Singapore Landlord Guide 2026: Rental Income Tax, Tenancy Agreements, Property Tax and Landlord Rights

Quick Answer: Singapore Landlord Key Facts 2026

- Rental income is taxable: Resident landlords pay progressive income tax (0–22%) on net rental income after allowable deductions. Non-residents pay a flat 24% on gross rent.

- Allowable deductions include: mortgage interest, property tax, fire insurance, maintenance and repair costs, and agent letting fees. Furniture, renovation, and capital improvements are not deductible.

- Property tax on rental property: the Non-Owner-Occupied (NOO) progressive rate applies — from 10% on the first S$30,000 of Annual Value up to 24% on amounts above S$75,000 (IRAS, from 1 January 2024).

- Stamp duty on tenancy agreement: 0.4% of total rent for leases of one year or less; tiered rates for longer leases. Must be stamped via IRAS within 14 days of signing.

- HDB landlords must complete their Minimum Occupation Period (MOP) — 5 years for standard flats, 10 years for Plus/Prime BTO — and obtain HDB’s written approval before renting out the entire flat.

- Short-term rentals (e.g. Airbnb): prohibited for all residential properties in Singapore. Minimum rental term is three consecutive months under the Planning Act.

- Security deposit: typically one to two months’ rent. Disputes up to S$30,000 can be filed at the Small Claims Tribunal (SCT).

What Does It Mean to Be a Landlord in Singapore?

A landlord in Singapore is any person or entity that lets a residential property to a tenant in exchange for rent. The term covers the full spectrum: from an HDB flat owner renting out a spare bedroom, to a property investor managing a portfolio of private condominiums in the Core Central Region.

Singapore’s rental market is regulated by multiple government bodies. The Inland Revenue Authority of Singapore (IRAS) collects income tax on rental proceeds and administers stamp duty on tenancy agreements. The Housing and Development Board (HDB) regulates the subletting of public housing flats. The Urban Redevelopment Authority (URA) sets rules for private residential properties, including the minimum rental period. The Building and Construction Authority (BCA) governs strata management corporations (MCSTs) for condominiums. Understanding who regulates what is the first step to staying compliant and protecting your net yield.

Singapore’s residential rental market encompasses an estimated 58,000 private units and 56,000 HDB flats listed for rent at any given time. With median gross rental yields at 2.5–3.5% for condominiums and 3.5–4.5% for HDB flats (indicative 2026 figures), understanding the full cost and compliance picture is essential for any landlord.

Rental Income Tax: What Landlords Owe IRAS

Rental income received by a Singapore tax resident is assessable income under the Income Tax Act 1947. It must be declared on IRAS Form B1 (individuals) or Form B (self-employed persons and those with non-employment income) by 15 April each year, covering income from the preceding calendar year.

IRAS defines rental income broadly: monthly rent, any payment for the right to use the property, furniture rent charged separately, and even a lump-sum premium or key-money received at the start of a tenancy are all assessable.

Resident Landlords: Net Income After Allowable Deductions

For Singapore tax residents, the taxable base is net rental income: gross rent received less the following allowable deductions recognised by IRAS:

- Mortgage interest: interest on the loan used to purchase the property. Principal repayments are not deductible. For joint owners, only the portion of interest proportional to each individual’s share applies.

- Property tax: the annual IRAS property tax bill for the rented property.

- Fire and landlord insurance premiums taken out on the property.

- Maintenance and repair costs: reasonable wear-and-tear repairs — replacing broken fixtures, repainting between tenancies. Capital improvements that enhance property value are not deductible.

- Agent letting commission: the fee paid to a property agent for sourcing the tenant. Typically one month’s rent for a two-year lease, deductible in the year paid.

Net rental income is then added to the landlord’s total chargeable income and taxed at the applicable progressive resident rates: 0% on the first S$20,000, rising to 22% on amounts exceeding S$320,000.

Non-Resident Landlords: Flat-Rate Tax on Gross Rent

Non-resident individuals — for example, a foreigner who owns Singapore property but is not tax-resident here — are taxed at a flat rate of 24% on gross rent, with no deductions permitted. Non-residents may elect to be taxed at the resident progressive rates if this produces a lower liability, subject to IRAS rules. Where tax is withheld by a tenant, the landlord is responsible for ensuring accurate filing.

