Jurong West Neighbourhood Guide Singapore 2026: Property Prices, Schools, JRL MRT and Investment Outlook

Click anywhere or press Esc to close

Jurong West is Singapore’s largest public housing new town by residential population — a sprawling western estate in District 22 (D22) that has evolved from its early industrial-adjacent origins into a well-equipped, MRT-connected community. Long viewed as a budget-friendly OCR option for first-time buyers and HDB upgraders, Jurong West is now attracting a broader investor audience, driven by the transformative Jurong Lake District (JLD) masterplan and the incoming Jurong Region Line (JRL).

This guide covers everything buyers, investors, and tenants need to know about Jurong West property in 2026: HDB and condo prices, MRT network, schools, lifestyle amenities, rental yields, capital growth prospects, and a full buyer worked example.

Quick Answer: Key Facts About Jurong West

- District: D22 (Jurong West, Boon Lay, Pioneer, Taman Jurong)

- MRT access: EWL — Lakeside, Chinese Garden, Boon Lay, Pioneer, Joo Koon; JRL opening from 2027; CRL Phase 2 JLD interchange ~2030

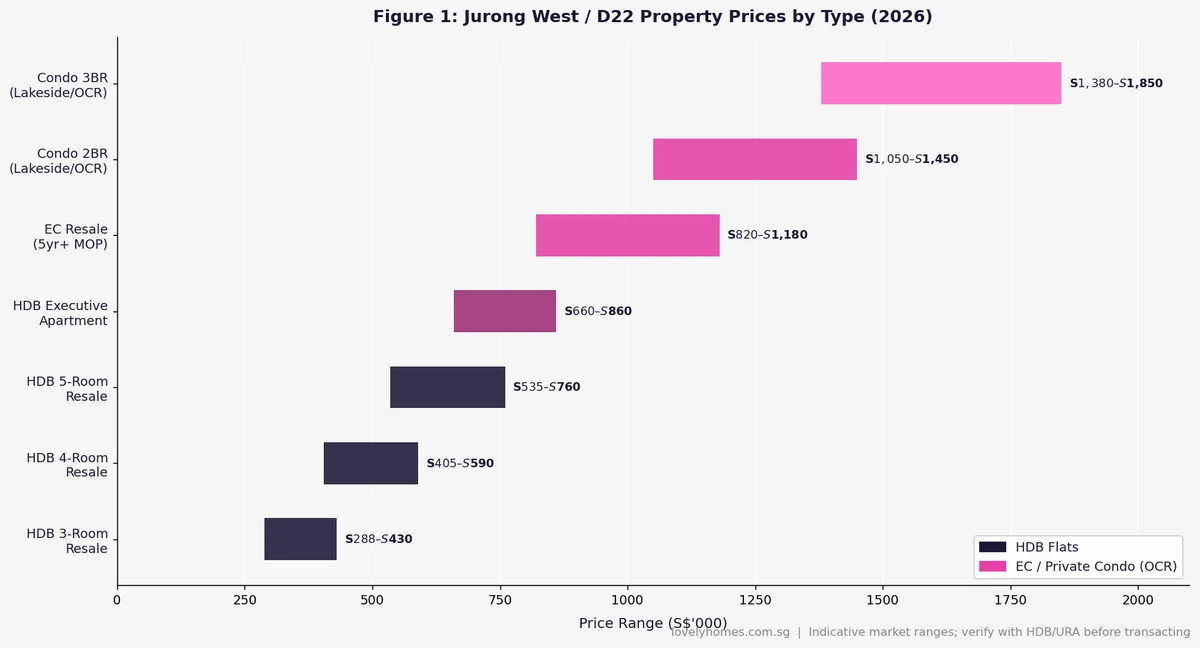

- HDB resale prices: 3-room S$288,000–S$430,000; 4-room S$405,000–S$590,000; 5-room S$535,000–S$760,000

- Private/EC prices: EC resale S$820,000–S$1,180,000; condo 2BR S$1,050,000–S$1,450,000; condo 3BR S$1,380,000–S$1,850,000

