Singapore Property MOP Guide 2026: HDB Minimum Occupation Period Rules Explained

Key Takeaways: Singapore MOP 2026

- HDB BTO, resale and DBSS flats: 5-year MOP from date of key collection — you cannot sell, sublet the entire flat, or acquire private residential property under HDB rules (though private purchase is allowed if ABSD is paid).

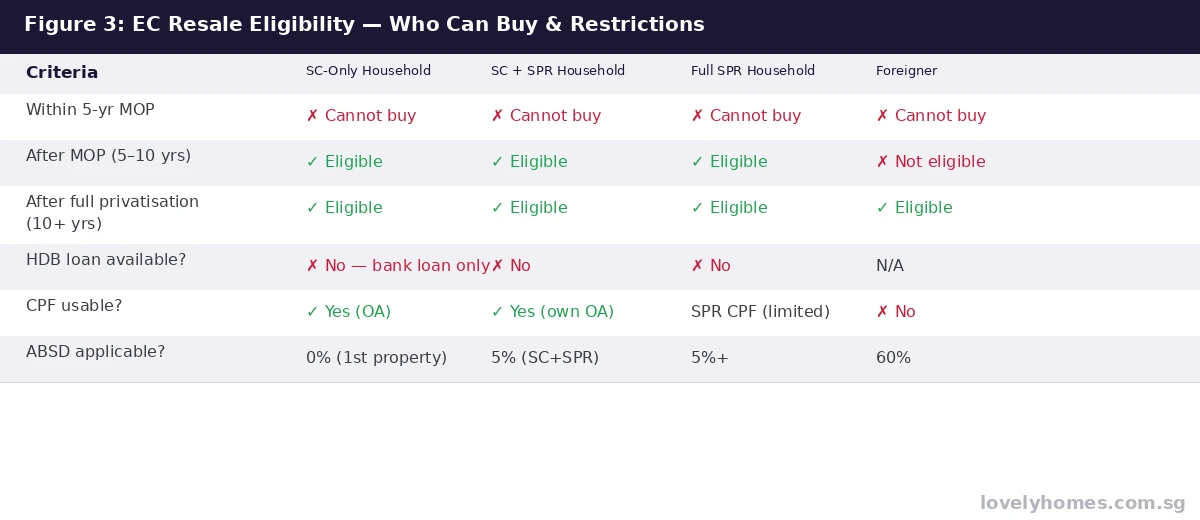

- Executive Condominiums (ECs): 5-year MOP measured from the date of Temporary Occupation Permit (TOP), not key collection. ECs count as HDB-equivalent for ABSD purposes during MOP.

- PLH (Prime Location Public Housing) flats: Extended 10-year MOP, subsidy clawback on resale, and cannot rent the whole flat to non-owner occupiers even after MOP.

- Private condominiums and landed property: No MOP at all — you may sell or sublet immediately after purchase.

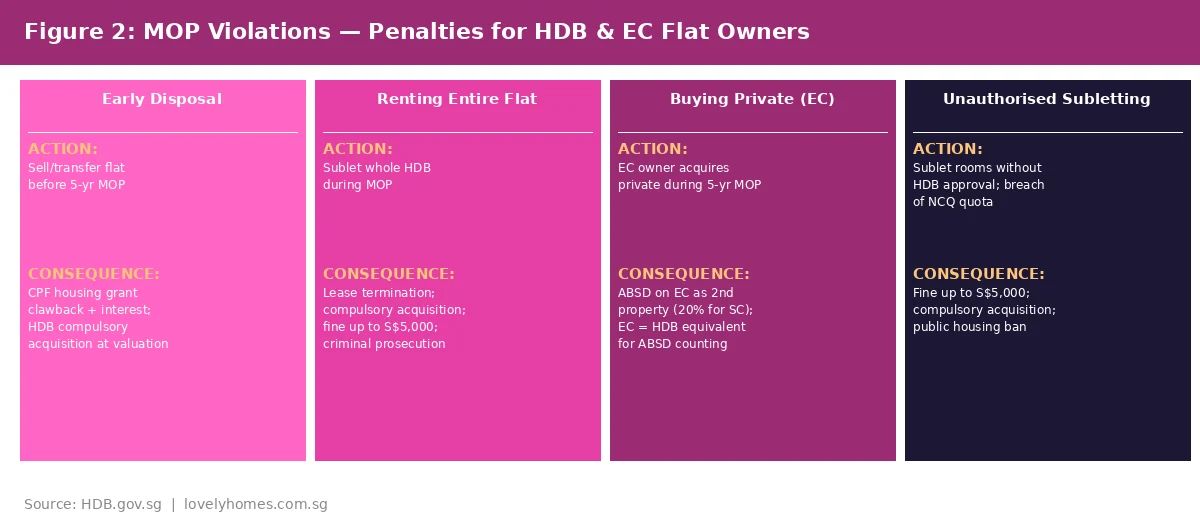

- Consequences of MOP breach: HDB may compulsorily acquire the flat; CPF housing grants are clawed back with accrued interest; fines up to S$5,000; potential criminal prosecution.

