Singapore Condo Sinking Fund and Maintenance Fee Guide 2026: What Every Owner Needs to Know

When Singaporeans talk about the monthly cost of owning a condominium, they usually quote the mortgage repayment. What often gets overlooked — until the first few months after moving in — are the maintenance fee and sinking fund levy: two mandatory monthly contributions that every strata-titled condo owner must pay to the Management Corporation Strata Title (MCST). Together, these can add S$300 to S$1,200 per month to the cost of condo ownership, and failing to pay them has real legal consequences. This guide explains exactly what these charges are, how they are set, what they pay for, and how to plan for them when buying a condo in Singapore.

Quick Answer — Condo Fees at a Glance

- Maintenance fee: monthly contribution for day-to-day estate running costs (security, cleaning, utilities, landscaping).

- Sinking fund levy: monthly contribution to a reserve for major capital expenditure (lift replacement, roof waterproofing, facade repainting).

- Both are collected by the MCST, the legal body representing all owners in a strata development.

- Contributions are set at the Annual General Meeting (AGM) based on unit share value — larger units pay more.

- Typical total condo fee (maintenance + sinking fund): S$300–S$1,200/month, depending on development size, age, and facilities.

- The sinking fund must be maintained at a minimum of 10% of the preceding year’s management fund under the BMSMA.

- Non-payment can result in MCST filing a court order against the owner. There is no grace period in law.

- Governed by the Building Maintenance and Strata Management Act (BMSMA), administered by the Commissioner of Buildings (COB) under HDB.

What Is the MCST and Who Sets the Fees?

Every strata-titled development in Singapore — from a two-unit walk-up to a 1,000-unit mega-project — is governed by a Management Corporation Strata Title (MCST). The MCST is a body corporate constituted automatically when the strata title plan is registered with the Singapore Land Authority (SLA). It has its own legal personality: it can sue, be sued, hold property, and enter contracts.

The MCST is governed by a Management Council, elected by subsidiary proprietors (owners) at the AGM. The Council sets annual budgets for two distinct funds: the Management Fund (covering day-to-day operations) and the Sinking Fund (covering capital expenditure). Individual owner contributions to each fund are proportional to their unit’s share value — an integer assigned to each lot at the time of development based on floor area and usage. A 1,500 sqft unit might have a share value of 10; a 600 sqft studio might have a share value of 5. Your monthly levy is therefore your unit’s share value divided by the total share values of all units in the development, multiplied by the total annual budget for that fund, divided by 12.

The legal framework governing all of this is the Building Maintenance and Strata Management Act (BMSMA), Cap. 30C. Key rules include: the sinking fund must hold at least 10% of the management fund budget; the MCST must prepare audited accounts annually; and owners who are in arrears can have their contribution recovered as a civil debt.

| Feature | Management Fund | Sinking Fund |

|---|---|---|

| Purpose | Day-to-day operations | Long-term capital expenditure reserve |

| Examples of use | Security, cleaning, gardening, utilities | Lift replacement, waterproofing, facade repainting |

| BMSMA minimum | No statutory minimum set | Must equal at least 10% of management fund budget |

| Planning horizon | Annual (reset each year) | Cumulative — builds over time; does not reset |

| Typical monthly levy | S$200–S$1,200 (varies by unit size) | S$30–S$200 (10–15% of management fee) |

| Recoverable on sale? | No — stays with MCST | No — stays with MCST |

Maintenance Fee — What It Covers

The maintenance fee (sometimes called the management fee or conservancy charge) finances the Management Fund, which covers the development’s recurring, day-to-day operating costs. These typically include:

Security services (24-hour guardpost, patrols, CCTV monitoring), cleaning and housekeeping of common areas, landscaping and horticultural maintenance, utility bills for common area lighting and lifts, pool and gymnasium upkeep (water treatment, equipment servicing), insurance for the building fabric and common property, property management agent fees, and routine maintenance and minor repairs. For luxury developments with concierge services, valet parking, or hotel-grade amenities, the management fund also covers these premium services — which is why fees in such projects can reach S$900+ per month for a large unit.