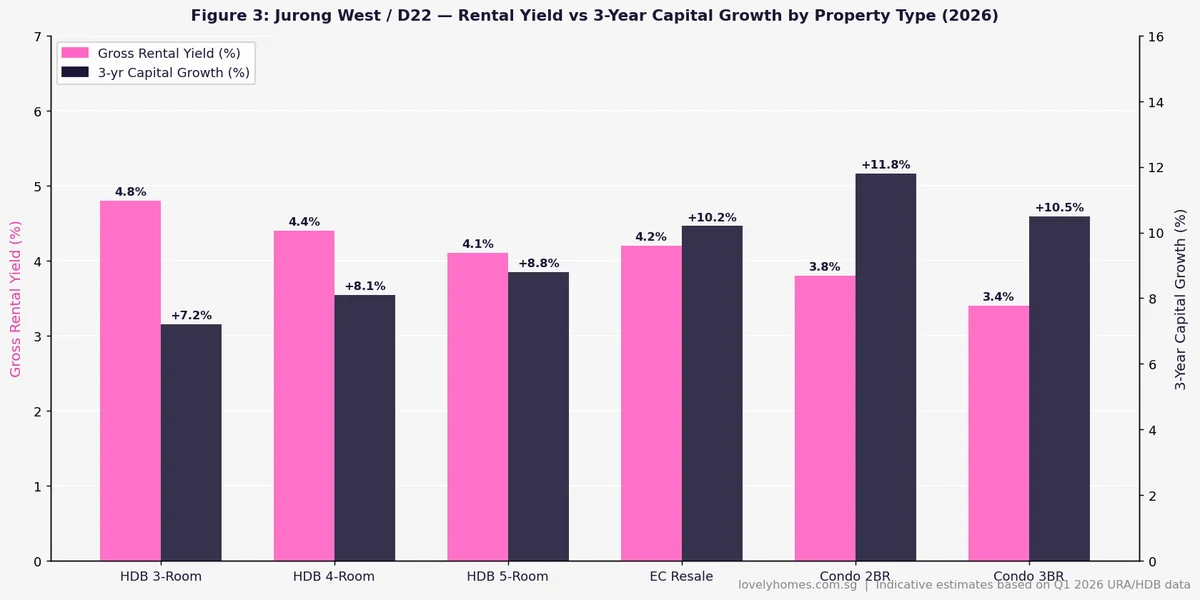

- Gross rental yield: HDB 4.1–4.8%; condo/EC 3.4–4.2%

- 3-year capital growth: private condos +10.5–11.8%; HDB flats +7.2–8.8%

- JLD uplift catalyst: 100,000 jobs target, S$100B+ investment pipeline; Cross Island Line (CRL) Jurong Lake District interchange ~2030

- Notable projects: Lake Grande (99yr, D22 flagship); Parc Riviera (99yr); Lakeville (99yr); J’den (JLD adjacent, fully sold)

- Buyer profile: First-time HDB buyers; NTU/NIE faculty and student tenants; industrial-worker tenants; JLD long-term investors

What Is Jurong West and Where Is It?

Jurong West is a planning area in Singapore’s Western Region, administered by URA. It encompasses the subzones of Boon Lay, Chin Bee, Kian Teck, Taman Jurong, Wenya, Yunnan, and the residential precincts stretching west from Chinese Garden to Joo Koon. The planning area is classified as Outside Central Region (OCR) throughout, making it Singapore’s quintessential value-segment residential market.

The estate was developed from the 1970s onward as Singapore’s answer to housing the industrial workforce of the Jurong Industrial Estate — then the backbone of the nation’s manufacturing economy. Today, Jurong West has matured into a self-sufficient community with comprehensive amenities, though it retains its character as Singapore’s most affordable major HDB town.

MRT Connectivity: EWL, JRL and the CRL Catalyst

Jurong West is served by five East West Line (EWL) stations — Lakeside (EW26), Chinese Garden (EW25), Boon Lay (EW27), Pioneer (EW28), and Joo Koon (EW29) — giving residents direct westbound access to Jurong East interchange and eastbound access to the CBD (City Hall, Raffles Place) within 35–45 minutes.

