Singapore HDB BTO Guide 2026: Eligibility, Grants, Step-by-Step Process and Prices Explained

- HDB Build-To-Order (BTO) is Singapore’s primary scheme for first-time buyers to purchase a new public flat directly from HDB at a subsidised price, with a 3–5 year construction wait.

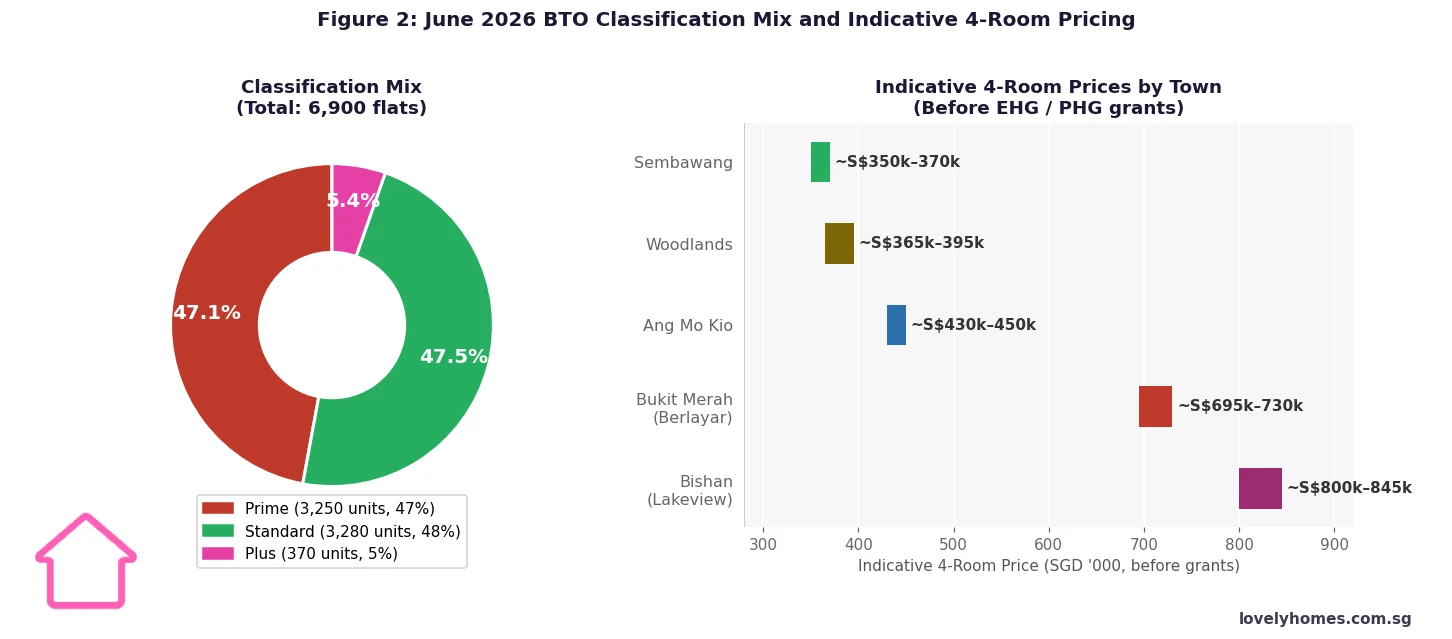

- Since October 2024, all BTO flats fall into one of three tiers — Standard, Plus, or Prime — with progressively tighter resale restrictions as location value increases.

- The Minimum Occupation Period (MOP) is 5 years for Standard and 10 years for Plus and Prime flats before you can sell or rent out the whole flat.