- EC privatisation: At year 10 from TOP, EC becomes fully privatised — foreigners may buy, no HDB restrictions remain.

- Wait-out period: Private residential property owners who sell must observe a 15-month wait-out period before buying a non-PLH HDB resale flat (as at June 2026).

What Is the Minimum Occupation Period (MOP)?

The Minimum Occupation Period is a restriction imposed by the Housing & Development Board (HDB) that requires flat owners to physically occupy their subsidised public housing for a set period before they are permitted to sell, sublet the entire flat, or — in certain cases — purchase additional private residential property. Administered under the Housing and Development Act (Cap. 129), the MOP exists to preserve the public housing system’s intent: subsidised flats are meant for Singaporeans who genuinely need a home to live in, not for short-term speculation or rental income.

As at June 2026, the standard MOP for HDB flats remains five years. For Executive Condominiums — hybrid public-private housing developed by private developers but sold at subsidised prices — the MOP is also five years, but the clock starts at the date of TOP rather than key collection, reflecting the longer construction timeline of EC projects.

Understanding MOP is essential for anyone planning an upgrade, a property portfolio move, or a change in living arrangements. Getting it wrong can mean losing your CPF housing grants, facing compulsory acquisition by HDB, or triggering a hefty Additional Buyer’s Stamp Duty (ABSD) bill that could have been avoided with proper timing.

HDB MOP: The Five-Year Rule in Detail

For the vast majority of HDB flat owners — whether they bought a Build-To-Order (BTO) flat, a resale flat or a Design, Build and Sell Scheme (DBSS) unit — the MOP is five years from the date they receive the keys and officially take possession of the flat. The MOP is continuous; it is not paused if you travel overseas for an extended period or temporarily work abroad, though HDB does allow a cumulative absence of up to three months per year for legitimate reasons such as work or medical treatment abroad.

During the five-year MOP, HDB flat owners:

- Cannot sell or transfer the flat to any party, including immediate family members, except in limited circumstances such as death of an owner or court order.

- Cannot sublet the entire flat. You may, however, rent out individual rooms with HDB’s approval, subject to the Non-Citizen Quota (NCQ) for your block and neighbourhood, and eligibility rules based on your flat type.

- Cannot acquire private residential property in Singapore if doing so would trigger HDB’s concurrent ownership restriction. Under current rules, HDB flat owners who purchase private residential property must dispose of the HDB flat within six months of the private property’s completion — but there is no hard bar on owning private property per se during MOP, provided ABSD is paid. The practical consequence is that HDB flat owners who wish to “upgrade” to a private home during the MOP face the 20% ABSD on their second property (for Singapore Citizens) and must either dispose of the HDB flat or hold both.

The MOP clock does not reset if you carry out renovations, change the flat’s tenants, or add or remove co-owners (with HDB’s approval). However, if HDB grants permission for a Change in Flat Ownership — for example, adding a family member as a co-owner — the MOP continues to run from the original key collection date.

PLH Flats: The Extended 10-Year MOP

Since November 2021, flats in mature, centrally located estates such as Queenstown, Bishan, Toa Payoh and Ang Mo Kio have been classified under the Prime Location Public Housing (PLH) model. PLH flats carry more restrictive conditions than standard HDB flats, including a 10-year MOP (double the standard five years). This means PLH flat owners must live in their flat for a full decade before they can sell on the open resale market.

Additional PLH restrictions include:

- A subsidy clawback on resale — owners must repay a proportion of the resale proceeds to HDB, reflecting the discount from market price they received at launch.

- PLH flats cannot be rented out in their entirety even after the MOP; they remain owner-occupied in perpetuity unless HDB changes the policy.

- Buyers of PLH flats on the resale market must also satisfy income ceiling and other eligibility criteria.

