Quick Answer — property conveyancing in Singapore at a glance

Conveyancing is the legal transfer of property ownership from seller to buyer, handled by a Singapore-licensed lawyer on each side.

For resale private property: the Option to Purchase (OTP) gives the buyer 14 calendar days to exercise, paying 1% + 4% option fee and BSD/ABSD.

BSD and ABSD are due within 14 days of signing the OTP or Sale and Purchase Agreement — whichever is earlier.

Completion (keys and balance payment) typically occurs 8–12 weeks after exercising the OTP for resale condo; 6–8 weeks for HDB resale.

Buyer’s conveyancing legal fees for a S$1 million resale condo are approximately S$2,700–S$3,500 (including GST).

For new launches, the developer’s lawyers handle the Sale and Purchase Agreement; you still need your own lawyer to review and for the mortgage.

CPF OA funds can be used to pay BSD, legal fees, and the balance of the purchase price — but not the 5% mandatory cash downpayment for bank loans.

What Is Conveyancing and Why Do You Need a Lawyer?

Conveyancing is the legal process by which the title (ownership rights) of a property is formally transferred from one party to another. In Singapore, all conveyancing for residential property must be handled by a qualified Singapore-licensed lawyer (advocate and solicitor). You cannot self-convey a property transaction — the Law Society of Singapore and the Land Titles Act require a qualified professional to prepare the instruments of transfer, conduct the requisitions, and handle the lodgement with the Singapore Land Authority (SLA).

The conveyancing lawyer acts as far more than a document drafter. They carry out title searches, verify that the property is free of encumbrances, co-ordinate with CPF Board to release CPF funds, liaise with the mortgagee bank, and ensure that all stamp duties are correctly assessed and paid on time. For buyers in particular, appointing a good conveyancing lawyer early — ideally before exercising the Option to Purchase — can prevent costly mistakes around timing and documentation.

Both buyer and seller must appoint their own separate lawyers. The same law firm cannot act for both parties in the same transaction (conflict of interest rules under the Legal Profession (Professional Conduct) Rules). In HDB transactions, HDB’s legal arm processes the resale procedures and buyers/sellers interact via the HDB Flat Portal, but a buyer may still choose to appoint a private lawyer to advise.

The Option to Purchase (OTP) — Singapore’s Property Buying Trigger

For private residential property, the conveyancing process formally begins with the Option to Purchase (OTP). The OTP is a legal document granted by the seller to the buyer, giving the buyer an exclusive right to purchase the property at the agreed price within a specified period — in Singapore, typically 14 calendar days from the date the option is granted.

The OTP process works as follows. First, the seller grants the OTP upon receipt of the option fee — conventionally 1% of the agreed purchase price, paid in cash. This amount is non-refundable if the buyer chooses not to exercise. The buyer then has 14 days to decide whether to proceed. If proceeding, the buyer exercises the OTP by signing the acceptance copy and returning it to the seller’s lawyer together with:

An additional exercise fee of 4% of the purchase price (also cash); and

Payment of the Buyer’s Stamp Duty (BSD) and, where applicable, Additional Buyer’s Stamp Duty (ABSD) — both are due within 14 days of the OTP being granted, not 14 days from exercise.

The total 5% (1% option + 4% exercise fee) forms the initial deposit, which is typically held by the seller’s solicitors in their client account and released to the seller upon completion. The balance of the purchase price — typically 95% — is paid on the completion date.

Step

Amount

Timing

Payment Mode

Option fee (grant OTP)

1% of price

Day 0

Cash/cashier’s order

Exercise fee (exercise OTP)

4% of price

Within 14 calendar days

Cash/cashier’s order

BSD (all buyers)

Progressive, ~0.6–3%+

Within 14 days of OTP date

Cash or CPF OA

ABSD (where applicable)

5–60% flat rate

Within 14 days of OTP date

Cash only (CPF for reimbursement later)

Balance purchase price

~95% of price

Completion date (8–12 weeks)

CPF OA + bank loan + cash top-up

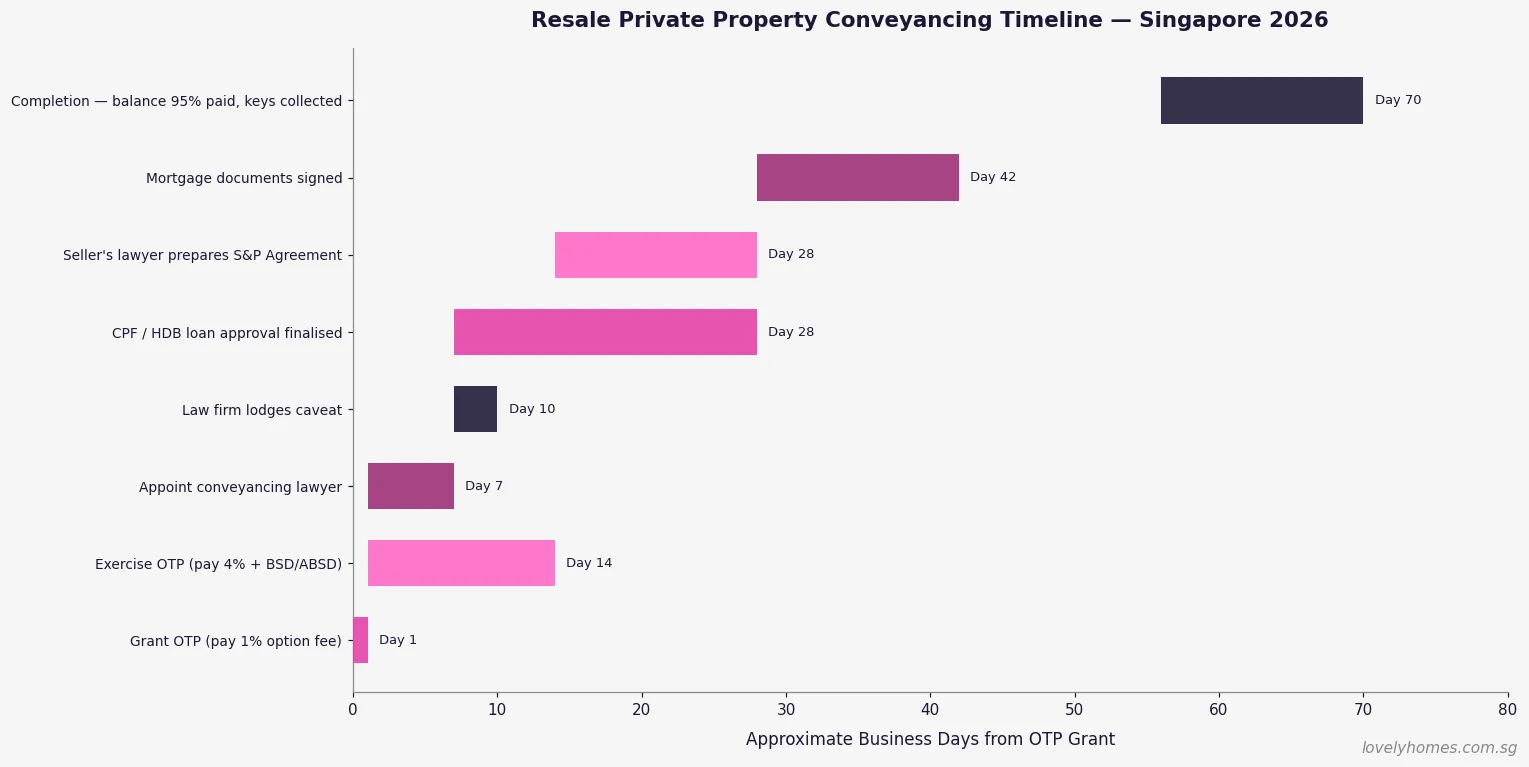

The Conveyancing Timeline — From OTP to Keys

Figure 1: Approximate conveyancing timeline for a resale private residential property, Singapore 2026. Timings are indicative and may vary depending on parties and conditions. Source: Singapore Law Society / LovelyHomes analysis.

After the OTP is exercised, your conveyancing lawyer moves through a series of standard steps. The requisition phase involves sending formal enquiries to government bodies — the Land Titles Registry (SLA), URA (planning queries), HDB (where applicable), PUB, SP Group, and others — to confirm there are no adverse encumbrances, outstanding charges, or regulatory issues on the title. This typically takes two to three weeks.

Simultaneously, if you are taking a bank loan, the mortgage documentation is being prepared: the bank’s solicitors (often the same firm acting for you) will prepare the mortgage instrument, and CPF Board will be notified to set aside or release your CPF OA funds for the purchase. For new citizens or PRs using CPF for the first time for property, additional verification steps apply.

The completion appointment brings all parties together (or their lawyers in escrow). The buyer’s lawyers hand over the balance payment; the seller’s lawyers hand over the title documents and release the keys. In Singapore, completion is a smooth, paperwork-driven process — you do not physically attend a courtroom or signing ceremony (unlike some other jurisdictions). The average buyer simply receives a call from their lawyer confirming completion, and then collects the keys.

New Launch Private Property — Different Process, Same Stamp Duties

When buying a new launch directly from a developer (whether a condo or an executive condominium), the conveyancing process differs in several important respects:

The developer uses its own solicitors to prepare the Sale and Purchase Agreement (S&P Agreement) — a standardised statutory form prescribed by the Controller of Housing under the Housing Developers (Control and Licensing) Act.

There is no OTP for new launches; instead, you first sign an Option to Purchase issued by the developer (usually after booking a unit and paying a booking fee of typically 5%), followed by the S&P Agreement within 3 weeks.

BSD and ABSD remain payable within 14 days of the S&P Agreement date.

Payment follows the Progressive Payment Scheme (PPS) — instalments tied to construction milestones over the build period (typically 3–5 years to TOP).

You should still appoint your own independent conveyancing lawyer to review the S&P Agreement and handle your CPF and mortgage documentation, even though the developer’s lawyers lead the transaction.