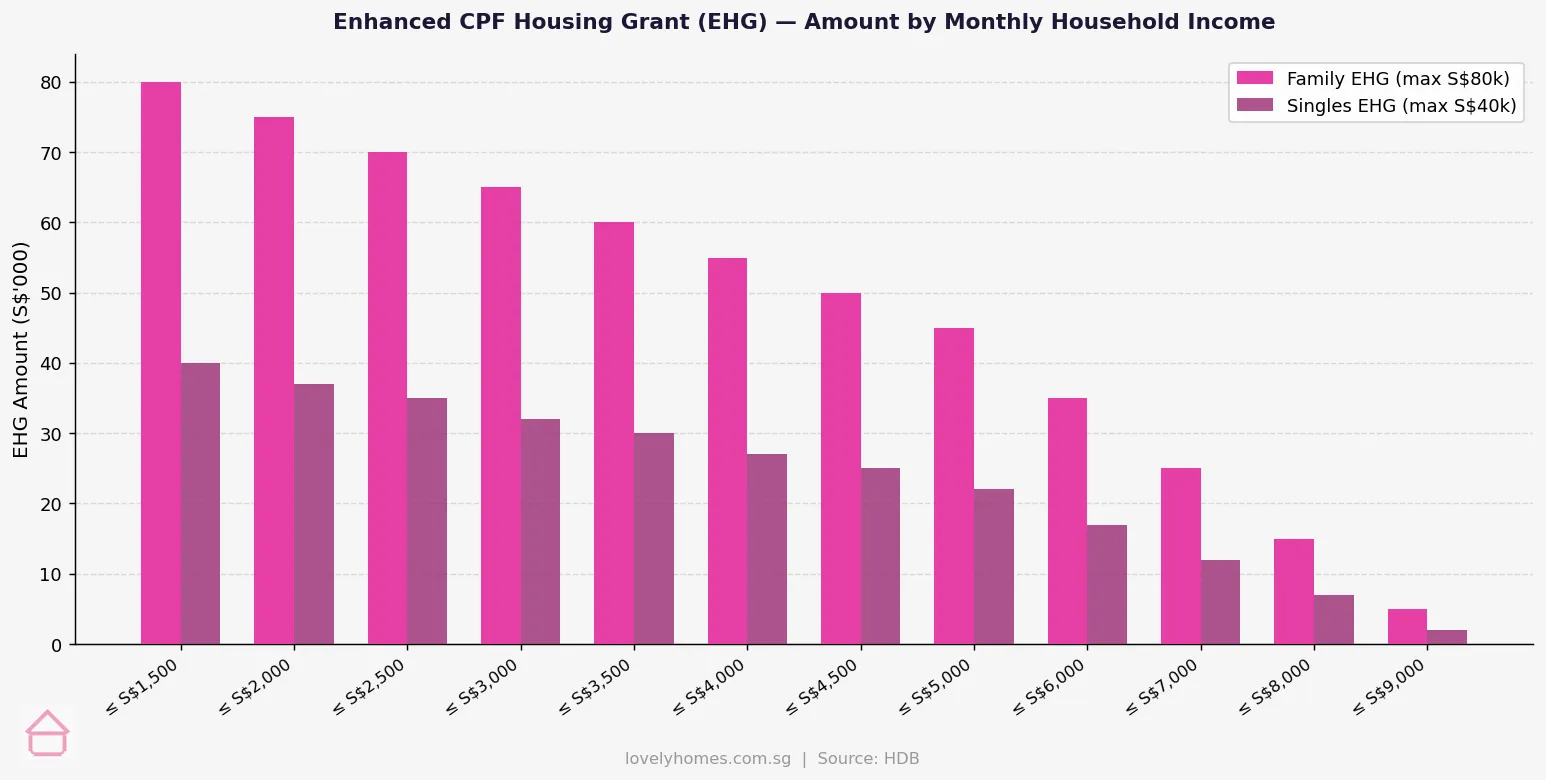

- Eligible first-timer families can receive the Enhanced CPF Housing Grant (EHG) of up to S$80,000; singles can receive up to S$40,000.

- The Proximity Housing Grant (PHG) adds up to S$30,000 for resale buyers living near parents; the Step-Up CPF Housing Grant adds S$15,000 for 2-room Flexi to 3-room upgraders.

- A valid HDB Flat Eligibility (HFE) letter is mandatory before applying for any BTO or Sale of Balance Flats exercise (introduced May 2023).