The 2026 HDB BTO exercises have continued to apply the PLH model to new projects in centrally located towns, so prospective buyers of Prime-classified BTO flats should factor in the 10-year MOP when planning their property journey.

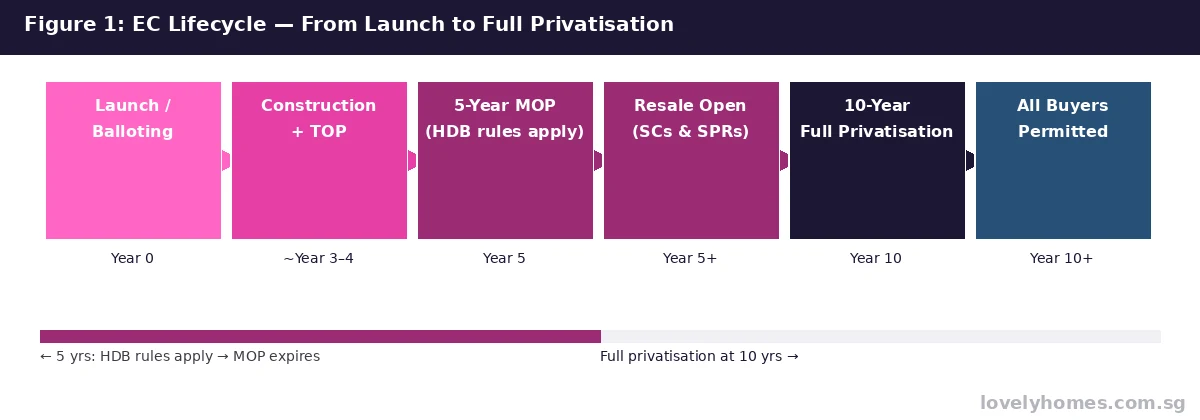

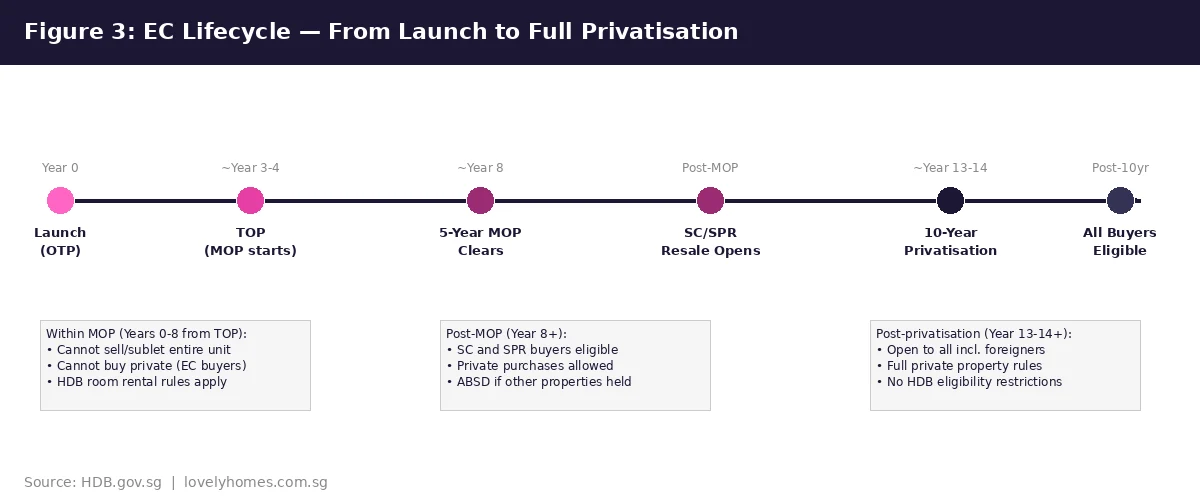

Executive Condominium MOP: Five Years from TOP

Executive Condominiums occupy a unique middle ground in Singapore’s housing landscape. They are developed by private developers, come with private-condo finishes, and are priced at a discount to purely private condominiums — but they are funded with CPF Housing Grants and regulated by HDB rules during their first five years. The MOP for ECs is five years, but crucially, the clock starts on the date of the Temporary Occupation Permit (TOP), not the date buyers collect their keys. Given that EC projects often take three to four years to complete from launch, buyers who purchased at launch may find they cannot sell their EC unit until eight to nine years after they signed the Sales and Purchase Agreement.

During the five-year EC MOP, owners:

- Cannot sell the EC unit on the open market.

