Tampines North Neighbourhood Guide Singapore 2026: Property Prices, MRT, Schools and Investment Outlook

- Tampines North is Singapore’s newest planned sub-town within the established Tampines New Town in District 18 (D18), located in the northeast of Singapore, approximately 25 km from the CBD.

- The area currently has excellent EWL access via Tampines MRT (EW2) and DTL access via Tampines DT32; the upcoming Cross Island Line (CRL) Tampines North Station (~2030) will significantly reduce journey times to the west and Jurong Lake District.

- Parktown Residence (1,193 units), the largest launch in Tampines in years, is integrated with the future Tampines North MRT station and includes a new hawker centre, community club, and retail space.

- HDB resale 4-room flats in Tampines currently trade between S$520,000 and S$700,000; executive condominiums such as Aurelle of Tampines launched from around S$1,100,000.

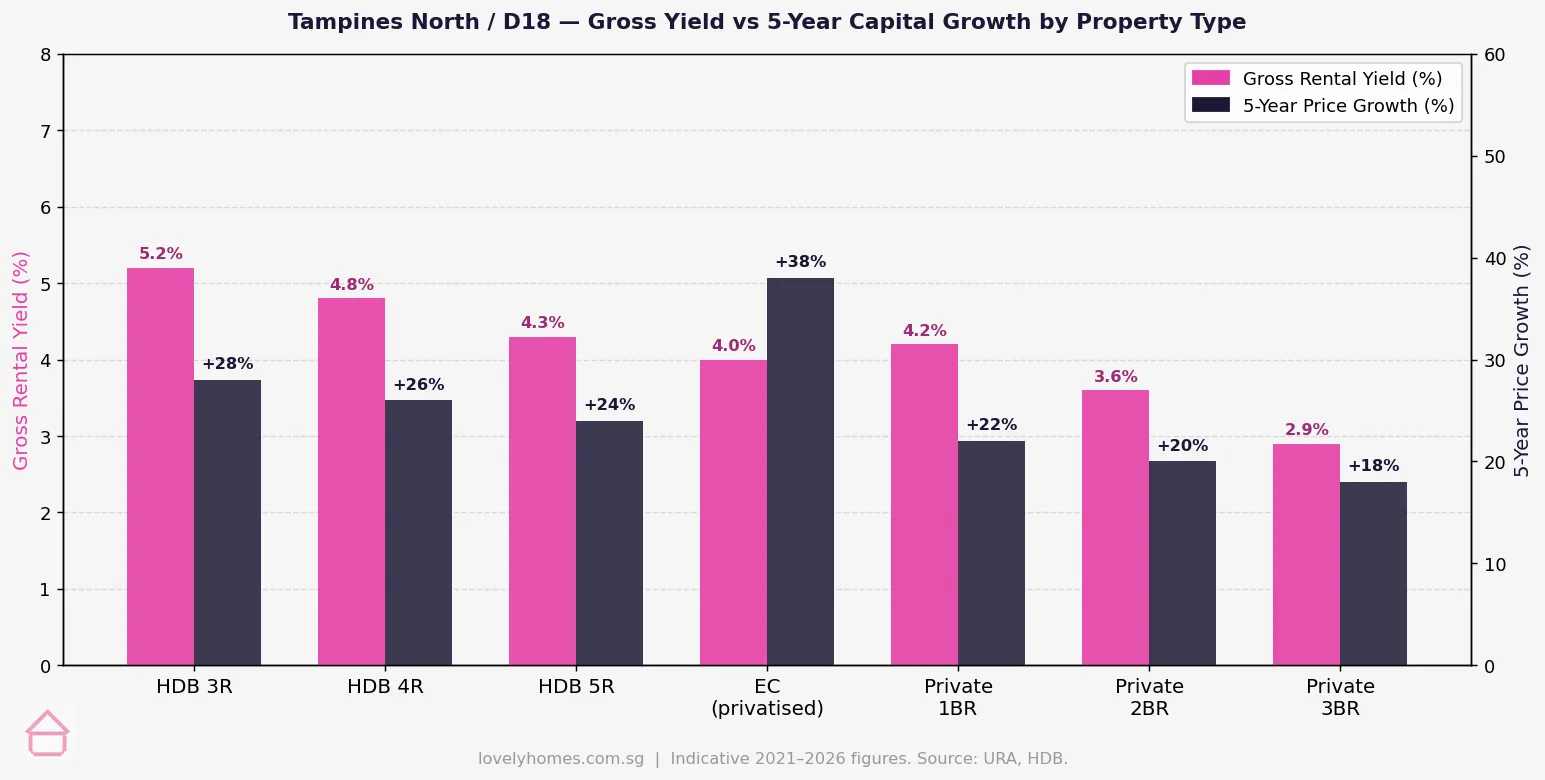

- Gross rental yields in D18 run from 4.8% (HDB 4-room) down to 2.9% (private 3-bedroom), above the Singapore average for the same flat types.

- UWCSEA East Campus, Temasek Polytechnic, and Singapore University of Technology and Design (SUTD) all anchor the area’s education catchment.

- Tampines Hub, Singapore’s largest community centre (60,000 sqm), Tampines Mall, Century Square, White Sands, and IKEA make Tampines North one of the best-served retail sub-markets outside the city.

- The 5-year HDB resale price growth in D18 has been approximately 24–28%, in line with the broader OCR market and supported by the CRL pre-announcement uplift.

Tampines North: Where Is It and Why Does It Matter?

Tampines North is the designated northern section of Tampines New Town — a planned urban extension built out on land that was, until the mid-2010s, largely farmland and industrial reserve. In URA’s parlance, “Tampines North” refers specifically to the sub-town north of Tampines Avenue 10, anchored by the future Tampines North MRT station on the Cross Island Line. The rest of Tampines — served by Tampines MRT on the East-West Line and Tampines DTL on the Downtown Line — is the mature, established town Singaporeans know well.

For property buyers, the distinction matters because Tampines North carries a CRL uplift thesis — the Cross Island Line station is expected to open circa 2030, bringing a third MRT line to the area and cutting the journey time to Jurong Lake District, Singapore’s second CBD, by more than 30 minutes compared to the current EWL route. This pre-station infrastructure play is similar to the uplift enjoyed by Jurong East in the early 2010s as the EWL–NSL interchange became a recognised commercial hub.

The broader Tampines district is classified as an OCR (Outside Central Region) submarket by URA, commanding lower per-square-foot prices than the city core but delivering superior gross rental yields for buy-to-let investors. In Q1 2026, URA data shows OCR private residential prices up approximately 2.2% quarter-on-quarter and HDB resale prices broadly stable across the east.

