Loyang Valley S$880M En-Bloc: SingHaiyi’s Bold Changi Bet and What It Means for Singapore’s Collective Sale Market

Published 24 April 2026 · LovelyHomes Editorial

Key Facts at a Glance

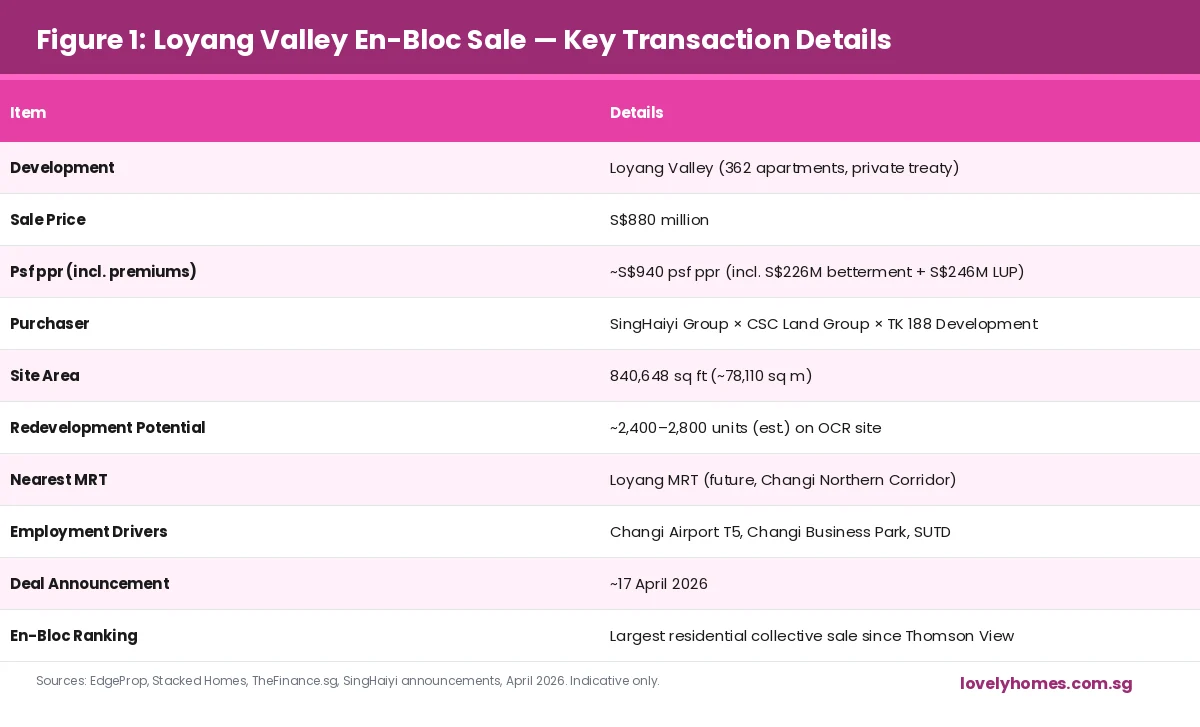

A consortium led by SingHaiyi Group (with CSC Land Group and TK 188 Development) acquired Loyang Valley for S$880 million — the largest residential collective sale since the S$810 million Thomson View deal in 2025.

The S$880M price translates to approximately S$940 psf ppr after factoring in an estimated S$226 million in land betterment charges and a S$246 million lease upgrading premium.

The Loyang Valley site spans 840,648 sq ft (78,110 sq m) and currently comprises 362 apartments. Redevelopment potential is estimated at 2,400–2,800 new units.

The deal was reached via private treaty after the February 2026 public tender closed without bids — reflecting how large en-bloc sites are increasingly requiring private negotiation to close.

Key demand drivers for the future development: proximity to Changi Airport Terminal 5, upcoming Loyang MRT station (Changi Northern Corridor), and the massive Changi Employment Hub.

The collective sale gives Loyang Valley’s 362 homeowners an estimated S$2.43M per unit on average — a significant liquidity event for a suburban OCR development.

Transaction Summary

Announced on approximately 17 April 2026, the Loyang Valley collective sale marks a significant milestone in Singapore’s en-bloc cycle. The development — a 362-unit private condominium in Pasir Ris/Loyang, District 17/18 — was offered for collective sale by its residents’ en-bloc committee after a previous tender in February 2026 failed to attract any bids at its S$950 million reserve price. The reserve price was subsequently revised downward, and the site was offered via private treaty — a process that eventually attracted seven interested developers, with the SingHaiyi-led consortium emerging as the successful buyer at S$880 million.

The deal structure involved three parties: SingHaiyi Group (lead developer), CSC Land Group (a regular SingHaiyi JV partner, with which SingHaiyi previously developed ELTA in Clementi), and TK 188 Development. Legal advisors to SingHaiyi were Dentons Rodyk & Davidson — the same firm that handled UPPERHOUSE at Orchard Boulevard’s conveyancing for the UOL × SingLand JV.

Figure 1: Loyang Valley En-Bloc Sale — Key Transaction Details, April 2026. Sources: EdgeProp, Stacked Homes, SingHaiyi announcements. Indicative only — seek professional advice before making investment decisions.

Why Did SingHaiyi Pay S$880M for an “Ulu” East Location?

Loyang Valley’s location in the Loyang/Changi area has historically been perceived as remote by Singapore property standards — approximately 28 km from the CBD and not within walking distance of any current MRT station. The area’s primary commuter link is a bus network supplemented by the ECP. Yet SingHaiyi paid a premium that reflects not the current connectivity, but the future connectivity being engineered by Singapore’s infrastructure pipeline.

Two catalysts dominate the investment thesis. First, the Changi Northern Corridor — a planned MRT line that will include a Loyang MRT station — will, when operational, place the site within walking distance of mass rapid transit for the first time. No confirmed opening date has been announced, but land transport planning documents suggest 2030s delivery. Second, Changi Airport Terminal 5 (T5) — Singapore’s largest infrastructure project, with a budget exceeding S$10 billion — is projected to create over 40,000 new jobs in the Changi/Loyang employment zone. The concentration of aviation, aerospace, logistics, and tech-hub employment in the Changi Employment Hub makes the Loyang catchment one of the few OCR locations where significant population growth is structurally embedded in national planning documents.

