HDB Grants Singapore 2026: EHG, CPF Housing Grant, Proximity Grant and Step-Up Grant Explained

Quick Answer: HDB Grants Singapore 2026 — Key Facts

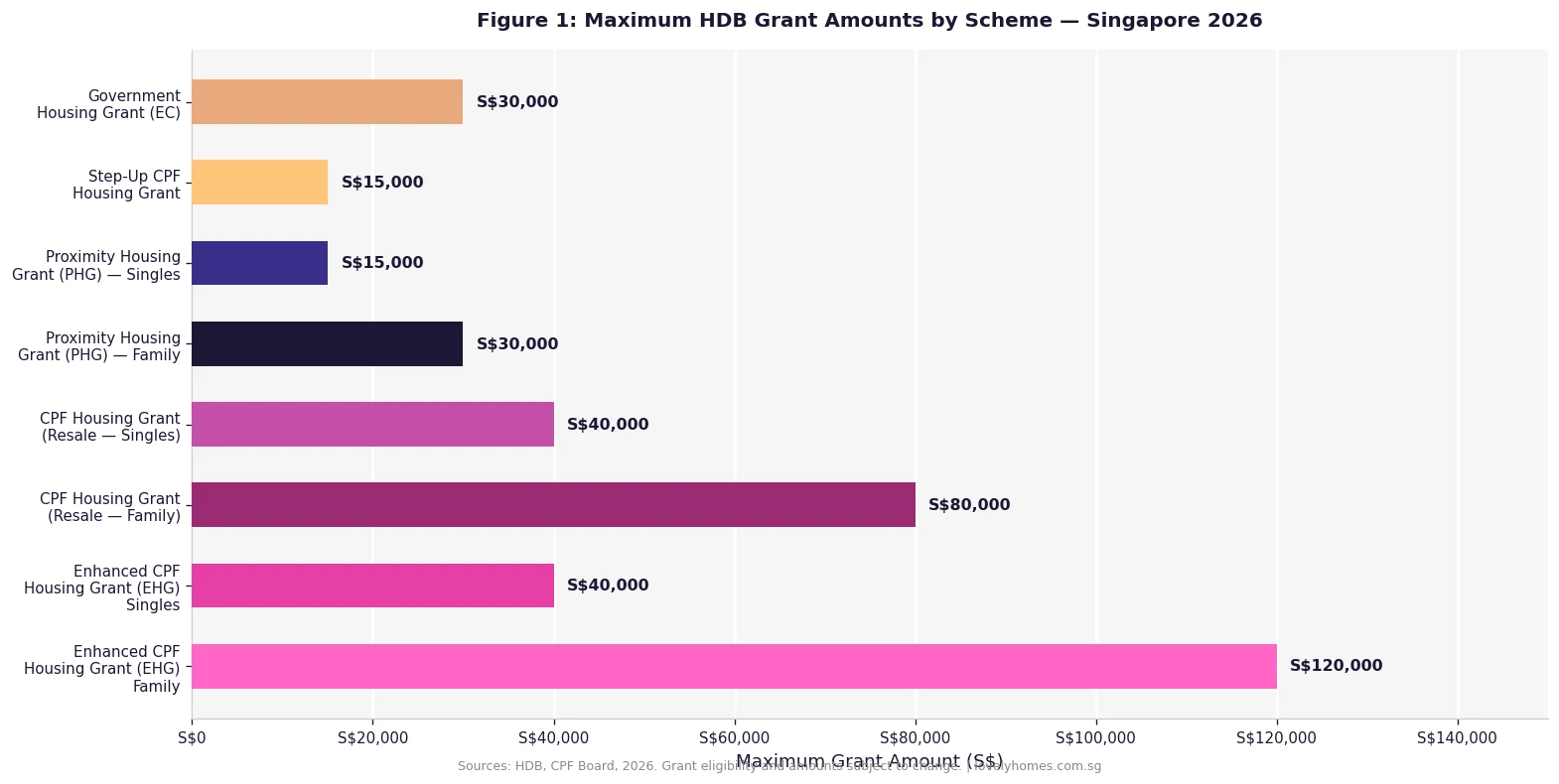

- Enhanced CPF Housing Grant (EHG): Up to S$120,000 for eligible first-timer families; up to S$40,000 for eligible singles. Applies to both BTO and resale flats.

- CPF Housing Grant (CHG): Up to S$80,000 for first-timer families buying a resale HDB flat; S$40,000 for singles.

- Proximity Housing Grant (PHG): Up to S$30,000 for families who buy a resale flat to live with or near parents; S$15,000 for singles.

- Step-Up CPF Housing Grant: S$15,000 for second-timer families upgrading from a 2-room to a 3-room or larger flat in a non-mature estate.

- Government Housing Grant (EC): S$30,000 for eligible first-timer families buying a new Executive Condominium.

- Grants are CPF-credited: All grants go into your CPF Ordinary Account and offset the purchase price — you do not receive cash.