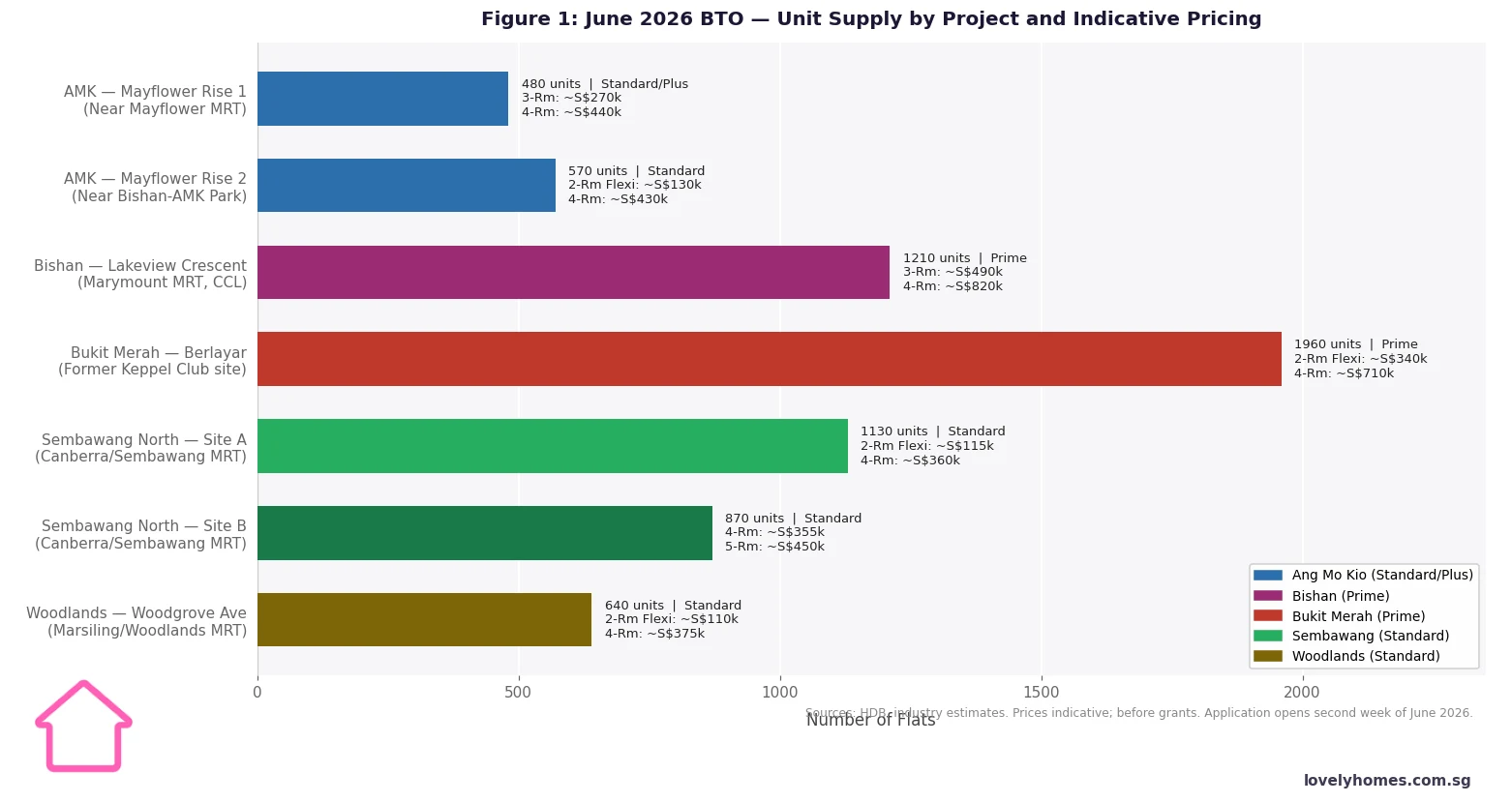

- HDB will launch approximately 19,600 BTO flats in 2026 across four exercises (February, June, October; the fourth in Q4 2026).

- First-timer applicants who do not book a flat in their first or second ballot receive additional chances through the First-Timer Priority scheme.

- The Tenants’ Priority Scheme (TCPS) was raised to 10% from the June 2026 BTO exercise, giving current HDB rental tenants a better chance of balloting a flat.

- BSD applies on all property purchases including BTO; ABSD is nil for Singapore Citizens buying their first residential property.

What Is HDB Build-To-Order (BTO)?

The Build-To-Order scheme is the Housing & Development Board’s main mechanism for selling new public flats to Singaporeans. Unlike the earlier system where HDB built flats speculatively before putting them on the market, BTO works in reverse: HDB announces a project, collects applications for approximately one month, then — only if take-up is sufficient — awards a construction contract and begins building. This demand-driven model, introduced progressively in the early 2000s, reduces the risk of unsold inventory and allows HDB to calibrate supply to genuine demand across Singapore’s towns.