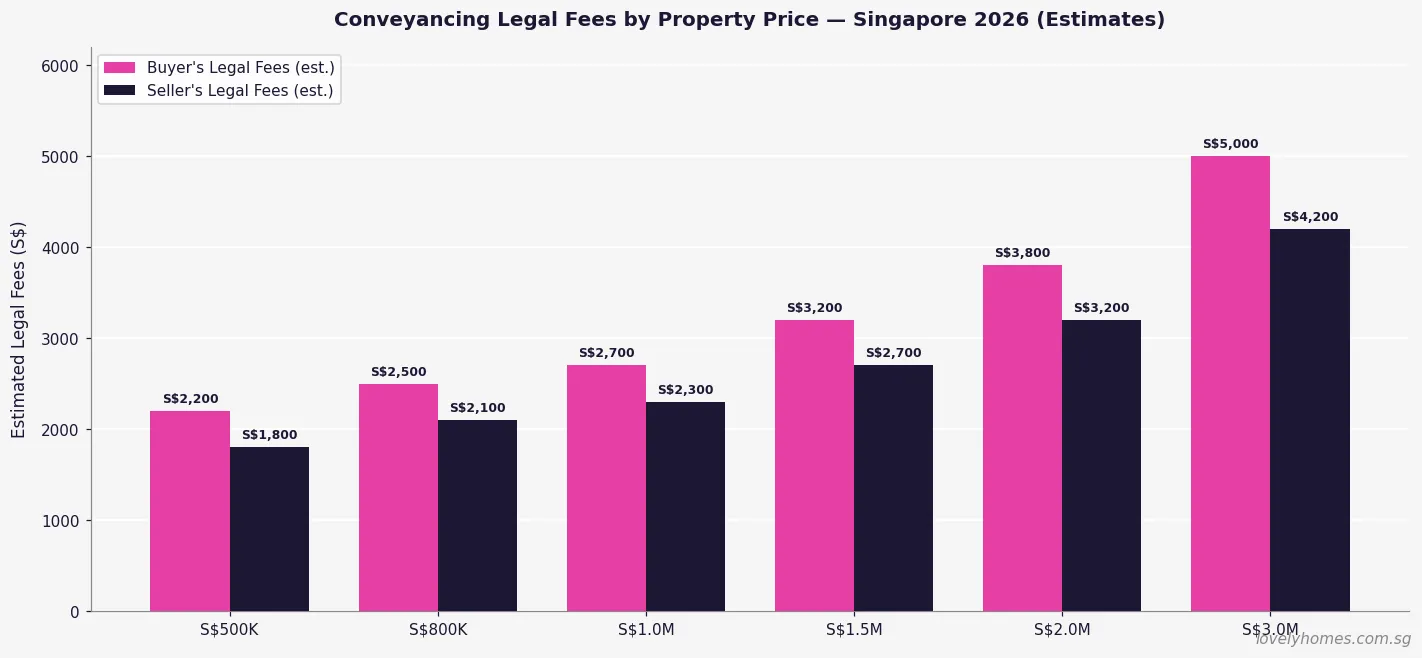

Conveyancing Legal Fees — What to Expect in 2026

Figure 2: Estimated conveyancing legal fees for buyer and seller by property price band, Singapore 2026. All figures are indicative estimates including GST; actual fees vary by law firm and complexity.

Conveyancing legal fees in Singapore are not regulated by a fixed scale for private property transactions (unlike some Commonwealth jurisdictions). Law firms set their own fees, though market rates are broadly competitive. As a rough guide for 2026:

Purchase Price

Buyer’s Legal Fees (est.)

Seller’s Legal Fees (est.)

Up to S$500,000

S$1,800–S$2,500

S$1,500–S$2,000

S$500,001–S$1,000,000

S$2,500–S$3,200

S$2,000–S$2,700

S$1,000,001–S$2,000,000

S$3,000–S$4,200

S$2,500–S$3,500

S$2,000,001–S$3,000,000

S$4,000–S$5,500

S$3,300–S$4,500

Above S$3,000,000

S$5,000+

S$4,000+

These figures include disbursements (SLA lodgement fees, title search fees, stamp certificate) but exclude the mortgage-related legal work, which is typically billed separately by the bank’s panel solicitors. Many buyers find that choosing a law firm on the bank’s mortgage panel saves money — you may qualify for a “combined” rate covering both the purchase and the mortgage documents.

For HDB resale transactions, the HDB Resale Flat Portal provides a standardised suite of forms and handles the administrative process centrally. A buyer may engage a private lawyer for S$1,000–S$2,000 for advice, but the HDB legal process itself is not separately billed to the buyer.

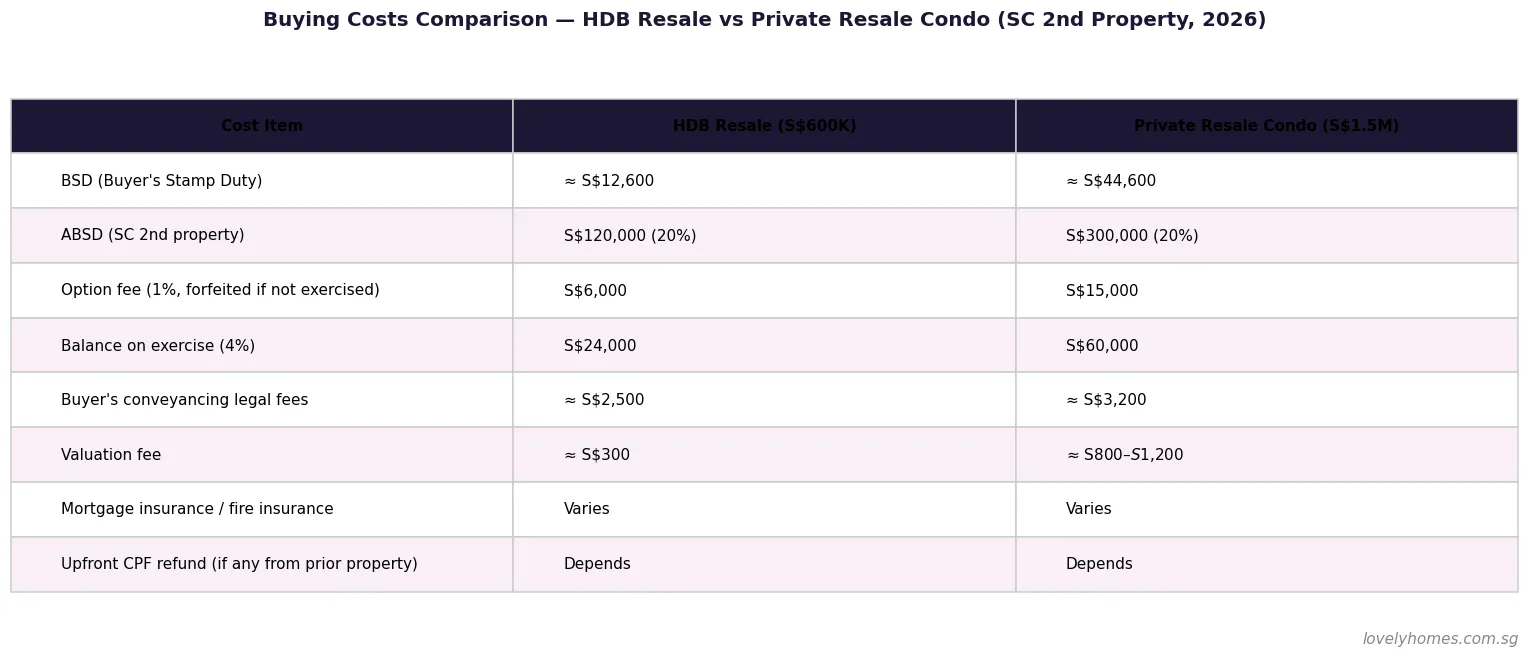

Worked Example — Full Buying Cost Breakdown, Resale Condo S$1.5 Million

Scenario: Singapore Citizen couple buying their second property — Resale Condo, S$1,500,000, District 15

Both buyers are Singapore Citizens. They already own their HDB flat (first property). They are purchasing the condo jointly as their second property.

Option fee (1%, cash): S$15,000 — paid when OTP granted. Non-refundable if not exercised.

Exercise fee (4%, cash): S$60,000 — paid within 14 days of OTP date.

BSD (progressive): S$44,600 — due within 14 days of OTP. Can be paid via CPF OA.

ABSD (20% for SC 2nd property): S$300,000 — due within 14 days of OTP. Must be paid in cash initially; CPF may be used for reimbursement after stamping.

Buyer’s legal fees: approximately S$3,200–S$4,200 (including GST and disbursements).

Valuation fee: approximately S$800–S$1,200 (required by the bank for mortgage drawdown).

Balance 95% at completion: S$1,425,000 — funded via CPF OA balance + bank mortgage.

Total upfront cash required before completion: S$15,000 + S$60,000 + S$300,000 (ABSD) + BSD disbursement + legal fees ≈ S$382,000–S$385,000 in cash before leveraging CPF. This illustrates why ABSD planning is critical for second-property buyers — the S$300,000 ABSD alone is a major cash drain.

Figure 3: Full cost comparison — HDB resale (S$600K) vs private resale condo (S$1.5M) for a SC buying a second property. Source: IRAS / HDB / LovelyHomes analysis (2026).

CPF and Conveyancing — What Can and Cannot Be Paid with CPF

Understanding which costs can be funded from your CPF OA and which must be cash is essential to avoid a last-minute shortfall. As a general rule:

Cost Item

CPF OA Usable?