- No double-counting: You can stack compatible grants (e.g., EHG + PHG for resale) but each grant type can only be used once per application.

What Are HDB Grants and Who Administers Them?

HDB housing grants are government subsidies administered jointly by the Housing & Development Board (HDB) and the Central Provident Fund (CPF) Board. They are designed to make homeownership accessible to Singapore Citizens and, in some cases, Permanent Residents, by directly reducing the effective purchase price of an HDB flat.

Grants are credited into your CPF Ordinary Account (OA) — not paid as cash — and can be applied towards the purchase price of your flat or used to reduce your outstanding home loan. This is an important distinction: you cannot withdraw grant amounts in cash, and they are subject to the CPF accrued interest rules when you eventually sell your property.

The grant framework in Singapore is tiered by household income, citizenship status, flat type, and whether you are a first-timer or second-timer applicant. First-timers consistently receive significantly higher grants than second-timers, reflecting the government’s policy of prioritising owner-occupancy and discouraging property speculation within the public housing segment.

Enhanced CPF Housing Grant (EHG) — The Largest Grant Available

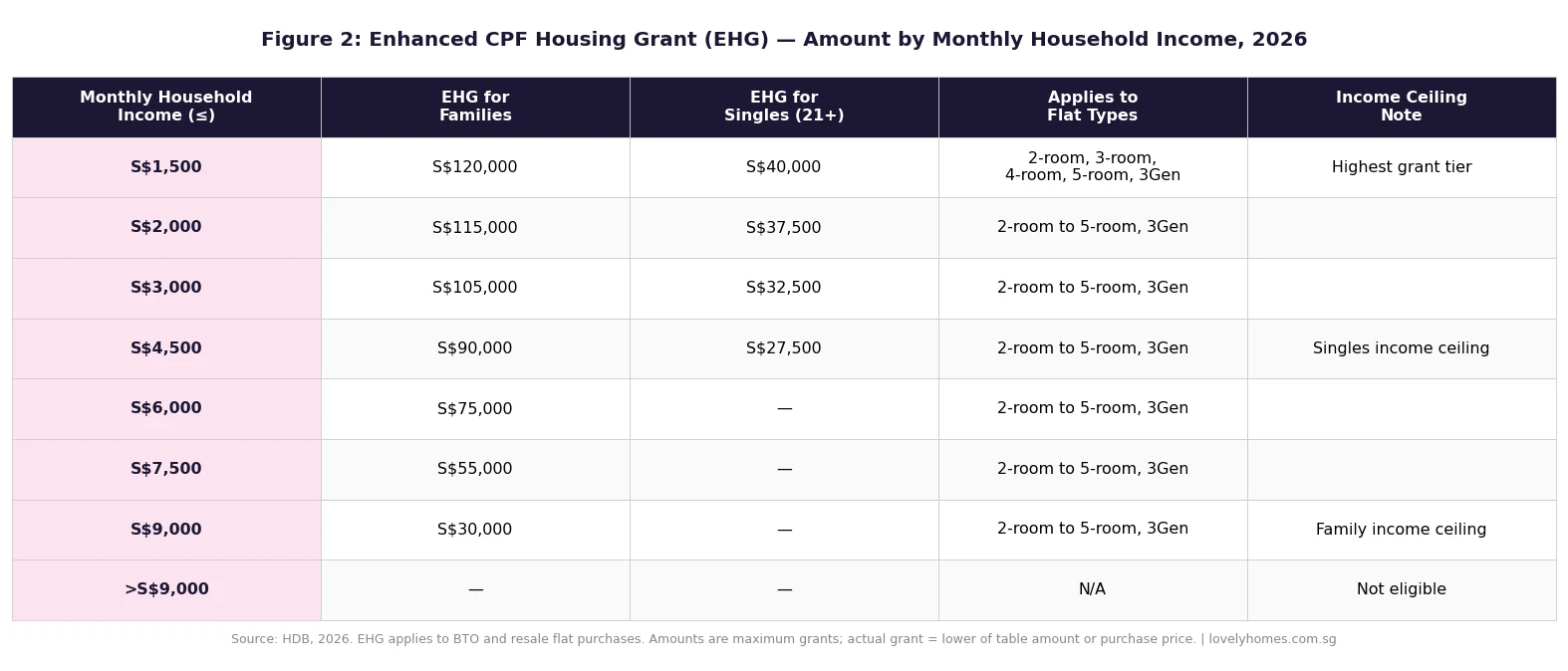

The Enhanced CPF Housing Grant, introduced in September 2019, replaced the Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG). It is the most substantial grant available to first-timer Singapore Citizen households and is specifically calibrated to assist lower- and middle-income buyers.

The EHG is means-tested: the amount decreases as household income rises, and the eligibility ceiling is S$9,000 per month for families and S$4,500 per month for singles (as at 2026). To qualify, at least one applicant must have worked continuously for at least twelve months before the flat application date, and must continue working at the time of application.

