HFE letter deadline: Submit all supporting documents to HDB by 15 September 2026 to ensure your HDB Flat Eligibility (HFE) letter is ready for the October sales exercise.

Estimated 4-room prices: Standard (Yishun/Tengah) ~S$360K–S$400K; Plus (Geylang) ~S$500K–S$540K; Prime (Bedok/Toa Payoh) ~S$500K–S$555K.

MOP: 5 years for Standard; 10 years for Plus and Prime classifications.

Subsidy clawback: Plus and Prime flats are subject to a subsidy clawback on resale, calculated as a percentage of the resale price or value.

Hottest picks: Toa Payoh Caldecott (only Prime project; next to Caldecott MRT interchange); Bedok Bayshore (waterfront precinct; near East Coast Park).

Overview: Singapore’s Final BTO Launch of 2026

The October 2026 Build-To-Order (BTO) exercise is the final sales launch of the year and one of the largest in recent memory, with the Housing and Development Board (HDB) offering approximately 7,970 flats across seven projects in six towns. The October exercise completes the government’s 2026 BTO calendar, which has collectively offered around 19,600 new flats — matching HDB’s earlier public commitment to sustain high supply to moderate resale prices and address first-timer demand.

The exercise is notable for the geographic spread of its projects: it spans the sought-after east (Bedok’s new Bayshore waterfront precinct), the central region (Toa Payoh’s Caldecott precinct), an inner-city mixed area (Geylang’s Mattar neighbourhood near the Downtown Line), and the established growth corridors of Yishun and Tengah. For first-timer applicants who missed earlier launches, this is a high-stakes application exercise with a meaningful mix of price points and location quality.

Figure 1: All 7 projects in the HDB BTO October 2026 exercise — location, classification, flat types, unit count, nearest MRT station and indicative 4-room prices. Prices are pre-launch market estimates and will be confirmed only when HDB releases official pricing during the sales exercise.

Project-by-Project Analysis

Bedok — Bayshore I & II Prime

The two Bedok Bayshore projects together supply 2,500 flats (1,640 and 860 units respectively) in the new Bayshore housing estate along Bayshore Drive, adjacent to East Coast Park. Both are served by Bayshore MRT station on the Thomson-East Coast Line (TEL), which provides direct access to the CBD via Marina Bay. The Bayshore precinct is a purpose-built waterfront residential neighbourhood — the first HDB estate developed in this part of Singapore — and the BTO flats sit alongside private condominiums and commercial amenities in a mixed-use environment.

Both projects carry Prime classification under HDB’s 2023 flat classification framework, meaning buyers are subject to a ten-year Minimum Occupation Period (MOP) and a subsidy clawback on resale. Flat types span 2-room Flexi, 3-room, and 4-room, with no 5-room units offered — reflecting the Prime classification’s intent to maximise accessibility for first-timers rather than offer larger investment-grade units. Indicative 4-room pricing is estimated at approximately S$500,000–S$520,000.

Toa Payoh — Caldecott Prime

The Toa Payoh Caldecott project is expected to be the single most competitive project in October 2026. With 1,430 units — comprising around 590 two-room Flexi flats, 580 four-room flats, and a tranche of public rental units — it occupies land immediately adjacent to Caldecott MRT station, the interchange between the Circle Line (CCL) and the Downtown Line (DTL). This provides unparalleled MRT connectivity in a mature estate known for its proximity to Bishan, Ang Mo Kio, and Novena.

Caldecott is the only Pure Prime project in this exercise. Indicative 4-room prices are estimated to start from approximately S$550,000, reflecting the mature estate premium and the exceptional MRT interchange location. The ten-year MOP and subsidy clawback apply. Ballot competition is expected to be intense — the June 2026 Queenstown Prime project saw approximately 8× first-timer ballot rates for 4-room units, and Caldecott may approach similar demand.

Geylang — Mattar Plus

The Geylang Mattar project offers approximately 440 flats near Mattar MRT station on the Downtown Line (DTL3), within walking distance of MacPherson and the MacPherson estate. Geylang carries Plus classification — a ten-year MOP and subsidy clawback — reflecting its central location and good MRT connectivity without meeting the full Prime threshold. Flat types are expected to be 2-room Flexi and 4-room, with indicative 4-room pricing around S$500,000–S$540,000. The Geylang Mattar neighbourhood is undergoing gradual upgrading, and the BTO project sits in an area with established hawker centres, schools, and neighbourhood commercial facilities.

Yishun — Chencharu Standard

The Yishun Chencharu project is the largest single project in the October 2026 exercise at 1,580 units. Flat types run the full range — 390 two-room Flexi, 80 three-room, 460 four-room, and 650 five-room units — making it the most options-rich project for buyers seeking larger flat types at Standard pricing. Chencharu is the fifth BTO project launched in this new Yishun sub-precinct, which HDB is systematically building out on the former Chencharu estate lands near Khatib MRT station. Standard classification means a five-year MOP and no subsidy clawback. Indicative 4-room prices are estimated around S$360,000–S$400,000 — among the most affordable in this exercise.

Tengah — Garden Avenue Standard

Tengah Garden Avenue continues the ongoing build-out of Tengah New Town, the first car-lite eco-town in Singapore’s western corridor. The project is expected to offer approximately 620 units with 3-room, 4-room, and 5-room flat types. Tengah’s future MRT stations on the Jurong Regional Line (JRL) are under construction; the nearest current public transport option is bus connectivity to Bukit Gombak and Bukit Batok MRT stations. Standard classification applies; indicative 4-room prices are approximately S$360,000–S$380,000. Tengah’s car-free town centre design and green corridors are a lifestyle draw for buyers who prioritise environment over MRT proximity.

Sembawang — North Standard

The Sembawang North project adds approximately 400 units in the northern growth corridor, near Canberra MRT on the North-South Line. Flat types are expected to include 2-room Flexi, 3-room, 4-room, and 5-room options. Standard classification; indicative 4-room prices around S$320,000–S$360,000 — the most affordable in this exercise. Sembawang has seen a consistent stream of BTO launches in recent years as HDB continues to develop the Sembawang New Town precinct. The area is served by Canberra Plaza (opened 2020), Sembawang Shopping Centre, and a growing number of amenities. Bus connectivity is the primary mode of access to the town centre from the BTO site.

Figure 2: Left — Indicative 4-room BTO prices by town and classification. Right — Unit count by project. Prime projects (Bedok, Toa Payoh) are expected to command the highest ballot rates. Prices are indicative pre-launch estimates; actual prices will be confirmed by HDB at launch.

BTO Flat Classification — Standard, Plus and Prime in October 2026

The October 2026 exercise marks the third full year under HDB’s revised flat classification framework (Standard / Plus / Prime), which replaced the former Open Market / Prime Location Housing (PLH) and Mature / Non-Mature estate designations. The classification is determined by HDB based on locational advantage, transport connectivity, and proximity to the city centre:

Feature

Standard

Plus

Prime

MOP

5 years

10 years

10 years

Subsidy clawback on resale

None

Yes (% of resale price)

Yes (higher % of resale price)

Private property ownership during MOP

Not allowed

Not allowed

Not allowed

Eligible buyers

Usual HDB eligibility

Only first-timers (for 95% of units at launch)

Only first-timers (for 95% of units at launch)

Rental during MOP

With HDB approval after 3 yrs (rooms only)

Not allowed during MOP

Not allowed during MOP

October 2026 projects

Yishun, Tengah, Sembawang

Geylang Mattar

Bedok Bayshore, Toa Payoh Caldecott

A critical implication of Plus and Prime classification is the subsidy clawback: when you resell a Plus or Prime flat after the ten-year MOP, HDB recovers a percentage of the gross resale price. This amount is not refunded to you — it is recovered by HDB as a repayment of the additional subsidy embedded in the below-market launch price. For buyers who plan to sell their flat after MOP to unlock equity, the subsidy clawback meaningfully reduces net sale proceeds.

Grants — What First-Timers Can Receive in October 2026

First-timer Singapore Citizen households applying for BTO flats may be eligible for the following CPF housing grants:

Grant

Maximum Amount

Eligibility

Income Ceiling

Enhanced CPF Housing Grant (EHG)

S$80,000 (couple); S$40,000 (single)

First-timer SC couple or single; buying new or resale HDB

S$9,000/mth (couple); S$4,500/mth (single)

CPF Housing Grant — BTO

S$40,000 (SC couple); S$20,000 (single)

First-timer buying directly from HDB (BTO, SBF)

S$14,000/mth

Step-Up CPF Housing Grant

S$25,000

Second-timer moving from 2-room to larger BTO in non-mature/Standard estate

S$7,000/mth

Proximity Housing Grant (Resale only)

S$30,000 (couple); S$20,000 (single)

Buying resale HDB within 4km of parents; does not apply to BTO

Not applicable for BTO

For a qualifying SC first-timer couple with household income below S$9,000 per month, the maximum combined BTO grant (EHG + CPF Housing Grant) is S$120,000. This means a Yishun Standard 4-room BTO estimated at S$380,000 could effectively cost as little as S$260,000 after grants — making it among the most subsidised home-ownership options available in 2026.