Notes

Buyer’s Stamp Duty (BSD)

Yes

Deducted from CPF at the time of payment

ABSD

No (initially)

Must be paid in cash first; CPF reimbursement applies after stamping

5% downpayment (bank loan)

No

Mandatory cash requirement; cannot use CPF

Balance above 5% (bank loan LTV)

Yes

CPF OA used for the remainder of the 25% equity requirement

Legal / conveyancing fees

Yes

Up to a cap set by CPF Board based on purchase price

Valuation fee

Generally No

Usually paid directly to the valuer in cash

Monthly mortgage instalments

Yes

Subject to CPF Withdrawal Limit and Valuation Limit

Why Conveyancing Matters — Common Mistakes to Avoid

Many first-time buyers in Singapore underestimate the legal and procedural complexity of a property transaction. The most frequent pitfalls encountered in conveyancing are:

Exercising the OTP without sufficient cash for ABSD: Buyers sometimes discover — after paying the 1% option fee — that they do not have the cash to cover ABSD on exercise. This is a costly error: forfeiting the 1% option fee and walking away. Pre-compute your full buying cost (including ABSD) before paying the option fee.

Delaying the BSD/ABSD payment: Both duties are due within 14 days of the OTP date — not 14 days from exercise. A buyer who exercises on day 13 still has only one day to pay stamp duty. Failure to stamp on time attracts penalties of 2–4× the duty payable.

Not checking encumbrances before exercising: A competent conveyancing lawyer will run a title search and caveat check before the exercise deadline. Buyers who rush this step can find themselves bound to a property with an undisclosed mortgage or legal charge.

Assuming the developer’s lawyer acts for you: For new launches, the developer’s solicitors act exclusively for the developer. Your interests are protected only by your own appointed lawyer.

Forgetting to budget for legal fees in the completion funds: On completion day, your lawyer will draw up a “completion account” showing exactly how the balance is funded (CPF, loan drawdown, cash). Buyers who have not kept the legal fees in their CPF or cash buffer occasionally face a shortfall at the last moment.

What Might Come Next — Conveyancing Reform Outlook 2026–2028

Singapore’s conveyancing framework is relatively mature and stable, but two developments bear watching. First, the Ministry of Law has been progressively digitising the conveyancing process — the Integrated Land Information Service (INLIS) already allows electronic title searches, and there are ongoing discussions around greater use of digital instruments of transfer. Second, the Law Society’s standardisation of HDB resale procedures has reduced friction significantly, and a similar standardisation framework for private property may be on the horizon. Buyers and sellers should expect a leaner, more fully digital process by the late 2020s, but the fundamental legal requirement for a qualified solicitor to handle the transfer is not expected to change.

Frequently Asked Questions

Do I need a lawyer to buy an HDB resale flat, or can HDB handle everything?

For most straightforward HDB resale transactions, the HDB Resale Flat Portal handles the administrative and procedural steps centrally — buyers and sellers submit resale applications online, and HDB’s in-house legal process manages the transfer instruments. You are not strictly required to appoint a private conveyancing lawyer. However, if your situation involves CPF complications, outstanding mortgages, an estate sale, unusual co-ownership structures, or a divorce settlement, engaging a private lawyer (typically S$1,000–S$2,000) for independent advice is well worthwhile. For private property transactions, a private lawyer is mandatory.

Can I use the same lawyer as the seller?

No. A Singapore law firm cannot act for both buyer and seller in the same property transaction. This rule exists to prevent conflicts of interest — your lawyer’s duty is to protect your interests alone, and the seller’s lawyer’s duty is the opposite. If a seller’s law firm approaches you offering to “save costs” by acting for both sides, this is in breach of the Legal Profession (Professional Conduct) Rules and should be declined.

What happens if the seller pulls out after granting the OTP?

The OTP is a binding contractual document. If the seller withdraws after granting the option and you have already exercised it, the seller is in breach of contract. You can seek specific performance (a court order requiring the seller to complete the sale) or claim damages including your costs of conveyancing, financing, and any foreseeable losses. Your conveyancing lawyer should advise you promptly if a seller attempts to back out post-exercise. The 1% option fee paid to obtain the OTP is generally retained by the buyer in such cases, but recovery of the full loss typically requires legal proceedings.

How long does conveyancing take for a new launch (BTO or developer)?

For new BTO flats, the HDB handles the conveyancing entirely in-house upon completion of the flat. The process typically takes 4–8 weeks after HDB notifies you that your flat is ready for collection (after Temporary Occupation Permit is granted and your unit passes inspection). For private new launches, the formal transfer of title occurs upon completion of the building project — conveyancing is triggered at that point, typically 3–5 years after the booking date. During the construction period, you are making progressive payments but do not yet hold the legal title to the unit.

Is there stamp duty on a rental tenancy agreement in Singapore?

Yes, but it is much smaller than BSD or ABSD. Tenancy agreements in Singapore attract stamp duty under the Stamp Duties Act. The rate is S$1 per S$250 of annual rent for leases of 4 years or less, and a higher rate applies for longer tenancies. For a 2-year tenancy at S$4,000/month (S$48,000 annual rent), the stamp duty would be approximately S$192. Stamp duty on tenancy agreements is normally split between landlord and tenant by convention, unless the tenancy agreement specifies otherwise. Payment is via IRAS e-Stamping portal and must be completed within 14 days of execution.

Can foreigners engage a Singapore conveyancing lawyer and buy private property?

Yes. Foreigners may engage any Singapore-licensed advocate and solicitor to handle a private residential property conveyancing. Under the Residential Property Act, foreigners may purchase non-landed private residential properties (condos and apartments) without restriction. Landed property, including terrace houses, semi-detached, and detached houses, generally requires SLA approval for foreign buyers, with limited exceptions (e.g., Sentosa Cove). ABSD at 60% applies on any residential property purchase by a foreigner. Your conveyancing lawyer will advise on eligibility and the ABSD position at the outset of the transaction.

Disclaimer: This article is intended for general information only and does not constitute legal or financial advice. Conveyancing procedures, stamp duty rates, and CPF rules are subject to change. Always consult a Singapore-licensed conveyancing lawyer before entering into any property transaction. For official guidance, refer to the Ministry of Law, Law Society of Singapore, IRAS Stamp Duty, and Singapore Land Authority.

Landed property in Singapore is the apex of local real estate — a scarce, tightly regulated asset class that accounts for just 5% of residential dwellings, occupies about 80 sqkm of the island, and is almost entirely reserved for Singapore Citizens. For buyers who qualify, landed homes deliver three things that condominiums cannot: private land ownership, multi-generational living space, and freehold tenure on the overwhelming majority of stock. This 2026 guide explains the four main landed typologies (Detached, Semi-Detached, Terrace and Cluster/Strata-Landed), the Residential Property Act rules that govern foreign and PR ownership, typical pricing by district, and the structural demand drivers that have made landed property Singapore’s most consistent long-term outperformer.

Figure 1: Singapore landed property — Good Class Bungalow, Detached, Semi-Detached, Terrace and Cluster.

Quick Answer

Landed property = Detached, Semi-Detached, Terrace, and Cluster/Strata-Landed.

Good Class Bungalow (GCB): detached on ≥ 1,400 sqm in one of 39 gazetted GCB areas.

Ownership: Singapore Citizens only (landed non-Sentosa); PRs and foreigners need LDAU approval.

Tenure: majority freehold; some 99-year and 999-year stock in specific estates.

Share of housing stock: approx. 5% of Singapore’s residential dwellings.

Median price (2026): Semi-D S$5.8M–S$7.5M; Terrace S$4.2M–S$5.8M; GCB S$25M+.

Sentosa Cove: the only landed enclave open to non-resident foreigners, subject to LDAU approval.

What Counts as Landed Property in Singapore

Under the Residential Property Act (RPA), “landed residential property” comprises detached, semi-detached and terrace houses, and — for legal purposes — vacant residential land. Strata-landed (cluster) housing sits in a hybrid zone: it is physically a landed house but legally a strata lot under the Building Maintenance and Strata Management Act.

Typology

Definition

Key Characteristics

Detached / Bungalow

Standalone house on its own plot; minimum 400 sqm plot by URA.

Full privacy; highest price point. GCB sub-category at 1,400+ sqm.

Semi-Detached

Pair of houses sharing one party wall; minimum 200 sqm per plot.

Second most expensive typology; balances space and price.

Terrace

Row houses sharing two party walls; minimum 150 sqm per plot.

Most affordable landed entry; concentrated in older estates.

Cluster / Strata-Landed

Gated enclave of landed units sharing common facilities (pool, gym, guardhouse).

Body-corporate-managed; foreigners eligible without LDAU approval (as strata).

Good Class Bungalow (GCB)

Detached on ≥ 1,400 sqm in a gazetted GCB Area (39 areas).

Singapore’s most exclusive housing; SC buyers only.

Shophouse (conservation)

Historically residential/commercial; zoned on a case-by-case basis.

Commercial-dominant usage today, but some remain residential.

The 39 Good Class Bungalow Areas

Good Class Bungalows — the pinnacle of Singapore residential — are concentrated in 39 gazetted areas. Each plot must meet four criteria: (1) minimum 1,400 sqm plot size, (2) minimum 18.5m plot width, (3) no more than two storeys plus an attic, and (4) at least 3m side setback. The best-known GCB areas include Tanglin, Nassim, Queen Astrid, Bishopsgate, Chatsworth, Cluny, Cornwall, Dalvey, Gallop, White House Park and Holland Park.

Key takeaway

There are approximately 2,800 GCB plots in Singapore — a fixed, non-expandable pool. The scarcity alone has driven GCB prices to compound at 7%–9% p.a. over the last two decades, outpacing the broader residential index.

Who Can Buy Landed Property in Singapore?

Singapore Citizens

SCs have the fewest restrictions: they can purchase any landed property on the mainland, in Sentosa Cove, or in strata form, subject only to ABSD rules (0% on 1st, 20% on 2nd, 30% on 3rd+ property) and standard financing rules.

Singapore Permanent Residents (PR)

PRs cannot purchase landed property on the mainland without specific approval from the Land Dealings (Approval) Unit (LDAU) of the Singapore Land Authority. In practice, LDAU approval for PRs is rare — usually granted only for PRs of at least 5 years’ standing who demonstrate substantial economic contribution to Singapore. PRs may freely purchase strata-landed (cluster) housing and Sentosa Cove landed (subject to LDAU).