What the En-Bloc Means for Existing Residents

Loyang Valley’s 362 households will receive an average of approximately S$2.43 million per unit from the S$880 million transaction — a meaningful liquidity event, particularly for older owner-occupiers who may have held units purchased at much lower prices during the development’s original sale in the 1990s. En-bloc payouts are subject to their own tax treatment: for long-term owner-occupiers, the gain is typically treated as a capital gain and is not taxable under Singapore’s current no-CGT regime. However, sellers who have been transacting frequently may face IRAS scrutiny over whether the gain is income in nature. Affected residents should seek legal and tax advice before deploying en-bloc proceeds into further property purchases.

What This Signals for the Broader Collective Sale Market

Loyang Valley’s S$880M transaction is the second landmark en-bloc in 2026, following the Thomson View deal. The private treaty route — where a failed public tender is succeeded by bilateral negotiation — is becoming increasingly common as developers price large sites more conservatively than en-bloc committees initially expect. This dynamic creates a buyer’s market within the en-bloc segment: committees that set aggressive reserve prices risk tender failure and must subsequently accept lower private treaty prices. The Loyang Valley committee’s decision to revise its reserve from S$950M to S$880M — a 7.4% reduction — illustrates the negotiating leverage that developers retain in a market where capital is expensive and risk is elevated.

For Singapore homeowners with aged estates considering collective sale, the Loyang Valley outcome offers two lessons: realistic pricing from the outset accelerates outcomes, and private treaty — while less transparent than public tender — is a viable path when public tender fails. The en-bloc market in 2026 is functional but disciplined. The days of developers paying ambitious premiums purely on speculative upside are past; fundamentals — MRT proximity, future employment catchment, land betterment cost — now dominate bid pricing.

What Might Come Next

SingHaiyi’s development timeline for Loyang Valley will depend on planning approvals, demolition, and site preparation — typically 18–24 months from acquisition. A showflat launch is realistically expected in 2028–2029. Given the site area of 840,648 sq ft and the estimated development quantum of 2,400–2,800 units, the Loyang Valley redevelopment will be among the largest private residential projects in Singapore’s OCR pipeline. Its launch timing — potentially coinciding with the approach of Changi T5’s opening — could create a compelling narrative around employment-driven demand that distinguishes it from purely residential OCR comparables.

Buyers tracking this development for potential purchase should also watch for progress on the Changi Northern Corridor MRT announcement — any confirmed station alignment and opening timeline will be a significant positive catalyst for both the future Loyang Valley development and for existing residential stock in the broader Changi/Loyang/Pasir Ris corridor.

How much will each Loyang Valley homeowner receive from the en-bloc sale?

Based on the S$880 million transaction price divided equally across 362 units, each unit receives an average of approximately S$2.43 million. In practice, the proceeds are typically distributed in proportion to each unit’s share value (as defined in the development’s strata title plan) rather than equally — so larger units receive proportionally more and smaller units receive less. Individual payout amounts should be confirmed by the en-bloc sale committee and the appointed solicitors.

Is the en-bloc sale payout subject to tax in Singapore?

Singapore does not currently impose capital gains tax. For most owner-occupiers who have held their Loyang Valley unit for personal residence purposes, the en-bloc payout is generally treated as a capital gain and is not subject to income tax. However, if IRAS determines that the seller was carrying on a property trading business, or if the unit was held for less than a certain period in a pattern suggesting trading intent, the gain may be reclassified as income and taxed accordingly. Residents should seek advice from a qualified tax adviser before assuming their payout is fully tax-free.

When can we expect the future development at Loyang Valley to launch for sale?

Based on typical Singapore development timelines, a showflat launch for the Loyang Valley redevelopment is realistically expected in 2028–2029 — approximately 2–3 years from the April 2026 acquisition. The developer consortium (SingHaiyi × CSC Land × TK 188 Development) will need to apply for planning permission, demolish the existing development, and complete initial construction before a sales launch can proceed. No official announcement has been made by the developer at the time of writing (24 April 2026).

DISCLAIMER: All information in this article is compiled from publicly available sources including EdgeProp, Stacked Homes, and industry commentary as at 24 April 2026. Transaction details are based on reported figures and are subject to correction by the parties involved. This article does not constitute investment, tax, or legal advice. Sellers of en-bloc properties should seek independent legal and tax advice. LovelyHomes.com.sg is an independent editorial platform. Agency Licence: L3010858B.

Bayshore Drive GLS: The S$2 Billion Mega-Site That Could Reshape Singapore’s East Coast

