Ang Mo Kio Neighbourhood Guide Singapore 2026: Property Prices, MRT, Schools and Investment Outlook

Quick Answer — Ang Mo Kio at a Glance (2026)

- Location: Central-North Singapore; URA planning area “Ang Mo Kio”; part of District 20 corridor.

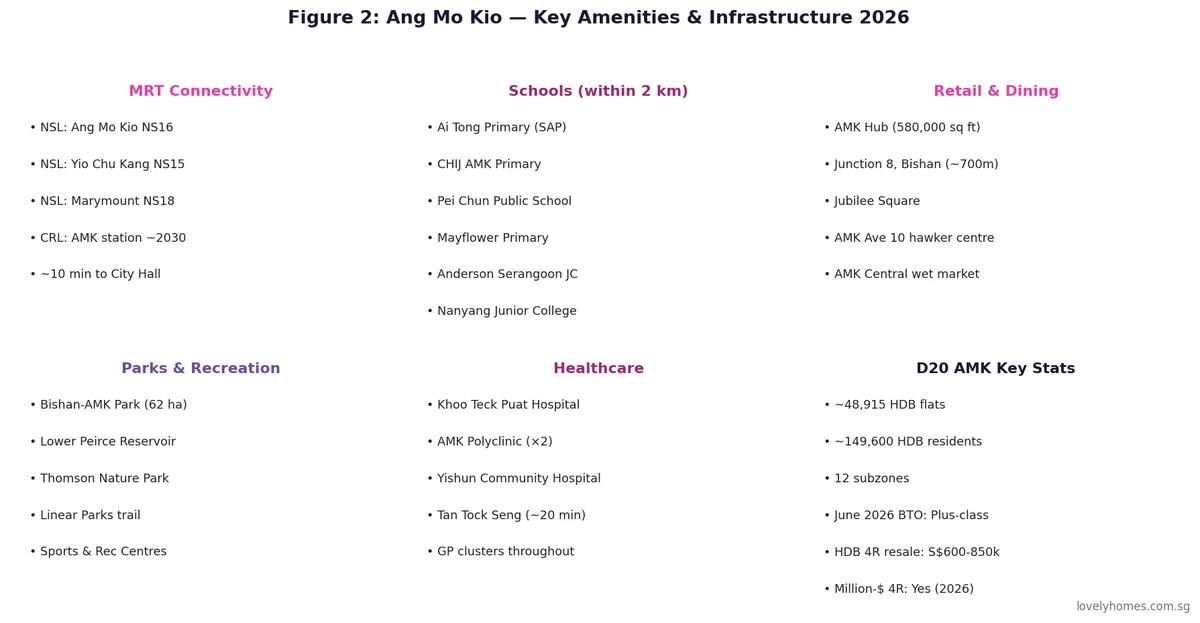

- MRT: NSL stations — Ang Mo Kio (NS16), Yio Chu Kang (NS15), Marymount (NS18). Cross Island Line (CRL) Phase 2 station in AMK expected ~2030.