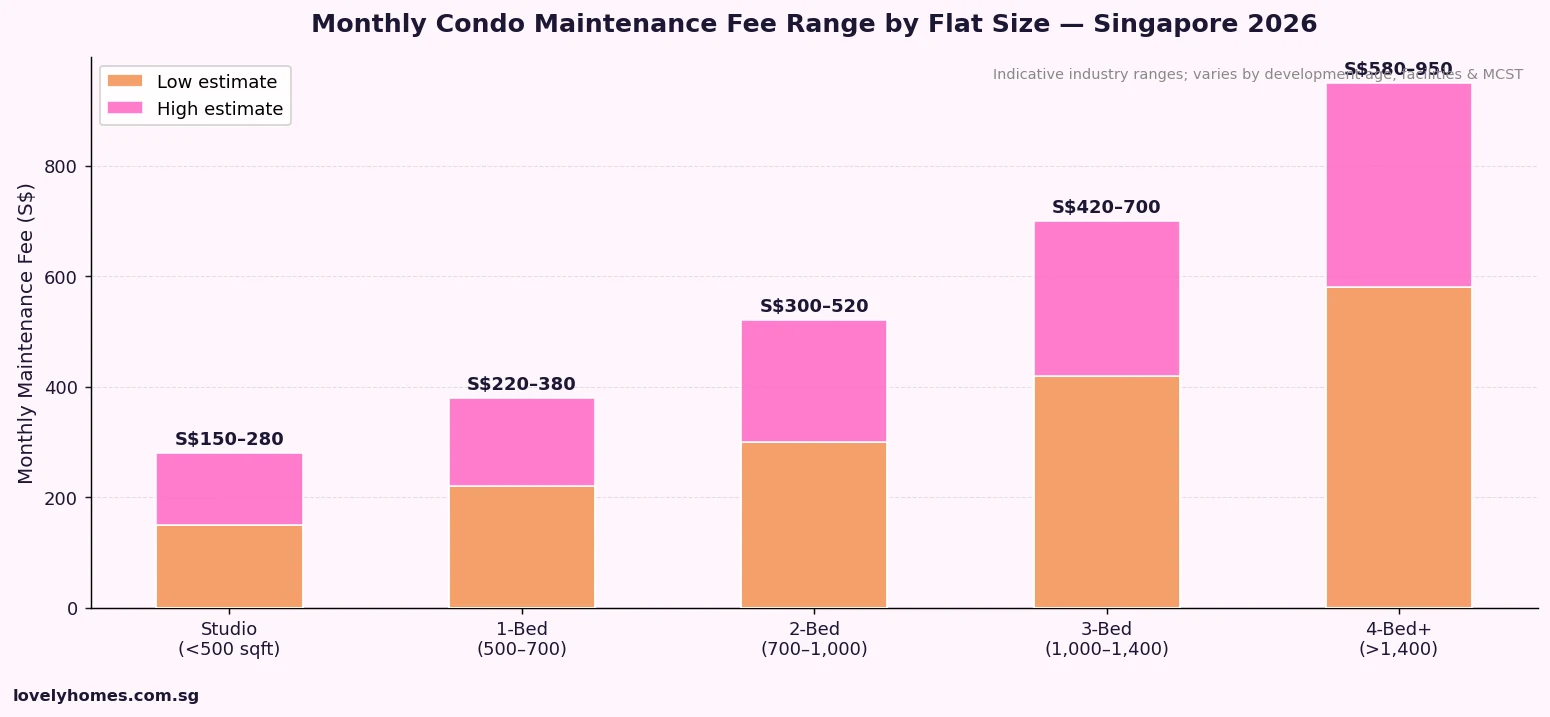

| Unit Size | Typical Monthly Maintenance Fee | Key Variables |

|---|---|---|

| Studio / 1-bed (<500–700 sqft) | S$150–S$380 | Older projects, fewer facilities: lower end |

| 2-bedroom (700–1,000 sqft) | S$300–S$520 | Most common resale condo bracket |

| 3-bedroom (1,000–1,400 sqft) | S$420–S$700 | City-fringe projects with full facilities |

| 4-bed / large unit (>1,400 sqft) | S$580–S$950 | CCR luxury projects at high end |

| Penthouse / duplex (>2,000 sqft) | S$900–S$1,500+ | Top-tier city projects, concierge, valet |

