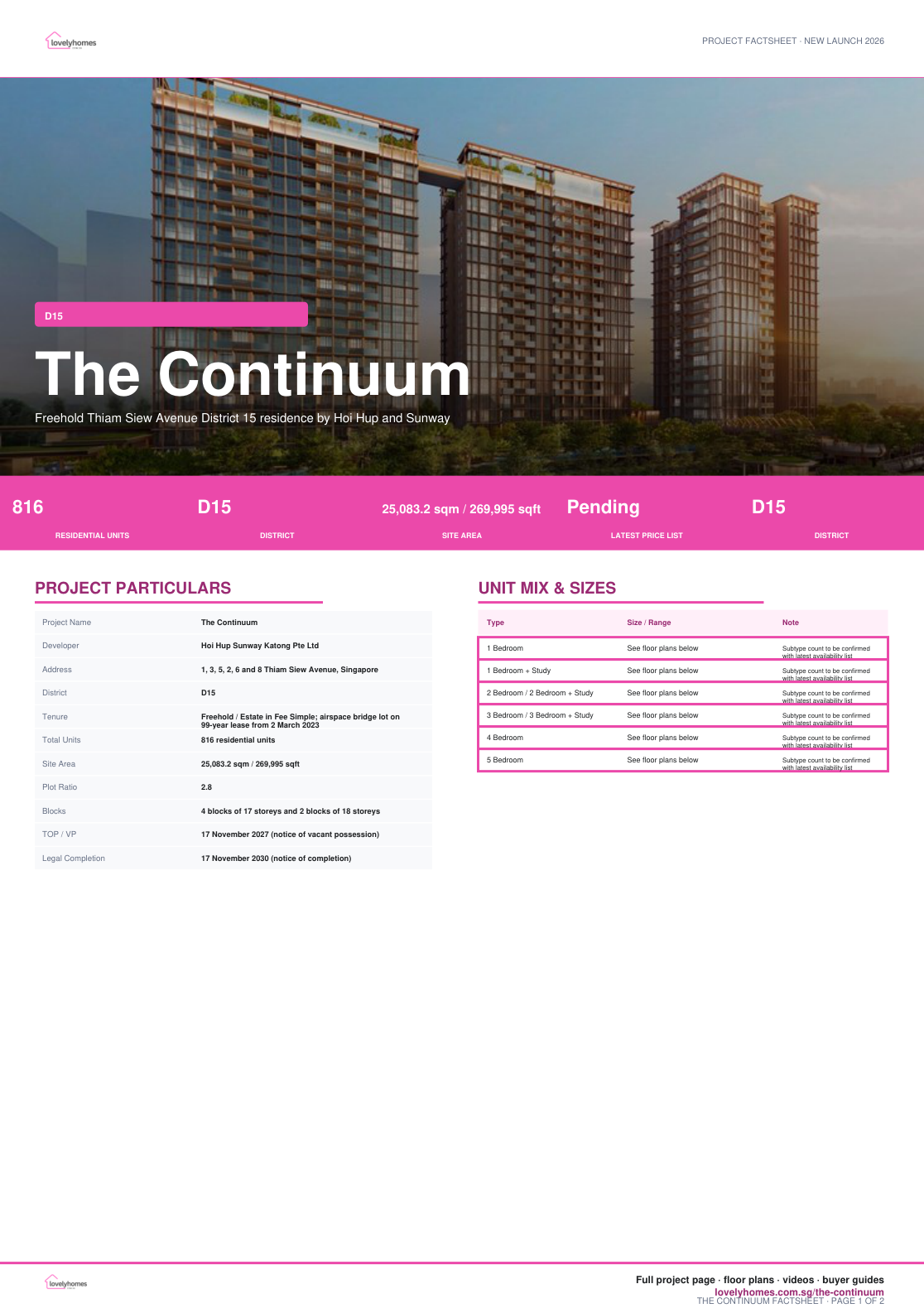

The Continuum The Continuum is a freehold District 15 residence across Thiam Siew Avenue, pairing Katong and Joo Chiat lifestyle access with 816 homes and a broad mix from compact layouts to larger private-lift homes.

01 · Address

D15 Location

1, 3, 5, 2, 6 and 8 Thiam Siew Avenue, Singapore

02 · Scale

816 residential units

4 blocks of 17 storeys and 2 blocks of 18 storeys

03 · Tenure

Freehold / Estate in Fee Simple; airspace bridge lot on 99-year lease from 2 March 2023

Confirm the latest availability before shortlisting.

Project At-a-Glance

Project Name

The Continuum

Developer

Hoi Hup Sunway Katong Pte Ltd

Address

1, 3, 5, 2, 6 and 8 Thiam Siew Avenue, Singapore

District

D15

Tenure

Freehold / Estate in Fee Simple; airspace bridge lot on 99-year lease from 2 March 2023

Total Units

816 residential units

Site Area

25,083.2 sqm / 269,995 sqft

Plot Ratio

2.8

Blocks

4 blocks of 17 storeys and 2 blocks of 18 storeys

TOP / VP

17 November 2027 (notice of vacant possession)

Legal Completion

17 November 2030 (notice of completion)

Viewing Preparation

Use the factsheet, selected floor plans and site plan below to compare the north and south plots, unit positions and larger-format layouts.

Confirm current pricing, stack availability and final specifications before booking.

Unit Mix and Sizes

Bedroom Type

Size / Range

Availability Note

1 Bedroom

See floor plans below

Subtype count varies by latest balance-unit list

1 Bedroom + Study

See floor plans below

Subtype count varies by latest balance-unit list

2 Bedroom / 2 Bedroom + Study

See floor plans below

Subtype count varies by latest balance-unit list

3 Bedroom / 3 Bedroom + Study

See floor plans below

Subtype count varies by latest balance-unit list

4 Bedroom

See floor plans below

Subtype count varies by latest balance-unit list

5 Bedroom

See floor plans below

Subtype count varies by latest balance-unit list

Unit areas and availability may change. Confirm the latest stack, price and size information before shortlisting.

Indicative Pricing

Entry Units

From S$1.378M

1BR + Study, 560 sqft

3BR Units

From S$2.880M

3BR, 1,076-1,141 sqft

Larger Units

From S$3.653M

4BR; 5BR from S$5.487M

Available units from S$1.378M; 3BR from S$2.880M, 3BR+Study from S$3.372M, 4BR from S$3.653M, 4BR Premier from S$4.481M and 5BR from S$5.487M. Source: The Continuum public price list updated 7 Mar 2026, accessed 29 Apr 2026.

Why Buyers Are Watching

1

Freehold District 15 address near the Katong/Joo Chiat lifestyle corridor.

2

816 units are planned across six residential blocks.

3

Conservation bungalow and proposed overhead bridge are included in the project description.

4

Selected 3-, 4- and 5-bedroom homes include private-lift lobby layouts.

5

Notice of vacant possession is listed as 17 November 2027.

6

The page includes a site plan image and representative floor-plan pages.

Location and Connectivity

MRT

Paya Lebar / Dakota / Katong access

Location material places the project in the East Coast / city-fringe network.

Lifestyle

Katong and Joo Chiat

Dining, conservation streets and East Coast amenities support daily convenience.

Schools

District 15 education options

Verify current school distance bands with OneMap before enrolment planning.

Roads

ECP / PIE / city routes

City and airport routes are accessible through the East Coast road network.

Schools Nearby

School Planning

Confirm current school distance bands and eligibility with OneMap and MOE before relying on any school-distance claim.

Lifestyle and Amenities

Daily Convenience

Review nearby retail, food, transport and park connections before shortlisting stacks.

Neighbourhood Fit

Compare the surrounding precinct with your commute, school and lifestyle needs.

Viewing Check

Confirm walking routes, traffic patterns and future works during your site visit.

Site Plan

Actual site plan showing blocks, facilities, access points and internal landscaping.