The practical consequence for buyers is a waiting time of three to five years between balloting and key collection, though HDB has been actively piloting shorter-wait BTO projects with waiting times of under three years. As of 2026, projects like Tampines Nova and selected Woodlands projects have offered sub-three-year waiting times under the Short Waiting Time (SWT) initiative.

BTO flats are priced at a discount to the open market to ensure affordability. The subsidy is built into the purchase price — not paid as a separate cheque — and is “clawed back” when you sell the flat by requiring CPF refunds and, in the case of Plus and Prime flats, a percentage of the resale price to be returned to HDB.

Standard, Plus and Prime — The October 2024 Framework

The biggest structural change to the BTO system since the scheme’s launch was the introduction of the Standard, Plus and Prime classification framework in October 2024. The framework replaced the older Build-To-Order and Prime Location Public Housing (PLH) Model and applies to all BTO projects from the October 2024 exercise onwards.

Standard flats are in suburban locations with no exceptional accessibility advantage. They carry the existing 5-year MOP, can be rented out in whole after MOP, and carry no clawback on the resale price. Most estates — Woodlands, Choa Chu Kang, Sembawang, Sengkang — will be Standard designation.

Plus flats are in locations with better-than-average accessibility and amenities — typically mature towns or well-served suburban sites. They carry a 10-year MOP, may not be rented out in whole before the end of MOP, carry a clawback of a percentage of the resale price returned to HDB, and have an income ceiling of S$14,000 per month (identical to Standard in 2026). Bishan, Ang Mo Kio, and many Bukit Merah BTO sites now fall under Plus.

Prime flats are in the most central and accessible locations, including city-fringe and central-area sites such as Queenstown, Kallang/Whampoa, and Henderson. They carry the same 10-year MOP and clawback as Plus, have stricter subletting restrictions, and apply a higher clawback rate. The June 2026 BTO exercise includes Bukit Merah Berlayar, widely expected to be classified as Prime.

The rationale is that public housing subsidies should be appropriately scaled to how choice a location is. A flat at Queenstown — where resale prices touch S$1,000 per square foot — receives a larger implicit subsidy than a flat in Woodlands. The clawback is the mechanism for recapturing some of that subsidy when owners eventually sell at market prices.

Grants: EHG, PHG, Step-Up CPF and More

Singapore’s housing grants form a multi-layered system designed to ensure that the effective cost of a first BTO flat is within reach of lower- and middle-income families. The key grants available in 2026 are:

Enhanced CPF Housing Grant (EHG). Administered by CPF Board and HDB jointly, the EHG replaced the Additional CPF Housing Grant and Special CPF Housing Grant in September 2019. It is means-tested against average gross monthly household income over the preceding 12 months. For families, EHG ranges from S$5,000 at an income of S$9,000/month to S$80,000 at an income of S$1,500/month or below. Singles buying a 2-room Flexi flat receive half the family rate. EHG is paid into your CPF Ordinary Account (OA) and can be used for the flat’s purchase price and mortgage payments; it is not a cash grant.

Proximity Housing Grant (PHG). The PHG is available for resale flat purchases (not BTO directly, but relevant to those who buy resale instead of BTO). It pays S$30,000 if you live with parents/children or within 4 km of them, and S$20,000 if you live with or near a sibling. Singles receive half the family rate.

Step-Up CPF Housing Grant. For second-timer applicants who currently live in a 2-room HDB flat (rental or owned) and wish to buy a 2-room Flexi or 3-room BTO flat, the Step-Up Grant provides S$15,000. It recognises that some residents need a nudge rather than a full subsidy to upgrade from the smallest flat types.

Eligibility: Who Can Apply for a BTO Flat?

BTO eligibility is governed by several overlapping criteria under the Housing and Development Act (Cap. 129). The main conditions in 2026 are:

Citizenship. At least one applicant must be a Singapore Citizen. Singapore Permanent Residents may only apply under the Public Scheme together with a Citizen family member. Foreigners are not eligible to buy new HDB flats.

Age. Applicants must be at least 21 years old for family schemes. Singles may apply from age 35 under the Single Singapore Citizen (SSC) Scheme, but only for 2-room Flexi flats in non-mature estates.

Family nucleus. Eligible family units include married couples, fiancé/fiancée (Option to Purchase granted on condition of marriage within 3 months), parents with children, and orphaned siblings. Singles must buy alone (no co-applicant outside of parents or siblings if orphaned).

