HPS Mortgage Insurance Singapore 2026: Home Protection Scheme, MRTA & When to Opt Out

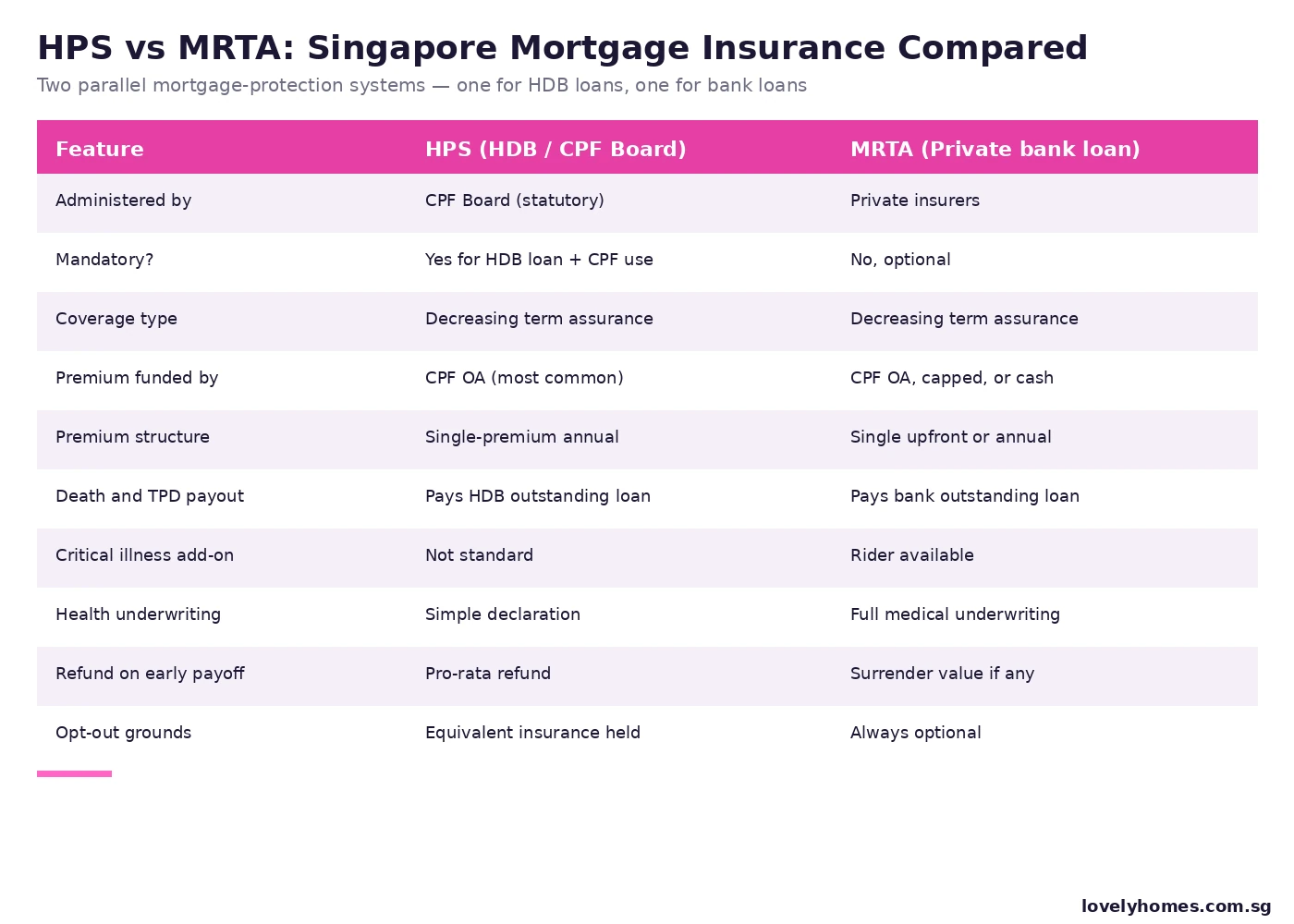

When you buy a Singapore home, the lender is not the only party who wants to be sure the loan gets repaid. The state, your family, and your CPF balance all have a stake — which is why mortgage insurance is built into the rules, not bolted on later. Singapore runs two parallel systems: the Home Protection Scheme (HPS) for HDB-loan flats, administered by the CPF Board, and Mortgage-Reducing Term Assurance (MRTA) for private bank loans, sold by commercial insurers. They look similar but behave very differently — and choosing wrong can cost you S$300 to S$1,200 a year, or worse, leave your spouse holding a six-figure loan.