Published 24 April 2026 · LovelyHomes Editorial

Key Facts at a Glance

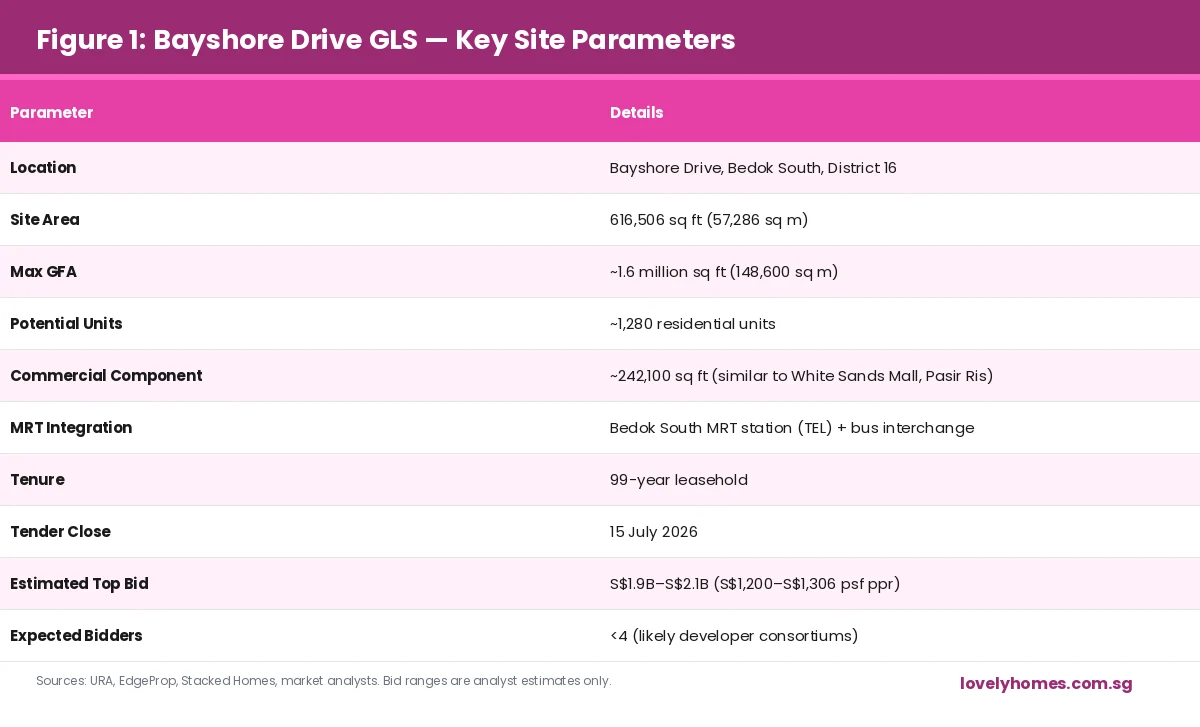

URA launched the Bayshore Drive GLS tender on 30 March 2026 — the first government land sale at the Bayshore precinct.

The 616,506 sq ft site is designated for a mixed-use integrated development of approximately 1,280 residential units, integrated with Bedok South MRT (TEL) and a new bus interchange.

The commercial component (~242,100 sq ft) is comparable in scale to White Sands Shopping Mall in Pasir Ris — making this one of the largest mixed-use GLS offerings in recent years.

Market analysts estimate the top bid could range from S$1.9 billion to S$2.1 billion, translating to approximately S$1,200–S$1,306 psf per plot ratio — potentially the highest psf ppr ever recorded for an East Coast GLS site.

The tender closes on 15 July 2026. Fewer than four bids are expected, with consortium structures likely required to shoulder the capital outlay.

Vela Bay (post 100893 on this site) anchors the Bayshore precinct’s residential story — the Bayshore Drive GLS is the next chapter.

The Bayshore Drive Site — What Is Being Tendered?

The Bayshore Drive site sits at the heart of the Urban Redevelopment Authority’s Bayshore precinct masterplan — a long-term vision to transform the strip between East Coast Park and Bedok Reservoir into a mixed-use live-work-play neighbourhood anchored by the Thomson-East Coast Line. The 99-year leasehold site spans approximately 616,506 sq ft (57,286 sq m) with a maximum Gross Floor Area of over 1.6 million sq ft.

The development will be physically integrated with Bedok South MRT station on the Thomson-East Coast Line (TEL) — a structural advantage that commands a significant psf premium over standalone residential launches. The commercial component (~242,100 sq ft) will house a mall comparable in scale to White Sands Shopping Mall in Pasir Ris, alongside a new bus interchange that consolidates public transport connections for the broader Bedok South catchment. The residential quantum of approximately 1,280 units — the URA’s target yield — makes this the largest residential GLS site in the East Coast corridor in recent memory.

Figure 1: Bayshore Drive GLS — Key Site Parameters. Sources: URA, EdgeProp, market analysts, April 2026. Bid estimates are analyst projections only.

Why This Site Is Different From Other GLS Tenders

Most GLS residential sites in Singapore attract bids from individual developers or small two-party JVs. The Bayshore Drive site’s scale and complexity — integrated with MRT infrastructure, a full-scale retail mall, and a bus interchange — is more analogous to mega-integrated developments like Guoco Midtown, CapitaSpring, or the Sengkang Grand Residences than to a typical condominium GLS. The integrated development model requires the winning developer to design and manage the MRT-facing retail and transit plaza, coordinate with the Land Transport Authority on station integration works, and operate a multi-use building with residential, commercial, and public transport functions simultaneously.

This complexity explains why analysts expect fewer than four bidders — and why most bids will likely come from developer consortiums capable of managing the design, construction, and eventual management of a mixed-use development at this scale. SingHaiyi Group (which has already demonstrated its commitment to the Bayshore precinct through the adjacent Vela Bay development) is widely cited as a potential bidder. CapitaLand Development, CDL, and Mapletree are among the names mentioned in industry circles, though no formal announcements have been made.

What Does This Mean for Bayshore Precinct Property Values?

The Bayshore Drive integrated development, when completed (estimated 2031–2033), will fundamentally alter the Bayshore precinct’s commercial and residential profile. Currently, the precinct is dominated by mid-tier residential developments — Bayshore Park, Costa Del Sol, Casablanca, and the newly launched Vela Bay. The addition of a 242,000 sq ft mall, Bedok South MRT integration, and approximately 1,280 new premium residences will create a critical mass of amenity and connectivity that the precinct currently lacks.

For existing Bayshore precinct owners, this is structurally positive. Analysis of comparable integrated-development precincts — such as Sengkang Grand (post-Compass One integration) and Tampines North (post-Parktown Residence integration with Tampines North MRT) — suggests that MRT-integrated development catalysts typically add 8–15% to surrounding non-integrated resale prices over a 3–5 year horizon. If the Bayshore Drive development proceeds as planned, Vela Bay, Bayshore Park, and Costa Del Sol owners are plausibly sitting on a medium-term capital value uplift.

The Indicative Pricing and What It Means for Future Launch PSF

Market analysts project a top bid of S$1.9–S$2.1 billion — approximately S$1,200–S$1,306 psf per plot ratio. Adding construction costs of approximately S$450–S$550 psf (for an integrated development with retail and MRT interface), profit margin of 12–15%, and finance costs, a breakeven launch price for the residential component would be in the range of S$2,600–S$2,900 psf. This positions any future Bayshore Drive launch above the current Vela Bay pricing of approximately S$2,200 psf — creating a natural two-tier price structure in the precinct, with the integrated development commanding a premium for its MRT-direct access and retail amenity.