Income ceiling. For Standard and Plus flats, the gross monthly household income ceiling is S$14,000 (S$7,000 for singles). For 2-room Flexi flats in non-mature estates, there is no income ceiling for some schemes.

Ownership restrictions. Applicants must not own or have recently sold private residential property in Singapore or overseas, and must not have enjoyed a previous housing subsidy (e.g., a previous BTO purchase) within the applicable waiting period.

HFE letter. Since May 2023, all applicants must obtain a valid HDB Flat Eligibility (HFE) letter before applying for any BTO or Sale of Balance Flats (SBF) exercise. The HFE letter confirms your eligibility, loan eligibility, and grant amounts in a single integrated assessment. It is valid for 9 months and should be obtained well before any exercise opens.

The Application and Balloting Process

HDB opens BTO application windows for approximately one month, typically twice a year (February and June/July, with an October exercise since 2022). During the window, eligible buyers submit a single application for one project of their choice, along with their preferred flat type. There is no fee to apply.

After the application window closes, HDB runs a computerised ballot to determine the order in which applicants may choose their units. Priority queues exist within the ballot: Married Child Priority Scheme (MCPS) for applicants buying near parents, Multi-Generation Priority Scheme (MGPS) for two households applying together, Tenants’ Priority Scheme (TCPS) for existing HDB rental tenants (raised to 10% from June 2026), and First-Timer Families Priority ensuring first-timers get precedence.

Applicants who are balloted but do not find a flat they want, or who miss their booking appointment, are deemed “unsuccessful” and may re-apply in future exercises. After a first unsuccessful ballot, first-timers receive one additional ballot chance in subsequent applications. After two unsuccessful ballots, they receive priority queue status, significantly improving their odds. HDB has indicated that the median waiting time for a first-timer to successfully book a BTO flat is approximately two application exercises.

Upon selection, applicants pay a booking fee of S$500 to S$2,000 (depending on flat type) and sign the Agreement for Lease, committing to buy the flat. The balance of the purchase price, plus BSD, is paid in tranches as construction milestones are met.

What Does a BTO Flat Actually Cost?

The out-of-pocket cost of a BTO flat depends on flat type, location (Standard vs Plus vs Prime), income-linked grants, whether you use a HDB concessionary loan or a bank loan, and CPF OA balances. The figures below represent the after-grant purchase prices for a typical Singapore Citizen first-timer family with a joint monthly income around S$6,000–8,000.

Summary Comparison Table

| Parameter | Standard BTO | Plus BTO | Prime BTO | HDB Resale |

|---|---|---|---|---|

| Location | Non-mature estates | Mature / well-served towns | Central / city-fringe | Any estate |