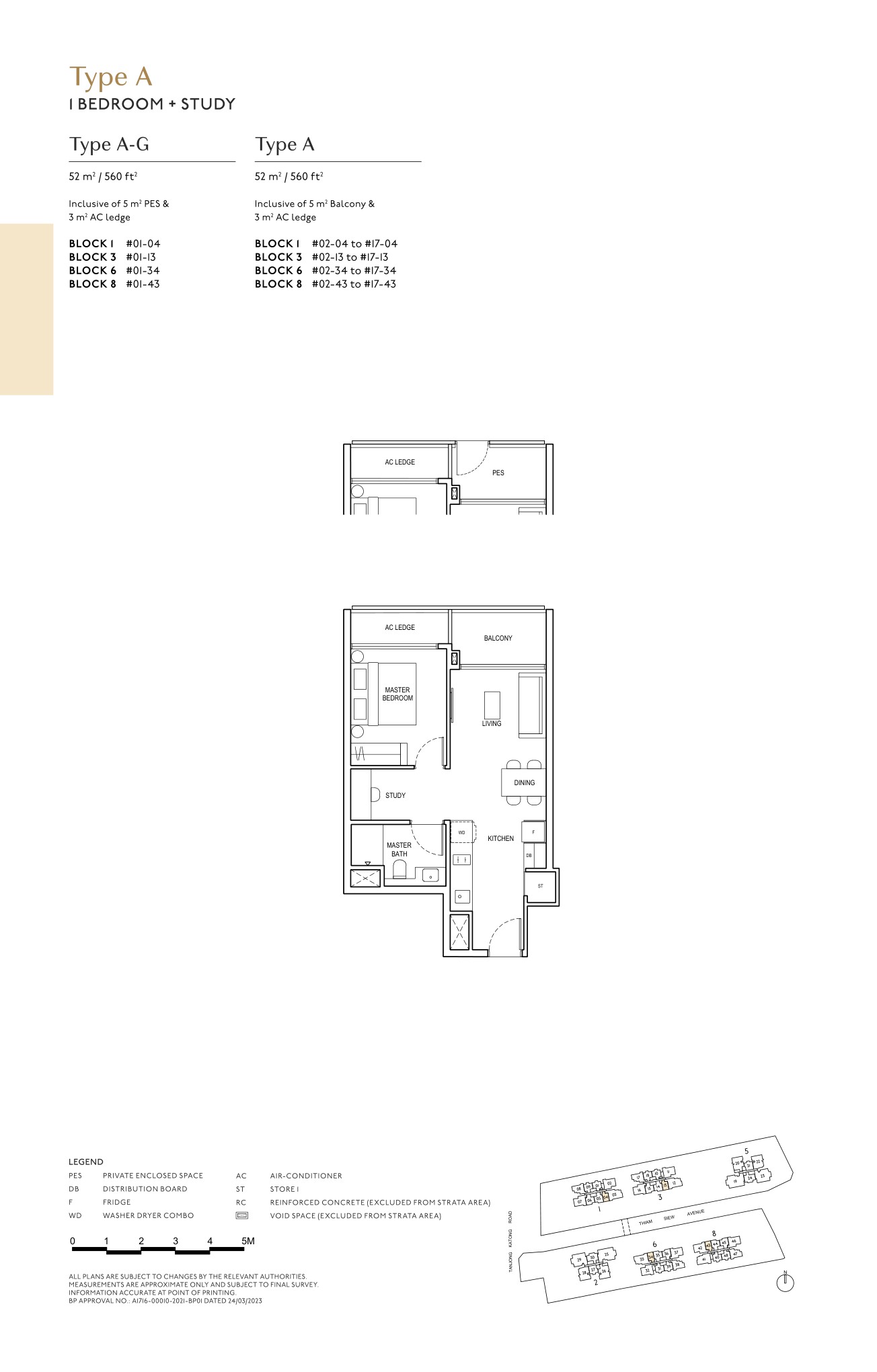

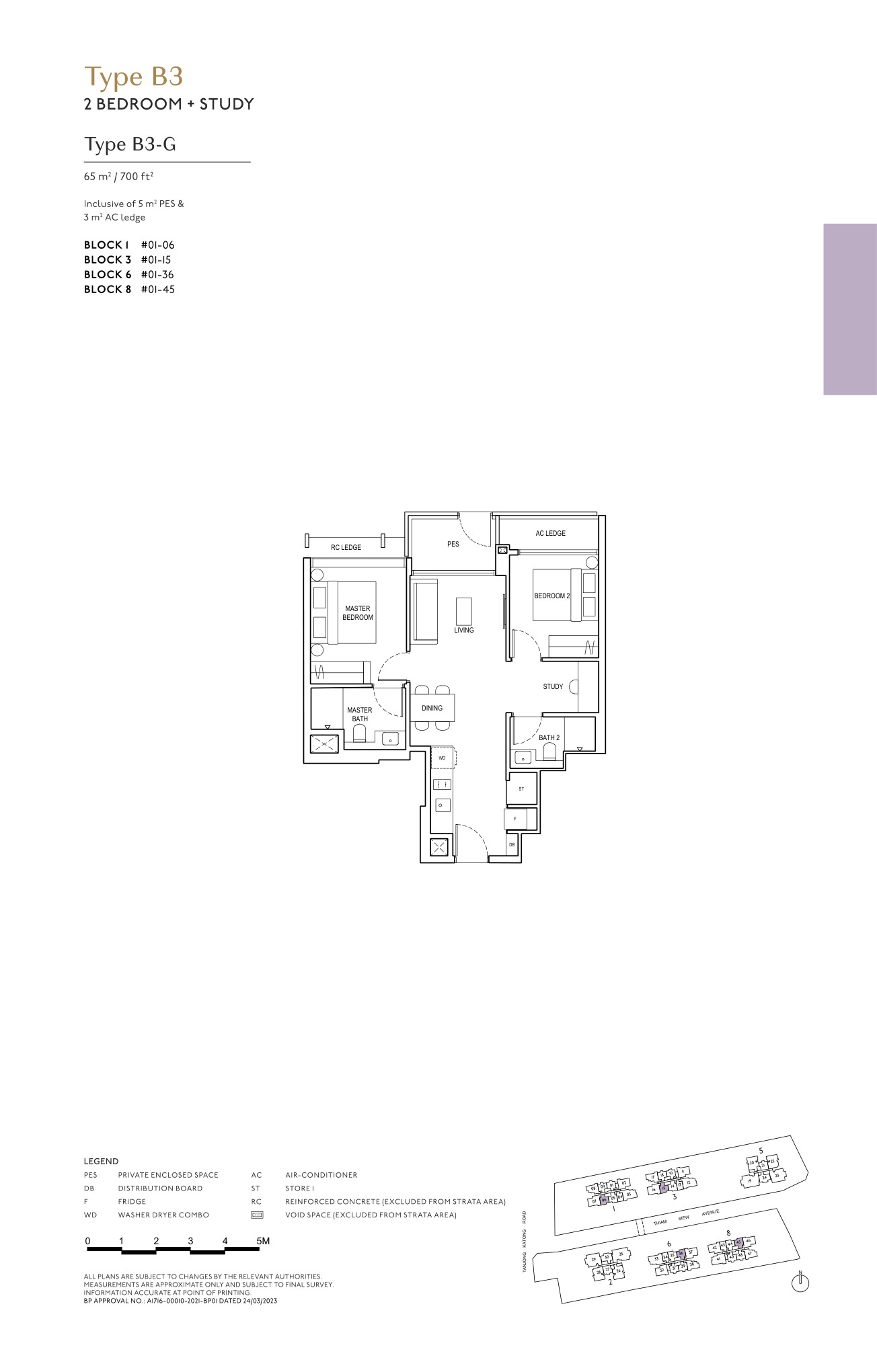

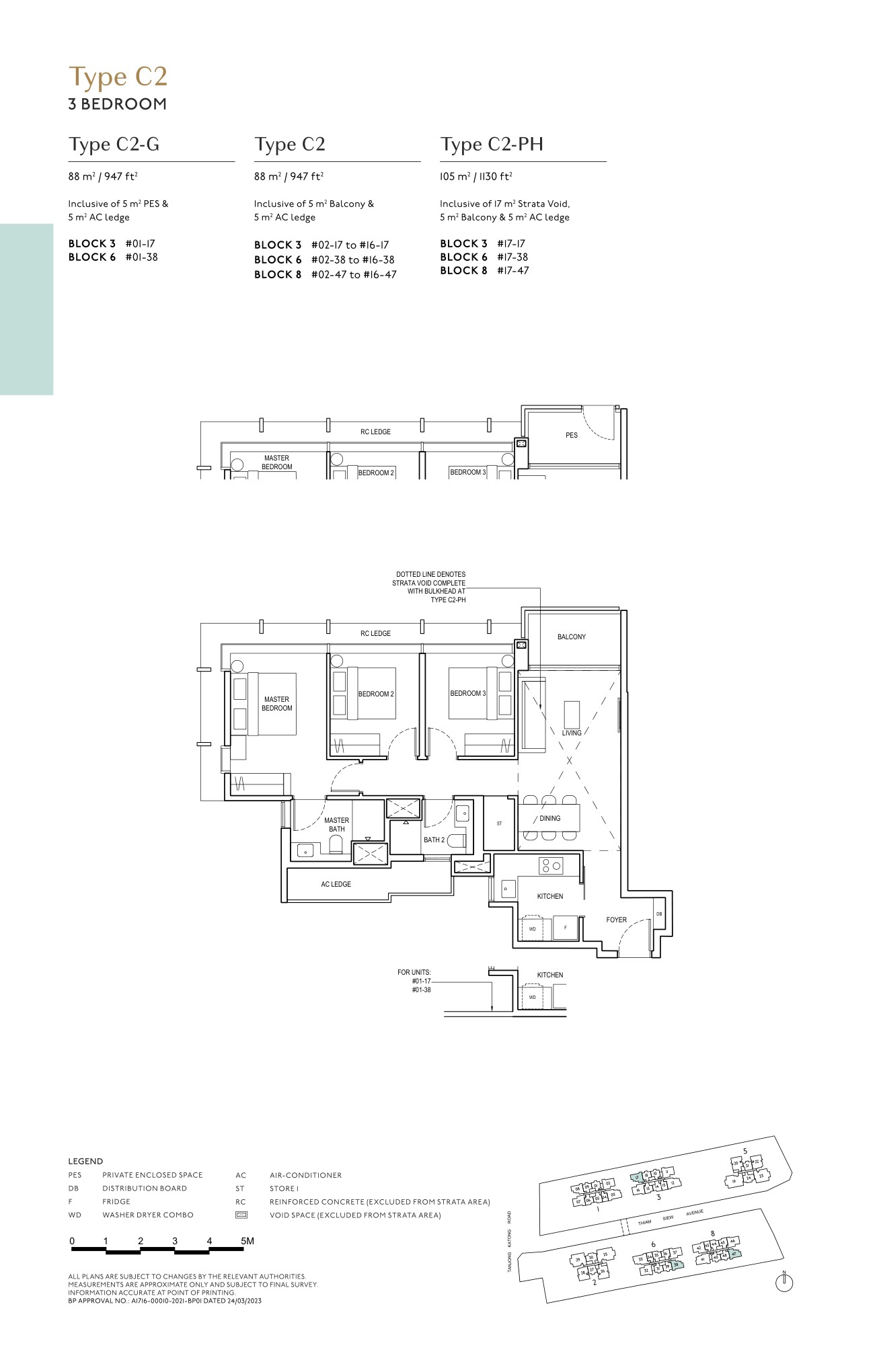

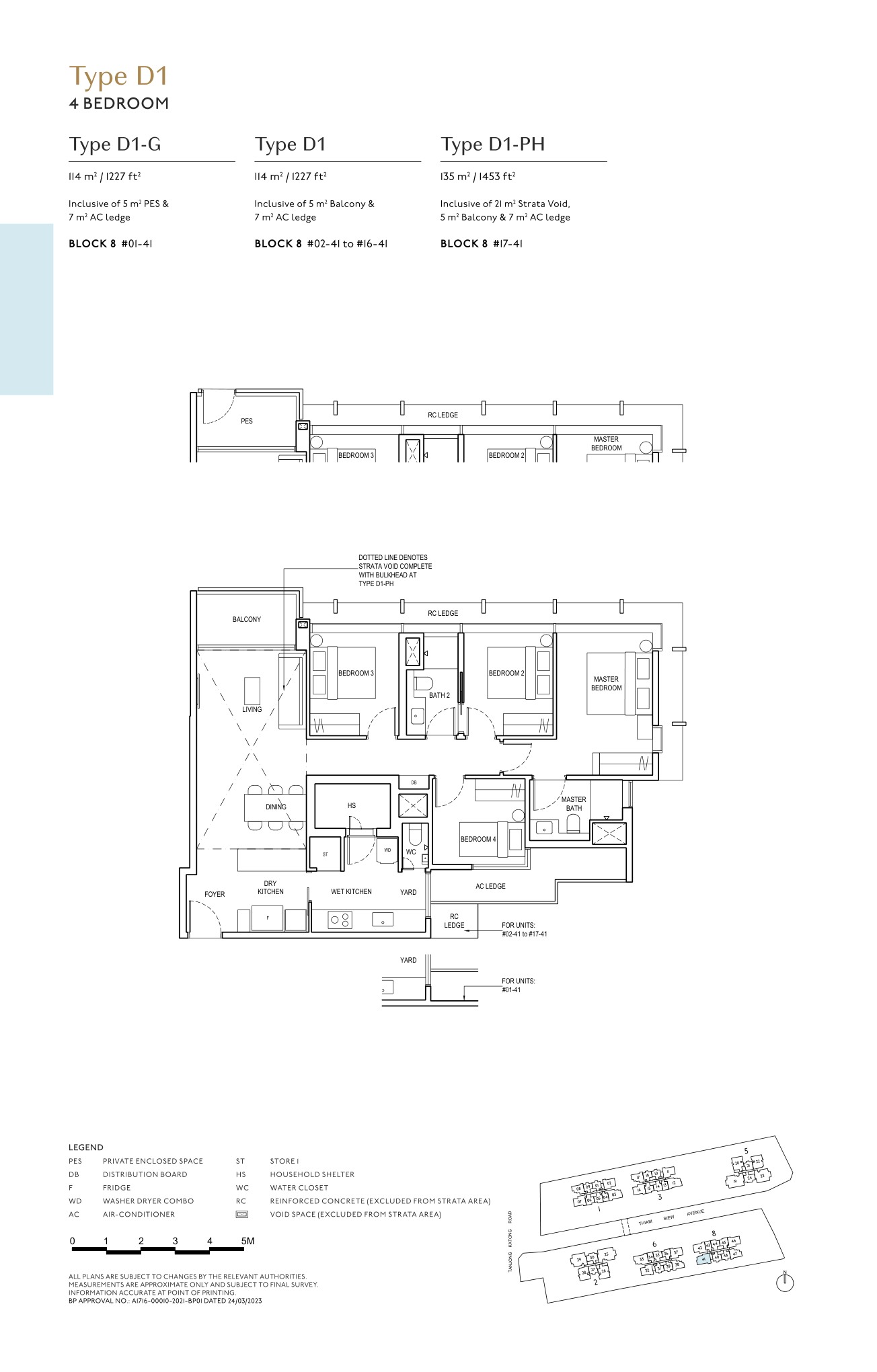

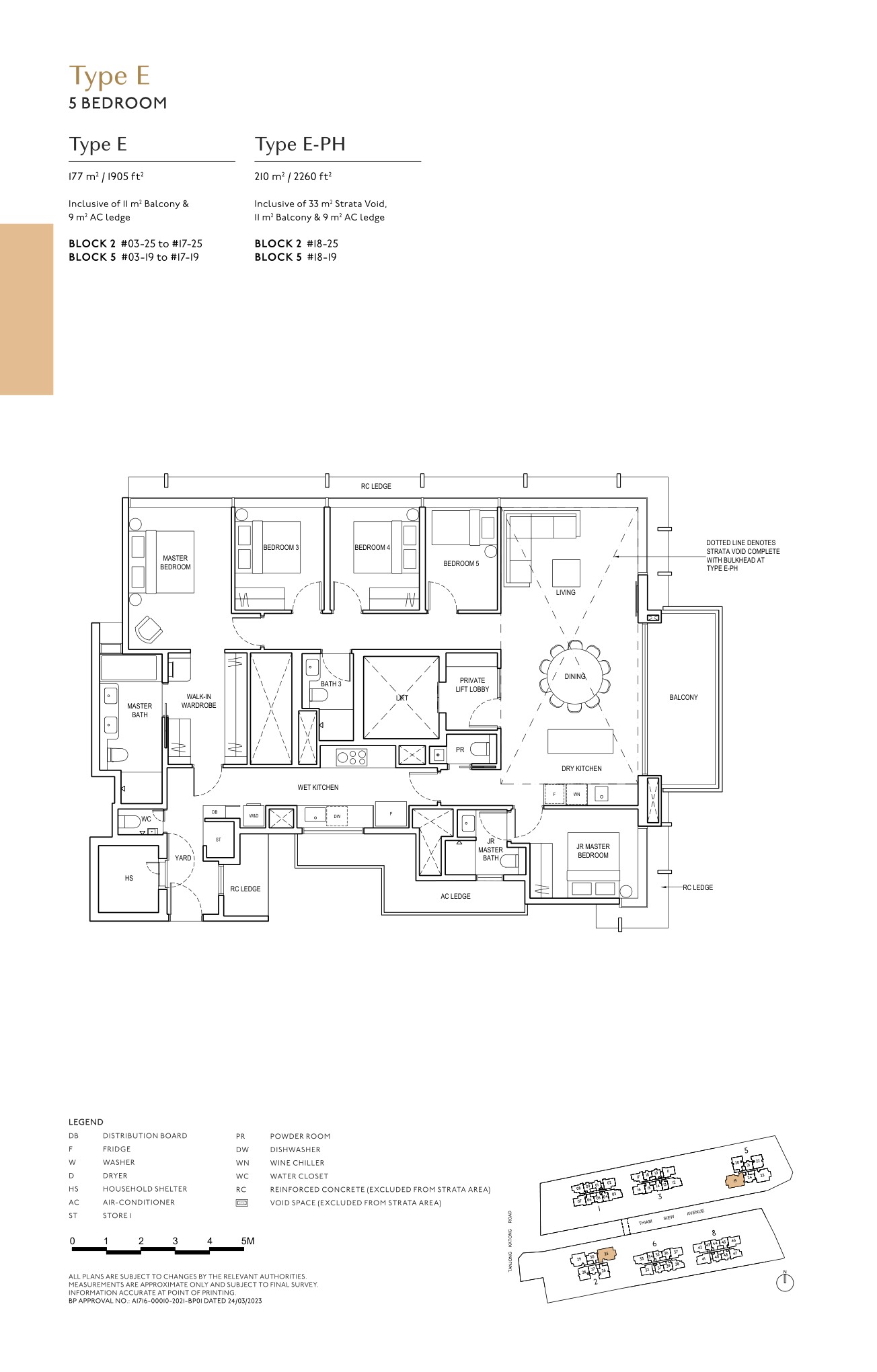

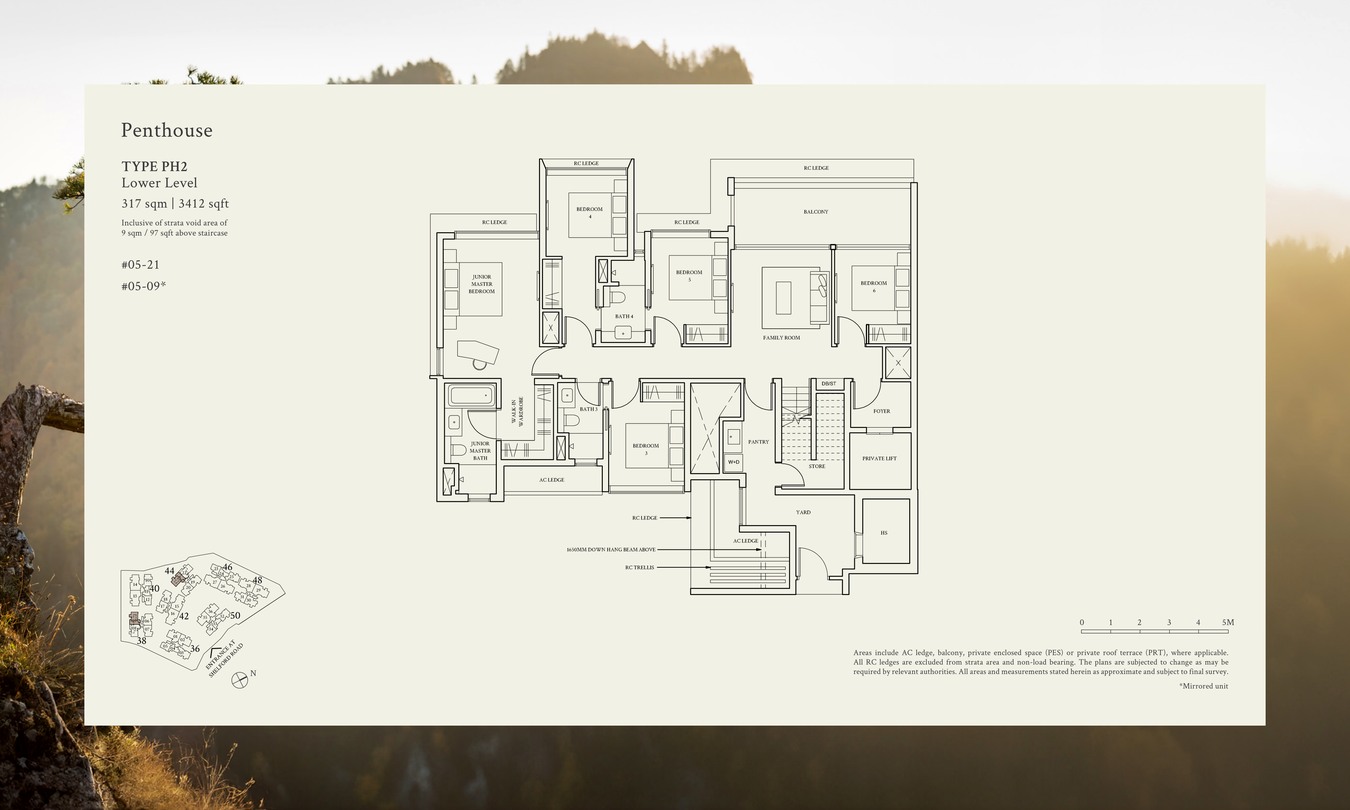

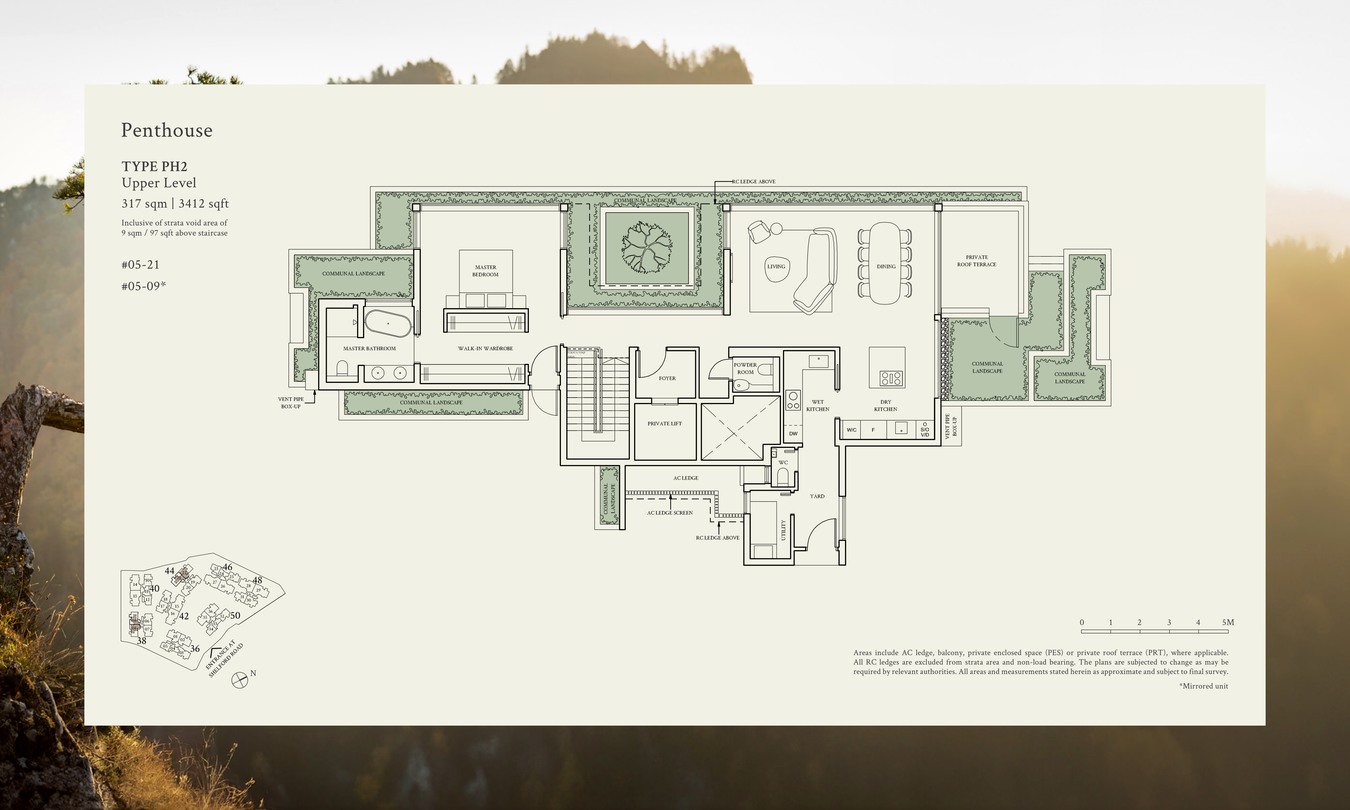

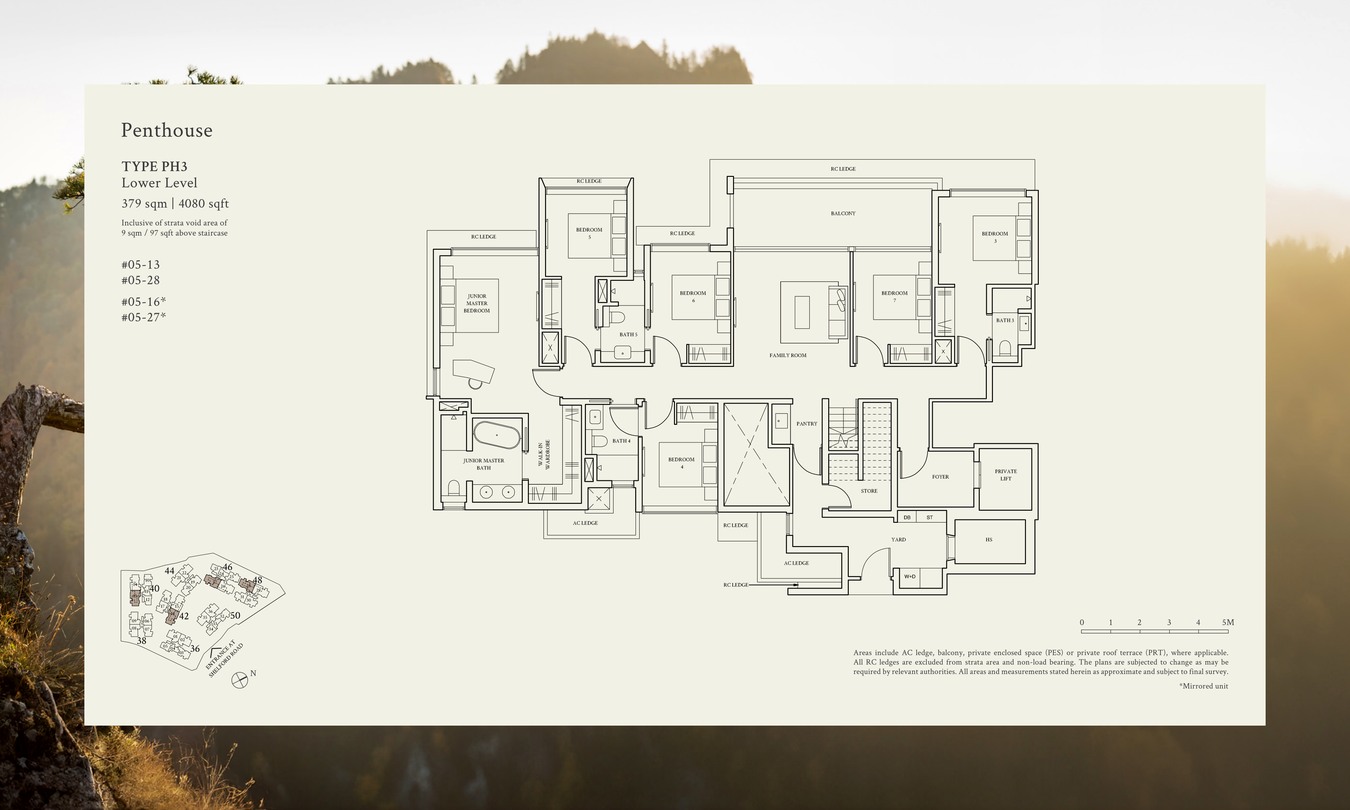

Floor Plans (Selected)

Representative actual floor plans by unit type. The full floor-plan PDF belongs in the download button below this section.

1 Bedroom Type A

2 Bedroom + Study Type B

3 Bedroom Type C

4 Bedroom Type D

5 Bedroom Type E

Full Floor Plans PDF

Selected layout pages prepared as a clean PDF download.

Refer to the site plan, selected layouts and full floor-plan PDF for stack orientation, floor levels and facing checks.

Facilities (30+)

Pool DeckClubhouseGymLandscape CourtyardsFunction RoomsFamily FacilitiesArrival CourtSmart Home Provisions

Gallery

Developer and Consultant Team

Hoi Hup Sunway Katong Pte Ltd

Before committing, verify the latest developer licence, project account details and contractual documents with the appointed sales team.

Sustainability and Specifications

Specifications, finishes, smart-home provisions and sustainability ratings vary by unit. Refer to the latest developer brochure and sale documents for final approved details.