Quick Answer

- HPS is mandatory for any flat owner servicing an HDB loan and using CPF for repayments — no exceptions unless you can prove equivalent cover.

- MRTA is optional on bank loans, but most lenders strongly encourage it, and you can often pay the premium with CPF (subject to caps).

- Both pay the lender first on death or total permanent disability (TPD). Only what is left after settling the loan reaches your estate.

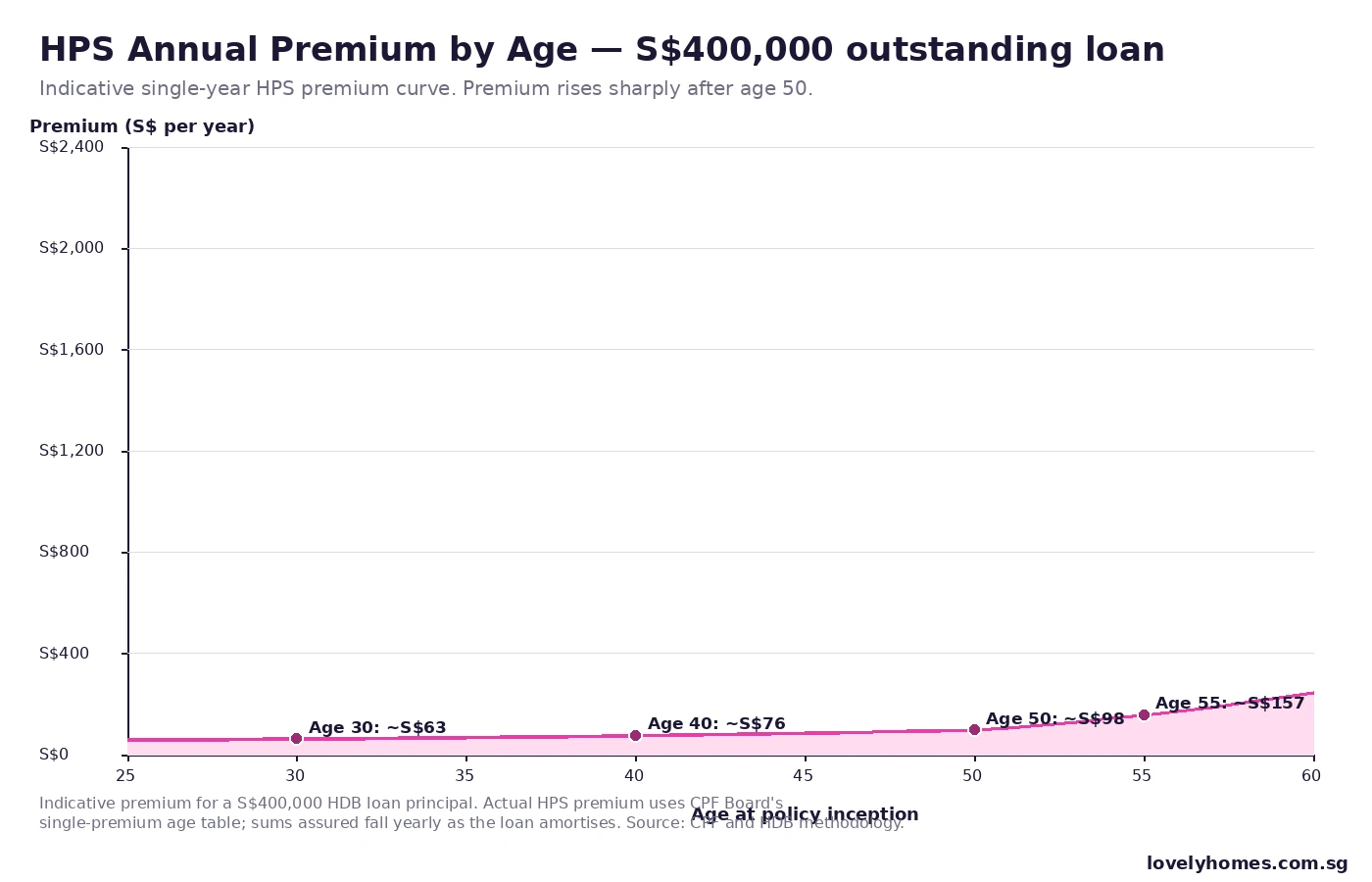

- HPS premium rises sharply after age 50 — a 30-year-old pays roughly S$200 to S$400 a year on a S$400,000 loan; a 55-year-old can pay over S$1,800.

- Opt-out is allowed only if you hold a separate life policy that covers the outstanding HDB loan and names the lender or estate appropriately.

- MRTA can carry critical-illness or retrenchment riders; HPS cannot. For older buyers or self-employed earners, the rider economics often beat HPS.

- If you redeem the HDB loan early, CPF Board refunds a pro-rata HPS premium. MRTA’s surrender value depends on the policy.

What HPS actually is — and why it exists

The Home Protection Scheme is a statutory mortgage-reducing decreasing term insurance administered by the CPF Board. Every owner who services an HDB loan and uses CPF Ordinary Account (OA) for repayments must be covered, with sums assured equal to the outstanding HDB loan and a coverage period matching the remaining loan tenure (capped at age 65). When a covered owner dies or is certified TPD, CPF Board pays the outstanding HDB loan on the deceased’s share — so the surviving family inherits a flat that is unencumbered to the extent of the deceased’s HPS share.

HPS exists because the policy intent of public housing is to keep families housed even after a tragedy. Without HPS, a sudden death could force a forced sale to clear the HDB mortgage, exactly when the family can least afford to move. The trade-off is mandatory enrolment — and a premium schedule that rises with age and outstanding loan size.

What MRTA covers and where it differs