Foreigners (Non-Resident)

Non-resident foreigners may purchase Sentosa Cove landed property (subject to LDAU approval, typically granted for 1 plot with owner-occupation conditions), and may freely purchase strata-landed cluster housing. Mainland landed is effectively closed to foreign buyers.

Entities (Companies, Trusts)

Entities are generally prohibited from owning landed residential property. Certain family-office and LDAU-approved trusts have been granted exceptions, but these are the minority. Entities face a 65% ABSD rate across the board.

Buyer Type

Mainland Landed

Strata-Landed (Cluster)

Sentosa Cove

Singapore Citizen

Yes

Yes

Yes

PR (≥ 5 yrs)

LDAU approval (rare)

Yes

LDAU approval

PR (< 5 yrs)

Effectively No

Yes

Rare

Foreigner

No (mainland)

Yes

LDAU approval

Entity

No

Yes (subject to ABSD 65%)

No

Tenure: Freehold, 999-Year and 99-Year Landed

Most landed stock in Singapore is freehold, a product of colonial-era land grants. A material minority is 999-year leasehold — functionally equivalent to freehold for all planning purposes. A smaller segment is 99-year leasehold, typically in newer developments such as Sentosa Cove and specific GLS strata-landed projects.

Freehold / 999-year command a 5%–12% price premium over 99-year peers. At the 60-year leasehold mark, CPF usage begins to taper (by the 30-year remaining point, CPF is materially restricted), which structurally caps the buyer pool for older leasehold landed — and compresses prices.

Price Benchmarks by Typology and District (2026)

Typology

Representative Districts

Tenure Mix

2026 Price Band

Detached (GCB)

D10 Tanglin / D11 Nassim

Freehold

S$25M – S$80M+

Detached (non-GCB)

D10 / D11 / D15

Freehold

S$8M – S$18M

Semi-Detached

D10 Holland / D11 Novena / D15 Katong

Freehold

S$6.5M – S$9M

Semi-Detached

D13 Potong Pasir / D14 Eunos / D19 Hougang

Freehold / 999-yr

S$4.5M – S$6M

Terrace (Inter / Corner)

D10 / D11 / D15

Freehold

S$5M – S$7.5M

Terrace (Inter / Corner)

D13 / D14 / D19 / D25

Freehold / 999-yr / 99-yr

S$3M – S$5M

Cluster / Strata-Landed

D10 / D11 / D16 / D19

Freehold / 99-yr

S$3.5M – S$7M

Sentosa Cove Bungalow

D4 Sentosa

99-yr

S$15M – S$40M+

Cluster Housing: The Strata-Landed Alternative

For buyers who want a landed lifestyle without the upkeep burden — and for PRs and foreigners whose mainland landed options are effectively zero — cluster (strata-landed) housing offers a compromise. Cluster developments are gated enclaves of terraces or semi-detached units, managed under a body corporate with shared facilities (swimming pool, gym, tennis court, 24/7 security). Because the units are legally strata lots rather than landed titles, they fall outside the RPA’s landed-ownership restrictions.

Flagship cluster developments include The Shaughnessy (Holland), Victoria Park Villas (Bukit Timah), Jardin (Bukit Timah) and Archipelago (Bedok Reservoir). Pricing typically runs at a 15%–25% discount to comparable freehold detached landed within the same district.

Financing Landed Property

Landed purchases are subject to the same LTV, TDSR and MSR frameworks as condominiums — up to 75% LTV for first housing loan, stepped down for second and subsequent loans. Because absolute quantums are higher, the cash requirement is significant. For a S$6M terrace:

Line Item

Amount

Purchase Price

S$6,000,000

Buyer’s Stamp Duty (BSD)

S$229,600

ABSD (SC 1st property)

S$0

Legal fees

S$5,000

Minimum Cash Downpayment (5%)

S$300,000

CPF + Cash Downpayment (20%)

S$1,200,000

Loan Quantum (75%)

S$4,500,000

Monthly Mortgage (4.0%, 25-yr)

Approx. S$23,750

Total Cash Upfront

S$534,600

Stress-test your borrowing envelope using our TDSR/MSR guide. Most banks will require comfort on both household income resilience and liquid asset reserves for landed quantums > S$5M.

The Landed Investment Case

Scarcity

Singapore’s landed stock is capped. URA’s Master Plan does not meaningfully add new landed zoning — the only additions are small infill sites and occasional en-bloc redevelopments. The approximately 72,000 landed units on the island represent a finite pool that cannot grow in line with population or wealth.

Demand: Second-Generation Singaporean Wealth

A generation of Singaporeans who benefited from the 1998–2008 and 2013–2023 property cycles are now handing down wealth. Landed is the preferred destination for that capital: it is stable, defensible, and tax-efficient (no capital gains tax on primary residence). The “upgrade ladder” — HDB → condo → landed — is a real phenomenon driving steady demand at the mid-tier.

Underperformance in Weak Markets

The counter-argument: landed prices are less liquid than condominiums. In the 2008–2009 GFC drawdown and the 2014–2017 cooling-measures cycle, landed stock took 18–30 months longer than the condo market to clear at the new equilibrium. Buyers with time horizons shorter than 10 years should consider this liquidity premium.

Landed vs Condominium: Trade-offs

Dimension

Landed

Condominium

Privacy

Full

Shared common areas

Land ownership

Yes (freehold / 99-yr)

No (strata lot)

Maintenance

Owner’s responsibility

Managed by MCST

Facilities

None unless built by owner

Pool, gym, security, lounges

Renovation flexibility

High (subject to URA GFA)

Low (interior only, MCST rules)

Price entry (2026)

S$3.5M – S$80M+

S$1.2M – S$20M+

Typical absolute quantum

S$4.5M+ mid-tier

S$1.8M+ mid-tier

Foreign/PR eligibility

Restricted (mainland)

Open to all

Annual property tax (AV)

Generally higher (land)

Lower per sqft

Capital growth 2000–2024

Approx. 6.2% p.a.

Approx. 4.8% p.a.

Regulatory and Planning Considerations

Envelope Control

URA enforces an “Envelope Control” regime across most landed estates, capping building height (typically 2 storeys plus attic; 3 storeys in designated zones), setback distances (at least 2m front, 2m side for terraces), and GFA. Reconstruction or redevelopment must comply with the prevailing envelope.

Conservation Areas

Certain shophouse and black-and-white bungalow zones are gazetted conservation areas, subject to URA’s Conservation Guidelines. External alterations require URA written approval and must preserve heritage character.

Drainage Reserves and Plot Ratio

Some landed plots carry URA drainage reserves or setback obligations that effectively reduce buildable GFA. Always confirm with URA’s Master Plan zoning map and the developer’s Schedule of Conditions before offering.

Frequently Asked Questions

Can a foreigner buy landed property in Singapore?

Not on the mainland — the Residential Property Act restricts mainland landed to Singapore Citizens. Foreigners can purchase strata-landed (cluster) housing freely, and Sentosa Cove landed with LDAU approval.

What is the minimum plot size for a bungalow?

400 sqm under URA guidelines. A Good Class Bungalow requires a minimum 1,400 sqm plot in one of 39 gazetted GCB areas.

Is a cluster house considered landed?

Physically yes, legally no. Cluster units are strata lots under BMSMA and are not subject to the RPA’s landed restrictions. Foreign and PR buyers can purchase them without LDAU approval.

Can a PR buy a mainland terrace house?

Only with LDAU approval, which is granted selectively to PRs with substantial economic contribution to Singapore. Most PR applications for mainland landed are declined.

How is property tax calculated on landed?

Based on Annual Value (AV) set by IRAS, which reflects the market rental value of the property. Owner-occupier rates range from 0% to 32% (progressive); non-owner-occupier rates from 12% to 36%. See our property tax guide.

What is the difference between GCB Area and GCB?

A GCB Area is a gazetted zone (one of 39) in which GCB controls apply. A GCB is a specific detached bungalow within a GCB Area that meets the plot-size and setback criteria. A house in a GCB Area that does not meet GCB criteria is simply a detached house within that zone.

Can I convert a terrace into a semi-detached?

In theory yes, subject to URA planning approval and sufficient GFA, side setback and party-wall agreements. In practice, such conversions are rare and require consent from the neighbouring unit owner.

Is Sentosa Cove a good buy?

Sentosa Cove is Singapore’s only waterfront landed enclave and the only mainland-adjacent landed market open to foreign buyers (with LDAU approval). It has underperformed the broader landed index since 2014 due to cooling measures and limited tenant pool, but has recently re-rated on non-resident demand.

Disclaimer: Specifications, price bands and eligibility rules are current as at the time of writing. Always verify regulatory positions with URA, SLA and a qualified conveyancing lawyer before committing to a landed purchase. Nothing on this page is financial, tax, or legal advice.