| MOP | 5 years | 10 years | 10 years | 5 years (existing MOP) |

| Whole-unit rental after MOP | Yes | Yes (after 10yr MOP) | Restricted | Yes |

| Resale clawback | No | Yes (% of resale price) | Yes (higher %) | No |

| EHG applicable? | Yes | Yes | Yes | Yes |

| PHG applicable? | No | No | No | Yes (up to S$30k) |

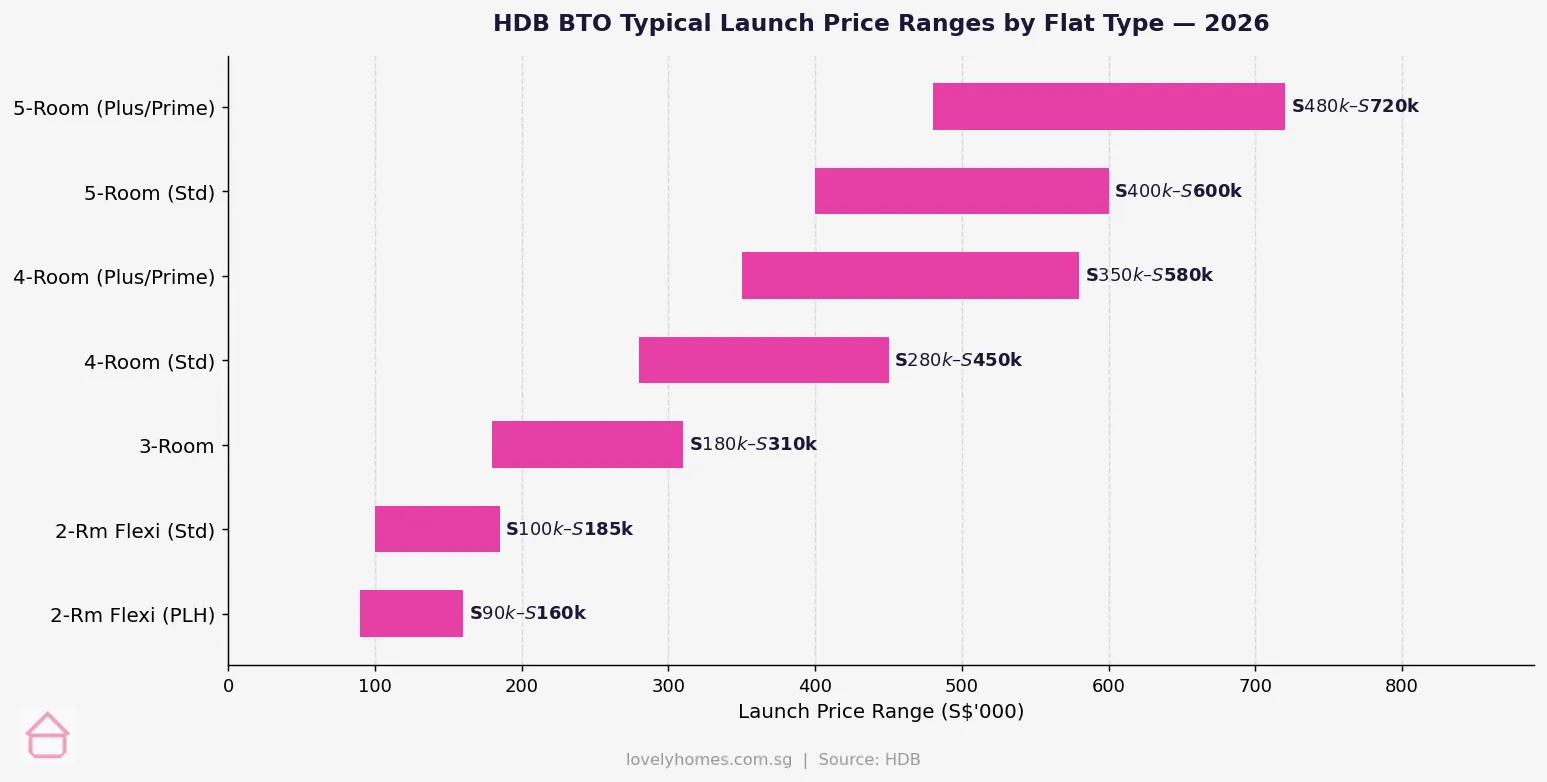

| Typical 4-Room price (2026) | S$280k – S$450k | S$350k – S$580k | S$400k – S$700k | S$500k – S$900k |

| Waiting time | 3–5 years | 3–5 years | 3–5 years | Immediate |

Worked Example — Mr & Mrs Lim, Bishan Standard 4-Room BTO

Mr and Mrs Lim are a Singapore Citizen married couple in their late 20s. Their combined gross monthly income is S$7,200. They apply for a 4-Room Standard BTO flat in a Bishan project priced at S$395,000 (hypothetical launch price).

Grant calculation: At a household income of S$7,200, EHG for families is S$25,000. The flat is a BTO (not resale), so PHG does not apply. Net purchase price: S$395,000 − S$25,000 = S$370,000.

BSD: On S$370,000 — first S$180,000 at 1% = S$1,800; next S$180,000 at 2% = S$3,600; balance S$10,000 at 3% = S$300. BSD = S$5,700. ABSD: nil (SC first property).

Financing: HDB concessionary loan LTV 80% → loan = S$370,000 × 80% = S$296,000 (subject to HFE eligibility and credit assessment). The couple must fund at least 20% (S$74,000) from CPF OA and/or cash. Monthly instalment on a S$296,000 HDB loan at 2.6% over 25 years: approximately S$1,345 per month. MSR check: S$1,345 / S$7,200 = 18.7% — within the 30% MSR limit. TDSR: 18.7% — well within 55%.

Upfront cash: Booking fee (4-room) S$2,000 + BSD S$5,700 + balance of 20% downpayment via CPF OA S$72,000. If CPF OA balance is below S$72,000, the shortfall must be paid in cash.