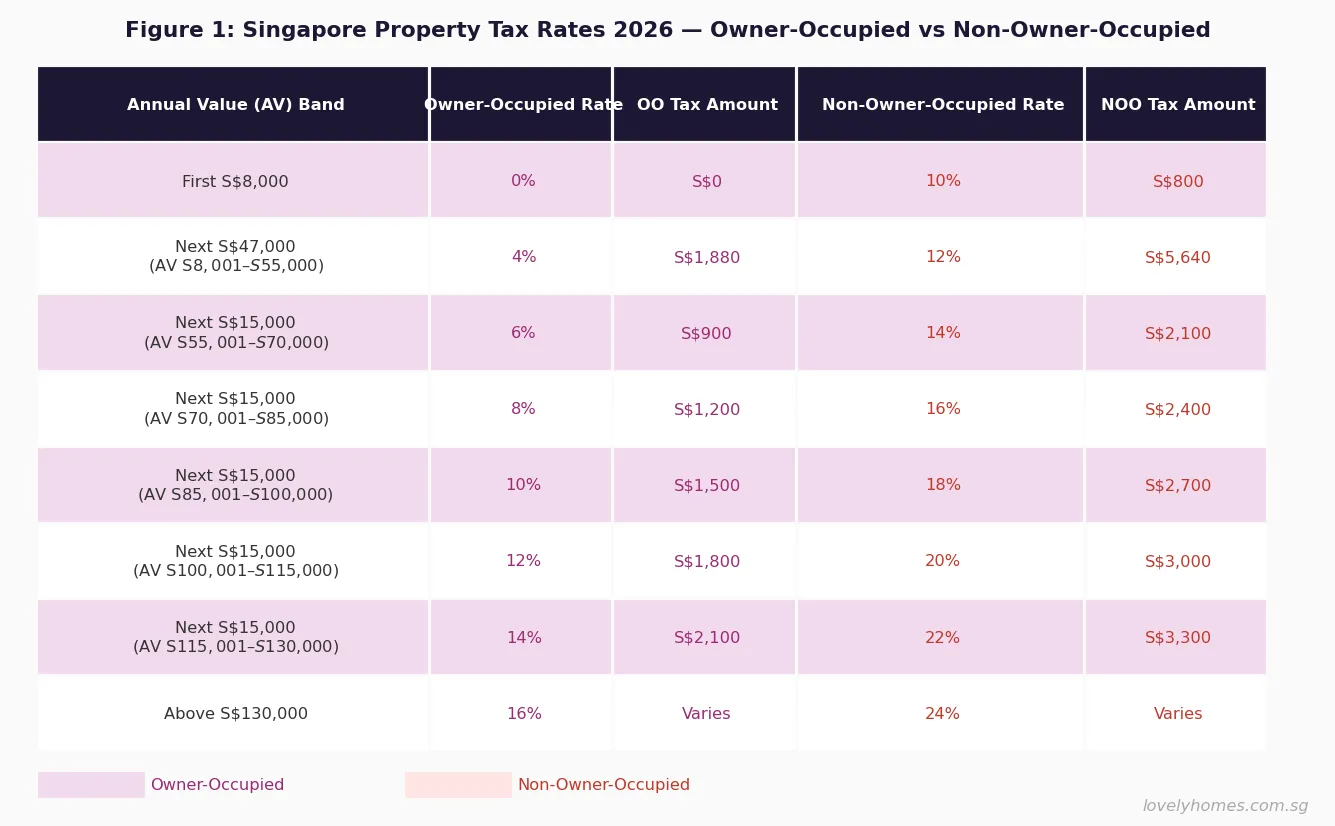

Property Tax for Landlords: The NOO Rate

Every property owner in Singapore pays property tax, regardless of whether the property is occupied or rented. When a residential property is rented out, the Non-Owner-Occupied (NOO) progressive rate applies — substantially higher than the owner-occupied (OO) rate. This differential is a deliberate policy to discourage speculative property holding.

The NOO rate is applied to the property’s Annual Value (AV) — IRAS’s estimate of the property’s annual market rent if let unfurnished. The AV is reviewed periodically. As a reference: a typical 4-room HDB flat in a mature estate carries an AV of approximately S$16,000–S$22,000; a mid-range condominium 2-bedroom unit in the Rest of Central Region may carry an AV of S$28,000–S$40,000. NOO property tax for a condo unit with AV S$30,000 is approximately S$3,000 per year (IRAS, 2024 rates).

