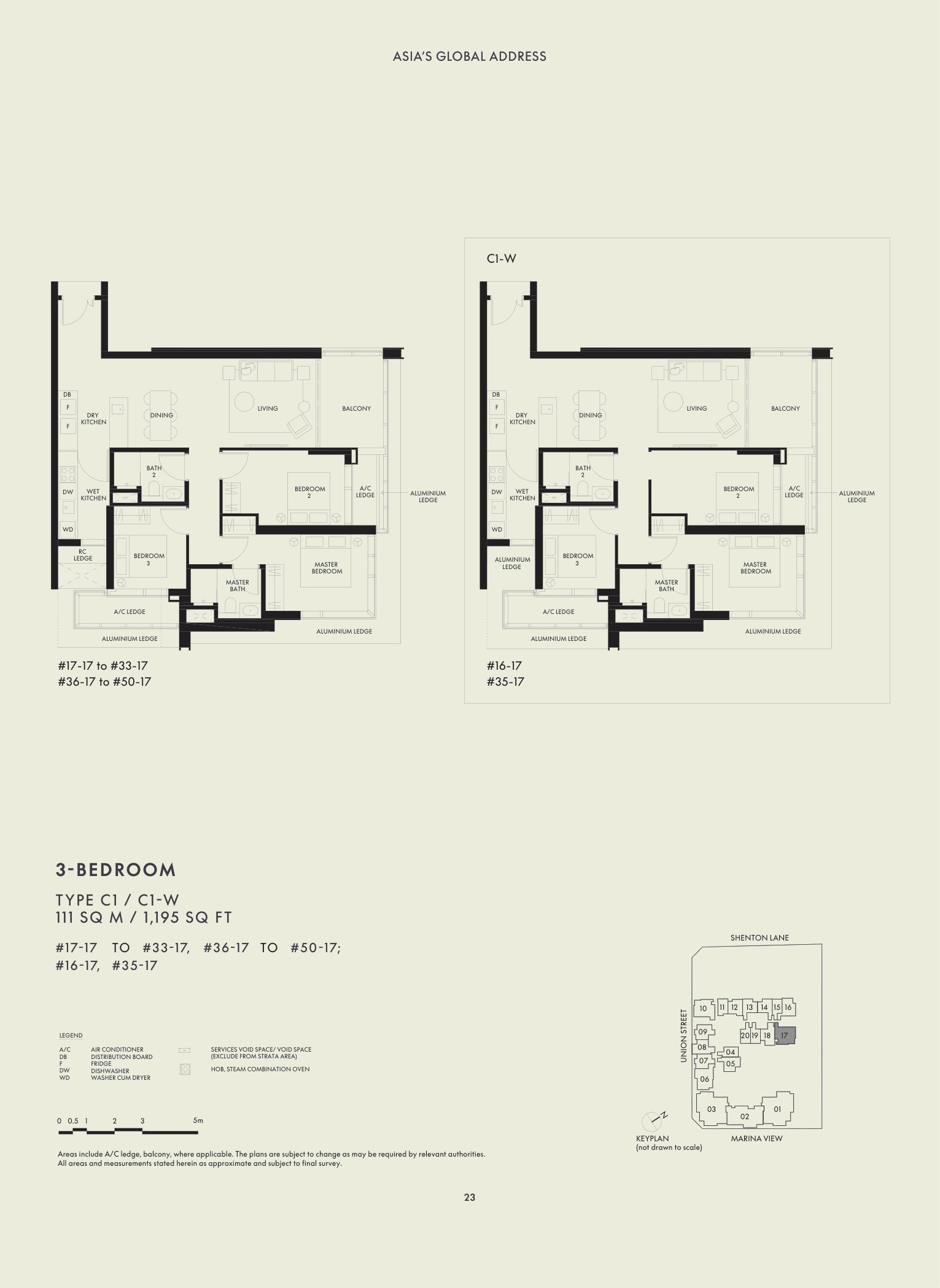

Unit Mix and Sizes

| Bedroom Type |

Size (sqft) |

Units |

% of Total |

| 1 Bedroom |

538 – 570 |

171 |

25.0% |

| 2 Bedroom |

710 – 850 |

310 |

45.4% |

| 3 Bedroom |

1,195 – 1,249 |

103 |

15.1% |

| 4 Bedroom |

2,250 |

32 |

4.7% |

| 5 Bedroom |

2,809 |

64 |

9.4% |

| Penthouse Simplex |

5,199 |

2 |

0.3% |

| Penthouse Duplex |

5,350 |

1 |

0.1% |

| Total |

538 – 5,350 |

683 |

100% |

Unit mix and sizes are taken from the abridged project factsheet dated 7 October 2024. Areas are approximate and subject to final survey.

Indicative Pricing

1BR

From S$1.778M

538-570 sqft

2BR

From S$2.383M

710 sqft

5BR

From S$11.360M

2,809 sqft

Current public balance-unit snapshot shows 1BR from S$1.778M, 2BR from S$2.383M, 3BR from S$3.860M, 4BR from S$8.740M and 5BR from S$11.360M. Source: W Residences Marina View NewLaunches price list updated 27 Jan 2026, accessed 29 Apr 2026.

Why Buyers Are Watching

-

1

First waterfront branded residence in Marina Bay — source USP notes frame the project as an early mover in Marina Bay’s new downtown.

-

2

Integrated W hotel living — residences sit above W Singapore Marina View, with hotel-style managed services and branded-residence positioning.

-

3

Five MRT stations nearby — buyer notes reference Shenton Way, Downtown, Marina Bay, Raffles Place and Tanjong Pagar MRT within walking reach.

-

4

Large branded-residence scale — 683 apartments enable a broad facilities programme across Levels 15, 34 and 51.

-

5

Views and future transformation — USP material references marina waterfront, city, Greater Southern Waterfront and Sentosa views, plus Marina Bay masterplan upside.

-

6

Green Mark Platinum — project document positions the project as a BCA Green Mark Platinum certified development.

Location and Connectivity

MRT

Five station options

Shenton Way TEL is cited as a 2-minute walk; Downtown, Marina Bay, Raffles Place and Tanjong Pagar MRT are also referenced nearby.

Roads

CBD expressway access

Source connectivity notes reference quick access to MCE, AYE and KPE.

Lifestyle

Marina Bay landmarks

Gardens by the Bay, Marina Bay Sands, Esplanade, Singapore Flyer, Clarke Quay and CBD lifestyle nodes sit in the broader precinct.

Growth

New Downtown / GSW

URA Marina Bay and Greater Southern Waterfront planning remains the long-term precinct story.

Schools Nearby

| School Planning |

Confirm current school distance bands and eligibility with OneMap and MOE before relying on any school-distance claim. |