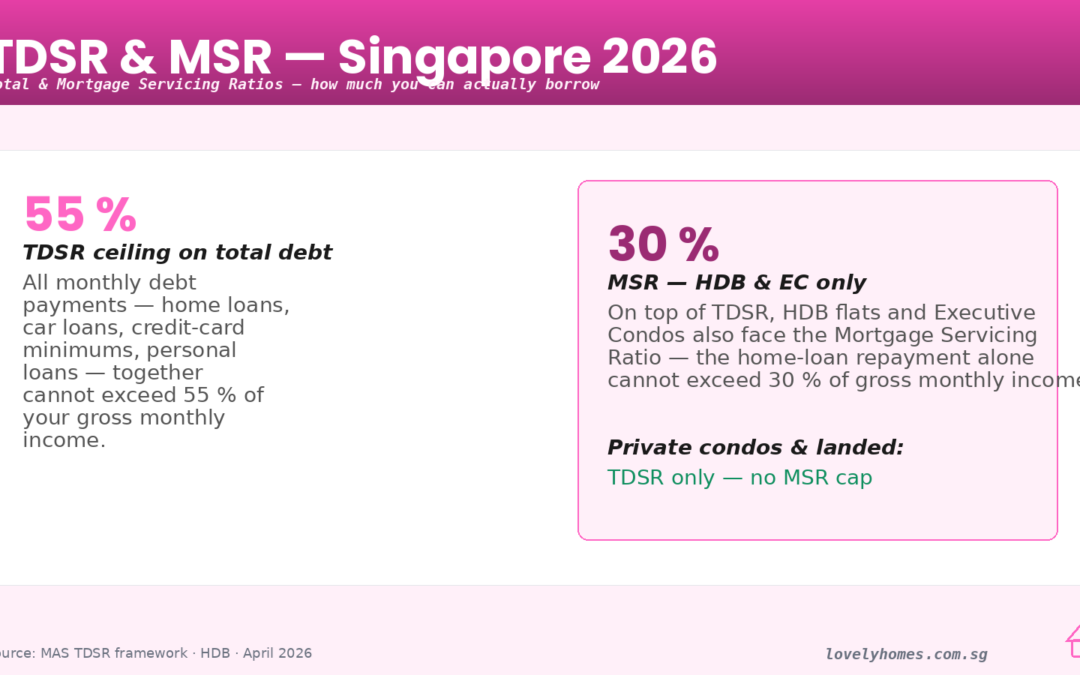

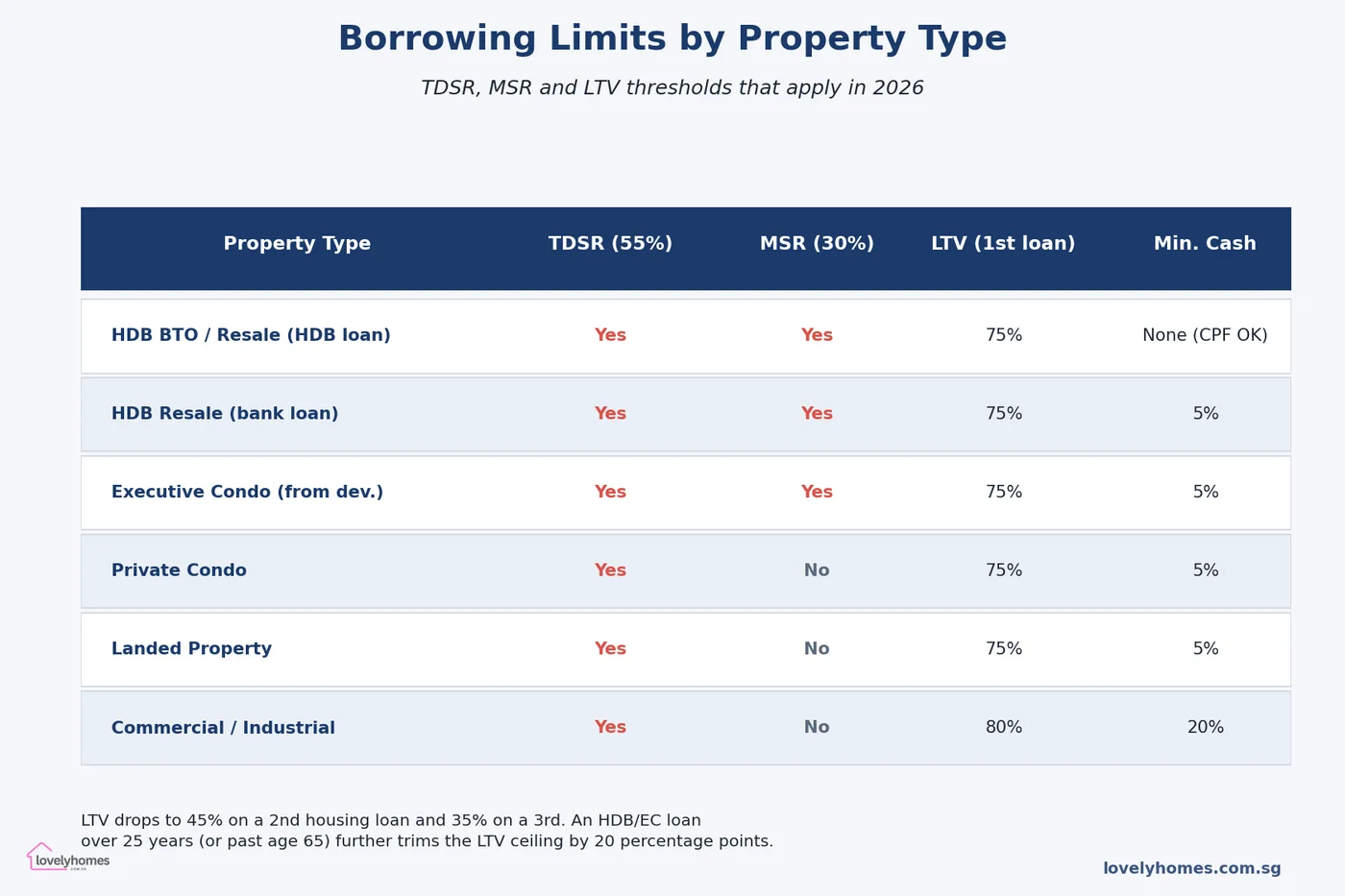

Figure 1: The two numbers that decide every Singapore home loan — TDSR at 55% of income and MSR at 30% for HDB and EC purchases.

If you have ever wondered why the bank’s pre-approval letter gave you a smaller loan than you budgeted for — or why a friend on the same salary can borrow noticeably more than you — the answer almost always comes down to two acronyms: TDSR and MSR. These are the two borrowing limits the Monetary Authority of Singapore (MAS) bakes into every residential mortgage, and in 2026 they are the single biggest determinants of how much home you can actually finance.

This guide is the 2026 edition. It covers exactly how TDSR and MSR are calculated, how they interact with the loan-to-value (LTV) cap, where the 4.0% stress-test rate comes from, what counts as income, what doesn’t, and — crucially — how to game the numbers in your favour without breaking any rules. We walk through a fully-worked Singapore example end-to-end and finish with the policy trajectory so you know what to watch for next.

Quick Answer: The 10 Things Every Singapore Borrower Should Know

TDSR is 55%. Total monthly debt repayments — including the new mortgage — cannot exceed 55% of your gross monthly income. Applies to every residential property loan.

MSR is 30%. Mortgage repayments on an HDB flat or Executive Condominium (EC) bought from the developer cannot exceed 30% of gross monthly income. Private condos and landed property have no MSR.

Stress-test rate is 4.0%. TDSR and MSR are calculated at a medium-term interest rate of 4.0% for residential loans, regardless of the rate you actually pay today.

LTV caps layer on top. First housing loan: up to 75% of purchase price. Second housing loan: up to 45%. Third and beyond: up to 35%.

Age and tenure matter. If the loan tenure pushes past age 65, or exceeds 30 years (25 for HDB), the LTV cap drops by 20 percentage points.

Variable income is haircut by 30%. Commission, bonus, rental and freelance earnings are only counted at 70% of the proven figure.

Existing debts eat into headroom. Car loans, credit-card minimum payments, student loans, and other mortgages all hit your TDSR ceiling before the new home loan does.

Guarantors are counted too. If you guarantee a sibling’s loan, it may sit in your TDSR — not theirs.

Cash down-payment rules mirror LTV. The first 5% (25% at higher LTV tiers) must be paid in cash; the balance can be CPF Ordinary Account funds.

Refinancing carve-out. Borrowers refinancing an owner-occupied property with no cash-out may be exempted from TDSR — a narrow but useful escape hatch.

What Is TDSR — The Framework That Underpins Every Home Loan

The Total Debt Servicing Ratio was introduced in June 2013 as part of MAS’s cooling-measures programme (see our full cooling measures timeline for the wider context). Its purpose is simple: to stop households from levering up to a level where a modest rise in interest rates would push them into negative cash flow. The 2010s saw Singapore’s household debt-to-GDP ratio climb past 70%, and MAS wanted a circuit-breaker that worked the same way regardless of which bank a buyer walked into.

TDSR caps all monthly debt obligations at 55% of gross monthly income. “All debt” is deliberately broad: it includes the prospective home-loan instalment (calculated at the stress-test rate), existing mortgages, car loans, personal loans, renovation loans, student loans, credit-card minimum repayments and any loans you have personally guaranteed. Even a dormant credit card with a S$20,000 limit is counted if the bank uses the 3% minimum-payment convention.

The ratio was originally set at 60% in 2013 and tightened to 55% in December 2021, where it remains in 2026. That three-percentage-point shave looks small on paper but at a typical Singapore household income removes roughly S$150,000–S$200,000 of borrowing capacity.

What Is MSR — The Second Ratio You Cannot Ignore for HDB and EC Buyers

The Mortgage Servicing Ratio is narrower but stricter. Introduced for HDB loans in 2011 and extended to bank loans on HDB flats in 2013, MSR caps the mortgage portion alone at 30% of gross monthly income for purchases of HDB flats and Executive Condominiums bought directly from the developer.

MSR is a subset of TDSR, not a substitute. HDB and new-EC buyers must clear both ratios — the tighter of the two binds. In practice MSR is almost always the binding constraint for HDB buyers because existing debt rarely adds up to the 25-percentage-point gap between MSR (30%) and TDSR (55%). For EC buyers the numbers narrow as the project moves through its 10-year maturation period — after the five-year minimum occupation period and the ten-year privatisation, a resale EC is treated like a private condo for borrowing-limit purposes, so TDSR alone applies.

For a side-by-side look at which ratios hit which property type, the matrix below summarises 2026 rules.

Figure 2: 2026 borrowing limits by property type. HDB flats and ECs face both MSR and TDSR; private condos, landed property and commercial assets only face TDSR.

How the 4.0% Stress-Test Rate Works — And Why It Matters More Than Your Actual Rate

Here is the trap that catches most first-time buyers: banks must calculate your monthly instalment using an assumed rate of 4.0% for residential mortgages, even if your actual rate is 2.5% or 3.0%. This is the medium-term interest rate, set by MAS and reviewed from time to time. It was revised upward from 3.5% to 4.0% in September 2022 and has not moved since.

