MOP first: You must fulfil the Minimum Occupation Period (5 years for most flats; 10 years for Prime and Plus flats launched from August 2024) before selling your HDB flat on the open market or buying a private residential property while retaining the flat.

Two upgrade strategies: “Sell first, buy later” avoids ABSD on your private purchase (you are a first-time private buyer). “Buy first, sell later” triggers 20% ABSD on the private property for SCs — S$270,000 on a S$1.35M condo — though an ABSD remission is available if you sell within 6 months.

CPF refund: When you sell your HDB flat, all CPF OA monies used for the purchase — plus accrued interest — must be refunded to your CPF account. The net cash you receive is the sale price minus the outstanding HDB loan (if any) and the CPF refund.

Grant repayment: CPF Housing Grants (EHG, Family Grant, etc.) used for the HDB flat do not need to be repaid upon sale — they are subsumed into the CPF OA refund.

HDB loan discharged on sale: The HDB loan is discharged at the point of the flat sale. Any outstanding balance is deducted from the sale proceeds before cash is released.

Private property financing: After selling your HDB flat, you are eligible for a bank loan of up to 75% LTV for a private property purchase. You cannot use an HDB concessionary loan for private property.

ABSD remission (SC married couples): If you buy a private property before selling your HDB flat, you can claim an ABSD refund if the HDB flat is sold within 6 months of completing the private purchase.

Who is an HDB Upgrader?

In Singapore’s property lexicon, an HDB upgrader is a flat owner — typically a Singapore Citizen couple who purchased a Housing & Development Board flat as their first home — who subsequently wishes to sell the flat and purchase a private residential property. The upgrade journey is one of the most significant financial decisions many Singaporeans make: it unlocks accumulated HDB equity, introduces bank mortgage financing (with its stricter credit requirements), and subjects the buyer to ABSD unless the timing is managed carefully.

The upgrader market is a structural pillar of Singapore’s private residential demand. According to the Urban Redevelopment Authority (URA), HDB upgraders historically account for 30–40% of new private condominium sales in Outside Central Region (OCR) developments. Policy levers — chiefly ABSD and MOP duration — are calibrated in part to pace the rate at which HDB flat owners enter the private market.

Understanding the mechanics of the upgrade journey — from MOP completion to key collection — is essential to avoid costly timing errors, particularly the S$270,000+ ABSD cash outlay that catches many upgraders off guard.

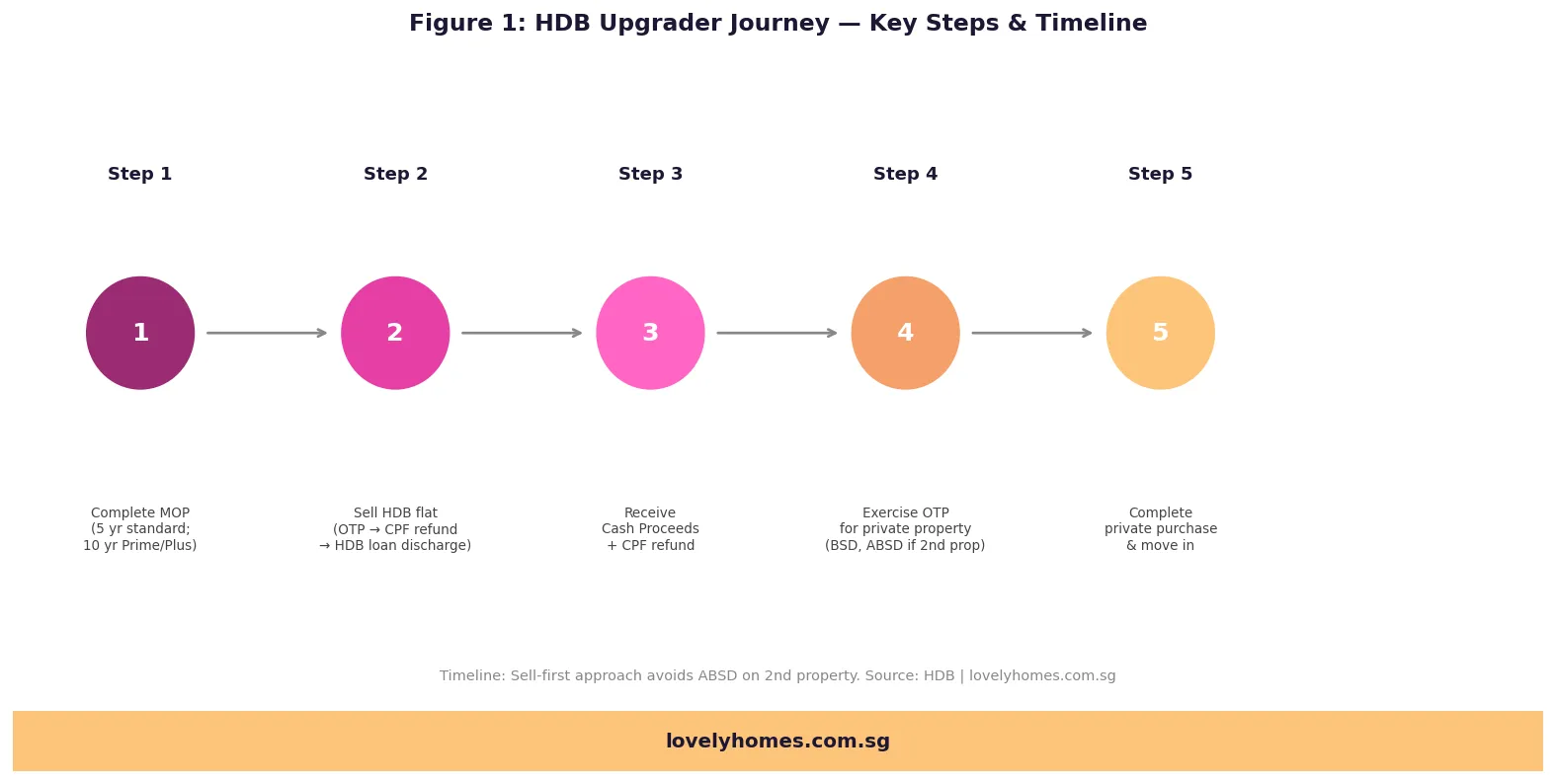

Step 1: Confirm Your MOP Status

The Minimum Occupation Period (MOP) is the period during which an HDB flat owner must occupy the flat as their principal residence before they are permitted to sell it on the open market or to purchase a private residential property.

The standard MOP is 5 years from the date the keys are collected (the date of possession), not from the date the sale was exercised or the mortgage was drawn. The MOP clock stops if the flat is rented out in full, if the flat owner stays overseas for extended periods, or in other prescribed circumstances — so owners who sublet their flat prematurely may find their effective MOP extended.

For Prime and Plus classification flats launched from August 2024 onwards under the new HDB classification framework, the MOP is 10 years, and additional ownership restrictions apply (including an income ceiling on resale buyers and a clawback provision on subsidy). Owners of these flats face a longer upgrader journey.