Property Prices — What You Can Expect to Pay in 2026

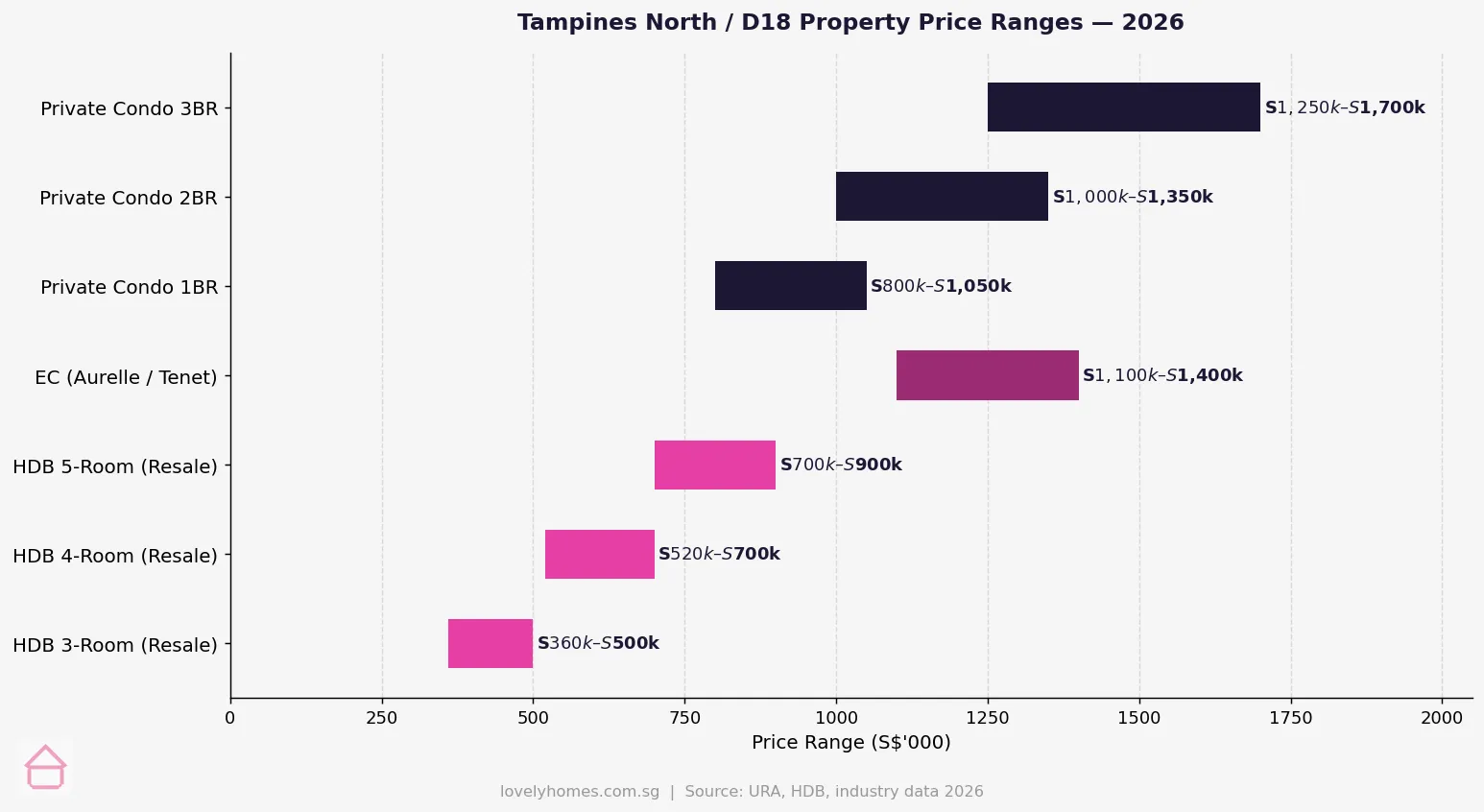

HDB resale prices in Tampines have risen meaningfully since the 2021 cooling-measure-driven market trough. A typical HDB 4-room resale flat in the Tampines North sub-town trades between S$520,000 and S$700,000 depending on floor level, specific block location relative to greenery and noise, and remaining lease. Units closer to Tampines North (the newer blocks built from 2018–2023) tend to command slight premiums given longer remaining leases and proximity to the future CRL station.

Executive Condominiums — a uniquely Singaporean asset class that blends subsidised pricing for SC/PR buyers with private condominium facilities — are prominent in Tampines North. Aurelle of Tampines EC (583 units, Sim Lian Group) launched in 2025 at an average of approximately S$1,350 per square foot, with entry prices from around S$1.1M for 2-bedroom units. The project sits within a 10-minute walk of the future CRL station site. Tenet EC, an older privatised EC in the area, now trades on the resale market between S$1.0M and S$1.3M for 3-bedroom units.

Private condominiums in Tampines North are dominated by the mega-project Parktown Residence — a 1,193-unit, 99-year leasehold integrated development launched in 2025 by a UOL Group, CapitaLand and HDB co-development. It is physically integrated with the Tampines North MRT station and includes a hawker centre, a community club, and a retail precinct. Entry pricing for 1-bedroom units started at approximately S$800,000–S$900,000; 3-bedroom units were in the S$1.35M–S$1.7M range at launch.

MRT Connectivity — The CRL Catalyst

Tampines North is already well-connected by two existing MRT lines and will gain a third by around 2030, making it one of the best-positioned OCR sub-towns for transport connectivity outside the mature estates closer to the city.