The transformative addition is the Jurong Region Line (JRL), a new MRT line opening in phases from 2027. The JRL will provide cross-island connectivity independent of the EWL trunk, serving the Tengah, Jurong Industrial Estate, and Nanyang Technological University (NTU) corridors. Key stations serving Jurong West precincts include Boon Lay JRL (interchange with EWL), and the Taman Jurong and Enterprise nodes. LTA has confirmed JRL Stage 1 (Choa Chu Kang to Boon Lay) targeting completion in mid-2027, with Stage 2 and Stage 3 by 2028.

Looking further ahead, the Cross Island Line (CRL) Phase 2 is planned to include a Jurong Lake District station, creating a future CRL–EWL–JRL interchange at Jurong East — one of the most powerful multimodal nodes outside the CBD. This interchange, expected around 2030, is the single largest infrastructure catalyst underpinning the JLD property investment thesis.

Property Prices in Jurong West 2026

Jurong West offers the most affordable HDB resale flats among Singapore’s mature towns, making it a popular choice for first-time buyers and families on tighter budgets. A 4-room resale flat in Boon Lay or Taman Jurong typically commands S$405,000 to S$590,000 in 2026, with premium blocks in Lakeside precinct (near waterfront and MRT) occasionally reaching S$600,000–S$630,000. Five-room flats trade at S$535,000 to S$760,000, reflecting their larger floor area and suitability for multigenerational families.

The private residential market in D22 is more limited than in eastern or central districts. The flagship developments are the three Jurong lakeside condos — Lake Grande (710 units, 99yr, launched 2016 at ~S$1,350 PSF, now trading at approximately S$1,500–S$1,700 PSF resale), Parc Riviera (752 units, 99yr), and Lakeville (696 units, 99yr). These projects form the benchmark private condo tier for D22 OCR. EC resale — particularly Westwood Residences and The Topiary (both past 5-year MOP) — provides an intermediate option between HDB and private, with transacted prices of S$820,000 to S$1,180,000 for units that have fully privatised.