Project Timeline

Launch / Sales Phase

Live new-launch project page

TOP / Vacant Possession

17 November 2027 (notice of vacant possession)

Legal Completion

17 November 2030 (notice of completion)

Project Factsheet

A shareable 2-page PDF snapshot of everything on this page — bring it to viewings, forward it to family.

Available units start from S$1.378M based on the public price list updated 7 Mar 2026. Confirm stack-specific pricing, discounts and availability before shortlisting.

Ready to see The Continuum in person?

Request current availability, developer pricing, showflat slots and financing checks.

Disclaimer: Prices, availability, areas, specifications and timelines may change without notice. Buyers should verify all details with the developer-appointed sales team and relevant authorities before committing.

Watten House is a 180-unit freehold residential development in District 11, Singapore, developed by UOL × Singapore Land Group with an estimated TOP of 2028.

01 · Location

District 11 Address

Well-connected neighbourhood with access to public transport, schools, and lifestyle amenities.

02 · Scale

180 Residences

Freehold development with quality fittings, smart-home provisions, and full condominium facilities.

03 · Value

New-Launch Advantage

Progressive payment schedule, 12-month Defects Liability Period, and modern specifications throughout.

Project At-a-Glance

Project Name

Watten House

Developer

UOL × Singapore Land Group

District

D11

Tenure

Freehold

Total Units

180

Est. TOP (VP)

2028

Est. Legal Completion

2031

Unit Mix and Sizes

Bedroom Type

Size (sqft)

Units

% of Total

Download the project factsheet for the full unit mix breakdown and confirmed sizes.

Refer to the developer’s official sales kit for confirmed unit types, sizes, and availability. Download factsheet (PDF).

Indicative Pricing

3BR to 5BR

From S$4.799M

Remaining balance units

Availability

2 units

98% sold snapshot

Tenure

Freehold

Shelford Road, D11

Current public availability shows 3BR to 5BR balance units from S$4.799M, with 2 of 180 units available in the 7 Mar 2026 snapshot. Source: Watten House NewLaunches price page and official update dated Apr 2026, accessed 29 Apr 2026.

Why Buyers Are Watching

1

District 11 location — well-connected address with MRT access, expressways, and lifestyle amenities in an established residential corridor.

2

Freehold — Freehold title with no lease decay — perpetual ownership ideal for long-term holds and estate planning.

3

180 residential units — boutique scale ensuring exclusivity and a curated ownership community.

4

Developer pedigree — UOL × Singapore Land Group brings a track record of quality residential development across Singapore’s private property market.

5

Progressive payment advantage — staggered cash outlay during construction typically saves S$30,000–S$60,000 in loan interest compared to a full resale drawdown.

6

12-month Defects Liability Period — legally binding developer obligation to rectify defects at no cost within 12 months of TOP.

Location and Connectivity

Transport

MRT Access

Conveniently located near MRT stations connecting to the wider Singapore rail network.

Expressways

Road Connectivity

Access to major expressways for quick connections to the CBD, Changi Airport, and key destinations.

Lifestyle

Shopping & Dining

Nearby malls, hawker centres, supermarkets, and F&B within the immediate neighbourhood.

Schools

Education Belt

Primary and secondary schools within 1–2 km, with tertiary institutions in the broader district.

Schools within 1–2 km — refer to MOE SchoolFinder for 2026 Phase 2B catchment zones at this address.

Secondary Schools

Secondary schools serving the District 11 catchment — verify distances via OneMap.

International Schools

Multiple international schools within the broader district and surrounding areas.

Lifestyle and Amenities

Recreation & Wellness

Swimming pool, gymnasium, function rooms, and landscaped communal spaces for an active lifestyle.

Dining & Retail

Nearby malls, hawker centres, and F&B outlets serving everyday needs and weekend leisure.

Green Spaces

Parks and park connectors supporting an active outdoor lifestyle in Singapore’s City in Nature vision.

Site Plan

Actual site plan from project source materials.

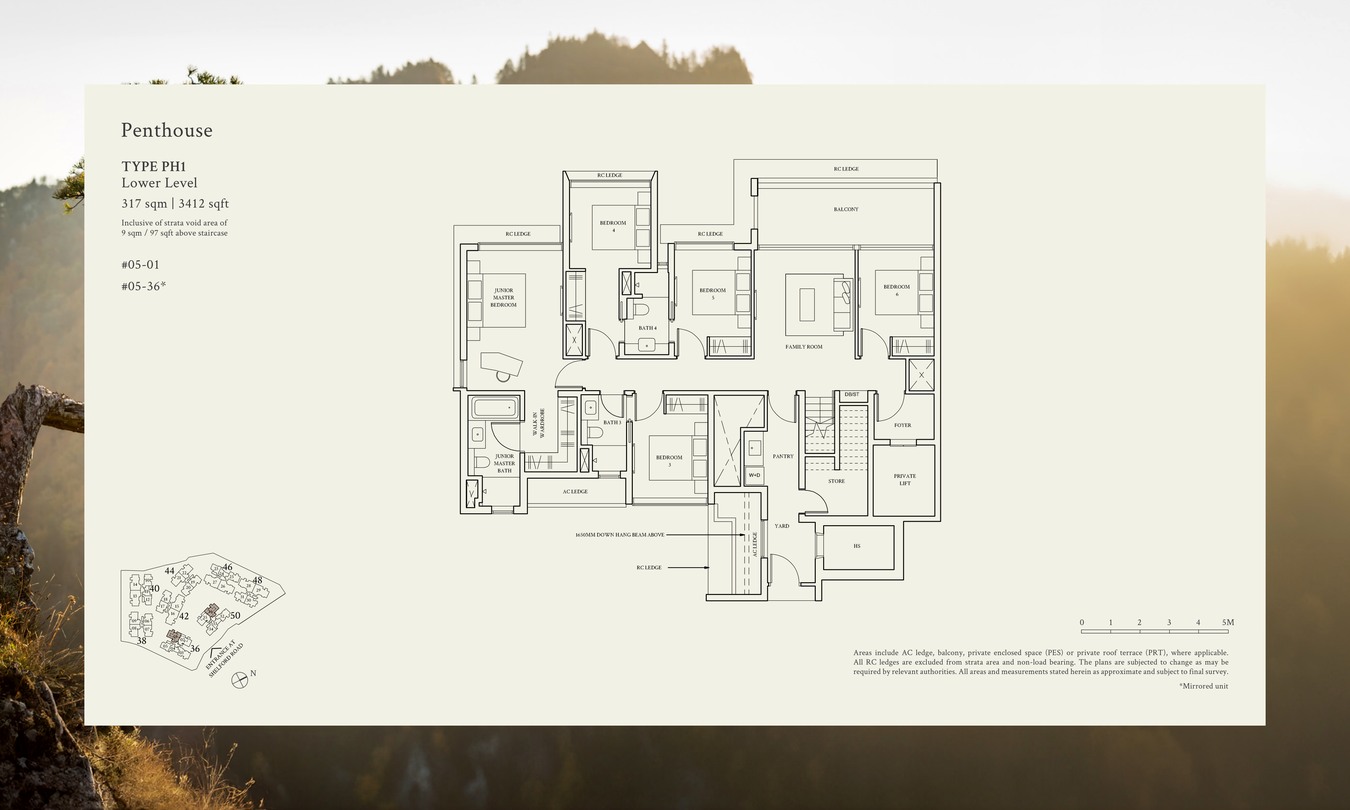

Floor Plans (Selected)

Representative actual floor plans for the unit types available in the current source package: 3 Bedroom, 4 Bedroom, 5 Bedroom, 5 Bedroom Premium and Penthouse. The source materials reviewed for Watten House do not include 1-bedroom or 2-bedroom layouts. Download the full floor-plan PDF below for the complete source set.

3 Bedroom

4 Bedroom

5 Bedroom

5 Bedroom Premium

Penthouse

Full Floor Plans PDF

All selected layout pages and unit dimensions for buyer review.

Elevation overview · indicative only · refer to developer’s official stack chart for confirmed positions

Facilities (30+)

Swimming PoolGymnasiumFunction RoomsBBQ PavilionsChildren’s PoolJacuzziClub LoungeGarden PavilionSky TerraceYoga LawnSmart Home SystemEV Charging24-Hour SecurityBicycle BaysPneumatic Waste System

Gallery

Developer and Consultant Team

UOL × Singapore Land Group

Developer of Watten House with residential development expertise in Singapore’s private property market. Consultant team details are available in the project factsheet.

Developer

UOL × Singapore Land Group

District

D11

Estimated TOP

2028

Sustainability and Specifications

BCA Green Mark: Designed to meet BCA Green Mark standards with energy-efficient envelope and water-efficient fittings.

Smart Home: Smart home management provisions across all units for access control and utilities.

EV Infrastructure: Electric vehicle charging provisions in basement carpark.

Quality Finishes: Premium materials and fittings in line with developer specifications throughout.

Project Timeline

2023–2024

Land Award & Licence

2024–2025

Sales Launch

2025–2028

Construction Phase

2028

Estimated TOP (VP)

2031

Legal Completion

Project Factsheet

A shareable 2-page PDF snapshot — bring it to viewings, share with family.

DISCLAIMER: All information is compiled from publicly available sources and developer-issued materials for informational purposes only. Prices, unit mix, specifications, and timelines are indicative and subject to change without notice. This page does not constitute an offer to buy or sell. Seek advice from a licensed property agent and legal counsel. LovelyHomes.com.sg is an independent editorial platform. Agency Licence: L3010858B.

Quick Answer — the Q1 2026 picture in five bullets

URA’s Q1 2026 flash estimate for the Private Residential Property Price Index (PPI) points to a measured quarter-on-quarter gain, continuing the moderating trend first visible in mid-2025.