Lifestyle and Amenities

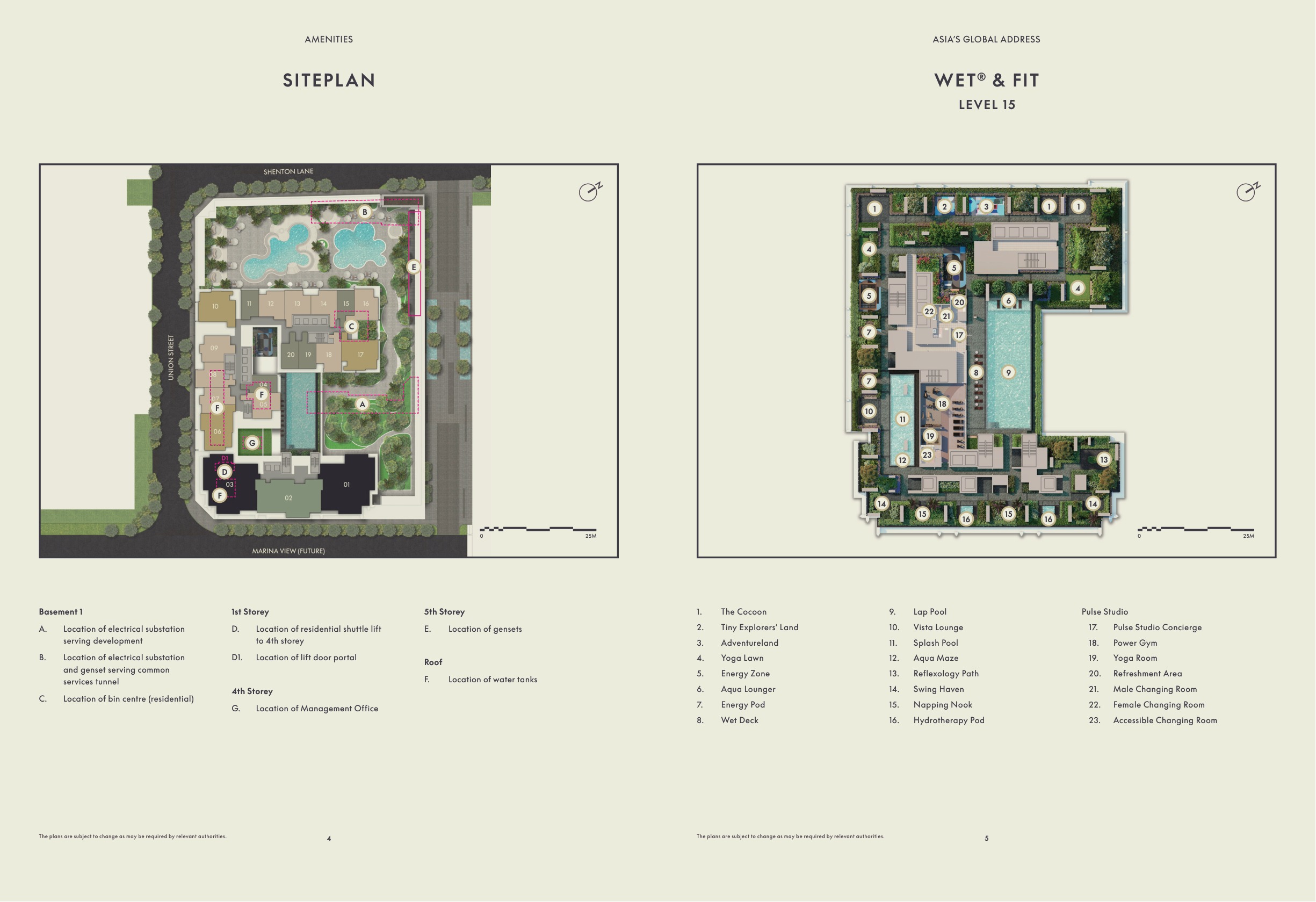

Level 15 · WET & FIT

Infinity Tranquillity Pool, sun deck, wet deck, kids’ pool, hydrotherapy pool, Power Gym, yoga room and outdoor fitness.

Level 34 · Living Room

Gourmet Pavilions, Sommelier Lounge, home cinema room, Oasis Lounge, private dining lounge and golf simulator.

Level 51 · AWAY

Sky Pool, chill deck, The Hangout, Club 51, onsen, steam room, sauna, meditation room, treatment room and Zen Garden.

Site Plan

Actual Level 15 facilities/site plan from W Residences Marina View floor-plan project document · indicative and subject to developer confirmation

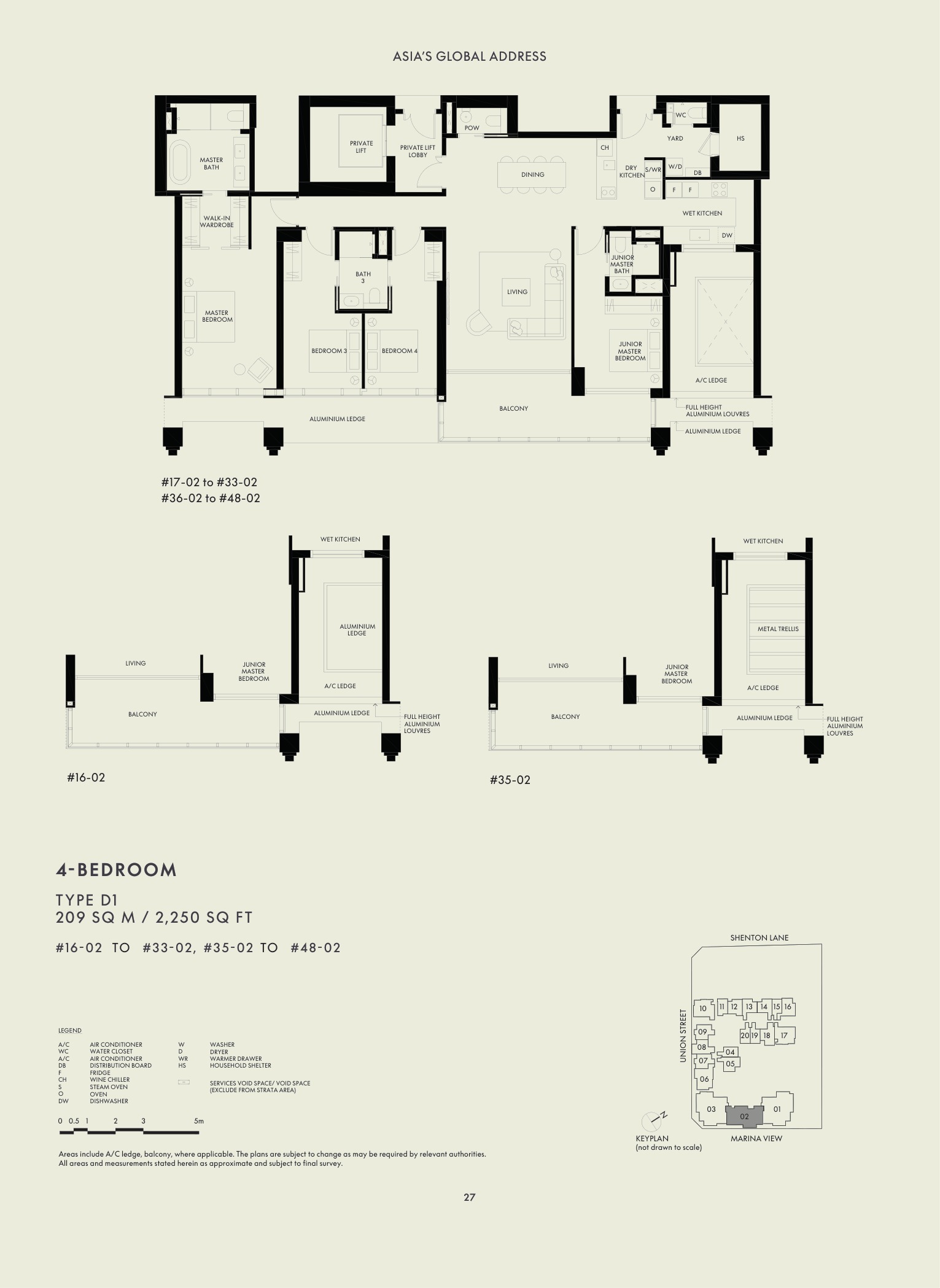

Floor Plans (Selected)

Representative actual plans by unit type. Download the clean full floor-plan PDF below for the complete selected plan pack.