Figure 1: The HDB upgrader’s journey — five key steps from MOP completion to private property key collection. Source: HDB | lovelyhomes.com.sg

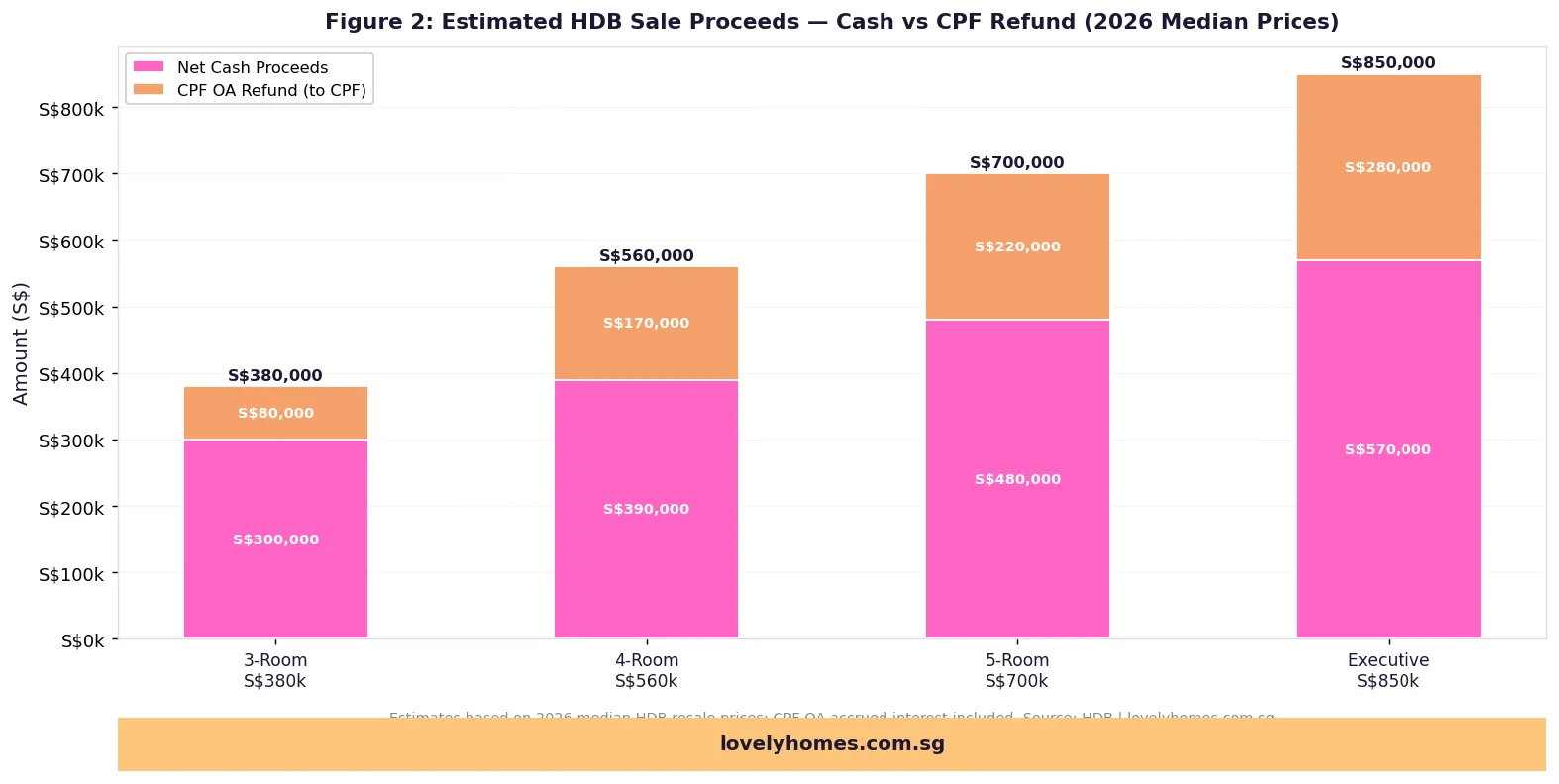

Step 2: Understand What You Will Receive from the HDB Sale

The sale of your HDB flat generates two streams of value: a cash component and a CPF refund. The distinction matters enormously for financial planning, because the CPF refund goes back into your CPF Ordinary Account — it cannot be used freely as cash, though it can be used for the down payment and stamp duty on your subsequent private property purchase.

The CPF OA refund comprises: (a) the principal CPF OA amount withdrawn for the flat, and (b) accrued interest — the notional interest CPF Board charges on those withdrawn funds at the CPF OA rate (currently 2.5% p.a. on the first S$20,000 of OA, 3.5% p.a. thereafter, effective 1 January 2024). Accrued interest compounds over the full holding period and can be significant: on S$150,000 CPF withdrawn over 8 years, accrued interest at 2.5% compounding amounts to approximately S$34,000.

Figure 2: Estimated HDB sale proceeds by flat type — cash component vs CPF OA refund, based on 2026 median resale prices. Source: HDB | lovelyhomes.com.sg

If there is an outstanding HDB concessionary loan, the remaining balance is deducted from sale proceeds before cash is released to the seller. HDB loan interest rate is currently set at the CPF OA rate + 0.1% (i.e. approximately 2.6% p.a.), making it among the most competitive mortgage rates in Singapore — but flat owners who have used HDB loans extensively may find less net cash available after discharge.

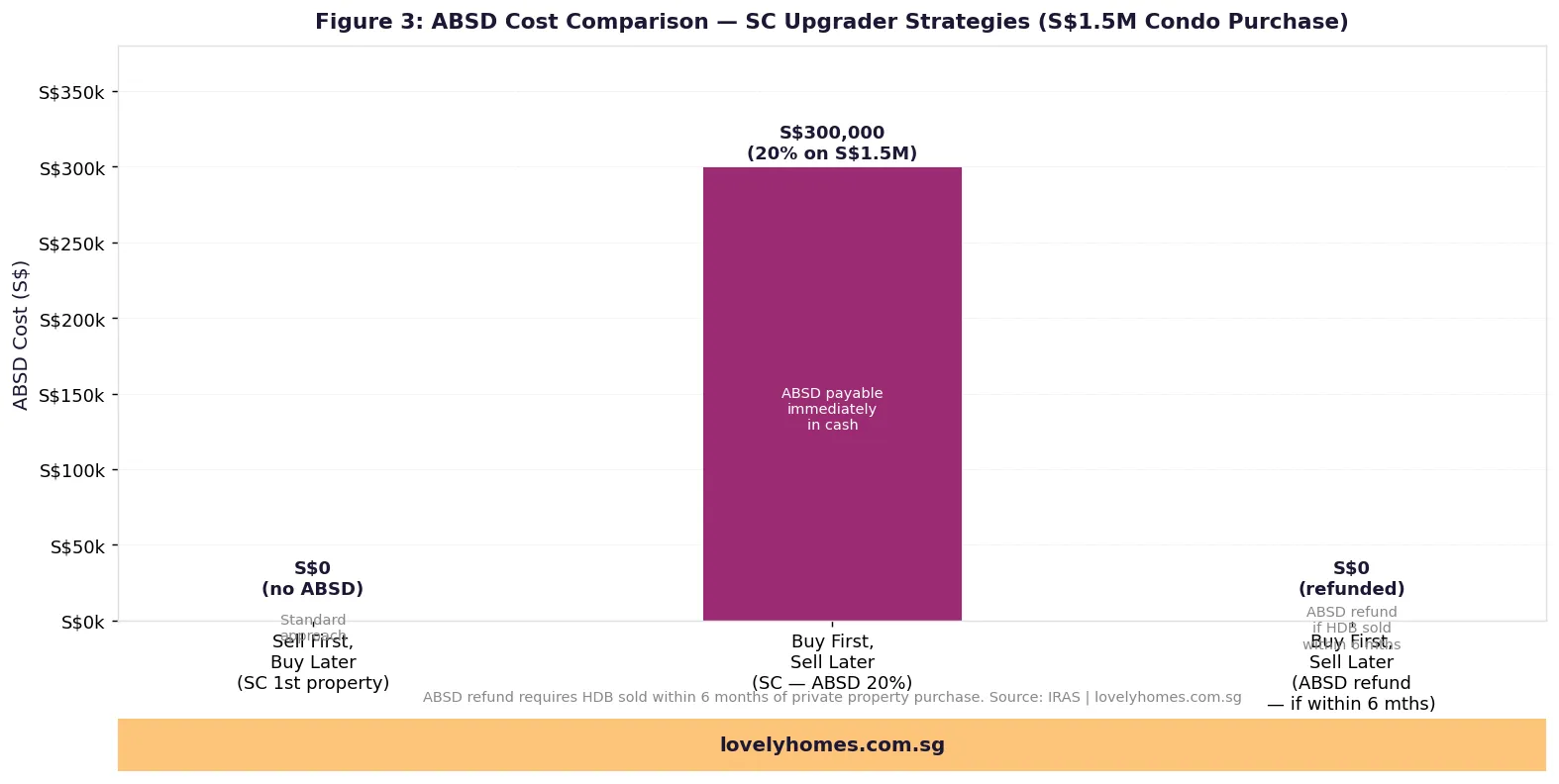

Step 3: Decide on Your Upgrade Strategy — Sell First or Buy First?

