Singapore HDB Room Rental Guide 2026: Complete Guide to Renting Out Your HDB Room

Quick Answer: HDB Room Rental Singapore 2026

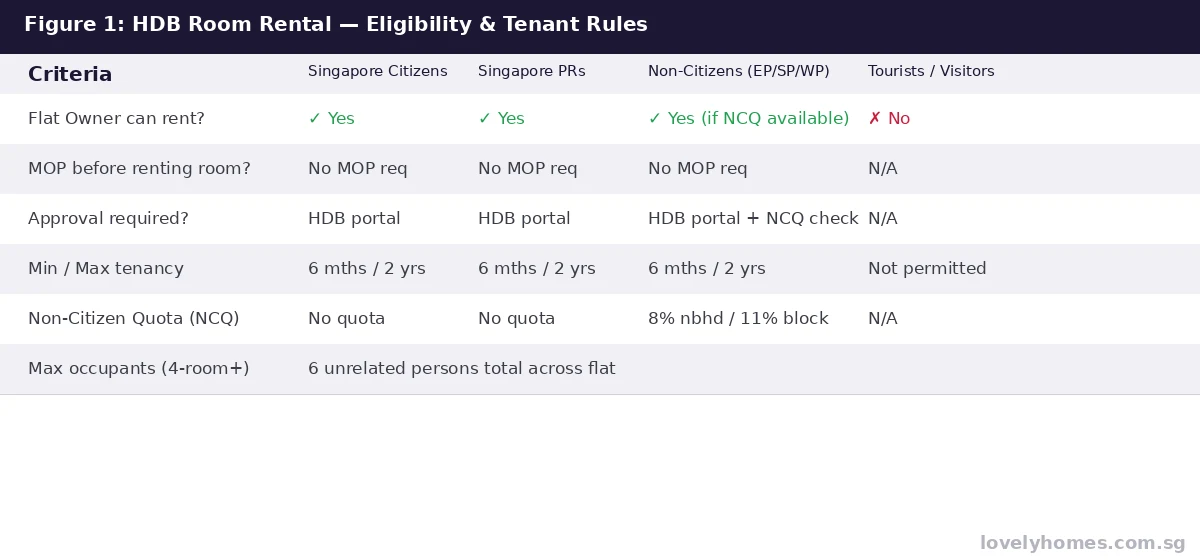

- No MOP required — you can rent out a room in your HDB flat immediately after taking possession; the Minimum Occupation Period applies only to whole-flat subletting.

- HDB portal approval is required before any tenancy starts, including room rentals to non-citizens.

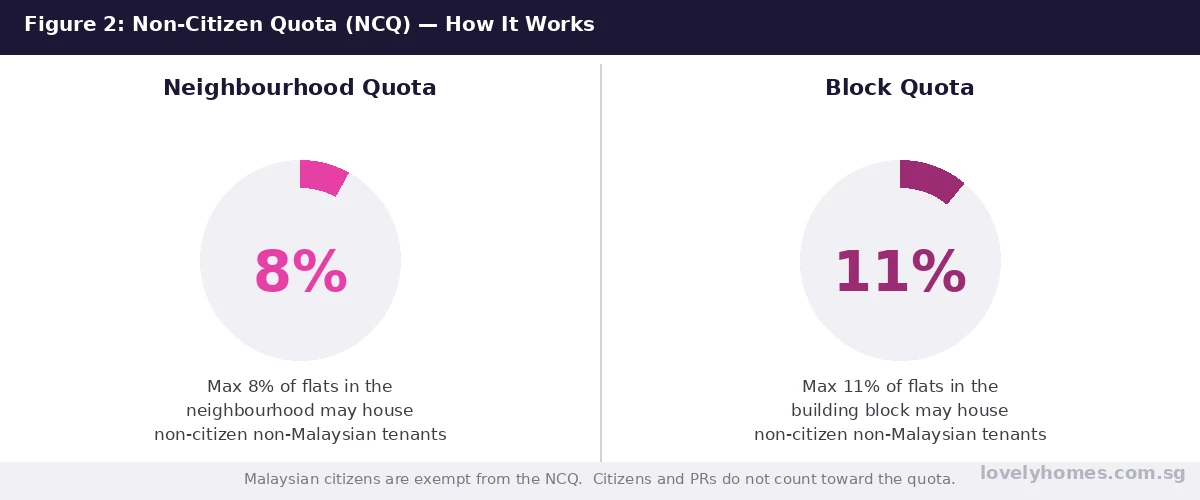

- Non-Citizen Quota (NCQ): only 8% of flats in a neighbourhood and 11% in any block may house non-citizen, non-Malaysian tenants at any one time.

- Malaysian citizens are NCQ-exempt — they may rent from any eligible HDB flat owner regardless of the quota.