1 Bedroom Type A150 sqm / 538 sqft

2 Bedroom Type B166 sqm / 710 sqft

3 Bedroom Type C1111 sqm / 1,195 sqft

4 Bedroom Type D1209 sqm / 2,250 sqft

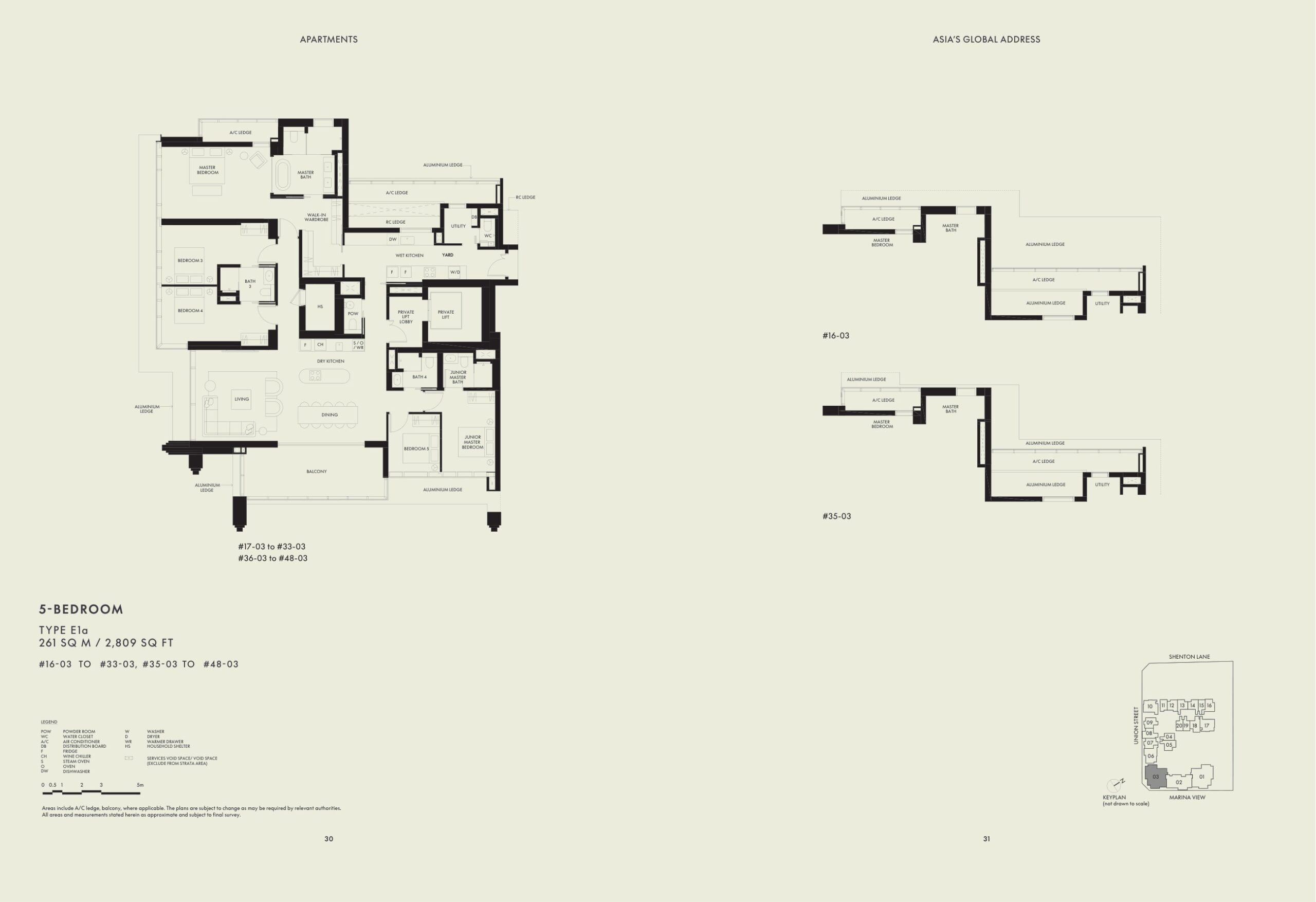

5 Bedroom Type E1a261 sqm / 2,809 sqft

Penthouse Type PH1483 sqm / 5,199 sqft

Full Floor Plans PDF

Clean plan pack extracted from the source floor-plan PDF, excluding agency appendix pages.

Download PDF

Elevation and Stack Chart

Refer to the site plan, selected layouts and full floor-plan PDF for stack orientation, floor levels and facing checks.

Facilities (30+)

Infinity Tranquillity PoolSky PoolGourmet PavilionsSommelier LoungeHome Cinema RoomPower GymGolf SimulatorPrivate Dining LoungeOnsenSteam RoomSaunaZen GardenHydrotherapy PoolAdventure PlaygroundYoga LawnSky View Deck

Developer and Consultant Team

Boulevard Development Pte Ltd · IOI Properties Singapore

IOI Properties Singapore is listed as the developer group in the project documents, with Boulevard Development Pte Ltd as the project developer.

| Project Architect |

Architects61 Pte Ltd |

| Landscape Architect |

Coen Design International Pte Ltd |

| Main Contractor |

Woh Hup Pte Ltd |

| M&E Engineer |

J Roger Preston (S) Pte Ltd |

| C&S Engineer |

KTP Consultants Pte Ltd |

| Interior Design |

Hachem Singapore Pte Ltd |

Sustainability and Specifications

- Green Mark Platinum: project document positions the project as a BCA Green Mark Platinum certified development.

- Smart home provisions: source e-book references smart fire alarm devices, leak detectors, smart elevator and smart booking/delivery systems.

- Premium finishes: project document references European marble, European granite, European timber and Dornbracht sanitary fittings.

- EV provision: factsheet lists active and passive EV-charging lots within the residential carpark allocation.

Project Timeline

27 Dec 2021

Lease commencement

2024

Abridged factsheet source

Legal

2031 developer documents

Project Factsheet

A shareable 2-page PDF snapshot of everything on this page — bring it to viewings, forward it to family.

Download the Full Sales Pack

PDF · 2 pages

LovelyHomes Factsheet

Two-page project factsheet in the project format.

Download PDF

PDF · floor plans

Full Floor Plans

Clean selected floor-plan pack with 1BR through penthouse plans.

Download Floor Plans

Image · location

Location Map

Marina Bay map and connectivity context from project document.

Open Map

Frequently Asked Questions

Where is W Residences Marina View located?

The project address is 22 Marina View, near the junction of Union Street and Marina View in District 01.

Who is the developer?

The source factsheet lists Boulevard Development Pte Ltd as developer, under IOI Properties Singapore.

What is the tenure?

99-year leasehold commencing from 27 December 2021.

How many units are there?

683 residential units, with types from 1-bedroom to 5-bedroom and three penthouses.

When is the expected TOP?

The abridged source factsheet states Q1 2029, subject to developer and authority confirmation.

What is the current from-price?

Current public balance-unit snapshot shows 1BR from S$1.778M, 2BR from S$2.383M, 3BR from S$3.860M, 4BR from S$8.740M and 5BR from S$11.360M. Source: W Residences Marina View NewLaunches price list updated 27 Jan 2026, accessed 29 Apr 2026.

Ready to see W Residences Marina View in person?

Request the latest availability, price guide, floor plans and stamp-duty estimate before shortlisting.

WhatsApp Enquiry

Related Buying Guides

Stamp Duty

Complete ABSD rates, remissions, and worked examples.

Finance

BSD rates and calculation methodology.

Buying Guide

Progressive payment, ABSD timing, and resale comparison.

DISCLAIMER: All information is compiled from developer-issued project documents and public references for informational purposes only. Prices, unit mix, specifications and timelines are indicative and subject to change without notice. This page does not constitute an offer to buy or sell. Seek advice from a licensed property agent and legal counsel. LovelyHomes.com.sg is an independent editorial platform. Agency Licence: L3010858B.

by Lovelyhomes Editorial Team | Apr 24, 2026 | Condo Reviews, Property Reviews & Analysis

NEW LAUNCH · DISTRICT 26 · SINGAPORE

Springleaf Residence

Wing Tai × Hong Leong · 473 Units · 99-Year Leasehold · District 26

~S$TBC psf

Avg Launch PSF

Why Springleaf Residence

Springleaf Residence is a 473-unit 99-year leasehold residential development in District 26, Singapore, developed by Wing Tai × Hong Leong with an estimated TOP of 2028.

