Novena Neighbourhood Guide Singapore 2026: D11 Medical Hub, Prices & Investment Outlook

- District 11 (D11) — Newton and Novena planning areas in the Core Central Region (CCR). Almost entirely private residential.

- Freehold condos average S$2,600–3,200 psf in Q1 2026; 99-year leasehold condos range from S$2,100–2,600 psf.

- Medical hub demand: Mount Elizabeth Hospital, Mount Elizabeth Novena Hospital, and Tan Tock Seng Hospital (TTSH) generate sustained rental demand from healthcare professionals and medical tourists.

- MRT connectivity: Novena (North South Line) and Newton (NSL + Downtown Line) provide direct access to Raffles Place, Marina Bay, and Orchard Road.

- Gross rental yield: approximately 2.5%–3.2% for condos, comparable to other prime CCR districts.

- Supply constraint: no new Government Land Sales (GLS) sites have been released in D11 since 2019, reinforcing price resilience for existing freehold stock.

- Ideal buyer: upgraders, medical professionals, expatriate tenants, long-term capital preservation investors.

What Makes Novena Singapore’s Medical Hub Precinct?

Novena sits within District 11 — one of Singapore’s most established and tightly held residential precincts. Bounded roughly by Thomson Road to the north, Bukit Timah Road to the west, Newton Circus to the south, and Balestier Road to the east, D11 is home to a cluster of private hospitals that is unmatched anywhere else on the island. Mount Elizabeth Hospital on Orchard Road, its sister facility Mount Elizabeth Novena Hospital on Novena Rise, and Tan Tock Seng Hospital on Moulmein Road together form Singapore’s largest private medical hub. This concentration of world-class healthcare institutions is not just a lifestyle amenity — it is a structural driver of residential demand.

Medical professionals, hospital support staff, and visiting doctors on short-term rotations all need housing within comfortable distance of these facilities. International patients and their families, many from across Southeast Asia, the Middle East, and China, often prefer to base themselves in Novena rather than Orchard so they can be close to treatment. The result is a rental market that is unusually resilient even during broader property downturns, because hospital activity does not follow the economic cycle in the same way that corporate leasing does.

Beyond healthcare, Novena offers the quiet residential character of the old Central Region without the intensity of Orchard Road. United Square on Thomson Road is Singapore’s best-known education mall, drawing families with school-age children. Novena Square 1 and 2 and Square 2 along Thomson Road provide everyday retail and dining. St. Joseph’s Institution International, Anglo-Chinese School (Primary), and the Singapore Chinese Girls’ School are all within close proximity, adding an education premium on top of the medical one.