- Minimum tenancy is 6 months; maximum is 2 years per tenancy agreement (renewable).

- Maximum occupancy for a 4-room or larger flat is 6 unrelated persons across all rooms.

- All rental income is taxable under the Income Tax Act 1947; deductible expenses include mortgage interest, property tax, and maintenance fees.

- IRAS filing deadline is 15 April each year for the preceding year’s rental income.

What Is HDB Room Rental and Who Administers It?

Renting out a room in your Housing Development Board (HDB) flat is one of the most tax-efficient ways to generate supplementary income in Singapore. Unlike renting out the entire flat — which requires the flat to have cleared its Minimum Occupation Period (MOP) — room rental has no MOP prerequisite. You can begin renting a spare bedroom the day after you collect your keys, provided you register the tenancy through the HDB e-Service portal and comply with the occupancy and quota rules administered by HDB.

HDB oversees room rental under the Housing and Development Act 1959 (Cap 129) and associated policies. The Inland Revenue Authority of Singapore (IRAS) governs the tax treatment of rental income under the Income Tax Act 1947. Both agencies updated their guidelines in 2024–2025; this guide reflects the rules as at June 2026.

Room rental is distinct from whole-flat subletting, which requires MOP clearance and a distinct approval process. For subletting of the entire flat, refer to our HDB Subletting Guide 2026.

HDB Room Rental Eligibility Rules

To rent out a room in your HDB flat, you must be a registered owner who satisfies all of the following conditions:

- Flat ownership: You must be a registered owner of the flat (joint or sole). Tenants of HDB flats cannot sublet rooms.

- Residency: At least one owner must continue to reside in the flat during the rental period. You cannot rent out all bedrooms and vacate — that constitutes whole-flat subletting and requires separate approval.

- No MOP restriction for room rental: Unlike whole-flat subletting, there is no MOP period to serve before renting a room. This applies to BTO, resale, and DBSS flats.

- Citizen/PR ownership: Only Singapore Citizens and Singapore Permanent Residents may own HDB flats.

Who Can Be Your Tenant?

Eligible tenants include Singapore Citizens, Singapore Permanent Residents, and non-citizens holding long-term passes such as Employment Passes (EP), S Passes, Work Permits (WP), Long-Term Visit Passes (LTVP), Student Passes, and Dependent’s Passes. Short-term visitors and tourists are not eligible. Non-citizens are subject to the Non-Citizen Quota (NCQ) — with the important exception that Malaysian citizens are NCQ-exempt.

Before commencing any tenancy with a non-citizen tenant, verify that NCQ slots are available for your block and neighbourhood, then register the tenancy on the HDB e-Service portal. Tenancies with Citizens and PRs do not require quota checks but must still be registered.

The Non-Citizen Quota (NCQ): How It Works

The Non-Citizen Quota was introduced by HDB to maintain social integration in public housing estates and prevent over-concentration of foreign nationals in any single block or neighbourhood. Under the NCQ:

- No more than 8% of all HDB flats in a neighbourhood may be occupied by non-citizen, non-Malaysian tenants at the same time.

- No more than 11% of all HDB flats in any single block may be occupied by non-citizen, non-Malaysian tenants at the same time.

If either limit is reached, no new tenancy with a non-citizen, non-Malaysian tenant may commence in that neighbourhood or block until an existing occupancy clears. Malaysian citizens are entirely exempt from the NCQ. You can check real-time NCQ availability using the HDB NCQ portal.

Tenancy Duration and Registration

Each room rental tenancy must have a minimum duration of 6 months and a maximum of 2 years per agreement. Tenancies of less than 6 months — including Airbnb-style arrangements — are strictly prohibited and may result in compounding or flat confiscation. Registration is completed online via the HDB e-Service portal within 7 days of the tenancy start date.

Maximum Occupancy Limits

| Flat Type | Max. Occupants (All Rooms Combined) | Notes |

|---|---|---|

| 1-Room / 2-Room | 4 unrelated persons | Including the flat owner(s) |

| 3-Room | 6 unrelated persons | Including the flat owner(s) |

| 4-Room and above | 6 unrelated persons | Including the flat owner(s) |

| Executive / DBSS | 6 unrelated persons | Including the flat owner(s) |

| Studio Apartment | Not eligible for room rental | Intended for elderly residents only |

The occupancy cap includes the flat owner(s) and all residents. A 4-room flat with two owner-occupiers can therefore accommodate at most 4 additional persons as tenants across all rooms.