01 · Location

District 26 Address

Well-connected neighbourhood with access to public transport, schools, and lifestyle amenities.

02 · Scale

473 Residences

99-Year Leasehold development with quality fittings, smart-home provisions, and full condominium facilities.

03 · Value

New-Launch Advantage

Progressive payment schedule, 12-month Defects Liability Period, and modern specifications throughout.

Project At-a-Glance

| Project Name |

Springleaf Residence |

| Developer |

Wing Tai × Hong Leong |

| District |

D26 |

| Tenure |

99-Year Leasehold |

| Total Units |

473 |

| Est. TOP (VP) |

2028 |

| Est. Legal Completion |

2031 |

Unit Mix and Sizes

| Bedroom Type |

Size (sqft) |

Units |

% of Total |

| Download the project factsheet for the full unit mix breakdown and confirmed sizes. |

Refer to the developer’s official sales kit for confirmed unit types, sizes, and availability. Download factsheet (PDF).

Indicative Pricing

Prices are indicative and subject to change. Before ABSD, BSD, and legal fees. See our ABSD guide for stamp duty rates.

Why Buyers Are Watching

-

1

District 26 location — well-connected address with MRT access, expressways, and lifestyle amenities in an established residential corridor.

-

2

99-Year Leasehold — 99-year leasehold enabling full CPF usage and bank financing from day one.

-

3

473 residential units — comprehensive development with full condominium facilities and an active resident community.

-

4

Developer pedigree — Wing Tai × Hong Leong brings a track record of quality residential development across Singapore’s private property market.

-

5

Progressive payment advantage — staggered cash outlay during construction typically saves S$30,000–S$60,000 in loan interest compared to a full resale drawdown.

-

6

12-month Defects Liability Period — legally binding developer obligation to rectify defects at no cost within 12 months of TOP.

Location and Connectivity

Transport

MRT Access

Conveniently located near MRT stations connecting to the wider Singapore rail network.

Expressways

Road Connectivity

Access to major expressways for quick connections to the CBD, Changi Airport, and key destinations.

Lifestyle

Shopping & Dining

Nearby malls, hawker centres, supermarkets, and F&B within the immediate neighbourhood.

Schools

Education Belt

Primary and secondary schools within 1–2 km, with tertiary institutions in the broader district.

Schools Nearby

| Primary Schools |

Schools within 1–2 km — refer to MOE SchoolFinder for 2026 Phase 2B catchment zones at this address. |

| Secondary Schools |

Secondary schools serving the District 26 catchment — verify distances via OneMap. |

| International Schools |

Multiple international schools within the broader district and surrounding areas. |

Lifestyle and Amenities

Recreation & Wellness

Swimming pool, gymnasium, function rooms, and landscaped communal spaces for an active lifestyle.

Dining & Retail

Nearby malls, hawker centres, and F&B outlets serving everyday needs and weekend leisure.

Green Spaces

Parks and park connectors supporting an active outdoor lifestyle in Singapore’s City in Nature vision.

Site Plan

Development overview · indicative only · refer to official site plan in the factsheet download

Floor Plans (Selected)

Download the full floor plans PDF for all bedroom types, stack-by-stack layouts, and balcony dimensions.

Full Floor Plans PDF

All bedroom types, stack charts, and unit specifications available for download.

Download PDF

Elevation and Stack Chart

Elevation overview · indicative only · refer to developer’s official stack chart for confirmed positions

Facilities

Swimming PoolGymnasiumFunction RoomsBBQ PavilionsChildren’s PoolJacuzziClub LoungeGarden PavilionSky TerraceYoga LawnSmart Home SystemEV Charging24-Hour SecurityBicycle BaysPneumatic Waste System

Developer and Consultant Team

Wing Tai × Hong Leong

Developer of Springleaf Residence with residential development expertise in Singapore’s private property market. Consultant team details are available in the project factsheet.

| Developer |

Wing Tai × Hong Leong |

| District |

D26 |

| Estimated TOP |

2028 |

Sustainability and Specifications

- BCA Green Mark: Designed to meet BCA Green Mark standards with energy-efficient envelope and water-efficient fittings.

- Smart Home: Smart home management provisions across all units for access control and utilities.

- EV Infrastructure: Electric vehicle charging provisions in basement carpark.

- Quality Finishes: Premium materials and fittings in line with developer specifications throughout.

Project Timeline

2023–2024

Land Award & Licence

2025–2028

Construction Phase

Project Factsheet

A shareable 2-page PDF snapshot — bring it to viewings, share with family.

Download the Full Sales Pack

PDF · 2 pages

Springleaf Residence Factsheet

2-page LovelyHomes project factsheet — share with family, bring to viewings.

Download Factsheet

PDF · floor plans

Full Floor Plans

All bedroom type floor plans with dimensions and stack positions.

Download Floor Plans

PDF · location map

Location Map

High-resolution location map showing MRT, schools, and key amenities.

Download Map

Frequently Asked Questions

Where is Springleaf Residence located?

Springleaf Residence is located in District 26, Singapore. For the full address, refer to the project factsheet above.

Who is the developer of Springleaf Residence?

Springleaf Residence is developed by Wing Tai × Hong Leong.

What is the tenure?

Springleaf Residence is a 99-Year Leasehold development.

How many units does Springleaf Residence have?

Springleaf Residence comprises 473 residential units.

When is the expected TOP?

The estimated date of Vacant Possession (TOP) for Springleaf Residence is 2028. Subject to BCA approval.

Is Springleaf Residence subject to ABSD?

Yes. Springleaf Residence is a private residential development. ABSD applies at prevailing rates. See our

complete ABSD guide.

Can I use CPF to buy Springleaf Residence?

Yes, subject to CPF Withdrawal Limit rules. See our

CPF for Property guide.

Ready to see Springleaf Residence in person?

Register your interest for a complimentary project briefing and showflat tour.

WhatsApp Enquiry

Related Buying Guides

Stamp Duty

Complete ABSD rates, remissions, and worked examples.

Finance

BSD rates and calculation methodology.

Property Law

Bala’s Table, lease decay, and value impact.

Buying Guide

Progressive payment, ABSD timing, and rental income.

CPF

OA withdrawal, accrued interest, and limits.

Finance

How much can you actually borrow in Singapore?

DISCLAIMER: All information is compiled from publicly available sources and developer-issued materials for informational purposes only. Prices, unit mix, specifications, and timelines are indicative and subject to change without notice. This page does not constitute an offer to buy or sell. Seek advice from a licensed property agent and legal counsel. LovelyHomes.com.sg is an independent editorial platform. Agency Licence: L3010858B.