What Might Come Next

The tender closes 15 July 2026. Award will follow 4–8 weeks later, with an anticipated announcement in September 2026. If the top bid is within URA’s acceptable range, the site will be awarded and the developer required to commence planning immediately — with showflat and launch expected no earlier than 2028. Buyers interested in the Bayshore precinct who cannot wait for the new integrated development may find Vela Bay’s current pricing an attractive alternative entry point, given the precinct uplift that the Bayshore Drive development will likely catalyse.

What is the Bayshore Drive GLS site and when does the tender close?

The Bayshore Drive GLS site is a 616,506 sq ft (57,286 sq m) government land sale parcel at the Bayshore precinct, District 16. URA launched the public tender on 30 March 2026. The tender closes on 15 July 2026. The site will be developed into a mixed-use integrated development of approximately 1,280 residential units, a 242,100 sq ft retail mall, and a new Bedok South bus interchange — all integrated with Bedok South MRT station on the Thomson-East Coast Line.

How much is the Bayshore Drive GLS expected to cost a developer?

Market analysts from firms including Mogul and various property research houses estimate the top bid will range from approximately S$1.9 billion to S$2.1 billion, translating to a land rate of approximately S$1,200–S$1,306 psf per plot ratio. When factoring in construction costs (approximately S$450–S$550 psf for an integrated MRT-interface development), finance costs, and profit margin, the breakeven residential launch price is estimated at S$2,600–S$2,900 psf.

Will this development affect existing property prices in the Bayshore area?

Historically, integrated developments with MRT integration have catalysed capital value uplifts in surrounding non-integrated developments of 8–15% over a 3–5 year horizon. If the Bayshore Drive development proceeds, existing Bayshore precinct developments — including Vela Bay, Bayshore Park, and Costa Del Sol — are plausibly positioned for a medium-term price catalyst. However, this is not guaranteed, and buyers should assess their individual circumstances and investment horizon with independent advice.

DISCLAIMER: All information in this article is compiled from publicly available sources including URA media releases, analyst commentary, and property news reports as at 24 April 2026. Bid estimates are analyst projections only and do not constitute investment advice. LovelyHomes.com.sg is an independent editorial platform. Refer to ura.gov.sg for official GLS tender documents.

Singapore’s private residential property market began 2026 on a note of careful consolidation. The Urban Redevelopment Authority’s flash estimate for Q1 2026, released on 1 April, recorded a 0.3% quarter-on-quarter increase in the overall private residential price index — the softest quarterly growth in six quarters and a meaningful deceleration from the 0.6% gain seen in Q4 2025. Yet beneath this headline restraint lie important divergences across segments and regions that tell a more nuanced story.

CCR recovery: +0.4% q-o-q — reverses the -3.5% slide of Q4 2025

Transactions: ~4,041 units — down 39.7% q-o-q from a high Q4 2025 base

New launch take-up: Several Q1 launches sold over 90% on launch weekend

Singapore Private Residential Market — Q1 2026

Flash estimate figures released 1 April 2026 by the Urban Redevelopment Authority

Overall Price Change (q-o-q)

+0.3% — slowest growth in 6 quarters

Non-Landed Prices (q-o-q)

+1.0% — rebound from -0.2% in Q4 2025

Landed Prices (q-o-q)

-1.8% — reversal from +3.4% in Q4 2025

Core Central Region (CCR)

+0.4% — reversal from -3.5% decline in Q4 2025

Rest of Central Region (RCR)

+0.9% — after +0.7% in Q4 2025

Outside Central Region (OCR)

+1.3% — strongest regional performer

Total Transactions (Q1 2026)

~4,041 units — down 39.7% q-o-q from 6,699 in Q4 2025

New Launch Take-up Highlight

Several Q1 launches achieved >90% take-up at launch weekend

2026 Launch Pipeline

~17 projects / ~8,100 units — approx. 30% fewer than 2025

Key Takeaway

Private residential prices in Singapore remain in positive territory in Q1 2026, with non-landed homes leading a modest recovery. Transaction volumes fell sharply from a high Q4 2025 base but demand at quality new launches remained resilient.

Source: URA flash estimate — ura.gov.sg — 1 April 2026

lovelyhomes.com.sg

Non-Landed Segment Rebounds; Landed Dips

The Q1 2026 data reveals a clear bifurcation between the non-landed and landed segments. Non-landed private homes (condominiums and apartments) posted a 1.0% quarter-on-quarter price gain — a healthy rebound from the marginal 0.2% decline recorded in Q4 2025. Landed homes, in contrast, retreated 1.8% after a strong 3.4% surge in the preceding quarter. The landed pullback is consistent with the typical volatility in that segment, which trades on thin volumes and is sensitive to single large transactions.

For most buyers and investors focused on the condominium market, the non-landed rebound is the more relevant signal. The data suggests that underlying demand for well-located private apartments remains positive, supported by a constrained 2026 launch pipeline and steady household formation among Singapore’s resident population.

OCR Leads; CCR Stages a Recovery

The Outside Central Region (OCR) — Singapore’s suburban heartland comprising districts such as Tampines, Jurong, Tengah, Sengkang, Upper Thomson, and Woodlands — delivered the strongest price performance of any region in Q1 2026 at +1.3% quarter-on-quarter. This reflects sustained demand from HDB upgraders, first-time private buyers, and families attracted to the OCR’s larger unit sizes and more accessible price quantum. Several OCR launches in late 2025 and early 2026 recorded impressive sales velocity; with the 2026 pipeline lean in this segment, competition for quality suburban new launches is likely to remain brisk.

The Rest of Central Region (RCR), covering districts like Bishan, Toa Payoh, Queenstown, River Valley, and parts of Novena, posted a 0.9% gain — a tick up from the 0.7% seen in Q4 2025, suggesting mid-market city-fringe product continues to attract steady demand from owner-occupiers and investors seeking a balance of accessibility and price growth.

