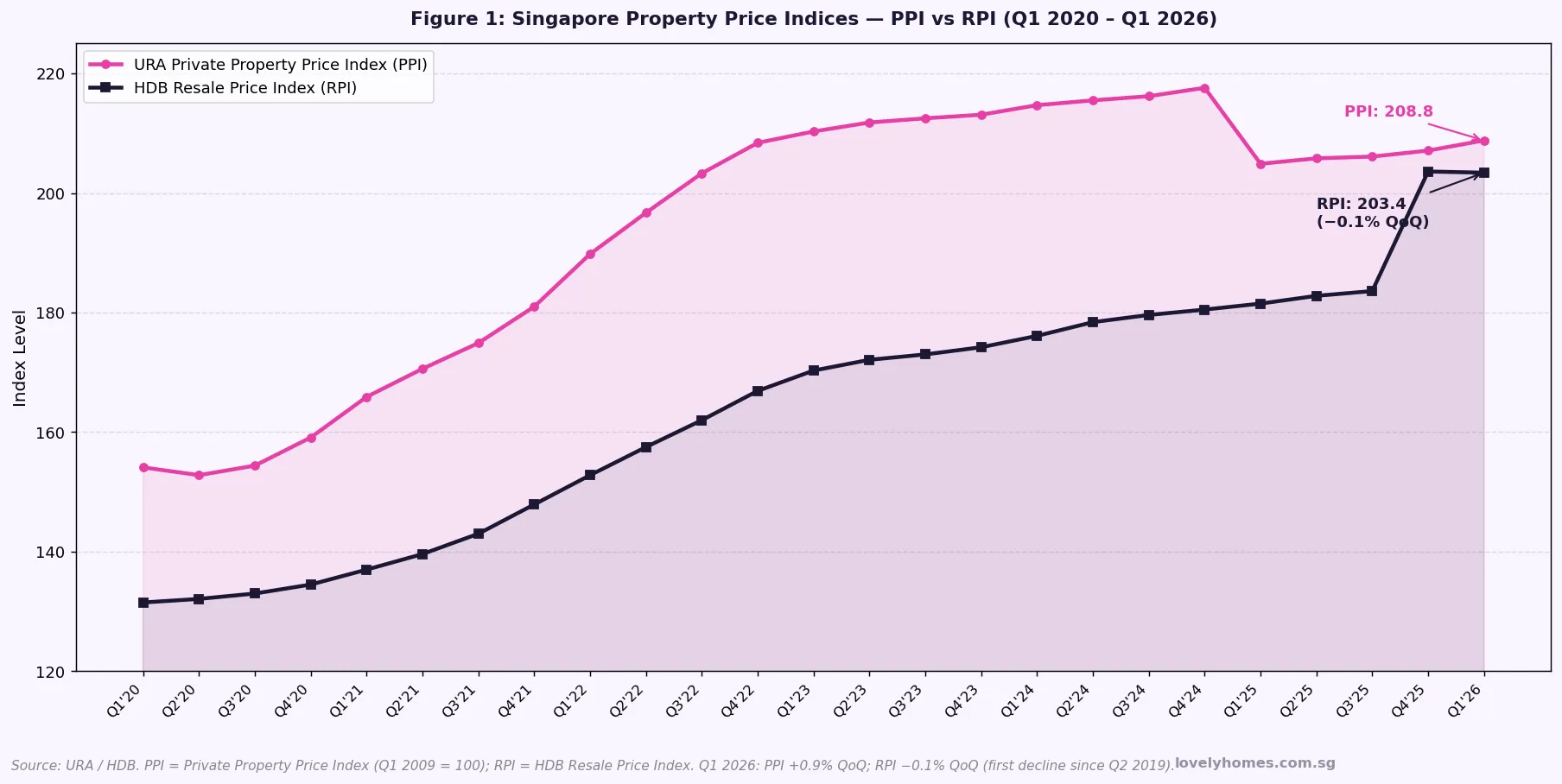

The HDB Resale Price Index (RPI) fell 0.3% in Q2 2026 (flash estimate, 1 July 2026), following a 0.1% decline in Q1 2026.

This marks the first back-to-back quarterly RPI decline since early 2019 — a meaningful shift after a 12-quarter streak of price growth from mid-2020.

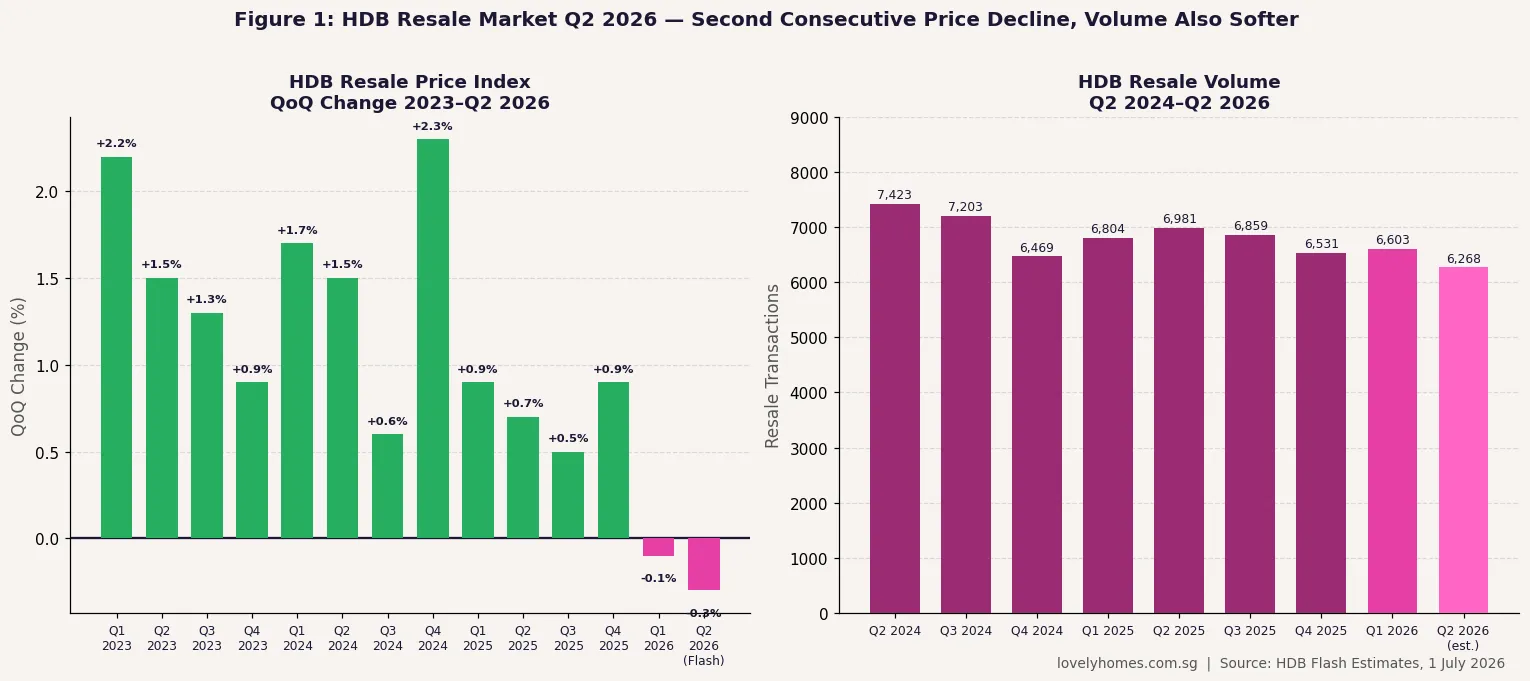

Estimated transactions: ~6,268 in Q2 2026 (as at 29 June 2026), down about 10.2% versus Q2 2025’s 6,981 transactions.

The full Q2 data from HDB — including town-level breakdowns and flat-type analysis — is expected by 23 July 2026.

Meanwhile, private residential prices rose 0.5% in Q2 2026 (URA flash estimate), a divergence between public and private markets.

The October 2026 BTO exercise (~8,000 flats, 7 projects) and a growing private pipeline should continue to moderate resale demand in 2H 2026.

HDB Resale Prices Fall for a Second Consecutive Quarter in Q2 2026

The Housing & Development Board released its Q2 2026 flash estimate on 1 July 2026, showing the Resale Price Index (RPI) declined 0.3% quarter-on-quarter — deepening the 0.1% dip recorded in Q1 2026. The two consecutive quarterly declines are the first since early 2019, ending a remarkable run of price growth that had seen the RPI climb more than 30% from its 2020 post-pandemic lows.

The data point comes on the same day as URA’s Q2 2026 private residential flash estimate, which showed a more modest picture: private home prices rising 0.5%, with gains concentrated in the Core Central Region (+2.0%) and landed segment (+2.6%), while the Rest of Central Region (-1.4%) and Outside Central Region (-0.2%) softened. The divergence between the two markets — private prices edging up while HDB resale prices retreat — is a notable feature of Singapore’s mid-2026 property landscape.

Figure 1: (Left) HDB Resale Price Index QoQ change, Q1 2023 to Q2 2026. Two consecutive declines in Q1 and Q2 2026 mark the first back-to-back quarterly retreat since early 2019. (Right) Estimated resale transaction volume, Q2 2024 to Q2 2026 — Q2 2026 volume (~6,268) is the softest in the chart window. Source: HDB Flash Estimates, 1 July 2026.

Why Are HDB Resale Prices Softening?

Several structural forces are bearing down on HDB resale demand in mid-2026. First, the sheer volume of BTO supply entering the market is creating competition at the margins. HDB launched approximately 19,600 BTO flats across 2026, with the October exercise alone adding close to 8,000 units across seven projects — including two projects at Bayshore (Prime classification, 2,500 units combined), Caldecott (Prime, 1,430 units), and Yishun Chencharu (Standard, 1,580 units). Buyers who might previously have turned to the resale market for faster access to housing in desired towns now have BTO options that, while involving a wait of several years, offer meaningful subsidies.

Second, resale volume has been declining. An estimated 6,268 transactions in Q2 2026 represents a drop of approximately 10.2% compared to 6,981 in Q2 2025. Fewer transactions mean fewer comparable sales pushing prices higher — the resale market is losing the self-reinforcing momentum it enjoyed during 2021–2024.

Third, the cooling measures introduced in 2022–2023 — the 15-month wait-out period for private property owners wanting to buy HDB resale flats, tightened income ceilings under the HFE framework, and the introduction of Plus and Prime classifications — have added friction for demand that was previously unconstrained. The Ethnic Integration Policy (EIP) also continues to block transactions in certain blocks, narrowing the effective buyer pool in popular mature estates.

What the Divergence Between Private and HDB Prices Means

The contrast between private (+0.5%) and HDB resale (-0.3%) prices in Q2 2026 reflects different demand profiles. Private residential demand in Singapore is increasingly driven by upgraders, high-net-worth individuals, and (at the CCR end) wealthy foreigners paying the 60% ABSD — a buyer cohort that is relatively insensitive to BTO supply. HDB resale demand, by contrast, comes principally from first-timers who cannot get a BTO (due to ballot failure, income ceiling, or timing), second-timers who have completed their MOP and want a larger resale flat before upgrading, and PRs who have been resident long enough to qualify. This segment is more directly substitutable with BTO supply.

The CCR’s 2.0% private price gain in Q2 2026 also reflects some flight-to-quality within the private market — buyers who can afford CCR are moving upstream as OCR and RCR sentiment softens. This bifurcation is a characteristic of a market entering a more discerning phase after broad-based appreciation.

Context: Is This a Correction or a Reset?

A 0.3% quarterly decline does not in isolation constitute a correction — it represents a modest pullback after an extended run-up. The HDB RPI reached its cycle high in Q4 2025 or Q1 2026 (the full data will clarify the exact peak). From cycle trough in Q2 2019 to approximate peak in Q4 2025, the RPI gained roughly 30%+ over six years. A mild two-quarter retreat is, from a long-term perspective, a normalisation.

Industry figures suggest the retreat is orderly rather than distressed. Median resale flat prices remain close to or at multi-year highs on an absolute basis — it is the rate of growth that has reversed, not a broad-based collapse. The Bidadari estate’s record S$945,000 resale transaction (a 3-room flat at 118A Alkaff Crescent in June 2026, as reported by LovelyHomes) shows that premium locations can still command record prices even as the broader index softens.

What to Watch in 2H 2026

The full Q2 2026 HDB statistics (expected 23 July 2026) will provide the town-level and flat-type breakdown that the flash estimate lacks. Market participants will be looking at whether the price softening is concentrated in particular flat types (5-room and executive flats, which saw the sharpest run-up) or distributed across the board. The MOP unlock pipeline — the volume of BTO flats reaching their 5-year MOP in 2026 — is also a factor: a large cohort of flats from 2019–2021 BTO launches reaching MOP simultaneously could add resale supply.

With the October BTO exercise applications opening in September 2026 (HFE deadline 15 September 2026), buyer attention is likely to shift toward the BTO market in 3Q 2026, further dampening resale activity near term. The 2H 2026 private pipeline includes several significant new launches — any softening in developer sales could, through the upgrader channel, reduce demand for HDB resale from MOP-cleared flat owners looking to cash out for a private upgrade.