Rental Income Tax: What You Must Declare to IRAS

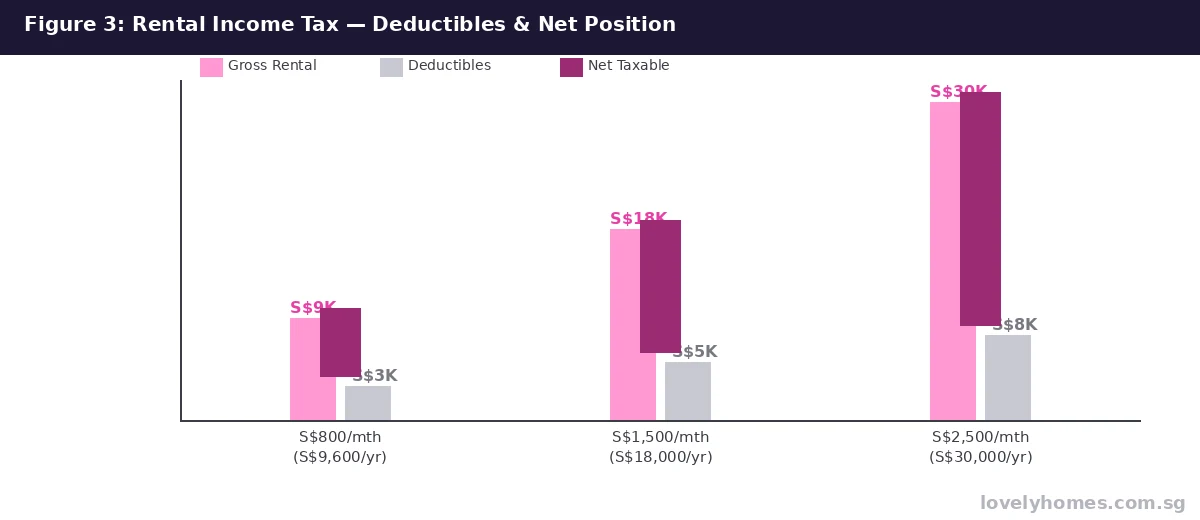

All rental income from HDB room rental is assessable income under the Income Tax Act 1947 administered by IRAS. There are no exemptions for small amounts or casual arrangements. IRAS allows a range of deductible expenses that significantly reduce your net taxable rental income.

What Is Taxable?

Your gross rental income includes all amounts received from tenants: monthly rent, any lump-sum advance payment, and reimbursements for utilities or services. Security deposits are not income when received but become income if forfeited.

Allowable Deductions

| Deductible Expense | Basis | Notes |

|---|---|---|

| Mortgage interest | Actual interest portion of HDB or bank loan payments | Principal repayment is NOT deductible |

| Property tax | Annual property tax paid to IRAS | Deductible in full as a cost of letting |

| Maintenance and conservancy charges | Monthly S&CC paid to Town Council | Pro-rated to rental period if flat was partly vacant |

| Repairs and maintenance | Revenue repairs to restore lettable condition | Capital improvements are NOT deductible |

| Insurance premiums | Fire/content insurance attributable to the rental | Home Protection Scheme premiums are NOT deductible |

| Agent commission | Fees to a licensed estate agent for securing the tenancy | Deductible in full in the year paid |

The net rental income is added to your other income and taxed at Singapore’s progressive personal income tax rates (0% on the first S$20,000 of chargeable income, up to 24% above S$1,000,000 effective from YA 2024).

When and How to File

Rental income must be declared annually in your income tax return via IRAS’s myTax Portal. The filing deadline is 15 April of the following year. Retain receipts and tenancy agreements for at least 5 years as IRAS may audit rental declarations.

Worked Example: The Tan Family, Tampines 4-Room

Mr and Mrs Tan are Singapore Citizens who own a 4-room HDB flat in Tampines. They have one spare room and decide to rent it to a Malaysian work-pass holder at S$1,500 per month from 1 April 2026.

Step 1 — Eligibility: No MOP required. NCQ check: Malaysian citizens are NCQ-exempt. HDB portal registration completed 29 March 2026.

Income calculation (Year of Assessment 2027, calendar year 2026):

- Gross rental income: S$1,500 x 9 months (Apr–Dec 2026) = S$13,500

- Mortgage interest (annual S$8,400, pro-rated 9/12): S$6,300

- Property tax (annual S$720, pro-rated 9/12): S$540

- Maintenance fees (S&CC S$56 x 9 months): S$504

- Total allowable deductions: S$7,344

- Net taxable rental income: S$13,500 minus S$7,344 = S$6,156

Tax impact: Mr Tan earns S$72,000/yr. Adding S$6,156 raises chargeable income to approximately S$78,156. Marginal rate: 7% (S$40K–S$80K band). Incremental tax: approximately S$431. Net monthly cash after all costs and taxes: approximately S$1,014/month.