Why 4.0%? The rate is designed to approximate the long-run average that Singapore floating-rate loans have oscillated around over a 30-year horizon. It is deliberately punitive — regulators would rather have borrowers told “you qualify for less” at origination than have the same borrowers go into arrears when rates spike. Anyone who lived through the 2022–2023 rate cycle, when three-month SORA went from 0.2% to 3.8% in 18 months, will appreciate the logic.

The mechanic: the bank plugs a 4.0% rate into the standard amortisation formula using your chosen loan tenure, derives an assumed monthly instalment, and tests that figure against your TDSR (55%) and, if applicable, MSR (30%). Your actual repayment — calculated at whatever rate the bank is offering — will be lower in most cases, leaving you with a margin of safety that MAS consciously engineered.

What Counts as Income — And Why Variable Pay Is Penalised

Income for TDSR/MSR purposes is not what you see on your IRAS tax statement. MAS prescribes a structured treatment:

Fixed salary. Counted at 100%. Evidenced by payslips (usually three to six months) and the latest CPF contribution history.

Variable income. Commission, bonus, overtime, and freelance earnings are haircut by 30%, so only 70% of the verified average is recognised. The haircut applies to the entire variable component, even if you can show multiple years of steady track record.

Rental income. Counted at 70% of the gross rent receivable, net of void periods. A two-year tenancy agreement is strong evidence; month-to-month leases are viewed more sceptically.

Self-employed / business income. Two years of Notice of Assessment (NOA) are the default evidentiary bar, with the 30% haircut applied.

Allowances and AWS. Typically 100% if contractual and evidenced; otherwise haircut.

This is where the seemingly simple 55% number becomes surprisingly individual. A banker earning S$12,000 monthly but with 40% of that as variable gets assessed on S$7,200 fixed + S$3,360 post-haircut variable = S$10,560 — so the TDSR ceiling drops to S$5,808 per month rather than the nominal S$6,600.

What Counts as Debt — The Items Borrowers Miss

The other half of the equation is debt. The headline items — the new home loan instalment, existing mortgages, and car loans — are obvious. Less obvious items often catch borrowers out:

Credit-card minimum payments. Banks use a 3% minimum convention on the outstanding balance (or sometimes on the total credit limit). If you carry S$30,000 revolving credit across cards, that is a S$900 monthly hit on your TDSR — shaving S$192,000 off your loan ceiling at a 4.0% stress rate over 30 years.

Renovation and personal loans. Unsecured loan instalments count in full.

Student loans. Included in TDSR from the date repayments begin.

Guarantor obligations. If you have co-signed a relative’s loan and there is no formal debt-transfer, some banks will count the full instalment against you. Others use 50%. Ask the relationship manager explicitly.

Outstanding ABSD remission obligations. If you are on a remission schedule (e.g. from selling a prior property to claim remission on a new purchase), the existing loan remains in TDSR until the sale completes.

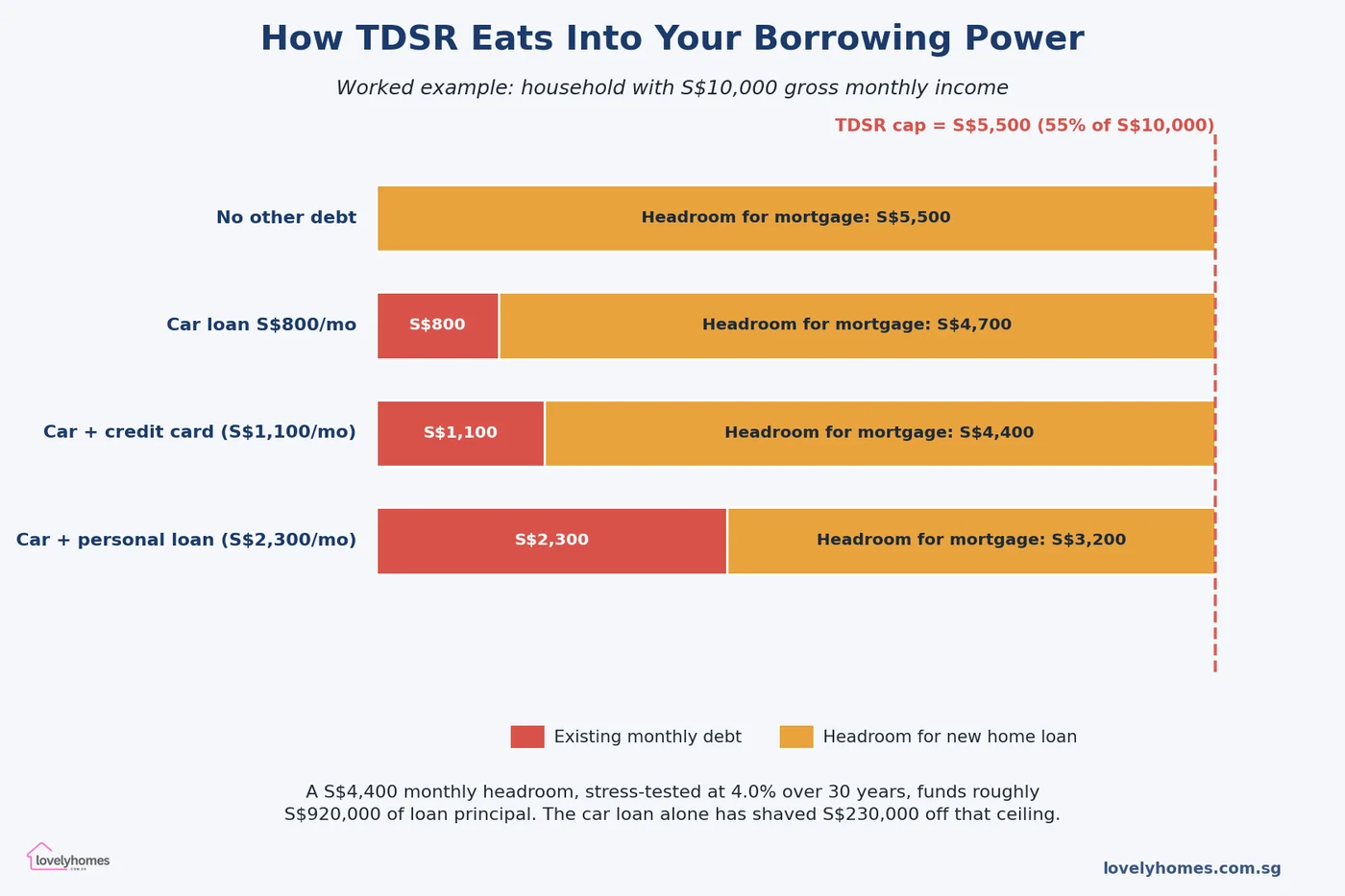

A Fully-Worked Example: A S$10,000-a-Month Household Buying a Private Condo

Figure 3: How different existing-debt profiles crater the monthly headroom available for a new mortgage, given a household earning S$10,000 gross.

Consider a dual-income couple: combined gross monthly salary S$10,000, both on fixed pay, no variable component. They are looking at a S$1.8 million resale private condo in District 15.

Step 1 — TDSR cap. 55% × S$10,000 = S$5,500. No MSR applies because this is a private condo.

Step 2 — Existing debts. One car loan at S$800/month and revolving credit balances generating a S$300/month minimum payment. Total existing obligations: S$1,100.

Step 3 — Headroom for the new mortgage. S$5,500 − S$1,100 = S$4,400 per month available for the new home loan instalment.

Step 4 — Maximum loan principal. At the 4.0% stress rate over a 30-year tenure, S$4,400 monthly funds approximately S$922,000 of loan principal (standard amortisation formula: P = M × [(1 − (1 + r)^(−n)) / r]).

Step 5 — LTV cap. At 75% LTV on an S$1.8m purchase, the bank could lend up to S$1,350,000 — but TDSR limits them to S$922,000 here, so TDSR binds, not LTV. The couple needs S$878,000 of combined cash and CPF equity.

Flip the same household to an HDB flat at S$700,000: now MSR binds first. 30% × S$10,000 = S$3,000 maximum mortgage instalment. That fundamentally funds roughly S$628,000 — well below the 75% LTV ceiling of S$525,000… wait. In this case the 75% LTV actually binds below MSR, because S$525,000 of loan needs only about S$2,500/month at 4.0% over 25 years, comfortably inside MSR. So the couple’s CPF-plus-cash needs to fill the remaining S$175,000.

These two scenarios show the recurring pattern: for HDB/EC buyers, MSR or LTV usually binds; for private/landed buyers, TDSR usually binds. The flow of the calculation matters, and every added dollar of existing debt has a disproportionate impact through the 30-year amortisation lever.

How to Legitimately Maximise Your Borrowing Ceiling

Nothing below involves gaming the system — each lever is recognised by banks and MAS. Together they can add S$200,000–S$400,000 to a buyer’s loan ceiling.

Close dormant credit facilities. A S$50,000 unused overdraft or a clutch of credit cards still hits TDSR via the 3% minimum rule. A week of admin before you apply for pre-approval can move the needle.

Pay down the car loan. High-instalment vehicle finance is the single most common TDSR killer. A S$1,000 monthly car note costs you roughly S$210,000 of home-loan capacity at 4.0%/30yr.

Lengthen the tenure (cautiously). A 30-year tenure beats a 25-year one on headline TDSR because the stress-rate instalment is lower — but watch the age-65 and 30-year triggers that knock the LTV down 20 points.

Co-apply with a higher earner. Joint applications aggregate income and debt. If spouses have different debt loads, consider which combination maximises the pooled headroom.

Formalise variable income. A commissioned sales professional with one year of written contracts may be haircut more heavily than one with two years of NOAs. Waiting one tax cycle can unlock meaningful capacity.

Use a Loan Assessment before committing. Banks in Singapore offer in-principle approval (IPA) at no cost. Three IPAs from different banks let you benchmark the figure.