Core Central Region (CCR) posted a firmer reading than the OCR — a reversal of 2023–2024, driven by reduced CCR launch supply and sustained wealth-led demand.

Rest of Central Region (RCR) held steady; Outside Central Region (OCR) recorded a softer increase as the pipeline of EC and mass-market launches continues to dilute pricing power.

Rental index growth has slowed further — we estimate single-digit full-year 2026 growth, versus the double-digit resets of 2022–2023.

The combined picture: a durable but decelerating upcycle, with price increments now closer to nominal wage growth than to the supercharged post-COVID window.

Singapore Private PPI — Q1 2026 Flash — LovelyHomes editorial infographic, 22 April 2026.

Context — why the Q1 2026 flash is worth reading carefully

URA’s flash estimate is the first public signal of where private residential prices settled in any given quarter. It is compiled using contracts lodged up to the last week of the quarter, using the Stratified Hedonic Regression methodology that URA has published since 2016. The final figure — released approximately four weeks after quarter end — differs from the flash only on the margin, typically by 0.1–0.3 percentage points.

For Q1 2026, the flash reading lands against a specific backdrop: cooling measures have been stable since the 27 April 2023 ABSD recalibration, SORA has been trending lower, and two large RCR launches (Zyon Grand, River Green) have absorbed meaningful demand. Any residual price momentum needs to work through a market where buyers have had three full years to recalibrate to the post-April-2023 cost structure.

What the flash suggests about each region

Singapore PPI Q1 2026 — Regional Snapshot (estimated)

Source: URA flash estimate tracking and internal analysis · 22 April 2026

Segment

Q1 2026 (QoQ, est.)

12-month moving (est.)

Overall Private Residential PPI

+0.8% to +1.2%

+3.0% to +3.8%

CCR (Core Central Region)

+1.2% to +1.6%

+3.8% to +4.6%

RCR (Rest of Central Region)

+0.5% to +0.9%

+2.5% to +3.3%

OCR (Outside Central Region)

+0.3% to +0.7%

+2.2% to +3.0%

Private Rental Index

+0.2% to +0.6%

+1.8% to +3.2%

Ranges are our internal estimates pending URA’s official flash release; the final quarterly figure typically lands within 0.1–0.3 percentage points of the flash.

The CCR reversal — why the prime segment is firmer in 2026

The narrative dominant in 2023–2024 ran: CCR is broken, OCR is the new leader. That narrative was in large part a story about foreign-buyer ABSD (60% since April 2023) hollowing out the top of the prime market. Three years on, several forces have reshuffled the cards:

Supply discipline in the CCR: Few new CCR launches have come to market since 2024 — UPPERHOUSE at Orchard Boulevard, Reignwood Hamilton Scotts, and a handful of freehold boutiques. Inventory is being absorbed faster than it is being replenished.

Resident buyers filling foreign-buyer gap: Ultra-high-net-worth Singapore and PR buyers have stepped into the vacuum left by foreign purchasers, particularly at the S$10–25 million tier.

Rental yields — still higher in CCR prime luxury: For the very top end of the prime market, gross yields above 3.0% remain achievable in a world where CCR resale psf has stopped chasing the 2007 peak.

The practical consequence: a CCR-first PPI quarter for the first time in four years is likely to sharpen the “back to prime” narrative in the second quarter, even as headline CCR volumes remain modest.

The RCR — held steady by a clean sweep of launch absorptions

The RCR in Q1 2026 reads as a market in balanced health. Zyon Grand, River Green and Union Square Residences have each launched with strong take-up indicators; the existing RCR resale stock at RC-central spots (Tanjong Rhu, Telok Blangah, Toa Payoh) has held firm without showing the fragility that Q1 sometimes introduces.

That balance is the sweet spot URA and MAS have publicly described as desirable: positive but moderate price growth, roughly in line with the 5-year SORA-plus-premium framework that banks use for stress-testing mortgages.

The OCR — softening, but not weakening

The OCR reading is the softest of the three regional buckets in Q1. This is not a weakening story; it is a supply story. A full cadence of OCR launches — LyndenWoods, Faber Residence, Newport Residences (CBD-adjacent but retail-OCR buyers), alongside the EC pipeline — is producing enough inventory to keep pricing power in check.

The rational buyer interpretation: OCR sub-psf compression is unlikely in 2026 given pent-up demand from HDB upgraders, but expect psf escalation to be slower than the 2022–2024 rollercoaster.

Rental trend — the single softest indicator

The rental index is the most instructive forward signal. Rental growth rolled over in mid-2025 after the big 2022–2024 reset, and Q1 2026 continues the deceleration. Two structural forces are at work:

Large tranche of MOP / EC completions that began coming through the rental market from late 2024, adding supply.

Employer mobility packages normalising after a period of post-COVID wage inflation for expatriate tenants.

If Q1 rental growth confirms at around +0.4% QoQ (our estimate), full-year 2026 rental growth is unlikely to exceed +3.2% — a material step-down from the +14.8% print of 2022 and +8.9% of 2023. Landlords pricing renewal increases should calibrate accordingly.

What this means for buyers, sellers and landlords

For buyers

Mass-market OCR launches: Psf escalation pressure is manageable; lock the psf you want and do not panic-buy.

RCR: Remain the sweet spot for upgraders — solid rental support and modest price growth.

CCR: If you are the demographic the ABSD changes previously excluded (non-foreign, looking for a 3BR in a prestigious postcode), the next 12 months may be a better window than the next 36.

For sellers

Resale pricing in the RCR should land close to psf of comparable transactions in the preceding two quarters — there is no sharp upward break to exploit.

In OCR resale, be realistic about competing against fresh launch stock. Price to the competition, not to a 2022 print.

For landlords

Renewals at +3% to +4% are defensible in most districts; above +5% may trigger a vacancy risk in the softer end of the rental market.

Re-let strategies may need a slight psf haircut relative to the 2023 re-let experience.

How the Q1 2026 flash connects to the policy story

Regulatory policy has been stable throughout Q1. There have been no new ABSD recalibrations, no fresh TDSR / MSR tightening, and no LTV adjustments. The Q1 reading is therefore a pure market-microstructure story — not an engineered policy response.

That has two implications. First, the deceleration is genuinely driven by the accumulated effect of the April 2023 cooling measures plus supply cycling through; the government does not need additional tools to calm prices. Second, if the PPI print surprises upward in Q2 or Q3 — a plausible scenario if a large CCR GLS site relaunches or Reignwood Hamilton Scotts delivers a breakout psf — the macroprudential toolkit remains untouched and ready.

The three charts to watch next quarter

CCR psf premium over RCR — if this widens two quarters running, the “back to prime” narrative becomes the dominant market story.

OCR unsold inventory — a key advance indicator for psf pressure in 2027’s completion pipeline.

Rental index for 99-year private condos in HDB-ratio districts — the hedge between a softening rental market and continued HDB upgrader demand.

Key takeaway

Key takeaway — a decelerating upcycle, not a correction

The Q1 2026 PPI flash reads as a confirmation, not a reset. Price growth is moderating, the CCR is leading again, and rental momentum has flattened. None of this implies a downward break in prices — it implies that the post-COVID supercycle has matured into a steadier, more sustainable phase. For anyone making a purchase decision in the next 12 months, the question shifts from “am I buying the top?” to “am I buying at fair psf given the yield outlook?”. That is a far healthier question than the one that dominated 2022.

Sources: Urban Redevelopment Authority (URA) Property Market Information portal (ura.gov.sg); Monetary Authority of Singapore (MAS) Financial Stability Review. Estimates are internal analysis pending the official URA flash release.

Source: URA — flash-estimate monitoring as at 22 April 2026.

Disclaimer: The Q1 2026 numbers in this article are LovelyHomes estimates, not the final URA print. Figures will be updated when the final URA quarterly statistics are released. This article is for information only and does not constitute investment advice.

Critical dates: BSD/ABSD in 14 days, SSD tracked from purchase date (3-year holding for resales), and TOP/CSC windows for new launches.

OTP to Completion — Milestones — LovelyHomes editorial infographic, 22 April 2026.

Why the legal timeline matters more than the price

Most Singapore condo buyers focus on the right things — psf, unit selection, bank loan, cooling measures — but then under-invest in understanding the legal timeline that sits between “I love this unit” and “here are my keys”. Missed deadlines in that window can cost the 1% option money, trigger additional stamp duty, invalidate loan approvals, or leave buyers unable to complete. This guide is the full walk-through: a calendar-day breakdown of what happens, who signs what, and where the common mistakes are.

We cover three transaction types: resale private condo, new launch from developer, and sub-sale (buying a unit whose TOP has not yet occurred from a first buyer who wants to exit). Each follows the same overall arc but has different sub-deadlines.

Stage 1 — Pre-OTP: the due diligence window

Before you sign an Option to Purchase, you have the cheapest leverage in the entire transaction. A buyer who walks away before the OTP loses only viewing time and the occasional lawyer consultation fee. After the OTP, that number jumps to 1% or more. Spend the pre-OTP window on:

Home loan in-principle approval (IPA). Secure this before signing the OTP. An IPA is typically valid for 30 days and costs nothing.

Property valuation. Have the bank’s valuation in hand. For a resale flat, if the offer price is above valuation, you must top up the difference in cash.

Physical inspection. Walk the unit at different times of day, check for water stains, examine the corridors, parking, lift lobbies.

Legal check — encumbrances. Your lawyer should run a pre-OTP title search to confirm no caveats, mortgages, or writs that haven’t been discharged.

MCST search. Confirm no active arrears on the property, no pending special assessments, no upcoming major works (which could mean sinking-fund levies).