The East-West Line (EWL) passes through Tampines (EW2) and Simei (EW3), connecting directly to Changi Airport in one stop and to the city core via Paya Lebar in seven stops. The Downtown Line (DTL) has Tampines (DT32) as its eastern terminus, connecting via Bedok Reservoir, Kembangan, and Marine Parade to the Botanic Gardens and Buona Vista, then turning north-west toward the city. The DTL journey from Tampines to the Botanic Gardens is approximately 30 minutes.

The transformative addition is the Cross Island Line (CRL), specifically Phase 2 (CRL2), which brings a dedicated Tampines North station. CRL links Tampines North westwards through Defu, Hougang, Serangoon North, Ang Mo Kio, and onwards to Jurong Lake District — bypassing the city core and eliminating the need for a transfer at Paya Lebar or City Hall for passengers heading west. The LTA has indicated Phase 2 is targeted for completion around 2030. For property buyers, the practical implication is that the CRL uplift is currently priced into Parktown Residence (which fronts the station site) but only partially priced into the wider HDB resale market, meaning today’s buyers may capture some of the remaining discount-to-station pricing.

Amenities — Everything You Need Within 10 Minutes

Retail and food. Tampines is arguably the best-served OCR sub-market for retail outside Bishan/Ang Mo Kio. The town centre is anchored by Tampines Mall (280,000 sqft), Century Square (revamped in 2021, 560,000 sqft), and White Sands. The IKEA Tampines store and Courts Megastore on Tampines North Link add destination retail. Tampines Hub — opened in 2017 and at 60,000 sqm Singapore’s largest integrated community and lifestyle hub — houses the community library, an Olympic-sized swimming complex, a hawker centre, sports courts, and a 5,000-seat stadium.

Parks and greenery. The Tampines Boulevard Park (completed late 2025) runs along the length of Tampines Avenue 9 as a 3.2-km linear park connecting Tampines North to the Central Catchment, with cycling paths, fitness stations, and community gardens. Tampines Eco Green (36 ha) is a secondary forest reserve within the town, unusual for an urban estate and valued by residents for birdwatching and nature trails. The Bedok Reservoir Regional Park is a 10-minute cycle away.

Healthcare. Changi General Hospital (CGH), a 1,000-bed acute regional hospital, is approximately 5 km from Tampines North. Tampines Polyclinic and Bedok Polyclinic both serve the broader catchment, with a third polyclinic at Pasir Ris serving the eastern corridor.

Schools — A Strong Education Catchment

UWCSEA East Campus (United World College of South-East Asia) sits within Tampines, consistently ranked among the top international schools in Singapore and drawing an expat tenant base that anchors higher-end rental demand. Temasek Polytechnic (TP), one of Singapore’s five polytechnics, is located on Tampines Avenue 1 and adds a significant student population of approximately 18,000 enrolled students. Singapore University of Technology and Design (SUTD), a research university set up in partnership with MIT and ZHEJIANG University, is located at the Changi-Tampines border and draws an educated demographic to the wider east. Primary and secondary schools within the Tampines North catchment include Tampines Primary School, Elias Park Primary, Junyuan Secondary, and St. Hilda’s Primary (popular 1-km circle school further south).

Investment Outlook — Yield vs Capital Growth

The investment case for Tampines North rests on two distinct thesis strands depending on the buyer’s horizon. Short-to-medium-term (1–5 years), the yield-on-cost argument favours HDB resale and older privatised ECs: gross yields of 4.8% on a S$600,000 4-room resale flat, with low vacancy and a large tenant pool anchored by UWCSEA, SUTD, and TP staff and students. Longer-term (5–10 years), the capital growth argument points to the CRL opening circa 2030 as the primary catalyst, with EC and Parktown Residence buyers positioned to benefit from station-adjacency re-rating.

Five-year price growth (2021–2026) in D18 has been approximately 24–28% for HDB resale and 35–38% for privatised ECs, both broadly in line with or slightly above the URA OCR PPI growth over the same period. Private condominiums have grown more modestly at 18–22% given higher absolute entry prices. The important caveat is that the Tampines North private market is predominantly occupied by projects launched from 2022–2025 whose resale data is limited; the 2030 CRL opening is the true test of the station-adjacency premium thesis.