The single most consequential decision in the upgrade journey is the sequencing of transactions: do you sell your HDB flat before purchasing the private property, or do you purchase first and sell after?

The sell-first strategy means you complete the sale of your HDB flat, receive the sale proceeds (cash + CPF refund), arrange interim accommodation (typically renting), and then purchase the private property as a first-time private-property buyer. The key advantage: you pay 0% ABSD on the private purchase (for SC buyers with no other property). The key risk: you may miss your preferred private property while searching for one during the rental period, and the private property market may move against you in the interim.

The buy-first strategy means you exercise an OTP on a private property while still owning the HDB flat, paying 20% ABSD on the private purchase price in cash. You then have 6 months from the date of completing the private property purchase (Legal Completion) to sell the HDB flat and apply for an ABSD remission refund from IRAS. If the HDB flat is sold within 6 months, IRAS refunds the ABSD paid (less a processing deduction of 0.1% p.p. on the refunded amount, effective from certain periods). If you miss the 6-month window, the ABSD is forfeited — a potentially catastrophic financial loss.

Figure 3: ABSD cost comparison — “sell first” avoids ABSD entirely; “buy first” triggers 20% ABSD but may be remitted if HDB flat sold within 6 months. Source: IRAS | lovelyhomes.com.sg

Summary Table: Key Upgrader Decision Points

Decision Point

Sell First, Buy Later

Buy First, Sell Later (+ ABSD remission)

ABSD upfront

S$0 (first-time private buyer)

20% on purchase price (e.g. S$270,000 on S$1.35M) — cash only

ABSD recovery

N/A — not paid

Refundable if HDB sold within 6 months of private completion

CPF available

Full CPF refund from HDB sale usable for private downpayment

CPF still tied up in HDB until flat sold

Accommodation

Must rent during search period

Can stay in HDB until private is ready

Market risk

Private prices may rise during rental period

Locks in private price; HDB sale price uncertainty

Bridge financing

Not required

May need bridging loan if cash-flow is tight

MOP Standard flat

5 years from possession

5 years from possession

MOP Prime/Plus flat

10 years from possession

10 years from possession

Worked Example: The Tan Family Upgrade

Profile: Mr Tan (SC, 42) and Mrs Tan (SC, 40) own a 4-room HDB flat in Bishan, purchased in 2016 for S$470,000 using an HDB concessionary loan of S$376,000. MOP completed May 2021. Current market value: S$620,000. Outstanding HDB loan: S$92,000 (after 10 years of repayments). Total CPF OA withdrawn (both): S$185,000. Accrued CPF interest: S$42,000. Combined gross income: S$13,000/month.

HDB Sale proceeds:

Sale price: S$620,000

Less HDB loan discharge: S$92,000

Less CPF refund (principal + accrued interest): S$227,000

Net cash proceeds: S$301,000

CPF OA balance after refund: S$227,000 (reusable for private purchase)

Target private property: 3-bedroom resale condominium in Bishan (D20), S$1,380,000.

25% down payment = S$345,000 (5% cash min = S$69,000; remaining S$276,000 from CPF OA)

Available CPF OA after BSD: S$227,000 − S$39,800 = S$187,200 → cash shortfall of S$276,000 − S$187,200 = S$88,800 (to be covered by net cash proceeds S$301,000)

Bank loan: 75% × S$1,380,000 = S$1,035,000 at 3.5% over 25 years → monthly S$5,183

The Tans must fund S$276,000 ABSD + S$345,000 down payment + S$39,800 BSD simultaneously — total cash need: S$660,800 at exercise. If their HDB sale is completed within 6 months of private legal completion, IRAS refunds S$276,000 ABSD (less 0.1% = S$275,724 net refund).

Risk: HDB not sold within 6 months → S$276,000 lost.

Verdict: For the Tan family, sell-first is clearly superior — the net cash from HDB sale is sufficient to fund the private purchase without triggering ABSD, and TDSR is comfortably met. Buy-first requires bridge financing of ~S$660,000 simultaneously, which is feasible but expensive and risky if HDB sale stalls.

Why This Matters: Common Upgrader Mistakes

The three most expensive upgrader mistakes in Singapore each carry a six-figure price tag. First, miscounting the MOP: flat owners who sublet their entire flat for periods during the MOP — even with HDB approval — pause the MOP clock, sometimes discovering that their expected MOP date is later than they assumed. A single year’s delay translates into a year’s additional rent if the family has already moved out.

Second, assuming ABSD remission is automatic: the IRAS remission must be actively applied for, with evidence of the HDB sale completion. Families who miss the 6-month window — even by days — forfeit the remission entirely. Delays in HDB sale registration at the HDB Hub can erode the 6-month window; upgraders should build in a buffer and not list the HDB flat for sale at the last possible moment.

Third, ignoring CPF accrued interest: many upgraders are surprised to find that their CPF OA balance after the flat sale is materially lower than expected, because accrued interest — compounding for 5–10 years — has grown the CPF refund obligation substantially. This reduces the CPF available for the private property down payment and may require a larger cash component.

What Might Come Next: Policy Outlook for Upgraders

The Singapore government has shown a willingness to adjust ABSD policy in response to market conditions. The August 2024 introduction of the Prime and Plus HDB flat classification — with its 10-year MOP — signals an intent to slow the entry of Prime/Plus flat owners into the private market, preserving HDB estates as long-term communities rather than transient stepping-stones.

The ABSD remission for SC married couples remains in place as at July 2026. There is periodic market commentary that the 6-month window may be reduced if private prices accelerate — buyers should not rely on the remission window remaining unchanged. IRAS reviews the scheme in conjunction with broader cooling measure calibration.

On financing, MAS guidelines on TDSR and LTV have been stable since 2023. Any future tightening — such as a reduction in the 75% LTV cap for bank loans on private residential property — would increase the cash required for the down payment and could reduce upgrader demand at higher price points.

Frequently Asked Questions

1. Can I buy a private property while still in my HDB flat’s MOP?

No. HDB rules prohibit flat owners from owning or purchasing a private residential property in Singapore during the MOP. You must wait until the MOP is fully served before exercising an OTP on a private property. If you purchase a private property during the MOP, HDB may compulsorily acquire your flat. The prohibition covers direct ownership — owning shares in a company that owns private property is a separate issue and subject to its own rules.

2. Do I have to sell my HDB flat when I buy a private property?

No — you are not legally required to sell your HDB flat when you purchase a private property after MOP completion, provided you pay the applicable ABSD (20% for SC buying a 2nd residential property). Many upgraders choose to retain the HDB flat as a rental asset. However, renting out an HDB flat requires HDB approval, and both flat owners must be at least 35 years old (for non-family schemes). Also note: retaining both properties means the HDB flat rental income may affect TDSR calculations for the private property mortgage.

3. How long does an HDB resale typically take to complete?

An HDB resale transaction typically takes 8–12 weeks from the date an Option to Purchase (OTP) is granted to the HDB Hub’s completion and key handover. The process involves the HDB resale portal submission within 7 days of exercising the OTP, a First Appointment (HDB confirms eligibility), and a Second Appointment (key handover). Delays can occur if there are CPF accrued interest calculations to resolve, outstanding town council arrears, or if HDB flat type or scheme eligibility checks surface issues.