Figure 3: Maximum CPF housing grant amounts by buyer profile and grant type for the October 2026 BTO exercise. SC couples (both first-timers) are eligible for the highest total grant quantum of up to S$120,000 for BTO. Grants are means-tested against average household income over the 12 months preceding application.

How to Apply — Key Steps and Dates

The October 2026 BTO application process follows the standard HDB BTO application procedure:

1. Obtain a valid HDB Flat Eligibility (HFE) Letter. An HFE letter confirms your eligibility to buy an HDB flat, the loan amount you qualify for, and the grants you may receive. HFE letters are valid for six months. HDB recommends applying for the HFE letter early — submit all required documents by 15 September 2026 to ensure your letter is processed before the October application window opens. Apply via the HDB Flat Portal at homes.hdb.gov.sg.

2. Select your project and flat type. When the October 2026 sales exercise opens (HDB will announce the exact application window), log into the HDB Flat Portal, browse available projects, and submit your application for one project and flat type.

3. Ballot and queue number. HDB conducts a computer ballot. First-timer SC applicants receive priority balloting status (two ballot chances before being deemed a second-timer). Your queue number determines the order in which you book a flat. A lower queue number (closer to 1) means you have first pick of available units within your shortlisted flat type.

4. Flat selection and signing of Agreement for Lease (AFL). When called for flat selection, you choose a specific unit, pay the option fee (typically S$2,000), and subsequently sign the Agreement for Lease and pay the down payment (5% of flat price from cash/CPF, plus stamp duty).

5. Keys collection. BTO construction timelines typically run 3–5 years. For most projects in non-mature towns (Yishun, Tengah, Sembawang), expected completion is 2029–2031. For Prime projects in mature areas, timelines may be shorter given higher development priority, though HDB has not yet released official completion estimates for the October 2026 projects.

Worked Example: The Wong Family Apply for Yishun Chencharu 4-Room

Scenario

Mr and Mrs Wong, both Singapore Citizens aged 28, are first-time home buyers. Combined gross monthly income: S$7,500/mth. Both are applying for the Yishun Chencharu 4-room BTO in October 2026.

Grant eligibility:

EHG (S$7,500/mth income → proportionate to income): approximately S$50,000

CPF Housing Grant (BTO, SC couple): S$40,000

Total grants: S$90,000

Estimated 4-room flat price: S$380,000

Effective price after grants: S$380,000 − S$90,000 = S$290,000

HDB Loan (90% LTV on post-grant price, subject to MSR):

Maximum HDB loan: 80% of flat price = S$304,000 (before grants reduce the price quantum; HDB loan is on flat price, grants reduce initial outlay)

Monthly instalment at HDB loan rate 2.6% p.a., 25 years on ~S$290,000: approximately S$1,320/mth

MSR check: S$1,320 / S$7,500 = 17.6% — well within the 30% MSR cap — PASS

Cash outlay at sign of AFL: approximately S$3,200 (option fee S$2,000 + legal S$1,200)

Estimated waiting time: approximately 3.5–4 years; expected keys collection 2030–2031.

For this couple, the Yishun BTO is an exceptionally affordable path to home ownership — the effective post-grant cost of S$290,000 for a new 4-room flat in a growth precinct compares favourably to current HDB resale 4-room prices in Yishun (~S$420,000–S$490,000).

What Might Come Next — BTO Supply and Policy Outlook

The October 2026 exercise completes the government’s publicly stated 19,600-flat target for 2026. For 2027, HDB is expected to announce the BTO supply target in January — industry observers anticipate a maintained high supply of 18,000–22,000 units given continued strong first-timer demand. The government has signalled that BTO supply will remain elevated until the HFE application-to-first-timer-receipt wait time is consistently below four years for most non-Prime projects.

The longer-term supply story for October 2026 buyers is positive: Bedok Bayshore (TEL fully operational 2025), Toa Payoh Caldecott (Caldecott interchange operational), and Yishun Chencharu (fifth project in a maturing precinct) will all benefit from continued infrastructure investment and precinct maturation during the waiting period. Tengah buyers face a longer MRT wait — the Jurong Regional Line stations serving Tengah are not expected to open until 2028–2029 — but the car-free town centre design and cycling-focused layout are increasingly valued by younger buyers.

Summary: October 2026 BTO At-a-Glance

Town

Project

Class

Units

MOP

Est. 4-Room

MRT

Bedok

Bayshore I

Prime

1,640

10 yrs

~S$510K

Bayshore (TEL)

Bedok

Bayshore II

Prime

860

10 yrs

~S$510K

Bayshore (TEL)

Toa Payoh

Caldecott

Prime

1,430

10 yrs

~S$555K

Caldecott (CCL+DTL)

Geylang

Mattar

Plus

~440

10 yrs

~S$520K

Mattar (DTL)

Yishun

Chencharu

Standard

1,580

5 yrs

~S$380K

Near Khatib (NSL)

Tengah

Garden Avenue

Standard

~620

5 yrs

~S$370K

Future JRL

Sembawang

North

Standard

~400

5 yrs

~S$340K

Canberra (NSL)

Total

~7,970

HFE deadline: 15 September 2026

Frequently Asked Questions

What is the difference between Prime, Plus and Standard BTO flats in October 2026?

The classification reflects the locational advantage of each project and determines the restrictions placed on the flat. Prime flats (Bedok Bayshore, Toa Payoh Caldecott) carry a ten-year MOP, a subsidy clawback on resale, and a restriction on renting out the whole flat or any room during the MOP period. Plus flats (Geylang Mattar) have the same ten-year MOP and clawback, but the subsidy is calibrated as less than Prime. Standard flats (Yishun, Tengah, Sembawang) have a five-year MOP and no subsidy clawback — they behave like traditional BTO flats and can be resold on the open market at prevailing prices after the MOP. If you are buying primarily as a home rather than as an investment, the classification matters mainly for your lifestyle flexibility during MOP. If you intend to sell after five to seven years, Standard is strongly preferable.

Can I apply if I currently own a private property?

No. HDB BTO eligibility requires that you do not own a private residential property (in Singapore or overseas) at the time of application, and that you have not disposed of any private property within 30 months before the HDB flat application date. If you or your co-applicant own or recently sold a private property, you are ineligible to apply for a BTO flat. This 30-month wait-out period also applies if your private property is held through a company or other entities where you hold a significant interest. Check your eligibility carefully via the HDB Flat Eligibility portal before submitting an application.

What happens if my ballot number is beyond the available units — can I try again for free?

Yes. If you applied as a first-timer and your ballot number is beyond the available units (or you did not receive any ballot chance), you are considered to have made an unsuccessful attempt. Your first-timer priority status is not used up by simply not receiving a queue number low enough to select a flat. You retain your first-timer priority ballot chips for future exercises. However, if you receive a queue number and are called for flat selection but decline to select a flat, you lose one ballot chip and may be deemed a non-first-timer for subsequent exercises. HDB provides two priority ballot attempts for first-timer SC households before reclassifying them as second-timers.

Can Singapore Permanent Residents (SPRs) apply for October 2026 BTO flats?

SPRs cannot apply for BTO flats as the sole applicant or as two SPR co-applicants. However, a SPR can co-apply as a joint applicant with a Singapore Citizen spouse or family member under the Public Scheme or Fiance/Fiancee Scheme. In that case, the SC-SPR household is eligible to apply for Standard and Plus classification BTO flats but may not apply for Prime classification flats (which are restricted to SC households only at launch). The SC-SPR household also qualifies for a reduced set of CPF grants — for example, the CPF Housing Grant for BTO is capped at S$20,000 (rather than S$40,000 for SC-SC couples), and EHG applies at the SC first-timer level for the SC co-applicant only.

How is the EHG (Enhanced CPF Housing Grant) calculated — is it always S$80,000?

The EHG is means-tested. The maximum of S$80,000 (for SC couples) is only available to households with an average gross monthly income of S$1,500 or less. As income rises, the EHG tapers down in steps. At S$4,500/mth the EHG for a couple is approximately S$50,000; at S$6,000/mth it is approximately S$30,000; at S$9,000/mth (the income ceiling) it is S$5,000. Income is assessed as the average gross monthly household income over the 12 months preceding the flat application, including variable components such as overtime, commissions, and bonuses. Check the official HDB EHG calculator at hdb.gov.sg for your specific income band.

Can I buy a BTO flat on a single income if I am not applying as a single?

Yes, but your borrowing capacity and grant eligibility are assessed on the household’s combined income. If you are applying as a couple (Public Scheme or Fiance/Fiancee Scheme) but only one person is currently working, HDB assesses your income ceiling based on the working person’s income alone for grant purposes, but the MSR (Mortgage Servicing Ratio) of 30% is applied to the working person’s gross monthly income for loan affordability. At an income of S$4,000/mth, MSR 30% allows a monthly HDB loan repayment of up to S$1,200, which at 2.6% over 25 years supports a loan of approximately S$268,000. Combined with grants, this can comfortably support a 4-room BTO in a Standard estate like Yishun or Tengah.