Schools in Jurong West

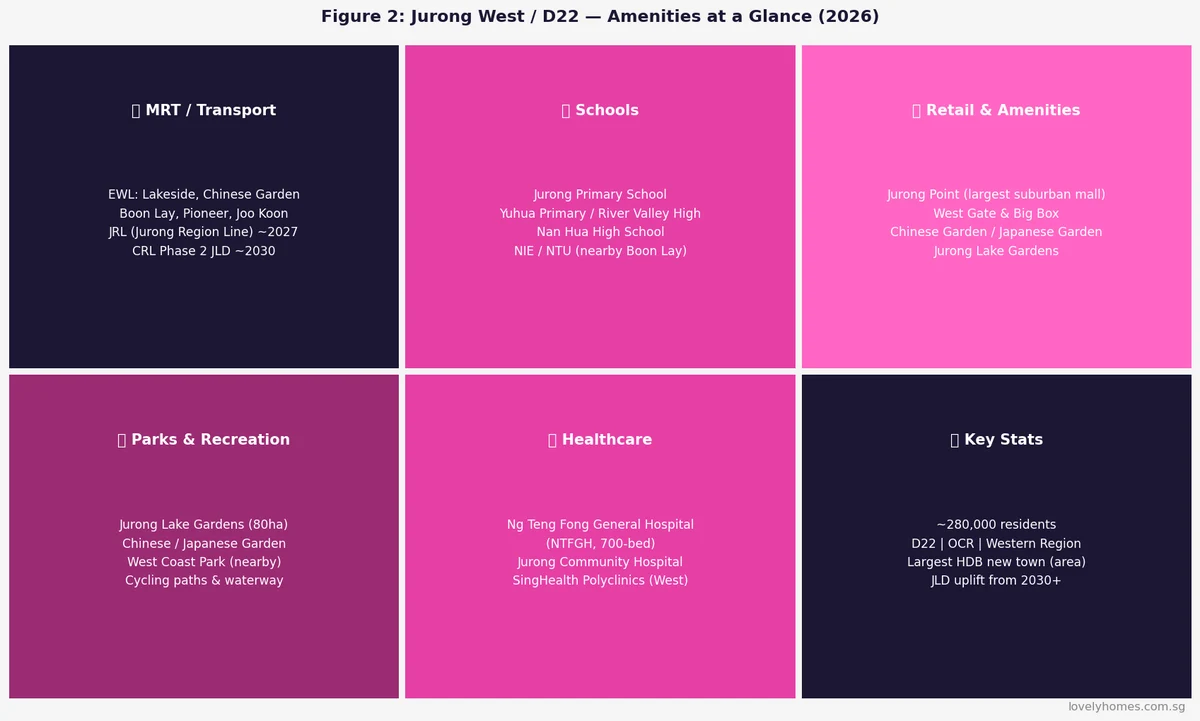

Jurong West is well-stocked with primary schools spread across its precincts, providing good within-1km options for families with young children. Key schools include Jurong West Primary School, Yuhua Primary School, Lakeside Primary School (in the waterfront precinct), and the SAP school Nan Hua Primary School on Clementi Avenue 1 (within reach of the western Clementi–Jurong border).

At secondary level, Nan Hua High School, River Valley High School (a centralised independent school, accessible via EWL), Yuan Ching Secondary, and Jurong Secondary all fall within the D22 ecosystem. For tertiary education, Nanyang Technological University (NTU) and the National Institute of Education (NIE) — both in the adjacent Jurong/Boon Lay area — generate a steady pool of academic-sector tenants, making the estate attractive for buy-to-let investors targeting the education cluster.