Landlords should budget for this cost at the start of each financial year. IRAS issues property tax bills in December for the following year; the due date is 31 January.

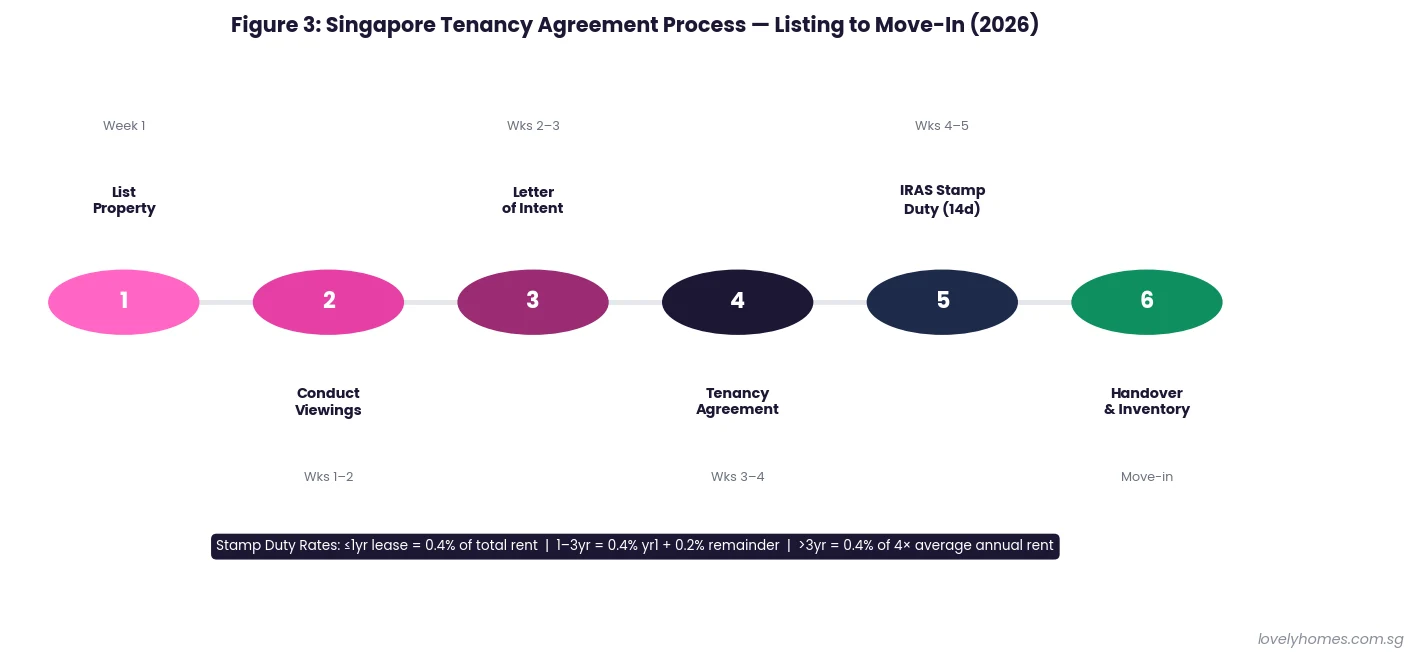

Stamp Duty on Tenancy Agreements

A tenancy agreement is a dutiable document under the Stamp Duties Act. Stamp duty must be paid via the IRAS myStampDuty portal within 14 days of signing if the document is signed in Singapore, or within 30 days if signed overseas.

The stamp duty rate depends on the length of the lease:

- Lease of one year or less: 0.4% of the total rent for the full lease period.

- Lease of more than one year up to three years: 0.4% of average annual rent for the first year, plus 0.2% of average annual rent for each remaining year.

- Lease of more than three years or indefinite period: 0.4% of four times the average annual rent.

Who pays? By default, the tenant pays. However, landlord and tenant may agree otherwise and should record this in the tenancy agreement. Failure to stamp on time incurs a penalty of up to four times the duty owed.

HDB-Specific Subletting Rules 2026

Owners of HDB flats face a more regulated environment than private property owners. The key rules as at 7 July 2026 are as follows.