MRTA is the private-market analogue: a decreasing term-life policy underwritten by a commercial insurer, sized to your bank-loan amortisation. Unlike HPS, MRTA is voluntary, requires full medical underwriting rather than a simple declaration, and offers the flexibility of single-premium upfront payment (often funded out of the bank loan itself or your CPF OA up to a cap) or annual premiums.

The key practical edges MRTA has over HPS:

- Critical illness (CI) rider — pays out on a covered diagnosis (cancer, heart attack, stroke and a defined list) before death. HPS does not offer this.

- Retrenchment or disability income riders — keep paying instalments for 6 to 12 months on involuntary unemployment.

- Smoker / non-smoker pricing — a healthy young non-smoker can be priced below HPS, especially for large bank loans.

- Joint policies — couples can buy a single MRTA covering both lives, with the loan paid on the first death.

How HPS premiums are calculated

HPS uses a single-premium annual model: each year the CPF Board recalculates your premium based on your age (next birthday), the outstanding loan, your share of ownership, and the remaining tenure. The single premium can be paid from CPF OA (most common) or in cash. Because the sum assured falls each year as you amortise the loan, the premium tends to plateau or fall mildly through your 30s and 40s, before rising sharply through your 50s and into early 60s.

The shape of the curve is the most important number for buyers to internalise. A 30-year-old buying a S$400,000 HDB-loan flat might pay around S$210 in year one. The same flat held by a 55-year-old refinancing across to a longer tenure could see HPS premium hit S$1,800 a year — a 9-fold gap that compounds across the loan term.

CPF use, eligibility and payout mechanics

HPS premium can be paid from CPF OA without breaching the broader CPF housing limits — it is treated as an essential cost of using CPF for housing. MRTA can also be funded from CPF OA, but the amount is capped (typically by the lender’s policy and the CPF Board’s housing rules), and any excess must be in cash.