4. What is a bridging loan and when do upgraders need one?

A bridging loan is a short-term loan from a bank that covers the period between purchasing the new private property and receiving the proceeds from the HDB flat sale. Upgraders who adopt the buy-first strategy often need a bridging loan to fund the initial private property down payment (or ABSD, if applicable) before their HDB sale proceeds are available. Bridging loans in Singapore typically carry interest rates of 5–7% per annum and are repaid in full when the HDB sale is completed. They are a useful tool but add cost — every month the bridge is outstanding costs approximately S$400–S$500 per S$100,000 borrowed.

5. Can I use CPF OA from my HDB sale refund to pay the ABSD on my new private property?

No. ABSD must be paid entirely in cash — it cannot be funded from CPF OA. This is one of the most important cash-flow constraints in the upgrade journey. At S$270,000 ABSD on a S$1.35M private property, an upgrader using the buy-first strategy must have S$270,000 in cash available at the point of OTP exercise, in addition to the cash portion of the 25% down payment. CPF OA (including the refund from the HDB sale) can be used for the BSD and the down payment for the private property, but not for ABSD.

6. What happens if I cannot sell my HDB flat within 6 months for the ABSD remission?

If the HDB flat is not sold (legal completion of resale) within 6 months of the private property’s legal completion, the 20% ABSD paid upfront is forfeited — it is not refundable under any extension of time. IRAS does not grant extensions. If you have not yet found a buyer for the HDB flat and the 6-month deadline is approaching, you may need to price the flat more aggressively to accelerate the sale. This is why upgraders using the buy-first strategy typically list their HDB flat for sale as soon as they have exercised the OTP on the private property.

7. Are there any grants available to HDB upgraders buying private property?

No — CPF Housing Grants (EHG, Family Grant, Step-Up Grant, Singles Grant, Proximity Housing Grant) are only available for HDB flat purchases, not for private residential property. When you upgrade to a private property, you do not receive any government grant. The only financial assistance is the ability to use your CPF OA savings for the private property down payment and BSD, subject to the CPF Withdrawal Limit and Valuation Limit rules.

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or tax advice. ABSD rates, MOP requirements, CPF rules, HDB regulations, and financing policies are subject to change. Readers should verify current information with the relevant authorities — the Housing & Development Board (HDB) at hdb.gov.sg, the Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg, the Central Provident Fund Board (CPF) at cpf.gov.sg, and the Monetary Authority of Singapore (MAS) at mas.gov.sg — and consult a licensed conveyancing solicitor and/or a registered estate agent before making any property transaction decisions.

For Singapore’s “sandwich class” — households who earn too much to qualify for subsidised HDB flats but find new private condominiums financially out of reach — the Executive Condominium (EC) remains the most important rung on the property ladder. Priced typically S$400–S$700 per square foot lower than comparable private condominiums at launch, ECs are purpose-built by private developers on government land, sold to eligible buyers with CPF grants, and eventually privatised ten years after their Temporary Occupation Permit (TOP) date. At that point, they trade freely on the open market like any private condominium.

This guide covers everything you need to know about buying an EC in Singapore in 2026 — who is eligible, how much you can borrow, which CPF grants apply, the full cost breakdown, and how the new cooling measures announced on 8 May 2026 change the landscape. Where relevant, we cross-reference the EC rule changes in our separate article Singapore EC Rule Changes May 2026: 10-Year MOP, No DPS and 90% First-Timer Quota Explained.

Quick Answer — EC Buying Guide at a Glance

ECs are built by private developers but sold under HDB rules — eligibility, income ceiling (S$16,000/month for families), and a 5-year MOP apply.

New ECs in 2026 are launching at an estimated S$1,400–S$1,550 psf — roughly S$400–S$600 psf lower than comparable OCR private condominiums.

Eligible buyers can access the CPF Additional Housing Grant (AHG) of up to S$30,000 and the Family Housing Grant (FHG) of up to S$10,000.

As of 8 May 2026, new EC rules include: 10-year MOP before an EC unit can be rented out in its entirety, 15-year privatisation period (up from 10), 90% first-timer priority ballot, and abolition of the Deferred Payment Scheme (DPS).

ABSD is not payable on a first EC purchase from the developer; standard ABSD rates apply if buying a fully privatised EC on the open market.

You cannot own any private property for 30 months before applying, and must not own another HDB flat at the time of EC application.

The Minimum Occupation Period is 5 years for selling; the unit cannot be rented out in its entirety during this 5-year period (and now 10 years for full-unit rental under the new rules).

At privatisation (15 years from TOP under the new rules), the EC may be purchased by foreigners at standard ABSD rates.

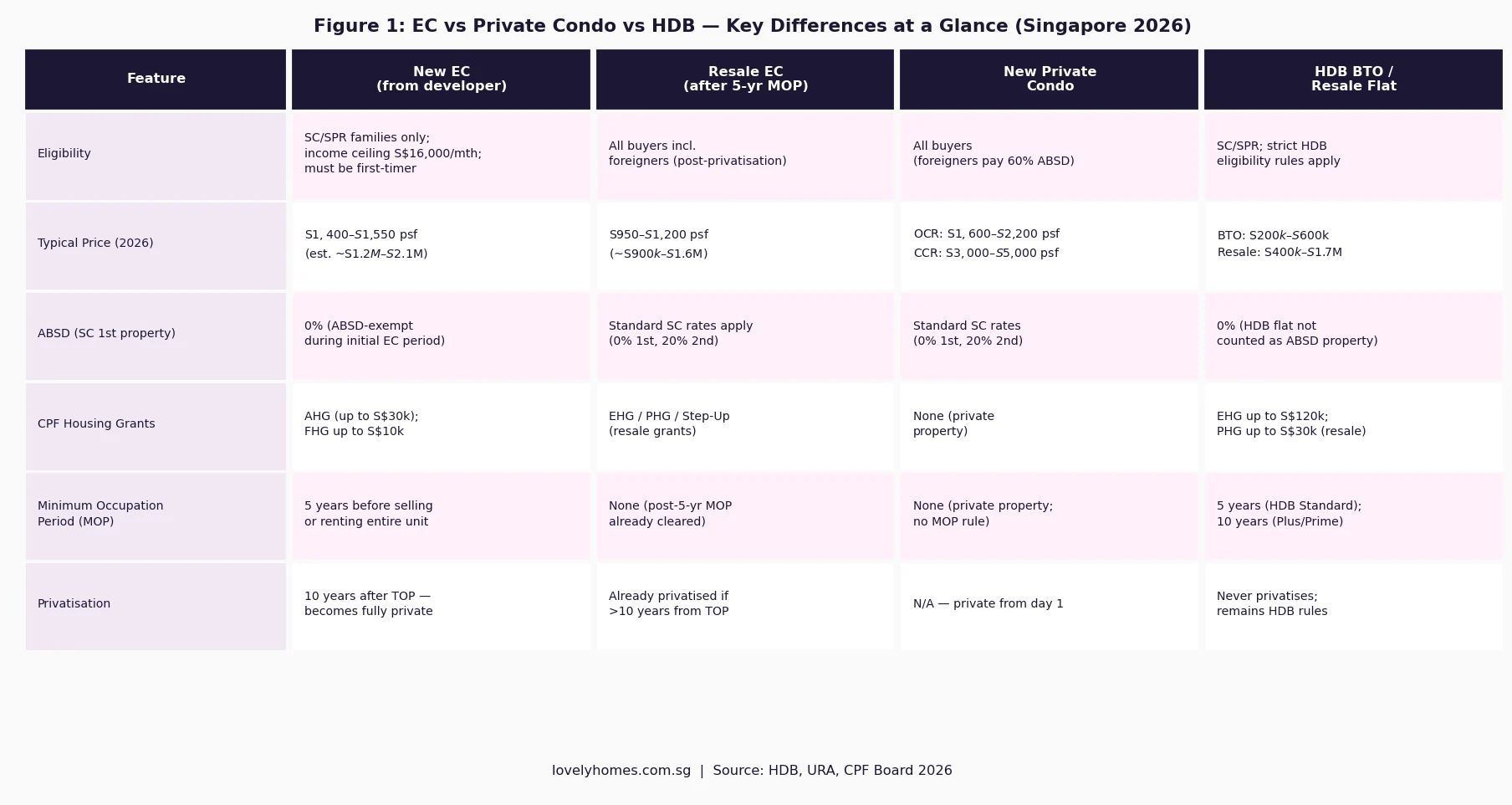

What Is an Executive Condominium?