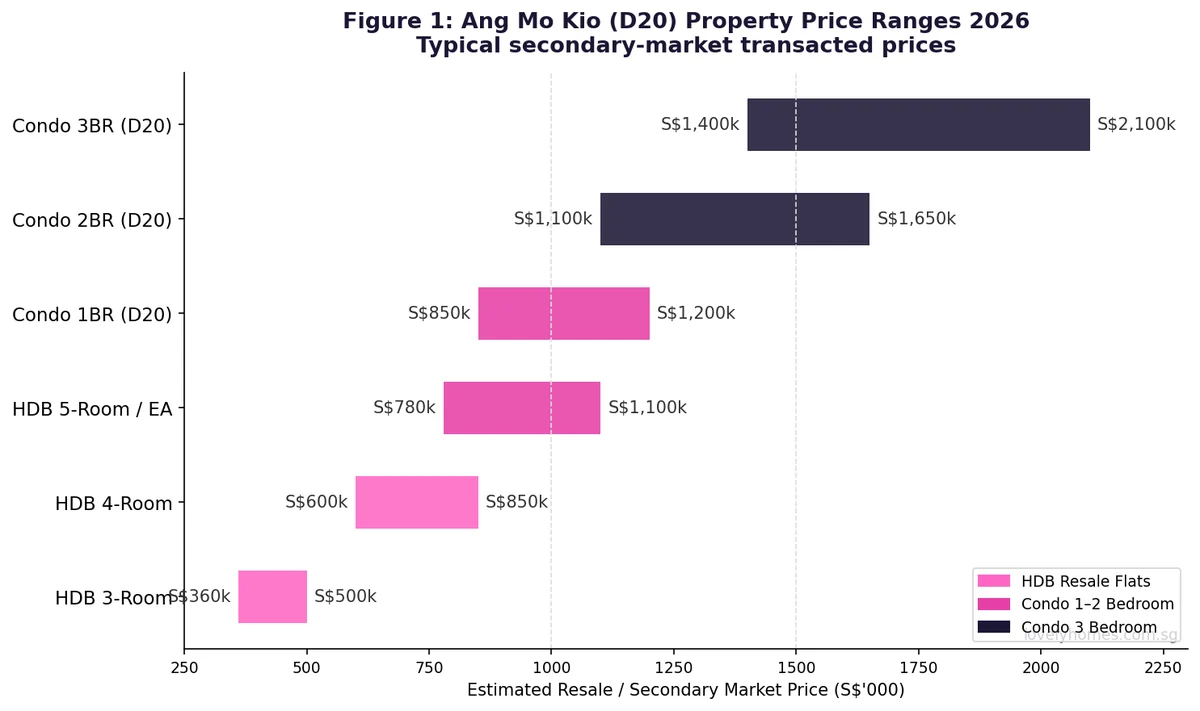

- HDB resale prices (2026): 3-Room S$360k–S$500k · 4-Room S$600k–S$850k · 5-Room S$780k–S$1,050k. First million-dollar 4-room deal (S$1.11M) recorded at AMK Court in January 2026.

- Private condo prices: 2-Bedroom S$1.1M–S$1.65M · 3-Bedroom S$1.5M–S$2.2M (limited supply, mostly 99-year leasehold).

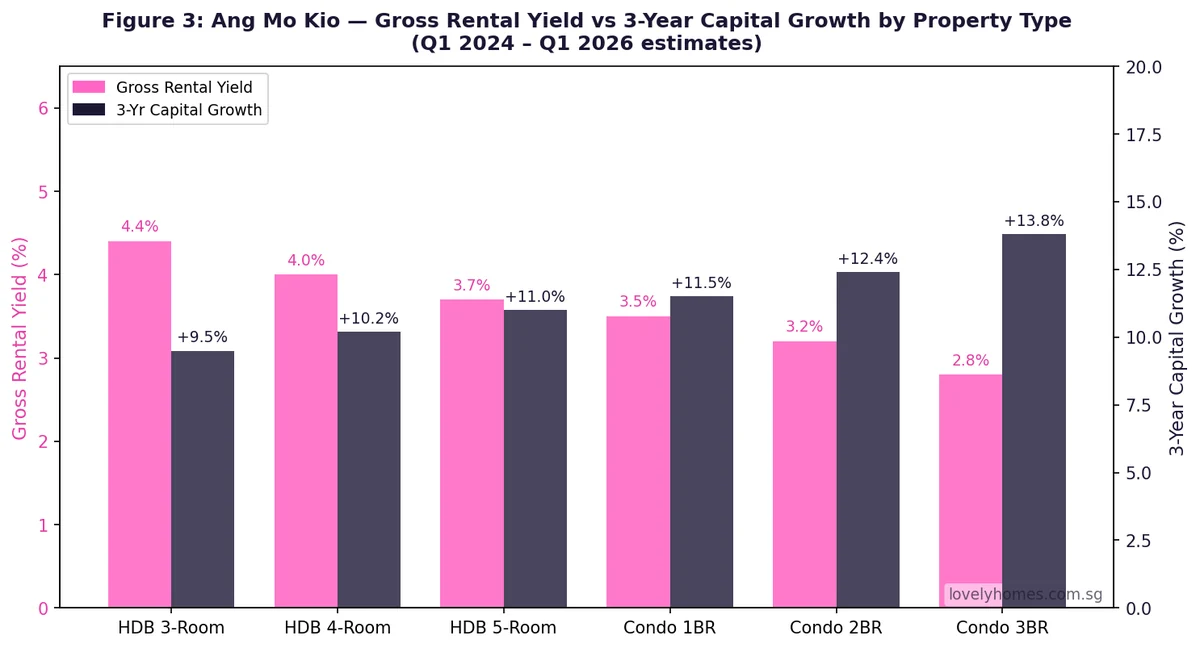

- Gross rental yield (2026 est.): HDB 4-Room ~4.0–4.4% · Condo 2BR ~3.2–3.5%.

- Schools: Ai Tong Primary (SAP), CHIJ AMK Primary, Nanyang Junior College, Anderson Serangoon Junior College.

- Healthcare: Khoo Teck Puat Hospital (762 beds), AMK Polyclinics (2 branches).