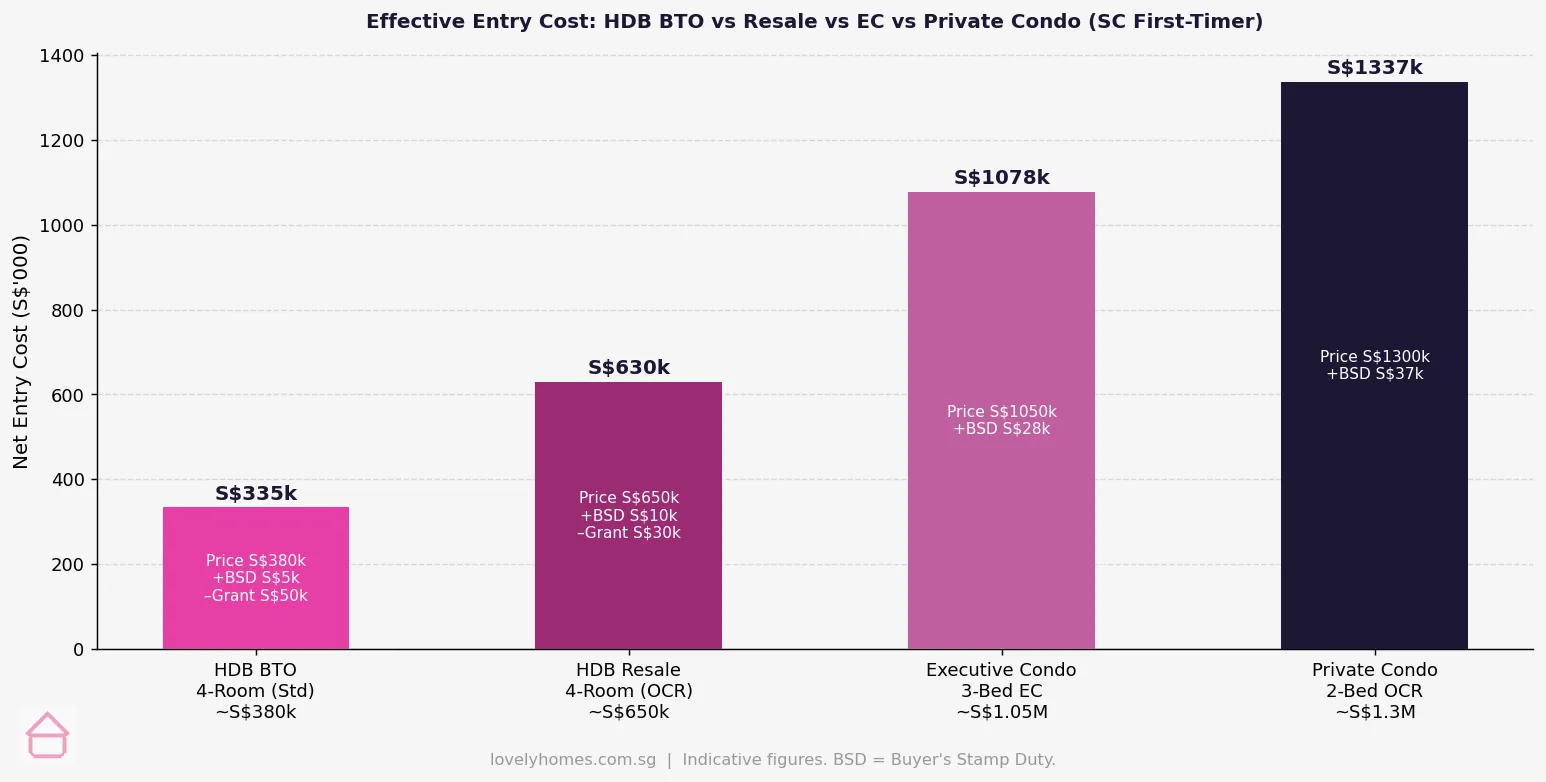

Outcome: The Lims can feasibly service the flat on their combined income. The total effective entry cost of S$335,700 (after grants) is S$364,300 less than the equivalent OCR private condo — illustrating the ongoing role of BTO as Singapore’s primary affordability tool.