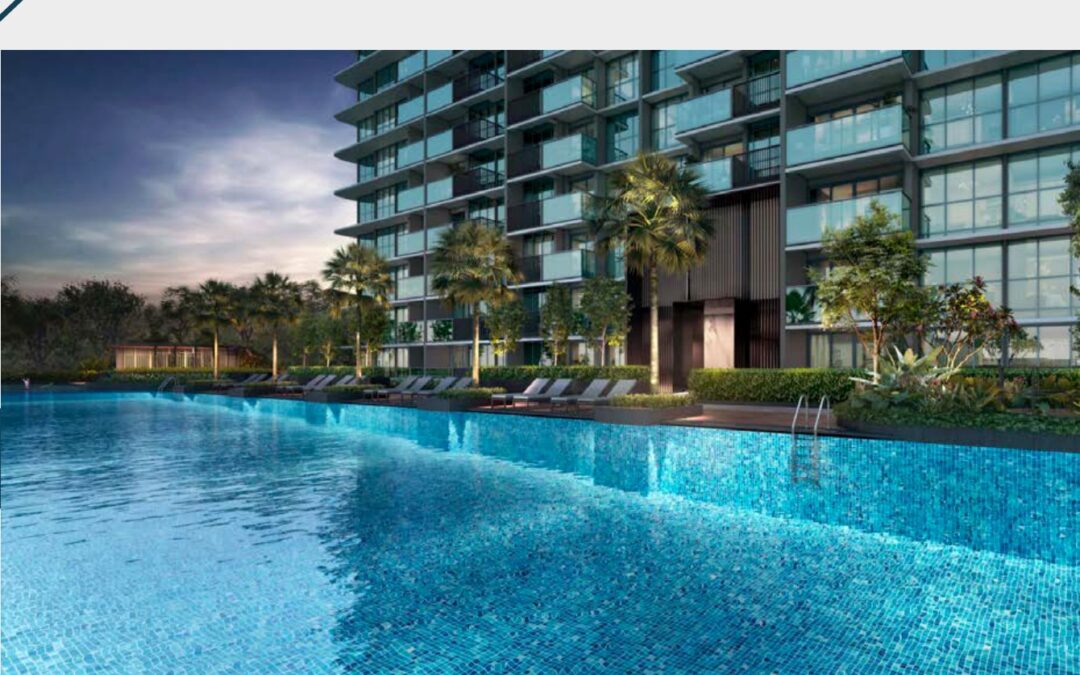

by Lovelyhomes Editorial Team | Apr 23, 2026 | Condo New Launches, New Launches

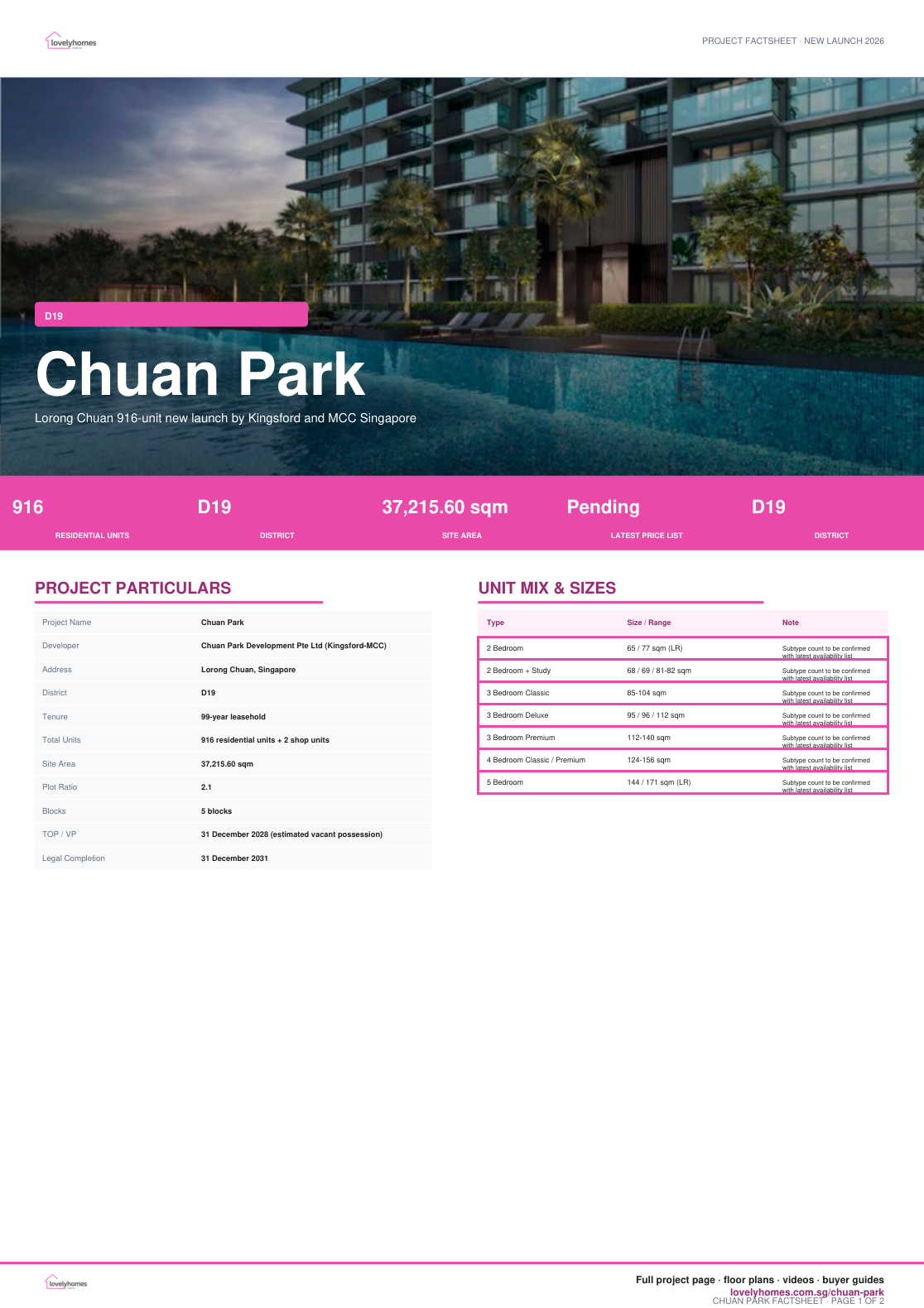

NEW LAUNCH · LORONG CHUAN · DISTRICT 19

Chuan Park

Lorong Chuan 916-unit new launch by Kingsford and MCC Singapore

From S$1.961M

Current From Price

Why Chuan Park

Chuan Park Chuan Park brings a 916-unit residential redevelopment back to the Lorong Chuan corridor, combining scale, rail access and family-sized layouts in an established District 19 neighbourhood.

01 · Address

D19 Location

Lorong Chuan, Singapore

02 · Scale

916 residential units + 2 shop units

5 blocks

03 · Tenure

99-year leasehold

Confirm the latest availability before shortlisting.