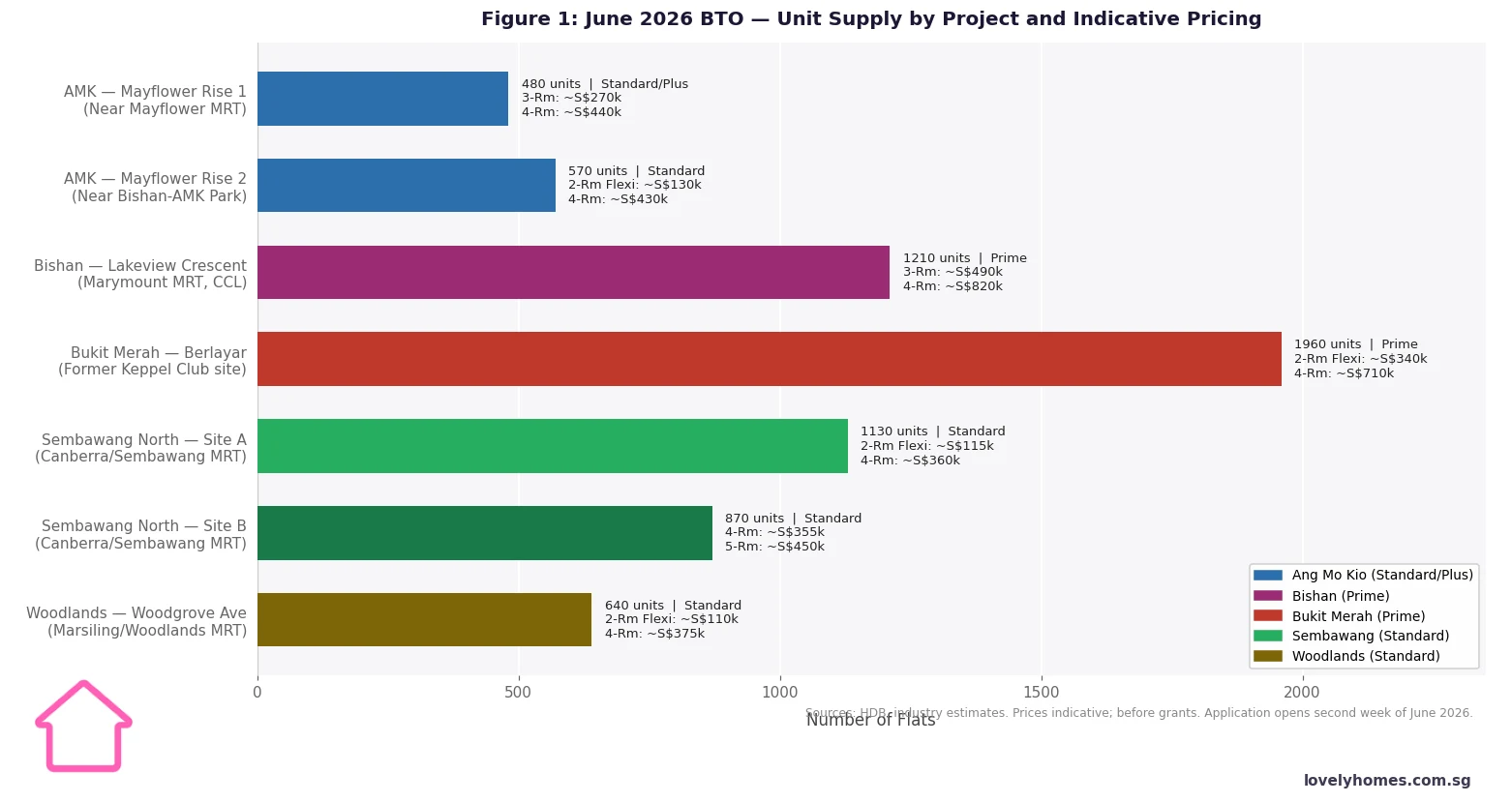

- June 2026 BTO: HDB is launching two Plus-class projects in Ang Mo Kio as part of the June 2026 exercise — expect tighter resale restrictions (10-year MOP, subsidy clawback) on these units.

What Is Ang Mo Kio — and Why Does It Matter to Property Buyers?

Ang Mo Kio (AMK) is one of Singapore’s oldest and most established Housing & Development Board (HDB) new towns, planned by the HDB and URA in the 1970s and progressively built out through the 1980s. The name — loosely translated from Hokkien as “junction of the Ang Mo (European/Western) bridge” — hints at its colonial-era heritage. Today, AMK is a thriving, self-contained community of approximately 149,600 HDB residents spread across 12 subzones and roughly 48,915 flats.

For property buyers, AMK sits at an interesting intersection: it is close enough to the city (Ang Mo Kio MRT is approximately 20 minutes from Raffles Place by North–South Line) to command a pricing premium over more distant towns such as Woodlands or Jurong West, yet its predominantly HDB landscape keeps prices meaningfully below the Core Central Region (CCR). In the first quarter of 2026, four-room resale flats in AMK transacted at a median of S$720,000–S$750,000 — competitive with neighbouring Bishan and Toa Payoh, and well below the CCR’s equivalent private housing.