Is there a priority ballot for applicants near the project location?

Yes, under certain conditions. HDB provides a Married Child Priority Scheme (MCPS) for applicants whose parents live in the same town or within 4km of the BTO project. MCPS allocates a portion of units (typically 30% for those in the same town, 15% for within 4km) to eligible applicants before the general ballot. This priority scheme is separate from the EHG and does not require an income ceiling. To qualify, both the applicant household and the parents’ household must be Singapore Citizens, and the parents must be registered at an HDB address in the applicable town or within 4km of the BTO site. There is no corresponding scheme for applicants working near the project — only family proximity qualifies.

Disclaimer: This article is for general informational and educational purposes only. Flat prices shown are indicative pre-launch estimates compiled from publicly available market commentary and are not official HDB figures. Actual flat prices, flat types, unit counts and specific project details will be confirmed only when HDB officially launches the October 2026 sales exercise. Grant eligibility and amounts are subject to HDB’s assessment of your specific household circumstances. Always verify eligibility, pricing, and grant quantum directly with HDB at hdb.gov.sg or homes.hdb.gov.sg before making any decision. This article does not constitute financial, legal, or housing advice.

Minimum occupation period: 5 years for HDB flats before you can sell on the open market; no MOP for private property.

Seller’s Stamp Duty (SSD): 12% / 8% / 4% / NIL for private property sold within Year 1 / 2 / 3 / 4+ of purchase. HDB flats are exempt from SSD.

Agent commission: typically 1–2% of sale price for the seller’s agent; 0% for the buyer’s agent (paid by buyer).

CPF refund: every dollar of CPF used (plus 2.5% p.a. accrued interest) must be returned to CPF at completion — this reduces your cash proceeds.

OTP process: Seller grants a 14-day Option to Purchase; buyer pays 1% option fee; upon exercise buyer pays another 4–9%.

Completion timeline: typically 10–16 weeks from OTP grant to key handover; HDB resale takes 8–16 weeks.

Net proceeds formula: Sale Price − Outstanding Loan − CPF Refund (principal + accrued interest) − SSD − Agent Fee − Legal Fees = Cash in Hand.

Valuation: Banks and HDB commission independent valuations; if you sell above valuation on an HDB flat the buyer must pay the difference (“Cash Over Valuation”) in cash.

What Does It Mean to Sell Property in Singapore?

Selling a property in Singapore is a structured, legally regulated process administered by the Urban Redevelopment Authority (URA), the Housing and Development Board (HDB), the Inland Revenue Authority of Singapore (IRAS), and the Central Provident Fund Board (CPF). Whether you are selling a Housing and Development Board flat or a private condominium, the transaction follows a defined sequence — Option to Purchase, valuation, loan redemption, stamp duty, CPF refund, legal completion — and each step carries financial consequences that sellers must understand before listing.

In 2026, Singapore’s resale property market is active but more deliberate than the pandemic-era surge. HDB resale transaction volumes have moderated, private resale prices have risen a measured 2–3% year-on-year, and the government’s Seller’s Stamp Duty framework remains in full force. This guide explains the complete selling process from the first decision to sell to the final cash deposit — and equips you to compute your actual net proceeds before you sign anything.

Figure 1: The 8-step property selling timeline in Singapore — from engaging an agent to receiving your keys-handover proceeds. Most HDB resales complete in 10–14 weeks; private resales in 12–16 weeks.

Step 1: Deciding to Sell — Eligibility and Timing

Before listing your property, confirm that you are legally entitled to sell. For HDB flat owners, the critical gate is the Minimum Occupation Period (MOP), which is five years from the date of key collection for most flats. Prime and Plus-classification flats (under the 2023 HDB flat classification framework) carry a ten-year MOP. During the MOP, you may not sell on the open market, rent out the entire flat, or purchase a private residential property in Singapore. Selling before the MOP ends is a serious breach of HDB regulations and can result in compulsory acquisition of the flat.

For private residential properties — condominiums, landed houses, executive condominiums after the five-year privatisation period — there is no MOP. However, the Seller’s Stamp Duty framework imposes a financial penalty for selling within three years of purchase, which effectively discourages short-term flipping.

Once eligibility is confirmed, consider the market context. Check URA’s Private Residential Property Price Index (PPI) and HDB’s Resale Price Index (RPI) for trend data. In Q1 2026, the URA PPI rose 0.9% quarter-on-quarter (+2.63% year-on-year) while the HDB RPI dipped a marginal 0.1% — the first dip since Q2 2019, though volume remains high. Timing your sale to a period of stable or rising prices, and avoiding major political or economic events, is prudent.

Step 2: Valuation — Setting the Right Price

Property valuation in Singapore has two purposes: establishing a credible asking price and satisfying bank loan requirements for the buyer. For HDB flats, HDB commissions valuations through its panel of approved valuers. For private property, banks engage their own valuers (from their panel of approved valuation firms) as a condition of the mortgage loan offer.

As a seller, you may commission your own valuation — at approximately S$300–S$700 depending on property type — to anchor your asking price. This is not compulsory but is advisable for unique properties (high-floor penthouses, large freehold units, unusual configurations) where comparable transaction data is sparse.

For HDB resale, if your agreed transacted price exceeds the HDB-commissioned valuation, the difference — known as Cash Over Valuation (COV) — must be paid entirely in cash by the buyer. COV is non-fundable from CPF or HDB loan proceeds. In the current market, COV for popular estates (Queenstown, Bishan, Buona Vista) can reach S$30,000–S$80,000, while non-mature towns typically transact at or below valuation. As a seller, setting an aspirational price above valuation is legitimate but risks a longer time-on-market.

Step 3: Engaging an Agent — What You Pay and What You Get

Under the Council for Estate Agencies (CEA) guidelines, property agents must be licensed and registered. CEA introduced major reforms in 2024 requiring co-broking arrangements to be disclosed and prohibiting dual representation without written consent from both parties. As a seller, you typically engage one agent (the “seller’s agent”) and pay that agent a commission of 1–2% of the transaction price, negotiated upfront in a written agreement.

The buyer’s agent commission is typically paid by the buyer, though in practice some co-broking arrangements share the seller’s commission. Always confirm in writing who pays what before signing any engagement letter.

Figure 2: Left — Net proceeds breakdown for a typical HDB 4-room (S$850K sale) and an OCR condo 3-bedroom (S$1.8M sale), both held more than three years. Right — Typical agent commission rates by sale price band in 2026.

Step 4: Marketing and the Option to Purchase

Once you have signed an exclusive agreement with your agent (usually for 3 months, though non-exclusive arrangements are permissible), your property will be listed on PropertyGuru, 99.co, and SRX. ViewThat, Carousell Property, and direct developer channels are secondary platforms.

When a buyer makes an offer you wish to accept, the transaction proceeds via an Option to Purchase (OTP). The OTP is a standardised legal document — HDB provides its own form; private property uses the CEA-prescribed format or a solicitor-drafted version. Key OTP terms:

OTP Term

HDB Resale

Private Resale

Option fee (on grant)

S$1 (symbolic) to S$5,000 max

1% of agreed price

Option exercise period

21 calendar days

14 calendar days (customary)

Exercise fee (on exercise)

S$5,000 − option fee (HDB loan) or up to 9% (bank loan)

4% of agreed price

OTP validity

21 days, non-extendable

14 days; extendable by agreement

If buyer does not exercise

Option fee forfeited to seller

Option fee forfeited to seller

Administering body

HDB Resale Portal

Law Society / solicitors

Once the buyer exercises the OTP, the transaction is binding. Both parties must engage solicitors to proceed to legal completion.

Step 5: Seller’s Stamp Duty — Know Your Exit Cost

The Seller’s Stamp Duty (SSD), administered by IRAS, applies to private residential property sold within three years of acquisition. It is calculated on the higher of the sale price or market value:

Holding Period

SSD Rate

Example: S$1.5M Sale Price

Year 1 (within 12 months)

12%

S$180,000

Year 2 (12–24 months)

8%

S$120,000

Year 3 (24–36 months)

4%

S$60,000

Year 4 and beyond

NIL

S$0

SSD does not apply to HDB flats. For private property sellers, SSD must be paid within 14 days of the option exercise date. It cannot be funded from CPF and is payable in cash. Failing to pay SSD on time incurs a penalty of up to four times the duty owed.

Exemptions exist for inherited property (where the holding period restarts from the date of inheritance), court-ordered sale, and transfers pursuant to divorce proceedings. Check IRAS’s e-Stamping portal for the precise holding period calculation — the clock starts from the date of OTP exercise, not the date of completion.

Step 6: CPF Refund — The Cost That Surprises Most Sellers

If you used CPF Ordinary Account (OA) savings to fund your property purchase — whether for the down payment, monthly mortgage instalments, or BSD — you are required by the CPF Act to return the full amount withdrawn, plus accrued interest at the CPF OA rate of 2.5% per annum compounded annually. This refund is deducted from your sale proceeds at completion and credited back to your CPF OA. It does not go to you in cash.