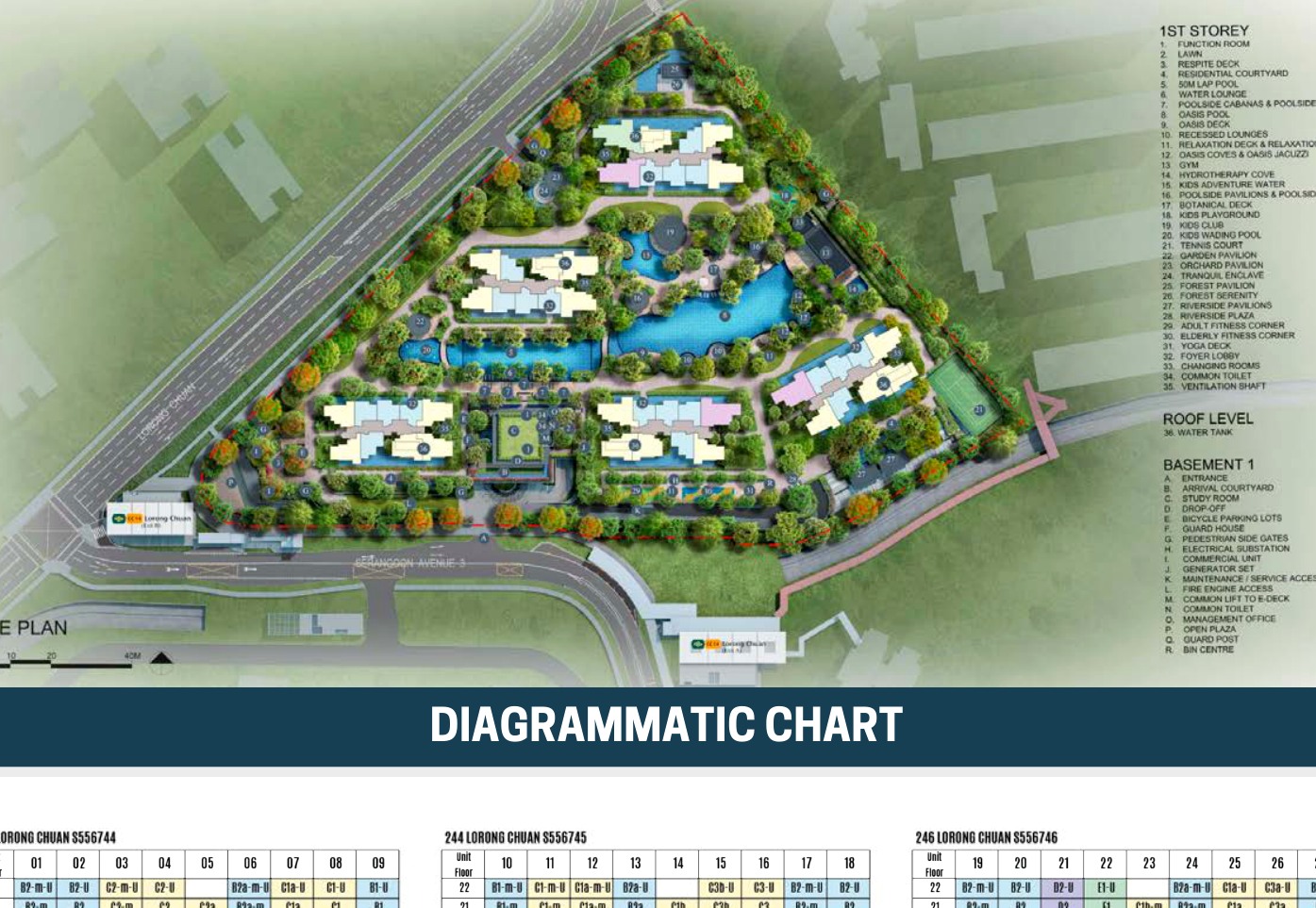

Project At-a-Glance

| Project Name |

Chuan Park |

| Developer |

Chuan Park Development Pte Ltd (Kingsford-MCC) |

| Address |

Lorong Chuan, Singapore |

| District |

D19 |

| Tenure |

99-year leasehold |

| Total Units |

916 residential units + 2 shop units |

| Site Area |

37,215.60 sqm |

| Plot Ratio |

2.1 |

| Blocks |

5 blocks |

| TOP / VP |

31 December 2028 (estimated vacant possession) |

| Legal Completion |

31 December 2031 |

Viewing Preparation

Use the factsheet, selected floor plans and site plan below to compare layouts, arrival points and facility zones before a viewing.

Confirm current pricing, stack availability and final specifications before booking.