The URA’s master plan for AMK focuses on renewal: upgrading ageing commercial nodes, expanding park connectivity through the 62-hectare Bishan–Ang Mo Kio Park, and improving public transport with the forthcoming Cross Island Line (CRL) Phase 2 station, which will add a second rail line to the town by around 2030.

Ang Mo Kio Property Prices 2026 — HDB Resale and Private Market

AMK’s property market is dominated by HDB resale flats, which account for well over 95% of all transactions in the planning area. Private condominiums are relatively scarce, making the few available developments — such as The Panorama (698 units, 99-year leasehold, AMK Avenue 2) — significant benchmarks for the area.

HDB resale highlights (Q1 2026):

- 3-Room flats: S$360,000–S$500,000. Common in older precincts such as AMK Avenue 3 and AMK Avenue 6. Compact at 60–69 sqm, these are popular with singles (age 35+), divorcees, and small families on tighter budgets.

- 4-Room flats: S$600,000–S$850,000. The workhorse of AMK’s resale market. The first million-dollar 4-room deal in AMK Court was registered in January 2026 at S$1,110,000 — a landmark that signals premium-located units (high floor, near MRT) now breach seven figures even in non-CCR towns.

- 5-Room and Executive Apartments (EA): S$780,000–S$1,150,000+. Larger families and upgraders seeking spacious HDB living without the private-condo price tag favour these units. EA layouts in AMK typically offer around 140–145 sqm.

Private condominium prices (2026): With very limited new supply, AMK condominiums trade on scarcity. The Panorama (TOP 2018, 698 units) remains the main 2BR benchmark at S$1.1M–S$1.55M; 3BR units range from S$1.5M to S$2.2M depending on floor level and facing. Gross rental yields on AMK condominiums are estimated at 3.2–3.5% for 2BR units — lower than equivalent HDB yields but supported by a steady tenant pool including Nanyang Junior College lecturers, hospital staff from Khoo Teck Puat Hospital, and corporate professionals working in the nearby Ang Mo Kio industrial estate.