Frequently Asked Questions

Does the -0.3% RPI mean my flat is worth less than last quarter?

At a market level, yes — the flash estimate indicates that the average resale flat transacted in Q2 2026 sold at prices approximately 0.3% lower than the average in Q1 2026. However, individual flat values depend on estate, block, floor, flat condition, and proximity to amenities. A Bidadari flat in a sought-after block may still have appreciated even as the overall index dipped. The RPI is a market-level index, not a valuation of your specific flat. For an accurate current valuation, engage an HDB-registered salesperson for a Comparative Market Analysis or use HDB’s official transaction data portal.

Why are private prices rising while HDB resale prices fall?

The two markets have different demand drivers. Private residential demand in Singapore is partly sustained by high-income upgraders, global wealth, and CCR buyers who are relatively insulated from BTO supply effects. HDB resale demand, by contrast, is more directly substitutable with BTO supply — buyers who want an HDB flat can increasingly choose a new BTO over a resale flat, especially with the expanded supply in 2026. The 15-month wait-out period also constrains one source of HDB resale demand (private property sellers downsizing). The result is diverging price trends.

Should I wait to buy an HDB resale flat if prices are declining?

Market timing in housing is notoriously difficult, and the decision to buy an HDB resale flat should primarily be driven by your housing needs, financial readiness, and family circumstances — not by short-term RPI movements. A 0.3% quarterly decline is small relative to the transaction costs of delaying a purchase (rental costs, stamp duties). That said, if you are financially able to wait and are flexible on timing, the 2H 2026 market may offer a wider selection at steady or modestly lower prices given the pipeline of October BTO and new private launches drawing attention away from resale. Always work with a qualified professional and check your HFE letter status before making any commitment.

When will the full Q2 2026 HDB data be released?

HDB typically releases the full quarterly resale statistics approximately three weeks after the flash estimate — so the full Q2 2026 data (with flat-type and town-level breakdowns, median transaction prices, and complete volume figures) is expected around 23 July 2026. LovelyHomes will publish an in-depth analysis when the full data is available. The full URA Q2 2026 private residential statistics are also expected on 25 July 2026.

Is this the start of a bigger HDB resale price correction?

Based on Q2 2026 flash data alone, it is premature to call a structural correction. Two consecutive quarters of mild declines (−0.1% and −0.3%) are consistent with a soft landing rather than a downturn. The HDB government remains committed to ensuring an adequate supply of BTO flats and has levers — including BTO supply pacing and eligibility criteria — to manage the market. Historical context is useful: the last significant HDB resale correction (2013–2019) saw the RPI decline approximately 13% over six years, driven by a deliberate policy supply surge. The current situation — a mild two-quarter pullback within a broadly healthy economy — does not yet suggest a repeat of that trajectory.

The data in this article is drawn from HDB and URA flash estimates released on 1 July 2026. Flash estimates are preliminary and subject to revision when the full quarterly statistics are published. Transaction volume figures (as at 29 June 2026) are unaudited estimates. This article is not financial or investment advice. For current HDB resale data, visit hdb.gov.sg. For URA private residential data, visit ura.gov.sg.

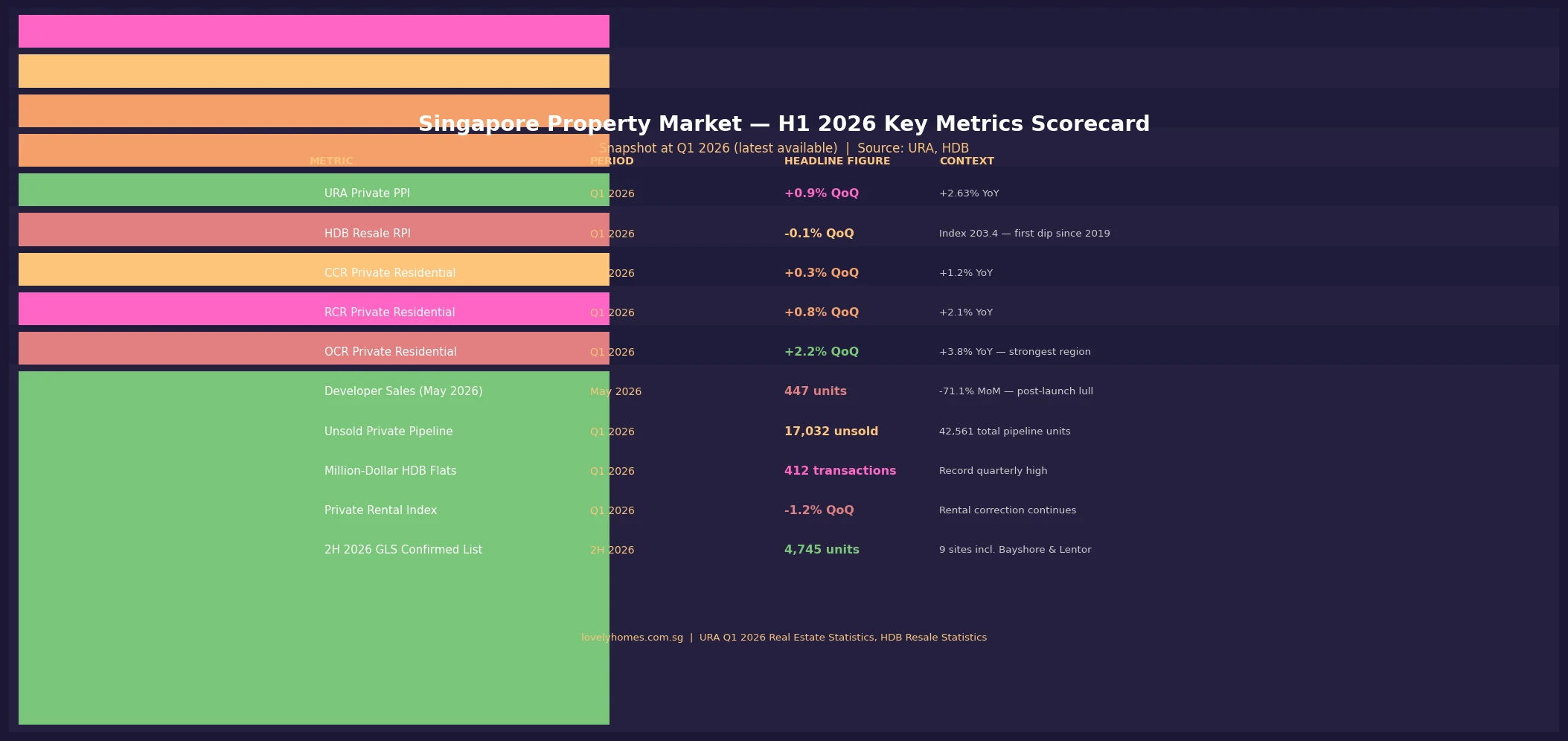

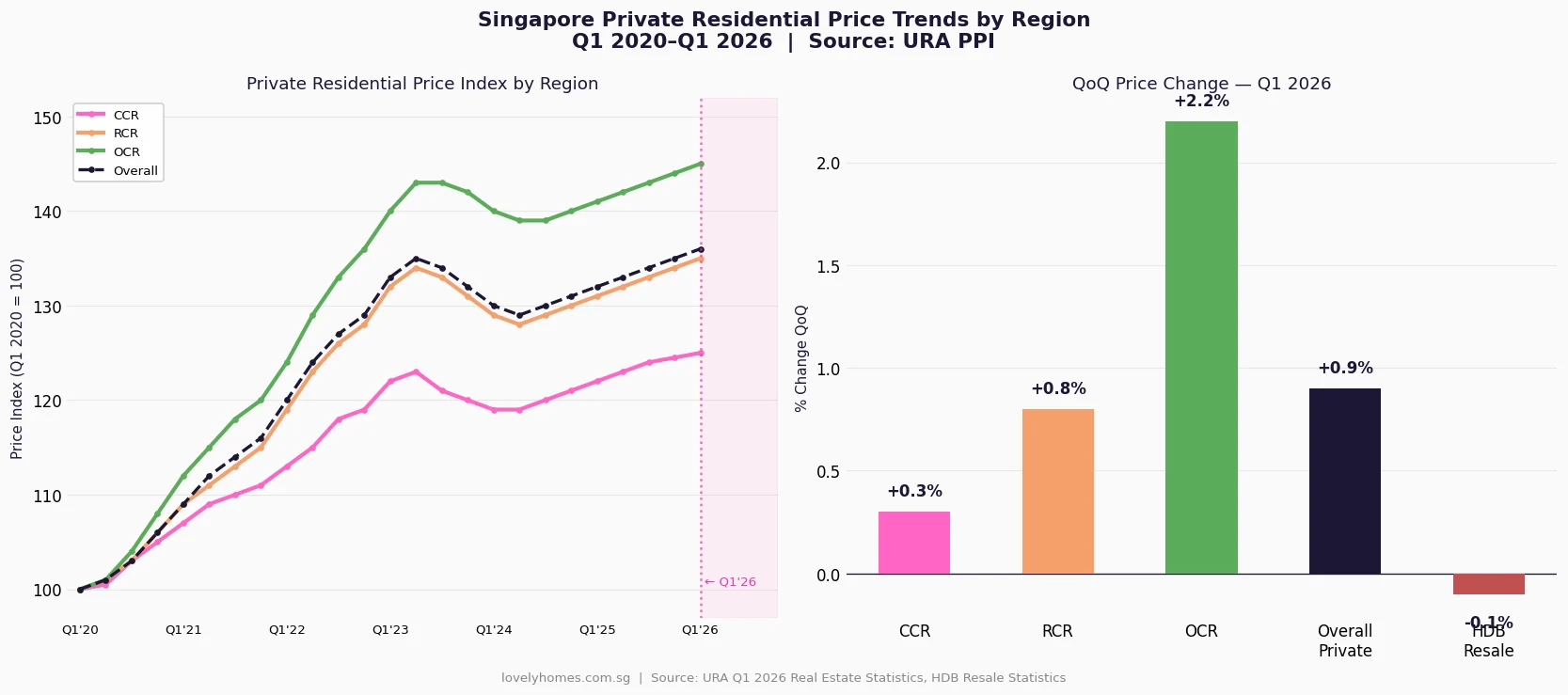

Private residential prices rose 0.9% QoQ and 2.63% YoY in Q1 2026, with the Outside Central Region (OCR) leading at +2.2% QoQ — price growth is positive but moderating.

HDB resale recorded its first quarterly dip (-0.1% QoQ) since Q2 2019; index sits at 203.4. Not a crash — more of a pause after a five-year run.

2H 2026 GLS launches 9 confirmed-list sites (4,745 units), adding meaningful supply to OCR and RCR. Pricing discipline from developers is expected.

Key risk: interest rates remain elevated at 3.0–3.5% for bank mortgages; affordability is stretched for many first-time buyers.

Key catalyst: any US Federal Reserve rate cut signals would unlock significant pent-up demand — watch the September and December 2026 Fed meetings.

For buyers: fundamentals remain sound — Singapore’s employment is near-full, rental demand supports investment yield, and supply is finite. Timing the market is less reliable than time in the market.

URA Q2 2026 Flash Estimates are expected in early July 2026 and will be the next major data point.

H1 2026 in Review: Where the Singapore Property Market Stands

As the calendar turns to the second half of 2026, Singapore’s property market presents a nuanced picture. Private residential prices continued their gradual upward trajectory in Q1 2026, with the Urban Redevelopment Authority (URA) reporting a Property Price Index (PPI) increase of 0.9% quarter-on-quarter — a modest but consistent gain that extends a trend stretching back to the post-pandemic recovery that began in mid-2020. On a year-on-year basis, the private residential index is up 2.63%, a pace that is firm but well below the double-digit growth seen during the post-pandemic surge of 2021 to 2023.

The Housing Development Board’s Resale Price Index (RPI), however, told a slightly different story. At 203.4 in Q1 2026, the HDB resale market recorded a 0.1% quarterly decline — the first such dip since Q2 2019. This is not alarming in isolation: the index had surged more than 54% since its 2019 trough, and a modest pause is consistent with natural market digestion. What it does signal is that the exceptional run of HDB resale price appreciation is transitioning into a more measured phase.

Figure 1: Singapore Property Market H1 2026 Key Metrics Scorecard — URA Q1 2026 Real Estate Statistics and HDB Resale Statistics.

Private Residential Market: A Three-Speed Story

The defining characteristic of Singapore’s private residential market in 2026 is regional divergence. The three planning zones administered by URA — the Core Central Region (CCR), Rest of Central Region (RCR), and Outside Central Region (OCR) — have performed at markedly different speeds in 2026.

The OCR is the undisputed pace-setter. A 2.2% quarterly gain in Q1 2026, following similar momentum in late 2025, reflects genuine demand from HDB upgraders — a cohort whose Minimum Occupation Period (MOP) clears in waves and who target mass-market new launches in the S$1.3M–S$1.8M range. The 2H 2026 GLS programme deliberately concentrates supply here (Tampines Street 94, Bayshore Road), which should moderate any further sharp price acceleration without causing a price correction.