One critical requirement that catches many applicants off-guard: the EHG is only available for flats purchased with a remaining lease of at least 20 years at the time of application, and whose remaining lease can cover the youngest buyer to at least age 95. This lease requirement affects certain older resale flats, which may otherwise be eligible by income but fail the lease longevity test.

CPF Housing Grant (CHG) — For Resale Flat Buyers

The CPF Housing Grant (sometimes called the Family Grant or Singles Grant in older HDB materials) is specifically available to first-timer buyers purchasing a resale HDB flat on the open market. Unlike the EHG, which applies to both BTO and resale purchases, the CHG is resale-only — BTO buyers receive the EHG instead.

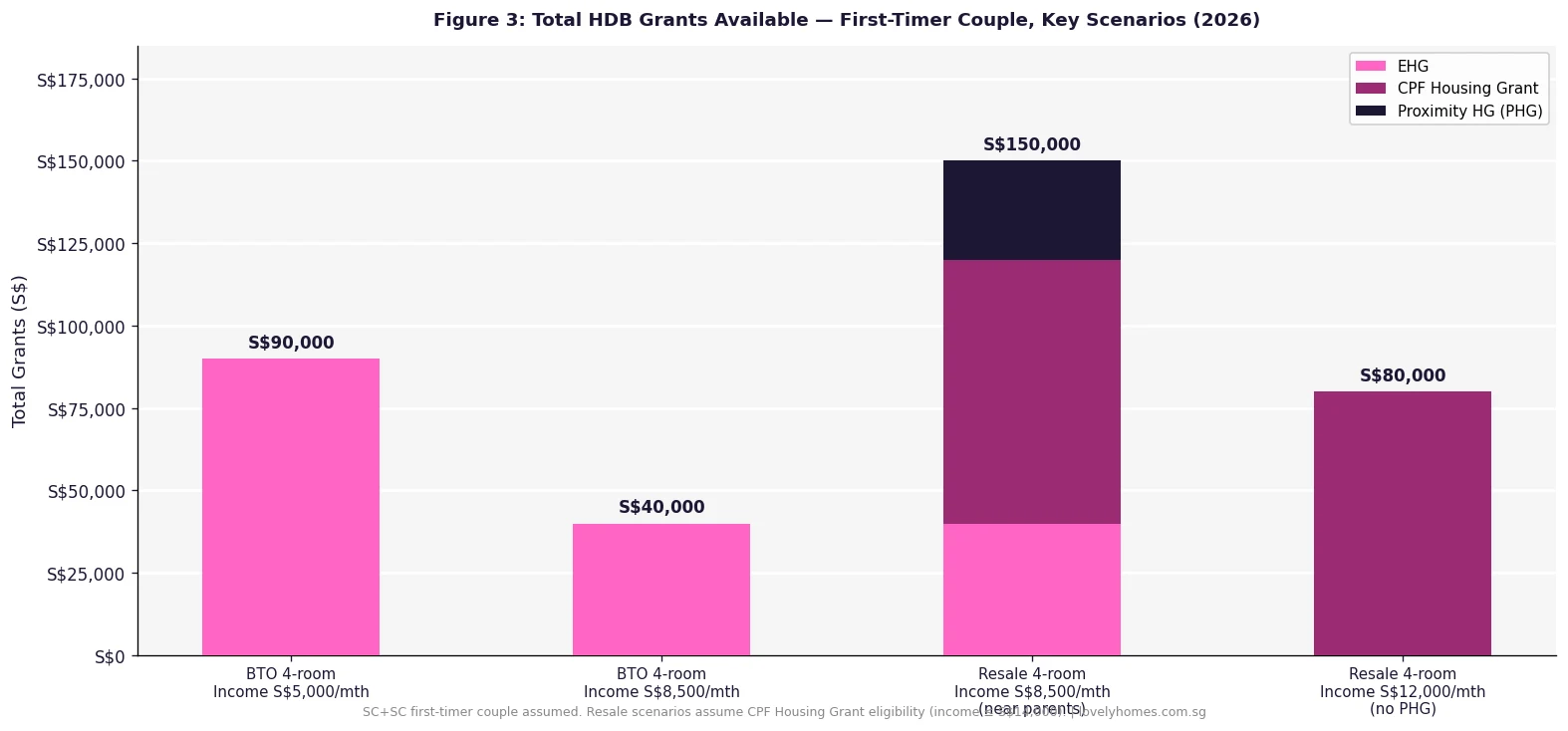

As at 2026, the maximum CHG is S$80,000 for first-timer Singapore Citizen families (where both applicants are Singapore Citizens) and S$40,000 for first-timer Singles aged 35 or above. For households where one applicant is a Singapore Citizen and the other is a Permanent Resident, the grant reduces to S$50,000. The income ceiling for the CHG is S$14,000 per month — notably higher than the EHG ceiling, meaning more households are eligible.