The accrued interest calculation compounds monthly over the period you held the property. On a S$300,000 CPF withdrawal held for ten years, accrued interest amounts to approximately S$83,000 — meaning S$383,000 is refunded to CPF, not the original S$300,000. Many sellers underestimate this figure and are surprised to find their cash proceeds are far lower than expected.

CPF Board’s online CPF Property Withdrawal Statement is the authoritative source for your specific CPF amount to be refunded. Request this before accepting an offer so you can compute net proceeds accurately.

Figure 3: Left — CPF accrued interest compounding on S$300K used over different holding periods at 2.5% p.a. Right — How SSD reduces (or eliminates) the net gain on a S$1.5M property bought for S$1.35M (S$150K gross gain), depending on when you sell.

Step 7: Computing Your Net Proceeds

Your actual cash payout at completion is not your sale price. The correct formula is:

Item

Example: HDB 4-Room S$850K Sale

Example: Condo OCR 3BR S$1.8M Sale

Sale Price

S$850,000

S$1,800,000

Less: Outstanding HDB/Bank Loan

−S$0 (paid off)

−S$560,000

Less: CPF Refund (principal + accrued)

−S$420,000

−S$630,000

Less: Agent Commission (1%)

−S$8,500

−S$18,000

Less: Legal Fees (seller’s solicitor)

−S$3,000

−S$5,500

Less: Seller’s Stamp Duty (if applicable)

NIL (HDB exempt)

NIL (held >3 yrs)

Net Cash Proceeds

S$418,500

S$586,500

Note that the CPF refund goes back into your CPF OA, not your bank account. If you plan to use CPF again for your next property purchase, this is neutral — but if you need cash liquidity (for retirement or other purposes), plan around this constraint.

Worked Example: The Lim Family Sell Their Tampines 5-Room HDB

Scenario

Mr and Mrs Lim, both Singapore Citizens in their early 50s, purchased their Tampines 5-room HDB flat in July 2019 for S$530,000. They took an HDB loan of S$477,000 at 2.6% per annum over 25 years. They have made regular monthly CPF contributions to service the mortgage. They are now upgrading to an OCR condominium and wish to sell the flat in July 2026 (exactly 7 years’ hold, MOP fully satisfied).

Sale agreed: S$785,000 (a COV of approximately S$18,000 above the HDB-commissioned valuation of S$767,000)

Outstanding HDB loan at completion: approximately S$362,000 (after 7 years of repayments)

CPF OA used (principal withdrawn): S$148,600

CPF accrued interest @ 2.5% over 7 years: approximately S$27,400

Total CPF refund to CPF OA: S$176,000

Agent commission (1%): S$7,850

Seller’s legal fees: S$2,800

SSD: NIL (HDB exempt)

Net cash proceeds: S$785,000 − S$362,000 − S$176,000 − S$7,850 − S$2,800 = S$236,350 cash in hand

Additionally, S$176,000 is credited to their CPF OA — available for the next property purchase.

Total equity released: S$236,350 cash + S$176,000 CPF = S$412,350 — significantly less than the S$785,000 sale price, illustrating why understanding the net proceeds formula is essential before committing to an upgrade.

What This Means for You: Key Considerations Before Selling

Singapore’s property market has historically rewarded patient long-term ownership. The government’s SSD framework, CPF accrued interest rules, and agent commission structure all work in the same direction: discouraging short-term transactions and encouraging owners to hold property for meaningful periods. Before deciding to sell, ask yourself:

Have you satisfied MOP? (HDB sellers only — non-negotiable)

Is SSD payable? (Private sellers within 3 years of purchase — calculate the cost against your expected gain)

What is your actual CPF refund? (Get the exact figure from CPF Board before accepting any offer)

Do you have a replacement housing plan? (If selling HDB and upgrading to private, the 15-month wait-out period applies if you buy first)

Is the market timing favourable? (Track URA PPI and HDB RPI quarterly; selling in a rising quarter often justifies a short delay)

What Might Come Next: Singapore Property Market and Seller Policy Outlook

As at mid-2026, there are no credible signals of an SSD rate change or new seller-specific cooling measures. The government has consistently stated that the existing ABSD-SSD-TDSR framework is sufficient to manage speculative demand. The more likely policy development affecting sellers is the ongoing refinement of the HDB flat classification system (Standard / Plus / Prime), which introduces a subsidy clawback on resale if the flat is sold within the enhanced MOP.

For the second half of 2026, the primary variable affecting seller proceeds is interest rate direction. If the US Federal Reserve continues its easing cycle (as widely anticipated), Singapore mortgage rates — priced off SORA — should trend modestly lower, improving buyer affordability and potentially supporting seller-side pricing power in Q3 and Q4 2026. The URA Q2 2026 Flash Estimates, expected in the first week of July 2026, will provide the next definitive data point on private residential price momentum.

Summary: Seller’s At-a-Glance Table

Item

HDB Flat

Private Property

Minimum Occupation Period

5 years (standard); 10 years (Plus/Prime)

None

Seller’s Stamp Duty

Exempt

12% / 8% / 4% / NIL (Yrs 1–4+)

Agent commission (seller pays)

1–2% negotiable

1–2% negotiable

Legal fees (seller)

~S$2,500–S$4,000

~S$3,500–S$8,000

CPF accrued interest

2.5% p.a. compounded on all CPF used

2.5% p.a. compounded on all CPF used

OTP option period

21 days

14 days (customary)

Completion timeline

8–14 weeks from OTP exercise

10–16 weeks

Key regulator

HDB (flat) + IRAS (stamp duty) + CPF Board

URA + IRAS + CPF Board

Administering portal

HDB Resale Portal

SLA e-lodgement + IRAS e-Stamping

Frequently Asked Questions

Can I sell my HDB flat if I still have an outstanding HDB loan?

Yes. At completion, your solicitors will arrange for the outstanding HDB loan to be repaid from your sale proceeds. HDB provides a “Loan Balance Statement” that gives the exact redemption figure as at the completion date. You do not need to clear the loan before listing — the redemption is handled at the point of legal completion. However, if the outstanding loan and CPF refund together exceed your sale price, you may have a “negative sale” — meaning you would owe money at completion. This is rare but possible if you purchased at a high price and have not held long enough for equity to build. Always compute your net proceeds before committing.

What happens if I sell my property at a loss — do I still pay CPF accrued interest?

Yes, with an important exception. If your sale proceeds are insufficient to cover the full CPF refund (principal + accrued interest), CPF Board will only recover what is available from the proceeds. The shortfall is waived — you are not personally liable to make up the difference from other savings. However, if you took a bank loan and the bank’s outstanding loan is redeemed first (which is typical), the CPF amount recovered may be further reduced. This scenario arises in cases of significant negative equity, usually only following a sharp market correction or after a very short holding period with SSD also payable. For most long-term sellers, selling at a nominal loss after holding for many years is uncommon in the Singapore market, but not impossible in specialised segments like commercial shophouses or declining lease leasehold properties.

Do I need a lawyer to sell my property in Singapore?

Yes. Unlike some jurisdictions where private sales without solicitors are possible, Singapore requires conveyancing solicitors for all property transactions. As a seller, you must engage a Singapore-qualified solicitor (or a law firm with a licensed conveyancing practice) to handle the title transfer, prepare the completion documents, redeem your outstanding mortgage, arrange the CPF refund, and liaise with the buyer’s solicitors. Solicitor fees for a seller typically range from S$2,500 to S$8,000 depending on property type, transaction complexity, and whether a mortgage is involved. Always obtain a fee quote from at least two firms before engaging. The Law Society of Singapore maintains a directory of licensed conveyancing lawyers at lawsociety.org.sg.

What is the 15-month wait-out period and how does it affect HDB sellers who want to buy private?

The 15-month wait-out period, introduced in September 2022, requires that Singapore Citizens and Permanent Residents who own an HDB flat — or who have sold an HDB flat — must wait 15 months from the date of the HDB flat sale before purchasing a private residential property. The measure was designed to prevent HDB sellers from immediately using sale proceeds to compete in the private market, which was driving up private prices. If you sell your HDB flat in July 2026, you cannot exercise an OTP for a private property until October 2027 at the earliest. Note that the wait-out period applies from the date of HDB sale completion, not the date of OTP grant. Buying under a spouse’s name alone does not avoid the restriction if the spouse also owns or has owned an HDB flat. Check with your solicitor for any exemptions applicable to your specific circumstances (e.g., purchase of a completed private property where the OTP was granted before the HDB sale was completed, subject to specific conditions).

Can I grant an OTP while my flat is still within the MOP?

No. HDB does not allow you to grant an OTP, list on the open market, or accept any purchase deposit while the MOP is still running. Any such agreement would be void and could expose both buyer and seller to HDB enforcement action. For HDB resale, the HDB Resale Portal is the official platform for registering the OTP — it will reject submissions where the MOP has not been satisfied. The MOP clock starts from the date of flat purchase (key collection), not from the date of legal completion. For PLH (Prime Location Public Housing) and Plus flats launched from 2023 onwards, the enhanced MOP is ten years.