Property Comparison Summary

| Property Type | Price Range (2026) | PSF (est.) | Gross Yield | Tenure | Key Development |

|---|---|---|---|---|---|

| HDB 3-Room (Resale) | S$360k – S$500k | S$420–S$560 psf | ~5.2% | 99yr (remaining) | Various blocks |

| HDB 4-Room (Resale) | S$520k – S$700k | S$450–S$600 psf | ~4.8% | 99yr (remaining) | Tampines North BTO blocks |

| HDB 5-Room (Resale) | S$700k – S$900k | S$420–S$540 psf | ~4.3% | 99yr (remaining) | Various blocks |

| EC (privatised/resale) | S$1.0M – S$1.4M | S$900–S$1,200 psf | ~4.0% | 99yr leasehold | Tenet EC, Aurelle of Tampines |

| Private Condo 1BR | S$800k – S$1,050k | S$1,400–S$1,700 psf | ~4.2% | 99yr leasehold | Parktown Residence |

| Private Condo 2BR | S$1.0M – S$1.35M | S$1,300–S$1,600 psf | ~3.6% | 99yr leasehold | Parktown Residence, Pinery |

| Private Condo 3BR | S$1.25M – S$1.70M | S$1,200–S$1,500 psf | ~2.9% | 99yr leasehold | Parktown Residence |

Worked Example — Mr & Mrs Ng, Buying Tampines North 4-Room HDB Resale

Mr and Mrs Ng are a Singapore Citizen married couple, both in their early 30s. Their combined gross monthly income is S$9,500. They wish to sell their current 3-room HDB flat in Jurong West (fully paid off at S$480,000) and upgrade to a 4-room resale HDB flat in Tampines North, targeting proximity to Temasek Polytechnic where Mrs Ng works.

They identify a 4-room resale flat on the 12th floor of a Tampines North block with a remaining lease of 72 years, listed at S$660,000.

Stamp duties: BSD on S$660,000 — first S$180,000 at 1% = S$1,800; next S$180,000 at 2% = S$3,600; next S$300,000 at 3% = S$9,000. BSD = S$14,400. ABSD: nil — SC married couple, concurrent sale of existing HDB means property count stays at one.

Grants: At S$9,500 joint income, EHG for resale is S$15,000. PHG: if Tampines North is within 4 km of Mrs Ng’s parents’ home in Pasir Ris — qualifying distance — PHG = S$20,000 (living near parents). Total grants = S$35,000. Net effective price = S$660,000 − S$35,000 = S$625,000.

Financing: HDB concessionary loan LTV 80% = S$500,000. Monthly instalment: S$500,000 at 2.6% over 25 years ≈ S$2,274/month. MSR: S$2,274 / S$9,500 = 23.9% — within the 30% MSR limit. TDSR: 23.9% — well within 55%. Cash upfront (5% cash + BSD): S$33,000 + S$14,400 = S$47,400.

Outcome: The Ngs can feasibly complete the purchase, using the S$480,000 proceeds from their Jurong West flat to fund the upfront costs and CPF top-up, with the CRL opening in 2030 providing a potential capital gain catalyst within their 10-year holding horizon.

What Might Come Next for Tampines North

The structural story for Tampines North is the CRL. Once the Cross Island Line Tampines North station opens (~2030), the area transitions from “well-connected east sub-town” to “triple-line MRT hub” — a designation shared by fewer than ten stations in Singapore. The immediate consequence is typically a rental yield compression (higher prices) and a transaction volume uplift as buyers from outside the east discover the area.

Beyond CRL, the URA Master Plan 2025 identifies a stretch of land near Sungei Loyang — northeast of Tampines North — as a potential new neighbourhood study area. An environmental study is underway; if positive, this could yield an additional residential supply pipeline of several thousand units beyond 2030, including park space and community facilities that would benefit Tampines North residents further north.