Proximity Housing Grant (PHG) — For Families Buying Near Parents

The Proximity Housing Grant incentivises multigenerational living by rewarding families who buy a resale HDB flat to live with or within 4 kilometres of their parents’ or children’s existing HDB flat. It is a resale-only grant and is available regardless of whether the buyer is a first-timer or second-timer, making it one of the few grants accessible to second-timers on a meaningful scale.

To live with parents or married children (same address), the PHG is S$30,000 for families and S$15,000 for singles. To live within 4 km of parents’ or children’s existing flat, the PHG is S$20,000 for families and S$10,000 for singles. There is no income ceiling for the PHG — any household, regardless of income, may apply as long as the proximity and family relationship conditions are met.

The PHG can be stacked with the EHG and CPF Housing Grant for resale buyers. A first-timer SC+SC couple earning S$8,500 per month buying a resale flat to live near parents could, in theory, receive EHG of S$40,000 + CHG of S$80,000 + PHG of S$30,000 = a total of S$150,000 in grants — making a resale flat in a mature estate substantially more affordable than it appears at headline price.

Step-Up CPF Housing Grant — Second-Timers Upgrading Within HDB

The Step-Up CPF Housing Grant of S$15,000 is specifically for second-timer Singapore Citizen families who currently live in a 2-room HDB flat (Flexi or standard) and wish to upgrade to a larger 3-room or bigger flat in a non-mature housing estate, sourced directly from HDB (i.e., a BTO flat in the relevant sales exercise). It is not available for resale flat purchases.

The income ceiling for the Step-Up Grant is S$7,000 per month, and at least one applicant must have been a Singapore Citizen for at least five years. This grant is deliberately narrow in scope — it targets a specific population of residents in smaller flats who need a capacity upgrade but remain in the lower-to-middle income band.

Government Housing Grant (GHG) for Executive Condominiums

First-timer Singapore Citizen families purchasing a new Executive Condominium (EC) directly from a developer are eligible for the Government Housing Grant of S$30,000, credited into the purchaser’s CPF OA. The income ceiling for the EC grant is the same as the EC purchase income ceiling — S$16,000 per month as at 2026. This grant cannot be combined with the EHG or CHG, as those apply only to HDB flat purchases; the GHG is the equivalent grant mechanism for the EC segment.

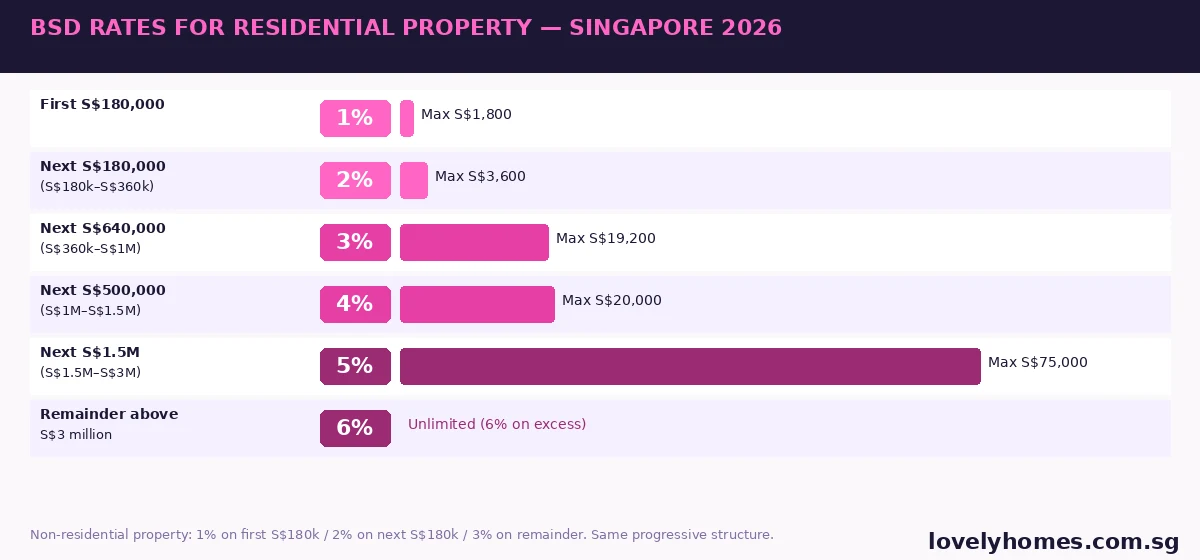

Summary: Grant Comparison Table

| Grant | Max (Family) | Max (Singles) | Income Ceiling | BTO? | Resale? | First-Timer? |