Minimum Occupation Period (MOP): A flat owner must complete the MOP before renting out the entire flat. The MOP is five years for standard BTO, resale, and DBSS flats, measured from the date of key collection. For Plus and Prime BTO flats launched from the February 2024 exercise onwards, the MOP is ten years. There is no MOP restriction on renting out individual bedrooms, provided the owner continues to physically reside in the flat.

HDB Approval Required: Before renting out the entire flat, the owner must obtain HDB’s written approval via the HDB Resale Portal. Approval is granted online and must be renewed every three years. Renting out without approval may result in enforcement action, including compulsory acquisition of the flat by HDB.

Eligible Tenants: HDB flats may only be rented to Singapore Citizens, Singapore Permanent Residents, and non-citizens holding a valid long-term or work pass (Employment Pass, S Pass, Work Permit, Dependant’s Pass, Long-Term Visit Pass). Visitors and tourists are ineligible tenants for both entire flats and individual bedrooms.

Occupancy Cap: HDB 1- to 3-room flats: maximum four occupants total. HDB 4-room flats and larger: maximum six occupants. This includes all persons residing in the flat, whether family members, tenants, or sub-tenants.

Short-Term Rentals Prohibited: Renting any HDB flat or private residential unit for periods shorter than three consecutive months is prohibited under the Planning Act. URA enforces this actively; owners face composition fines and court action.

Annual Landlord Costs: What Eats Into Your Yield

A landlord’s gross rent is not the same as net yield. Several recurring cost lines erode returns:

- Agent commission: typically one month’s rent for a new two-year lease. Some landlords negotiate a reduced fee for renewal tenancies.

- Income tax on net rental income: a landlord in the 11.5% marginal bracket with S$20,000 net rental income may pay approximately S$2,300 in tax attributable to rental.

- NOO property tax: significantly higher than OO rates. An HDB 4-room flat with AV S$18,000 incurs approximately S$1,800/year at NOO rates; a condominium 2BR with AV S$30,000 incurs approximately S$3,000/year.

- MCST maintenance fees (condo landlords): typically S$200–S$600/month. These continue even during vacancy periods and cannot be passed to tenants unless contractually agreed.

- Void periods: vacancy between tenancies reduces annual yield. In 2026, average void periods range from two to eight weeks depending on property type, location, and prevailing demand.

Summary: Key Landlord Obligations at a Glance

| Obligation | Authority | Requirement | Penalty for Non-Compliance |

|---|---|---|---|

| Declare rental income | IRAS | Form B / B1, by 15 April annually | Penalty, back taxes, and interest |

| Stamp tenancy agreement | IRAS | Within 14 days of signing | Up to 4× stamp duty owed |

| HDB subletting approval | HDB | Before renting out entire HDB flat | Compulsory acquisition possible |

| Minimum 3-month rental period | URA | All residential properties | Composition fine; court action |

| Pay property tax (NOO rate) | IRAS | Annual bill; due 31 January | 5% surcharge on arrears |

| Maintain structure and fittings | Common law | Quiet enjoyment and habitability | Tenant may withhold rent or sue |

| Register HDB tenants | HDB | Register via HDB Resale Portal | Warning and enforcement action |

Worked Example: Mr Ng Rents Out His 4-Room HDB in Bishan

Mr Ng (Singapore Citizen) owns a 4-room HDB flat in Bishan. He completed his MOP in August 2023 and obtained HDB subletting approval in September 2023. He rents the entire flat to a Korean couple on Employment Passes for S$3,000/month on a two-year lease commencing 1 October 2023.

Annual gross rental income: S$3,000 × 12 = S$36,000.

Allowable deductions for Year of Assessment 2024:

- Mortgage interest (HDB loan S$350,000, approximately 25 years remaining, ~3.2% annual interest): S$11,200

- NOO property tax (AV S$18,000, first S$18,000 at 10%): S$1,800

- Fire and landlord insurance: S$380

- Maintenance and minor repairs: S$720

- Agent letting commission (1 month, amortised over 2-year lease): S$1,500

Total deductions: S$15,600. Net rental income: S$20,400.

Stamp duty on tenancy (paid by tenant): 2-year lease, total rent S$72,000. Stamp duty = 0.4% × S$36,000 (Year 1) + 0.2% × S$36,000 (Year 2) = S$144 + S$72 = S$216.

Income tax on rental income: Mr Ng’s total chargeable income (employment income S$82,000 + net rental S$20,400 = S$102,400). Tax at resident rates: approximately S$5,920. Rental’s share (~20%): approximately S$1,184 attributable to rental income.

