HDB Resale Process Singapore 2026: Step-by-Step Guide from OTP to Key Collection

Quick Answer: HDB Resale Process 2026

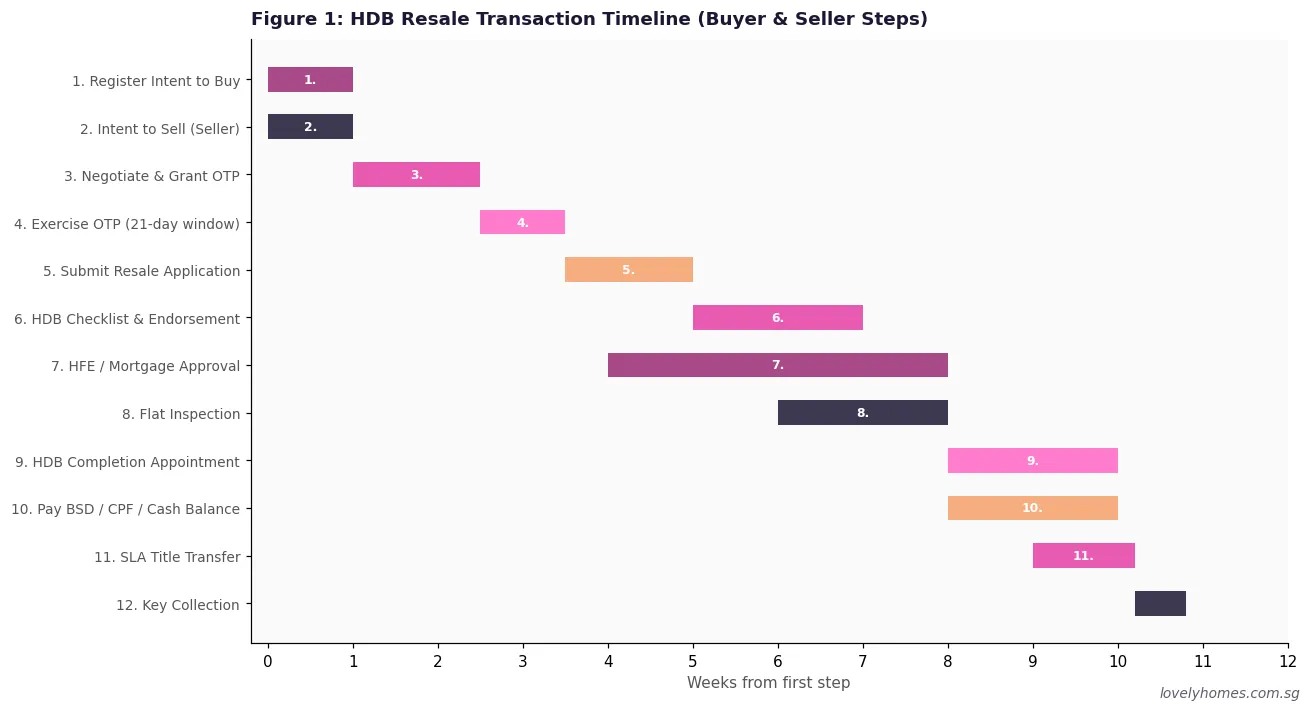

- The HDB resale process typically takes 8–12 weeks from granting the Option to Purchase (OTP) to key collection.

- Buyers must obtain an HDB Flat Eligibility (HFE) letter before granting or exercising an OTP — skipping this step is one of the most common costly mistakes.

- Both buyer and seller register their intent on the HDB Resale Portal before any private negotiation. The portal manages all submissions, checklists, and appointment scheduling.

- The OTP option fee is capped at S$1,000; the total option fee plus exercise fee cannot exceed S$5,000 (HDB administrative rule).