Unit Mix and Sizes

| Bedroom Type |

Size / Range |

Availability Note |

| 2 Bedroom |

65 / 77 sqm (LR) |

Subtype count varies by latest balance-unit list |

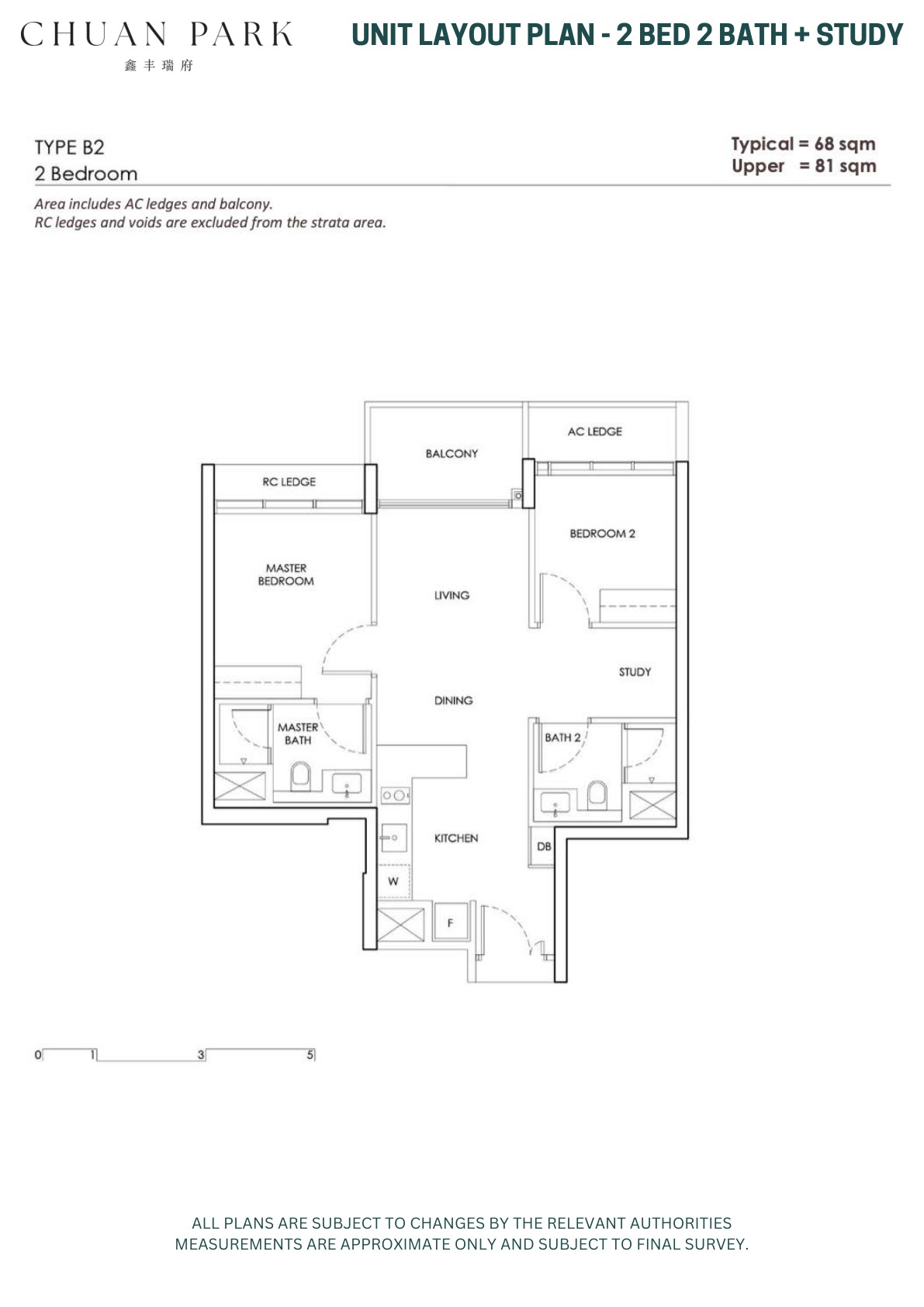

| 2 Bedroom + Study |

68 / 69 / 81-82 sqm |

Subtype count varies by latest balance-unit list |

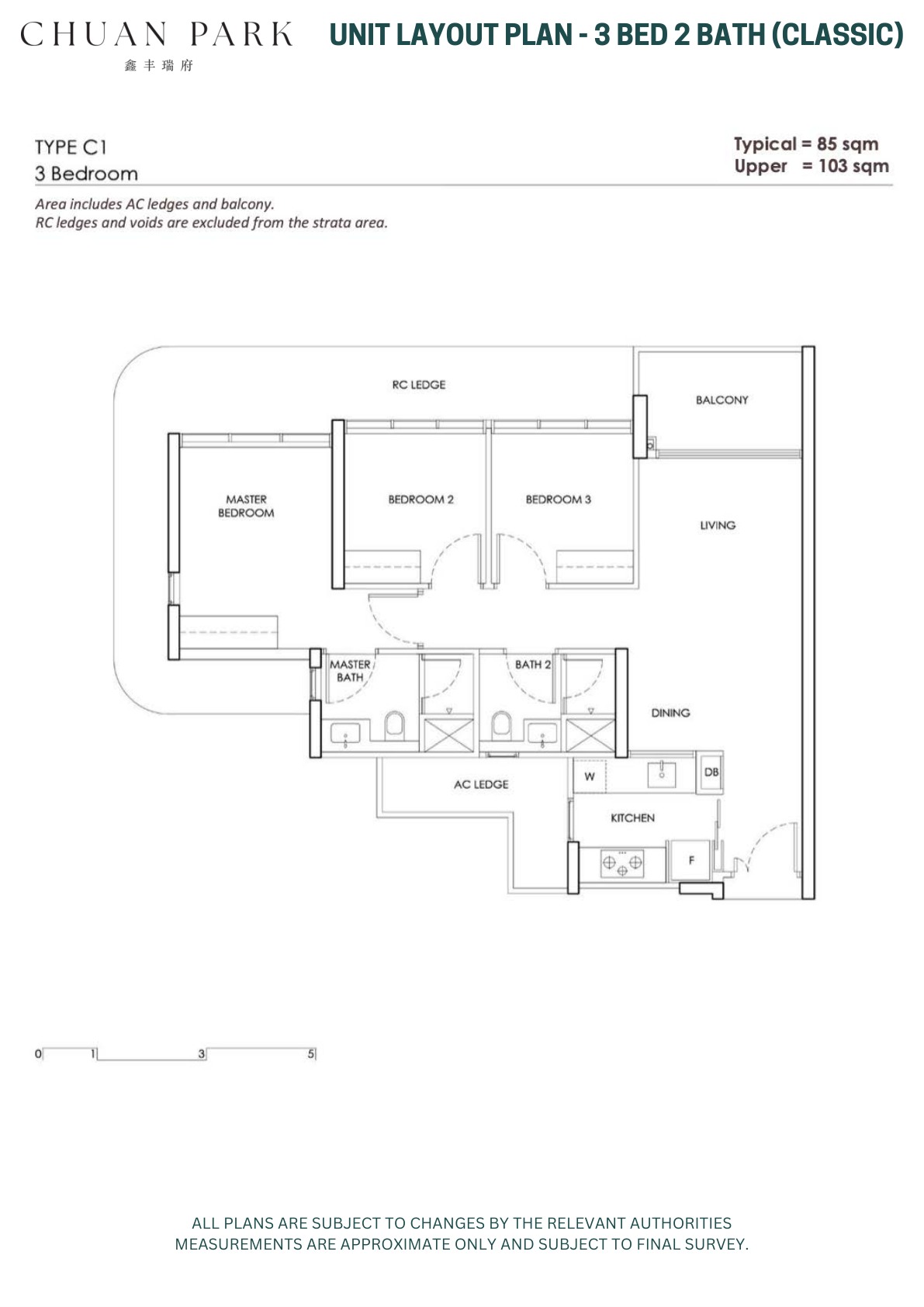

| 3 Bedroom Classic |

85-104 sqm |

Subtype count varies by latest balance-unit list |

| 3 Bedroom Deluxe |

95 / 96 / 112 sqm |

Subtype count varies by latest balance-unit list |

| 3 Bedroom Premium |

112-140 sqm |

Subtype count varies by latest balance-unit list |

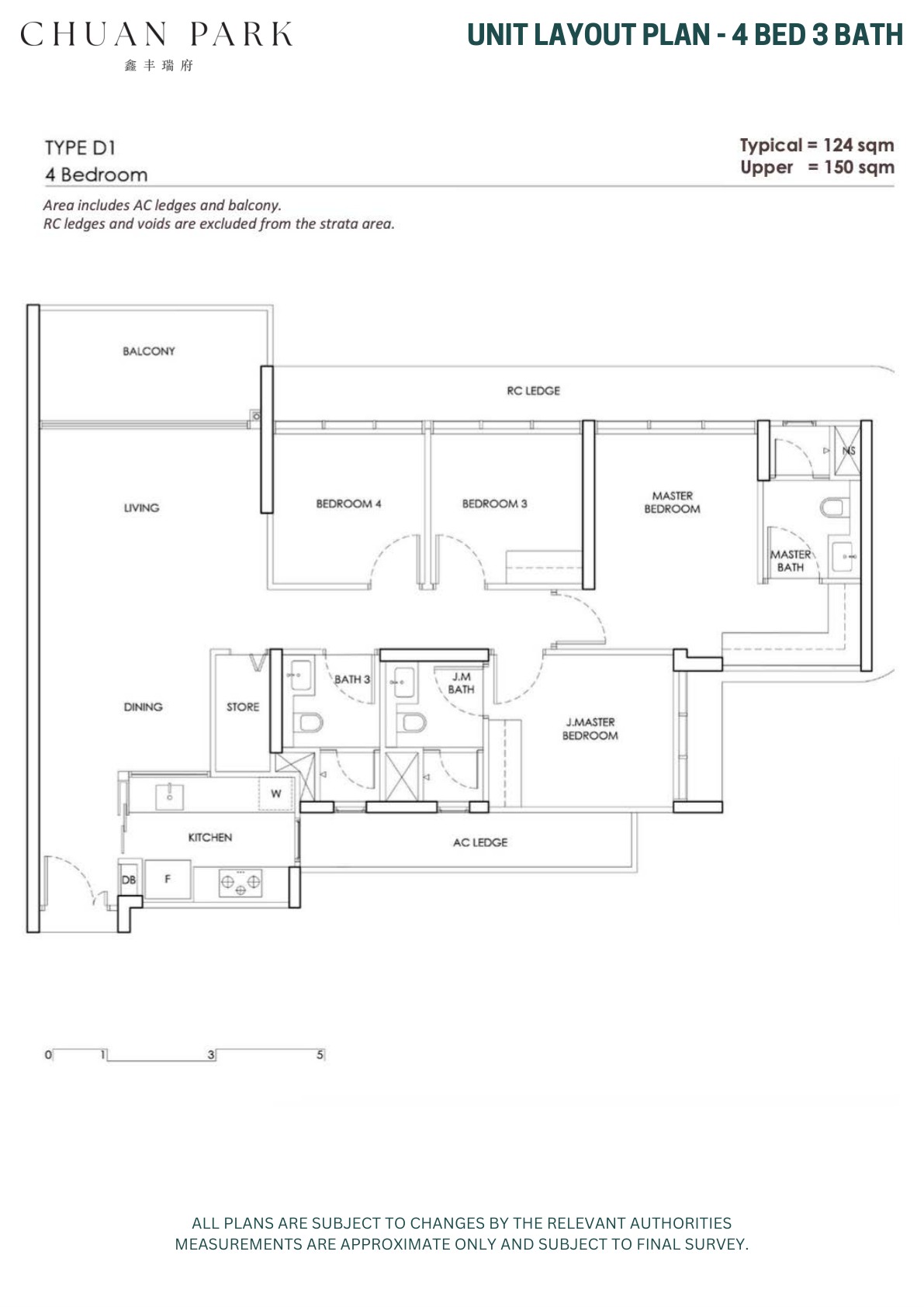

| 4 Bedroom Classic / Premium |

124-156 sqm |

Subtype count varies by latest balance-unit list |

| 5 Bedroom |

144 / 171 sqm (LR) |

Subtype count varies by latest balance-unit list |

Unit areas and availability may change. Confirm the latest stack, price and size information before shortlisting.

Indicative Pricing

Entry Units

From S$1.961M

2BR + Study, 743-883 sqft

Family Units

From S$3.171M

3BR, 1,206-1,507 sqft

Larger Units

From S$3.557M

4BR; 5BR from S$3.939M

Available units from S$1.961M; 2BR from S$2.030M, 2BR+Study from S$1.961M, 3BR from S$3.171M, 4BR from S$3.557M and 5BR from S$3.939M. Source: Chuan Park public price list updated 19 Mar 2026, accessed 29 Apr 2026.