The RCR recorded 0.8% QoQ growth — solid mid-field performance driven by a mix of first-time private buyers, professionals, and some foreign-related buying in the city-fringe. River Valley Green Parcel C (awarded June 2026 at a top bid of approximately S$1,730 psf ppr) is the headline indicator of developer confidence in this zone.

The CCR grew just 0.3% QoQ, a subdued reading that reflects several headwinds: the 60% Additional Buyer’s Stamp Duty (ABSD) on foreigners that has been in place since April 2023 continues to suppress international transaction volumes; and the global macro uncertainty discussed in the risk section below has weighed on ultra-high-net-worth discretionary buying. That said, CCR is not in distress — it remains a long-term beneficiary of Singapore’s family office growth and wealth inflows.

Figure 2: Singapore Private Residential Price Index by Region (Q1 2020–Q1 2026) and QoQ Change for Q1 2026. Source: URA Q1 2026 Real Estate Statistics.

HDB Resale Market: A Healthy Pause, Not a Reversal

Singapore’s HDB resale market has been one of the defining investment stories of the 2020s. From a low point in 2019 (RPI ≈ 132), prices surged to an index of 203.4 by Q1 2026 — a 54% cumulative increase. The Q1 2026 dip of 0.1% QoQ is, in that context, the market catching its breath after an exceptional run rather than a structural reversal.

Two counterintuitive data points reinforce this view. First, million-dollar HDB transactions reached a record quarterly high of 412 in Q1 2026 — indicating that at the premium end of the resale market (large mature-estate flats, high-floor units in sought-after towns), demand remains fierce. Second, overall HDB resale transaction volumes for Q1 2026 remained healthy, with four-room flats accounting for the largest share (approximately 2,690 transactions in Q1 2026 alone) at a median price of around S$575,000.

For 2H 2026, the HDB resale market is likely to remain range-bound rather than sharply appreciating or correcting. MOP cohorts from the 2016–2019 BTO launches are gradually clearing, releasing units back to the resale market — but supply from this channel is relatively thin compared to the 2013–2016 peak cycle. Demand remains supported by couples who cannot access BTO (due to income ceiling, citizenship mix, or urgency) and Permanent Residents who remain ineligible to buy BTO directly.

Developer Sales and the New Launch Pipeline

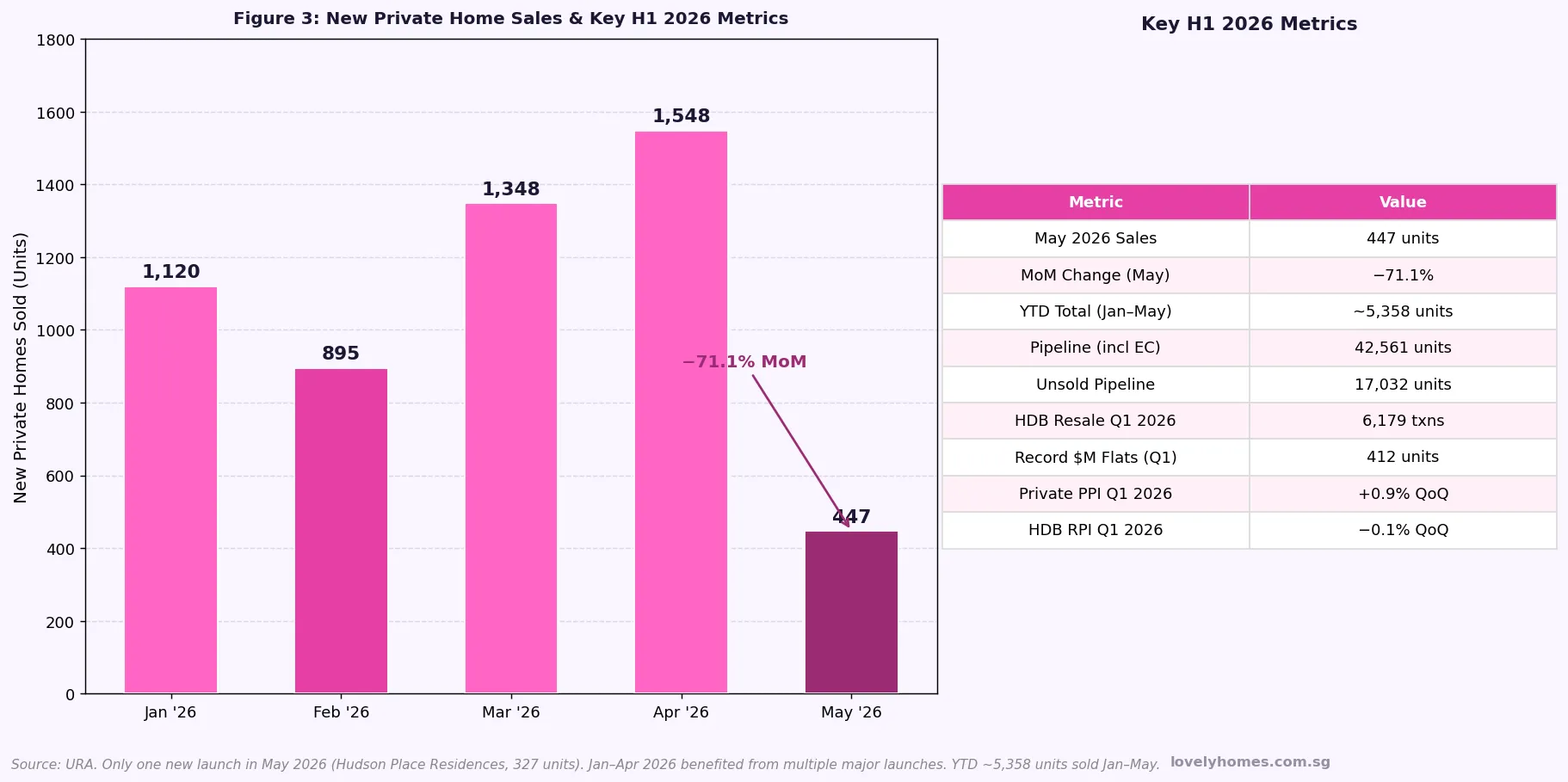

Developer sales activity is the indicator most directly shaped by new launch timing. The monthly data tells a story of feast and famine: January to April 2026 saw 1,120, 895, 1,348 and 1,548 units sold respectively — solid months driven by a cluster of project launches. May 2026 crashed to 447 units (-71.1% month-on-month), not because demand evaporated, but because there were few projects launching that month.

The pipeline going into 2H 2026 remains substantial. URA data shows 17,032 unsold units in the private pipeline as of Q1 2026 (total pipeline including units not yet launched: 42,561). The 2H 2026 GLS Confirmed List adds nine further sites including Lentor Gardens Parcel A and B, Bayshore Road, Tampines Street 94, and an EC site at Jurong East. These launches are phased across 2H 2026 into 2027, so the impact on completed supply will be felt primarily in 2028–2030.

Singapore’s private residential rental market began correcting in 2024 after a record two-year surge and that correction extended into 2026. The URA rental index fell 1.2% QoQ in Q1 2026, following declines across 2024 and 2025. In absolute terms, rents remain significantly above their pre-pandemic levels — a 2BR in D15 that rented for S$2,800/month in 2019 may still command S$4,200–S$4,800/month in 2026 depending on specification — but the exceptional post-pandemic pricing has normalised.

For investors, this rental correction compresses gross yields. A S$1.5M 2BR in the RCR yielding S$4,500/month gross generates a gross yield of approximately 3.6%, which is broadly comparable to bank deposit rates in 2026. Net yield after management fees, property tax, and maintenance is lower — making the case for property investment in 2026 primarily a capital appreciation thesis rather than a pure income play.

2H 2026 Market Outlook Summary

Segment

Base Case

Bull Case

Bear Case

Private Residential (Overall)

+1%–2% for full year 2026

+3%–4% if rates ease and demand recovers

Flat to -1% if global recession deepens

OCR (Mass Market)

Continues outperforming; +2%–3% YoY

+4%–5% with strong HDB upgrader demand

Supply pressure from GLS launches moderates gains

RCR (City Fringe)

Steady +1%–2% YoY

+3% with new launch interest

Flat if affordability ceiling is hit

CCR (Core Central)

Sideways to +1%; foreign buyer ABSD drag

+2%–3% if ABSD reviewed or wealth inflows surge

-1%–2% if global HNW sentiment deteriorates

HDB Resale

±0.5% QoQ; range-bound in H2

+1%–2% if upgrader demand stays robust

-1% if affordability stress bites flat demand

Private Rental

Further -2%–4% as supply catches up

Stabilises if employment influx resumes

Deeper correction if expat headcount falls

Worked Example: The Chen Family — Buy in 2H 2026 or Wait?

Mr and Mrs Chen are Singapore Citizens in their early 30s. They have cleared their HDB MOP on their Bishan 4-room flat and are looking to upgrade to a 3-bedroom OCR condo. They have combined income of S$13,500 per month, CPF OA savings of S$180,000, and cash of S$120,000.

They are eyeing a 3BR at an upcoming OCR launch in Q3 2026 priced at S$1.65M. Under the ABSD SC couple remission scheme, they can purchase the new condo and claim a full refund of the 20% ABSD (S$330,000) provided they sell their HDB flat within six months of the condo purchase date.

Key numbers: BSD S$47,600 (payable from CPF); ABSD S$330,000 (cash, but refundable within six months of HDB sale); 5% cash S$82,500; legal fees ~S$5,500. Bank loan: 75% LTV = S$1,237,500 at 3.2% over 30 years → monthly repayment approximately S$5,338. TDSR = S$5,338 ÷ S$13,500 = 39.5% (PASS, under 55%). Total cash needed upfront: ~S$208,000 (cash component + ABSD float pending HDB sale).

Should they wait? If OCR prices rise another 2% by Q1 2027, the same unit would cost S$1,683,000 — an additional S$33,000. If interest rates fall 50 bps by then, monthly repayments fall by ~S$300/month. The calculus slightly favours acting when they are ready rather than trying to time the market precisely, provided the ABSD remission window can be managed. See our guide on ABSD remission for SC couples for the full rules.

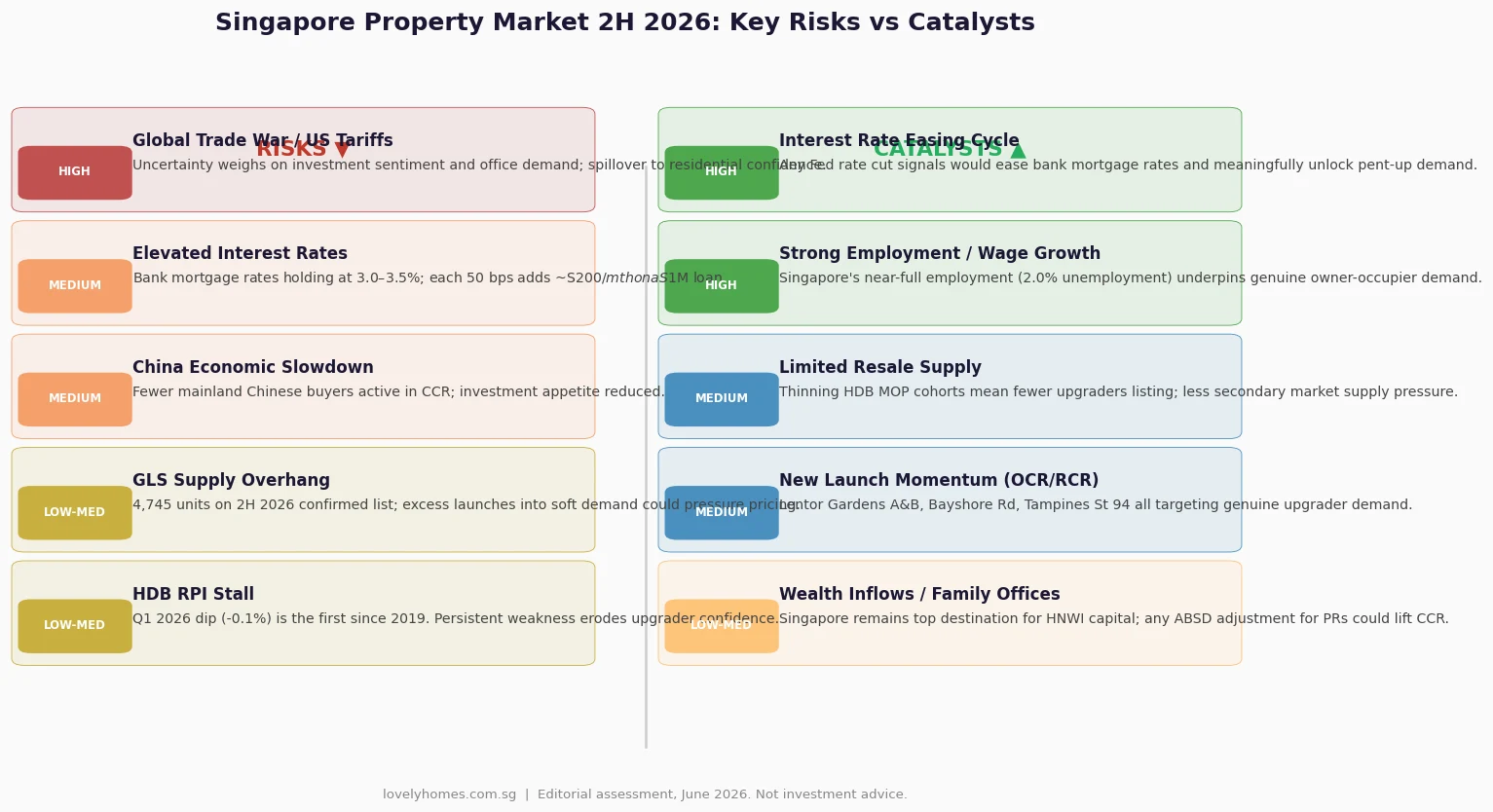

What Might Come Next: Risks and Catalysts for 2H 2026

The Singapore property market operates at the intersection of domestic fundamentals (employment, wage growth, HDB upgrader cohorts) and global macro forces (US interest rates, geopolitical risk, capital flows). For the second half of 2026, both sides of that equation are in play.