Why This Matters for Singapore Landlords in 2026

The Singapore rental market has undergone significant structural change since 2022. Post-COVID demand from expatriates pushed prime condominium rents 30–40% above 2019 levels by 2023. By 2025–2026, those gains moderated as a record Government land sales pipeline — 9,320 units in the 2026 Confirmed List alone — fed new supply into the market. HDB rents similarly softened by 4–8% in 2025 as demand normalised.

The HDB Resale Price Index fell for a second consecutive quarter in Q2 2026 (to 202.7, down 0.3% quarter-on-quarter), a sign of broader market softening that affects rental demand confidence. For landlords, pricing discipline and tenant retention matter more than they did in the peak years.

Compared with other regional cities, Singapore stands out for regulatory transparency: IRAS publishes clear guidance on rental tax, HDB’s portal is fully digital, and Small Claims Tribunal procedures are accessible to ordinary landlords and tenants alike. The administrative burden is manageable for compliant landlords who treat property rental as the regulated business activity it is.

What Might Come Next

Several policy developments are worth monitoring. The Government’s ongoing BTO completions in Tengah, Bidadari, and Bayshore — adding more than 30,000 units through 2027–2028 — will sustain downward pressure on HDB resale and rental prices in the medium term. IRAS is also expected to review Annual Values for private residential properties in late 2026, reflecting the more moderate rental market of 2025; any downward revision would reduce NOO property tax bills.

There are ongoing policy discussions about whether to introduce more formal licensing requirements for private residential landlords, similar to frameworks in the United Kingdom and Australia. No formal proposal has been tabled as at July 2026, but landlords with multiple properties should monitor parliamentary proceedings and Ministry of National Development announcements closely.

Frequently Asked Questions

Do I need to declare rental income if I am only renting out a spare bedroom?

Yes. Any payment received for the right to use your property — including a single bedroom — is assessable rental income. You may claim deductions proportional to the rented area (for example, 25% of mortgage interest and property tax if one of four rooms is let). Declare on Form B1 by 15 April. There is no de minimis exemption threshold for rental income in Singapore.

Can I use CPF to pay my property tax or income tax on rental income?

No. CPF Ordinary Account (OA) funds may only be used for specific property-related payments: the downpayment, monthly mortgage instalments, and Buyer’s Stamp Duty on purchase. Annual property tax, income tax on rental proceeds, agent commissions, and all other landlord costs must be paid in cash. This is a common point of confusion for first-time landlords.

What can I do if my tenant stops paying rent?

First, issue a formal written notice of the breach and allow a reasonable cure period (typically 14 days). If unpaid rent does not exceed S$30,000, the Small Claims Tribunal (SCT) provides a faster and lower-cost route than the civil courts. For larger amounts, a civil suit in the District Court or High Court may be necessary. The landlord may also apply for a Writ of Distress to seize the tenant’s goods. The security deposit held may be applied against arrears at the end of the tenancy, but not unilaterally mid-lease unless the agreement expressly permits this.

Do I need HDB approval to rent out a bedroom in my flat before completing the MOP?

The MOP restriction applies only to renting out the entire flat. Before completing the MOP, you may rent out individual bedrooms, provided you continue to physically reside in the flat alongside the tenants. You must still register the subletting of bedrooms with HDB via the Resale Portal. Tourists and visitors without valid passes remain ineligible as tenants for rooms as well as for entire flats.

Is the security deposit I receive from a tenant taxable income?

No, not when received. A security deposit is a refundable sum held as security against the tenant’s obligations; it is not income at the point of receipt. However, if you legitimately forfeit all or part of the deposit — for example, because the tenant terminated early and the agreement entitles you to retain one month as a penalty — the forfeited amount becomes assessable income in the year of forfeiture and must be declared to IRAS.

Can foreigners rent HDB flats in Singapore?

Foreigners may rent HDB flats provided they hold a valid long-term pass. Eligible pass types include the Employment Pass (EP), S Pass, Work Permit, Dependant’s Pass (DP), and Long-Term Visit Pass (LTVP). Tourists and visitors on Social Visit Passes, Student’s Passes used for short stays, and persons without a valid pass are not eligible tenants for HDB flats — whether for an entire flat or a room. The HDB Resale Portal enables flat owners to verify a prospective tenant’s eligibility before signing.