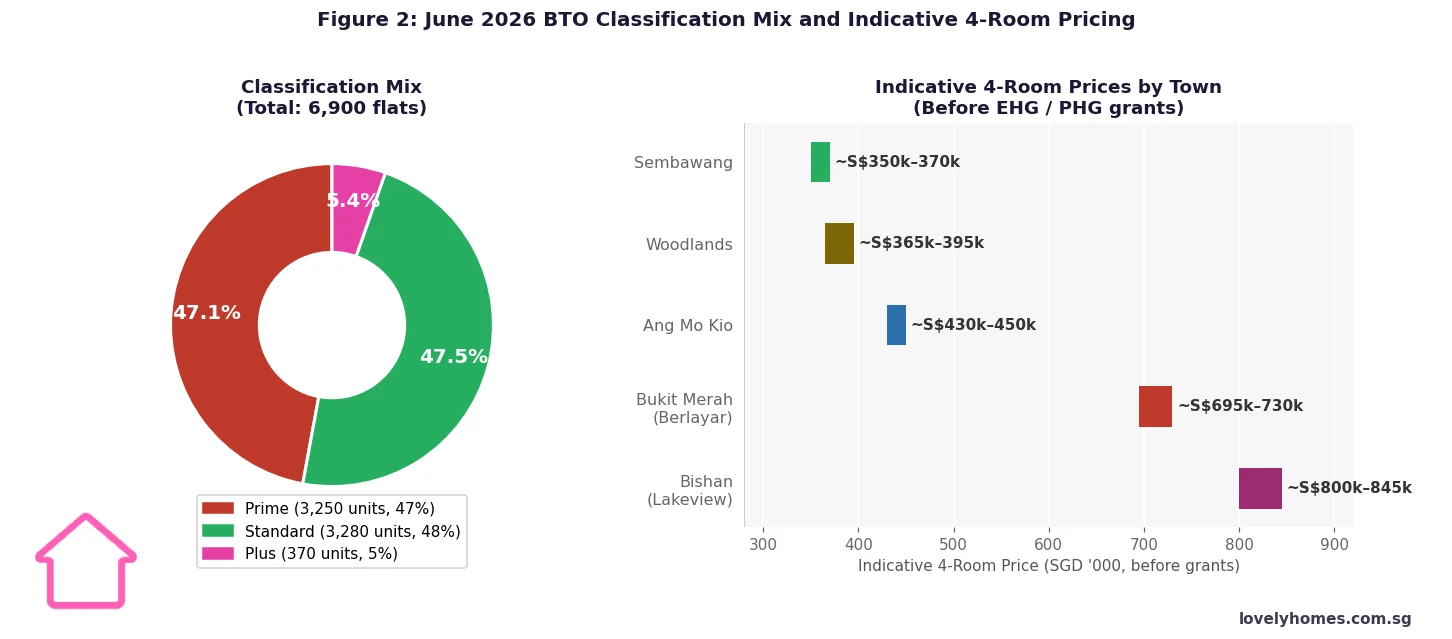

The June 2026 BTO Launch and Its Implications

HDB’s June 2026 BTO exercise — the largest single launch of the year at approximately 6,900 flats across seven projects in five towns — includes two Plus-class projects in Ang Mo Kio. Under HDB’s classification framework (Prime, Plus, Standard), Plus flats carry tighter resale conditions: a 10-year Minimum Occupation Period (MOP), income ceiling of S$14,000/month for buyers, and a subsidy clawback upon resale. Buyers considering these BTO units should factor in that the longer MOP reduces near-term liquidity, and the clawback mechanism limits capital appreciation on the resale of Plus flats compared with Standard flats in the same town.

MRT Access and Transport Connectivity

AMK’s North–South Line (NSL) connectivity is its biggest transport asset. Three NSL stations serve the planning area:

- Ang Mo Kio (NS16): The town’s primary interchange. Train travel time to Orchard is approximately 14 minutes; Raffles Place approximately 22 minutes. AMK MRT is directly integrated with AMK Hub shopping centre and the AMK bus interchange.

- Yio Chu Kang (NS15): Serves the northern AMK precincts and the Yio Chu Kang Stadium area. Journey time to City Hall is approximately 25 minutes.

- Marymount (NS18): Serves the southern AMK fringe bordering Bishan; useful for residents in AMK Avenue 1 and the Thomson area.

The upcoming Cross Island Line (CRL) Phase 2, currently under planning by the Land Transport Authority (LTA), is expected to include a station in the AMK planning area by approximately 2030. A second rail line would significantly improve east–west connectivity for AMK residents — currently, all NSL journeys into town require heading south before branching east or west.

Schools and Education

AMK has long been one of Singapore’s most sought-after school belts, anchored by several high-demand primary schools within the 1-km priority registration radius of key precincts:

- Ai Tong School: Special Assistance Plan (SAP) primary school; one of the most oversubscribed schools in AMK, drawing buyers to precincts within 1 km of AMK Avenue 6.

- CHIJ Ang Mo Kio Primary: All-girls school under the Singapore Catholic Mission; strong ballot demand in Phase 2B registration.

- Pei Chun Public School: Bilingual SAP school near Marymount MRT.

- Mayflower Primary School: Government school serving AMK’s northern subzones.

- Anderson Serangoon Junior College (ASRJC): Formed in 2020 from the merger of Anderson JC and Serangoon JC; located on Upper Serangoon Road, approximately 2.5 km from AMK MRT.

- Nanyang Junior College (NYJC): On Serangoon Avenue 3, near the AMK–Serangoon border; one of Singapore’s highest-performing JCs by A-Level results.

Amenities: Retail, Recreation and Healthcare

Retail: AMK Hub at the town centre is the neighbourhood’s retail anchor — a six-storey, 580,000 sq ft mall directly connected to AMK MRT. It houses over 200 tenants spanning food, fashion, electronics, and family services. Junction 8 in Bishan (approximately 700 m from the AMK border) provides additional retail depth for residents in southern AMK precincts near Marymount MRT.

Recreation: The 62-hectare Bishan–Ang Mo Kio Park is Singapore’s largest urban park and one of the country’s best examples of biophilic urban design — the Kallang River was naturalised in 2012 to run through the park, creating a rain garden ecosystem. It is a favourite for cycling, jogging, kayaking, and weekend picnics. Thomson Nature Park and the Lower Peirce Reservoir Park add further green buffer to AMK’s northern fringe.

Healthcare: Khoo Teck Puat Hospital (KTPH), a 762-bed acute-care hospital administered by the National Healthcare Group (NHG), is located approximately 700 m from AMK MRT. Two Ang Mo Kio Polyclinics (AMK Ave 10 and AMK Ave 9) serve primary care needs. Residents requiring specialist care can access Tan Tock Seng Hospital (TTSH) in Novena, approximately 20 minutes by NSL.

Investment Analysis — Why Ang Mo Kio Holds Its Value

AMK’s investment case rests on four structural pillars:

- Scarcity of private supply: Unlike Tampines, Bedok, or Woodlands — which have significant private condo pipelines — AMK has no meaningful new private residential launch since The Panorama in 2014. Scarcity supports secondary-market pricing.

- Transport upgrade optionality: The CRL Phase 2 station represents a structural re-rating catalyst. Investors tracking Singapore’s MRT pipeline history will note that the opening of TEL stations in Marine Parade and Marine Terrace (June 2023) triggered a 12–18% uplift in nearby transaction prices within 12 months. An equivalent re-rating in AMK is plausible upon CRL opening.