What is Cash Over Valuation (COV) and is it normal to pay it?

COV is the amount by which the agreed transaction price of an HDB resale flat exceeds HDB’s commissioned valuation. It must be paid entirely in cash by the buyer — it cannot be funded from CPF or HDB loan proceeds. COV is legal and common in desirable estates (mature towns, near MRT, high floors) but can range from zero to over S$100,000 depending on market conditions and unit specifics. As a seller, setting a price that implies COV is your right, but it narrows your buyer pool to those with sufficient cash reserves. In 2026, COV is present in popular estates but has moderated from the elevated levels seen during the 2021–2023 market peak. HDB publishes quarterly resale transaction data which allows you to benchmark transacted prices by block and floor range before setting your asking price.

When is the best time of year to sell property in Singapore?

Historically, the Singapore property market sees higher transaction volumes in Q2 (April–June) and Q3 (July–September), with Q4 (October–December) being softer as the year-end holiday period approaches and buyers delay decisions. The Chinese New Year period (January–February) is typically the quietest. However, market-wide price trends matter far more than seasonal patterns — selling in a rising market at any time of year will generally yield better proceeds than selling in a falling market during the “peak” season. If you have flexibility, tracking URA PPI and HDB RPI quarterly and listing when momentum is positive is more impactful than calendar timing. In 2026, the private market is in a modest uptrend with URA PPI at +0.9% QoQ in Q1; the Q2 flash estimates (expected July 2026) will indicate whether momentum is sustained.

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or tax advice. Property transactions in Singapore are subject to specific rules and regulations that may have changed since publication. Always verify stamp duty rates, CPF rules, and HDB eligibility with the official authorities: IRAS (iras.gov.sg), CPF Board (cpf.gov.sg), HDB (hdb.gov.sg), and URA (ura.gov.sg). Engage a licensed solicitor and, where appropriate, a licensed financial adviser before making any property transaction decisions. Agency commission rates and transaction costs used in this article are indicative only and may vary.

The Progressive Payment Scheme (PPS) is the default payment structure for new-launch private residential property in Singapore. Under the scheme, you pay a small deposit on booking, incremental tranches as construction reaches each milestone, and the final balance only when the keys are handed over at TOP. This 2026 guide walks through each stage, the CPF and cash flow at every milestone, and the practical cash-flow implications for a typical Singapore buyer.

Quick Answer

The Progressive Payment Scheme spreads purchase payments across seven construction milestones, from OTP booking to CSC (final 12-month defect period).

On launch day you pay 5% in cash (the Option fee). Within 8 weeks you pay a further 15% on Sale & Purchase signing — of which up to 5% may be from your CPF Ordinary Account.

The remaining 80% is drawn progressively from your home loan as construction reaches foundation, walls, ceiling/roof, TOP and CSC.

Monthly mortgage payments begin after the first drawdown — not on the day you sign the OTP.

PPS is the default for new-launch condominiums. The Deferred Payment Scheme (DPS), where available, pushes the bulk of payments to TOP but typically carries a price premium and stricter eligibility.

What is the Progressive Payment Scheme?

The Progressive Payment Scheme is the payment structure prescribed by the Urban Redevelopment Authority for property sold in the primary market under the Housing Developers (Control and Licensing) Act. Under PPS, the purchase price is paid in incremental tranches timed to construction milestones, rather than in a single lump sum at handover. The structure exists for two reasons: it reduces the buyer’s financing burden during the 3–4 year build period, and it gives the developer progressive cash-flow to fund construction without requiring 100% escrow.

PPS applies to all uncompleted private residential property purchased directly from the developer. For completed-and-TOP-issued stock sold in the primary market, the payment structure is different — typically the full balance is due within 12 weeks of OTP.

The seven PPS milestones

Stage 1 — Option to Purchase (5% in cash)

On launch day, you pay a 5% Option fee to the developer in cash or cashier’s order. This secures your right to purchase the specific unit for a 3-week Option period. During this window, you finalise financing, commission a conveyancing lawyer and decide whether to proceed. If you do not exercise the Option, you forfeit 1.25% of the Option fee (one-quarter of the 5%) and the developer returns the balance 3.75%.

Stage 2 — Sale & Purchase Agreement (15% within 8 weeks)

Within 8 weeks of Option exercise, you sign the Sale & Purchase Agreement and pay a further 15% of the purchase price. A typical split is 5% in additional cash and 10% from CPF Ordinary Account, though this varies by buyer. At this stage, you also pay Buyer’s Stamp Duty and, if applicable, Additional Buyer’s Stamp Duty to IRAS — due within 14 days of S&P signing.

Stage 3 to 5 — Construction-linked draws (45% total)

Once construction reaches each milestone, the developer issues a payment notice. Your home-loan bank draws down against your loan facility to pay the developer directly. Monthly mortgage instalments begin on the bank side after the first drawdown. The three construction-linked milestones are: foundation complete (10%); reinforced concrete framework, carpark and partition walls complete (10%); ceiling, roof and external wall complete with windows installed (25%). Typical elapsed time between Stage 2 and Stage 5 is 24–30 months for a mid-size project.

Stage 6 — TOP and key handover (25%)

When the Temporary Occupation Permit is issued, the developer notifies the buyer. You pay the next 25% tranche and receive the keys. You can now occupy the unit, lease it out, or commission renovation work. The MCST (management corporation strata title) is also constituted at or shortly after this milestone, and your monthly maintenance-fee obligation begins.

Stage 7 — Certificate of Statutory Completion (10%, within 12 months)

The final 10% is held back and released when the Certificate of Statutory Completion is issued — typically within 12 months of TOP. CSC confirms that all building works conform to the approved plans and that the defects-liability period has been honoured. This hold-back is the buyer’s main leverage during the first-year defects period, and you should work through your defects snag list methodically before authorising the final tranche.

How the CPF + cash + loan split actually works

The payment split varies by buyer, but a common structure for a Singapore Citizen first-time buyer is:

The 5%/15% split at the front of the scheme is not legally fixed — it is the default under URA rules. A buyer with additional CPF headroom may redirect more of Stage 2 from cash to CPF. A buyer with limited CPF but strong cash flow may pay Stage 2 entirely in cash. Your conveyancing lawyer will confirm the precise split on your S&P, and your bank’s mortgage specialist will coordinate the CPF withdrawal application.

Worked example — S$2,000,000 purchase

Consider a Singapore Citizen first-time buyer purchasing a S$2 million new-launch condominium under PPS. Total BSD is S$64,600, ABSD is nil on a first property.

BSD (paid in 14 days): S$ 64,600 (from cash or CPF)

Upfront total (weeks 0-8):

Cash required: S$ 200,000 – 264,600

CPF required: S$ 200,000 – 264,600

Stages 3-7 (24-48 months):

80% loan drawdown: S$1,600,000 (monthly instalment from first drawdown)

Approx. monthly mortgage at 3.5% / 30 yrs on S$1.6M:

Full-loan equivalent: S$ 7,184 per month

Starts: After Stage 3 first drawdown, scales as loan balance grows

Note two things. First, the BSD payment at Stage 2 is often overlooked in cash-flow planning. A S$2 million purchase carries approximately S$64,600 of BSD due within 14 days of S&P — a buyer who has budgeted only the 5% cash at OTP is likely to be caught short. Second, the monthly mortgage payment ramps up over the construction period: from roughly S$900 per month after Stage 3 (10% of loan drawn) to the full S$7,184 once all drawdowns are complete at TOP.

How monthly mortgage payments scale across milestones

This ramp is the single most important cash-flow feature of PPS. A buyer who qualifies on the full-loan TDSR check still has a much lighter monthly burden in the first 18–24 months of construction, which can be useful for offsetting stamp duty and renovation savings.

PPS vs Deferred Payment Scheme (DPS)

For completed inventory of some developments — particularly foreign-developer-owned assets and late-cycle unsold stock — developers sometimes offer a Deferred Payment Scheme as an alternative. Under DPS, the buyer pays 20% at OTP and S&P combined, defers the remaining 80% to TOP (or up to 3 years later for completed units), and takes no home-loan drawdowns during the deferral period.

DPS improves short-term cash flow at the cost of a slightly higher purchase price. For a buyer expecting a large cash event (bonus, asset sale, parental gift) at TOP, DPS can make sense. For a buyer with steady cash flow through the construction period, PPS is materially cheaper on a total-cost basis.

Common pitfalls to avoid

Pitfall 1 — Budgeting only the 5% at OTP

The 5% OTP is not the upfront cost. You need 20% plus BSD/ABSD in the first 8 weeks. Add renovation, agent, legal and moving costs and you are looking at 22–25% of purchase price in the first 12 weeks, not 5%.

Pitfall 2 — Forgetting BSD is due 14 days after S&P

BSD is not paid at TOP. It is due within 14 days of S&P signing. On a S$2M purchase that is S$64,600 — budgeted separately from the 20% downpayment.

Pitfall 3 — Mixing up loan disbursement schedule with own cash flow

The bank draws your loan on the developer’s notice — you do not pay the developer directly. But the bank’s monthly instalment on the drawn loan balance comes out of your account from the first drawdown.