D11 Property Price Ranges — What Buyers Pay in 2026

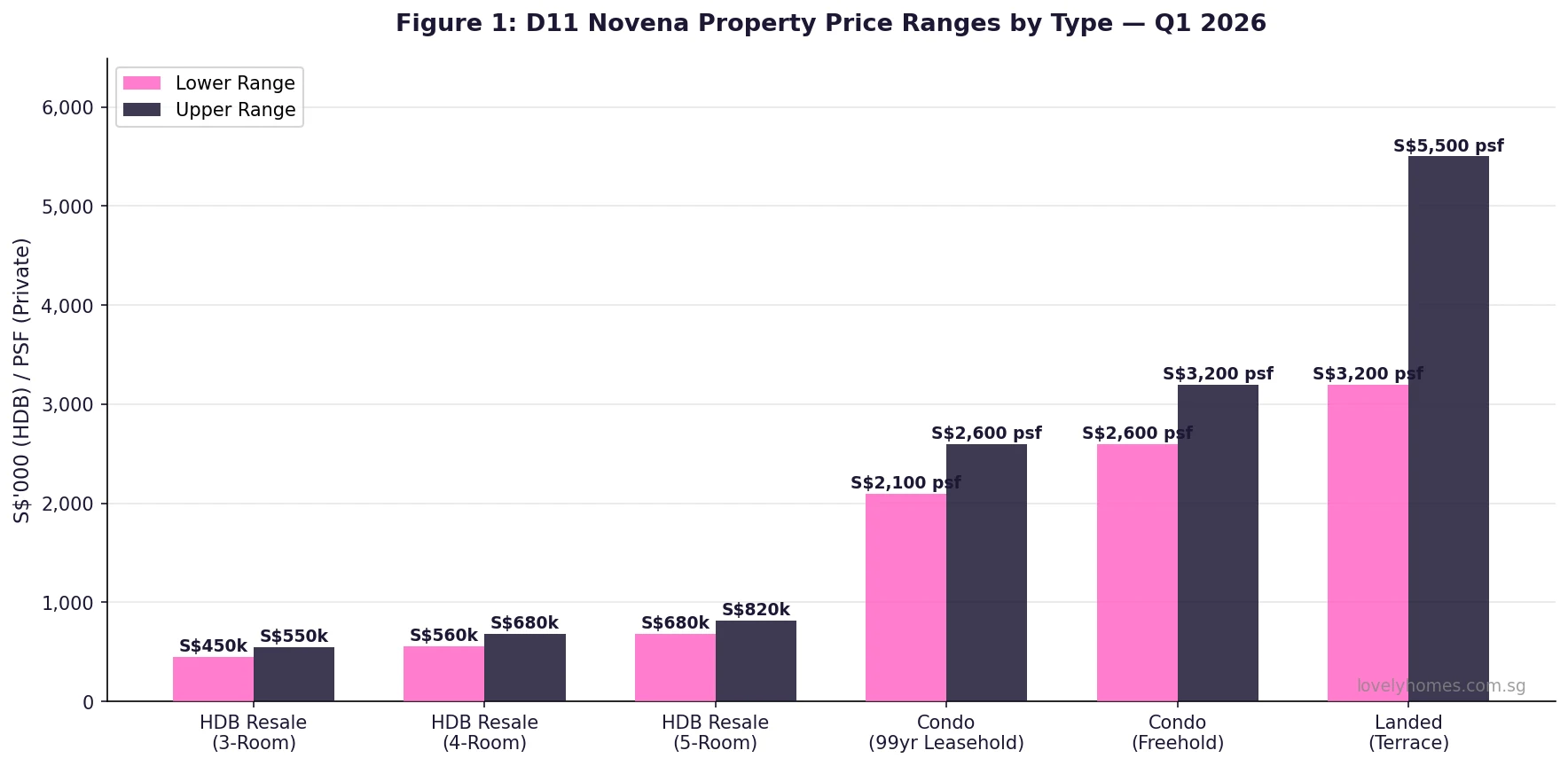

Figure 1: D11 Newton/Novena residential property price ranges by type — Q1 2026. HDB resale figures reflect fringe estates (Moulmein/Thomson). Sources: URA REALIS, HDB Resale Portal Q1 2026.

District 11 is overwhelmingly private residential. The handful of HDB resale flats that fall within or immediately adjacent to the planning area — mainly in the Moulmein and Newton fringe — transact at a premium to equivalent flat types elsewhere, given their central address. A 4-room HDB resale in this catchment has fetched S$560,000–680,000 in Q1 2026, reflecting the locational scarcity: only a few hundred HDB flats exist across the entire D11 footprint.

The dominant residential product in D11 is the private condo. Freehold condos — which make up the majority of stock given the age of development — have held between S$2,600 and S$3,200 psf in Q1 2026. Key developments such as City Square Residences (freehold, Kitchener Road), Novena Regency (freehold, Thomson Road), and The Trizon (freehold, off Mount Sinai) sit in this range. Newer 99-year developments have traded at a 15–20% discount to equivalent freehold stock, at S$2,100–2,600 psf, reflecting the leasehold haircut that remains deeply ingrained in Singapore buyer psychology.