Why Buyers Are Watching

-

1

Large 916-unit redevelopment beside the Lorong Chuan residential corridor.

-

2

Five-block scale with full condominium facilities and two shop units.

-

3

Site plan and diagrammatic layout references are available below for stack and facilities review.

-

4

Unit range starts from 2-bedroom homes; no 1-bedroom layout is listed in the available floor-plan set.

-

5

Estimated vacant possession is 31 December 2028.

-

6

Nearby MRT, schools and Serangoon/Lorong Chuan amenities support owner-occupier demand.

Location and Connectivity

MRT

Lorong Chuan MRT corridor

The project sits in the Lorong Chuan / Serangoon Garden area.

Schools

Neighbourhood schools

Catalogue highlights nearby schools and established landed/residential precincts.

Amenities

NEX / Serangoon Garden

Serangoon, Bishan and Ang Mo Kio amenities are reachable from the site.

Roads

CTE / PIE access

Central and north-east road connections support citywide access.

Schools Nearby

| School Planning |

Confirm current school distance bands and eligibility with OneMap and MOE before relying on any school-distance claim. |

Lifestyle and Amenities

Daily Convenience

Review nearby retail, food, transport and park connections before shortlisting stacks.

Neighbourhood Fit

Compare the surrounding precinct with your commute, school and lifestyle needs.

Viewing Check

Confirm walking routes, traffic patterns and future works during your site visit.

Site Plan

Actual site plan showing blocks, facilities, access points and internal landscaping.

Floor Plans (Selected)

Representative actual floor plans by unit type. The full floor-plan PDF belongs in the download button below this section.

Chuan Park starts from 2-bedroom layouts, so selected thumbnails begin at the smallest available unit type.

2 Bedroom + Study Type B2

3 Bedroom Classic Type C7

4 Bedroom Type D1

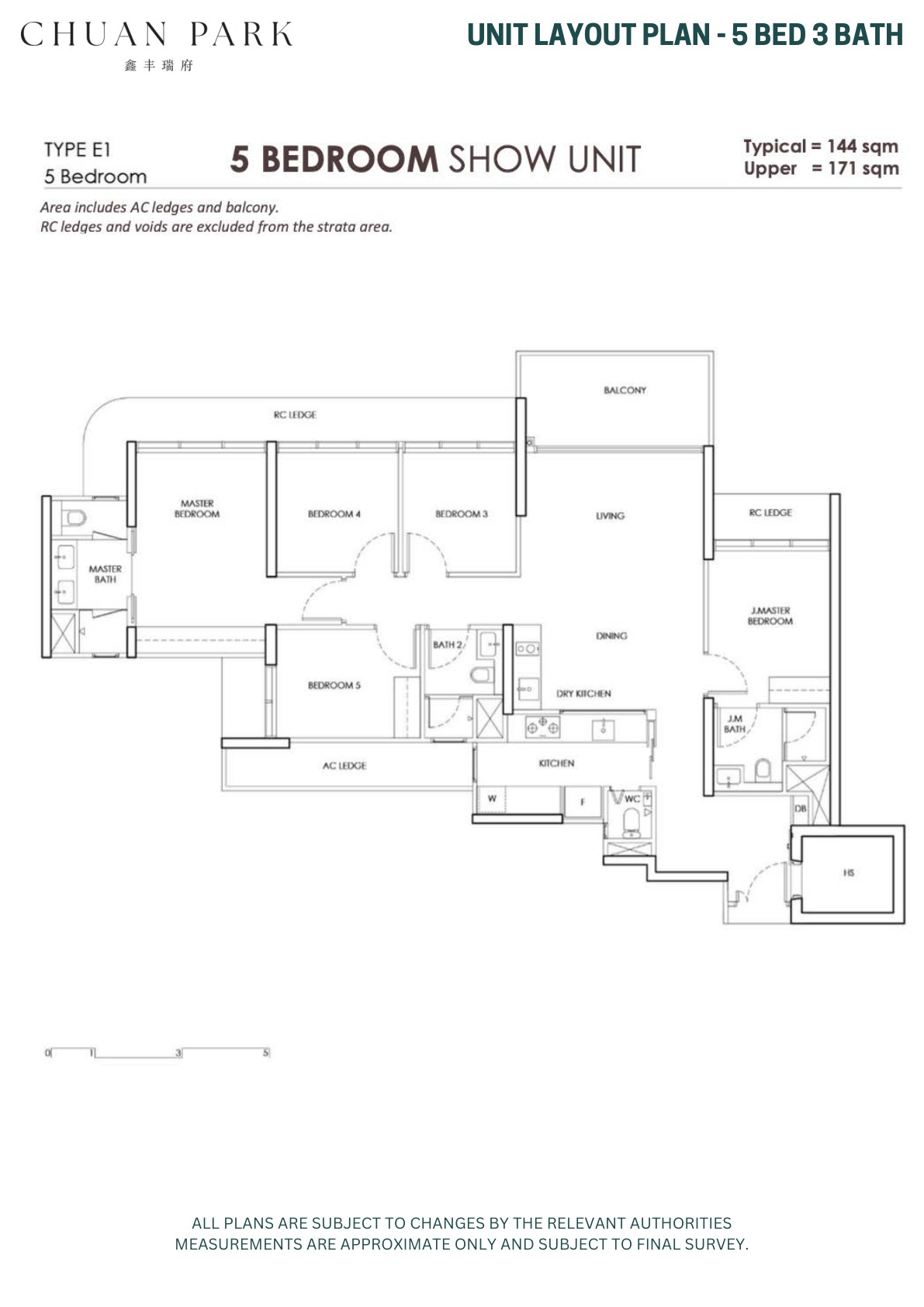

5 Bedroom Type E1

Elevation and Stack Chart

Refer to the site plan, selected layouts and full floor-plan PDF for stack orientation, floor levels and facing checks.

Facilities (30+)

Pool DeckClubhouseGymLandscape CourtyardsFunction RoomsFamily FacilitiesArrival CourtSmart Home Provisions

Developer and Consultant Team

Chuan Park Development Pte Ltd (Kingsford-MCC)

Before committing, verify the latest developer licence, project account details and contractual documents with the appointed sales team.

Sustainability and Specifications

Specifications, finishes, smart-home provisions and sustainability ratings vary by unit. Refer to the latest developer brochure and sale documents for final approved details.

Project Timeline

| Launch / Sales Phase |

Live new-launch project page |

| TOP / Vacant Possession |

31 December 2028 (estimated vacant possession) |

| Legal Completion |

31 December 2031 |

Project Factsheet

A shareable 2-page PDF snapshot of everything on this page — bring it to viewings, forward it to family.

Download the Full Sales Pack

PDF · Factsheet

Chuan Park Factsheet

2-page project factsheet with key facts, unit mix and buyer notes.

Download Factsheet

PDF · Floor Plans

Full Floor Plans

Selected floor-plan pages and layouts for quick comparison.

Download Floor Plans

Image · Site Plan

Site Plan

Site plan showing blocks, facilities and arrival points.

Download Site Plan

Frequently Asked Questions

Where is Chuan Park located?

Lorong Chuan, Singapore

Who is the developer?

Chuan Park Development Pte Ltd (Kingsford-MCC)

How many units are there?

916 residential units + 2 shop units

What is the current from-price?

Available units start from S$1.961M based on the public price list updated 19 Mar 2026. Confirm stack-specific pricing, discounts and availability before shortlisting.

Ready to see Chuan Park in person?

Request current availability, developer pricing, showflat slots and financing checks.

Enquire Now

Related Buying Guides

Stamp-duty planning before purchase.

Budget, timeline and financing basics.

Holding cost and exit considerations.

Disclaimer: Prices, availability, areas, specifications and timelines may change without notice. Buyers should verify all details with the developer-appointed sales team and relevant authorities before committing.