Pitfall 4 — Releasing the CSC tranche before defects are fixed

The final 10% is your main leverage during the 12-month defects-liability period. Work through the snag list methodically and only authorise CSC release when outstanding defects are resolved or formally noted.

The PPS stamp-duty timing gotcha

Buyer’s Stamp Duty and Additional Buyer’s Stamp Duty are payable within 14 days of the dutiable instrument. For a new-launch PPS purchase, the dutiable instrument is the Sale & Purchase Agreement signed at Stage 2 — not the Option to Purchase signed at Stage 1. This timing nuance matters for three reasons.

First, you have a measurable planning window — roughly 10 weeks from launch day — to assemble the cash to pay both the Stage 2 downpayment and the stamp duty. Second, the ABSD exemption application window (for married couples claiming spousal ABSD remission, for example) opens at the S&P stage, not at OTP. Third, if the government announces a cooling-measure change between OTP and S&P, the stamp-duty rate that applies is the rate in force on the S&P date, not the OTP date. This has historically been a source of significant buyer anxiety during cooling-measure cycles.

Frequently asked questions

1. Do all new-launch private condominiums in Singapore follow PPS?

Yes. PPS is the default payment structure prescribed by URA for uncompleted private residential property sold in the primary market. Deferred Payment Scheme alternatives are available only for completed or late-cycle inventory at the developer’s discretion.

2. When does my monthly mortgage payment start?

Your monthly mortgage payment starts after the first loan drawdown — typically at Stage 3 (foundation complete), which is usually 6–12 months after S&P signing. Until the first drawdown, you pay no mortgage instalment.

3. Can I pay the whole purchase price upfront?

No. URA rules require the developer to collect payment against milestones under PPS, and a lump-sum upfront payment is not permitted on a new-launch uncompleted unit. You can, of course, make an agreed partial pre-payment on your home loan at any time once the loan has been drawn.

4. What happens if I cannot meet a progress-payment milestone?

Your loan facility covers the milestone drawdowns automatically — the bank pays the developer against your loan balance. The mortgage instalment comes out of your bank account monthly. A genuine default scenario would only arise if your monthly cash flow cannot service the mortgage instalment. Speak to your bank immediately if this looks likely; options typically include a short-term restructure or, in extreme cases, a resale exit.

5. Can I use CPF for the 5% OTP booking fee?

No. The 5% OTP must be paid in cash or cashier’s order. CPF can be used from Stage 2 onwards, subject to the Valuation Limit and Withdrawal Limit framework.

6. When is ABSD payable under PPS?

ABSD (and BSD) is payable within 14 days of signing the Sale & Purchase Agreement at Stage 2, not at OTP. Budget the stamp duty separately from the Stage 2 downpayment.

7. What is the Option fee forfeiture if I do not exercise the OTP?

One-quarter of the 5% Option fee — 1.25% of the purchase price — is forfeited to the developer. The remaining 3.75% is returned within a reasonable period. This is the standard URA-prescribed position and cannot be waived.

8. Does PPS apply to Executive Condominiums?

Yes. Executive Condominiums follow the same PPS milestones as private condominiums. The main EC-specific difference is eligibility and resale-restriction rules on the buyer side, not on the payment-schedule side.

9. Does PPS apply to HDB BTO flats?

No. HDB BTO flats follow a different payment schedule: 10% Option fee at booking (mostly from CPF), then the balance at key collection. Construction-linked progressive drawdowns do not apply to BTO.

10. How long does the full PPS cycle take?

Typically 3–4 years from OTP to CSC for a mid-size project: 2–3 months from OTP to S&P, then 24–36 months through construction to TOP, then a further 12 months to CSC.

11. Can I sell the unit before TOP?

Yes, subject to the standard resale rules for private property. You can sell the uncompleted unit to another buyer via a ‘sub-sale’ arrangement, with the original buyer’s obligations novated to the new buyer. The Seller’s Stamp Duty framework applies on the gain, and Additional Buyer’s Stamp Duty applies to the new buyer — both on the sub-sale price, not the original purchase price.

12. What happens if the developer delays TOP?

The Sale & Purchase Agreement specifies a contractual TOP deadline. If the developer misses it, liquidated damages are payable to the buyer per the S&P terms — typically a fraction of the purchase price per month of delay. Review your S&P clauses carefully; liquidated damages are not uniform across developers.

Disclaimer. This article is for general information only and does not constitute legal, financial or tax advice. Figures referenced reflect the position as at 23 April 2026 and are subject to change without notice. Always verify the latest rates and policies with the official authority — IRAS, HDB, URA, CPF or MAS — before making any property decision. Consult a qualified lawyer, mortgage broker or accountant for advice specific to your circumstances.

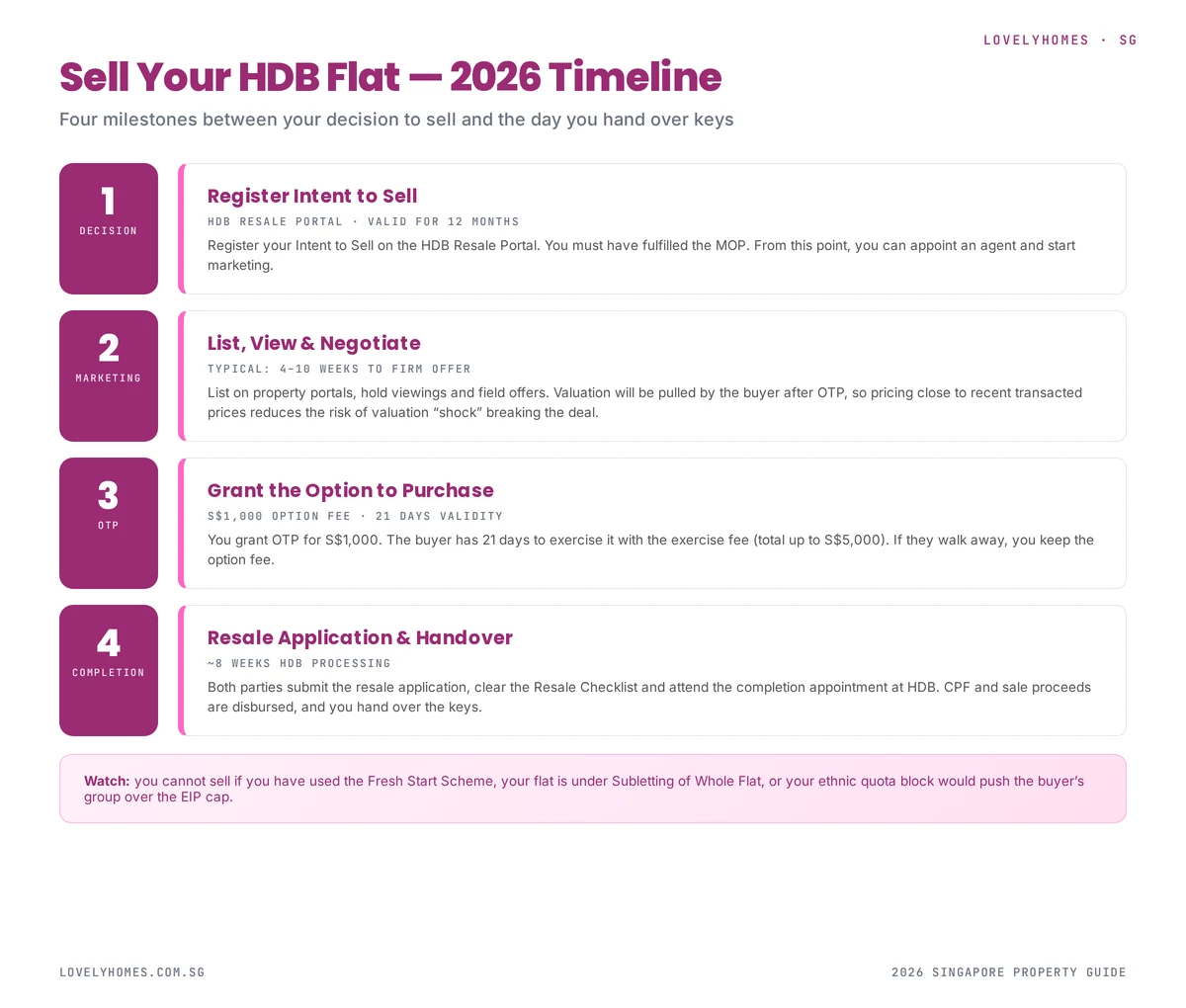

Selling your HDB flat in Singapore is a four-stage process — Intent to Sell, marketing and negotiation, OTP, and completion. Each stage has its own legal document, its own timing constraints, and its own price-breaking pitfalls. This 2026 guide walks through the full sequence from the seller’s side.

See HDB’s official selling page for the regulatory details. This guide explains the practical mechanics.

Quick Answer — Selling an HDB Flat

Check your MOP — 5 years from key collection for most flats.