Landed property in D11 — predominantly terrace and semi-detached houses in the Upper Thomson and Spring Road areas — commands S$3,200–5,500 psf on land area depending on remaining lease, configuration, and orientation. Good Class Bungalow (GCB) plots in the adjacent Ridout Road and Nassim areas start well above S$15 million for eligible parcels.

| Property Type | Typical Size | Price From | Price To | Notes |

|---|---|---|---|---|

| HDB Resale (3-Room) | 65–70 sqm | S$450,000 | S$550,000 | Moulmein/Newton fringe only |

| HDB Resale (4-Room) | 90–100 sqm | S$560,000 | S$680,000 | Moulmein/Newton fringe only |

| Condo 1-Bed (FH) | 45–55 sqm | S$1,200,000 | S$1,600,000 | Strong rental demand from medical staff |

| Condo 2-Bed (FH) | 75–95 sqm | S$1,700,000 | S$2,400,000 | Most liquid unit type in D11 |

| Condo 3-Bed (FH) | 120–150 sqm | S$2,800,000 | S$4,200,000 | Family-friendly, education catchment |

| Landed Terrace (FH) | 150–200 sqm land | S$3,200 psf land | S$5,500 psf land | Only Singapore Citizens eligible |

Location and Connectivity: MRT, TEL and Road Networks

Figure 2: Novena D11 — key neighbourhood facts for property buyers and investors, 2026.

Novena station on the North South Line (NSL) gives residents a 4-minute train ride to Toa Payoh and a 6-minute ride to Orchard. Newton interchange station — one of only five interchange stations on the NSL — connects to the Downtown Line (DTL), enabling direct access to Buona Vista, one-north, and the Botanic Gardens without a transfer. Journey times to Raffles Place run at approximately 13–15 minutes, making D11 one of the best-connected residential precincts for CBD workers in Singapore.

The Thomson-East Coast Line (TEL) has further enhanced D11’s connectivity position without D11 itself sitting on the new line. Stevens interchange (TEL + DTL, opened December 2022) is a 5-minute drive or short bus ride from Novena, linking residents to TE1 (Woodlands North) and the full TEL corridor south through Stevens, Napier, Orchard Boulevard, and Orchard into the eastern spine. For Novena residents, TEL Stage 4’s opening in 2024 — connecting Founders’ Memorial, Tanjong Rhu, and the East Coast corridor — extended journey time savings for those commuting eastward.

By road, the Central Expressway (CTE) entrance at Moulmein Road provides fast north-south access. The Pan Island Expressway (PIE) junction at Adam Road is under 10 minutes from Novena. These road links are especially valued by residents who need to reach Changi Airport, the western industrial corridor, or the north.

The Medical Hub Premium: Why Hospitals Drive Novena Property Values

Singapore’s position as Southeast Asia’s foremost medical tourism destination directly benefits D11 landlords. Mount Elizabeth Novena Hospital — a 333-bed private tertiary hospital opened in 2012 by Parkway Pantai — anchors the Novena Specialist Centre cluster along Irrawaddy Road, home to more than 200 specialist clinics. Tan Tock Seng Hospital, Singapore’s second-largest public acute care hospital with approximately 1,700 beds, generates thousands of shift-based healthcare workers who need residential options within cycling or walking distance.

The practical implication is a rental market that outperforms broader D11 yield expectations in the sub-S$5,000/month segment. A typical 1-bedroom freehold condo (50–55 sqm) in Novena commands S$3,800–4,500/month, yielding approximately 2.8–3.2% gross on an acquisition cost of S$1.4–1.6 million. Two-bedroom units (80–95 sqm) attract medical families and senior specialists, renting at S$5,500–7,000/month for a gross yield of 2.5–3.0% on a S$2.0–2.4 million entry price.

This yield compression relative to fringe districts reflects the capital value premium commanded by CCR freehold stock — buyers are partly paying for capital preservation and the scarcity of new supply, not just income return. Investors who entered D11 between 2017 and 2020 and chose freehold units are now sitting on total returns (rental + capital appreciation) of approximately 30–45% over six years, comfortably outperforming CPF Ordinary Account returns and most balanced investment portfolios.