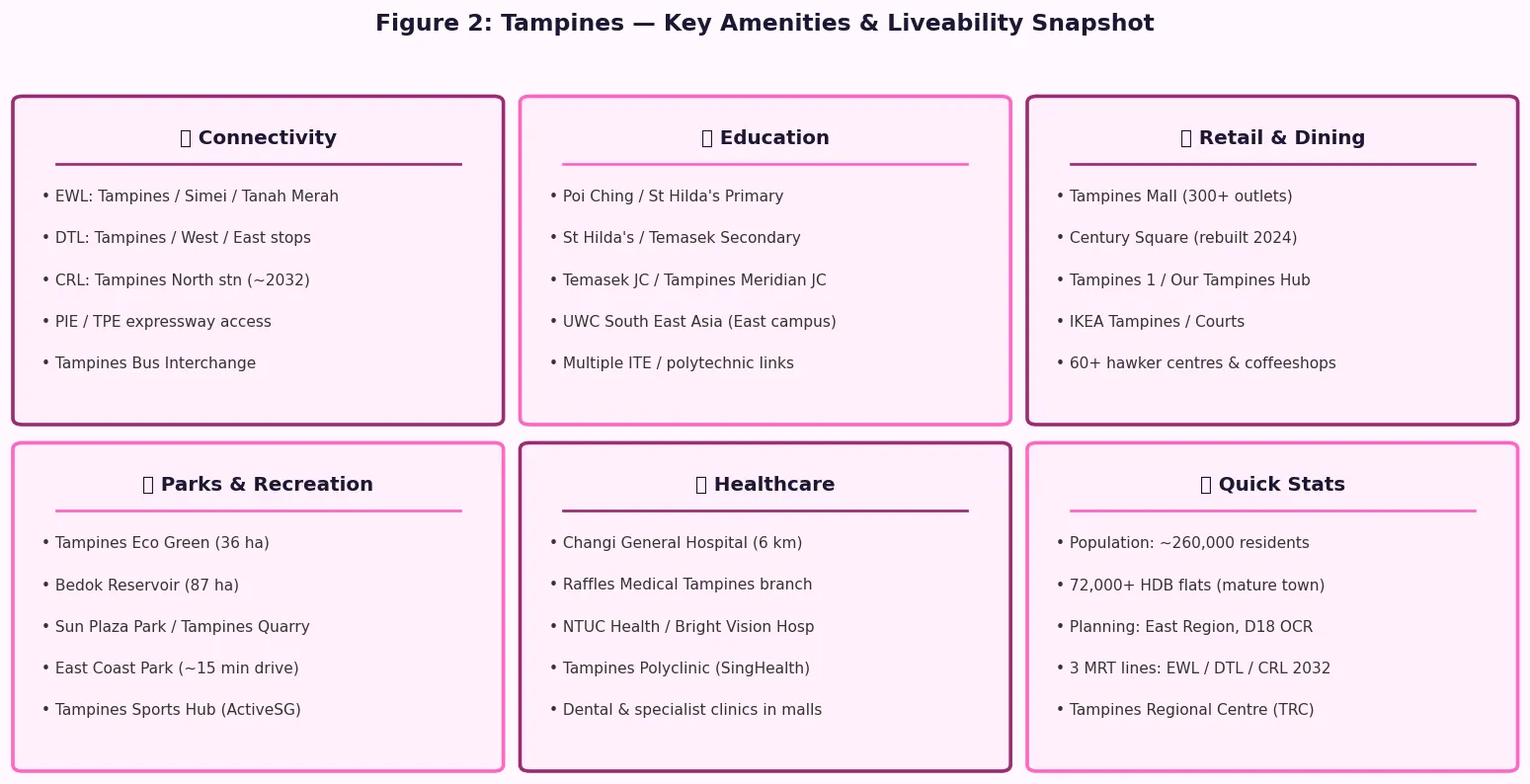

Lifestyle, Amenities and the JLD Masterplan

Jurong West’s retail anchor is Jurong Point — Singapore’s largest suburban shopping mall with over 500 tenants — located adjacent to Boon Lay MRT. The nearby WestGate and JEM malls at Jurong East further expand the retail catchment for western residents. For recreation, the Jurong Lake Gardens (an 80-hectare lakeside park opened in 2019) and the iconic Chinese Garden and Japanese Garden heritage parks provide significant green space at the estate’s eastern fringe.

The most consequential transformation for Jurong West buyers, however, is the Jurong Lake District (JLD) masterplan. URA has designated JLD as Singapore’s second Central Business District — a 360-hectare precinct centred on Jurong East, targeting 100,000 jobs and attracting major institutional anchors including the Singapore Tourism Board’s planned Tourism 2.0 hub. The URA masterplan envisions JLD as a mixed-use lakeside precinct with commercial towers, hotels, recreational facilities, and residential developments, all served by the future EWL–JRL–CRL mega-interchange. Healthcare in Jurong West is served by Ng Teng Fong General Hospital (NTFGH) — a 700-bed acute-care hospital opened in 2015 and designated as the western regional hospital — and Jurong Community Hospital on the same campus.