|---|---|---|---|---|---|---|

| EHG | S$120,000 | S$40,000 | S$9,000 / S$4,500 | ✅ | ✅ | Required |

| CPF Housing Grant | S$80,000 | S$40,000 | S$14,000 | ❌ | ✅ | Required |

| PHG (live with) | S$30,000 | S$15,000 | None | ❌ | ✅ | Not required |

| PHG (within 4km) | S$20,000 | S$10,000 | None | ❌ | ✅ | Not required |

| Step-Up Grant | S$15,000 | — | S$7,000 | ✅ | ❌ | Not required |

| Govt HG (EC) | S$30,000 | — | S$16,000 | EC only | ❌ | Required |

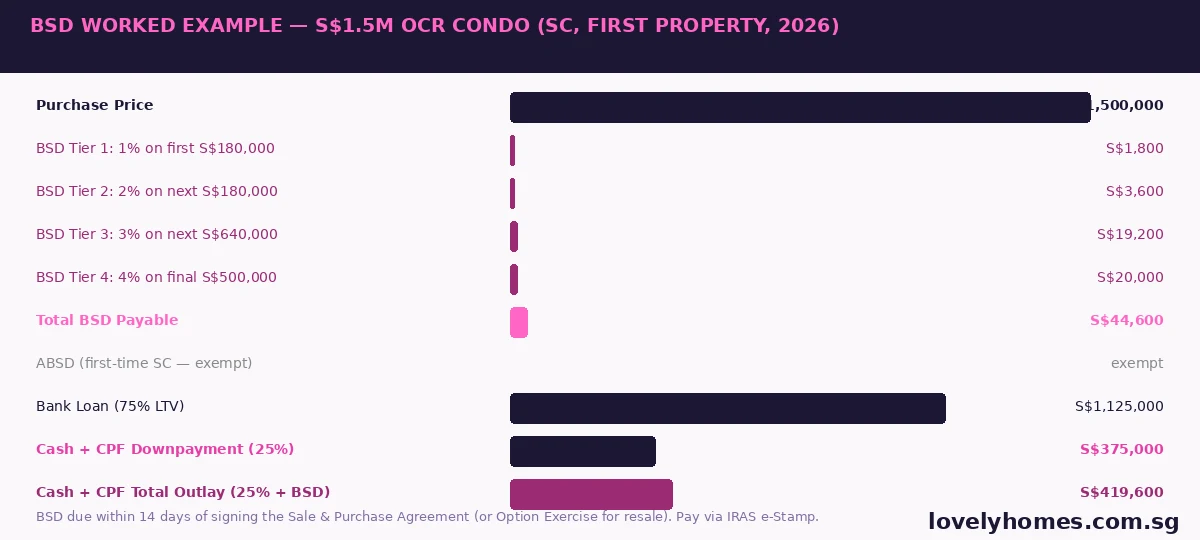

Worked Example: The Lim Family — Maximising HDB Grants on a Resale Flat

Mr and Mrs Lim are a Singapore Citizen married couple, both aged 29. Their combined gross monthly household income is S$6,500. They are first-timers. Mrs Lim’s parents own an HDB flat in Queenstown, and the couple would like to buy a resale 4-room flat in Buona Vista to live together with the parents.

Step 1 — EHG eligibility: Income S$6,500 → EHG for families at this income bracket = S$75,000. (From the EHG tier table: ≤S$7,500/mth = S$55,000. Correcting: S$6,000–S$7,500 range → S$55,000 EHG.)

Step 2 — CPF Housing Grant (resale): Income S$6,500 ≤ S$14,000 → CHG = S$80,000 (both SCs, first-timers, resale flat).

Step 3 — PHG (living with parents): Living with parents at same address → PHG = S$30,000. No income ceiling.

Step 4 — Total grants:

| Grant | Amount |

|---|---|

| Enhanced CPF Housing Grant (EHG) | S$55,000 |

| CPF Housing Grant (CHG) | S$80,000 |

| Proximity Housing Grant (PHG — live with parents) | S$30,000 |

| Total Grants (CPF OA credited) | S$165,000 |

| Indicative resale flat price (Buona Vista 4-room) | S$780,000 |

| Effective price after grants | S$615,000 |

| HDB Concessionary Loan (80% of S$780k − grants offset) | ~S$459,000 |

| Cash + CPF down payment (20%) | ~S$156,000 |

The Lims’ S$165,000 in grants reduces a S$780,000 resale flat to an effective out-of-pocket position requiring approximately S$156,000 in down payment (cash + CPF, with grants credited to OA first). Their HDB Concessionary Loan at 2.6% p.a. on approximately S$459,000 produces a monthly repayment of roughly S$2,060 — a MSR-compliant 31.7% of their S$6,500 combined income, below the 30% MSR cap when rounded down on the concessionary loan basis (HDB concessionary loan MSR = 30% of gross monthly income).

Note: CPF accrued interest will apply to the grants and CPF OA amounts used, payable upon eventual sale of the flat. The Lims should factor this into their long-term financial planning.

Why HDB Grants Matter in Singapore’s Property Market

Singapore’s HDB grant system is one of the most comprehensive public housing subsidy frameworks in the world. Unlike many countries where housing subsidies take the form of direct cash payments or tax credits, Singapore’s approach links grants directly to the CPF system and the property purchase process — ensuring subsidies are deployed towards asset acquisition rather than consumption spending.