What Might Come Next — BTO Pipeline for 2026–2028

HDB has confirmed approximately 19,600 BTO flats for 2026 across the four exercises. Noteworthy launches expected in the second half of 2026 and beyond include the Toa Payoh West BTO project slated for the October 2026 exercise — the first significant public housing release in central Toa Payoh in over a decade and almost certain to attract oversubscription as a Standard or Plus project. Pearl’s Hill — a large site in the Chinatown/Outram Park corridor — is expected to yield approximately 1,700 new homes in a future exercise, potentially as a Prime project given its proximity to the CBD.

HDB is also studying the gradual release of land in the Greater Southern Waterfront (GSW) area for public housing over the longer term, and the Tengah “forest town” BTO pipeline will continue with further phases through 2027–2028. Buyers who miss the current exercises should monitor the HDB website for upcoming announcements and apply for an HFE letter in advance.

Frequently Asked Questions

Can I rent out my BTO flat before MOP?

No. You are not permitted to rent out the entire flat before the end of your MOP (5 years for Standard, 10 years for Plus/Prime). You may, however, rent out individual rooms within your flat at any time, subject to HDB’s approval and occupancy limits. Renting out the whole flat before MOP is a breach of the Housing & Development Act and can result in HDB compulsorily acquiring the flat at below-market value.

What happens if I miss my BTO booking appointment?

If you do not attend your booking appointment or decline to select a flat during your appointed slot, your application is cancelled. You forfeit your booking priority for that exercise. You may re-apply in future exercises, but your first-timer queue advantage resets. HDB does not guarantee a rescheduled appointment.

Is a HDB loan or a bank loan better for a BTO flat?

The HDB concessionary loan offers a rate of 0.1 percentage points above the CPF OA rate — currently 2.6% per annum — and is generally lower than bank rates, which were around 3.0–3.5% per annum in 2026. The HDB loan allows an LTV of 80% and does not require a cash downpayment; the full 20% downpayment can come from CPF OA. However, if you take a bank loan, you must pay at least 5% of the purchase price in cash (with the remaining 20% from CPF or cash), and LTV is capped at 75%. For most first-time buyers with limited cash savings, the HDB loan is generally more accessible.

What is the Minimum Occupation Period and does it restart if I sell?

The MOP begins from the date you receive your keys. For Standard BTO flats, MOP is 5 years; for Plus and Prime BTO flats launched from October 2024 onwards, it is 10 years. When you sell and buy a second HDB flat, the MOP for the second flat runs from the date of that flat’s key collection — it does not inherit or carry over from the first flat. Crucially, you must have satisfied the MOP before you are eligible to sell on the open market or purchase a private residential property concurrently with HDB flat ownership.

Can PRs buy a BTO flat?

Singapore Permanent Residents (PRs) cannot buy new BTO flats on their own. A PR can only buy a BTO flat if they are applying together with a Singapore Citizen spouse or family member under an eligible scheme (e.g., Public Scheme). The Citizen must be a co-applicant, not just a supporting document. PRs buying alone may purchase HDB resale flats (but not new BTO units), subject to their own eligibility conditions and a minimum 3-year PR residency requirement.

What is the TCPS and how does it help current HDB tenants?

The Tenants’ Priority Scheme (TCPS) allocates up to 10% of BTO flat supply across all exercises — raised from 5% in the June 2026 BTO exercise — to eligible existing HDB rental flat tenants. To qualify, the applicant must have been living in an HDB rental flat for a minimum period and meet all standard BTO eligibility criteria. The scheme is designed to give long-term rental tenants a pathway to home ownership with a statistical advantage in the ballot. Applications under TCPS count alongside other priority schemes (MCPS, MGPS, First-Timer Priority) where multiple schemes apply.

Related Articles

- First-Time Property Buyer Guide Singapore 2026

- CPF Property Withdrawal Limits Singapore 2026

- Singapore Stamp Duty Complete Guide 2026

- ABSD Singapore 2026 — Complete Guide

- Singapore Property Selling Guide 2026

- Singapore Bridging Loan Guide 2026

Disclaimer: This article provides general information about the HDB Build-To-Order scheme and housing grants as at 3 June 2026. It is not financial, legal, or housing advice. Eligibility criteria, grant amounts, income ceilings, and BTO project details are subject to change by HDB and CPF Board. Always verify your eligibility and loan limits with the official HDB website, the CPF Board, and your preferred financial institution before making any property purchase decision.