How Singapore’s Framework Compares Globally

Singapore is not alone in prescribing debt-service ratios, but its combination is unusually strict. Hong Kong applies a 50% debt-service ratio with a 70% LTV cap for first-time owner-occupiers — broadly comparable but no separate MSR for public housing. The United Kingdom uses a 4.5× income loan-to-income ratio at most lenders (soft cap), with affordability stress-tested at 3 percentage points over the reversion rate. Australia’s prudential regulator APRA applies a serviceability buffer of 3 percentage points over the contracted rate — a rule-of-thumb approach rather than a hard ratio.

The common thread in all four jurisdictions is a stress-test mechanism designed to withstand a rate spike. Singapore’s 4.0% medium-term rate is higher (more conservative) than the contracted-rate buffers used in the UK and Australia, which is one reason Singaporean household debt has been more resilient through recent cycles than peers. MAS has been explicit that this is by design: household leverage is viewed as a systemic risk, not purely a consumer-protection issue.

What Might Come Next — The Forward View

The 4.0% stress rate has held since September 2022. Three scenarios could prompt a revision in the next 12–18 months:

Sustained higher long-term rates. If three-month SORA settles above 3.5% on a durable basis, MAS may nudge the medium-term rate to 4.25% or 4.5% to preserve the buffer it represents.

Renewed leverage in the private condo segment. If luxury-segment TDSR headroom is being used aggressively to bid up prime-district prices, expect tighter LTV on second/third loans rather than a TDSR change.

Public housing affordability stress. If HDB resale prices outrun wage growth materially, MSR could tighten from 30% to 25%. This would be the single most consequential move for first-time buyers.

None of the above is signalled by MAS at the time of writing (April 2026) — but the Financial Stability Review due in November 2026 is the data release to watch. Historically MAS has adjusted TDSR and MSR in the December statement that accompanies the cooling-measures package.

Frequently Asked Questions

1. Does TDSR apply to refinancing my existing mortgage?

For owner-occupied properties, a clean refinance without any cash-out and without extending the principal is generally exempted from TDSR under a carve-out MAS introduced to avoid penalising existing borrowers. If you take a cash-out top-up or increase the principal, the full TDSR test applies. For investment-property refinancing, TDSR applies in full regardless of cash-out status, so build in a review of your current debt profile before signing any refinance Letter of Offer.

2. How is TDSR calculated if I am self-employed with irregular income?

Banks use two years of Notice of Assessment (NOA) as the primary evidentiary source, take the simple average, apply the 30% haircut, and treat the resulting figure as your recognised gross monthly income. A particularly strong year — say a bumper bonus — will be smoothed. If you have less than two years of NOAs the bank will often decline or require a significantly larger down-payment. Incorporating yourself through a Pte Ltd does not change this; director’s remuneration drawn as salary is still subject to the haircut.

3. Can I borrow more by stretching the loan tenure?

Up to a point, yes. A 30-year tenure reduces the stress-rate instalment versus a 25-year tenure, increasing how much loan principal S$4,400 (in our worked example) can support. But two triggers cap the benefit: if your loan extends past age 65 or exceeds 30 years (25 for HDB), the LTV cap drops by 20 percentage points — from 75% to 55% on a first loan. The net effect is usually worse, not better. Most brokers recommend landing the tenure such that the loan concludes at or just before age 65.

4. Are joint-borrower applications better than going solo?

Usually, because they aggregate income while both parties still share the TDSR ceiling. The nuance is “income-weighted average age” for tenure calculations — if a 55-year-old and a 35-year-old co-apply, the bank blends their ages by income share to determine the maximum allowable tenure. Adding a much older co-applicant to a younger borrower can shorten the tenure and reduce the headroom on paper. Structured correctly, joint applications reliably produce higher approvals than solo for dual-income households.

5. What happens to TDSR if interest rates fall sharply?

Nothing, in the short run. The 4.0% stress rate is a regulatory input, not a market rate. Falling SORA means your actual monthly instalment shrinks and your actual debt-service ratio improves, but the ceiling at which MAS sets the TDSR bar is unchanged. Over a multi-year horizon, if rates settle well below 4.0% on a sustained basis, MAS may consider lowering the stress rate — but the precedent is that adjustments are infrequent (the last move was September 2022).

6. Does CPF Ordinary Account balance count as income for TDSR?

No. CPF OA is treated as equity (part of the down-payment and subsequent instalments), not as income. The monthly CPF contribution inflow also does not count as additional income — your CPF contributions are already a reduction from your gross pay, and gross pay is what banks use. The only way CPF affects borrowing capacity indirectly is through the Home Protection Scheme (for HDB loans) and through the cash-CPF split in the down-payment.

7. I was denied because of TDSR — what are my options?

First, get the denial reasoning in writing and compare it with a second IPA at a different bank — underwriting interpretations vary on edge cases, particularly around variable income and guarantor obligations. Second, tackle the debt side: clear a car loan, consolidate or close credit cards, discharge a guarantor role. Third, stretch the timeline: a fresh NOA next April may unlock the variable-income shortfall. Fourth, reduce the target property price — a 10% lower purchase price typically requires a proportionally smaller loan and therefore a smaller headroom. Finally, consider a joint application with a fixed-income parent (though this binds their future TDSR too).

This article is an editorial guide for general information only and does not constitute financial, legal or mortgage advice. The figures quoted reflect rules in force on the date of publication (April 2026) and may change. Confirm the authoritative position with the Monetary Authority of Singapore (MAS), the Housing & Development Board (HDB), your bank’s credit officer and a licensed mortgage broker before committing to any loan or property purchase. Interest-rate scenarios and worked examples are illustrative; your actual borrowing ceiling depends on the full underwriting review at application.

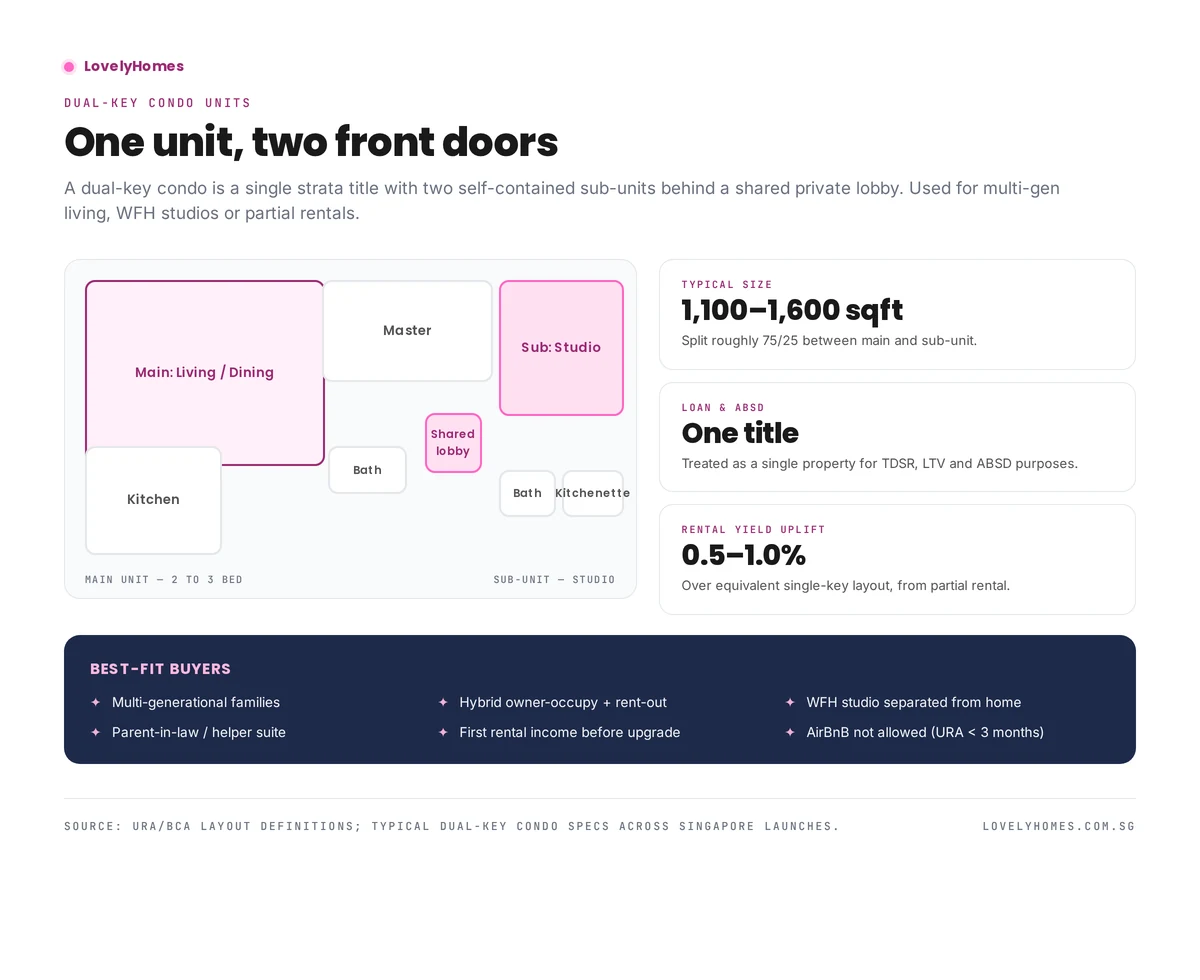

A dual-key condo is a single strata title with two self-contained sub-units — typically a main 2 or 3-bed and a separate studio — behind a shared private lobby. It counts as one property for ABSD, LTV and TDSR. Typical size is 1,100–1,600 sqft. Rental yield uplift from partial rental is 0.5–1.0% over an equivalent single-key unit. Best for multi-gen families, WFH separation, or partial rentals while occupying the main unit.

The dual-key layout was a mid-2010s development marketing innovation: take a standard 3-bedroom floorplate, wall off one of the rooms into a self-contained studio with its own kitchenette and bathroom, and sell the whole thing as one strata title. Ten years on, dual-keys are a small but durable slice of the launch menu — and the rental maths often makes sense.

This guide covers the layout, the financing treatment, the rental-yield case, and the situations where a dual-key actively hurts you. If dual-key is on your shortlist alongside other condo formats, our condo downpayment guide covers the cash/CPF/LTV maths you’ll need to price it.