Stage 2 — Option to Purchase (OTP)

The OTP is a unilateral contract: you pay the seller 1% of the purchase price (the “Option Fee”) and, in return, the seller gives you an exclusive right (an “option”) to buy the property within 14 days for the agreed price. The seller cannot sell to anyone else during the option period.

What the OTP includes

Purchase price.

Option Fee (1% of purchase price).

Exercise Fee (usually 4% of purchase price for resale; 9% for some resale negotiations where 5% + 5% split is bundled).

Completion date (normally 10–12 weeks after option exercise).

Full schedule of fixtures and fittings.

Specific representations and warranties (title, encumbrances, occupation).

The 14-day clock starts

From Day 0 (date of OTP), the buyer has 14 calendar days to “exercise” the option — i.e., sign the acceptance copy and pay the remainder of the deposit (typically 4%). If the buyer lets Day 14 pass without exercising, the OTP lapses and the 1% Option Fee is forfeit.

Re-issue options and walking away

Occasionally buyers negotiate a re-issue of the OTP (e.g., pay another 1% for another 14 days). This is a commercial negotiation, not a statutory right. Always document the re-issue in writing with both parties’ lawyers.

Stage 3 — Exercise of Option (Day 1–14)

Exercising the option converts the one-sided right into a binding contract of sale. On exercise:

Buyer pays the Exercise Fee (4% of purchase price, bringing total paid to 5%).

Buyer’s lawyer lodges a caveat on the property title.

Stamp duty clock starts — BSD (Buyer’s Stamp Duty) and ABSD are due within 14 days of the date of exercise.

The 3-year SSD (Seller’s Stamp Duty) holding period starts ticking from the exercise date (for future resale planning).

Stamp duty deadlines are strict

BSD and ABSD attract late-payment penalties from day 15 onwards:

1% per month of unpaid duty, pro-rated.

Maximum penalty: 4 × duty amount or S$25,000, whichever is lower.

In practice, the conveyancing lawyer coordinates stamp duty payment within 14 days because buyers almost never have the cash outlay ready on Day 1. This is the single most common source of late-fee surprises.

Stage 4 — Conveyancing (Day 14–56)

Between exercise and completion, the conveyancing team executes a full transaction checklist. The major items:

Conveyancing Checklist (resale private condo)

Day

Action

Responsible

Day 1–3

Lodge caveat, confirm option exercise, notify bank

Buyer’s lawyer

Day 1–7

Full title search, confirm no encumbrances, verify registered proprietor

Buyer’s lawyer

Day 7–10

BSD + ABSD paid, acknowledgements received

Buyer / lawyer

Day 14–28

Bank letter of offer finalised; loan documentation signed

CPF drawdown (if using CPF), cashier’s order prepared for balance

Buyer / lawyer

Day 56–70

Physical inspection, final meter readings, MCST transfer of records

Buyer / seller

Day 70–84

Completion: balance paid, title transferred, keys handed over

Both lawyers

Stage 5 — Stamp duties, explained

Buyer’s Stamp Duty (BSD)

BSD is payable on every purchase — residential or commercial. The progressive rates (as at April 2026) for residential are:

First S$180,000 — 1%

Next S$180,000 — 2%

Next S$640,000 — 3%

Next S$500,000 — 4%

Next S$1,500,000 — 5%

Amounts above S$3,000,000 — 6%

Additional Buyer’s Stamp Duty (ABSD)

ABSD is payable on top of BSD and depends on your citizenship and your order of residential property ownership. For a full rate table, see the ABSD Singapore 2026 guide. Key rates:

SSD applies if you sell within 3 years of purchase: 12% (Year 1), 8% (Year 2), 4% (Year 3). From Year 4 onward, SSD is zero. Factor SSD into any short-hold investment thesis.

New-launch timeline is different: Progressive Payment Scheme

For an uncompleted new-launch condo bought directly from a developer, the buyer does not pay 100% upfront. Instead, payment is staggered through the Progressive Payment Scheme (PPS), matching the construction milestones. A typical schedule:

Stamp duties are still payable in full within 14 days of S&P signing, not progressively. This is a common cash-flow shock for first-time new-launch buyers.

Worked example — resale purchase, first-property Singapore citizen

The single most expensive mistake. If the bank declines, you either pay the exercise fee plus the balance in cash or forfeit the option.

2. Missing the 14-day stamp duty window

Late stamp duty triggers a 4× penalty cap. Calendar the due date from the moment you exercise.

3. Treating ABSD refund as a discount

Married SC couples buying a second residential property can apply for ABSD refund if the first property is sold within the statutory window. That refund is not automatic — applications must be filed with IRAS within 6 months of selling the first property.

4. Forgetting the MCST requisition

Outstanding MCST fees, pending special assessments and upcoming major works are all liabilities that pass with title. Always ask the lawyer to raise specific requisitions on the MCST — “outstanding contributions” alone is too narrow a question.

5. CPF drawdown timing

CPF refunds to the seller’s CPF accounts must settle before completion. If the seller’s CPF balance is below the refund required, they top up in cash. A buyer who waits too long to instruct the lawyer on CPF usage can delay completion.

6. Not verifying title before exercising

Run the full title search before exercising, not after. A pending caveat or unreleased mortgage is a show-stopper that should stop the transaction at Day 1, not Day 45.

7. Forgetting the 3-year SSD window

Not a completion-day issue, but a common regret: buyers who flip within 3 years pay SSD of 4–12% on the selling price. Model this into any exit plan.

Special cases

Sub-sale transactions

A sub-sale is a transaction where a buyer who has signed an S&P with a developer sells their rights to a third party before TOP. The original buyer is the “sub-seller”. The sub-sale attracts SSD if within 3 years of the original purchase date. Conveyancing is more complex because both the original S&P and the sub-sale agreement must be reviewed.

Joint buyers (siblings, parents + children, business partners)

For joint buyers, each party’s ABSD is assessed individually. If one joint buyer already owns a property, the ABSD for the purchase is computed at the highest applicable rate across all joint buyers — not the average.

Decoupling to avoid ABSD

Decoupling — one spouse buying the other’s share to allow the seller spouse to buy a second property without ABSD — was substantially tightened by post-2021 cooling measures. Not all decouplings are now effective to avoid ABSD; consult a tax-aware conveyancing lawyer before relying on the structure.

Frequently Asked Questions

Can I extend the 14-day option period? Only by mutual agreement, usually via a fresh re-issue. It is not a statutory right.

What if my loan is declined after exercising? You must complete the purchase with cash or forfeit your 5% deposit. Always secure IPA before exercising.

Can I change my mind after signing the OTP? Before exercise, yes — you lose only the 1% Option Fee. After exercise, you are contractually bound.

Who pays for repairs discovered during inspection? Generally the seller for any defects existing before completion, subject to the S&P representations. Minor wear and tear is usually the buyer’s risk.

Can I use CPF for the Option Fee? No. The 1% Option Fee must be paid in cash.

How long does a new-launch S&P negotiation take? Typically 3 weeks from the Option to signing the S&P. Developers will not negotiate price in writing during this window, but rebate structures can be adjusted.

Does the lawyer represent the bank too? Yes — the buyer’s conveyancing lawyer is typically appointed by the bank for the mortgage. Their first duty is to the bank on the mortgage, but they owe the buyer duties on the purchase.

What happens if the seller dies before completion? Completion is delayed while the estate is administered. The S&P generally binds the estate; the buyer can either wait or — in limited cases — terminate.

Can I buy without a lawyer? Technically yes, practically no. Bank-required mortgages and complex stamp duty calculations make DIY conveyancing a genuine risk.

Do I pay stamp duty on the rebate or on the gross price? Stamp duty is on the net purchase price after any rebate credited on completion. For rebates paid post-completion, the treatment depends on whether IRAS treats the rebate as forming part of the consideration.

Key takeaway — discipline the calendar, not just the price

Key takeaway

Buyers who write down the OTP, exercise, stamp-duty, and completion dates at the point of signing the OTP have materially fewer problems than those who leave it to the lawyer. Get the IPA before signing, exercise on time, stamp within 14 days, and diarise the SSD window. The transaction then becomes a legal formality rather than a crisis.

Source: Singapore conveyancing practice and IRAS stamp duty rates as at April 2026.

Disclaimer: This article is for general informational purposes only and is not legal or financial advice. Every property transaction is unique. Engage a qualified conveyancing lawyer before committing to a purchase.

First-timer couples can now receive up to S$80,000 EHG (Enhanced Housing Grant) for new BTO flats, staggered by monthly household income.

Resale buyers can stack CPF Housing Grant + EHG (Resale) + Proximity Housing Grant — combined ceiling of up to S$230,000 for eligible first-timer couples buying a 4-room resale flat near parents.

Singles get about half of every family-level grant, subject to the same income ceilings.

Income ceilings: S$9,000/mth (family, new flat), S$14,000/mth (family, resale), S$7,000/mth (singles).

All grants are paid as CPF credit, not cash — they reduce your CPF-OA usage, not your cash outlay.

EC buyers: Family Grant only, up to S$30,000 (cap is markedly lower than HDB flats).

CPF Housing Grant Stack — 2026 — LovelyHomes editorial infographic, 22 April 2026.

Why CPF housing grants matter more than most buyers realise

Singapore’s CPF housing grant framework is easily the most generous public-housing subsidy programme in Southeast Asia — yet a meaningful share of eligible buyers under-claim or mis-stack the grants they qualify for. The reasons are structural rather than careless: the policy evolves frequently, the grants interact in non-obvious ways, and the income ceilings use different bases for different grants. This guide walks through every current (April 2026) grant, who qualifies, how they stack, and what the worked numbers look like across three typical buyer profiles.