Why HDB Room Rental Matters for Flat Owners

Singapore has one of the highest rates of homeownership in the world — roughly 90% of residents live in public housing. Room rental offers a way to monetise a spare bedroom without the complexity of selling or refinancing. Industry figures show median room rents ranging from S$900/month in non-mature estates to S$2,200/month in central areas as at early 2026. With Singapore’s economy drawing a continued influx of international professionals, demand for affordable HDB rooms is expected to remain resilient.

For retirees, room rental income can supplement CPF LIFE payouts and reduce dependence on drawing down CPF savings. The Silver Housing Bonus (SHB) scheme, administered by HDB, provides additional cash bonuses of up to S$30,000 for elderly flat owners who right-size to smaller flats.

What Might Come Next: Future Policy Considerations

This section is editorial speculation and does not constitute confirmed government policy.

Short-term rental platforms such as Airbnb remain prohibited in HDB flats, and HDB is expected to continue enforcing this restriction. IRAS is rolling out auto-assessment for rental income by 2027, cross-checking declared rental income against HDB portal tenancy registrations. Flat owners who have not been filing rental income should consider voluntary disclosure via IRAS’s myTax Portal before automated enforcement begins. The NCQ thresholds of 8% and 11% have remained unchanged since 2012 and selective adjustments in newer estates with lower foreign-national density remain a possibility, though no change has been signalled as at June 2026.

Frequently Asked Questions

Can I rent out my HDB room before completing the Minimum Occupation Period?

Yes. The MOP restriction applies only to renting out the entire flat (whole-flat subletting), not to individual rooms. Room rental may commence immediately after the flat is handed over to you, subject to HDB portal registration and compliance with tenant eligibility and NCQ rules. If you are in the MOP period, you must continue to reside in the flat.

My block’s Non-Citizen Quota is full. Can I still rent to my Malaysian colleague?

Yes. Malaysian citizens are entirely exempt from the Non-Citizen Quota. The NCQ applies only to non-citizens who are not Malaysian. Your Malaysian colleague does not count toward the 8% neighbourhood or 11% block quota regardless of the pass type they hold. You can proceed with registration on the HDB portal without a quota check for Malaysian tenants.

Does HDB rental income affect my CPF contributions?

No. Rental income from HDB room rental is not employment income and is not subject to CPF contributions. It is, however, assessable income under the Income Tax Act and must be declared to IRAS. CPF voluntary top-up contributions remain available regardless of whether you earn rental income.

What happens if I rent out my room without registering on the HDB portal?

Renting out a room without HDB portal registration is a breach of the HDB lease. Consequences include a formal warning and compounding fine of up to S$5,000 per breach. Repeated or serious violations can result in HDB compulsorily acquiring the flat at HDB’s assessed valuation, which may be below open-market value. HDB conducts enforcement raids and acts on complaints from neighbours and town councils.

Can I deduct renovation costs or furniture purchases against rental income?

Generally, no. IRAS distinguishes between capital expenditure (acquiring or improving an asset) and revenue expenditure (maintaining the asset in its existing condition). Only revenue repairs are deductible. Furniture purchases are capital in nature and are not deductible. For specific situations, seek advice from a qualified tax practitioner or consult IRAS’s e-Tax Guide on rental income at iras.gov.sg.

How do I calculate the deductible mortgage interest for a joint HDB loan?

For an HDB concessionary loan, your annual statement from HDB shows the principal and interest breakdown for each repayment. Add up the interest components paid during the calendar year — this is your deductible amount. For a bank loan, your bank provides an annual loan statement. If you jointly own the flat, each co-owner may only deduct interest in proportion to their ownership share.

Can I rent a room to a family member who is a foreigner?

Yes, provided the family member holds an eligible pass (EP, S Pass, WP, LTVP, DP, Student Pass) and the NCQ is not exhausted for your block and neighbourhood (unless the family member is Malaysian). You still need to register the tenancy on the HDB portal. Close family ties do not create any exemption from HDB’s room rental registration requirements, though there is no restriction on the commercial terms of the tenancy.

Related Articles

- Singapore HDB Subletting Guide 2026: Whole-Flat Rental, NCQ and Approval Process

- Singapore HDB Resale Levy Guide 2026: What Second-Timer Flat Buyers Pay

- Singapore CPF Accrued Interest for Property 2026

- HDB Loan vs Bank Loan Singapore 2026: Which Saves You More?

- Singapore Annual Property Tax Guide 2026: AV, IRAS Rates and 2026 Rebate

- Singapore HDB Resale Flat Prices 2026: Trends, COV and Valuations

- Singapore CPF Housing Grant Guide 2026: EHG, PHG, Family Grant

Disclaimer

This article is produced by the LovelyHomes Editorial Team for general information purposes only. It is not legal, tax, or financial advice. HDB rules and IRAS tax regulations are updated periodically; always verify current requirements on hdb.gov.sg and iras.gov.sg before entering into any tenancy agreement. For personalised tax advice, consult a qualified tax practitioner.