Register Intent to Sell on the HDB Resale Portal.

List, view, negotiate — typically 4–10 weeks.

Grant the Option to Purchase (OTP) — S$1,000 option fee, 21-day validity.

Both parties submit the resale application — ~8 weeks HDB processing.

Completion appointment at HDB Hub — hand over keys.

Total: 3–4 months from listing to completion.

Four milestones between listing decision and handing over keys.

Step 1: Check Your MOP

You cannot sell an HDB flat until the Minimum Occupation Period (MOP) has been fulfilled. For most modern flats this is 5 years from key collection; for Plus and Prime flats it is 10 years. See our MOP guide for the exceptions and consequences of breach.

Time spent overseas for more than 6 months at a stretch does not count. If you have been posted abroad, verify with HDB that your effective MOP is what you think it is.

Step 2: Register Intent to Sell

Log into the HDB Resale Portal with Singpass and submit Intent to Sell. This is valid for 12 months. It:

Confirms your eligibility to sell (MOP, ethnic quota impact)

Allows you to appoint a licensed property agent

Triggers HDB’s valuation pipeline when an OTP is later granted

Gives buyers assurance that the flat is legitimately for sale

Step 3: Price, List and Negotiate

HDB resale is now in a tight market with COV back on the table. Price correctly:

Pricing benchmarks

Recent transacted prices on the HDB Resale Portal for the same block, type, and floor

Recent COV spread — has the estate been transacting above or below valuation?

Remaining lease — a shorter lease narrows the buyer pool considerably

Block-level ethnic quota — a block that is “closed” to major ethnic groups has a reduced buyer pool and attracts weaker offers

Agent vs no-agent

The HDB Resale Portal is designed to let sellers transact without an agent. However, a good agent will:

Run marketing on PropertyGuru, 99.co, and Facebook/IG for 2–4 weeks

Coordinate viewings (typically evenings and weekends)

Shepherd both parties through resale application submission

Typical seller-side commission in 2026 is 2% of the transacted price. See our agent commission guide.

Step 4: Grant the OTP

Once you and the buyer agree on a price, you grant the OTP. The option fee is fixed at S$1,000. The buyer then has 21 calendar days to exercise by paying the exercise fee (up to S$4,000 more, so total S$5,000 maximum). Key points:

If the buyer fails to exercise, you retain the S$1,000 option fee.

If the buyer does exercise, the sale becomes unconditional. You cannot then grant an OTP to another buyer.

Valuation is requested at this point — if it comes in below the agreed price, the buyer must pay the shortfall in cash (COV).

Step 5: Resale Application

Within 7 days of OTP exercise, both seller and buyer log into the HDB Resale Portal and jointly submit the resale application. You will:

Confirm the agreed price and terms

Select your conveyancing solicitor (HDB Legal or private)

Complete the Resale Checklist — a set of confirmations from both parties

Pay the administrative fee (S$80 for 1-2 room, S$120 for 3-room and above)

HDB then processes the application, targeted at 8 weeks. During this time, HDB will audit your ownership, verify the buyer’s eligibility, compute CPF refunds, and arrange the completion appointment.

Step 6: Completion Appointment

Typically 8–12 weeks after the resale application, you attend the completion appointment at HDB Hub. Both parties sign the transfer documents, CPF refund is credited to your Ordinary Account, the buyer’s loan is disbursed, and you hand over the keys.

What Happens to Your CPF and Sale Proceeds

The sale proceeds flow in this sequence:

Outstanding HDB or bank loan is repaid in full from the proceeds.

CPF refund — the principal you used from CPF, plus accrued interest, is refunded back into your CPF Ordinary Account. This can be substantial on a flat you have lived in for 10+ years.

Balance — what remains is your cash-in-hand from the sale.

If the flat has appreciated slowly or you used a large CPF component, the CPF refund may consume most of the proceeds, leaving little cash. This is the “negative sale” scenario and a real risk for short-lease resale.

Worked Example: Selling a S$680k 4-Room Flat

You bought the flat 9 years ago for S$420k, paid using S$100k CPF (principal) and a S$300k HDB loan, and have S$150k outstanding on the loan:

Item

Amount

Sale price

S$680,000

Less: outstanding HDB loan

(S$150,000)

Less: CPF refund (principal + 9yr accrued @ 2.5%)

(S$125,000)

Less: agent commission (2%)

(S$13,600)

Less: legal fees

(S$500)

Net cash in hand

S$390,900

CPF Ordinary Account now holds

S$125,000 more

Common Pitfalls

Accepting an offer before verifying buyer HFE status — if the buyer cannot get HFE, the deal collapses.

Ethnic quota surprise — HDB rejects the application because the sale would push the block over its EIP cap for the buyer’s ethnic group.

Valuation shortfall — the buyer walks away if the valuation is too low and they cannot fund the cash COV.

Underestimating CPF accrued interest — many sellers find far less cash in hand than expected.

Overestimating the flat — overpricing leads to extended listing periods and ultimately a lower final transacted price.

FAQ — Selling an HDB Flat 2026

Can I sell my flat before MOP is fulfilled?

Only under exceptional circumstances (divorce, death, financial hardship) and with HDB’s explicit approval. Otherwise, sale before MOP is not permitted.

How much cash will I actually get from the sale?

Sale price minus outstanding loan minus CPF refund minus agent commission minus legal fees. For most owners 5–10 years in, cash in hand is 40–60% of sale price.

Do I pay Seller Stamp Duty on an HDB resale?

Only if you have owned the flat for less than 3 years (very rare because of MOP). See our SSD guide.

Can I reject a buyer after accepting their OTP offer?

No. Once the OTP is granted and the buyer has paid the option fee, you are legally bound to sell to them if they exercise within 21 days.

What if the buyer’s HDB loan gets denied?

The buyer can walk away from the OTP, forfeiting the option fee (and exercise fee if already paid). You are then free to re-list and sell to another buyer.

Disclaimer: HDB processes, fees and scheme rules change over time. Verify the current rules with HDB before committing to sale. Consult your conveyancing lawyer for advice on your specific situation.

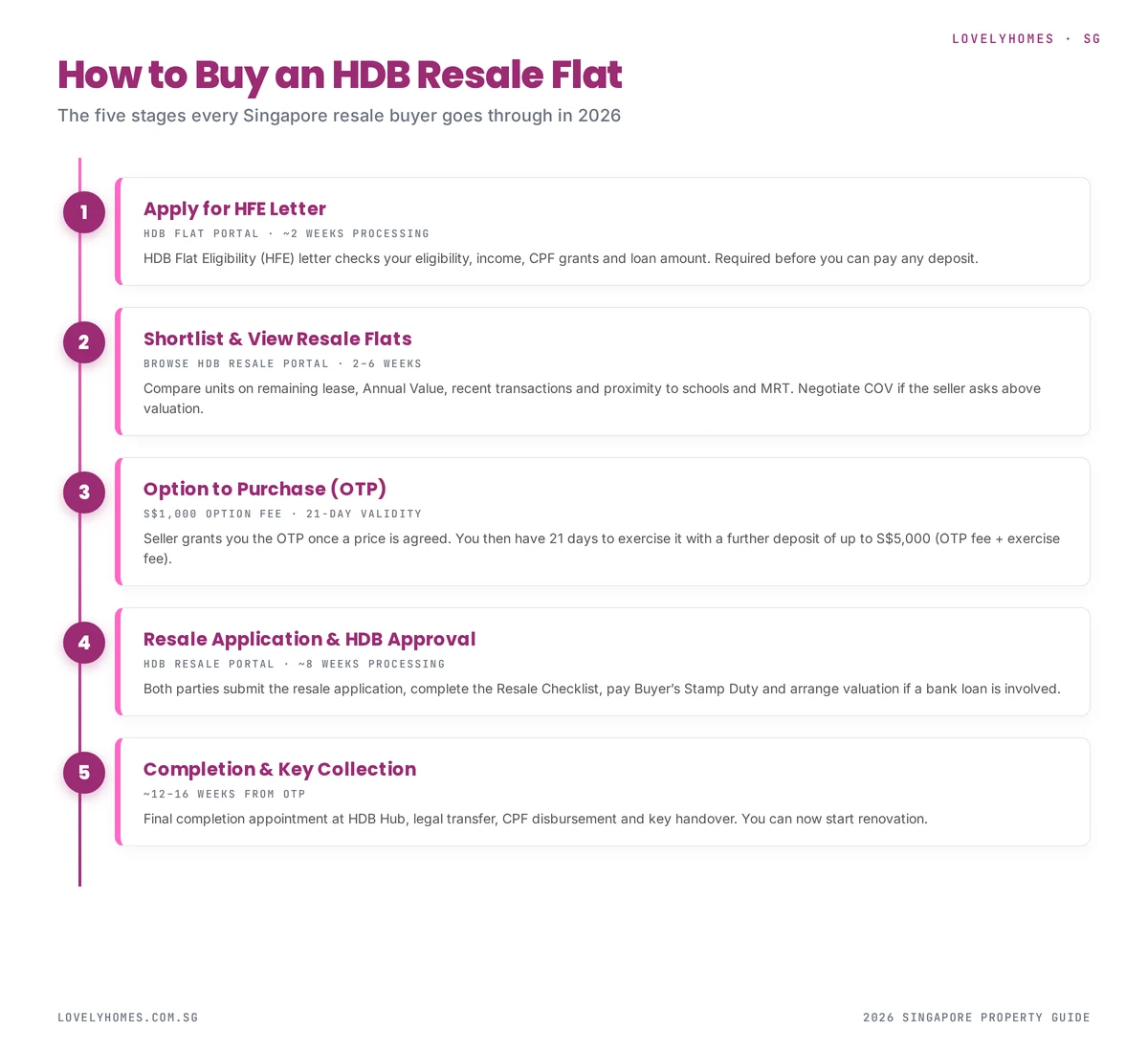

Buying an HDB resale flat in Singapore in 2026 is a process with clear, legally-defined stages. Miss one, and the deal either stalls or collapses entirely. This guide walks you through every step in the exact order you will actually encounter it — from securing your HDB Flat Eligibility (HFE) letter to collecting the keys.