- Cannot purchase private residential property as EC units count as HDB-equivalent property for ABSD purposes. An EC owner who buys a private condo during the MOP will be treated as a second-time property purchaser and pay the corresponding ABSD rate.

- Cannot sublet the entire unit, though subletting individual rooms may be allowed with HDB approval, subject to the same NCQ rules as HDB flats.

After the five-year MOP, EC units may be sold to Singapore Citizens and Singapore Permanent Residents. At the 10-year mark from TOP, the EC is fully privatised and may be sold to any buyer, including foreigners and foreign companies — at which point it operates under the full private property regime, with no HDB eligibility or ownership restrictions.

MOP and the ABSD Interaction

The MOP has significant interplay with the Additional Buyer’s Stamp Duty (ABSD) framework. Understanding how they interact is critical for property upgraders, investors and couples planning their next property move.

HDB upgraders: Singapore Citizen couples who own an HDB flat and wish to purchase a private property will pay ABSD at the second-property rate (20% for SC as at June 2026) upfront on the private purchase. They may subsequently apply for an ABSD remission under the Joint Singles Scheme or the standard married couple remission — but only if they sell the HDB flat within six months of the private property’s completion date (for completed properties) or the date of the Sales and Purchase Agreement (for uncompleted projects). Critically, the HDB flat must have cleared its MOP before it can be sold to enable this remission plan.

Private property downgraders: Owners of private residential property who wish to purchase an HDB resale flat must dispose of the private property within six months of the HDB flat key collection. In addition, since September 2022, private residential property owners (including those with a prior private property) must observe a 15-month wait-out period after selling their last private property before they are eligible to purchase a non-PLH HDB resale flat. This rule was introduced to prevent a “round-trip” strategy of selling private property, buying HDB resale at a subsidised price, and quickly flipping it.

EC buyers must take extra care: the EC counts as an HDB-equivalent property for ABSD purposes throughout its MOP. An EC owner who buys a private condo during the five-year MOP is treated as a second-property purchaser and will pay the full ABSD applicable to their buyer profile on the private condo.

Worked Example: HDB Upgrader ABSD + MOP Strategy

The Tan Family — Timing an Upgrade from HDB to Private Condo

Profile: Mr and Mrs Tan, Singapore Citizens (SC), joint income S$14,000 per month. They own a 4-room HDB flat in Tampines purchased in January 2020 at S$420,000. MOP clears January 2025.

Target: A 2-bedroom resale condo in the East Coast area, listed at S$1,550,000.

Timeline scenario A — upgrade in January 2025 (MOP just cleared):

- BSD on S$1,550,000 = first S$180K × 1% + next S$180K × 2% + next S$640K × 3% + balance S$550K × 4% = S$1,800 + S$3,600 + S$19,200 + S$22,000 = S$51,200 BSD

- ABSD at SC second-property rate (20%): S$1,550,000 × 20% = S$310,000 ABSD upfront

- Bank loan: 75% LTV = S$1,162,500 @ 3.1% over 30 years → monthly repayment ~S$4,963/mth; TDSR = 35.5% — PASS

- Cash required: 5% cash = S$77,500; 20% cash/CPF = S$310,000; BSD S$51,200; ABSD S$310,000 = total cash outlay before CPF ~S$438,700

- ABSD remission: Sell HDB flat within six months of SPA date → recover S$310,000 ABSD. Net outlay after remission ~S$128,700 (excl. HDB sale costs, legal fees and agent commission).

- MOP check: HDB flat MOP cleared January 2025 — eligible to sell ✅

Timeline scenario B — attempt to upgrade in July 2024 (MOP not yet cleared): HDB flat MOP clears January 2025. If Tans buy the condo in July 2024, the HDB flat cannot be sold until January 2025 at the earliest. This means they cannot complete the HDB sale within six months of the SPA (July 2024 + 6 months = January 2025 — tight). More importantly, if the resale condo completes in less than six months, the ABSD remission window is at risk. For uncompleted new launches, the six-month clock runs from SPA date. The safer strategy is always to clear MOP first, then buy the private property.