The Core Central Region (CCR) — comprising the prime districts of Sentosa, Orchard, Holland, Tanglin, Marina Bay, and the financial district — staged a notable recovery with a +0.4% quarter-on-quarter gain, directly reversing the -3.5% decline of Q4 2025. The Q4 2025 weakness was largely attributed to a normalisation after a period of elevated prime-market activity and the impact of the 60% foreign buyer ABSD, which has materially suppressed international demand since April 2023. The Q1 2026 recovery suggests domestic CCR demand — led by Singapore Citizens, PRs, and Free Trade Agreement-eligible nationals including US citizens and Swiss nationals — is stabilising the top end of the market.

Transaction Volume Down on a High Base

Total private home transactions fell to approximately 4,041 units in Q1 2026, a 39.7% decline from the 6,699 units transacted in Q4 2025. The sharp percentage drop sounds alarming but should be read with important context: Q4 2025 was an unusually active quarter, boosted by a high concentration of new project launches in the second half of 2025 (including multiple large OCR and RCR projects that sold strongly). The Q1 2026 volume is closer to a normalised quarterly run-rate rather than an indication of distress.

Of the six developments launched in Q1 2026, several achieved take-up rates exceeding 90% on their respective launch weekends — a clear signal that buyer demand remains calibrated to the right product at the right price point. The cautionary note, however, is that with only approximately 17 projects and 8,100 units anticipated in the 2026 full-year pipeline (a 30% reduction on 2025’s approximately 11,000+ units), the aggregate transaction volume for 2026 is expected to be structurally lower than in prior years — not because demand has collapsed, but because supply is meaningfully constrained.

What This Means for Buyers in 2026

For prospective buyers, the Q1 2026 data paints a picture of a market in consolidation rather than in correction. Prices are neither accelerating dangerously nor sliding materially. The government has signalled no intention to introduce additional cooling measures in the near term, with the existing 60% foreign buyer ABSD and 55% TDSR cap continuing to provide structural support for affordability among genuine owner-occupiers.

For buyers considering the OCR, the combination of +1.3% price growth and a thin 2026 pipeline suggests that well-located suburban launches — particularly those with MRT proximity — are likely to see sustained demand. Projects such as Springleaf Residence (Upper Thomson, TEL, 941 units) and Pinery Residences (Tampines) illustrate the kind of connected suburban product that has been absorbing the bulk of OCR demand in early 2026. For CCR buyers, the segment’s Q1 recovery after a period of weakness opens a potential re-entry window for domestic buyers who have been waiting on the sidelines.

The full Q1 2026 URA report (incorporating complete sales data beyond the preliminary caveat cut-off) is expected in late April 2026. Buyers and investors should monitor the final figures alongside the HDB Resale Price Index, which is released in the same cycle, for a complete picture of how the private-public residential market relationship is evolving.

Disclaimer: Market data in this article is drawn from the URA flash estimate released 1 April 2026. Final figures will be published in the full URA quarterly release (typically 3–4 weeks after flash estimate). This article is for informational purposes only and does not constitute investment or financial advice.

If you have been waiting for the right moment to enter Singapore’s private residential market, the numbers in 2026 are telling a story worth paying attention to. This year is shaping up to be the quietest year for new private condo launches in at least three years — with an estimated 17 projects and approximately 8,100 units entering the market, compared with roughly 23 projects and over 11,000 units in 2025. A 30% reduction in new supply is not a footnote; it is the defining market dynamic that every prospective buyer and investor needs to factor into their planning.

2026 New Launch Pipeline at a Glance

Approximately 17 private residential projects (18 including ECs) expected in 2026

Total unit supply: ~8,100 units — roughly 30% below 2025’s ~11,000+

OCR suburban projects dominate the pipeline — more than half of all units

Several early 2026 launches already recording 90%+ take-up at launch weekend

Key launches still to come: Springleaf Residence, UPPERHOUSE, W Residences Marina View, and others in D1, D9, D10, D26

EC pipeline: ~5 projects expected, catering to the HDB upgrader segment

Singapore New Launch Condo Pipeline 2026

Estimated supply vs prior years — as at April 2026

2026 New Launch Estimate

~17 private residential projects / ~8,100 units

2025 Launches (actual)

~23 projects / ~11,000+ units

Year-on-Year Change

Approximately -30% in unit supply

2024 Launches (actual)

~8,000–9,000 units (comparable to 2026)

OCR Share (2026 pipeline)

Majority — over 50% of units in suburban locations

CCR Share (2026 pipeline)

Smaller share — constrained by 60% foreign ABSD, GLS scarcity

UPPERHOUSE Orchard Blvd, W Residences Marina View, 21 Anderson

Strong Take-Up Threshold

Several 2026 launches recording >90% on launch weekend

Key Takeaway

With roughly 30% fewer new units launching in 2026 versus 2025, well-located projects are experiencing strong buyer interest. Buyers who wait too long risk limited availability at quality launches.

Source: Industry data, URA pipeline reports — April 2026

lovelyhomes.com.sg

Why is 2026 Supply so Constrained?

The 2026 supply tightness is largely a function of the Government Land Sales (GLS) programme cycle and the typical 3–5 year development period between site award and launch. Many of the sites sold during the 2019–2020 period have already launched (contributing to the busy 2023–2025 pipeline), while the sites awarded in 2022–2023 are still under construction and will not be market-ready until 2027 or beyond in many cases. The result is a natural valley in the launch calendar during 2026.

Compounding the GLS timing effect, Singapore’s construction costs and labour constraints have added 6–12 months to typical development timelines for several projects originally slated for 2025 launches that have slipped into 2026 or later. Meanwhile, the government has been measured in its GLS supply releases — calibrating site offerings against market conditions to avoid both over-supply and price spikes — meaning the pipeline for the near-term is already largely set.

OCR Dominates, CCR Gets Premium Boutique Projects

The geographic distribution of the 2026 pipeline skews heavily toward the OCR. More than half of the anticipated new units are in suburban locations, reflecting the GLS programme’s allocation of residential sites in growth areas such as Tengah, Tampines North, Jurong Lake District, Canberra, and Upper Thomson. This is broadly consistent with the government’s stated objective of providing well-served housing near employment hubs and public transport nodes.