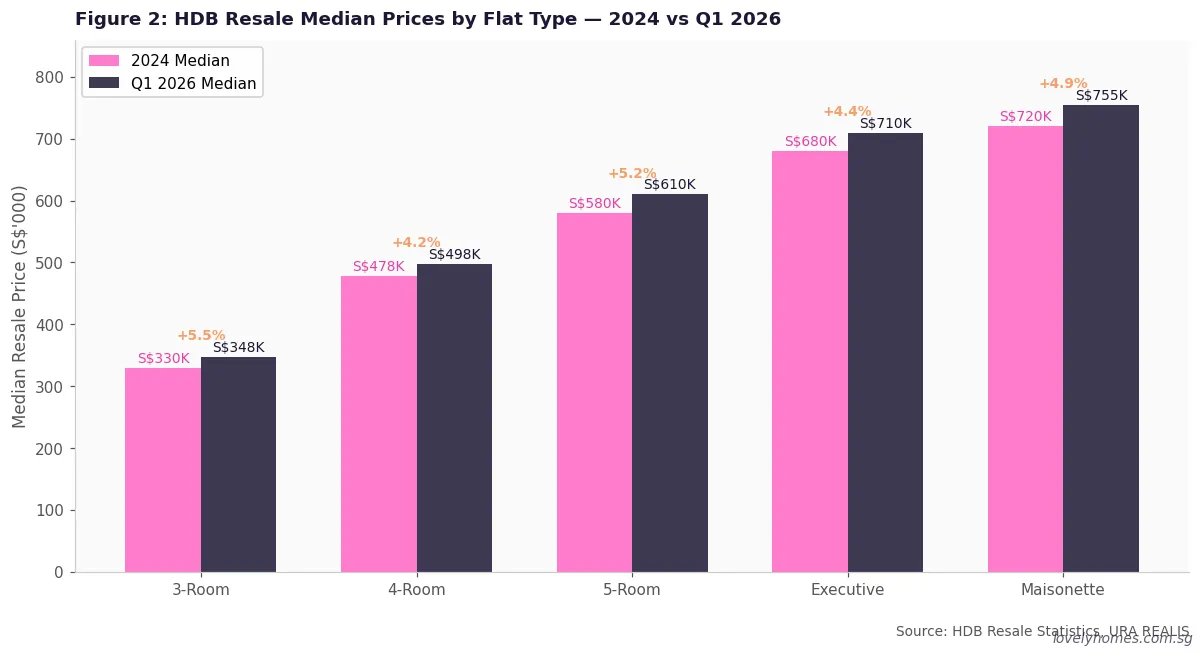

- As of Q1 2026, the median HDB resale prices are: 3-room S$348K, 4-room S$498K, 5-room S$610K, Executive S$710K.

- Resale flats are eligible for CPF Housing Grants including the Enhanced Housing Grant (up to S$120,000), the Family Grant (S$50,000), and the Proximity Housing Grant (S$30,000).

- A buyer must meet the HDB eligibility conditions: at least one Singapore Citizen applicant, family nucleus, income ceiling (S$14,000 for resale with no income ceiling waiver), and the 30-month private property disposal requirement (if applicable).

The HDB Resale Market in 2026

Buying a resale HDB flat remains the most direct path to home ownership for many Singapore families. Unlike Build-To-Order (BTO) flats, resale units are available immediately — there is no construction wait of four to five years. You can inspect the actual flat, assess the neighbourhood, and negotiate directly with the existing owner. The tradeoff is price: resale flats generally command premiums over BTO prices, particularly for mature estates and well-located units.

In Q1 2026, HDB resale transaction volume remained robust at approximately 6,300 units, driven by the large cohort of flats completing their Minimum Occupation Period (MOP) — nearly 13,480 flats reached MOP in 2026 alone, roughly 70% more than in 2025. Resale prices have moderated from the 2022–2023 peak but remain elevated. The Housing & Development Board (HDB) continues to administer all resale transactions through its digital Resale Portal, which was significantly upgraded in 2022 to consolidate all buyer and seller steps in a single system.

Step 1: Check Eligibility and Obtain Your HFE Letter

The first practical step for any resale buyer is to apply for an HDB Flat Eligibility (HFE) letter via the HDB Resale Portal (accessible via Singpass at resale.hdb.gov.sg). The HFE letter replaces the former Eligibility Letter and is now mandatory — you cannot grant or exercise an OTP for an HDB resale flat without a valid HFE letter.

The HFE letter confirms your eligibility to purchase (flat type, location restrictions, income ceiling), the CPF Housing Grants you qualify for, and the maximum HDB loan you can obtain. It is valid for nine months from the date of issue. The application processing time is typically three to five working days.