Sinking Fund — What It Covers and Why It Matters

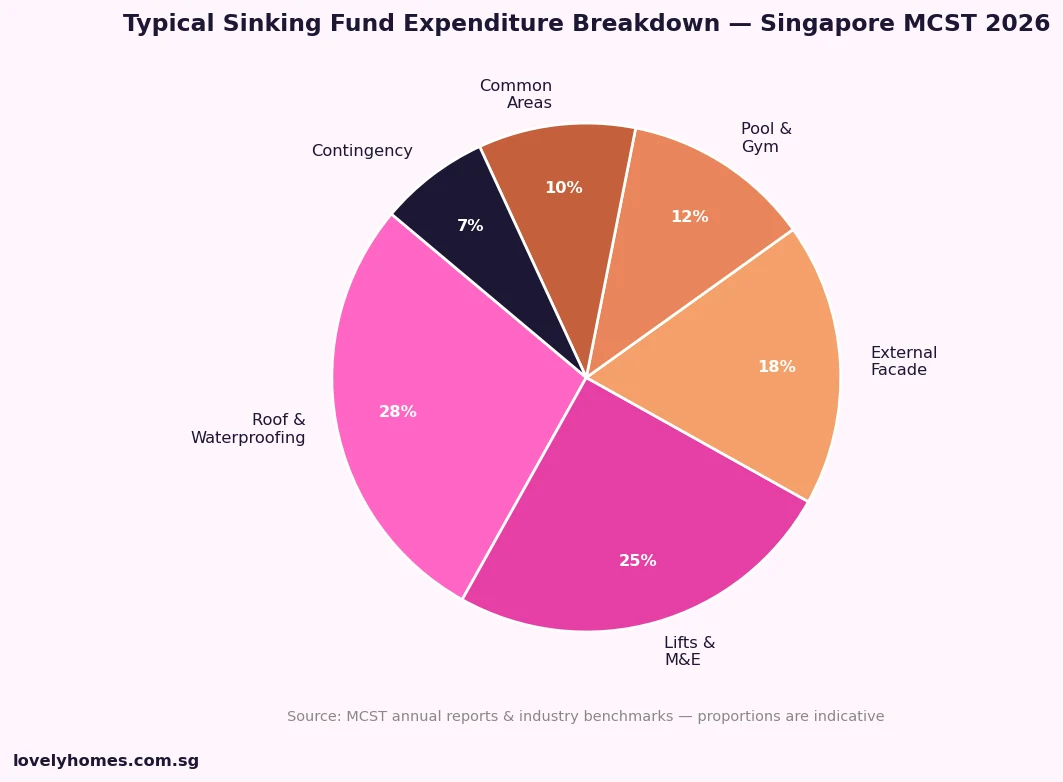

The sinking fund is a long-term capital reserve. Where the management fund covers ongoing operating costs, the sinking fund accumulates money for expenditure that is infrequent but extremely expensive — the kind of expenditure that cannot be funded from a single year’s management budget without creating a financial crisis for the MCST. Examples include: full lift replacement (typically every 20–25 years, S$200,000–S$500,000 per lift), external facade repainting (every 5–7 years for projects with extensive external surfaces), roof waterproofing membrane replacement, major mechanical and electrical (M&E) infrastructure overhaul, and swimming pool resurfacing.

The BMSMA requires the sinking fund to be maintained at a minimum of 10% of the preceding year’s management fund amount. In practice, well-managed MCSTs maintain a sinking fund that is a multiple of this minimum — particularly for older developments approaching major capital expenditure cycles. A prudent MCST will commission a 5-year capital expenditure plan and set sinking fund contributions accordingly. Buyers of older condos (15+ years old) should always ask for the current sinking fund balance and the 5-year capex plan before purchasing, as a depleted sinking fund may result in a special levy — a one-time extraordinary contribution demanded of all owners to fund urgent repairs.