D11 Condo Price Trend 2019–2026

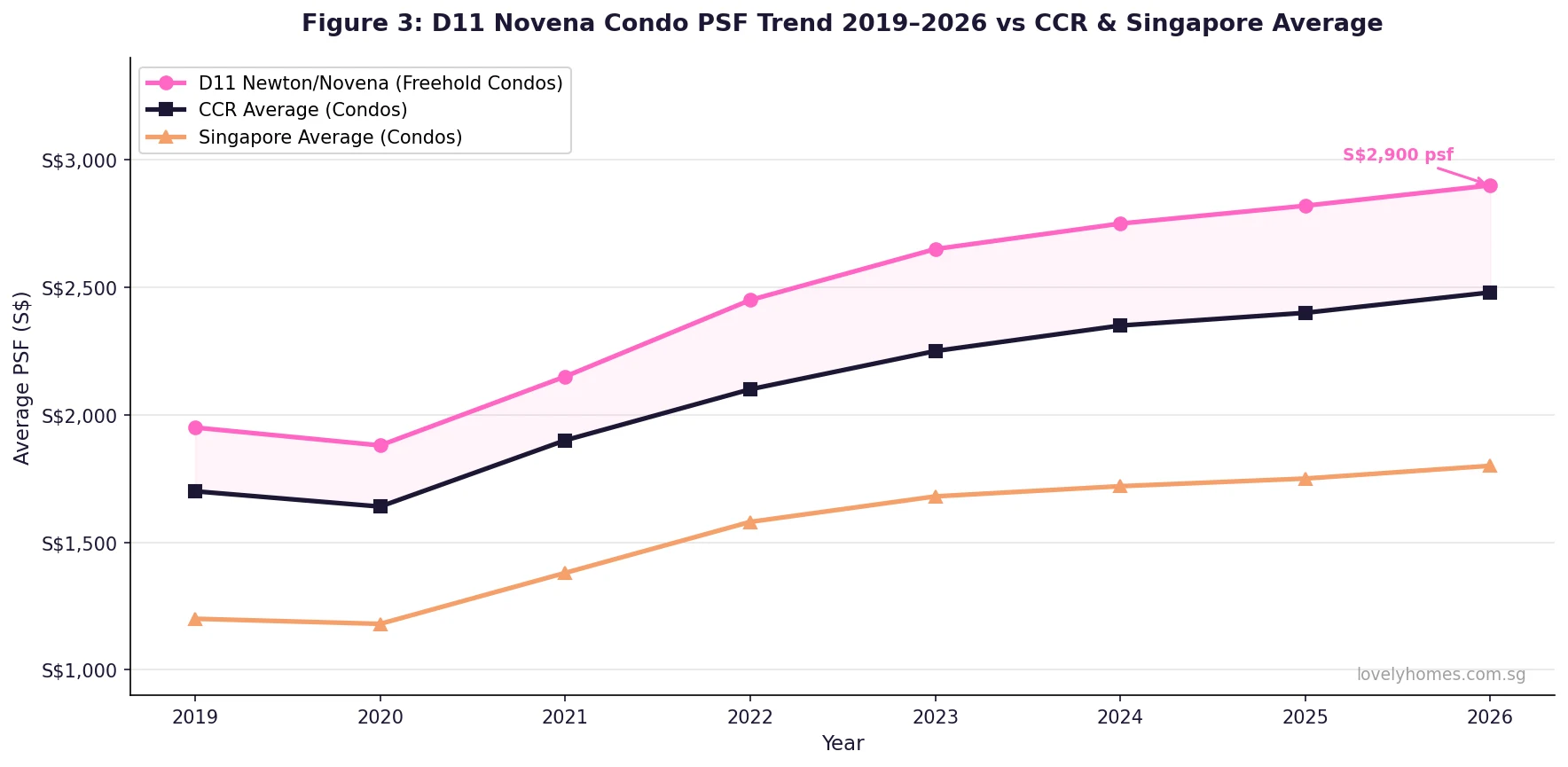

Figure 3: D11 Newton/Novena average condo PSF trend 2019–2026 versus CCR and Singapore overall average. Source: URA REALIS, LovelyHomes analysis.

The chart above illustrates D11’s trajectory over the past seven years. Starting from roughly S$1,950 psf in 2019, freehold D11 condos contracted slightly during the pandemic-affected 2020 period before recovering strongly through 2021–2022 on the back of Singapore’s post-Covid reopening and a structural shift in buyer demand toward quality freehold assets. By 2023, D11 average freehold condo PSF had crossed S$2,600 psf for the first time. The 2022 and 2023 ABSD increases tempered transaction volumes — particularly for foreigners and second-property buyers — but did not dent per-unit pricing meaningfully, as supply in D11 is too constrained for any oversupply dynamic to emerge.