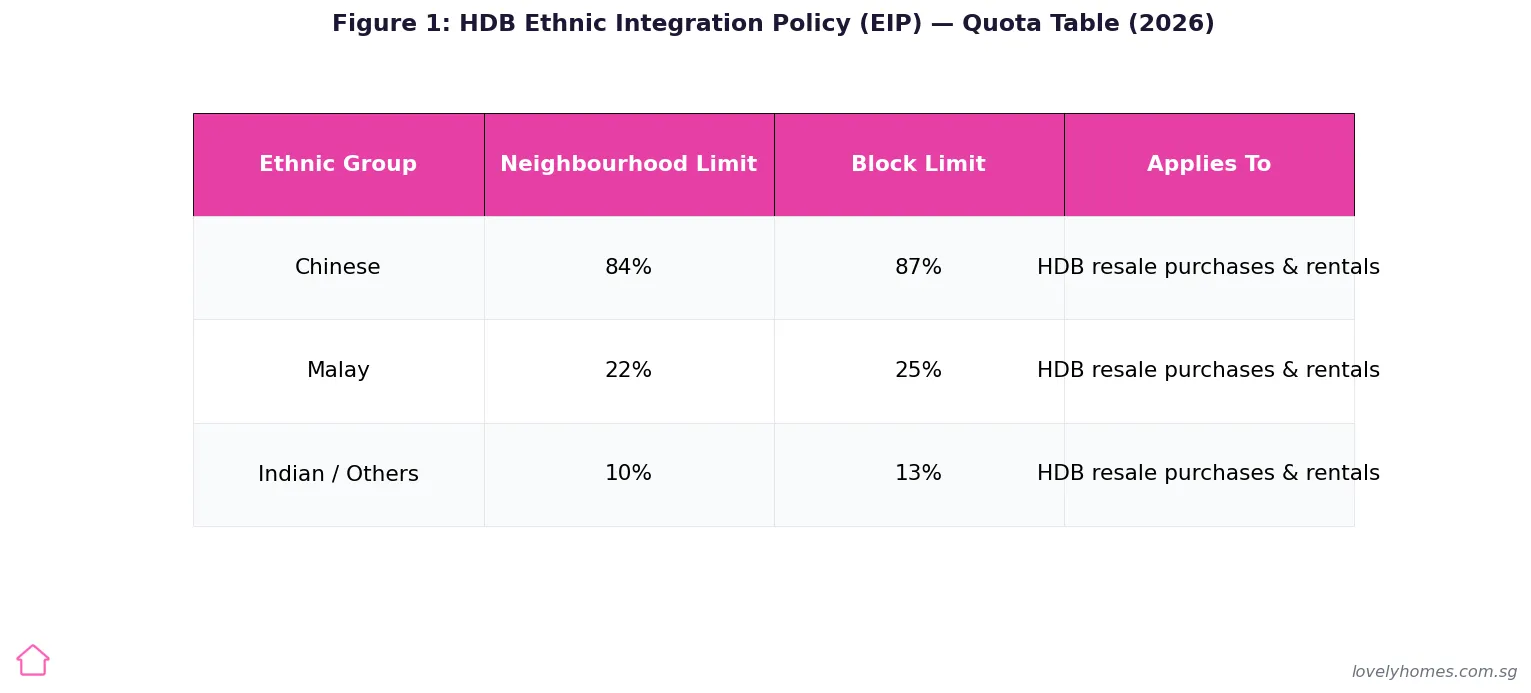

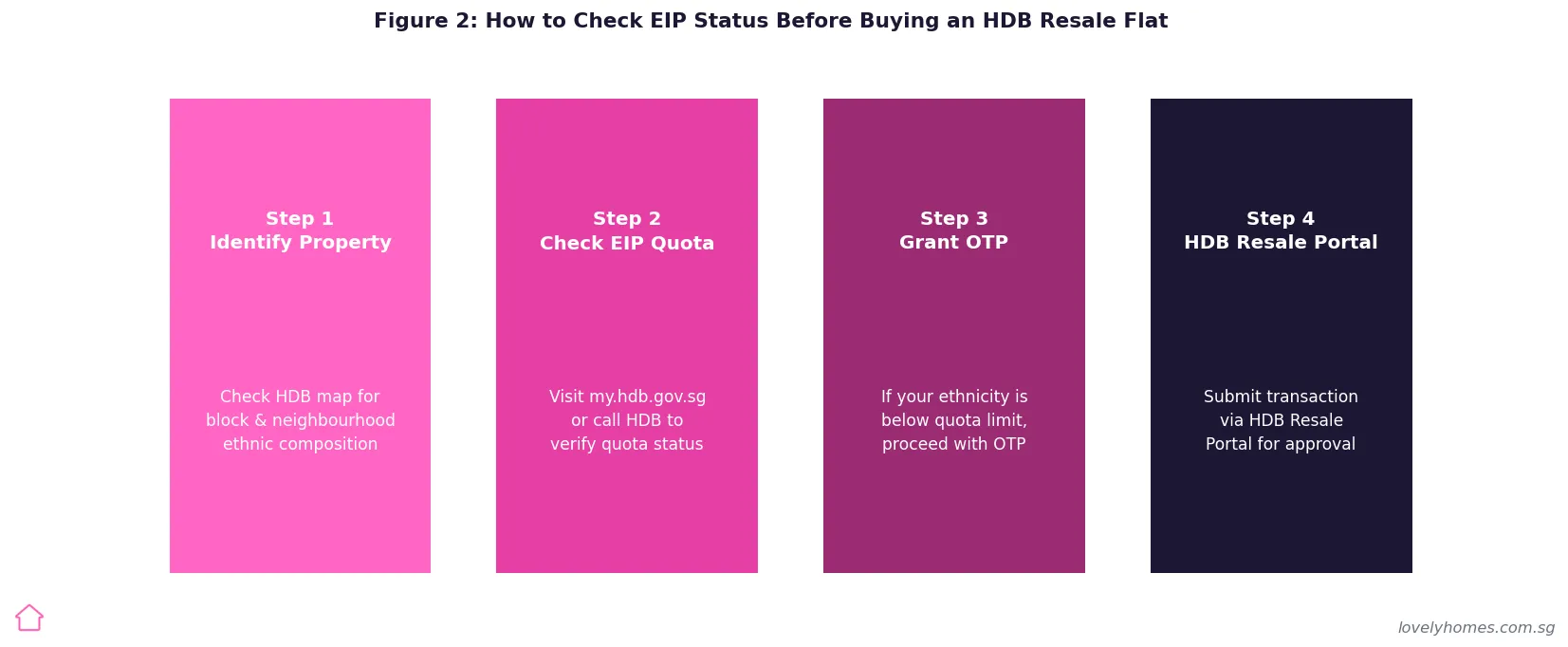

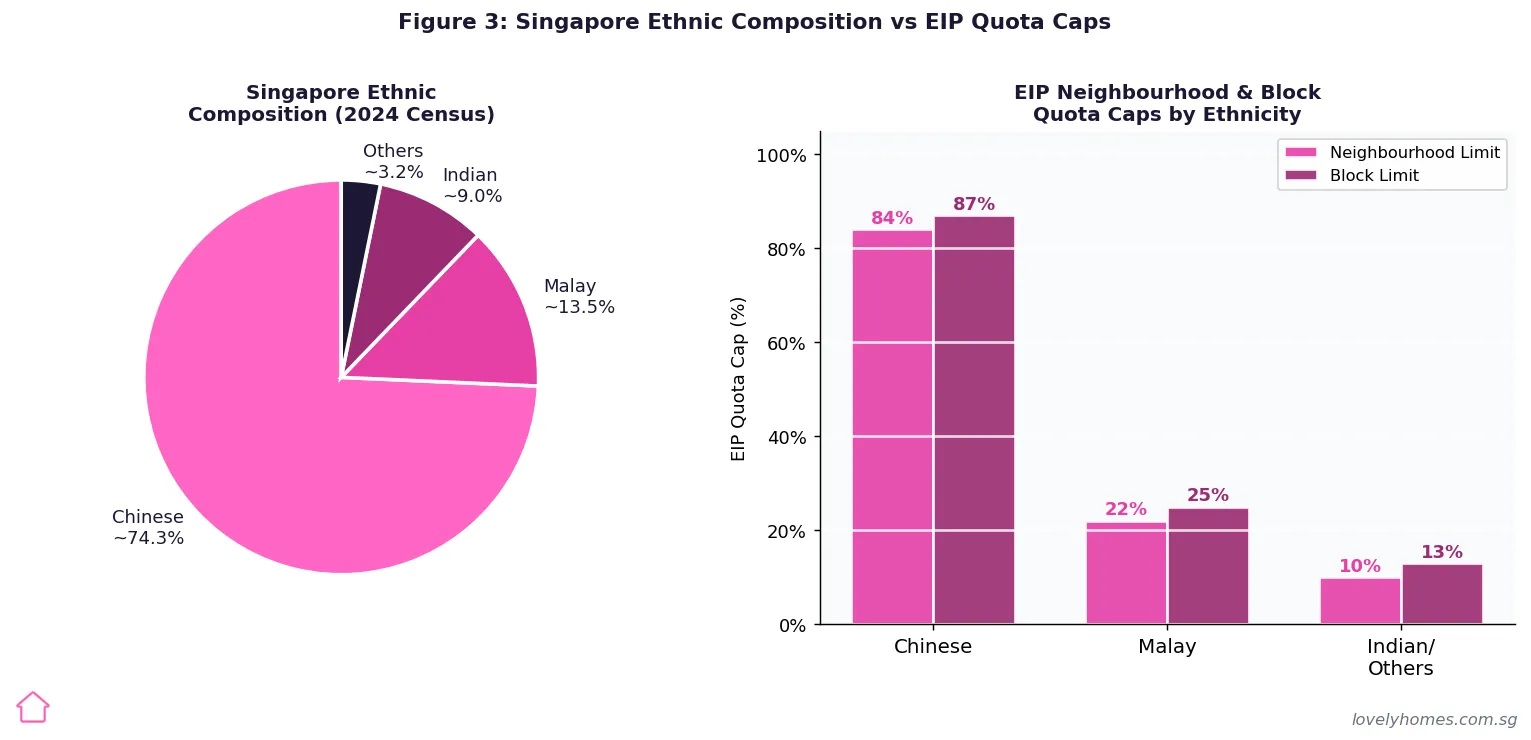

Eligibility conditions for Singapore Citizens purchasing a resale HDB flat in 2026 include: at least one SC in the family nucleus, a minimum of one other member in the family nucleus (spouse, fiancé/e, parent, child, or sibling), no private property ownership by any applicant within the past 30 months, income not exceeding S$14,000/month for families (S$7,000 for singles), and compliance with the Ethnic Integration Policy (EIP) and Singapore Permanent Resident (SPR) Quota for the block.

Step 2: Register Intent to Buy (and Intent to Sell)