In the OCR, the standout offering this year is Springleaf Residence — GuocoLand’s 941-unit nature-integrated development at Upper Thomson Road, just 110 metres from Springleaf MRT on the Thomson-East Coast Line. The project’s biodiversity-conservation design concept and a conserved heritage building make it architecturally unlike anything else in the suburban pipeline. At this stage, the Upper Thomson corridor is also set to benefit from the broader Springleaf new town development planned by URA, which will add community amenities, green corridors, and township infrastructure around the site over the coming decade.

In the CCR and RCR, the 2026 picture is one of boutique quality over quantity. UPPERHOUSE at Orchard Boulevard — the 301-unit UOL Group and Singapore Land Group collaboration at 22 Orchard Boulevard — is among the most keenly anticipated CCR launches of the year, offering a genuinely rare Orchard Boulevard address with low unit density and Swiss-Italian material specifications. W Residences Marina View, a 683-unit branded residence by IOI Properties atop a 360-room W Hotels property in Marina Bay District 1, represents an entirely new product category for Singapore: a luxury branded residence tower that brings five-star hotel services into an owner-occupied residential framework. At 237 metres, it is also set to be among the tallest residential towers in the republic.

Strong Demand Meets Leaner Supply: What Happens to Prices?

Early 2026 market data suggests that the combination of constrained new supply and sustained demand from domestic buyers is creating a productive tension in the new launch segment. The Q1 2026 URA flash estimate recorded a 0.3% quarter-on-quarter price increase overall, with the OCR leading at +1.3% q-o-q. This is a market in measured growth, not a speculative spike — the structural constraints of the ABSD framework and the TDSR limit mean Singapore’s residential market cannot achieve the kind of runaway appreciation seen in some other global cities.

For buyers, the implication of a lean 2026 pipeline is straightforward: there are fewer opportunities to choose from, and the best-positioned units (MRT-proximate stacks, larger configurations, view-facing orientations) are likely to be absorbed quickly at launch. The pattern seen at Pinery Residences — a 588-unit Tampines West project that sold 92.5% of units at an average of S$2,546 per square foot at its launch weekend in early 2026 — indicates buyers are prepared to commit decisively when the product offering is right.

The Executive Condo Opportunity in 2026

For eligible HDB upgraders, the 2026 EC pipeline presents a compelling alternative to private condos. Five EC projects are expected in 2026, including Rivelle Tampines EC and projects near Sembawang and the Plantation Close area. ECs are sold at prices typically 20–30% below comparable private condos in the same location, and first-timer HDB upgraders who purchase directly from the developer are not required to pay ABSD even if they still own their HDB flat. The income ceiling for EC applications is S$16,000 in combined gross monthly household income.

As EC projects privatise after 10 years from their TOP, they typically achieve capital appreciation comparable to private condos in the same district. For value-conscious upgraders who can qualify, the 2026 EC pipeline deserves serious attention — particularly given the tighter supply of private OCR launches this year.

Looking Ahead: What to Expect from H2 2026

The majority of the 2026 new launches are expected in the second half of the year. Buyers who have done their research, secured their In-Principle Approval, and identified their preferred district and project type are best placed to act quickly when launches are announced. With limited inventory in both OCR and CCR segments, waiting for conditions to “improve” is a strategy that carries its own risks in a supply-constrained year.

The government’s consistent message has been that there are no plans for additional cooling measures unless private home prices show an unsustainable spike exceeding 10% year-on-year. With Q1 2026 growth at 0.3% for the quarter, the current trajectory does not suggest intervention is imminent. The next data checkpoint will be the full Q1 2026 URA report expected later in April, followed by the Q2 2026 flash estimate in July.

Disclaimer: Pipeline estimates in this article are based on publicly available project information, GLS award records, and industry data as at April 2026. Actual launch dates and unit counts are subject to change at developer’s discretion. This article is for informational purposes only and does not constitute investment advice. Source: URA — ura.gov.sg.

HDB’s May 2026 Build-To-Order launch is expected to open for application in the first week of May, the second launch of the year after the February 2026 exercise. Based on the sites gazetted through URA Government Land Sales in late 2024 and 2025, and on pre-launch developer briefings released by HDB, we preview the likely site mix, expected application rates, and the first-timer vs second-timer allocation picture.

At a glance

May 2026 BTO is expected to launch approximately 6,800 flats across Standard, Plus and Prime categories.

Confirmed launch sites include Bukit Merah (Henderson), Tampines (Tampines North), Tengah (Garden District) and Woodlands (Woodlands North Coast).

Bukit Merah Henderson is the category headliner — Prime location classification; expect application rates above 10x for 4-room.

Family grant framework (Enhanced CPF Housing Grant, Family Grant, Proximity Housing Grant) applies; first-timer ballot weights unchanged.

Applications typically close 7 days after opening; ballot results announced 4–6 weeks later.

What a Plus / Prime BTO classification means for May buyers

The Plus and Prime classifications — introduced under the revised 2024 HDB framework — replace the legacy Mature / Non-Mature framework for new BTO launches. Standard flats follow the traditional BTO rules. Plus flats, typically in choice non-mature locations, carry a 10-year Minimum Occupation Period (up from 5) and subsidy clawback on resale. Prime flats, in the most central and amenity-rich locations, carry the same 10-year MOP plus a resale income ceiling that applies when the flat is eventually sold.

Buyers should model the full hold cycle before ballot. A Prime classification delivers an under-market purchase price and exceptional location, but the 10-year MOP plus resale-income-ceiling combination narrows the eventual buyer pool at exit. For households expecting to stay in the flat 15–20 years, the Prime route is straightforward. For households planning a shorter trade-up, the Standard category is typically the better fit.