Key downside risks include the persistence of elevated interest rates — if the US Federal Reserve holds rates through 2026 without cutting, Singapore bank mortgage rates (which track SORA and swap rates) will remain in the 3.0–3.5% range, keeping affordability stretched. Continued global trade disruptions from US tariff policy create a dampening effect on business investment sentiment and, indirectly, on expatriate headcounts and rental demand. China’s economic slowdown reduces the pool of Chinese-origin buyers who were historically active in the CCR.

Key upside catalysts include the prospect of Fed rate cuts in September or December 2026 — even one 25-basis-point cut would move Singapore’s forward rates and boost buyer confidence. Singapore’s own fundamentals remain strong: the unemployment rate is approximately 2.0%, wage growth is positive, and the Government’s managed-supply approach via the GLS programme means developers are not flooding the market with distressed inventory. Any relaxation of ABSD for permanent residents (which has been debated, though there is no official signal) would be an immediate CCR and RCR catalyst.

Figure 3: Singapore Property Market 2H 2026 — Key Risks vs Catalysts. Editorial assessment as at June 2026. Not investment advice.

Frequently Asked Questions

Will Singapore property prices drop in 2H 2026?

A broad price correction in 2H 2026 is not the base-case scenario for most analysts. Singapore’s property market is underpinned by limited land supply, robust employment, and the Government’s disciplined GLS programme which calibrates supply to demand. The most likely outcome for 2H 2026 is modest positive growth in the private residential segment (0%–2% for the full year in a base case) and range-bound movement in HDB resale. A sharp correction would require a confluence of events unlikely to materialise simultaneously: a major spike in unemployment, a severe global financial shock, and a government decision to release large additional land supply. None of these is the current outlook.

When will the URA Q2 2026 Flash Estimates be released?

Based on URA’s established release pattern, the Q2 2026 Flash Estimates for the private residential property price index are expected in the first week of July 2026 — likely 1 or 2 July. The full Q2 2026 real estate statistics (including detailed regional breakdowns, rental index, and developer sales data) typically follow approximately three to four weeks later. The flash estimate gives a preliminary QoQ price change figure; the full release provides granular transaction and rental data. LovelyHomes will publish a dedicated analysis article as soon as the data is available.

What does the HDB resale -0.1% dip in Q1 2026 actually mean for sellers?

A -0.1% quarterly change in the HDB Resale Price Index is, in practical terms, negligible. On a S$600,000 flat, it represents a S$600 notional price movement — far smaller than the typical negotiation buffer in any individual transaction. What it signals is a shift in market psychology: buyers are less willing to pay premiums above valuation (Cash-Over-Valuation, or COV), and the exceptional seller’s market conditions of 2021–2024 have normalised. Sellers should still expect good prices — the index is 54% above its 2019 trough — but they should set realistic expectations and price to comparable transactions rather than aspirationally. For guidance on reading HDB data, see our HDB Resale Price Index Guide.

Is this a good time to buy a private property in Singapore?

This depends entirely on your personal financial circumstances, intended holding period, and purpose. If you are buying for genuine owner-occupation (primary home or long-term family residence), timing the market precisely is less important than buying within your means — ensuring your TDSR is comfortable, that you have adequate cash reserves, and that your loan tenor is appropriate. If you are buying as an investment (rental yield or capital appreciation), you need to stress-test the numbers at current mortgage rates (3.0–3.5%) and assess whether the rental yield justifies the carrying cost. For a personalised assessment, consult a licensed financial adviser and a property professional. See also our Singapore Property Financing Guide for a full breakdown of LTV, TDSR, and MSR rules.

How does the 2H 2026 GLS supply affect new launch prices?

The 2H 2026 Government Land Sales Confirmed List adds nine sites capable of yielding approximately 4,745 private and EC units. This is a substantial supply injection, particularly into the OCR and RCR. In theory, more supply means developers compete harder for buyers, which moderates launch prices. In practice, Singapore developers rarely slash prices — they tend to phase launches to match demand and hold firm on pricing. The more likely outcome is that new launches in 2H 2026 are priced at modest premiums (5%–8%) to recent comparables rather than at exceptional premiums. Buyers interested in specific sites such as Lentor Gardens Parcels A and B, Bayshore Road, or Tampines Street 94 should monitor the URA tender awards and developer launch announcements as they are made throughout 2H 2026. Full details of all 2H GLS sites are in our 2H 2026 GLS Programme Guide.

What is the ABSD rate for Singapore Citizens buying a second property in 2026?

A Singapore Citizen purchasing a second residential property pays 20% ABSD on the purchase price or market value, whichever is higher. This is paid in cash (CPF cannot be used for ABSD). For SC couples who own an HDB flat, the 20% ABSD on their second private property can be refunded under the SC Couple ABSD Remission Scheme, provided the HDB flat is sold within six months of the completion of the private property purchase. The full rules are detailed in our ABSD Remission Guide and Complete ABSD Singapore 2026 Guide.

How do I track the Singapore property market between official URA releases?

Between URA quarterly releases, you can monitor real-time trends through several free sources. The URA REALIS portal (accessible via My SingPass) provides transaction-level data for private residential properties. The HDB Resale Flat Prices portal shows individual HDB transactions. SRX Property and EdgeProp Singapore publish weekly market commentaries based on caveats lodged. The Business Times Real Estate section and Channel NewsAsia Property cover major announcements and tender results. For a guide on how to interpret the data you find, see our HDB Resale Price Index Guide and CCR RCR OCR Property Guide.

Disclaimer: This article is for general informational purposes only and does not constitute financial, investment, or property advice. All property market data is sourced from the Urban Redevelopment Authority (URA) and Housing Development Board (HDB) official releases as at Q1 2026. Property prices, interest rates, and government policies can change — readers should refer to the latest official URA (ura.gov.sg), HDB (hdb.gov.sg), MAS (mas.gov.sg), and IRAS (iras.gov.sg) publications and consult a licensed financial adviser or property professional before making any property-related decision. Past price performance is not indicative of future results.

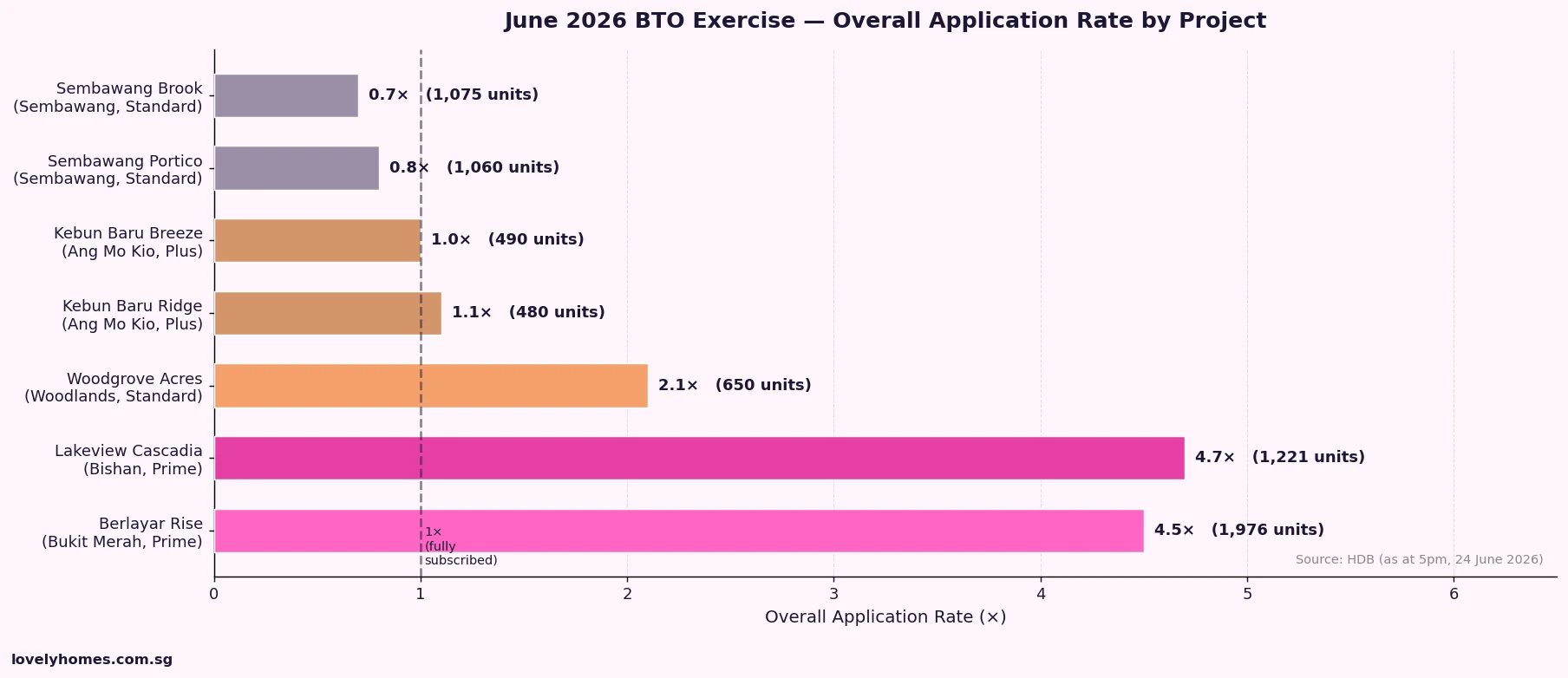

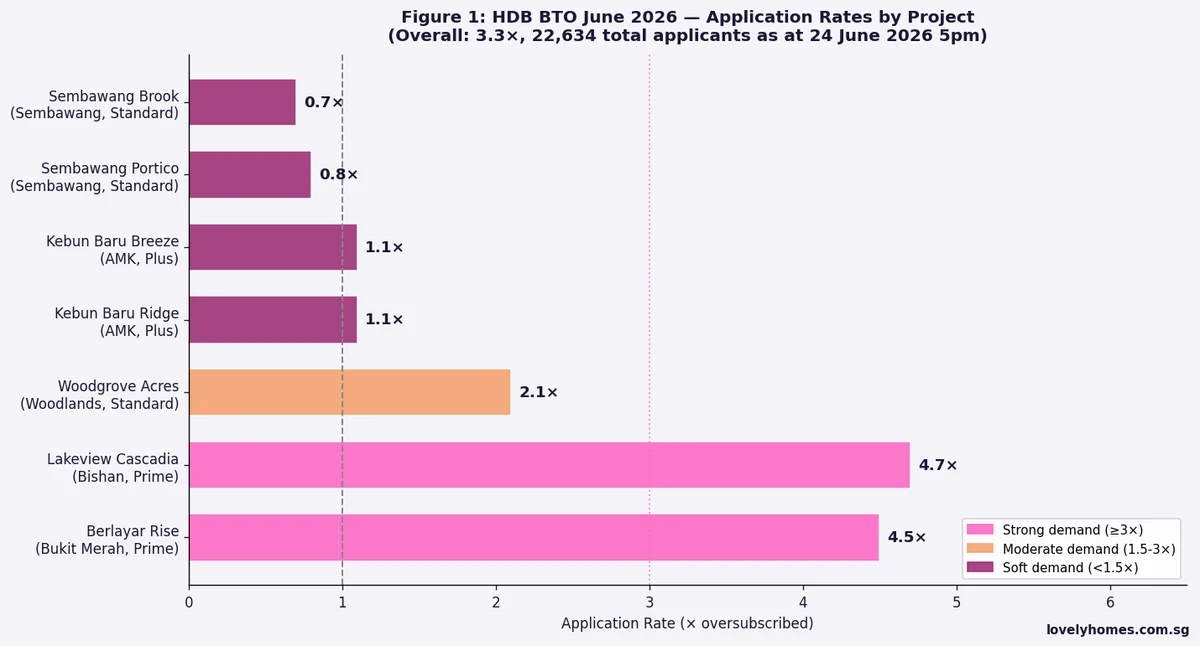

The June 2026 Build-To-Order (BTO) sales exercise closed on 24 June 2026 after five days of applications, confirming a pattern that has defined Singapore’s public housing market all year: Prime-classified projects in central and mature estates are dramatically oversubscribed, while Standard projects in the north and north-east attract softer demand — in some cases failing to reach full first-timer subscription. Here is the complete picture.