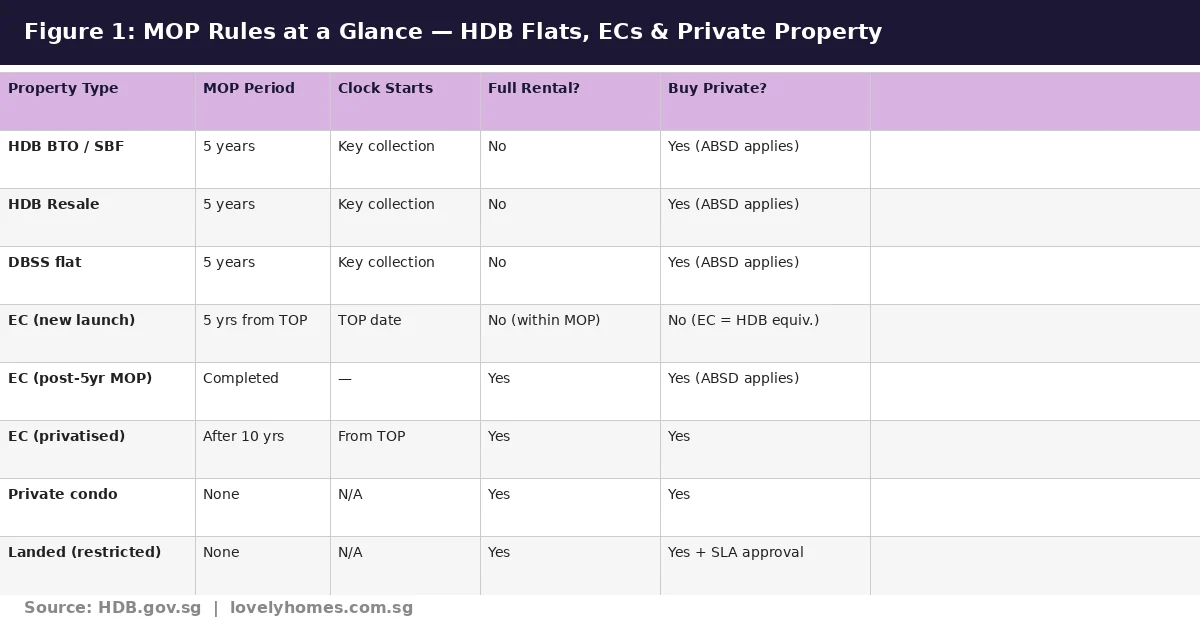

Summary: MOP Rules at a Glance

| Property Type | MOP | Clock Starts | Full Rental During MOP? | Buy Private During MOP? |

|---|---|---|---|---|

| HDB BTO / SBF | 5 years | Key collection date | No (rooms only) | Yes — but ABSD applies |

| HDB Resale | 5 years | Key collection date | No (rooms only) | Yes — but ABSD applies |

| DBSS flat | 5 years | Key collection date | No (rooms only) | Yes — but ABSD applies |

| PLH flat (Prime BTO) | 10 years | Key collection date | No — even post-MOP | Yes — but ABSD applies |

| EC (new launch) | 5 years from TOP | TOP date | No | No — EC = HDB equiv. for ABSD |

| EC (post-privatisation) | N/A (completed) | — | Yes | Yes |

| Private condo / apartment | None | N/A | Yes | Yes |

| Landed (restricted) | None | N/A | Yes | Yes (SLA approval for foreigners) |

What the MOP Rules Mean for Your Property Strategy

Singapore’s MOP framework serves as the primary mechanism by which HDB ensures that subsidised public housing serves its intended purpose: long-term, owner-occupied residence. For property buyers and investors, the practical implications are significant.

For first-time HDB flat buyers, the MOP defines the earliest date at which they can upgrade to a private home without sacrificing ABSD remission eligibility. Planning around this date — and ensuring the private property purchase timing aligns with the MOP clearance — can save hundreds of thousands of dollars in ABSD.

For EC buyers, the extended timeline from launch to MOP clearance (potentially eight to nine years) is often underestimated. Buyers who anticipate needing to sell or purchase another property within that window should model the ABSD exposure before committing.

For private property owners considering a “downgrade” to HDB resale, the 15-month wait-out period is a material planning constraint. Those who sold their private property expecting to buy an HDB resale flat immediately will find themselves renting for at least 15 months, which has cost implications that must be factored into the financial model.

Internationally, Singapore’s MOP is unusual in its strictness relative to most developed-world housing markets, reflecting the government’s deliberate policy choice to subordinate short-term speculative returns to long-term housing stability. Countries like Australia, the United Kingdom and the United States have no equivalent restriction on subsidised public housing resale — Singapore’s approach is more aligned with the social housing models of Hong Kong (where HDB equivalent flats have a two-year MOP) and parts of continental Europe.