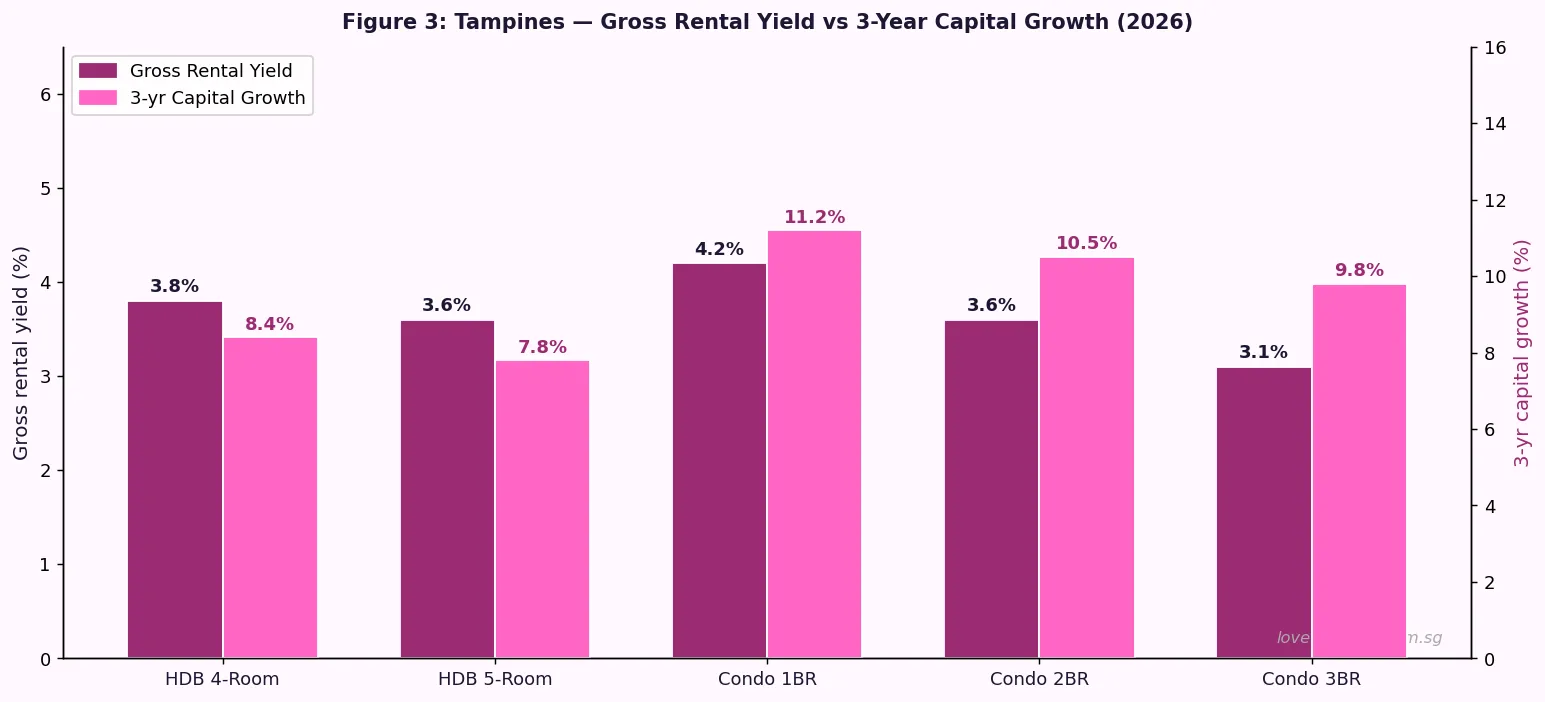

Rental Yields and Investment Case

Jurong West’s primary investment draw is its high gross rental yield relative to the rest of Singapore. HDB 3-room flats in the estate yield approximately 4.8% gross, the highest among Singapore’s major HDB towns, driven by affordable entry prices and consistent demand from blue-collar workers, NTU/NIE staff, and junior industrial-sector tenants. Four-room flats yield around 4.4% gross, and 5-room flats approximately 4.1%.

Private condo yields in D22 are lower due to higher entry PSF, but the JLD re-rating thesis has driven stronger capital appreciation. Lake Grande 2BR units have appreciated approximately +11.8% on a 3-year basis through Q1 2026, in line with the broader lakeside corridor outperformance. EC resale units — benefiting from their mixed private/HDB character and fully privatised status after MOP — have delivered the strongest combined return profile: yield around 4.2% with 3-year capital growth of approximately +10.2%.

Summary: Jurong West Property Types at a Glance

| Property Type | Typical Price Range | Gross Yield | 3yr Capital Growth | Tenure |

|---|---|---|---|---|

| HDB 3-Room Resale | S$288,000–S$430,000 | ~4.8% | +7.2% | 99-yr (HDB) |

| HDB 4-Room Resale | S$405,000–S$590,000 | ~4.4% | +8.1% | 99-yr (HDB) |

| HDB 5-Room Resale | S$535,000–S$760,000 | ~4.1% | +8.8% | 99-yr (HDB) |

| EC Resale (5yr+ MOP) | S$820,000–S$1,180,000 | ~4.2% | +10.2% | 99-yr (privatised) |

| Condo 2BR (Lakeside OCR) | S$1,050,000–S$1,450,000 | ~3.8% | +11.8% | 99-yr |

| Condo 3BR (Lakeside OCR) | S$1,380,000–S$1,850,000 | ~3.4% | +10.5% | 99-yr |

Worked Example: First-Time Buyer Purchasing an HDB Resale Flat in Jurong West

Profile: Mr and Mrs Rajan, both Singapore Citizens, joint monthly income S$7,200. First-time buyers seeking an HDB resale flat in Jurong West close to Boon Lay MRT for Mr Rajan’s commute to the Jurong Industrial Estate.

Target unit: 4-room resale flat, Boon Lay Drive, asking price S$498,000.

- CPF Housing Grants available: Enhanced CPF Housing Grant (EHG) — joint income S$7,200, within EHG ceiling of S$9,000; EHG for family = S$30,000. Proximity Housing Grant (PHG) — not applicable (not buying near parents). Total grants: S$30,000.