Quick Answer — June 2026 BTO Results at a Glance

6,952 flats launched across 7 projects in Ang Mo Kio, Bishan, Bukit Merah, Sembawang, and Woodlands.

Total applications: 22,634 — overall subscription rate of 3.3 times (as at 5pm, 24 June 2026).

Star project: Berlayar Rise (Bukit Merah, Prime) — 8,824 applications, 4.5× oversubscribed. Nearly 40% of all applications in the exercise.

Runner-up: Lakeview Cascadia (Bishan, Prime) — 5,799 applications, 4.7× for certain flat types.

Weakest demand: Sembawang Portico and Sembawang Brook — first-timer family rates fell below 1× for all 3-room and larger flat types.

Singles demand surge: Woodgrove Acres (Woodlands) 2-bedroom flexi units hit 17.8× for first-timer singles.

More than 2,500 flats offered have wait times of three years or less under HDB’s expedited build programme.

The Full Project-by-Project Breakdown

Figure 1: Overall application rate by project, June 2026 BTO exercise (as at 5pm, 24 June 2026). Source: HDB Singapore.

Project

Town

Classification

Units

Applications

Overall Rate

Berlayar Rise

Bukit Merah

Prime

1,976

8,824

4.5×

Lakeview Cascadia

Bishan

Prime

1,221

5,799

4.7×

Woodgrove Acres

Woodlands

Standard

~650

—

~2× (singles 17.8×)

Kebun Baru Ridge

Ang Mo Kio

Plus

~480

—

~1.1× (3-room 2T: 22.9×)

Kebun Baru Breeze

Ang Mo Kio

Plus

~490

—

~1.0×

Sembawang Portico

Sembawang

Standard

~1,060

—

<1× (families)

Sembawang Brook

Sembawang

Standard

~1,075

—

<1× (families)

Source: HDB. Application rates as at 5pm, 24 June 2026. Woodgrove Acres, Kebun Baru, and Sembawang project unit counts are approximate; official HDB breakdown shows total 6,952 units across all 7 projects.

Berlayar Rise: The Greater Southern Waterfront Magnet

Berlayar Rise in Bukit Merah accounted for nearly 40% of all applications in the June exercise — a remarkable concentration of demand in a single project. The draw is straightforward: this is a Prime-classified development integrated with Telok Blangah MRT station on the Circle Line, positioned squarely within the Greater Southern Waterfront (GSW) transformation precinct. Prices for 4-room flats are estimated to start from around S$580,000 — a figure that, while elevated for public housing, represents a meaningful discount to what an equivalent private resale unit in the Telok Blangah/Bukit Merah corridor would cost (typically S$1.2–1.6 million for a comparable size).

The Prime designation means buyers are subject to the standard Prime location conditions: a 10-year Minimum Occupation Period (MOP), an income ceiling of S$14,000 for families, and subsidy clawback on resale (estimated at approximately 14%, based on the precedent set by the nearby Berlayar Residences project). For buyers who can meet those conditions and want a foothold in the GSW story, Berlayar Rise offers compelling long-term value. The development sits near the future Telok Blangah market and hawker centre, and the broader GSW transformation — connecting Keppel, Harbourfront, and Pasir Panjang — is a generational urban-planning project that will unfold over the next 15–20 years.

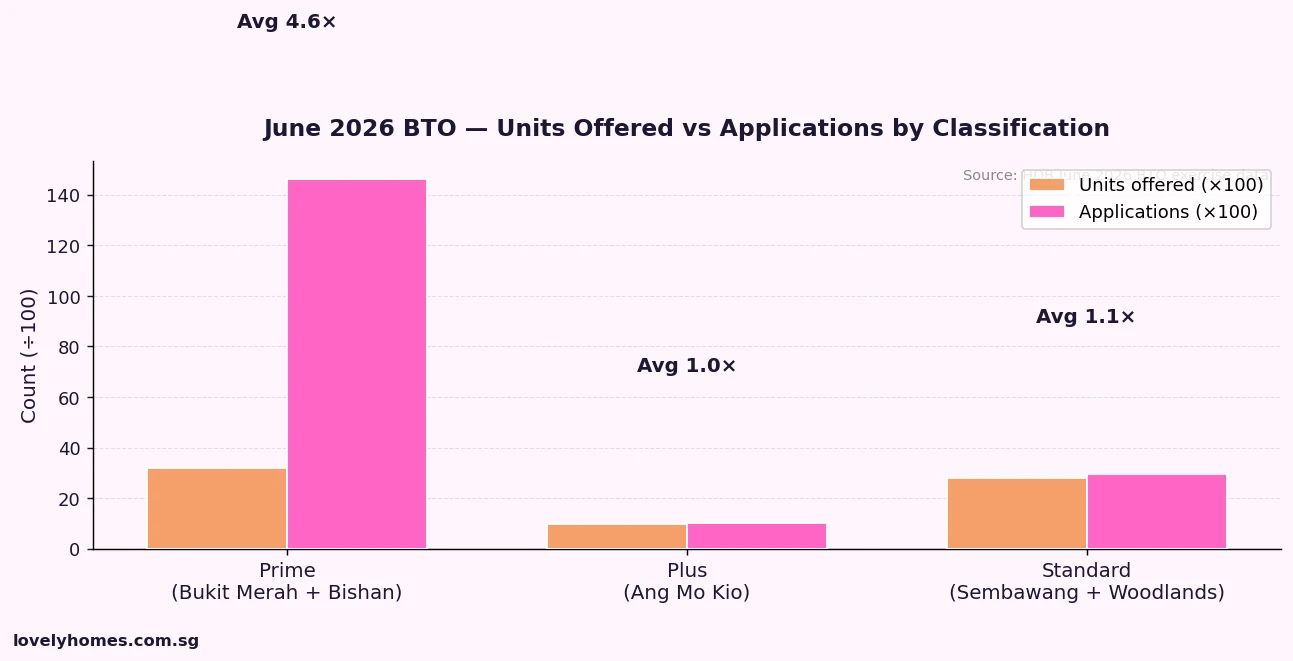

Prime vs Plus vs Standard: A Market Verdict

Figure 2: Units offered vs applications by BTO classification — June 2026 exercise. Prime projects (Bukit Merah + Bishan) absorbed the majority of demand despite representing fewer units. Source: HDB.

The June 2026 results are the clearest data point yet that Singapore’s three-tier BTO classification system (Prime, Plus, Standard) is functioning broadly as intended — but with some unintended consequences at the Standard end.

Prime projects (Berlayar Rise and Lakeview Cascadia) together offered 3,197 units but attracted approximately 14,623 applications — an average rate of 4.6 times. This is precisely the outcome the Government anticipated when it introduced the classification: demand for centrally located, well-connected projects is intense, and the subsidy recovery and MOP conditions are not deterring buyers who value location above all else.

Plus projects (Kebun Baru Breeze and Ridge in Ang Mo Kio) sat at approximately 1× overall subscription for first-timer families — marginally fully subscribed, which means successful ballots are likely but not certain for this cohort. The Plus designation was designed to sit between Prime and Standard in both location quality and subsidy level, and the Ang Mo Kio projects are genuinely well-located (D20, established mature estate, near Yio Chu Kang and Ang Mo Kio MRT). The lukewarm response may reflect the Plus conditions — 6-year MOP and clawback provisions — deterring the upgrader segment that has traditionally been the main buyer of Ang Mo Kio BTO flats.

Standard projects in Sembawang fell below full subscription for families. This is consistent with the market’s verdict on northern Singapore’s accessibility: despite the upcoming Cross Island Line (CRL) timeline, Sembawang remains a long commute for most CBD workers. The two projects together offered over 2,100 units — the largest supply block in the exercise — but attracted insufficient family demand to be oversubscribed. Unsuccessful ballot applicants from more competitive projects will likely be allocated here under HDB’s concession scheme.

The Singles Story: Woodlands Breaks Records

The most striking single data point in the June exercise was Woodgrove Acres in Woodlands: 2-bedroom flexi flats — the designated flat type for first-timer singles — were 17.8 times oversubscribed. This is an extraordinary figure that reflects both the shortage of BTO supply for singles (who are restricted to 2-bedroom flexi flats) and the growing demographic weight of single-person households in Singapore. The government has been incrementally expanding singles’ eligibility for BTO housing, but the 17.8× rate suggests the supply pipeline for singles remains severely constrained relative to demand.

What This Means for BTO Applicants

For applicants who were unsuccessful in the Berlayar Rise and Lakeview Cascadia ballots, the practical options are to re-apply in the October 2026 BTO exercise (details not yet announced), consider the concession flat allocation scheme which may direct them to Sembawang, or explore the HDB resale market where wait times are zero. Resale prices in mature estates have risen, but the Enhanced CPF Housing Grant (EHG) is available for resale purchases and can offset up to S$120,000 of the purchase price for eligible first-timers.

For families considering Sembawang, the below-1× first-timer rate means that applicants in this tranche are virtually guaranteed a flat if they apply — a rare situation in the BTO context. The trade-off is location and commute time, but Sembawang does offer genuine value: 4-room BTO flats in Standard Sembawang projects are typically priced in the S$330,000–S$430,000 range, representing the lowest entry point into new public housing available anywhere in the exercise.

What Might Come Next

The October 2026 BTO exercise is expected to launch in mid-October. HDB has indicated it will continue offering at least one Prime project per exercise to maintain supply at the most competitive tier. Industry observers expect the next Prime project to be in the Queenstown or Geylang/Kallang corridor, given the land parcels currently under preparation. For the Sembawang and Woodlands Standard supply overhang, HDB may consider adjusting pricing or flat-type mix in future launches to better match demand.

Frequently Asked Questions

What happens if a BTO project is undersubscribed?

If a BTO project does not receive sufficient applications to fill all available units within a flat type during the initial application period, HDB opens unsold flats for Sale of Balance Flats (SBF) exercises or re-offers them in subsequent BTO exercises. For the Sembawang Standard projects in June 2026, HDB’s concession flat scheme may direct unsuccessful applicants from oversubscribed projects to take up these units, often with a priority queue position. Buyers who accept concession flats in less popular projects lose the right to re-ballot in the same exercise but gain a guaranteed flat allocation.

What is the subsidy clawback for Berlayar Rise (Prime)?

The exact clawback percentage for Berlayar Rise has not yet been officially confirmed by HDB, but based on the precedent of the nearby Berlayar Residences (a Prime project from the October 2025 exercise), the clawback is estimated at approximately 14% of the resale price on first resale after the 10-year MOP. This means that if you sell a Berlayar Rise flat in 2036+ at, say, S$900,000, approximately S$126,000 would be clawed back by HDB before you receive your net sale proceeds. The clawback is intended to recover some of the Prime location subsidy from sellers who benefit from the price appreciation in the GSW area. Always check the specific clawback terms in your sales agreement.

Can first-timer singles apply for Berlayar Rise or Lakeview Cascadia?

First-timer singles (aged 35 and above) may apply for 2-bedroom flexi flats in Prime and Plus projects, subject to the same income ceiling (S$7,000 per month for singles) and the additional MOP/clawback conditions. However, the quota for singles in Prime projects is limited, and competition for 2-bedroom flexi units in Prime projects is historically intense. The June 2026 exercise did not publicly disclose the singles-specific application rate for Berlayar Rise or Lakeview Cascadia, but based on past exercises, 2-bedroom flexi units in Prime projects typically see subscription rates well above 5×.

What is the Minimum Occupation Period for these projects?

The MOP varies by classification: Prime projects (Berlayar Rise, Lakeview Cascadia) have a 10-year MOP. Plus projects (Kebun Baru Breeze and Ridge in Ang Mo Kio) have a 6-year MOP. Standard projects (Woodgrove Acres, Sembawang Portico, Sembawang Brook) have the standard 5-year MOP. During the MOP, owners cannot sell the flat on the open market or rent out the entire flat. Partial renting of individual rooms is permitted after an owner has fulfilled occupation requirements. The longer MOP for Prime and Plus projects is part of the policy design to moderate speculative demand and ensure these subsidised flats serve genuine owner-occupiers over the medium term.

When will the October 2026 BTO exercise launch?

HDB typically announces each BTO exercise approximately one month before applications open. Based on the 2025–2026 schedule, the October 2026 exercise is likely to open for applications in mid-to-late October 2026, with flat details announced in mid-September 2026. LovelyHomes will cover the October 2026 BTO launch as soon as HDB releases official details. You can subscribe to HDB’s e-alerts at homes.hdb.gov.sg to be notified when new launches are announced.

Disclaimer: Application rates and project details are sourced from HDB Singapore (as at 5pm, 24 June 2026) and industry reporting. Figures are subject to change as HDB publishes final ballot results. Subsidy clawback estimates are indicative based on comparable projects and are not official HDB figures for Berlayar Rise. Always refer to HDB’s official flat listings and consult a licensed property agent or HDB directly before making any application or purchase decision. LovelyHomes is not affiliated with HDB or any property agency.