For the official rules, refer to the HDB Resale Buying page. This article explains what those rules mean in practice and how the numbers add up for a typical 2026 buyer.

Quick Answer — The HDB Resale Buying Process

Apply for HFE letter on the HDB Flat Portal (~2 weeks processing).

Shortlist and view flats (typically 2–6 weeks).

Negotiate, then receive the OTP from the seller (S$1,000 option fee).

Exercise the OTP within 21 days with the exercise fee (up to S$4,000 more).

Submit the resale application on the HDB Resale Portal.

Complete the purchase at the HDB Hub appointment and collect keys.

Total elapsed time: typically 12–16 weeks from OTP to keys.

The five stages of buying an HDB resale flat, from HFE letter to keys.

Step 1: Apply for Your HFE Letter

The HDB Flat Eligibility (HFE) letter is the gating document for any HDB purchase. It confirms three things in a single statement: whether you are eligible to buy, how much CPF housing grant you qualify for, and the maximum HDB loan you can take.

You apply through the HDB Flat Portal using Singpass. The portal will check your household income, ages, citizenship, and existing property holdings. Processing usually takes around two weeks — but longer if HDB needs clarification on income or existing flat ownership.

The HFE letter is valid for six months, and you cannot exercise any OTP without one. Budget for your HFE to be ready before you start serious viewings — you will see sellers, and agents expect you to have it lined up.

What the HFE letter tells you

Whether your household meets the eligibility conditions (at least one SC, under the S$14,000 monthly household income ceiling, no overlapping private-property ownership).

The exact CPF Housing Grants you qualify for (CPF Housing Grant, Enhanced CPF Housing Grant, Proximity Housing Grant).

The maximum HDB Concessionary Loan you can take, based on TDSR and MSR.

The minimum cash required at OTP and exercise stages.

Step 2: Shortlist Flats and Conduct Viewings

Once you have your HFE letter in hand, you can begin serious viewings. The HDB Resale Portal and third-party sites (PropertyGuru, 99.co, ourselves at LovelyHomes) let you filter by town, flat type, remaining lease and recent transacted price.

What to actually evaluate at a viewing

Remaining lease: Directly affects your maximum loan tenure and CPF usage. Anything under 60 years of remaining lease starts restricting grants and CPF usage significantly.

Condition of the flat: Look past the paint. Check ceilings for water marks (upstairs leaks), windows for water ingress, and door frames for termite damage.

Ethnic quota status: Your ethnic group must be under the block-level EIP cap. Ask the agent if the block is “open” for your group.

Noise and dust: Traffic, MRT, and construction noise. Visit twice — once at peak hour, once in the evening.

Ownership history: The agent should be able to confirm the number of previous owners and whether any structural alterations were made without HDB approval.

Step 3: Negotiate the Price and Receive the OTP

Once you and the seller agree on a price, the seller grants you the Option to Purchase (OTP). The option fee is fixed by HDB at S$1,000, paid on the spot. This buys you the exclusive right to purchase that flat at the agreed price for 21 calendar days.

The OTP is a legally binding document for the seller during those 21 days — they cannot sell to anyone else. But you, the buyer, can walk away by simply not exercising the option. You forfeit the S$1,000 but have no further obligation.

Cash-Over-Valuation (COV) in 2026

If the agreed price exceeds HDB’s official valuation, the gap must be paid in cash — never from CPF or loan. This is Cash-Over-Valuation, and it is firmly back on the table in 2026’s tight resale market. Budget for it if you are bidding on a popular estate or a high-floor unit. See our full COV guide for negotiation tactics.

Step 4: Exercise the OTP

Within the 21-day window, you exercise the OTP by paying the exercise fee. The option fee plus exercise fee cannot exceed S$5,000 combined — typically structured as S$1,000 option + S$4,000 exercise. At this point the sale becomes unconditional.

In the same 21 days, you should:

Engage a conveyancing lawyer (HDB’s in-house Legal & Claims Registry is a low-cost option for straightforward cases).

If taking a bank loan, finalise your loan offer and submit it for valuation.

Prepare the Buyer’s Stamp Duty (BSD) — due within 14 days of OTP exercise.

Step 5: Submit the Resale Application

Once the OTP is exercised, both parties log into the HDB Resale Portal and submit the resale application jointly. The portal walks you through the Resale Checklist, financial plan, and any declarations.

You will pay stamp duty, agree on the completion timeline, and nominate your solicitor. Your CPF refund to the seller, the loan disbursement and the final cash shortfall are all calculated at this point. HDB aims to process the resale application within eight weeks.

Typical fees at application stage

Resale application fee: S$80 (1-room / 2-room flats) or S$120 (3-room and above).

Buyer Stamp Duty (BSD): Graduated — 1% on first S$180k, 2% on next S$180k, 3% on next S$640k, 4% thereafter. On a S$600k resale, BSD comes to S$12,600. See our BSD guide for the full maths.

Legal fees: S$350–S$600 via HDB Legal, S$1,800–S$3,000 via a private conveyancing firm.

Step 6: Completion and Key Collection

About twelve to sixteen weeks after you first exercised the OTP, you will attend the completion appointment at HDB Hub. Both parties sign the legal transfer documents, CPF disbursements are triggered, your bank or HDB loan is drawn down, and you receive the keys.

From this moment, the flat is legally yours. Your MOP clock starts ticking from this date — see our MOP guide for what that means going forward.

Worked Example: Buying a S$620,000 4-Room Resale Flat

Let’s walk through a realistic 2026 purchase. A young couple, both Singapore Citizens and first-time buyers, buy a 4-room resale flat in Sengkang at S$620,000 — S$30,000 above HDB’s valuation of S$590,000.

Component

Amount

Purchase price

S$620,000

HDB valuation

S$590,000

COV (cash)

S$30,000

HDB loan @ 75% of valuation

S$442,500

Cash + CPF downpayment (25% of valuation)

S$147,500

Buyer Stamp Duty

S$13,200

Legal fees (HDB route)

~S$500

Minimum cash needed upfront

~S$60,000

The couple might qualify for an Enhanced CPF Housing Grant of up to S$80,000 depending on their combined income, which offsets a large chunk of the downpayment. See our CPF for property guide for how the grants flow into the purchase.

Common Mistakes That Delay or Kill the Deal

No HFE letter in hand: You cannot exercise an OTP without one. Plan at least three weeks of buffer before you start offering.

Underestimating COV: It has to come from cash savings, not CPF. Many deals collapse at OTP because buyers find their cash short.

Ignoring the ethnic quota: Your offer can be accepted, only to have HDB reject the resale application because the block is full for your group.

Not checking structural alterations: Unauthorised renovations (load-bearing wall removal, unpermitted window grilles) are the buyer’s problem after completion.

Valuation shock: If the valuation comes in below the purchase price, the cash shortfall must be covered by you — not CPF.

FAQ — HDB Resale Buying 2026

How long does the entire HDB resale process take?

Typically 12–16 weeks from OTP exercise to keys. Add another 2–6 weeks for your flat search, and 2 weeks for the HFE letter.

Can I use CPF to pay the option fee?

No. The S$1,000 option fee and the up-to-S$4,000 exercise fee both come from cash. CPF Ordinary Account funds only flow in at the resale-application stage.

What happens if I cannot exercise the OTP in time?

You forfeit the S$1,000 option fee. The seller is then free to grant the OTP to someone else.

Do I need a property agent to buy HDB resale?

No. HDB’s Resale Portal is designed to let buyers and sellers complete the process without an agent, though you are welcome to use one. Total agent commission on the buyer side is typically 1% of the purchase price.

Can I back out after I exercise the OTP?

Only with the seller’s agreement, and you would likely forfeit both the option and exercise fees (up to S$5,000). HDB does not have a “cooling-off” period for resale buyers once OTP is exercised.

Disclaimer: This is general guidance, not legal advice. Rules, fees and grant amounts change periodically — always verify with HDB directly before committing. Consult a qualified conveyancing lawyer for your specific purchase.