An Executive Condominium is a hybrid residential property type unique to Singapore, introduced by the Housing and Development Board (HDB) in 1995. It is developed by private developers on land sold by HDB under the Government Land Sales (GLS) programme, and comes with private condominium facilities — swimming pool, gymnasium, clubhouse, security, and landscaped grounds — at a price point made accessible through an eligibility framework similar to HDB flats.

Unlike a standard HDB flat, an EC is sold under a hybrid legal framework: it is a private strata-title property governed by the Building Maintenance and Strata Management Act (BMSMA), but for the first ten to fifteen years (depending on the vintage), it is subject to HDB ownership rules including the Minimum Occupation Period (MOP) and eligibility requirements. After the privatisation date, these HDB rules fall away entirely and the property trades as a full private condominium.

HDB administers the EC scheme. The Singapore Land Authority (SLA) maintains the land register. The Urban Redevelopment Authority (URA) tracks EC transaction data under the same REALIS system that covers private condominiums. Applications for new EC launches are made through the HDB portal at hdb.gov.sg.

Figure 1: Executive Condominium vs Private Condo vs HDB — key differences at a glance (Singapore 2026). Source: HDB, URA, CPF Board.

EC Eligibility in 2026 — Who Can Buy?

Eligibility for purchasing a new EC from the developer is strictly governed by HDB. The primary eligibility schemes are the Public Scheme (family nucleus), Fiance/Fiancee Scheme, Orphans Scheme, and Joint Singles Scheme. The overwhelming majority of EC buyers purchase under the Public Scheme: a Singapore Citizen applicant forms a family nucleus with a spouse, children, or parents.

Eligibility Criterion

Requirement

Citizenship

At least one applicant must be a Singapore Citizen. The other occupier may be a Singapore Citizen or Permanent Resident.

Age

At least 21 years old (18 years old for orphans scheme)

Income ceiling

Monthly household gross income ≤ S$16,000 (families); ≤ S$8,000 (singles — Joint Singles Scheme only, age 35+)

First-timer status

Must not have previously owned a private residential property in the 30 months before the EC application. Both applicant and occupier must not currently own an HDB flat (unless selling within 6 months of EC key collection).

Previous subsidies

If previously purchased an HDB flat with CPF grants or sold an HDB flat with HDB loan, there are waiting periods or resale levy implications. Check HDB’s eligibility calculator.

30-month private property rule

Neither the applicant nor any listed occupier may have disposed of a private residential property within 30 months before the EC application date.

Ownership of HDB flat

Must not own an HDB flat unless you commit to sell within 6 months of EC TOP (for existing HDB owners upgrading).

Under the new rules effective 8 May 2026, 90% of units in each EC launch are balloted exclusively to first-timer families in the initial launch phase. This is a significant increase from the previous 70% first-timer priority, and is designed to ensure that ECs continue to serve their target demographic — upgraders who have not previously benefited from a subsidised property. Second-timer families (who have previously owned an HDB flat) are permitted to ballot only for the remaining 10% allocation during the first month of launch, and gain unrestricted access from the second month.

EC Pricing, CPF Grants, and Affordability in 2026

The pricing advantage of an EC over a comparable OCR private condominium has been the scheme’s defining attraction since its introduction. In the 2026 launch pipeline, new ECs are expected to price at S$1,400–S$1,550 per square foot, against OCR private condominiums averaging S$1,900–S$2,200 psf. For a 1,000 sq ft three-bedroom unit, that translates to a launch price of approximately S$1.4M–S$1.55M for the EC versus S$1.9M–S$2.2M for a comparable private condo — a saving of S$450,000–S$700,000 before grants.

On top of the pricing discount, eligible EC buyers may apply for CPF housing grants. The two principal grants for new EC purchases are the CPF Additional Housing Grant (AHG) and the Family Housing Grant (FHG), both administered by the CPF Board and HDB:

Figure 2: EC income ceiling and CPF grant amounts for EC buyers (Singapore 2026). AHG = Additional Housing Grant; FHG = Family Housing Grant. Source: HDB, CPF Board.

Grant

Maximum Amount

Income Ceiling to Qualify

Notes

CPF Additional Housing Grant (AHG)

S$30,000

≤ S$10,000/month (family)

Tiered based on income; only first-timers eligible; credited to CPF OA

Family Housing Grant (FHG)

S$10,000

≤ S$16,000/month (family)

Available to all eligible EC first-timer families; credited to CPF OA

Step-Up CPF Housing Grant

S$15,000

≤ S$7,000/month (2nd-timer)

For 2nd-timer families who previously lived in a 2-room or smaller HDB flat; not stacked with AHG

CPF grants for ECs are credited to your CPF Ordinary Account (OA) and may be used to offset the purchase price or reduce the mortgage. Unlike HDB resale grants, EC grants do not require you to hold the property for the MOP before they are “used up” — but CPF OA funds used are subject to the standard CPF accrued interest rules on eventual sale.

Financing an EC: Bank Loans, CPF, and the TDSR/MSR Framework

ECs may only be financed via bank loans — HDB concessionary loans are not available for EC purchases. The loan is subject to the standard Monetary Authority of Singapore (MAS) framework: Total Debt Servicing Ratio (TDSR) of 55% and, for EC purchases, the Mortgage Servicing Ratio (MSR) of 30% of gross monthly income. The MSR applies because ECs are treated as HDB-type properties for the purposes of borrowing limits during the initial eligibility period.

Under the prevailing LTV rules, a buyer with no outstanding property loans may borrow up to 75% of the purchase price (or market valuation, whichever is lower) from a financial institution. With the new 2026 rules abolishing the Deferred Payment Scheme (DPS), buyers are required to service the loan from the point of purchase or from when construction milestones are reached under the Normal Progressive Payment scheme.

Financing Parameter

Applicable Rule

Loan type

Bank loan only (no HDB concessionary loan for ECs)

Maximum LTV

75% of purchase price / valuation (whichever is lower), assuming no existing property loans

Minimum cash payment

5% in cash; remaining 20% downpayment may come from CPF OA

TDSR (total debt)

All monthly debt obligations ≤ 55% of gross monthly income

MSR (mortgage only)

EC mortgage repayment ≤ 30% of gross monthly income

Maximum loan tenure

30 years (capped such that loan maturity does not exceed age 65 of youngest borrower)

DPS (Deferred Payment Scheme)

Abolished effective 8 May 2026 — all purchases use Normal Progressive Payment

EC Cooling Measures 2026: What Changed on 8 May 2026?

The Government announced a package of EC-specific cooling measures on 8 May 2026 — the most significant changes to the EC framework in over a decade. The changes are designed to reinforce the EC’s role as a subsidised housing product for genuine owner-occupiers and to curtail speculative demand. The four key changes are:

10-year full-unit rental restriction: EC owners may not rent out their entire unit for 10 years from the unit’s TOP date (up from the previous 5-year restriction). During this period, individual rooms may still be rented to authorised occupants. This effectively extends the owner-occupier commitment period significantly.

15-year privatisation period: An EC is now privatised 15 years from its TOP date (up from 10 years previously). Until privatisation, the HDB ownership rules continue to apply. From the privatisation date, the EC becomes a full private condominium and may be sold to foreigners and entities without restriction.

90% first-timer priority ballot: In the first month of each EC launch, 90% of units are reserved for first-timer families — up from 70%. This ensures that the primary beneficiaries of the EC subsidy are those who have not previously owned a subsidised property.