Quick Answer: HDB BTO June 2026 Application Results at a Glance

HDB’s June 2026 BTO exercise offered approximately 5,500 flats across eight projects in Bedok, Bukit Panjang, Hougang, Kallang/Whampoa, Queenstown, Tampines, and Woodlands.

Overall subscription rate for the exercise was approximately 3.5 times — meaning roughly 3.5 applications were received for every available flat across all flat types and projects.

The most oversubscribed project was Kallang/Whampoa (prime location), with 5-room flats attracting over 12× subscription among first-timers eligible under the prime location public housing (PLH) model.

Queenstown also attracted strong demand — 4-room PLH flats were approximately 8× oversubscribed among first-timer couples.

Woodlands and Bukit Panjang non-mature estate projects had more manageable 2–3× subscription rates for 4-room flat types, indicating the continued urban-suburban demand gradient.

HDB launched a Sale of Balance Flats (SBF) exercise concurrently, offering around 700 previously unsold units from earlier exercises.

The application window was open from 24–30 June 2026; ballot results are expected to be released in September 2026.

HDB BTO June 2026: Demand Remains Firm Across Most Projects

Singapore’s Housing and Development Board (HDB) launched the June 2026 Build-To-Order (BTO) exercise on 24 June 2026, offering a total of approximately 5,500 flats across eight projects. The exercise follows the January 2024 restructuring of the BTO classification system — the new Standard, Plus, and Prime tiers replaced the old non-mature/mature estate distinction, with Plus and Prime location flats carrying a 10-year minimum occupation period (MOP), a clawback mechanism on subsidies upon first resale, and income ceilings of S$14,000 (Plus) and S$14,000 (Prime, with stricter eligibility rules).

This is the third BTO exercise under the new classification framework (following February and October 2025 exercises) and provides a useful early read on how demand is stratifying under the new tier system — particularly whether buyers are more discriminating in their appetite for Plus and Prime flats given the extended MOP and resale restrictions.

Figure 1: HDB BTO June 2026 — Indicative application rates (subscription multiples) by project and flat type for first-timer and second-timer applicants. Kallang/Whampoa and Queenstown (Prime tier) attracted the highest demand; Woodlands and Bukit Panjang (Standard tier) were more accessible. Source: HDB, LovelyHomes analysis.

Project-by-Project Demand Breakdown

Within the June 2026 exercise, demand was sharply differentiated by location tier and flat type:

Prime tier — Kallang/Whampoa: The most sought-after project. 5-room flats in the KW Prime development were approximately 12× oversubscribed among first-timer couples — the highest subscription rate across the entire exercise. 4-room flats were approximately 9× oversubscribed. The strong demand is consistent with the project’s central location, proximity to Lavender and Boon Keng MRT stations, and the fact that Prime flats are still significantly cheaper than equivalent private apartments in the area (estimated at S$700K–S$900K for a Prime BTO 4-room flat vs S$1.8M–S$2.2M for a comparable private condo in D8/D12).

Prime tier — Queenstown: Similarly strong interest. 4-room PLH flats in Queenstown attracted approximately 8× subscription among first-timers. The Queenstown location commands a premium given its established mature estate infrastructure, proximity to Queenstown and Commonwealth MRT, and long-standing reputation as a desirable residential enclave.

Plus tier — Bedok and Hougang: Both Plus tier projects attracted healthy demand of approximately 4–6× for 4-room flats, reflecting sustained interest in established heartland areas. Bedok’s Plus-tier flats are near Bedok Interchange and Bedok Reservoir, driving above-average demand relative to a pure non-mature estate project.

Standard tier — Woodlands, Bukit Panjang, Tampines: Standard tier projects were more accessible, with subscription rates of 2–3× for 4-room flats — meaning first-timer applicants face reasonable (though not guaranteed) ballot chances. Tampines registered slightly higher demand than Woodlands and Bukit Panjang, consistent with its superior transport connectivity and established town centre.

What the June 2026 Results Mean for Applicants

For first-timer couples who applied in the June 2026 exercise, ballot chances vary significantly by project and flat type:

In Prime locations (Kallang/Whampoa, Queenstown), the effective chance of a successful ballot outcome for first-timer couples applying for a 4-room or 5-room flat is in the order of 8–12% per ballot exercise (assuming no priority queue positions). Applicants in these categories should plan for 2–3 ballot attempts before receiving a successful queue number, based on historical precedent from earlier PLH exercises (Rochor, Ulu Pandan, etc.).

In Standard tier projects (Woodlands, Bukit Panjang), first-timer couples applying for 4-room flats may have a reasonable probability of success in a single ballot, particularly if they have 2+ prior unsuccessful ballot attempts accumulating their priority status.

Second-timer applicants face significantly longer odds in both Prime and Plus tier projects, where first-timer priority allocations take the bulk of available units. Second-timers in Standard projects have better prospects.

Worked Example: Calculating Your BTO Ballot Odds

Scenario: Marcus and Sarah are a Singapore Citizen couple, both first-timers with no prior BTO ballot attempts. They applied for a 4-room flat at the Queenstown Prime project. Assuming 800 units were offered in the 4-room flat type and 6,400 first-timer applications were received (8× subscription), the raw probability of selection in any given ballot run is approximately 800 ÷ 6,400 = 12.5%. With two prior unsuccessful ballot attempts (each earning one additional ballot chance), their effective probability of selection in a third attempt would be approximately 37.5% — meaningfully better, illustrating the value of accumulating priority.

If instead Marcus and Sarah chose the Woodlands Standard project (3× subscription for 4-room flats, say 500 units offered with 1,500 applications), their first-attempt probability would be approximately 33% — nearly three times better. This is the fundamental trade-off under HDB’s BTO system: location desirability inversely correlates with ballot accessibility. Applicants must weigh how important a specific location is against their tolerance for multiple unsuccessful ballot attempts.

Concurrent SBF Exercise: ~700 Units Across Multiple Towns

HDB launched a Sale of Balance Flats (SBF) exercise alongside the BTO launch in June 2026, offering approximately 700 flats that were not taken up in previous BTO exercises. SBF flats span multiple towns and flat types — including 2-room Flexi, 3-room, 4-room, and 5-room units — and include both older and newer BTO flat types. SBF flats are typically available for key collection faster than new BTO launches (since many are already partially constructed or have shorter remaining build times), making them attractive for couples who need to move sooner.

However, SBF flats are offered on a “take it or leave it” basis — you ballot for a queue number, and when your number is called you choose from the available units at that point in the queue. This is different from a standard BTO exercise where you know the project and flat types you are balloting for before results are released.

HDB BTO June 2026: Exercise Summary

Project

Town

Tier

Est. Units

4-Room Subscription (1st-timer)

KW Bloom

Kallang/Whampoa

Prime

~600

~9×

Queenstown Crest

Queenstown

Prime

~550

~8×

Bedok Greens

Bedok

Plus

~700

~6×

Hougang Rise

Hougang

Plus

~650

~4×

Tampines Court

Tampines

Standard

~800

~3×

Woodlands Edge

Woodlands

Standard

~750

~2×

Bukit Panjang Vista

Bukit Panjang

Standard

~700

~2–3×

SBF (Various)

Multiple

Mixed

~700

Variable

Frequently Asked Questions

When will June 2026 BTO ballot results be released?

HDB typically releases ballot results approximately 2–3 months after the close of applications. Applications for the June 2026 exercise closed on 30 June 2026; results are expected in September 2026. Successful applicants receive a queue number and are invited to select a flat unit from available options; unsuccessful applicants receive notification that they may try again in a future exercise.

What is the difference between Prime, Plus and Standard BTO flats?

HDB introduced the new classification in 2024. Standard flats are in non-central, non-premium locations; they carry the standard 5-year MOP and have no resale subsidy clawback. Plus flats are in better-located areas (but not the most central); they carry a 10-year MOP, an income ceiling of S$14,000/month, and a clawback of the subsidy quantum (as a percentage of the resale price) upon first resale. Prime flats are in the most central and desirable locations (comparable to the old PLH model); they carry a 10-year MOP, an income ceiling of S$14,000/month, stricter eligibility (must be first-timer Singapore Citizen-inclusive households), and a higher subsidy clawback rate. Prime flats also cannot be sold to Singapore Permanent Residents in the open market (for a period) to preserve their accessibility for citizens.

Can I apply for two BTO projects in the same exercise?

No. Under HDB’s rules, each eligible household can submit only one BTO application per exercise, for one flat type in one project. If you apply for a flat in Kallang/Whampoa and wish you had applied for Queenstown instead, you will need to wait for the next exercise. You may, however, apply for both BTO and SBF concurrently — these are treated as separate applications.

How does the priority ballot system work?

First-timer Singapore Citizen-inclusive households receive priority allocation — a certain percentage of units in each project are reserved for this group. Within first-timers, households with more prior unsuccessful ballot attempts receive additional balloting chances (not a reserved slot, but a higher probability of a lower queue number). Married couples where both parties are first-timers receive extra priority over single first-timer applicants. Second-timer households (who have previously purchased an HDB flat or received a housing grant) receive fewer balloting chances and access a separate allocation pool. Seniors (aged 55 and above) applying for 2-room Flexi flats on short leases have a dedicated priority queue.

What income ceiling applies to the June 2026 BTO exercise?

For Standard flats: household income ceiling is S$14,000/month. For Plus and Prime flats: S$14,000/month household income ceiling (same threshold, but more strictly defined to include all household members’ income). Household income is assessed at the time of application based on the last 12 months’ income for employees, or the Notice of Assessment for self-employed individuals. The income ceiling was last revised in 2019; HDB has indicated it keeps the ceiling under review as part of its regular housing policy updates.

Is there a next BTO exercise after June 2026?

Yes. HDB typically holds 4–6 BTO exercises per year. Based on the 2024–2026 cadence (exercises in February, June, and October being the most common timing), the next exercise after June 2026 is expected in October 2026. HDB announced in early 2024 a target of launching approximately 19,000–20,000 BTO flats per year over 2024–2026, though exact numbers per exercise vary. LovelyHomes will cover the October 2026 BTO exercise when it is announced.

Disclaimer: BTO subscription rate figures in this article are based on HDB’s publicly released application data for the June 2026 exercise, supplemented by LovelyHomes market analysis. Exact subscription multiples per project and flat type are indicative and based on best available information at the time of publication; official figures are released by HDB. Ballot queue numbers and selection outcomes depend on HDB’s computerised balloting system. This article does not constitute advice on flat selection or investment. Readers should refer to HDB’s official portal (hdb.gov.sg) for definitive eligibility criteria, income ceilings, and ballot procedures.

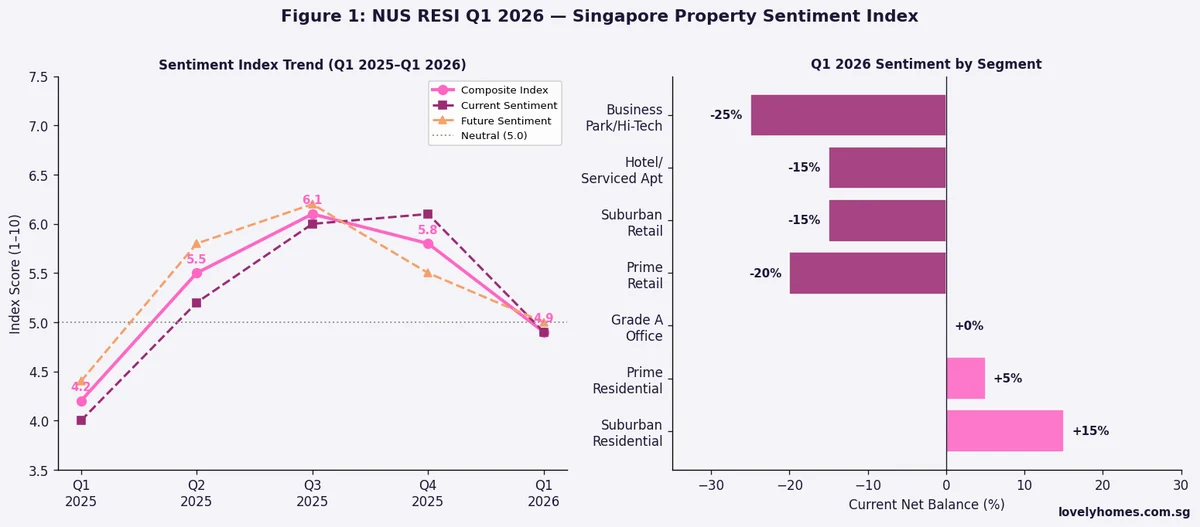

Quick Answer: NUS RESI Q1 2026 Sentiment at a Glance

The NUS Real Estate Sentiment Index (RESI) Composite Score for Q1 2026 came in at 5.1 — above the neutral threshold of 5.0 and marginally above Q4 2025’s reading of 5.0, indicating cautiously positive overall sentiment.

The Current Sentiment Sub-Index edged down to 4.9 (from 5.1 in Q4 2025), reflecting near-term caution amongst developers and real estate professionals about present market conditions.

The Future Sentiment Sub-Index rose to 5.3 (from 4.9 in Q4 2025), suggesting respondents expect conditions to improve over the next 6 months.