- Effective purchase price after grants: S$498,000 − S$30,000 = S$468,000

- Buyer’s Stamp Duty (BSD): S$1–S$180,000 @ 1% = S$1,800 + S$180,001–S$360,000 @ 2% = S$3,600 + S$360,001–S$468,000 @ 3% = S$3,240 = BSD S$8,640

- ABSD: Nil — SC first residential property

- Loan option — HDB Loan: 80% LTV on purchase price = S$398,400 (before EHG offset); effective loan after EHG S$368,400 at 2.6% p.a. over 25 years = approximately S$1,669/month

- Mortgage Servicing Ratio (MSR): S$1,669 ÷ S$7,200 = 23.2% — well within the 30% MSR cap

- CPF/cash upfront: 20% downpayment from CPF OA = S$99,600; BSD S$8,640 from CPF; legal fees ~S$2,500 cash; total CPF draw ~S$108,240; cash ~S$2,500

The Rajans are comfortably within MSR at 23.2% and their CPF OA savings (assuming S$120,000 combined) are sufficient for the downpayment. The HDB loan — while carrying a higher interest rate than a bank loan — provides the security of no lock-in penalty and the ability to overpay without fee. Monthly repayments of S$1,669 represent a very sustainable 23.2% of joint income, leaving ample capacity for savings and family expenditure.

Why Jurong West Matters: The JLD Long-Term Thesis

Jurong West’s investment case rests substantially on the Jurong Lake District masterplan, which URA has been developing since 2008 and accelerated post-2020. JLD is Singapore’s most significant decentralisation initiative: the government is deliberately shifting high-value economic activity, including financial services, technology, and medical tourism, from the traditional CBD to the western lakeside precinct. The S$100 billion development pipeline, anchor commitments from major corporations, and the planned CRL–JRL–EWL interchange at Jurong East by 2030 collectively underpin a structural case for western property appreciation that stretches well into the 2030s.

Comparable precedents exist elsewhere in Singapore: the build-out of Marina Bay from the 2000s transformed adjacent Districts 1 and 2 values; the development of Punggol Digital District has re-rated Punggol condos. JLD is a substantially larger initiative by both scale and investment quantum, with government backing and legislative commitment.

What Might Come Next for Jurong West

This section contains forward-looking analysis and should not be construed as a prediction of future prices.

The most significant near-term catalyst is JRL Stage 1 opening in mid-2027. Historically, property values within a 500m radius of new MRT stations have appreciated 3–8% in the 12–24 months around station opening, based on LTA and academic studies of prior line openings. Jurong West precincts near planned JRL stations — particularly Taman Jurong — could see notable uplift. The CRL Phase 2 confirmation (expected from MND/LTA around 2026–2027) will also provide a milestone catalyst for JLD-adjacent properties. Conversely, the large public housing pipeline for Tengah (a new HDB town adjacent to Jurong West, expected to deliver 42,000 homes through the late 2020s) could exert moderate supply-side pressure on Jurong West HDB resale prices in the medium term.

Frequently Asked Questions

Is Jurong West a good area to buy property in 2026?

For value-seeking buyers and yield-focused investors, Jurong West offers the most affordable entry point among Singapore’s MRT-served estates, with the JLD masterplan providing a credible long-term capital appreciation case. The trade-off is a less vibrant lifestyle compared with central or eastern estates, longer commute times to the CBD for non-western employment nodes, and proximity to industrial zones in the southern precincts. For families on moderate incomes buying their first HDB home, or investors seeking the highest gross rental yield, Jurong West is one of Singapore’s more compelling value propositions in 2026.

Which MRT stations serve Jurong West?

Five EWL stations serve Jurong West: Lakeside (EW26), Chinese Garden (EW25), Boon Lay (EW27), Pioneer (EW28), and Joo Koon (EW29). The upcoming JRL (Jurong Region Line), opening from mid-2027, will add further stations in the Boon Lay, Taman Jurong, and Enterprise corridors, providing east–west connectivity independent of the EWL trunk. The CRL Phase 2 Jurong Lake District interchange (~2030) will link the Cross Island Line to both EWL and JRL at Jurong East, making the western node one of Singapore’s best-connected transport hubs outside the city.

What is the Minimum Occupation Period (MOP) for Jurong West HDB flats?