- School belt premium: Properties within 1 km of Ai Tong School consistently command a 6–10% price premium over equivalent flats in the same precinct but outside the priority radius — a durable premium driven by annual demand from parents in the Phase 2B registration priority window.

- Rental demand: AMK’s employment node (AMK Industrial Park and the Ang Mo Kio Avenue 10 light industrial precinct) sustains a tenant base of technicians, healthcare professionals, and small-business owners who prefer proximity to their workplace. KTPH’s ~4,000 staff represent a structural rental demand pool.

Ang Mo Kio Property Price Summary Table

| Property Type | Est. Price Range (2026) | Typical Size | Gross Yield (est.) | Tenure |

|---|---|---|---|---|

| HDB 3-Room | S$360k – S$500k | 60–69 sqm | ~4.2–4.6% | 99-yr lease (HDB) |

| HDB 4-Room | S$600k – S$850k | 90–105 sqm | ~4.0–4.4% | 99-yr lease (HDB) |

| HDB 5-Room / EA | S$780k – S$1,150k | 110–145 sqm | ~3.6–4.0% | 99-yr lease (HDB) |

| Condo 2BR (D20) | S$1.1M – S$1.65M | 65–90 sqm | ~3.2–3.5% | 99-yr leasehold |

| Condo 3BR (D20) | S$1.5M – S$2.2M | 90–120 sqm | ~2.8–3.2% | 99-yr leasehold |

Table 1: AMK property price summary. Prices are estimated secondary-market ranges for Q1–Q2 2026. Yields are gross estimates based on advertised rental data and HDB/URA transaction records. Not a valuation or financial advice.

Worked Example — Upgrading to AMK: Mr & Mrs Lim

Profile: Mr & Mrs Lim, Singapore Citizens, joint gross income S$10,500/month. Selling their Toa Payoh 4-room HDB flat (Minimum Occupation Period cleared). Moving to a larger 4-room HDB flat in Ang Mo Kio to be closer to parents (qualifying for the Proximity Housing Grant).

- Purchase price: AMK 4-room resale HDB at S$728,000

- Proximity Housing Grant (PHG): S$30,000 (parents/in-laws living within 4 km of proposed purchase, applicable to SC second-timers buying within 30 km of family)

- Buyer’s Stamp Duty (BSD): First S$180k × 1% = S$1,800 + next S$180k × 2% = S$3,600 + remaining S$368k × 3% = S$11,040 → Total BSD: S$16,440