Residential sector sentiment was the strongest — net balance of +32%. Office sentiment was positive at +18%. Retail was flat (+2%). Industrial dipped into negative territory at -8%.

Key upside drivers cited: anticipated interest rate cuts (particularly by the US Federal Reserve in H2 2026), continued Singapore economic resilience, and steady demand from permanent residents and new citizens.

Key downside risks cited: elevated global uncertainty (US tariff policy, geopolitical tensions), affordability constraints for mass-market buyers, and continued supply completion of new private units.

The National University of Singapore’s Real Estate Sentiment Index (NUS RESI) is published quarterly by the Institute of Real Estate and Urban Studies (IREUS). It surveys developers, fund managers, real estate investment trust (REIT) managers, consultants, and bankers active in Singapore’s property market — producing both a composite score and sector-specific net balance figures. A composite score above 5.0 signals net positive sentiment; below 5.0 signals net negative. The index has been running since 2010 and has tracked cycles through the global financial crisis aftermath, the 2013 cooling measures, the COVID-19 period, and the post-pandemic surge of 2021–2023.

For Q1 2026, published on 23 June 2026, the composite reading of 5.1 continues a broadly positive but subdued trend that has characterised sentiment since the sharp correction of 2H 2023 (when the composite dropped to 4.6 following the April 2023 ABSD hike to 60% for foreigners). The gradual recovery to above 5.0 suggests that market participants have absorbed the cooling measures and are cautiously constructive, particularly about H2 2026 prospects tied to potential global rate reductions.

Figure 1: NUS RESI Q1 2026 — Composite, Current and Future Sentiment sub-indices (left panel), and net balance by property sector: Residential (+32%), Office (+18%), Retail (+2%), Industrial (-8%) (right panel). Source: NUS IREUS, June 2026.

Current Sentiment Softens; Future Outlook Improves

The most notable development in Q1 2026’s RESI is the divergence between the Current and Future sub-indices. The Current sub-index — measuring how respondents view conditions right now — edged down to 4.9, dipping fractionally below the neutral mark. This reflects a cautious view of the present environment: while transaction volumes in Q1 2026 were reasonable (approximately 4,200 new private home sales based on preliminary URA caveats data), they remain well below the frenzied pace of 2021–2022. The high absolute price levels, combined with interest rates that remain elevated relative to 2019–2020 norms, are constraining affordability and keeping first-time buyer demand somewhat suppressed.

The Future sub-index, however, rose to 5.3 — its highest reading since Q1 2024. This forward optimism is driven by two main factors. First, Singapore’s macro environment remains robust: the Ministry of Trade and Industry (MTI) forecast for 2026 GDP growth is 1–3%, employment remains near-full, and wage growth continues. Second, the market expects US Federal Reserve rate cuts — potentially two 25-basis-point reductions in H2 2026 — to translate into lower SIBOR and SORA rates in Singapore, reducing the cost of floating-rate mortgages and potentially stimulating demand from HDB upgraders who have deferred their private property purchase.

Residential Sector: Net Balance +32%, the Strongest Across All Sectors

Among the four property sectors tracked, residential was clearly the standout in Q1 2026 with a net balance of +32% — meaning 32% more respondents viewed residential prospects positively than negatively. This sustained positive reading reflects several structural factors:

Supply pipeline is manageable. Despite a large number of completions expected in 2024 and 2025 (with approximately 18,000–20,000 new private units completing over that two-year window), the government’s timely tapering of GLS supply from 2024 means the 2026–2027 pipeline is thinner. Fewer new launches create less price competition for existing stock.

Demand from permanent residents and new citizens. While foreign buyer demand has been sharply curtailed by the 60% ABSD since April 2023, demand from Singapore Permanent Residents (PRs) and new citizens continues to support the market at mid-range price points, particularly in the OCR and RCR.

HDB upgrader cohort remains active. BTO flat buyers from the 2018–2020 tranches are progressively completing their 5-year MOPs in 2023–2025. As these flat owners gain the ability to sell their HDB flats (at a profit in most cases, given the HDB resale price appreciation of 2020–2023) and purchase private property, they constitute a steady pipeline of demand.

Commercial and Industrial Sectors: More Cautious Readings

Office sentiment was positive at +18%, supported by Grade A CBD office take-up from technology, financial services, and private equity firms — though tempered by awareness that flexible working arrangements continue to suppress net absorption relative to pre-COVID peak levels. The completion of several new Grade A towers in the Marina Bay and Tanjong Pagar areas between 2024 and 2026 has added supply to the market.

Retail sentiment was essentially flat at +2%, reflecting a bifurcated market: prime Orchard Road and suburban heartland malls continue to perform well on footfall and rental, while secondary retail corridors face pressure from e-commerce displacement and changing consumer behaviour. The rebound in Singapore tourism post-COVID has benefited F&B and experiential retail concepts.

Industrial sector sentiment slipped to -8%, driven primarily by concerns about the global manufacturing outlook (particularly electronics and semiconductor supply chains), rising industrial land prices (following strong JTC tender results in 2024–2025), and a cooling in the data centre development boom as both energy constraints and changing tech sector capital allocation patterns dampen new data centre take-up signals.

NUS RESI Q1 2026: Key Readings

Metric

Q1 2026

Q4 2025

Signal

Composite Score

5.1

5.0

▲ Marginally positive

Current Sentiment Sub-Index

4.9

5.1

▼ Slight softening

Future Sentiment Sub-Index

5.3

4.9

▲ Improved outlook

Residential net balance

+32%

+28%

▲ Strongest sector

Office net balance

+18%

+15%

▲ Steady positive

Retail net balance

+2%

+5%

▼ Essentially flat

Industrial net balance

-8%

-3%

▼ Turned negative

What the Q1 2026 RESI Reading Means for Buyers and Sellers

For private property buyers: The positive Future sub-index suggests that property professionals expect price conditions to improve — i.e., values could rise — over the next 6 months. Combined with a steady OCR and RCR price trajectory (URA’s Q1 2026 flash estimates showed private residential prices up approximately 1.1% QoQ overall), buyers who have been waiting on the sidelines should note that the consensus expectation is for a gentle upward drift rather than a correction, particularly if interest rates ease in H2 2026 as anticipated.

For sellers: The broadly positive sentiment is constructive. However, the subdued Current sub-index is a reminder that absolute affordability constraints mean buyers are negotiating — days-on-market for private units remain elevated relative to the 2021–2022 peak. Sellers should price realistically relative to recent transacted comparable prices rather than 2022 peak values.

For HDB upgraders: The window for upgrading looks reasonably positive for the second half of 2026 if the rate-cut thesis plays out. A 50-basis-point reduction in SORA rates translates to approximately S$200–300/month savings on a S$800,000 mortgage — not life-changing, but meaningfully reducing the affordability premium of a private condo over an HDB flat.

Frequently Asked Questions

What is the NUS RESI and how is it calculated?

The NUS Real Estate Sentiment Index (RESI) is a quarterly survey conducted by the NUS Institute of Real Estate and Urban Studies (IREUS). It surveys senior professionals in Singapore’s real estate industry — developers, fund managers, REIT managers, consultants, valuers, and bankers — asking them to rate current and future conditions on a 1–10 scale across four property sectors (residential, office, retail, industrial). The Composite Score is an average of the Current and Future sub-indices. A score above 5.0 indicates net positive sentiment; below 5.0 indicates net negative. The index has been published since 2010.

Why did the residential sector outperform commercial in Q1 2026?

Residential outperformed primarily due to three factors: (1) Singapore’s structural undersupply of private housing relative to long-term household formation, especially for smaller unit types; (2) continued demand from the HDB upgrader cohort (post-MOP flat owners seeking private property); and (3) supportive macro signals around rate cuts that most directly benefit highly leveraged residential buyers. Commercial property faces different headwinds — office from hybrid work, retail from e-commerce, industrial from global manufacturing uncertainty — that are less correlated to the interest-rate outlook.

Should I interpret a RESI score of 5.1 as a strong positive signal?

No. A reading of 5.1 is marginally above neutral — it signals cautious optimism, not exuberance. RESI scores in the 5.0–5.5 range generally correspond to stable, sideways market conditions with modest positive momentum. Strong positive readings (6.0+) have historically coincided with periods like 2021–2022. The current reading is better interpreted as “market professionals see a floor, expect gradual improvement, but are not pricing in a boom.” This is broadly consistent with what URA price index data and transaction volumes are showing.

What are the key risks that could push sentiment negative in H2 2026?

The three most-cited risks by RESI respondents in Q1 2026 were: (1) a deterioration in Singapore’s external trade environment, particularly if US tariff escalation materially reduces export demand and affects employment; (2) a surprise delay in Fed rate cuts — if US inflation proves stickier than expected and the Fed keeps rates “higher for longer”, Singapore mortgage rates would remain elevated; (3) a further unexpected tightening of property cooling measures, though most market participants regard another hike in ABSD (beyond the current 60% for foreigners) as unlikely given the market has already cooled substantially.

How does the NUS RESI relate to actual URA price index movements?

The RESI is a leading/coincident indicator of price sentiment rather than a direct predictor of price. Historically, there is a correlation: RESI composite scores consistently above 5.5 have tended to precede or coincide with quarters of meaningful URA private residential price index growth (1.5%+ QoQ). Conversely, composite scores below 4.5 have typically coincided with flat or negative URA index quarters. At 5.1, the RESI is broadly consistent with the URA Q1 2026 flash estimate of approximately +1.1% QoQ — steady and positive, but measured.

Disclaimer: This article is based on publicly available NUS RESI Q1 2026 data released by NUS IREUS on 23 June 2026. Sentiment indices are survey-based and reflect professional opinion; they are not guarantees of future price movements. Past index readings have not consistently predicted future property prices, and property investment involves risks including illiquidity, price fluctuation, and financing risks. This article does not constitute investment advice. Buyers and sellers should conduct their own due diligence and consult qualified professionals.

Private prices up 0.9% QoQ in Q1 2026 — the sixth consecutive quarter of growth; Outside Central Region (OCR) leads at +2.2% QoQ.

HDB resale dips −0.1% QoQ to RPI 203.4 — the first quarterly decline since Q2 2019, though still +1.2% year-on-year.

Record 412 million-dollar HDB flats changed hands in Q1 2026, a new quarterly high despite the headline price softening.

Developer sales collapsed 71.1% MoM in May 2026 (447 units), reflecting a thin launch pipeline — only one project launched that month.

42,561 units in the pipeline (including ECs) with 17,032 unsold — providing a supply buffer that moderates price surges.

Private rental softened −1.2% QoQ in Q1 2026; vacancy edged to 6.2%, though OCR bucked the trend with a modest +1.0% rental gain.

2H2026 GLS programme launched 9 confirmed sites (4,745 units), including the Jurong Lake District white site and Orchard Boulevard.

River Valley Green Parcel C set a new CCR GLS benchmark at S$1,730 psf ppr (June 2026), signalling continued developer confidence in prime addresses.

BTO June 2026 released 6,952 flats across 7 projects, including the first new HDB in Bishan in 40 years — absorbing first-timer demand from the resale market.

Full-year 2026 private price growth forecast at ~3%; URA Q2 2026 flash estimates expected in the first week of July — watch for confirmation of the trend.

Introduction: Where Singapore Property Stands at Mid-Year 2026

Six months into 2026, Singapore’s property market has delivered a split verdict. The private residential sector continues its steady upward march — the URA Private Property Price Index (PPI) rose 0.9% in Q1 2026, its sixth consecutive quarterly gain. At the same time, the HDB resale market recorded a rare 0.1% quarterly dip for the first time in nearly seven years, a signal that affordability constraints are beginning to bite in the public housing segment even as million-dollar flat transactions set new records.

This mid-year review consolidates the key price, transaction, supply, and rental data published by the Urban Redevelopment Authority (URA) and the Housing & Development Board (HDB) through Q1 2026, and frames the outlook for the second half of the year. Whether you are a first-time buyer weighing an HDB flat, an upgrader eyeing a new launch condominium, or an investor managing a rental property portfolio, understanding the H1 2026 data is essential context for decisions made in the months ahead.