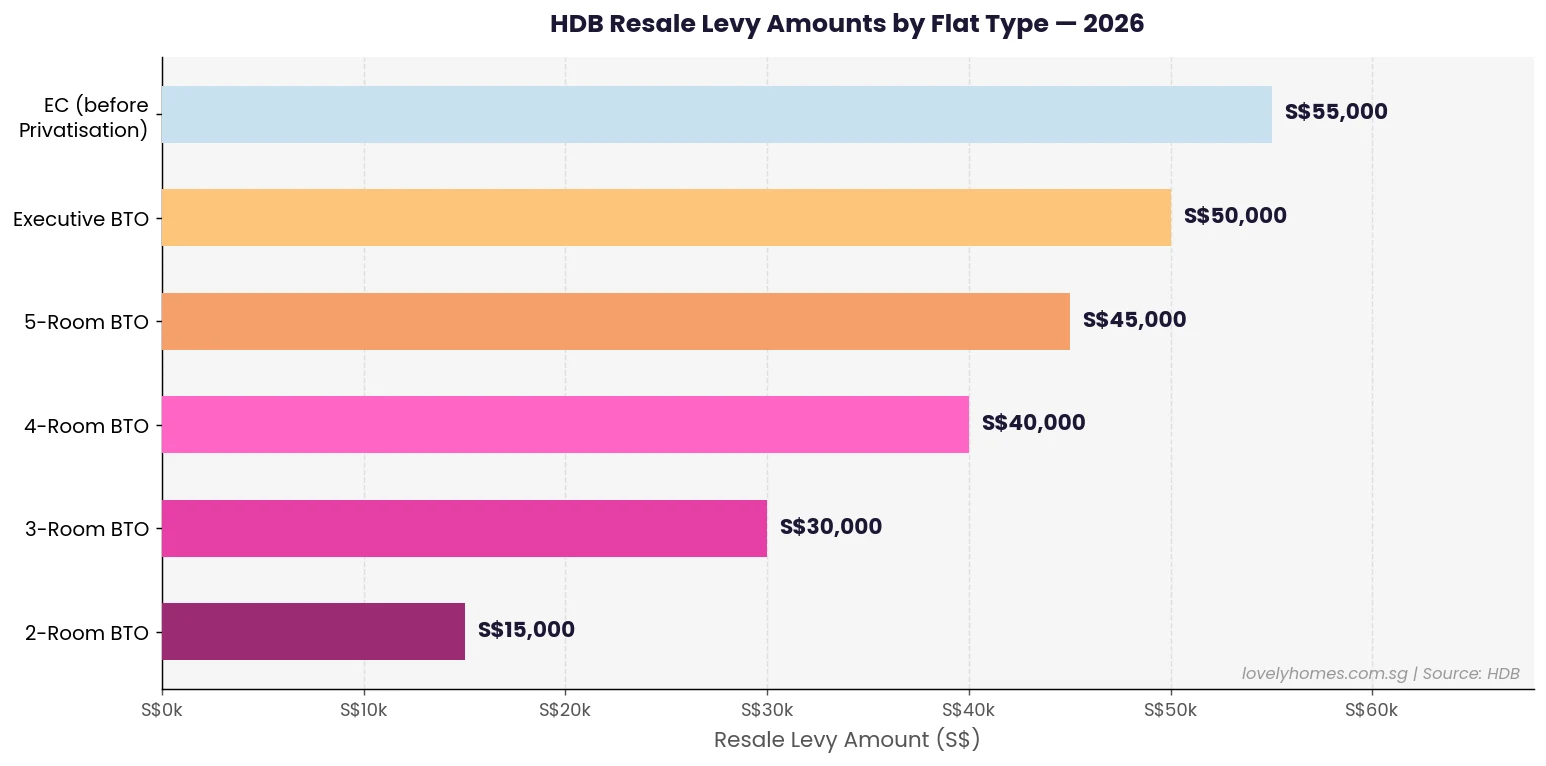

Once your HFE letter is in hand, register your Intent to Buy on the HDB Resale Portal. This is a formal declaration that you are actively seeking a resale flat and locks in your eligibility status for the transaction. Simultaneously, the seller must register their Intent to Sell before granting the OTP — a seller who issues an OTP without having registered their Intent to Sell is in breach of HDB procedures. Both registrations are free and can be done online. The Intent to Sell also auto-runs an eligibility check for the seller, confirming their right to sell and any Resale Levy payable.

At this stage, buyers typically engage a property agent (optional but strongly recommended for first-timers), shortlist units on HDB’s MyHDBPage or property portals, and begin flat viewings. When viewing a flat, confirm: the Ethnic Integration Policy (EIP) quota for your ethnicity at that block, the remaining lease (and its CPF implications), the Annual Value for property tax estimation, and any outstanding town council arrears the seller is responsible for clearing before completion.

Step 3: Negotiate and Grant the Option to Purchase (OTP)

The Option to Purchase (OTP) is a legally binding contract granting the buyer the exclusive right to purchase the flat at the agreed price within 21 calendar days. The seller issues the OTP after agreeing on the price and terms. Key parameters:

- Option Fee: Paid upon signing the OTP, up to S$1,000 (negotiated between parties). This is non-refundable if the buyer does not exercise the OTP.

- Option Period: 21 calendar days from the OTP date.

- Exercise Fee: Paid when exercising the OTP. Total option fee + exercise fee cannot exceed S$5,000.

- Cash Over Valuation (COV): If the agreed price exceeds HDB’s assessed market value, the excess must be paid fully in cash — CPF cannot be used for COV. COV can range from S$0 to over S$50,000 depending on demand for the specific unit.

Before exercising the OTP, buyers should commission a professional valuation (if not already done by HDB), confirm their bank or HDB loan quantum, and ensure sufficient CPF OA funds for the downpayment and instalment servicing.

Step 4: Exercise the OTP and Submit the Resale Application

To exercise the OTP, the buyer signs the “Acceptance to Purchase” section and pays the exercise fee before the 21-day option period expires. Within 7 calendar days of exercising the OTP, both buyer and seller must submit their respective halves of the Resale Application on the HDB Resale Portal. The submission is a critical legal step — failure to submit within 7 days of the other party’s submission voids the application and may lead to the OTP being treated as lapsed.

Each party submits their part independently: the buyer uploads financial documentation (HFE letter, CPF statements, mortgage approval letter) while the seller uploads proof of ownership, HDB flat particulars, and any relevant declarations. HDB issues a confirmation of receipt and a Resale Checklist for each party to sign and acknowledge before the transaction can proceed.