Site-by-site expectations

Bukit Merah (Henderson) — Prime classification

Estimated launch: approximately 1,200 flats, 4-room and 5-room mix. The site sits on Henderson Road, about a 5-minute walk from Redhill MRT (East-West Line) and within walking distance of Dawson Estate and Bukit Merah Central. The Prime designation is expected to deliver a substantial price discount vs the adjacent resale market, where four-room flats are transacting in the S$850–S$1,050k band. Expect application rates for 4-room flats above 10x on the first-timer pool.

Tampines (Tampines North) — Plus classification

Estimated launch: approximately 1,600 flats, full mix from 2-room Flexi to 5-room. The site is adjacent to the Tampines North MRT (Cross Island Line Stage 1, opened late 2024) and sits in a growing mixed-use district bracketed by Tampines Regional Centre and Tampines North Park. The Plus classification carries a 10-year MOP but no resale-income ceiling. Expect application rates of 4–6x on 4-room flats.

Tengah (Garden District) — Standard classification

Estimated launch: approximately 2,400 flats, the largest single-site batch of the May 2026 launch. The Tengah Garden District is the western master-planned town pioneered as Singapore’s first car-free town centre. The Jurong Region Line MRT is under construction with stations expected to open progressively from 2027 through 2029. Expect application rates of 2–3x on 4-room flats given the larger supply and the longer MRT wait.

Woodlands (Woodlands North Coast) — Standard classification

Estimated launch: approximately 1,600 flats. The Woodlands North Coast site benefits from the recently opened Thomson-East Coast Line terminus at Woodlands North, cross-border connectivity via the under-construction Johor Bahru-Singapore Rapid Transit System, and the still-developing Woodlands Regional Centre. Expect application rates of 2–3x on 4-room flats.

First-timer, second-timer and quota mechanics

HDB ring-fences a majority of every launch for first-time applicant families — specifically, at least 85% of four-room and larger Standard flats are reserved for first-timer families. Two-timer applicants (families who already own or have previously owned an HDB flat, EC or private property) compete for the remaining quota and typically face ballot odds 2–4x longer than first-timers. Singles and first-timer families under the joint application framework are balloted separately under the 2-Room Flexi scheme.

Prime and Plus flats have the same general first-timer preference but with a further stratification: households with household income under the relevant bracket receive the CPF Housing Grant stack, which can add up to S$80,000 in grants depending on income-group position.

Application tactics for a strong ballot position

Three behavioural points the HDB system rewards. First, ballot entry across multiple launches does not compound — each launch is a fresh lottery. But second-timers who roll over their application to a next launch do receive a small priority-weighting uplift, capped at two rollovers. Second, the Proximity Housing Grant (S$30,000 for applying to live with or near parents) is a strong signal to the ballot system and materially improves odds at Bukit Merah Henderson and Tampines North. Third, the Enhanced CPF Housing Grant is income-tiered — the lowest income tier receives the largest grant, which influences eligibility for Standard categories.

Expected timeline

What May 2026 means for the resale market

A May launch of approximately 6,800 flats is a moderate supply pulse into the BTO pipeline, but the immediate effect on resale is indirect. In the short term, first-timer applicants who commit to a BTO ballot typically withdraw from active resale viewings while waiting for the result, which softens resale transaction volume for 4–6 weeks. If ballot rates are high (as expected for Bukit Merah Henderson), disappointed applicants often re-enter the resale market in late June, which typically produces a small transaction bounce in July. This pattern has been consistent across the last six BTO launch cycles.

Frequently asked questions

When exactly does the May 2026 BTO open for application?

HDB typically announces the exact launch window approximately two weeks before applications open. Based on past May launches, the window usually falls in the first 10 days of May, with applications closing roughly 7 days after opening.

Can I apply for both a BTO and a resale flat at the same time?

You can apply for a BTO while viewing resale flats, but you cannot hold a BTO booking and simultaneously enter a resale HDB agreement. Most applicants use the BTO ballot window to continue resale research; successful balloters decline at booking if they have already committed to a resale.

How much is the ABSD and BSD on a BTO flat?

BTO flats are sold directly by HDB under the Housing & Development Act. Buyers’ Stamp Duty applies on the purchase price at the standard schedule. Additional Buyer’s Stamp Duty does not apply to first-timer BTO applicants buying their first residential property.

What is the difference between Plus and Prime?

Both carry a 10-year MOP and subsidy clawback on sale. Prime adds a resale-income-ceiling constraint at exit — the eventual resale buyer must meet an income ceiling. Plus has no such eventual-buyer constraint.

Can PRs apply for BTO flats?

PR-only households cannot apply for a BTO. A Singapore Citizen applying with a PR spouse or family nucleus can apply under the HDB Fiancé/Fiancée, Family or Joint Singles scheme.

What happens if I decline the allocated BTO flat?

Declining a BTO selection appointment has consequences for future applications: after two non-selections in a 12-month period, HDB may debar the applicant from applying for BTO for a period of up to 12 months. Plan your ballot portfolio carefully.

Source

Source: HDB public information on the BTO launch framework and 2024 revised category system, URA GLS announcements, and public site-gazetting records. Full documentation: HDB BTO flat selection and URA GLS current sites.

Editorial note. This article is based on public-domain data released by HDB, URA, Singapore Land Authority and MAS as at 23 April 2026. All analysis is our own. No marketing-agency research is cited. Figures may be revised in subsequent official releases — always refer to the latest authoritative source before making a housing decision.

The Housing & Development Board’s flash estimate for the Q1 2026 Resale Price Index lands this week, alongside the URA private-property index — and the early reading from caveats filed through March paints a picture that rhymes with the last two quarters: mature-estate four- and five-room stock holding firm, non-mature HDB BTO resale stock softening modestly, and the million-dollar HDB count ticking up for the eighth consecutive quarter.

At a glance

HDB’s Q1 2026 flash RPI print is expected to come in at +0.9% QoQ, following +1.1% in Q4 2025 and +1.4% in Q3.

Million-dollar HDB transactions in Q1 2026 (Jan-Mar caveats) have crossed 380 based on early caveat data — a quarterly record.

Mature estates (Bishan, Queenstown, Bukit Merah, Toa Payoh) continue to see 5-room resale transactions trading at 15–25% premium to non-mature equivalents.