For existing Tampines residents, the advice is to document their lease adequacy carefully: flats with remaining leases dropping below 60 years within a 20-year horizon will lose CPF financing eligibility, which progressively reduces the buyer pool for those units on resale. This is a watch-point particularly for older blocks in the southern part of Tampines town.

Frequently Asked Questions

Is Tampines North a good area to buy property in 2026?

For buyers with a 7-10 year investment horizon, Tampines North has a credible structural case built on the CRL opening (~2030), strong rental demand from UWCSEA and TP, one of Singapore’s best OCR retail hubs, and prices that remain below RCR comparables for similar connectivity. Short-term buyers should be aware that private condo prices in Tampines North are already partly pricing in the CRL uplift, particularly Parktown Residence. HDB resale buyers get better value relative to future connectivity than private condo buyers.

Which MRT lines serve Tampines North?

As of 2026, Tampines North is served by the East-West Line (EWL) at Tampines (EW2) and the Downtown Line (DTL) at Tampines (DT32). Both stations share a common paid concourse. The upcoming Cross Island Line (CRL) Tampines North station, targeted around 2030, will add a third line specifically serving the northern sub-town and integrated with Parktown Residence. Simei (EW3) on the EWL also serves the southern edge of Tampines North.

Can foreigners buy property in Tampines North?

Foreign individuals (non-PRs) may purchase private condominium units in Tampines North, such as Parktown Residence, subject to the 65% Additional Buyer’s Stamp Duty (ABSD) on the purchase price. Singapore PRs buying their first property pay 5% ABSD. Foreigners and PRs cannot purchase HDB flats or executive condominiums below 10 years old (except PRs buying resale HDB with a Citizen spouse). The 65% ABSD rate was introduced in April 2023 and remains in force as of June 2026.

What is Parktown Residence and how is it different from a regular condo?

Parktown Residence is a 1,193-unit 99-year leasehold integrated development co-developed by UOL Group, CapitaLand, and HDB, launched in 2025. “Integrated” in this context means it is physically connected to the Tampines North MRT station (CRL), a hawker centre, a community club, and a retail precinct within a single development. Residents will have sheltered, direct access to the CRL station without going to street level. This is similar to the Bidadari integration model (Woodleigh Residences + Woodleigh MRT) and commands a moderate premium over non-integrated private condos nearby.

How does Tampines North compare to nearby Bedok or Pasir Ris for property investment?

Tampines North has a younger housing stock on average than Bedok (where many leases are entering the 40-50 year range) and a cleaner CRL catalyst story than Pasir Ris (which benefits from the EWL and the Pasir Ris-Punggol Regional Line, but has already partly priced in those upgrades). Bedok offers more mature amenities and better CBD commute times via the EWL, while Pasir Ris offers more land area and green space. Tampines North is the strongest play for buyers specifically betting on the CRL station uplift over a 5-10 year horizon.

What income is needed to buy a condo in Tampines North in 2026?

For a 2-bedroom private condo in Tampines North at approximately S$1.2M, assuming a bank loan at LTV 75% and a 30-year tenure at 3.0% per annum: the loan quantum is S$900,000 and the monthly instalment approximately S$3,795. Under TDSR at 55%, the required gross monthly income is approximately S$6,900. In practice, lenders typically want comfortable headroom, so a combined household income of S$10,000–S$12,000 per month is advisable for sustainable financing at this quantum. Cash/CPF available for the downpayment (25%) plus BSD should be in the S$320,000–S$350,000 range.

Related Articles

- First-Time Property Buyer Guide Singapore 2026

- ABSD Singapore 2026 — Complete Guide

- CPF Property Withdrawal Limits Singapore 2026

- Serangoon Neighbourhood Guide Singapore 2026

- Bedok Neighbourhood Guide Singapore 2026

- Singapore Property Rental Guide 2026

Disclaimer: This article provides general information about the Tampines North property market as at 3 June 2026. Property prices, yields, and infrastructure timelines are indicative and subject to change. This is not investment advice. Refer to official sources including URA, HDB, and LTA for authoritative figures, and consult a licensed property agent and financial adviser before making any property purchase decision.