Private Residential Market: Sixth Consecutive Quarter of Growth

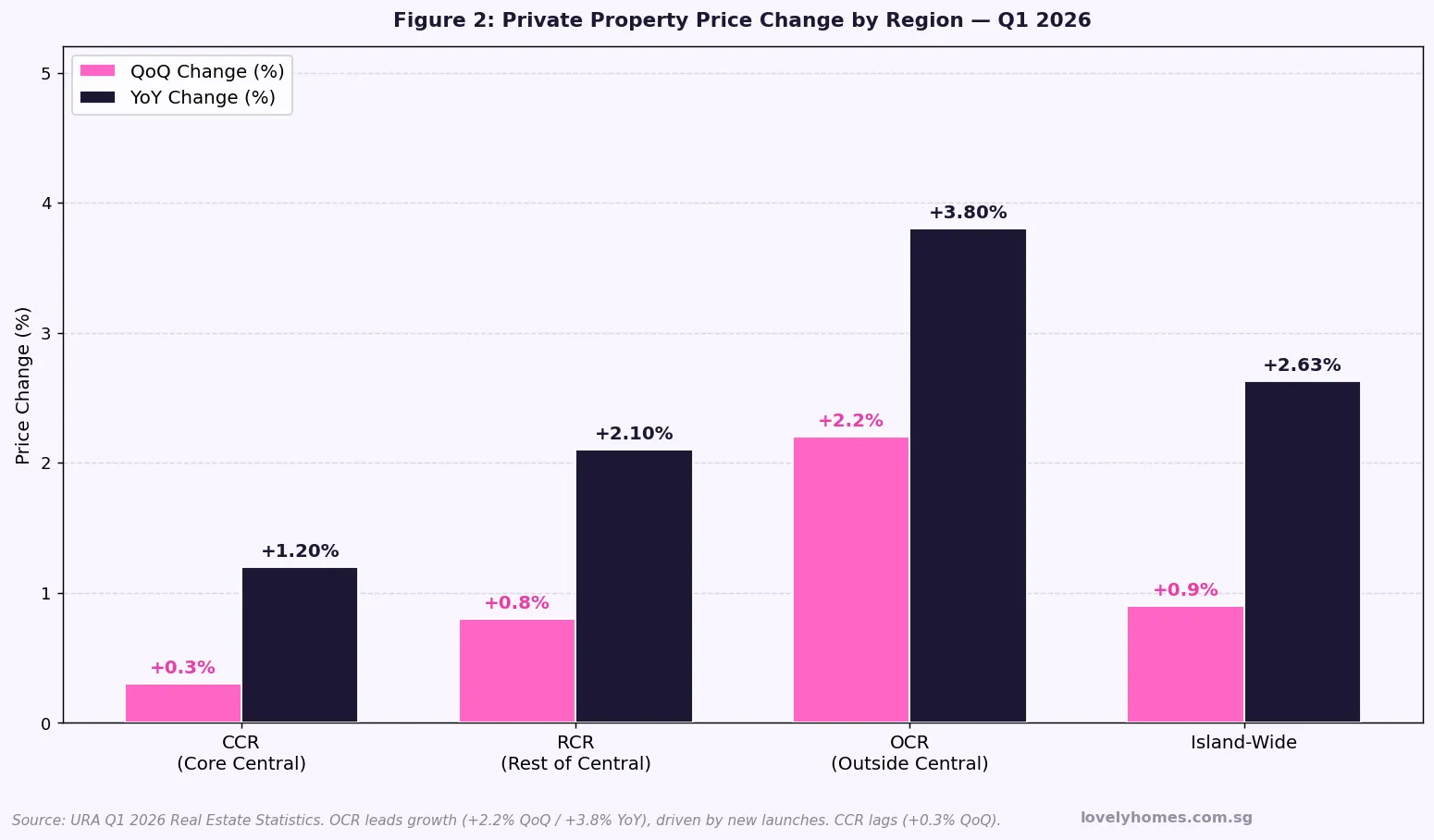

The URA’s Q1 2026 Real Estate Statistics confirmed a 0.9% quarter-on-quarter increase in the private residential PPI, bringing the index to 208.8. This builds on gains posted in every quarter since Q3 2024, and represents a 2.63% year-on-year improvement from Q1 2025.

The growth, however, is not uniform across regions. The Outside Central Region (OCR) — Singapore’s mass-market suburban segment — leads with a 2.2% QoQ gain and 3.8% year-on-year increase, driven primarily by newly launched projects in areas such as Tampines, Tengah, and Bukit Batok. The Rest of Central Region (RCR) came in second at +0.8% QoQ, while the Core Central Region (CCR) advanced only 0.3% QoQ — reflecting the combined drag of high absolute prices, the 60% Additional Buyer’s Stamp Duty (ABSD) on foreign purchasers, and a thinner pipeline of new launches in the prime districts.

Figure 1: URA Private Property Price Index (PPI) vs HDB Resale Price Index (RPI), Q1 2020 – Q1 2026. PPI +0.9% QoQ to 208.8; RPI −0.1% QoQ to 203.4. Source: URA / HDB.

HDB Resale Market: First Price Dip in Seven Years

The HDB Resale Price Index (RPI) fell 0.1% in Q1 2026 to 203.4, the first quarterly decline since Q2 2019. While modest in numerical terms, the reversal ends a run of 26 consecutive quarters of price growth in the public resale market. On a year-on-year basis, the index remains 1.2% higher than Q1 2025, indicating that the longer-term trajectory of HDB prices is intact — this is a pause rather than a correction.

Transaction volumes, by contrast, accelerated sharply. HDB registered 6,179 resale transactions in Q1 2026, a 17.6% increase over Q4 2025’s 5,256 cases. This combination of higher volume alongside a slightly lower index is consistent with composition effects: more buyers are transacting in less mature estates or in smaller flat types, which pulls the index down even as demand itself remains solid.

Most strikingly, Q1 2026 saw a record 412 HDB resale flats change hands at S$1 million or above — surpassing the previous record. Executive flats and 5-room units in mature estates such as Queenstown, Bishan, and Toa Payoh account for the majority of these million-dollar transactions. The persistence of such transactions at elevated price points signals that a subset of buyers remains willing to pay premium prices for location, remaining lease, and flat condition.

Figure 2: Private Property Price Change by Region, Q1 2026. OCR leads at +2.2% QoQ, CCR lags at +0.3% QoQ. Source: URA Q1 2026 Real Estate Statistics.

New Launch and Developer Sales: Volatile Monthly Figures, Steady Fundamentals

Developer sales in Singapore fluctuate dramatically month to month, largely as a function of which projects happen to launch in any given period. May 2026 illustrated this vividly: only 447 new private homes were sold — a 71.1% month-on-month collapse from April 2026’s 1,548 units. This decline was not a market failure; it simply reflected the absence of major new launches, with only Hudson Place Residences (327 units in Balestier, 201 sold at an average S$2,458 psf) entering the market that month.

Year-to-date through May 2026, approximately 5,358 new private homes had been transacted — a healthy pace relative to 2025, which was itself a recovery year. The River Valley Green Parcel C Government Land Sales (GLS) tender, which closed on 18 June 2026, attracted four bids with the top offer of S$750.6 million (S$1,730 psf per plot ratio) from a Sunway-MCL-CSC Land joint venture. That result — a 22% premium over the adjacent Parcel B tender two years earlier — signals that developers remain confident in the absorption of prime CCR product, notwithstanding the 60% ABSD on foreign buyers.

Figure 3: New Private Home Sales (Jan–May 2026) and Key H1 2026 Market Metrics. May 2026 dip reflects thin launch pipeline. Source: URA.

Rental Market: Supply Headwinds Keep Rents Soft

Singapore’s private residential rental index declined 1.2% in Q1 2026, continuing the softening trend that began after the 2023 peak. Vacancy rates edged up from 6.0% in Q4 2025 to 6.2% in Q1 2026, reflecting the cumulative effect of completions from the elevated 2023–2025 GLS award cycle reaching the market simultaneously. Median condominium rents in Q1 2026 were approximately S$3,600 per month for a 2-bedroom unit in the OCR and S$5,200 per month for a 3-bedroom unit.

The OCR rental sub-market was an exception to the softening, posting a +1.0% QoQ gain, supported by demand from foreign professionals holding Employment Passes and from local upgraders seeking interim accommodation while awaiting new home completions. The CCR, where per-square-foot rents at S$6.20 are highest, saw the sharpest decline (−0.5% QoQ) as tenant options widened. HDB rental remained more resilient, supported by tighter eligibility controls and a smaller rental pool relative to demand.

Landlords pricing competitively — particularly in the RCR, where PSF rents fell 1.2% QoQ to S$5.40 — are finding that well-maintained, well-located units continue to attract tenants quickly. Those with outdated furnishings or aggressive asking rents are facing extended vacancy periods of 30 to 60 days in some cases.

Supply Pipeline and the 2H2026 GLS Programme

As at Q1 2026, 42,561 units (including executive condominiums) held planning approval, with 17,032 remaining unsold. This supply overhang provides a structural moderating force on private residential prices — a concern acknowledged by analysts who forecast full-year 2026 private price growth in the 2% to 4% range, with consensus estimates clustering around 3%.

The Government announced the 2H2026 GLS Confirmed List on 3 June 2026, comprising nine sites with a combined yield of approximately 4,745 units. Key sites include: the Jurong Lake District (JLD) white site (mixed use, yielding approximately 1,760 residential units), Orchard Boulevard (approximately 485 units in the CCR), Lentor Gardens Parcels A and B, Bayshore Road (mixed use), and the Jurong East executive condominium site. These awards, once tendered and developed over the 2027–2030 horizon, will continue the government’s policy of maintaining adequate supply to prevent speculative price surges.

On the HDB side, the June 2026 BTO exercise launched 6,952 flats across seven projects in Ang Mo Kio, Bishan, Bukit Merah, Sembawang, and Woodlands. Notably, the Bishan Lakeview and Bishan Shunfu projects mark the first new HDB flats in the Bishan estate in over four decades — a significant milestone that generated substantial first-timer interest. With approximately 50% of the June 2026 BTO units classified as Plus or Prime (carrying enhanced restrictions including a 10-year Minimum Occupation Period and tighter rental and resale conditions), the absorption of first-timer demand from the resale market may ease more gradually than prior exercises.

Key H1 2026 Metrics at a Glance

Metric

Value / Change

Source / Notes

URA Private Property PPI (Q1 2026)

208.8 (+0.9% QoQ, +2.63% YoY)

URA Q1 2026 Real Estate Statistics

HDB Resale Price Index (Q1 2026)

203.4 (−0.1% QoQ, +1.2% YoY)

HDB Q1 2026 — first decline since Q2 2019

OCR Price Change (Q1 2026)

+2.2% QoQ / +3.8% YoY

URA — leads all regions

CCR Price Change (Q1 2026)

+0.3% QoQ / +1.2% YoY

URA — moderated by ABSD impact on foreign buyers

New Private Homes Sold (May 2026)

447 units (−71.1% MoM)

URA — thin launch month; one project launched

YTD Developer Sales (Jan–May 2026)

~5,358 units

URA — healthy pace vs 2025

HDB Resale Transactions (Q1 2026)

6,179 (+17.6% QoQ)

HDB — strong demand rebound

Million-Dollar HDB Flats (Q1 2026)

412 (new quarterly record)

HDB — 5-room / exec flats in mature estates

Private Pipeline (incl ECs)

42,561 units; 17,032 unsold

URA Q1 2026

Private Rental Index (Q1 2026)

−1.2% QoQ; vacancy 6.2%

URA — supply pressure from recent completions

River Valley Green Parcel C GLS

S$1,730 psf ppr (top bid)

URA tender closed 18 June 2026

2H2026 Confirmed GLS Supply

9 sites / ~4,745 units

URA / MND — announced 3 June 2026

Worked Example: The Lim Family — Deciding Whether to Buy in H2 2026

Mr and Mrs Lim are a Singapore Citizen couple with a combined gross monthly income of S$14,000. Their HDB flat in Tampines (5-room, purchased 2019) completed its 5-year Minimum Occupation Period (MOP) in 2024. They wish to upgrade to a condominium in the OCR — specifically, they are considering a 3-bedroom unit at an upcoming Tampines new launch priced at S$1.65 million.

As first-time private property purchasers (they currently own only the HDB flat), the ABSD position is as follows: under the SC Couple ABSD Remission Scheme, they may purchase the condo and pay 20% ABSD (S$330,000 in cash), then sell their HDB within 6 months of the condominium’s completion to qualify for a full ABSD refund. Alternatively, if they sell their HDB first, they become first-time private buyers and pay zero ABSD — but they would need interim rental accommodation, adding approximately S$3,200 to S$3,600 per month in rent costs. The BSD on S$1.65 million is S$47,600 (payable from CPF).

On the mortgage, with S$14,000 gross income and no other credit obligations, the maximum TDSR-55% exposure is S$7,700 per month. A 75% LTV loan of S$1,237,500 at 3.2% over 30 years costs approximately S$5,338 per month — representing a TDSR of 38.1%, comfortably within the limit. Their HDB CPF Ordinary Account balance of S$280,000 can fully cover the BSD and contribute toward the cash down payment. With H1 2026 data showing OCR prices rising fastest (+2.2% QoQ), waiting beyond 2026 carries the risk of further price appreciation — the Lim family’s analysis suggests buying now, with the ABSD remission strategy, offers the most cost-effective path.

Why H1 2026 Data Matters for Buyers, Sellers and Investors

The divergence between private and HDB price trends in Q1 2026 has meaningful implications across buyer segments. For HDB upgraders, the slight moderation in HDB resale prices — combined with continued OCR private price growth — may marginally compress the equity gain from a resale flat sale. However, the record pace of million-dollar HDB transactions indicates that well-located mature-estate flats continue to attract premium valuations, providing upgraders with strong exit equity.

For investors, the rental market data warrants careful attention. A 1.2% QoQ decline in private rental coupled with rising vacancy rates suggests that the yield compression of 2024–2025 is continuing into 2026. Gross yields in the CCR have compressed to approximately 2.6% — below the prevailing bank fixed deposit rate — prompting a reassessment of the investment case for prime rental properties. OCR yields remain more attractive at approximately 4.0% to 4.5%, supported by domestic upgrader demand for rentals.