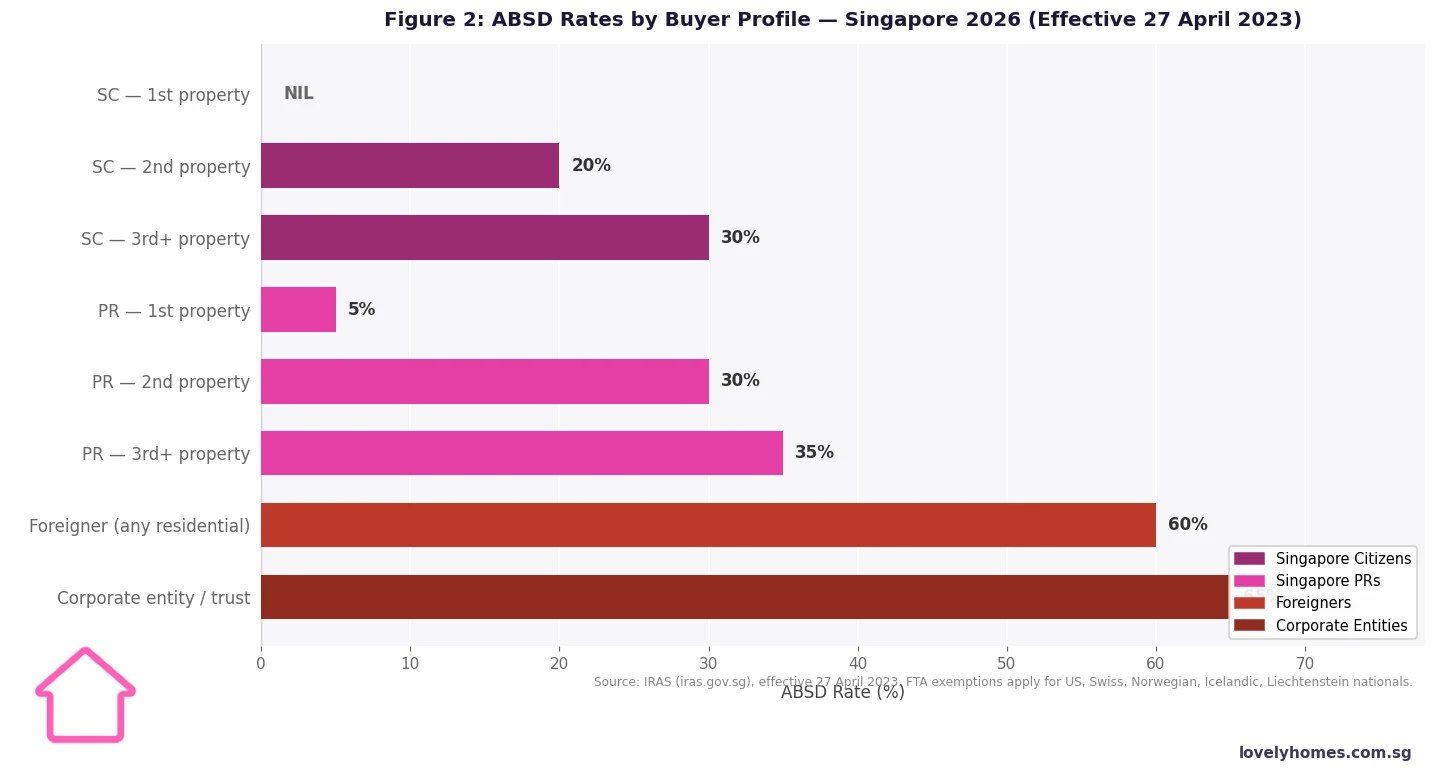

- Additional Buyer’s Stamp Duty (ABSD): Nil — sell-first approach: Toa Payoh flat sold and transferred before exercising AMK OTP. At point of purchase, property count = 0 for SCs. (See our ABSD complete guide for remission options.)

- HDB loan quantum (80% LTV): S$582,400 at 2.6% p.a. (CPF OA rate + 0.1%) over 25 years = approx. S$2,638/month

- Mortgage Servicing Ratio (MSR) check: S$2,638 ÷ S$10,500 = 25.1% — PASS (MSR ceiling 30%, administered by MAS)

- Upfront CPF/cash outlay: 20% downpayment S$145,600 − PHG S$30,000 = S$115,600 from CPF OA + BSD S$16,440 payable from CPF OA + legal/admin ~S$3,250 = approx. S$135,290 total (largely from CPF OA savings; zero min-cash requirement under an HDB loan)

Outcome: The Lims comfortably qualify on MSR. The sell-first approach eliminates ABSD entirely. The PHG grant reduces their effective CPF draw by S$30,000 at the point of downpayment. On a joint income of S$10,500/month, the monthly repayment of S$2,638 (25.1% MSR) leaves meaningful household cash flow for living expenses and savings. For CPF withdrawal limit rules, see our CPF property withdrawal limits guide.

Why Ang Mo Kio Matters — and What Comes Next

AMK occupies a strategic position in Singapore’s property hierarchy: it offers the school-belt credentials of Bishan and Toa Payoh at a modest discount, the healthcare infrastructure of a regional hub, and the CRL optionality of a town that investors have not yet fully priced in. For owner-occupiers — particularly HDB upgraders with school-age children — AMK’s combination of established amenities, transport access, and community facilities makes it one of the more defensible choices in Singapore’s non-CCR market.

Looking ahead to 2026–2030, three catalysts could reshape AMK’s property landscape: (1) the finalisation of CRL Phase 2 station details and tender award, which would crystallise the re-rating thesis; (2) the wave of maturing Plus-class BTO units from the June 2026 exercise becoming resaleable after 2036 — reshaping the supply composition of AMK’s resale market; and (3) possible Urban Redevelopment Authority master plan revisions under the forthcoming Long-Term Plan Review, which could unlock higher plot ratios in AMK’s town centre precinct.

None of these are certainties. Buyers should weigh AMK’s established fundamentals against the fact that the town has fewer “upside surprises” than less-developed areas such as Tengah or Bayshore — the infrastructure is largely in place, which means less speculative upside but also lower execution risk.

Frequently Asked Questions — Ang Mo Kio Property 2026

Is Ang Mo Kio a good place to buy property in 2026?

AMK is well-regarded for its school belt (Ai Tong, CHIJ AMK, Nanyang JC), mature HDB infrastructure, and proximity to Khoo Teck Puat Hospital. It is competitively priced relative to Bishan and Toa Payoh yet significantly cheaper than CCR neighbourhoods such as Orchard or Newton. The upcoming CRL Phase 2 station adds long-term transport upside. For buyers prioritising liveability, school proximity, and healthcare access, AMK scores highly. However, private condo supply is very limited, restricting choice for buyers who require private residential options.

Which MRT lines serve Ang Mo Kio?