On a death claim, both schemes pay the lender first. The HPS payout is calculated on the deceased’s ownership share of the flat — so a 50/50 couple sees HPS settle 50% of the outstanding HDB loan on the first death, leaving the survivor responsible for the remaining 50%. This is why most mortgage planners recommend HPS coverage be sized to your full share of the loan, not just half.

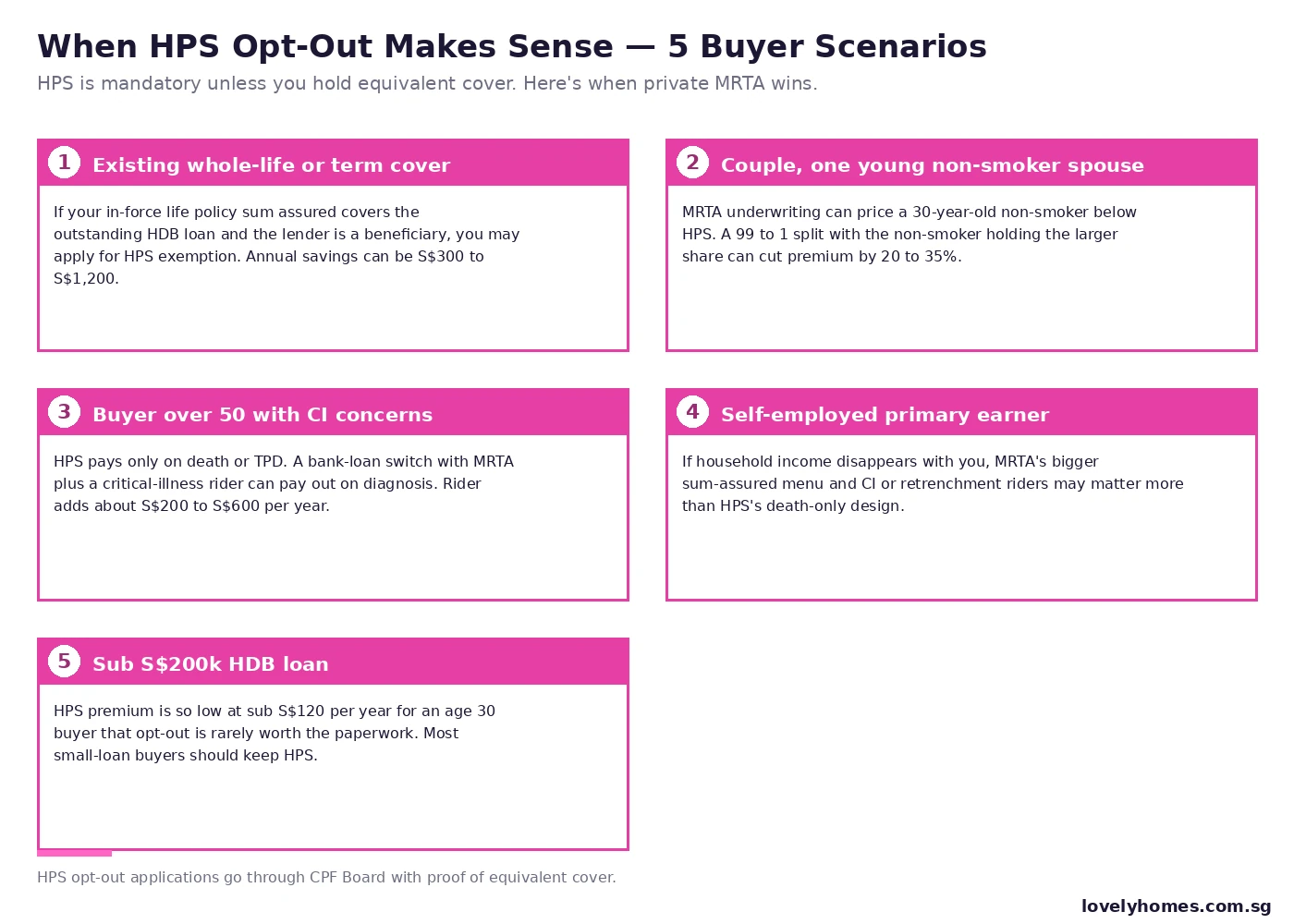

Opt-out: who qualifies and how

HPS is mandatory by default, but the CPF Act allows opt-out where the owner already holds equivalent insurance. In practice, “equivalent” means a life or term-assurance policy with sum assured at least equal to the outstanding HDB loan, naming a beneficiary structure that ensures the proceeds clear the loan on death — usually by naming the lender or the estate. Whole-life, term, and Group Term Life policies issued by employers can all qualify, subject to the policy term and sum assured tests.

The application is filed with CPF Board with a copy of the in-force policy schedule. Approval typically takes 4 to 6 weeks. If your equivalent policy lapses, you must rejoin HPS — at the age you are then, which may be considerably more expensive.

Summary table — at-a-glance feature comparison

The matrix below condenses the most-asked questions into a single summary view. Use it as the quick reference; the worked example below brings the numbers to life.