Standard (Open Market) HDB BTO flats in Jurong West carry a 5-year MOP from the date of key collection. During MOP, the flat cannot be sold on the open market, rented out in full (subletting individual rooms is permitted with HDB approval), or used to fulfil CPF accrued interest clawback. Jurong West is classified as a Standard location under HDB’s classification framework — not Plus or Prime — so no extended MOP applies. After MOP, HDB resale flats in Jurong West can be sold freely, and owners can purchase a private property concurrently (though they would pay 20% ABSD if retaining the HDB).

How does Jurong West compare with Tampines or Woodlands?

Jurong West offers the lowest HDB resale prices of the three, reflecting its OCR western location and industrial-adjacent character. Tampines (D18) commands a premium of approximately S$100,000–S$180,000 for equivalent HDB flat types, driven by its mature town status, stronger amenity base, and Tampines Regional Centre employment cluster. Woodlands (D25) is similarly priced to Jurong West but has a different JLD-equivalent catalyst in the Woodlands Regional Centre and the RTS Link to Johor Bahru. For JLD uplift exposure, Jurong West is unique. For established amenity and eastern-facing employment, Tampines is stronger.

Can a Singapore PR buy an HDB resale flat in Jurong West?

Yes. Permanent Residents who meet HDB eligibility — forming a family nucleus with another SPR or SC family member, and having held PR status for at least 3 years — can purchase HDB resale flats in Jurong West. However, SPRs pay a 5% ABSD on their first residential purchase and 15% ABSD on their second. SPRs are also subject to the Ethnic Integration Policy (EIP) quotas and SPR quota (8% per block, 5% per neighbourhood) when purchasing HDB flats.

What is the best precinct in Jurong West to buy?

For capital appreciation potential, the Lakeside precinct (near Lakeside MRT and Jurong Lake Gardens) offers the strongest JLD adjacency and lifestyle amenity. Lake Grande, Parc Riviera, and Lakeville are the benchmark developments here. For rental yield and affordability, the Boon Lay and Taman Jurong precincts offer higher yields from a lower entry base and benefit from Jurong Point’s retail anchor and Boon Lay MRT access. Families prioritising school catchments should focus on precincts within 1km of Nan Hua or Lakeside Primary schools.

How will the Tengah new town affect Jurong West property prices?

HDB’s Tengah new town — Singapore’s newest HDB estate, adjacent to Jurong West’s northern boundary — is expected to add approximately 42,000 public housing units through the late 2020s. In the short to medium term, this supply injection could exert modest downward pressure on Jurong West HDB resale prices, particularly for units competing with similarly priced Tengah BTO flats. However, Tengah BTO flats carry a 5-year MOP and are new-build (typically priced at a discount to resale), limiting direct substitution. The JRL will also serve Tengah, potentially enhancing connectivity of both estates and mitigating resale price pressure.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Jurong Lake District Property Outlook 2026: Prices, Investment Potential and What Is Coming

- HDB Loan vs Bank Loan Singapore 2026: Complete Comparison

- CPF Housing Grant for Resale Singapore 2026: EHG, PHG and Step-Up Grant

- Singapore Property Buying Checklist 2026: 12 Steps from IPA to Key Collection

- Condo vs HDB Singapore 2026: The Upgrader’s Complete Decision Framework

- Singapore EC Buying Guide 2026: Complete Guide to Executive Condominiums

Disclaimer

This article is for general informational purposes only and does not constitute financial, legal, or property advice. All property prices, rental yields, and capital growth figures are indicative estimates drawn from URA REALIS data, HDB resale portal transactions, and market analysis as at Q1 2026. Actual transaction prices vary by unit, floor, condition, and prevailing market conditions. ABSD, BSD, CPF rules, HDB eligibility, MSR, and TDSR policies are set by the Singapore Government (IRAS, HDB, MAS, CPF Board) and are subject to change. Readers should conduct their own due diligence and consult a licensed property agent, lawyer, and financial adviser before making any property transaction. For authoritative data, refer to URA (ura.gov.sg), HDB (hdb.gov.sg), IRAS (iras.gov.sg), MAS (mas.gov.sg), and CPF Board (cpf.gov.sg).