AMK is served by three stations on the North–South Line (NSL): Ang Mo Kio (NS16), Yio Chu Kang (NS15), and Marymount (NS18). There is no current East–West or Downtown Line access within the planning area. The Cross Island Line (CRL) Phase 2 is expected to add at least one station in the AMK corridor, improving east–west connectivity, but construction is not expected to complete until approximately 2030.

Can a Singapore Permanent Resident (PR) or foreigner buy property in AMK?

HDB resale flats in AMK — like all HDB flats — are available to eligible Singapore PRs (subject to HDB’s ethnic integration policy, income ceilings, and the PR scheme eligibility rules under the Public Scheme or Fiancé/Fiancée Scheme). PRs buying an HDB flat must occupy it as their principal residence and are subject to a 5-year resale levy deferral rule under certain conditions. Foreigners (non-PR, non-SC) cannot purchase HDB flats at all, but may purchase private condominiums in AMK subject to the Additional Buyer’s Stamp Duty (ABSD) of 60% as of April 2023. See our ABSD guide for the full rate table.

What are the best condominiums in Ang Mo Kio?

AMK has very limited private condominium supply. The most prominent completed development is The Panorama (698 units, 99-year leasehold, TOP 2018, AMK Avenue 2), which is the dominant price benchmark for 2- and 3-bedroom private units in the planning area. Grandeur 8 (99yr, earlier vintage) and Thomson Three (on the AMK–Thomson border) are secondary benchmarks. Given the scarcity of supply, buyers considering AMK condominiums should also compare nearby Bishan options — such as Sky Vista — which offer similar school-belt access with slightly different MRT coverage.

How does AMK compare to Bishan or Toa Payoh for property investment?

All three are mature NSL towns with strong school belts and established amenities. AMK typically offers slightly lower pricing than Bishan (which benefits from the Junction 8/Bishan MRT dual interchange) and is broadly comparable to Toa Payoh. Bishan commands a premium due to its CCR-adjacent positioning and the Thomson–East Coast Line (TEL) overlay at Caldecott (one stop from Bishan). Toa Payoh has a tighter new HDB supply pipeline but older flat leases. AMK’s differentiator is its forthcoming CRL re-rating potential and the Ai Tong/CHIJ school belt. For most buyers, the choice hinges on specific school requirements and whether proximity to Junction 8 or AMK Hub better suits daily life.

What is the impact of the June 2026 BTO Plus-class projects on AMK’s resale market?

Plus-class BTO flats are subject to a 10-year Minimum Occupation Period (double the standard 5 years), an income ceiling of S$14,000/month for buyers on the resale market, and a subsidy clawback upon resale that reduces the seller’s net proceeds. These restrictions mean that Plus flats will transact at a discount to Standard resale flats in the same town once they become eligible for resale — effectively creating a two-tier resale market within AMK by the mid-2030s. Buyers of existing Standard-class AMK resale flats are unlikely to be directly affected; if anything, restricted supply of Plus flats on the resale market may support pricing on the unrestricted Standard inventory.

What grants are available when buying an AMK HDB resale flat?

Eligible Singapore Citizen buyers purchasing HDB resale flats in AMK can access the Enhanced Housing Grant (EHG) of up to S$120,000 (families) or S$60,000 (singles), subject to income ceilings and a first-timer eligibility requirement. The Proximity Housing Grant (PHG) provides up to S$30,000 for families (S$15,000 for singles) who buy within 4 km of parents or children. The Step-Up CPF Housing Grant of S$15,000 is available to eligible second-timer families purchasing 2- or 3-room resale flats. See our CPF Housing Grant guide for full eligibility conditions and stacking rules.

Related Articles

- First-Time Property Buyer Guide Singapore 2026

- ABSD Singapore 2026 — Complete Guide to Additional Buyer’s Stamp Duty

- CPF Housing Grant Resale Singapore 2026 — EHG, PHG and Step-Up Explained

- HDB Loan vs Bank Loan Singapore 2026 — Complete Comparison Guide

- CPF Property Withdrawal Limits Singapore 2026

- Singapore Stamp Duty Complete Guide 2026 — BSD, ABSD, SSD and ACD

- Singapore Property Buying Checklist 2026 — 12 Steps from IPA to Key Collection

Disclaimer

This article is produced by LovelyHomes for general informational and educational purposes only. Property prices, rental yields, grant amounts, and stamp duty rates are subject to change; figures cited reflect publicly available data as of Q1–Q2 2026 and are estimates only. This article does not constitute financial, legal, or property valuation advice. Readers should verify current rates and eligibility conditions directly with the relevant authorities: Housing & Development Board (HDB) at hdb.gov.sg, Urban Redevelopment Authority (URA) at ura.gov.sg, Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg, and Central Provident Fund Board (CPF) at cpf.gov.sg. Engage a licensed property agent and, where appropriate, a lawyer and financial adviser before making any property decision.

Click anywhere or press Esc to close