| Dimension | HPS | MRTA |

|---|---|---|

| Required for HDB loan | Yes | No (HPS applies) |

| Required for bank loan | No | Optional, encouraged |

| Age 30 indicative premium (S$400k loan) | ~S$210/yr | ~S$180–S$320/yr |

| Age 50 indicative premium | ~S$1,100/yr | ~S$650–S$1,200/yr |

| CI rider available | No | Yes (~S$200–S$600/yr) |

| Underwriting | Health declaration only | Full medical |

| Smoker loading | No | Yes (15–35%) |

| Premium fundable from CPF OA | Yes | Yes (capped) |

| Refund on early loan payoff | Pro-rata | Surrender value if applicable |

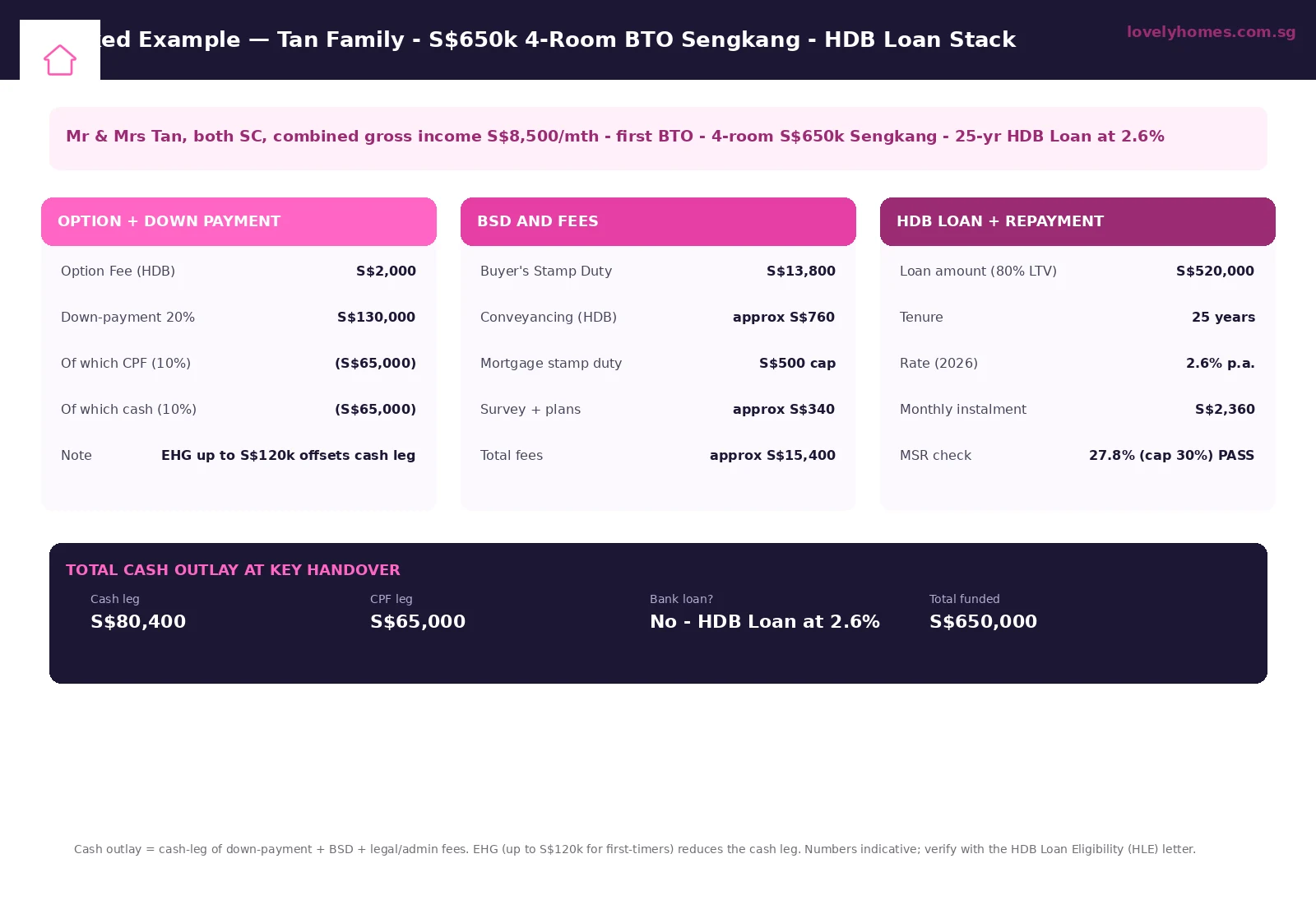

Worked Example: Mr and Mrs Tan, age 35, S$520,000 HDB loan

Profile. Tan, 35 (non-smoker), and Mrs Tan, 33 (non-smoker). Both Singapore Citizens, joint owners (50/50) of a S$650,000 4-room BTO in Sengkang, financed with a S$520,000 HDB concessionary loan over 25 years at 2.6% interest.

Default HPS path. Both spouses enrol in HPS at policy inception, each covering 50% (S$260,000) of the outstanding loan on their share. CPF Board’s age-35 single premium for a S$260,000 sum assured comes to roughly S$165 per spouse per year in year one — about S$330 combined. Premiums fall slowly through their 30s, plateau in the 40s, then rise into the 50s.

Alternative MRTA path. Both Tans hold a S$300,000 30-year level-term policy from before the BTO purchase, with sums assured already exceeding their HDB-loan share. Filing for HPS opt-out with CPF Board (typically 4 to 6 weeks) eliminates the HPS premium entirely. Annual saving in year one: S$330. Over a 25-year horizon, with HPS premiums rising into the 40s and 50s, the cumulative saving is approximately S$18,000 to S$24,000 in nominal terms.