Step 5: HDB Valuation, Checklist Endorsement, and Mortgage Approval

After submission, HDB arranges a valuation of the flat by one of its approved valuers (the cost, approximately S$120–S$180, is borne by the buyer). The valuation determines the market value for CPF and grant purposes. Buyers should note: if the purchase price exceeds the valuation, the excess (COV) must be paid in cash at completion.

The HDB Resale Checklist — a legal document — must be endorsed by both parties via the portal. It confirms that both sides have understood key policies: MOP rules (the buyer’s new five-year MOP clock begins from key collection), flat eligibility conditions, CPF usage rules, and grant terms. For buyers using a bank loan, the formal Loan Offer Letter from the bank must also be submitted at this stage.

For buyers using a HDB Concessionary Loan (available to eligible Singapore Citizen households with income below S$7,000/month), the HFE letter already contains the loan quantum. For bank loans, buyers must have received a formal Loan Offer Letter (typically secured after the HFE letter stage) with the interest rate, tenure, and monthly repayment confirmed.

Step 6: HDB Completion Appointment and Key Collection

HDB schedules the completion appointment typically within 6–8 weeks of accepting the Resale Application. At the completion appointment (held at HDB Hub, Toa Payoh), the title of the property is formally transferred from seller to buyer. Both parties, or their solicitors, must attend. The following payments are settled at or before completion:

- Buyer’s Stamp Duty (BSD) — must be paid within 14 days of OTP exercise or 14 days of completion, whichever is earlier. Payable via IRAS e-Stamping.

- Outstanding purchase price balance — funded by the bank loan disbursement, CPF OA, and any cash balance (including COV).

- Seller’s outstanding CPF refund — the seller’s CPF principal plus accrued interest is deducted from the sale proceeds and returned to the seller’s CPF OA.

- HDB resale administrative fee — S$80 for each party.

After the completion appointment, keys are handed over, and the buyer’s five-year MOP period begins. The Singapore Land Authority (SLA) registers the transfer, and the buyer becomes the registered owner in the land register within a few working days.

Financing Your HDB Resale Purchase

Buyers have two primary financing options for a resale HDB flat: an HDB Concessionary Loan or a bank loan. The HDB loan is available only to Singapore Citizen-led households with no existing private property and income below S$7,000/month (or S$3,500 for single applicants). It offers 75% LTV (down from 80% in August 2024), no cash downpayment requirement, and a fixed rate tied to CPF OA rate + 0.1% (currently 2.6% p.a.). The full comparison is covered in our HDB Loan vs Bank Loan Guide 2026.

Bank loans offer lower interest rates (typically 1.5%–2.2% fixed for the first 2–3 years in mid-2026) but require a minimum 5% cash downpayment and are subject to the Monetary Authority of Singapore’s Total Debt Servicing Ratio (TDSR, 55%) and Mortgage Servicing Ratio (MSR, 30% of gross income for HDB property). The MSR cap of 30% is the binding constraint for most HDB buyers. A couple earning S$9,000/month combined is capped at S$2,700/month mortgage, which at 2.0% over 25 years supports a loan of approximately S$514,000.

CPF Housing Grants (EHG, Family Grant, PHG, Step-Up Grant) are applied against the purchase price and reduce the loan quantum needed. For eligible families buying a resale flat, total grants can reach S$200,000. See our CPF Housing Grant Guide 2026 for the full breakdown.