What Might Change: MOP Policy Outlook 2026

As at June 2026, there are no announced changes to the standard five-year MOP for HDB BTO and resale flats, nor to the EC MOP framework. The Minister for National Development has consistently indicated that the MOP is a foundational element of Singapore’s public housing philosophy and that any relaxation would risk reintroducing speculative behaviour in the subsidised housing market.

The PLH model’s 10-year MOP, introduced in November 2021, has been applied consistently to Prime-classified BTO projects since then. There has been no signal that this extended MOP will be shortened, though some market observers have noted that as PLH flats begin to clear their 10-year MOPs from around 2031 onwards, there may be policy review of whether the extended restriction achieves its intended effect.

One area to watch is the possible extension of PLH-style restrictions to Plus-classified flats in certain “choicier” locations. As at June 2026, Plus-classified BTO flats carry a standard five-year MOP with income ceiling restrictions on resale, but not the 10-year MOP or full rental prohibition of PLH flats. Any shift in this classification could affect buyers in upcoming BTO exercises.

Frequently Asked Questions

Does the MOP reset if I renovate my HDB flat or add a co-owner?

No — the MOP clock does not reset due to renovation, change of occupiers, or an HDB-approved change of flat ownership (such as adding or removing a co-owner). The MOP continues to run from the original key collection date. However, if an ownership transfer results in a different occupancy arrangement, HDB will assess whether the flat continues to be used for owner-occupation as required during the MOP.

Can I buy a private property while my HDB MOP is still running?

Yes, you can — there is no absolute legal bar on HDB flat owners acquiring private residential property during the MOP, provided you pay the applicable ABSD. For a Singapore Citizen couple where one owns an HDB flat, any private property purchase would be a second property attracting 20% ABSD (as at June 2026). You are not required to sell the HDB flat immediately, but if you wish to claim the SC married-couple ABSD remission on the private purchase, you must sell the HDB flat within six months of the private property’s Temporary Occupation Permit (for new launches) or completion.

When does the EC MOP clock start — at launch, at TOP, or at key collection?

The EC MOP clock starts on the date of TOP (Temporary Occupation Permit) — not the date of the Sales and Purchase Agreement (launch date) and not the date keys are physically collected. Because EC projects typically take three to four years from launch to TOP, buyers who purchase at launch may effectively wait eight to nine years from their purchase before they can sell the unit on the open market.

What happens if I sublease my entire HDB flat during the MOP?

Subletting your entire HDB flat during the MOP without authorisation is a serious breach of HDB’s terms. Consequences can include termination of your tenancy agreement by HDB, compulsory acquisition of the flat at its assessed value (which may be below market price), a fine of up to S$5,000, and in egregious cases, criminal prosecution. HDB actively monitors flat occupancy and periodically checks whether flat owners are physically residing in their units.

Does the 15-month wait-out period apply to all private property owners who want to buy HDB?

The 15-month wait-out period (introduced in September 2022) applies to private residential property owners who dispose of their private property and subsequently wish to purchase an HDB resale flat. It applies to all non-PLH HDB resale flats. There are exceptions: seniors aged 55 and above who are purchasing a 4-room or smaller HDB resale flat are exempt from the wait-out period, as this policy is intended to help older owners right-size to smaller flats without penalising them. The wait-out period does not apply to HDB BTO flat applications.

Are PLH (Prime Location Public Housing) flats subject to the same five-year MOP?

No — PLH flats carry a 10-year MOP, double the standard five years. During the 10-year MOP, PLH flat owners cannot sell the flat, sublet the entire flat, or acquire private residential property without disposing of the HDB flat (subject to ABSD rules). Even after the 10-year MOP, PLH flat owners who sell must repay a subsidy clawback amount to HDB, and PLH flats can never be rented out in their entirety — they must remain owner-occupied.

Do foreigners face any special MOP considerations when owning Singapore property?

Foreigners cannot purchase new HDB flats or most HDB resale flats (with limited exceptions under special schemes). They can purchase EC units only after the 10-year privatisation mark. For private condominiums and apartments, there is no MOP. Foreigners who purchase private residential property may sell or sublet at any time, subject to the Residential Property Act restrictions on landed property. The 15-month wait-out period for HDB resale does not directly apply to foreigners, as they are not eligible to buy HDB flats in the first place.

Tags: HDB MOP, minimum occupation period Singapore, EC MOP, HDB MOP rules 2026, PLH 10-year MOP, HDB MOP private property, Singapore property MOP guide, EC privatisation, HDB upgrader guide, ABSD HDB MOP, Singapore housing policy 2026