Abolition of the Deferred Payment Scheme (DPS): Buyers can no longer defer mortgage repayments until TOP. All EC purchases from 8 May 2026 onwards use the Normal Progressive Payment scheme, which ties payments to construction milestones. This is consistent with the progressive payment rules that already apply to most new launches.

EC Minimum Occupation Period (MOP) — What You Can and Cannot Do

The EC Minimum Occupation Period is 5 years, measured from the date of key collection (i.e., from the date the unit is physically occupied, not from TOP or purchase date). During the 5-year MOP, the EC owner must live in the unit and cannot sell or sublet the entire unit to a third party. Individual rooms may be rented to authorised occupants, subject to HDB’s prevailing subletting rules.

After completing the 5-year MOP, the EC may be sold on the open market to Singapore Citizens and PRs (but not yet foreigners or entities, as the privatisation has not yet occurred). After the 15-year privatisation milestone (under the new rules), the EC may be sold to any buyer worldwide including foreigners and companies — at which point standard ABSD rates apply to the buyer based on their profile and property count.

EC vs Private Condo: Price Gap and Value Proposition (2016–2026)

The persistent price gap between EC new launches and comparable OCR private condominiums has historically closed over time as the EC approaches and then passes privatisation. Buyers who purchased ECs at launch in 2014–2017 have typically seen capital appreciation of 25–45% by the time of privatisation around 2024–2027, in many cases outperforming comparable OCR condominiums on a per-unit basis given the lower entry price.

Figure 3: EC new launch PSF vs OCR private condo average — Singapore 2016 to 2026. The shaded area represents the price gap available to EC buyers. Source: URA REALIS, HDB, LovelyHomes research.

The 2026 EC launch pipeline includes several projects across the OCR and RCR, including Altura EC (Bukit Batok West Avenue 8) and Novo Place (Tengah Garden Avenue), which are near-completion or recently TOP’d, as well as upcoming launches in Tampines, Tengah, and Bedok areas. Under the new 15-year privatisation rule, buyers of 2026 ECs should note that the privatisation milestone does not arrive until approximately 2040–2041, extending the HDB-rule period compared with earlier vintages.

Worked Example: The Lim Family Buying a 2026 EC Launch

Mr and Mrs Lim are a Singapore Citizen couple, both aged 34. Their combined gross monthly income is S$12,000. They are first-time buyers who have never owned any private property or subsidised HDB flat. They are applying for a new EC launch at Tengah, priced at S$1.45M for a 1,000 sq ft three-bedroom unit.

Item

Amount

Notes

Purchase price

S$1,450,000

1,000 sq ft, 3-bedroom EC at ~S$1,450 psf

CPF AHG (income S$12,000 — no AHG; AHG requires ≤S$10,000)

S$0

Income S$12,000 exceeds AHG S$10,000 ceiling

CPF Family Housing Grant (FHG)

S$10,000

First-timer family; income ≤ S$16,000 — fully eligible

Effective purchase price after grant

S$1,440,000

Grant applied against CPF OA balance

ABSD

S$0

First EC purchase from developer — ABSD-exempt

BSD

S$43,400

On S$1.45M: 1%×180k + 2%×180k + 3%×640k + 4%×450k

Bank loan (75% LTV)

S$1,087,500

Based on purchase price S$1.45M × 75%

Minimum cash downpayment (5%)

S$72,500

Must be paid in cash

CPF OA (remaining 20% downpayment)

S$290,000

From CPF OA (including FHG S$10,000)

Monthly mortgage (25 years @ 3.5%)

~S$5,440/month

MSR = 45.3% — EXCEEDS 30% MSR; must increase downpayment or reduce loan

MSR = 29.9% — within 30% MSR limit. Requires additional S$287,500 in CPF/cash.

This worked example illustrates a critical affordability tension: the MSR of 30% cap on the EC mortgage can force buyers with a combined income of S$12,000 to make a larger downpayment than the minimum 25% required by LTV rules. At S$1.45M and a 3.5% bank rate, a 75% LTV loan of S$1.0875M requires monthly repayments of approximately S$5,440 — an MSR of 45.3%, far above the 30% limit. The Lim family would need to either reduce the loan amount (by increasing their downpayment to approximately 44.8%), buy a smaller or lower-priced unit, or wait until their income increases. This is a common challenge for buyers in the S$11,000–S$16,000 income band looking at 3-bedroom ECs in 2026.

EC Buying Summary — Key Rules at a Glance (2026)

Rule / Parameter

Current Position (Post–8 May 2026)

Income ceiling (family)

S$16,000/month

Income ceiling (singles, age 35+)

S$8,000/month (Joint Singles Scheme)

First-timer priority at launch

90% of units — raised from 70% on 8 May 2026

ABSD on new EC purchase

Nil (ABSD-exempt for eligible buyers under EC scheme)

Minimum Occupation Period

5 years (from key collection date)

Full-unit rental restriction

10 years from TOP (new rule from 8 May 2026)

Privatisation period

15 years from TOP (new rule; previously 10 years)

Deferred Payment Scheme

Abolished — Normal Progressive Payment only (8 May 2026)

CPF AHG (max)

S$30,000 (income ≤ S$10,000/month)

CPF FHG (max)

S$10,000 (income ≤ S$16,000/month)

Loan type

Bank loan only (no HDB concessionary loan)

MSR cap

30% of gross monthly income

TDSR cap

55% of gross monthly income

Maximum LTV

75% (no existing property loans)

What Might Come Next for the EC Scheme?

The 8 May 2026 cooling measures signal a clear policy intent: the Government views the EC as a genuine first-home product for middle-income Singaporeans, not a short-to-medium-term investment vehicle. The extension of the rental restriction to 10 years and the privatisation period to 15 years both reduce the speculative premium that early-privatisation buyers have historically captured.

Going forward, it is possible that: the income ceiling is revised upward to keep pace with nominal wage growth; additional GLS sites are released to increase EC supply given strong demand from HDB upgraders; or that the 30-month private property wait-out period for EC applicants is extended further. These are speculative scenarios — any changes would be announced by HDB and take effect from the announcement date.

For buyers evaluating ECs in the 2026 pipeline, the longer privatisation horizon means a re-pricing of the “privatisation premium” into the expected hold period. Buyers who are genuinely owner-occupiers over a 15-year horizon are largely unaffected — but those who were banking on a 10-year exit into the private market will need to revise their investment thesis.

Can a Singapore PR buy a new EC directly from the developer?

No. At least one applicant in the household must be a Singapore Citizen to buy a new EC from the developer. A Singapore PR may be listed as an occupier or co-applicant only if the primary applicant is a Singapore Citizen. After the EC completes its 5-year MOP, it may be sold to SC or SPR buyers. After privatisation (15 years from TOP under the new rules), it may be sold to foreigners and entities as well.

Do I pay ABSD when buying an EC from the developer?

No, ABSD is not payable on a first EC purchase from the developer under the EC eligibility scheme, provided you qualify under one of HDB’s approved eligibility schemes and the purchase is your first-ever subsidised property. However, if you already own a private residential property (and have not disposed of it within 30 months before applying), you are ineligible for the EC scheme entirely. ABSD applies normally if you purchase a fully privatised EC on the resale market after the 15-year privatisation milestone, as that is treated as a standard private property purchase.

What is the difference between an EC’s MOP and the rental restriction?

These are two distinct rules. The MOP (5 years from key collection) governs when you can sell the EC unit — you must hold and occupy it for 5 years before selling on the open market. The full-unit rental restriction (now 10 years from TOP under the 8 May 2026 rules) governs when you can rent out the entire unit to a third-party tenant. You can rent individual rooms at any time to authorised occupants, but cannot vacate the unit entirely and sublet it as a whole during the 10-year period. Both rules apply concurrently — you may therefore sell after 5 years, but the buyer cannot rent it out until the 10-year rental restriction expires.