Worked Example — Monthly Fees for a 3-Bedroom Condo in Clementi

Mr and Mrs Tan are purchasing a 1,100 sqft 3-bedroom resale condominium in Clementi (District 5) for S$1,580,000. The development has 320 units, was built in 2008, and has a shared value allocation of 8 for their unit. Total share values across all units sum to 2,240. The MCST’s annual budgets are: Management Fund S$1,680,000; Sinking Fund S$210,000.

| Item | Calculation | Monthly Amount |

|---|---|---|

| Management Fund contribution | (8 ÷ 2,240) × S$1,680,000 ÷ 12 | S$500 |

| Sinking Fund contribution | (8 ÷ 2,240) × S$210,000 ÷ 12 | S$62.50 |

| Total monthly MCST levy | S$562.50 |

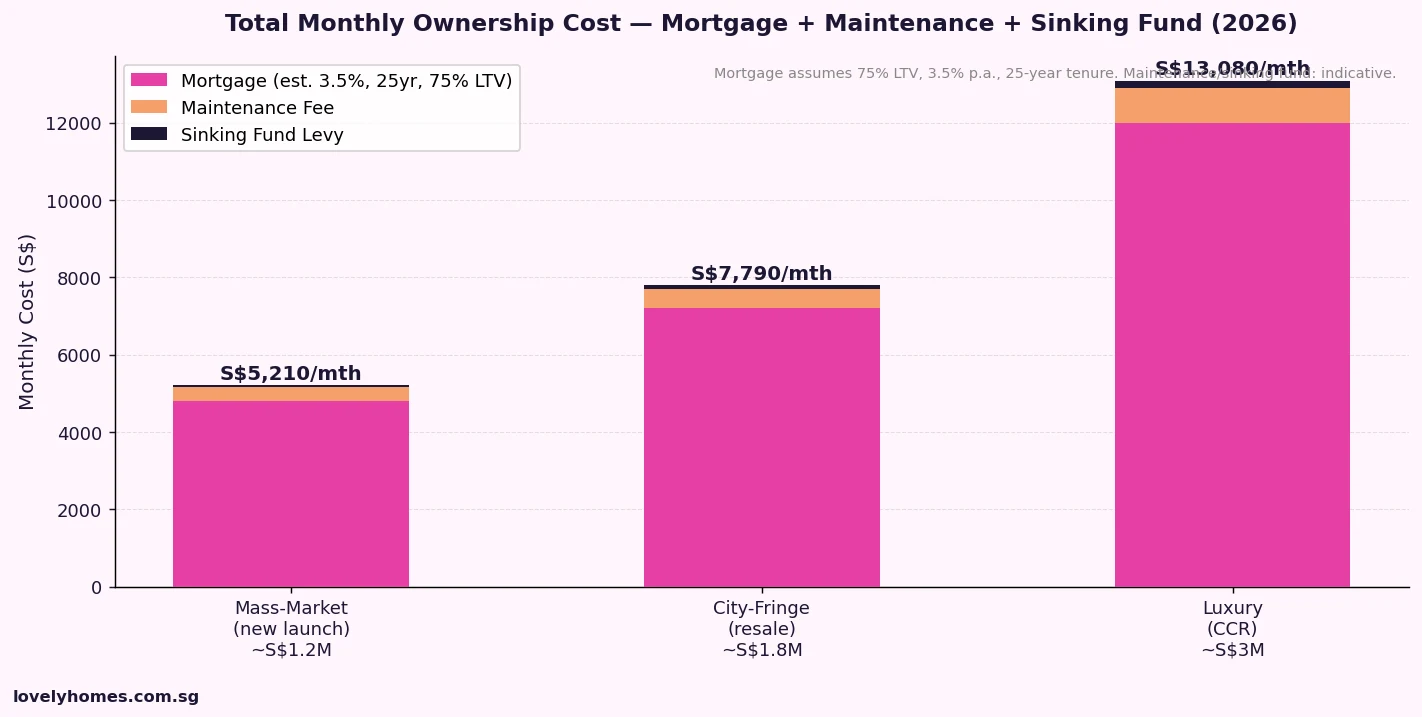

On top of this, the Tans’ estimated monthly mortgage repayment on a bank loan of S$1,185,000 (75% LTV) at 3.5% over 25 years is approximately S$5,926. Their total monthly ownership cost is therefore approximately S$6,488. When running TDSR calculations, the bank will factor in the maintenance fee as a financial commitment — check with your mortgage adviser on how this is treated.