For first-timer households earning S$6,000–S$8,000 per month — the Singapore median household income bracket — the combined effect of EHG, CHG, and PHG can reduce the effective purchase price of a resale flat by S$100,000 to S$165,000. On a S$600,000–S$800,000 resale flat, this represents a 15–25% effective discount, which is transformative for affordability.

The grant structure also reveals HDB’s policy priorities clearly: it heavily favours first-timers over second-timers, rewards proximity to elderly parents, and calibrates generosity inversely to income. Buyers who understand this structure can make significantly better purchase decisions — for example, choosing a resale flat with PHG eligibility over a BTO flat, purely because the grant stacking arithmetic makes the resale option more affordable net of grants.

What Might Come Next

The Singapore government reviews HDB grant parameters periodically, typically in line with National Day Rally announcements or budget statements. The most recent significant change was the introduction of the EHG in 2019 and the progressive upward revision of resale grant amounts in 2023. Given the ongoing focus on housing affordability — and the political salience of the HDB resale market — further adjustments to grant ceilings or income thresholds cannot be ruled out ahead of the next general election cycle. Buyers currently in the planning phase should check for the most current figures on the official HDB website before committing to a purchase.

Frequently Asked Questions

Can I receive grants as cash instead of CPF?

No. All HDB housing grants — EHG, CPF Housing Grant, PHG, Step-Up, and the Government Housing Grant for ECs — are credited directly into your CPF Ordinary Account. You cannot receive them as cash and you cannot use them for renovation or any purpose other than the property purchase. When you eventually sell the flat, the grant amounts (plus CPF accrued interest at 2.5% per annum) must be refunded to your CPF OA.

Do Singapore Permanent Residents qualify for HDB grants?

PRs have limited access to HDB grants. A PR who is part of an SC-PR couple applying for a resale flat may be eligible for a reduced CPF Housing Grant (S$50,000 for SC+PR families versus S$80,000 for SC+SC families). The EHG is only available where at least one applicant is a Singapore Citizen. The PHG and Step-Up Grant require at least one Singapore Citizen applicant. PRs applying as singles (single-nucleus PR household) are generally not eligible for HDB grants.

What is the difference between a first-timer and a second-timer?

A first-timer is a Singapore Citizen who has not previously received any HDB housing subsidy — meaning they have never owned an HDB flat bought directly from HDB, received a CPF Housing Grant, or been listed as an occupier of a subsidised flat that subsequently received a grant. A second-timer is anyone who has previously received an HDB housing subsidy. First-timers receive substantially higher grants and priority balloting across BTO exercises.

Can I use grants for the down payment?

Grants are credited to your CPF OA, which can then be used for the CPF-eligible portion of the down payment. For an HDB Concessionary Loan, the minimum cash down payment is 10% of the purchase price; the remaining 10% can be funded from CPF (including grants credited to CPF OA). For a bank loan, the cash down payment is 5% and the next 20% can be from CPF. So yes — grants effectively reduce the CPF component you need to contribute from your own savings, improving cash affordability.

What happens to grants when I sell my HDB flat?

When you sell your HDB flat, the total grant amount received — plus CPF accrued interest at 2.5% per annum compounded from the date of purchase — must be returned to your CPF OA. This is not a penalty; the accrued interest compensates for the fact that the grant money was in your CPF OA earning interest that was “diverted” to your flat purchase. The refunded amount forms part of your CPF savings and can be used for your next property purchase, subject to the applicable rules.

Do HDB grants affect how much I can borrow?

Not directly — grants do not increase your borrowing capacity, as loan quantum is determined by your income, credit profile, TDSR, and MSR (for HDB loans). However, grants reduce the effective purchase price, which means the loan quantum required to complete the purchase is lower. A lower loan quantum means lower monthly repayments, which in turn may make a higher-priced flat MSR/TDSR-compliant that would otherwise breach the borrowing limit.

Can grants be used to buy private property?

No. HDB housing grants — EHG, CHG, PHG, and Step-Up Grant — can only be used to purchase HDB flats (for BTO or resale). The Government Housing Grant can be used for EC purchases. None of these grants may be applied to the purchase of a fully private condominium, landed property, or commercial property. If you use grants to purchase an HDB flat and subsequently sell it to buy private property, the grant amounts plus accrued interest must first be refunded to your CPF OA.