The shaded pink band in Figure 3 represents the D11 freehold premium over the broader CCR average. This premium has widened from approximately S$250 psf in 2019 to over S$420 psf in Q1 2026, reflecting both the structural scarcity of freehold stock in D11 and growing buyer preference for fully private, low-density living with minimal commercial encroachment.

Worked Example: Buying a 2-Bedroom Freehold Condo in Novena

📋 Case Study: Mr & Mrs Lee (SC/SC) — 2-Bed Freehold Condo, Novena, S$2,100,000

Profile: Singapore Citizens, first property purchase for both, combined gross income S$14,000/month. Buying a 2-bedroom freehold condo in Novena at S$2,100,000 for owner-occupation, no existing properties.

- ABSD: S$0 (SC buying first residential property — no ABSD)

- BSD (Buyer’s Stamp Duty):

- 1% on first S$180,000 = S$1,800

- 2% on next S$180,000 = S$3,600

- 3% on next S$640,000 = S$19,200

- 4% on next S$500,000 = S$20,000

- 5% on next S$600,000 = S$30,000 (i.e. 2,100k less 1,500k threshold)

- Total BSD: S$74,600 (effective 3.55%)

- Loan: 75% LTV = S$1,575,000. At 3.5% p.a. over 25 years → monthly repayment ≈ S$7,882

- TDSR check: S$7,882 / S$14,000 = 56.3% — exceeds the 55% TDSR limit. FAIL.

- Resolution: Increase down payment to 35% (S$735,000), reducing loan to S$1,365,000 (65% LTV). Monthly repayment ≈ S$6,830. TDSR = 48.8% — PASS.

- Or: Look at 99yr leasehold option at S$1,750,000 — TDSR at 75% LTV = S$6,568/mth = 46.9% — PASS with standard down payment.

- Total upfront (with increased 35% down payment + BSD + legal fees ~S$8,000): approximately S$817,600

This example illustrates that D11 freehold condos at S$2M+ often push buyers to the TDSR boundary. Buyers with household income below S$13,000/month should model carefully before committing to prime CCR property at full 75% LTV.

What This Means for You: Investment Outlook for Novena 2026

D11’s investment case rests on three pillars: supply scarcity, institutional demand from the medical cluster, and the freehold tenure of the majority of its stock. No new GLS residential sites have been released in D11 since 2019, and URA’s long-term planning approach for the Novena area — classified as a Medical and Healthcare Hub in the 2019 Concept Plan — is to intensify medical uses rather than add residential supply. This means existing condo owners benefit from a structurally undersupplied rental market.

Peer-country comparison is instructive: Singapore’s medical tourism arrivals have recovered to pre-2020 levels and are projected to grow at 6–8% per year through 2030, according to Singapore Tourism Board data. Bangkok’s Sukhumvit medical precinct and Kuala Lumpur’s Bangsar medical cluster — both D11 comparators — trade at significantly lower absolute values but have shown similar rental demand dynamics when anchored by hospital clusters.

The 2023 ABSD increase to 20% for Singapore Citizens purchasing their second property has been the primary headwind, reducing the pool of upgrader-investors who would previously have held a D11 condo as a rental asset. However, institutional landlords, family offices, and HNW individuals — many of whom hold D11 property through structures exempt from or partially insulated from ABSD — have partially absorbed this demand withdrawal. Transaction volumes in D11 are lower than 2021–2022 peaks but prices have held firm.

For owner-occupiers, Novena remains one of Singapore’s best-value CCR living addresses on a “livability per dollar spent” basis: lower psf than Orchard/River Valley (D09/D10), with arguably better day-to-day amenities (healthcare, education, F&B) and equivalent MRT connectivity. First-time buyers with sufficient income ($13,000+/month household) priced out of Orchard condos will increasingly look to D11 freehold units as a value entry point into the CCR.

What Might Come Next for Novena?

URA’s Draft Master Plan 2025 (public consultation 2025–2026) has not released any residential-zoned GLS parcels within D11. The long-term direction for Novena is healthcare intensification: the Novena Health City vision positions the precinct as a full-service integrated medical district, with possible expansion of outpatient facilities and specialist centres along Irrawaddy Road and Balestier. Any rezoning of existing commercial or industrial sites in the area for residential use would be a meaningful catalyst — but industry observers see this as unlikely before 2030.