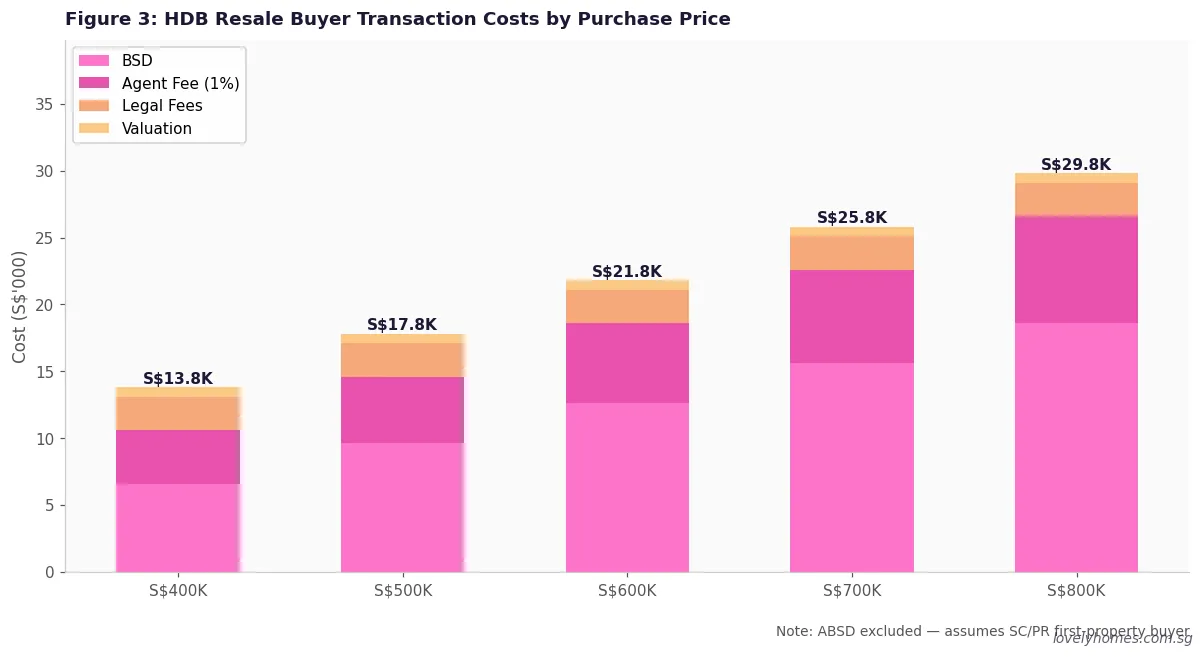

All-in Buyer Costs

| Cost Item | Who Pays | Typical Amount | Notes |

|---|---|---|---|

| Buyer’s Stamp Duty (BSD) | Buyer | S$5,400–S$20,600 (for S$400K–S$800K) | Progressive rates 1%–6%; payable via IRAS e-Stamping |

| ABSD | Buyer | Nil (SC 1st property); 20% SC 2nd | Most first-time buyers pay zero ABSD; HDB purchase counts as 1st property |

| Agent Commission | Buyer (for buyer’s agent) | ~1% of purchase price | Seller pays 2% for seller’s agent |

| Legal Fees | Buyer | ~S$2,500–S$3,000 | Conveyancing by HDB or appointed solicitor |

| Valuation Fee | Buyer | S$120–S$180 | Arranged by HDB; determines CPF-eligible amount |

| HDB Admin Fee | Buyer & Seller | S$80 each | Per party; paid at HDB completion appointment |

| Cash Over Valuation (COV) | Buyer | S$0–S$50,000+ (negotiated) | Payable in cash only; CPF cannot be used |

Worked Example: The Yeo Family

Mr and Mrs Yeo are Singapore Citizens (joint applicants, combined income S$8,500/month) purchasing a four-room resale flat in Tampines. They have an eligible HFE letter confirming: EHG S$45,000 (income S$8,500/month falls within the S$9,000 band for families), Family Grant S$50,000 (buying resale, both SC, first time applying for subsidy), and access to HDB loan at 75% LTV. The flat is offered at S$560,000 (valuated at S$558,000 — COV of S$2,000).

| Item | Amount |

|---|---|

| Purchase Price | S$560,000 |

| Less: EHG + Family Grant | − S$95,000 |

| Net price after grants | S$465,000 |

| HDB Loan (75% of S$558K valuation) | S$418,500 |

| CPF OA contribution (downpayment + ongoing) | S$44,500 |

| Cash for COV | S$2,000 |

| BSD (on S$560,000) | S$11,400 |

| ABSD | Nil (SC 1st property) |

| Agent + Legal + Valuation + HDB Admin | S$9,280 |

| Total Cash Outlay | ~S$22,680 |

| Monthly HDB loan repayment (@2.6%, 25yr) | S$1,894/month |

| MSR check: S$1,894 / S$8,500 | 22.3% — PASS (below 30%) |

The Yeos’ total cash outlay of S$22,680 is very manageable, and their monthly repayment of S$1,894 comfortably clears the 30% MSR cap. Without the grants, their cash outlay would have been over S$117,000 — the grants are doing significant heavy lifting. Their new five-year MOP period starts from the day of key collection.

Common Mistakes to Avoid

The HDB resale process is well-documented, but buyers regularly stumble at several predictable points. Exercising an OTP before receiving the HFE letter is the single most consequential error — buyers have been forced to forfeit the option fee and restart the process after discovering ineligibility. Failing to check the Ethnic Integration Policy (EIP) quota before viewing is another: if your ethnicity’s quota for a block is already full, you cannot purchase in that block regardless of price or seller willingness.

On the financing side, many buyers secure informal bank “approval-in-principle” letters rather than formal Loan Offer Letters — these are not the same thing, and only the formal letter satisfies HDB’s submission requirements. Buyers should also verify their CPF OA balance accounts for the downpayment, ongoing instalments, BSD, and a buffer for unexpected costs before committing to an OTP price. Our guide on Singapore property downpayment requirements 2026 explains the full cash and CPF calculation.

What Might Come Next

This section reflects editorial analysis and is not official HDB policy.

HDB has signalled an intent to keep resale flat supply elevated through 2026 and 2027, with the large cohort of MOP-completing flats adding to available stock. The policy priority of affordable home ownership, reaffirmed in Budget 2026, supports the continued availability of EHG grants. There is ongoing academic and policy debate about whether COV — which is not tracked publicly — is re-emerging as a significant affordability barrier in mature estates.

The HDB Resale Portal is scheduled for a further update in late 2026 to integrate more seamlessly with SLA’s e-conveyancing platform, potentially reducing the completion timeline to below eight weeks for straightforward transactions. Buyers should track announcements at hdb.gov.sg.

FAQ: HDB Resale Process 2026

Do I need a property agent to buy a resale HDB flat?