Can I use CPF to buy an EC?

Yes. CPF Ordinary Account (OA) savings may be used to pay the downpayment (except the mandatory 5% cash portion), stamp duties, and monthly mortgage instalments for an EC, subject to the Valuation Limit and Withdrawal Limit rules. CPF housing grants (AHG and FHG) are credited to your CPF OA and can be applied against the purchase price. The standard CPF accrued interest rules apply — any CPF OA used must be returned with accrued interest (currently 2.5% per annum) when the property is eventually sold.

Is an EC a good investment in 2026?

The investment case for ECs has historically been strong for genuine owner-occupiers. The entry price discount (versus comparable private condominiums) combined with appreciation to private-market values at and after privatisation has generated solid capital gains for many EC buyers over 10–15-year hold periods. However, the new 15-year privatisation rule extends the investment horizon and reduces the liquid exit window. ECs are best regarded as a long-term owner-occupier decision with an embedded investment component, not a short-cycle flip. Gross rental yields for EC units approaching privatisation (around 3.5–4.5%) are competitive with OCR private condominiums. Buyers should factor in the MSR borrowing constraint, which can require a higher-than-minimum downpayment at today’s price levels, reducing their effective leverage and upfront capital efficiency compared with a similarly-sized HDB flat purchase.

What upcoming EC projects are launching in 2026?

The 2026 EC launch pipeline includes several projects across the OCR. Watch the LovelyHomes EC Launches page for the latest project information as details are confirmed. Key sites in the URA 1H2026 GLS Confirmed List include Tengah Garden Avenue (multiple phases), Tampines North, and a Bedok South site. Pricing at new launches has been in the S$1,400–S$1,550 psf range based on recent comparable awards; final prices depend on developer cost structures and market conditions at the time of launch.

Disclaimer: This article is for general information and educational purposes only. It does not constitute legal, financial, or investment advice. EC eligibility rules, income ceilings, CPF grant amounts, and cooling-measure parameters are set by HDB and the Singapore Government and may change at any time. Always verify the current position on the HDB website and consult a licensed property agent (CEA-registered), conveyancing lawyer, and/or licensed financial adviser before making any property decision. LovelyHomes is not a licensed property agent and does not represent any developer, agent, or financial institution.

Upgrading from an HDB flat to a private condominium is the most common property milestone in Singapore. For a Singapore Citizen couple who bought their HDB in the early 2010s, the combination of substantial HDB appreciation, accumulated CPF savings, and rising household income has made condo upgrading more achievable than it has ever been — but the transaction is still the most financially consequential decision most families will make. Getting the sequencing wrong can cost S$300,000 or more in avoidable Additional Buyer’s Stamp Duty (ABSD). This guide walks you through every step, from checking your eligibility to collecting your new keys.

Quick Answer — HDB to Condo Upgrade at a Glance

Minimum Occupation Period (MOP): You must have fulfilled 5 years’ MOP before selling your HDB flat

ABSD — Sell First: Zero ABSD if you sell your HDB before purchasing the condo

ABSD — Buy First: 20% ABSD upfront, claimable if you sell the HDB within 6 months (SC couples only)

LTV for second property: 45% maximum loan-to-value (55% down payment required) if you still hold the HDB at the time of condo purchase

CPF usage: Your CPF OA (refunded from HDB sale + current balance) can fund the new condo’s down payment and monthly mortgage

2026 market context: Private prices up 0.3% q-o-q in Q1 2026; just ~8,100 new launch units in the 2026 pipeline — act with research but without panic

Step 1 — Check Your HDB Eligibility: Has Your MOP Been Met?

The first gateway to upgrading is the Minimum Occupation Period. For most HDB flats (BTO and resale), the MOP is 5 years from the date you collect the keys. You cannot sell your HDB flat, rent out the entire flat, or purchase a private property — whether in Singapore or overseas — until your MOP has been fulfilled. This applies to both joint owners.

Exceptions exist for certain special categories (e.g., divorce, death of owner, financial hardship), but these require HDB approval. For the vast majority of upgraders, the path is straightforward: wait out the MOP, then proceed. Check your MOP completion date on the HDB website or via the My HDBPage portal.

Step 2 — The Critical Decision: Sell First or Buy First?

This is the most consequential decision in the entire upgrader journey. It determines whether you pay S$0 or potentially hundreds of thousands of dollars in ABSD, and it shapes your entire financing plan. There is no universally right answer, but there is a framework for making the decision.

Option A — Sell First (Recommended for most upgraders)

You sell your HDB flat first, collect the proceeds, clear your HDB loan (if any), and receive your CPF refund (principal drawn plus accrued interest). You are then in the position of a first-time private property buyer: clean title history, 75% LTV (25% down payment), and zero ABSD as a Singapore Citizen buying your first private property. The trade-off is a temporary housing gap — you need somewhere to stay between selling the HDB and moving into the new condo. Options include renting privately, staying with family, or timing the HDB sale to coincide with a condo’s TOP date.

Option B — Buy First (ABSD Remission Route)

An SC couple can purchase a replacement private home while still owning the HDB flat, pay the 20% ABSD upfront, and then apply for a remission from IRAS after selling the HDB — provided the HDB is sold within 6 months of the condo’s purchase date (or 6 months after the condo’s TOP date for uncompleted projects). If the conditions are met, IRAS refunds the full 20% ABSD. The advantage is continuity of housing with no displacement. The risks are: (1) LTV drops to 45% because you hold two properties; (2) the 6-month sale deadline creates pressure; (3) if you miss the deadline for any reason, the ABSD is forfeited.

Important: Only SC-SC or SC-SPR couples qualify

The ABSD remission for replacement property purchases applies only to married couples where at least one spouse is a Singapore Citizen. Single buyers and SPR-SPR couples do not qualify for this remission. Always verify your eligibility with your conveyancing lawyer before relying on this route.

Sell First vs Buy First — Side-by-Side Comparison

Factor

Sell First

Buy First (with Remission)

ABSD payable upfront

S$0

S$370,000 (20% on S$1.85m)

ABSD recoverable?

N/A — no ABSD paid

Yes, if HDB sold within 6 months of new purchase

Interim housing needed?

Likely yes — bridge gap between sale and move-in

No — can stay in HDB until new condo TOP or handover

Bridging loan required?

Possibly (for IPA lapse or timing gap)

Usually no; but servicing 2 mortgages concurrently is a risk

Financial flexibility

Full sales proceeds available before next purchase

Tie-up of capital; dual mortgage risk

Ideal for

Buyers who want a clean break; financial discipline preferred

Families who need continuity of housing; confident of selling HDB within 6 months

Risk

Temporary displacement; may miss specific launch

ABSD remission application not guaranteed; timing pressure

Key Takeaway

For most HDB upgraders, Sell First eliminates ABSD entirely and reduces financial risk. Buy First suits families who cannot afford temporary displacement and are confident in selling their HDB within 6 months.

Source: IRAS / CPF Board — 24 April 2026

lovelyhomes.com.sg

Step 3 — Understanding Your Finances: How Much Can You Afford?

The upgrader’s budget equation has three inputs: net HDB sale proceeds, current CPF OA balance, and borrowing capacity. Here is how each works.

Net HDB proceeds: Your gross HDB sale price minus (a) the outstanding HDB loan balance (if any), (b) the CPF principal withdrawn plus accrued interest at 2.5% per annum (this is refunded back to your CPF OA, not paid in cash), (c) legal and conveyancing costs, and (d) agent commission (typically 1–2% of sale price). The cash proceeds are what remains after all of the above — in a fully-paid-up HDB bought in 2010, this could be substantial cash plus a large CPF refund.

CPF OA balance (post-refund): Once your HDB is sold, all CPF OA monies drawn for the purchase (plus 2.5% p.a. accrued interest) are returned to your OA. This refreshed CPF balance can be applied toward the down payment and monthly instalments of the new condo. Note: the CPF Usage Rules for private property limit how much you can use depending on the remaining lease of the property and your age at the time of purchase. For a 99-year leasehold condo with >60 years remaining, the full Valuation Limit applies.