Caveat. The opt-out only holds while the equivalent policies are in force. If either Tan’s term policy lapses or is cancelled, CPF Board requires immediate re-enrolment in HPS at the prevailing age — which by then could be 45 or 50, with premiums an order of magnitude higher.

What this means for you

For most young HDB buyers, HPS is exactly the right product: low premium, simple paperwork, no medical underwriting, and a state-administered safety net for the family. Trying to “optimise” it can quickly turn into false economy — especially if your existing life cover is only just large enough today and might not be tomorrow.

For older buyers, self-employed primary earners, or households with health-screening concerns ahead of a remortgage, the calculation changes. MRTA’s CI rider, smoker / non-smoker pricing differential, and the ability to lock in a single-premium policy at today’s age can compound into meaningful five-figure savings over a 20-year tenure. Run both quotes through the worked-example structure above before committing.

What might come next

The CPF Board reviews HPS premium tables periodically. With Singapore’s mortality assumptions improving and longevity stretching beyond age 85, the long-run direction of HPS premiums for younger buyers is broadly flat to slightly down, while older-age premiums may face upward pressure as more borrowers stretch tenures into their late 60s. Industry observers also expect the private MRTA market to continue expanding CI rider coverage and adding mental-health and severe-disability triggers — a useful tailwind for buyers who can underwrite cleanly today.