We will cover ten grants across the three buyer tracks (new flat / resale / EC) plus the Proximity Housing Grant and Step-Up scheme, with a full worked example at the end. Keep in mind that while numbers in this guide reflect the position as at April 2026, HDB and CPF Board periodically revise ceilings and quantums — always verify against the official HDB and CPF portals before making a commitment.

Your first decision: new flat, resale or EC

Your route through Singapore’s grant system depends entirely on which flat you buy. Each track has a different grant menu:

Three buyer tracks — grant availability at a glance

Track

Grants You Can Use

Total Ceiling (approx.)

New BTO flat (HDB)

EHG (New)

Up to S$80,000

Resale HDB flat

CPF Housing Grant + EHG (Resale) + Proximity Housing Grant (+ Step-Up)

Up to S$230,000

Executive Condominium

Family Grant only

Up to S$30,000

Track 1 — New BTO / Sale of Balance Flats: the Enhanced Housing Grant

What it is

The Enhanced Housing Grant (EHG) replaced the older Additional CPF Housing Grant and Special CPF Housing Grant in 2019. For a new BTO flat, EHG is the only cash subsidy available from HDB directly — there is no “Family Grant” on a new BTO flat because the BTO price is already below-market.

Who qualifies (as at April 2026)

First-timer family or first-timer single applying with a fiancé or fiancée or co-applicant.

Average monthly household income ≤ S$9,000.

At least one applicant must have been in continuous employment for 12 months at the point of flat application.

How much you get

EHG is staggered in S$5,000 tranches by household income, so buyers at the lowest income tiers get the most support:

EHG (New) — Couples (April 2026)

Monthly household income (S$)

EHG quantum

≤ 1,500

S$80,000

1,501 – 2,000

S$75,000

2,001 – 2,500

S$70,000

2,501 – 3,000

S$65,000

3,001 – 3,500

S$60,000

3,501 – 4,000

S$55,000

4,001 – 4,500

S$50,000

4,501 – 5,000

S$45,000

5,001 – 5,500

S$40,000

5,501 – 6,000

S$35,000

6,001 – 6,500

S$30,000

6,501 – 7,000

S$25,000

7,001 – 7,500

S$20,000

7,501 – 8,000

S$15,000

8,001 – 8,500

S$10,000

8,501 – 9,000

S$5,000

Singles applying alone receive half of every couple-level quantum (i.e., from S$2,500 to S$40,000), subject to the same household-income ceiling applied on a single-person basis. Source: HDB, EHG tables as at April 2026.

Track 2 — Resale HDB: stacking CPF Housing Grant, EHG Resale and Proximity Housing Grant

Resale is where the grant architecture rewards careful planning. A first-timer couple who buys a 4-room resale flat within 4 km of the parents’ address can stack the three main resale grants for a combined subsidy up to S$230,000 — a scale that moves the affordability equation meaningfully.

CPF Housing Grant (Family)

First-timer couples: S$80,000 (4-room or smaller) or S$50,000 (5-room or larger).

Fiancé / fiancée schemes: same as couples.

Singles Scheme: S$40,000 (4-room or smaller) or S$25,000 (5-room).

Income ceiling: S$14,000/mth household; S$7,000/mth single.

EHG (Resale)

Same staggered table as EHG (New) — up to S$80,000 for the lowest income bracket, tapering to S$5,000 at the S$9,000/mth household level. Singles receive half-quantum.

Proximity Housing Grant (PHG)

Introduced to keep extended-family networks intact:

Buying a resale flat to live with parents: S$30,000.

Buying a resale flat near parents (within 4 km): S$20,000.

Singles buying a flat to live with parents: S$15,000.

Singles buying a flat near parents (within 4 km): S$10,000.

PHG is a one-off grant; it is not affected by your income ceiling, only by the proximity test.

Maximum grant stack — first-timer couple buying 4-room resale near parents

CPF Housing Grant (4-room, couple)

S$80,000

EHG Resale (couple, income ≤ S$1,500)

S$80,000

Proximity Housing Grant (within 4 km)

S$20,000

Subsidy (before Step-Up)

S$180,000

If co-living with parents (+ S$10,000 proximity differential)

S$30,000

Theoretical maximum stack

S$190,000–S$230,000

The S$230,000 figure includes overlay scenarios with Step-Up and edge-case upgrades; most buyers practically see S$180–S$190k.

Track 3 — Executive Condominium: Family Grant only

First-timer couples earning ≤ S$12,000 / mth qualify for up to S$30,000 (S$10,000 tranches below S$10,000 / S$11,000 / S$12,000 household income).

Lower income tiers: S$10,000 grant (S$11,001–12,000), S$20,000 (S$10,001–11,000), S$30,000 (≤ S$10,000).

Second-timer couples receive no grant on ECs.

ECs are sold at full developer pricing; the grant offsets only the down-payment burden, not the headline price.

Worked example — 30-year-old couple buying a resale 4-room in Tampines

The same couple, earning instead S$9,500 / mth, would forfeit EHG (above the S$9,000 ceiling) and receive only S$100,000 total — still substantial, but half their income ceiling relative to the example above. This is why households at the S$8,501–S$9,000 tier often find it worthwhile to time their application around temporary income dips.

Common pitfalls buyers learn the hard way

1. EHG is assessed on continuous 12-month income, not the most recent payslip

If one spouse switched jobs 8 months ago, the income assessment goes back through both the old and new employment. Bonuses are averaged over the prior 12 months. Buyers who try to time applications around temporary bonuses often land in a higher EHG tier than intended.

2. The 5-year Minimum Occupation Period resets if you sell

Receiving a grant obliges you to occupy the flat for a minimum period before resale (5 years for subsidised flats). Selling earlier requires HDB approval and may trigger a partial grant clawback. Plan the 5-year window into any career or life-change strategy.

3. Proximity resets when the parents move

If you purchased on the “within 4 km” test but parents subsequently move further than 4 km, the PHG is not clawed back — but you cannot recover PHG on a subsequent purchase.

4. Second-timer couples have a different, lower grant menu

If either spouse has previously taken a housing grant, your couple is assessed as “second-timer” and lower quantum ceilings apply across the board — ranging from 50% to 100% reductions depending on the grant.

5. Grants are paid to CPF, not as cash

This is a common misunderstanding. The S$80,000 EHG does not land in your bank account — it credits the successful applicant’s CPF-OA and reduces the CPF amount you need to draw down for the flat payment. Useful for the eventual sale (because the grant is “refundable” to CPF with interest when you sell), but it does not relieve cash-flow pressure on the down-payment cheque.

The Step-Up CPF Housing Grant

Second-timer families upgrading from a 2-room Flexi flat to a 3-room flat (or 3-room to 4-room) in designated non-mature estates receive an additional S$15,000 Step-Up CPF Housing Grant. The intent is to smooth upgrading friction for smaller low-income households.

Grant timeline — when do you actually get the money

Application: Declare grant eligibility when you apply for the flat.

Assessment: HDB assesses against household income (average 12 months) and eligibility conditions.

Confirmation: Grant is pre-approved and appears in your HDB Flat Eligibility letter.

Disbursement: Grant credits CPF-OA on completion — offsets the amount drawn from CPF for purchase.

Post-completion: Grant is “locked” to the flat (refundable to CPF with interest if you eventually sell).

Frequently Asked Questions

Can I use CPF housing grants for an EC? Yes, but only the Family Grant (up to S$30,000). EHG, Proximity Grant and Step-Up do not apply to ECs.

Do singles get the same grants as couples? No. Singles generally receive half the couple-level quantum under the Singles Scheme, subject to a tighter income ceiling.

Does the grant reduce the loan amount, the down payment, or both? It reduces the CPF amount you need to draw for the flat. Your loan amount is determined by the after-grant purchase price and your LTV ratio, so in practice it reduces both the loan principal and the CPF contribution.

What if my income rises above the ceiling between application and completion? HDB uses the income at the point of flat application — subsequent changes do not affect the grant.

Is the grant clawed back if I divorce? Not automatically; it depends on whether the flat is retained, sold or transferred, and on HDB’s approval of the retention request. Complex cases should be reviewed with a qualified conveyancing lawyer.

Can foreigners or PRs claim CPF housing grants? No — CPF housing grants are only available to Singapore citizens. PRs cannot access EHG, CPF Housing Grant or PHG.

Does a grant affect my ABSD? Grants do not affect ABSD rates directly, but they reduce the CPF / cash burden of the transaction. The ABSD rates are calculated on the purchase price, which is before grant disbursement.

Can I take a grant and still buy a private property later? Yes. Many upgraders use grants to buy their first HDB, live through the Minimum Occupation Period, then sell and buy private. The grant amount is refunded to CPF with accrued interest at sale.

Do I lose the grant if I let HDB rent the flat while I am overseas? If you rent the flat as allowed under HDB’s rental rules after the MOP, the grant is not affected. Renting the whole flat before MOP typically is not allowed; check HDB rules.

Where can I find the official grant calculator? HDB’s official e-service “Flat Eligibility (HFE) letter” is the authoritative tool. Verify your eligibility and grant quantum there before committing to any flat.

Key takeaway — a S$230,000 grant stack exists for a reason

Key takeaway

CPF housing grants are a deliberately structured subsidy for first-timer families who buy near parents. If you are in that demographic, under-claiming the stack is the single most expensive mistake in first-time Singapore home-buying. Spend the evening working through the HFE letter, match your household to the right track, and — if timing permits — consider whether your current payslip situation puts you in the most favourable EHG tier before you lodge the flat application.

Source: HDB EHG and CPF Housing Grant quantum tables as at April 2026.

Disclaimer: This article is for general informational purposes only and is not financial or legal advice. Grant quantum, eligibility conditions and income ceilings are set by HDB and CPF Board and may be revised without notice. Always verify your specific entitlements via the HDB HFE letter before relying on any grant calculation.