Typical dual-key layout — one title, two self-contained homes.

What a dual-key actually is

Two separate self-contained units sharing a private lift lobby. Each unit has its own:

Front door

Kitchen or kitchenette

Bathroom

Living / sleeping area

But critically, they share one strata title, one loan, one ABSD payment, one property-tax account.

Typical sizes and configurations

Layout

Main unit

Sub-unit

Total size

2 + 1 dual-key

2-bed, ~700–900 sqft

Studio, ~300–400 sqft

1,100–1,300 sqft

3 + 1 dual-key

3-bed, ~950–1,200 sqft

Studio, ~400 sqft

1,400–1,600 sqft

Financing, ABSD and TDSR

One property, one set of duties

The entire dual-key unit is a single purchase. BSD and ABSD are calculated on the full purchase price; LTV is capped as if it were one property; TDSR and MSR apply once. This is the defining benefit over buying two shoeboxes — which would each attract separate ABSD.

Bank valuation quirks

Valuers apply a small discount to the sub-unit versus a freestanding studio, because it cannot be sold or remortgaged separately. Expect 3–6% under the sum of two equivalent standalone units.

The rental-yield case

The typical dual-key yield uplift runs 0.5–1.0 percentage points over an equivalent single-key 3-bedder. Two drivers:

The studio rents at studio PSF, which is always the highest PSF band.

Partial-rental frees the owner to occupy the main unit — keeping one-time ABSD exposure.

Who dual-keys suit

Multi-gen families: adult children, parents-in-law, or a helper with a separate bath/kitchen.

Hybrid owner-occupy + rent-out: owner in the main unit, studio leased on 12-month terms (short-term AirBnB is prohibited under URA < 3-month rule).

WFH professionals: completely separate workspace behind its own door.

First-time investors: live in the main unit, let the studio produce cash flow without triggering ABSD on a second property.

When the dual-key format hurts

Resale liquidity is thinner than a standard 3-bedder — the buyer pool is narrower (single families who want a standard 3-bed may skip dual-keys).

The sub-unit can feel cramped without good natural light — check window/air conditioning provisions.

PSF at launch is often above the comparable single-key because the developer prices in the yield-potential premium.

Frequently asked questions

Can I sell the two units separately later?

No. One strata title. The only way to sell separately is physical remodelling + strata subdivision, which is almost never approved.

Can I AirBnB the sub-unit?

No. URA forbids short-term rentals (< 3 months) of private residential property. 12-month leases are fine; serviced-residence-style rentals are not.

How does property tax work?

One tax account based on the unit’s Annual Value. If you owner-occupy the main and lease the sub-unit, the owner-occupier AV rates apply to the whole unit — a subtle benefit over leasing the entire unit. See our property tax guide.

Do dual-keys en bloc well?

Same as any other unit in the development — the en bloc sale is on the development, not the unit. Apportionment is usually by total share value, so dual-key owners are not disadvantaged.

This guide is for general information only and is accurate as of April 2026. Singapore property rules, taxes and cooling measures change frequently — always verify current figures with URA, IRAS, HDB or a licensed professional before committing. LovelyHomes is not a financial, legal or tax advisor.

Property agent commission in Singapore is never a published rate — it is negotiated on a case-by-case basis, constrained by market convention and the Council for Estate Agencies (CEA) framework. This 2026 guide walks through what is conventional, what is negotiable, who actually pays, and how to choose an agent worth the fee.

For the regulator’s side, the CEA website is authoritative on registration, disciplinary actions, and agent obligations.

Quick Answer — Typical 2026 Rates

HDB resale — sale: 2% (seller pays).

HDB resale — buy: 1% (buyer pays, optional).

Private condo — sale: 1–2% (seller pays).

Private condo — buy (resale): 0–1%; commonly covered by the seller via co-broke.

New launch condo: ~1% paid by the developer to the agent (buyer pays nothing).

Rental (1-year lease): 0.5–1 month’s rent, typically paid by landlord; split by custom.

Typical 2026 commission rates across HDB resale, private condo, new launch and rental transactions.

The CEA Framework

Every practising property agent in Singapore must be registered with the Council for Estate Agencies (CEA) and affiliated with a licensed estate agency. Key CEA rules:

Registration: Agents have a 6-digit CEA registration number. Check it on the public register before engaging.

One-party rule: The same agent cannot represent both buyer and seller in the same transaction. An agency can have different agents for each side, but not the same person.

Estate Agency Agreement (EAA): Every formal engagement must be documented in an EAA specifying the service scope, exclusivity, and commission structure.

Continuing education: CEA mandates continuing education each year, which is why you should check registration is current.

HDB Resale Commissions

Seller-side commission

The standard HDB resale seller-side commission in Singapore is 2% of the transacted price. On a S$600,000 flat, that is S$12,000 + GST, payable at completion.

For this fee, a competent agent typically delivers:

Coordination with the buyer’s agent, lawyers, and HDB

Buyer-side commission

HDB buyer-side commission is 1% of the transacted price, where paid. Many buyers use the HDB Resale Portal directly without an agent, in which case no commission applies. Where an agent is used on the buyer side, 1% is the market norm.

Private Condominium Commissions

Seller-side

Private condo sellers pay between 1% and 2% of transacted price, with 2% being common and 1.5% negotiable for larger sale values. The higher fee reflects stronger marketing requirements (larger buyer pool, more luxury property presentation).

Buyer-side (resale)

Buyers rarely pay a separate commission in private resale transactions. The seller’s 2% agent typically co-brokes with the buyer’s agent, splitting the seller’s 2% (typically 1%–1% but sometimes 1.2%–0.8% if the listing agent did most of the marketing work). The buyer pays nothing additional.

New launch

In a new launch condo, the developer pays the agent’s commission. Conventional market rates are 1% from the developer, though some luxury launches pay more to attract top agents. The buyer pays nothing for agent services.

Rental Commissions

The norm for residential rentals is a full month’s rent commission on a 2-year lease, split by custom:

2-year lease (standard): 1 month’s rent, paid by landlord.

1-year lease: 0.5 month’s rent, typically paid by landlord.

Expat rental ≥ S$5,000/month: landlord typically pays, as the rental amount justifies it.

Rental below S$3,500/month: the tenant’s agent may ask the tenant to pay the commission directly.

What Is Negotiable?

Commission rates are not fixed by CEA or by any regulation. They are market conventions, and everything is negotiable:

When you have leverage

Large transaction value. 1.5% on a S$3m condo (S$45,000) can be discussed.

Multiple properties under one engagement. Selling two units with one agent can justify a reduced rate on each.

Repeat business. An agent who has represented you before should reflect that.

Short timeline with minimal marketing. If the agent is simply facilitating a deal you already have, a flat fee rather than percentage commission is reasonable.

When you have less leverage

Short-dated MOP-edge flats. These require more marketing effort to attract rare eligible buyers.

Ethnic-quota-closed blocks. Narrowed buyer pool means harder selling.

Luxury condos in quiet markets. Agents may push for higher rates to justify the effort.

How to Choose a Good Agent

Commission rate is only part of the calculus. A 2% agent who sells at 2% above valuation out-performs a 1.5% agent who sells at 5% below. What actually matters:

1. Track record in your estate or property type

Ask for the agent’s recent transacted listings in the same estate and flat type. Most agents have a concentrated specialty — lean into that.

2. Responsiveness

Do they return calls and messages within 2 hours during working hours? If not, imagine trying to coordinate viewings with them.

3. Marketing approach

What listings will they use? Will they pay for PropertyGuru premium placement, professional photography, Facebook/IG ads? For sale-side, marketing budget matters.

4. Negotiation style

A good agent negotiates hard for your side, not for a quick commission. Ask how they handle price objections.

5. CEA registration and standing

Verify the CEA number is current. Check the public register for any disciplinary actions or complaints.

Estate Agency Agreement Essentials

Every engagement needs a written EAA. Key clauses to review:

Exclusivity: Sole agency (exclusive) vs non-exclusive. Sole agency typically gets more effort but you cannot switch easily during the term.

Term: 3 months is common, 6 months for private condo. Always specify an end date.

Commission rate: State the percentage and the basis (transacted price) clearly.

Marketing expenses: Whether the agent or the seller bears marketing costs.

Termination clause: Under what conditions either party can terminate before the term ends.

Post-termination tail: A common clause says the agent earns commission if the property is sold to a buyer the agent had introduced even after termination, for a period of 3–6 months.

Red Flags to Avoid

Agent without CEA number — illegal to transact.

Requests for upfront cash for marketing expenses — should be bundled in the commission.

Reluctance to sign a written EAA — a CEA violation.

Agent suggesting they represent both sides — also a CEA violation.

Pressure to sign OTP quickly without letting you consult a lawyer — a sign the agent is pushing for commission, not your interests.

Promise of guaranteed sale price — no agent can guarantee this in a market-driven transaction.

FAQ — Property Agent Commission 2026

Do I have to pay a commission if the deal falls through?

Typically no. Commission is earned on completion, not on introduction. The EAA should say this explicitly — ensure it does.

Can I use different agents for buying and selling the same property?

Yes. Many sellers use one agent for the sale and a different one for the onward purchase. There are no CEA restrictions on this.

Are commission rates negotiable even for new launches?

Not really — the developer sets the agent’s fee structure, and the buyer pays nothing either way. What is negotiable is which agent to use, as different agents may offer different rebates back to the buyer (check CEA rules on rebates).

Who pays the commission in a cash sale of a private condo?

The same parties as any other sale: the seller pays the seller-side commission, and the buyer-side commission (if any) depends on the co-broke arrangement. Cash vs financed makes no structural difference.

Can I file a complaint against an agent?

Yes, through the CEA complaints process at cea.gov.sg. Complaints about fees, conduct, misrepresentation or CEA rule violations are taken seriously.

Disclaimer: Commission rates are market conventions, not regulated minimums. Rates and customs may shift over time. Always document your engagement in an Estate Agency Agreement and verify your agent’s CEA status before engagement.