Separately, with the Plus and Prime flat categories taking root since August 2024, the universe of HDB-loan buyers will increasingly skew younger and tied to longer 10-year MOPs. That suggests HPS will remain the dominant cover for at least the next decade, with private MRTA growing its share among bank-loan EC buyers and refinancers above 45.

FAQ

Is HPS the same as life insurance?

No. HPS is a mortgage-reducing decreasing term assurance tied to your HDB-loan balance. The sum assured falls each year as the loan amortises, and HPS pays only on death or TPD — not on critical illness, hospitalisation or retrenchment. It is best thought of as protection for the bank, not protection for the family’s lifestyle. You still need separate life and CI cover for those.

Can I use CPF to pay HPS or MRTA premiums?

HPS premium is paid out of CPF OA by default — you do not need to top up cash unless your OA is depleted. MRTA premiums can also be funded from CPF OA up to a cap; any excess must be paid in cash. This makes HPS slightly more “cash-flow friendly” for younger buyers with healthy OA balances, even before comparing premium tables.

What happens if my spouse is uninsurable?

HPS uses a simple health declaration rather than full medical underwriting, so it accepts most applicants who can answer “no” to a small set of yes / no questions. If your spouse is medically declined for MRTA — for example, due to a chronic condition — HPS often becomes the only practical cover and is therefore precious. Plan accordingly: opt-out is rarely the right answer if one spouse is borderline insurable.

Does HPS pay out if I’m diagnosed with cancer?

Only if the cancer leads to death or to a state of total permanent disability as defined by CPF Board. HPS does not pay on diagnosis. If CI cover is important to you — and for buyers over 45 it usually is — pair HPS or MRTA with a separate CI rider or standalone CI policy, sized to the loan and ideally to a year or two of household income.

Can I switch from HPS to MRTA after buying?

Only by refinancing your HDB loan over to a bank loan and applying for HPS exemption with proof of equivalent cover. Once refinanced to a bank loan, HPS no longer applies (it covers HDB-loan flats only). This is an irreversible direction — once on a bank loan, you cannot return to an HDB concessionary loan, so weigh the long-term interest-rate exposure against the insurance economics carefully.

What does HPS cost relative to my mortgage repayment?

For a typical S$400,000 HDB-loan buyer in their 30s, HPS premium runs at well under 5% of annual interest. Through the 50s, that ratio can push 8 to 12% as premiums rise sharply with age. The cost is meaningful but not punishing — and the economics flip dramatically against any uninsured outcome where the family inherits an outstanding loan they cannot service.

If my equivalent insurance lapses, what happens?

You must rejoin HPS at the prevailing age. CPF Board will notify you, and you will need a fresh declaration. If you fail to rejoin, you risk being uncovered on the HDB loan — a bad outcome both for the lender and for any beneficiaries. Treat the equivalent-policy condition as a long-term commitment, not a temporary workaround.

Related Articles

- HDB Concessionary Loan Singapore 2026

- Refinancing Home Loan Singapore 2026

- TDSR Singapore 2026: How the 55% Cap and 4.0% Stress Test Work

- CPF Accrued Interest Singapore 2026

- Property Inheritance Singapore 2026

- Conveyancing Process Singapore 2026

Disclaimer

This article is general information for Singapore property buyers and does not constitute financial, insurance or legal advice. HPS is administered by the CPF Board and detailed premium tables and eligibility rules are published there and on the HDB portal. Bank-loan MRTA terms vary by insurer and lender; verify with the issuing insurer and consult a licensed financial adviser before committing. Premium figures cited are indicative and should not be relied upon for purchase decisions. For tax and CPF interaction, refer to IRAS and CPF Board guidance.

Tags: HPS Singapore, MRTA, mortgage insurance, Home Protection Scheme, HDB loan, bank loan, CPF Ordinary Account, decreasing term assurance, critical illness rider, opt-out, mortgage refinancing, Singapore property finance.