Related Articles

- HDB Income Ceiling Singapore 2026: BTO, EC, EHG and Resale

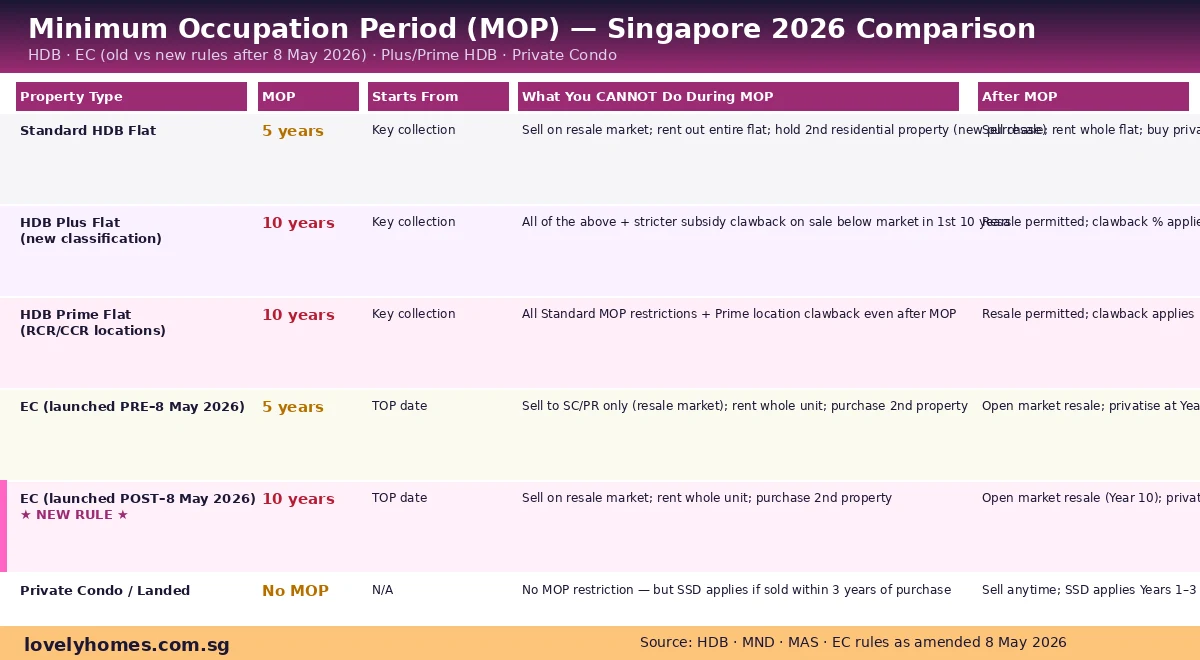

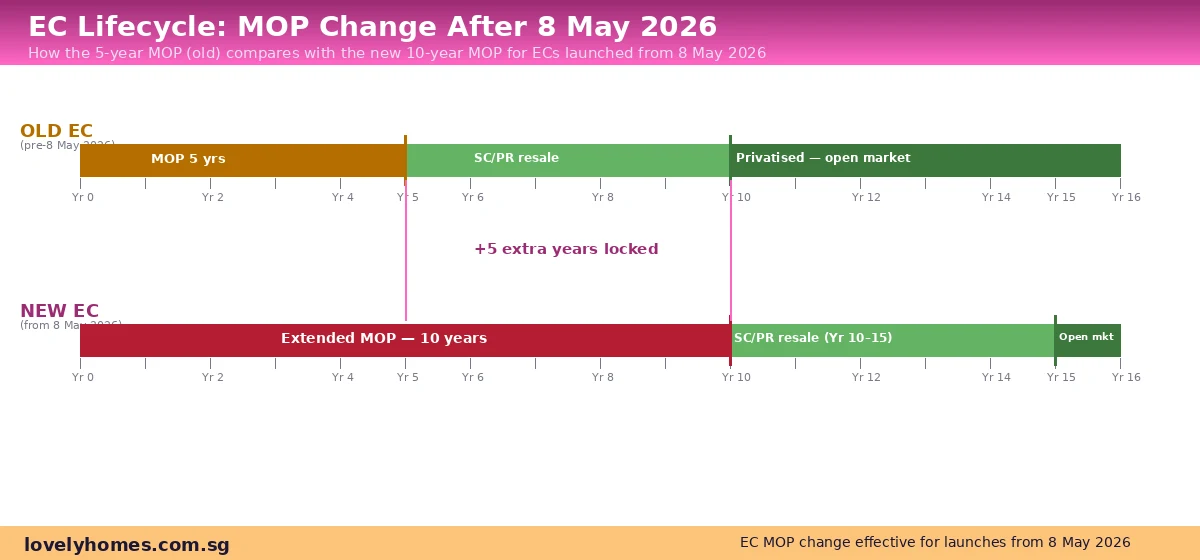

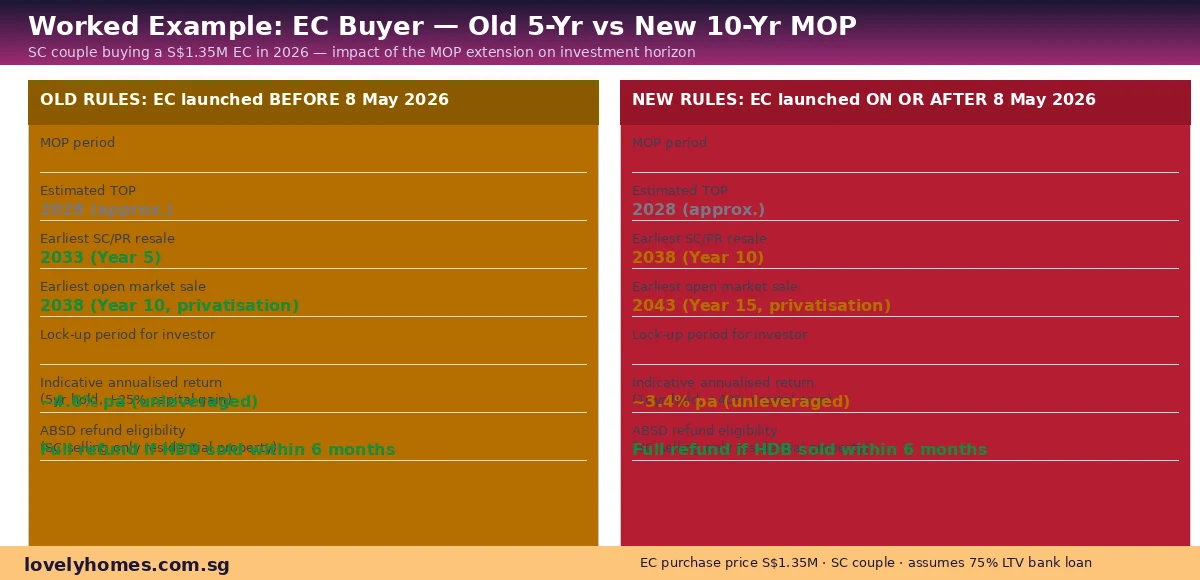

- Minimum Occupation Period (MOP) Singapore 2026: HDB, EC and Private Property Rules

- Executive Condominium Singapore 2026: Complete Guide to Eligibility, MOP and Pricing

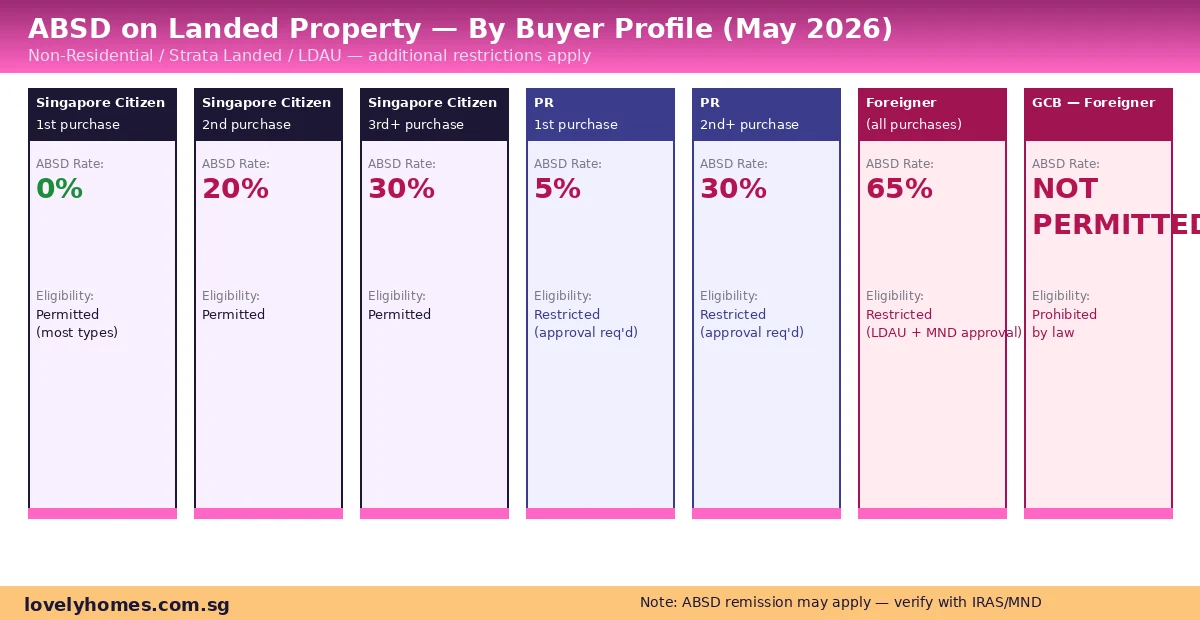

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- BSD Singapore 2026: Complete Guide to Buyer’s Stamp Duty Rates

- TDSR Singapore 2026: How the 55% Cap and Stress Test Decide Your Home Loan

Disclaimer: This article is for general informational purposes only and does not constitute financial or legal advice. HDB grant amounts, eligibility criteria, and income ceilings are subject to change by HDB and CPF Board at any time. Readers are strongly advised to verify current grant parameters directly with HDB at www.hdb.gov.sg, the CPF Board at www.cpf.gov.sg, and to consult a licensed financial adviser before making any property purchase decision.