Total Monthly Ownership Cost — Mortgage, Maintenance and Sinking Fund

What Happens If You Don’t Pay?

MCST contributions are not optional. Under Section 40 of the BMSMA, unpaid contributions (whether management fund or sinking fund) are a debt recoverable by the MCST in the same way as any civil debt. The MCST can file a Magistrate’s Court claim for outstanding amounts and, if judgment is obtained, apply for enforcement including attachment of the owner’s bank accounts or garnishment of rental income. The MCST also has the right to charge interest on late contributions at a rate fixed in its by-laws (commonly 10–12% per annum).

For landlords renting out their unit, unpaid MCST contributions remain the owner’s liability — not the tenant’s. If a seller has outstanding arrears at the point of property transfer, the arrears must be settled before the strata certificate of title is transferred. In practice, the conveyancing lawyers for both sides will conduct an MCST search to confirm that no arrears exist before completion.

Checking Sinking Fund Health Before You Buy

Before committing to a resale condo purchase, particularly in an older development, always request the following from the seller’s lawyers or directly from the MCST:

The current sinking fund balance (a healthy reserve is generally more than 3× the annual sinking fund budget); the 5-year capital expenditure plan (if available — well-run MCSTs have one); any pending special levies that have been voted on at an AGM but not yet collected; and the MCST financial statements for the past two years. A development with a healthy sinking fund and a documented capital plan is significantly lower risk than one that is underfunded and approaching major lift or roof works. In the latter case, you may be buying into an imminent S$10,000–S$50,000 special levy per unit.

What This Means for Condo Buyers in 2026

Condo maintenance fees have risen materially over the past three years, driven by higher labour costs for security and cleaning personnel, increased utility tariffs, and the generally higher cost of building materials for maintenance works. Industry data suggests average maintenance fees in mass-market condos have increased by 10–20% since 2022. For buyers underwriting their total monthly cost of ownership, this trend means that the maintenance fee is no longer a rounding error — it is a genuine budget line item that deserves the same scrutiny as the mortgage rate.

For investment buyers, maintenance fees directly affect net rental yield. A S$4,500/month rental on a unit with S$600/month in MCST fees represents a net operating yield (before mortgage) of about 3.2% on a S$1.5 million purchase — meaningful compression compared to the gross yield of 3.6%. Understanding and modelling the net yield after maintenance and sinking fund is essential for any investment analysis.

What Might Come Next

The COB has been increasingly attentive to poorly managed MCSTs. In 2024, the Building and Construction Authority (BCA) and COB jointly issued updated guidance on sinking fund adequacy, pushing MCSTs toward more rigorous 5-year planning. There is also ongoing discussion in the property management industry about whether the statutory minimum sinking fund (10% of management fund) is adequate for older developments — some practitioners argue it should be raised to 15–20% for projects over 20 years old. If such a change were legislated, monthly sinking fund levies would rise accordingly. Buyers of properties approaching their 15–20 year mark should factor in this regulatory risk.

Frequently Asked Questions

Can the management fee change from year to year?

Yes. The MCST Council proposes the annual budget at each AGM, and subsidiary proprietors vote on it. If costs have risen — for example, because security guard wages have increased or a landscaping contract was renewed at a higher rate — the management fee will be adjusted upward. Conversely, if the MCST finds cost savings, fees can decrease. In practice, fees rarely decrease; they tend to rise gradually with inflation. Buyers should ask for the last three years of AGM minutes to understand the fee trajectory of any development they are considering purchasing.

What is a special levy and when can the MCST charge one?