In the shorter term, the broader TEL completion in 2025 (Stages 4–5) and the continued growth of the Cross Island Line (CRL) network — which brings better connectivity to D11 feeder suburbs — are expected to sustain buyer appetite for CCR property including D11. If Singapore’s government chooses to recalibrate ABSD for second properties (reducing the 20% SC rate) as part of a future cooling-measures review, D11 would be among the prime beneficiaries given its investor-grade stock base.

Frequently Asked Questions: Buying Property in Novena

Are there HDB flats available in Novena for purchase?

Very few. D11 is almost entirely private residential, with only a small number of HDB resale flats in the Moulmein and Thomson fringe of the district. Buyers seeking public housing close to D11 typically look at nearby Toa Payoh (D12) or Novena-adjacent blocks in Moulmein Road. There are no BTO launches planned for D11 given the Master Plan’s designation of the area as a Medical and Healthcare Hub.

Can foreigners buy property in Novena?

Foreigners (non-Singapore Citizens and non-Permanent Residents) may purchase private condominiums (strata-titled, non-landed) in D11, including Novena, subject to paying Additional Buyer’s Stamp Duty (ABSD) of 60% on the purchase price as of April 2023. Landed property in D11 is restricted to Singapore Citizens only, with limited exceptions requiring Singapore Land Authority (SLA) approval for Permanent Residents in non-GCB landed categories.

What is the ABSD rate for a second property purchase in Novena?

As at 1 July 2026, a Singapore Citizen purchasing a second residential property pays ABSD of 20% on the purchase price. A Permanent Resident buying a first property pays 5% ABSD. A foreign buyer pays 60%. There is no ABSD for a Singapore Citizen purchasing their first residential property. For a D11 condo priced at S$2.0 million, the ABSD for a SC second-property purchase would be S$400,000 — a significant holding cost that most investors factor into their return model before committing.

What is the typical rental yield for condos in Novena?

Gross rental yields for condominiums in D11 Newton/Novena typically range from 2.5% to 3.2% per year in 2026, depending on unit size, floor level, and age of development. Smaller 1-bedroom units (45–55 sqm) tend to achieve the highest yields (2.9–3.2%) due to strong demand from single medical professionals, while larger 3-bedroom family units yield closer to 2.5% gross. Net yields after maintenance fees, property tax, and agent fees are typically 0.5–0.8% lower than gross.

What is the Minimum Occupation Period (MOP) for a condo in D11?

Private condominiums do not have a Minimum Occupation Period (MOP) requirement. Only HDB flats are subject to MOP (5 years for Standard flats, 10 years for Prime and Plus BTO flats). Private condo owners may rent out their unit from day one of ownership, provided they comply with URA tenancy regulations including the 3-month minimum rental period. This makes D11 condos immediately income-generating for buyers who intend to lease the property out.

How does Novena compare to Orchard Road (D09/D10) for property investment?

Novena (D11) generally offers lower entry prices than Orchard (D09) and River Valley (D10) at equivalent quality levels, with freehold condos in D11 averaging S$2,600–3,200 psf versus D09/D10 freehold at S$3,200–4,500 psf. Rental yields are comparable (2.5–3.2% across both zones). D11 benefits from the medical hub demand driver, which is more stable than the expatriate corporate demand that historically underpinned D09/D10 rentals. Buyers seeking CCR exposure with lower absolute outlay and a differentiated demand driver typically favour D11 over D09/D10.

Is Novena suitable for families with school-age children?

Yes — D11 is one of Singapore’s best-positioned districts for families prioritising education access alongside healthcare. Anglo-Chinese School (Primary) is located off Barker Road within the district. The Singapore Chinese Girls’ School (SCGS) is on Emerald Hill in adjacent D10. St. Joseph’s Institution International (SJI International) on Malcolm Road serves the international school market. United Square on Thomson Road is Singapore’s premier education-focused mall, housing enrichment centres, tuition providers, and learning-focused retail. Proximity to the Botanic Gardens (5 minutes by car) adds park space for families.