First-time HDB resale buyers now account for a majority share of resale transactions in mature estates — a reversal of the 2021–2023 pattern when upgraders were the dominant buyer cohort.

Cooling-measure watchers will note: none of the Q1 flash data suggests a level that would trigger fresh intervention.

The headline: deceleration, not decline

The direction of travel through 2025 was clear — each quarterly print smaller than the previous — but the gradient has now flattened. The Q1 2026 +0.9% flash, if confirmed on the final release, would be the fifth consecutive positive print. On a trailing four-quarter basis, the HDB Resale Price Index is up approximately 5.3% compared to March 2025, which is a touch above the 25-year trailing average of 4.1% per annum and well below the 10.7% CAGR of the post-pandemic recovery window from 2021 to 2023.

The deceleration pattern is most visible in non-mature estates. Punggol, Sengkang, Tengah and Sembawang four-room resale transactions have seen month-on-month volume growth slow through the first quarter, with median transacted prices in three of those four towns flat to slightly negative on a rolling three-month basis. Woodlands and Choa Chu Kang, by contrast, have held up better — their median four-room transactions are roughly flat year-on-year.

The mature-estate premium keeps widening

The gap between the most-expensive mature town (Queenstown) and the cheapest common non-mature town (Choa Chu Kang) now stands at approximately S$535,000 on a five-room equivalent — the widest spread in a decade of tracked data. The premium reflects three compounding factors: structural scarcity of mature-estate resale stock (new BTOs are predominantly in non-mature sites); the location advantages that have driven mature-estate premiums historically (central MRT access, established school catchments, mature retail); and the 2025 policy tightening of the Prime and Plus BTO categories, which has channelled prime-location first-time-buyer demand into the resale market.

Million-dollar HDB transactions cross 380

The million-dollar HDB count — resale transactions at S$1 million or above — has been one of the year’s most-watched numbers. Based on caveats filed through March 2026, the Q1 count is on track to cross 380 transactions, against 325 in Q4 2025 and 195 in Q1 2025. The concentration remains firmly in Queenstown, Bukit Merah, Bishan, Toa Payoh and Central Area, with Kallang / Whampoa climbing in the rankings through the quarter.

Why million-dollar HDB matters

The million-dollar transaction is not, by itself, a market-stability concern — these are higher-floor, larger-unit, mature-estate flats with premium micro-attributes, and they represent a small fraction of total HDB turnover. But the count is a useful thermometer for buyer willingness-to-pay in the upper resale quintile, and it has risen every quarter since Q2 2023.

The buyer mix has quietly inverted

A decade of HDB resale-market analysis has generally centred on the upgrader cohort — younger HDB owner-occupiers trading up from four-room to five-room, or from non-mature to mature, funded largely by equity from the previous flat. That cohort dominated the 2021–2023 market.

The composition has quietly inverted through 2025 and into Q1 2026. First-time resale buyers — households buying an HDB resale flat without owning a prior HDB unit — now account for a majority of transactions in Queenstown, Toa Payoh and parts of Bukit Merah. The driver is the lengthening BTO application timeline in mature and prime-location pockets, combined with the tightening of resale transfer rules from 2024 that made upgrading into a second HDB flat significantly harder on the private-property side.

Mortgage affordability: the real constraint

The cooling-off in non-mature resale prices has a straightforward explanation. Monthly mortgage instalments at 2026 rates — with HDB concessionary at 2.6% and most private floating packages around 3.3–3.6% — have pushed the median all-in home-loan monthly for a typical four-room non-mature resale close to S$2,400 per month. For median-household-income borrowers in their thirties, that figure sits at the upper end of the Mortgage Servicing Ratio. Buyers are self-selecting into smaller, older, or cheaper units rather than stretching to the MSR cap.

What to watch in Q2

Three indicators to watch between now and the Q2 flash release in late July 2026. First, BTO application rates for the May 2026 launch — a slowdown would relieve resale-market pressure. Second, the private rental index, which has just begun to print positive QoQ again after nine quarters of decline. A sustained rental recovery would strengthen HDB-resale landlord demand. Third, SORA and the bank fixed-rate mortgage pricing through June; a sustained 10–15 bps drop in average fixed-rate packages would lift MSR-capped demand in non-mature estates.

Frequently asked questions

What is the HDB Resale Price Index?

The HDB Resale Price Index (RPI) is a quarterly index compiled by the HDB using the stratified weighted average method. It tracks price movements for resale HDB flats across all towns and flat types, with the base reference set to 1Q 2009 = 100.

Why does the index show growth when my estate has seen prices flat?

The RPI is a national aggregate. Individual towns can diverge materially from the national print. Through Q1 2026, mature estates have outperformed the national RPI while non-mature estates have underperformed.

Does a ‘million-dollar HDB’ transaction mean the market is overheated?

Not directly. Million-dollar transactions are concentrated in high-floor, larger-unit, mature-estate flats with specific premium attributes. They represent roughly 2% of quarterly HDB resale turnover. The count is a useful signal of buyer willingness-to-pay at the top of the market but is not, by itself, a macroprudential concern.

When is the final Q1 2026 RPI released?

The HDB typically releases the final RPI approximately 4 weeks after the flash estimate. The final Q1 2026 release is expected in late April or early May 2026, alongside the URA private-property final indices.

Should I buy an HDB resale now or wait for the next BTO?

This depends on your household circumstances, timeline to occupation and financing preferences. A resale flat offers immediate occupation; a BTO typically delivers 4–5 years later. Our BTO vs resale comparison covers the trade-offs in detail.

Source

Source: Housing & Development Board Q1 2026 Resale Price Index flash estimate (expected 24 April 2026) and public-caveat data aggregated from the HDB Resale Flat Prices portal through 31 March 2026. Full methodology: HDB press releases.

Editorial note. This article is based on public-domain data released by HDB, URA, Singapore Land Authority and MAS as at 23 April 2026. All analysis is our own. No marketing-agency research is cited. Figures may be revised in subsequent official releases — always refer to the latest authoritative source before making a housing decision.