A special levy is an extraordinary, one-time contribution that the MCST can demand from all owners to fund urgent capital expenditure that cannot be covered by the existing sinking fund balance. Special levies require approval by a resolution at a general meeting (either an AGM or an Extraordinary General Meeting). They are most common in older developments where the sinking fund is under-provisioned and a major repair (such as lift replacement or waterproofing) is overdue. Special levies can range from S$5,000 to S$50,000 per unit depending on the size of the development and the scope of work. For this reason, checking the sinking fund balance before purchasing is critical.

Do maintenance fees apply to Executive Condominiums (ECs)?

Yes. Executive Condominiums are privately managed after the 10-year mark and are subject to the same BMSMA rules as private condominiums. During the initial period when HDB retains certain oversight, the management corporation is still constituted and maintenance fees apply from the date of key collection. EC buyers should budget for maintenance fees in the same way as any private condo buyer. EC maintenance fees are often somewhat lower than comparable private condos because ECs are typically built without the premium facilities found in luxury private developments, but the difference is not dramatic for mass-market comparisons.

Can landlords pass maintenance fees on to tenants?

In Singapore’s private residential tenancy market, there is no legal prohibition on a landlord including maintenance fees in the rent (i.e., charging a gross rent inclusive of the condo fee). In practice, however, most residential leases are structured on a net basis — the landlord pays the MCST contributions from the rental income and quotes the rent as an all-in figure. Some tenancy agreements explicitly state that maintenance fees are the landlord’s responsibility. Whatever the arrangement, the legal obligation to pay the MCST remains with the owner — the MCST cannot pursue the tenant for arrears.

How does share value affect my monthly levy?

Share value is a fixed integer assigned to each lot in the strata title plan at the time of development. It is broadly proportional to floor area but is also influenced by unit type and usage. A larger unit will have a higher share value and therefore pay a proportionally higher monthly levy. Share value cannot be changed by the MCST — it is set in the strata plan lodged with SLA and can only be altered by a unanimous resolution of all subsidiary proprietors followed by an amendment to the strata plan. Before buying, you can find out a unit’s share value by requesting the strata title plan from the developer, property agent, or MCST.

Is the sinking fund transferable when I sell?

No. The sinking fund belongs to the MCST, not to any individual owner. When you sell your unit, the accumulated sinking fund contributions you have made over the years remain with the MCST for the benefit of the development as a whole. You do not receive a refund of your share of the sinking fund balance on completion of sale. This is one reason why buying into a development with a healthy, well-funded sinking fund is in your interest even if you plan to sell within a few years — the sinking fund supports the quality of the common property, which in turn supports property values.

Where can I find out the exact maintenance fee before I buy?

For new launch condominiums, the developer is required to provide an estimated monthly maintenance fee in the sales documentation. For resale condos, the actual fee is best confirmed by requesting a copy of the latest MCST notice of contribution (which sets out the monthly levy per share value) or by asking the seller’s lawyer to conduct an MCST search. The MCST search will confirm the contribution rate, any arrears on the specific unit, and the sinking fund balance. This search is a standard step in any Singapore property conveyancing and costs approximately S$150–S$200.

Related Articles

- Singapore Home Loan Complete Guide 2026: Rates, TDSR, MSR and How to Choose

- Buyer’s Stamp Duty Singapore 2026: Complete Guide to BSD Rates, Calculation and Remissions

- Singapore Property Investment Guide 2026: Strategies, Yields and Market Outlook

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore En Bloc Guide 2026: How Collective Sales Work and What Owners Should Know

- Singapore Renovation Cost Guide 2026: HDB, Condo and Landed Budgets Explained

Disclaimer: This article is for general informational and educational purposes only and does not constitute legal, financial, or property management advice. MCST contribution rates, sinking fund balances, and BMSMA requirements are subject to change and vary by development. Always verify actual maintenance fees with the relevant MCST, confirm current statutory requirements with the Commissioner of Buildings (HDB Strata Management portal), and obtain independent legal and financial advice before purchasing any property. LovelyHomes is not a licensed property management, legal, or financial advisory firm.