No — HDB’s Resale Portal is designed for direct buyer-seller transactions without agents. However, most buyers and sellers engage agents for negotiation support, paperwork management, and expertise in checking EIP quotas, valuation, and neighbourhood comparables. Buyers do not pay agent commission for new launch properties, but for resale HDB they typically pay 1% commission to their own agent (the seller pays 2% to theirs). Using an agent registered with the Council for Estate Agencies (CEA) is strongly recommended; you can verify any agent’s registration at the CEA Public Register at cea.gov.sg.

What happens if the HDB valuation comes in below the agreed purchase price?

If HDB’s appointed valuer assesses the flat below the negotiated price, the difference (Cash Over Valuation, or COV) must be paid in cash — you cannot use CPF for COV. For example, if you agreed to pay S$580,000 but HDB values the flat at S$560,000, you owe S$20,000 COV in cash. Many buyers include a valuation clause in the OTP negotiations to give them the right to renegotiate or withdraw if the COV exceeds a specified amount, though sellers in a hot market may resist such clauses.

Can a Singapore Permanent Resident buy an HDB resale flat?

Yes, a Singapore PR may purchase an HDB resale flat as a joint purchaser with a Singapore Citizen (the essential occupier rule still requires at least one SC in the household). An SPR household (both applicants are PR and neither is SC) cannot buy an HDB flat. Additionally, SPR buyers are subject to a 5% ABSD on their first residential property purchase. An SPR couple buying a resale HDB where both are PR would pay 5% ABSD on top of BSD and other costs. The relevant ABSD rates are explained in our ABSD Singapore 2026 complete guide.

What is the difference between the Resale Checklist and the Option to Purchase?

The Option to Purchase (OTP) is a private contract between buyer and seller, granting the buyer an exclusive right to purchase at the agreed price within 21 days. The HDB Resale Checklist is a separate HDB administrative document — submitted via the Resale Portal — that both parties must acknowledge before HDB will process the resale application. The checklist confirms that both parties understand their legal obligations regarding MOP, CPF refunds, grant terms, and HDB regulations. Failing to submit the checklist endorsement within the required window delays the transaction and may require resubmission of the entire application.

Does buying an HDB resale flat affect my ability to buy a private property later?

Yes — once you buy any HDB flat (BTO or resale), you own an HDB property. If you subsequently wish to purchase a private residential property, you must either sell the HDB flat first (and observe HDB’s rules on timing and MOP) or hold both simultaneously and pay 20% ABSD as a Singapore Citizen buying a second property. For upgraders, the standard strategy is to sell the HDB flat within 6 months of purchasing the private property (for ABSD remission purposes) or to complete the HDB MOP before purchasing the private property. See our Stamp Duty Remission Guide 2026 for upgrader remission timing rules.

What happens to the seller’s outstanding CPF at completion?

When an HDB flat is sold, the seller’s CPF principal drawn plus accrued interest (at 2.5% p.a.) is deducted from the sale proceeds and returned to the seller’s CPF OA. This is not optional — it is a statutory obligation under the Central Provident Fund Act. The seller’s conveyancing solicitor or HDB will calculate the exact refund amount, which is paid directly by the buyer’s bank (or HDB loan disbursement) to the seller’s CPF account before the net cash balance is released to the seller. Long-term owners are sometimes surprised to find the CPF refund consumes much of the apparent price gain — our guide on CPF accrued interest for property 2026 explains this in detail.

Can I buy an HDB resale flat if I currently own a private property overseas?

Yes, with conditions. If you own private residential property overseas, you are not automatically disqualified from buying an HDB resale flat. However, from 9 May 2023 onwards, Singapore Citizen buyers of HDB flats (new or resale) who own private residential property — whether in Singapore or overseas — must dispose of that private property within six months of key collection. You also pay 20% ABSD on the HDB resale purchase if you already own one or more properties (including overseas ones) at the time of purchase, though you may apply for ABSD remission on disposal if you meet HDB’s approved buyer criteria.

Related Articles

- Singapore HDB BTO Application Guide 2026: Eligibility, Balloting and Key Collection Explained

- Singapore CPF Housing Grant Guide 2026: EHG, PHG, Family Grant and How to Apply

- HDB Loan vs Bank Loan Singapore 2026: Rates, LTV and Which Saves You More

- Singapore Property Downpayment Guide 2026: How Much Cash and CPF You Need

- Singapore CPF Accrued Interest for Property 2026: What You Owe Your CPF When You Sell

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Buyer’s Stamp Duty (BSD) 2026: Rates, Calculations and Worked Examples

- Singapore HDB Upgrading Programmes Guide 2026: HIP, NRP and What Flat Owners Pay

- Singapore Stamp Duty Remission Guide 2026: ABSD Upgrader Refunds and Exemptions

Disclaimer

This article is for general informational purposes only and does not constitute financial, legal, or property advice. HDB eligibility conditions, grant amounts, loan rules, and stamp duty rates are subject to change. Always verify current HDB resale requirements at hdb.gov.sg and current CPF rules at cpf.gov.sg. Stamp duty rates are administered by IRAS at iras.gov.sg. For personalised guidance, engage a property agent registered with the Council for Estate Agencies (CEA) and, for financial planning, a licensed adviser regulated by MAS. LovelyHomes.com.sg accepts no liability for reliance on the information contained herein.

Click anywhere to close