Loan eligibility (TDSR): Your Total Debt Servicing Ratio must not exceed 55% of your gross monthly income across all outstanding debt obligations. For most salaried couples in dual-income households, this is not the binding constraint. The loan quantum for a private property is subject to a 75% LTV (Sell First) or 45% LTV (Buy First while HDB still held). At 75% LTV, a S$1.85 million condo requires a S$462,500 down payment (25%), of which at least 5% (S$92,500) must be in cash.

Step 4 — Buyer’s Stamp Duty: What You Will Pay

BSD is payable by every buyer — it applies regardless of whether you hold any other property. It is calculated on the higher of the purchase price or the market value of the property, using the progressive table below.

BSD Rates in Singapore 2026

Purchase Price Band

BSD Rate

BSD on That Band

First S$180,000

1%

S$1,800

Next S$180,000 (S$180k–S$360k)

2%

S$3,600

Next S$640,000 (S$360k–S$1m)

3%

S$19,200

Next S$500,000 (S$1m–S$1.5m)

4%

S$20,000

Next S$1,500,000 (S$1.5m–S$3m)

5%

S$75,000 max in this band

Above S$3,000,000

6%

Variable

Key Takeaway

BSD on a S$1.85 million condo = S$1,800 + S$3,600 + S$19,200 + S$20,000 + (S$350,000 × 5%) = S$1,800 + S$3,600 + S$19,200 + S$20,000 + S$17,500 = ~S$62,100.

Source: IRAS — iras.gov.sg/taxes/stamp-duty — 24 April 2026

lovelyhomes.com.sg

Step 5 — New Launch vs Resale: Which Route for Upgraders?

New launch condos offer the Progressive Payment Scheme (PPS), where you pay in stages as construction milestones are reached. This creates a natural cash-flow buffer: you do not need the full loan amount drawn down on day one, giving you time to sell your HDB and rebuild savings before full monthly instalments begin. The trade-off is a 3–4 year wait for TOP, during which you may need to rent. New launches in Singapore’s 2026 pipeline are heavily subscribed — popular projects such as Pinery Residences achieved a 92.5% launch-weekend take-up rate in early 2026 — so acting decisively at launch is important for choice units.

Resale condos offer immediate occupation, avoiding the rental gap entirely. You can time the HDB sale to coincide with resale condo completion in as little as 8–12 weeks. The full loan amount is drawn down from day one, so your monthly commitment is immediate. Resale units in popular districts (15, 19, 23, 26) may command a premium over new launches on a per-square-foot basis, but you avoid the risk of TOP delays and the uncertainty of unit quality before handover.

Step 6 — Executive Condominiums: The Upgrader’s Middle Ground

Executive Condominiums (ECs) are a hybrid product developed by private developers but sold at subsidised prices to HDB upgraders. They are subject to an eligibility framework (Monthly Household Income ceiling: S$16,000; you must not have owned private property in the preceding 30 months; at least one applicant must be SC or PR), but if you qualify, ECs offer condo-standard facilities at prices typically 20–30% below comparable private condos in the same area. ABSD is not payable when buying a new EC directly from the developer, even if you still own your HDB flat — a significant advantage over the private condo route.

The 2026 EC pipeline includes Rivelle Tampines EC and projects in Sembawang and Plantation Close. These are worth considering for eligible upgraders who prioritise value over prime CCR address.

Step 7 — Getting Your In-Principle Approval (IPA)

Before signing any Option to Purchase (OTP), secure an In-Principle Approval (IPA) from your bank. An IPA gives you a formal indication of the loan quantum, interest rate, and tenure the bank is willing to offer, based on your income documents and credit profile. Having an IPA in hand at the showflat means you know your exact budget envelope and can make a confident, irreversible decision when the OTP is presented. Note that an IPA is not a formal Letter of Offer — the bank will conduct a full assessment when you submit a formal loan application — but it is the closest proxy available before a specific unit is identified. Most banks issue IPAs within 2–3 business days. Compare rates across at least 3 banks, including fixed-rate (typically 2.5–3.5% in 2026), floating SORA-linked, and fixed-SORA hybrid packages.

Step 8 — The Legal Process: From OTP to Keys

For a new launch condo, the process runs: (1) exercise the OTP (1% booking fee) → (2) sign the Sale & Purchase Agreement within 3 weeks (typically 4–9% more paid) → (3) engage a conveyancing lawyer → (4) pay BSD (and ABSD if applicable) within 14 days of OTP exercise → (5) progress payments as per the PPS schedule over the construction period → (6) collect keys at TOP → (7) complete final payment and receive Certificate of Statutory Completion. The conveyancing lawyer handles stamp duty payments, title searches, bank loan drawdown, and final completion. Budget S$3,000–S$5,000 in legal fees for a standard new-launch purchase.

2026 Market Context — Is Now the Right Time?

The Q1 2026 URA flash estimate showed a modest 0.3% quarter-on-quarter increase in private residential prices, with the OCR (where most upgrader condos are priced) leading at +1.3% q-o-q. The 2026 launch pipeline is significantly constrained at approximately 8,100 units across 17 projects, down 30% from 2025. This supply tightness tends to sustain prices and take-up rates at quality launches, as seen in the strong weekend sales figures at Pinery Residences (92.5% sold) in Q1 2026.

For upgraders, the current environment suggests a window of stable prices with limited new supply — not a runaway market, but also not a buyer’s market in the traditional sense. Prioritise location, unit type, and fit-for-purpose over speculation. The best condo purchase for an upgrader family is one they can comfortably afford and intend to occupy for at least 5 years.

Frequently Asked Questions

Can I own an HDB and a condo at the same time?

Yes, but only after fulfilling the HDB MOP. An SC or SPR can hold both an HDB flat and a private property simultaneously after MOP, subject to paying 20% ABSD (SC) or 30% ABSD (SPR) on the private purchase. You must then sell the HDB within the prescribed timeframe to claim ABSD remission (SC couples only). You cannot own an HDB and a private property at the same time before MOP — this would breach HDB ownership rules.

Does CPF need to be returned when I sell my HDB?

Yes. All CPF monies withdrawn for the HDB purchase (including the principal and accrued interest at 2.5% p.a.) are automatically returned to your CPF OA upon sale. You do not get this cash in hand; it goes back into your CPF OA. However, you can then re-use this CPF OA balance for the new condo purchase, subject to CPF usage rules for private properties.

What is the maximum loan for a condo if I still own my HDB?

If you hold an existing property (including an HDB flat) at the time of the condo purchase, the maximum LTV for a bank loan is 45% — meaning a 55% down payment is required, of which 25% must be in cash. This is a significant constraint and one of the key reasons most upgraders prefer the Sell First strategy.

Can I use my CPF to pay for the condo if the remaining lease is short?

CPF usage for private property is subject to the Lease Remnant Restriction: the property’s remaining lease must cover the youngest buyer to age 95. For most new-launch 99-year leasehold condos, this requirement is easily satisfied. Shorter-lease or older resale properties may restrict CPF usage or trigger a pro-rated cap. Check the CPF online calculator or consult your conveyancing lawyer.

What if I miss the 6-month ABSD remission deadline?

If you fail to sell your HDB within the 6-month window, the ABSD is not refunded. It is permanently forfeited. IRAS does grant extensions in exceptional circumstances (e.g., death of a co-owner), but these are discretionary and not guaranteed. If you are buying first, build in a buffer and engage a property agent to market your HDB promptly after exercising the condo OTP.

Disclaimer: This guide is for general information only and does not constitute financial, legal, or tax advice. ABSD rates, LTV limits, CPF rules, and HDB eligibility conditions are subject to change. Always verify current figures on the IRAS website and CPF Board, and consult a licensed property agent and conveyancing solicitor before proceeding.