Strata Title and MCST in Singapore 2026: How Your Condo Is Actually Run

If you own a condominium, executive condo, or strata-titled landed home in Singapore, you do not really own a building — you own a slice of one, a “strata lot“. Everything outside that slice (the lift you ride to work, the pool you swim in, the lobby that smells faintly of Diptyque) is common property, and it is run by a body corporate called the Management Corporation Strata Title — the MCST.

Most owners pay their monthly maintenance fee, attend an AGM once in a blue moon, and never think about it again. Then a leak appears in the carpark, the lifts hit 25 years and need a S$2 million modernisation, or someone wants to put a new awning on their balcony — and suddenly the structure that runs your home becomes very real, very fast. This guide walks you through how strata title actually works in Singapore, what your MCST does, where your money goes, and the rights and obligations you signed up for the moment your conveyancing lawyer registered your title at the Singapore Land Authority.

Quick Answer — strata title and MCST in 30 seconds

- You own a strata lot (your unit + accessory areas) plus a share value in common property.

- The MCST manages common property under the Building Maintenance and Strata Management Act (BMSMA 2004).

- Your monthly bill funds two ring-fenced pots: a Management Fund (~75%) for day-to-day running and a Sinking Fund (~25%) for major capital works.

- Decisions are made at AGMs by share-value vote — ordinary majority for routine matters, ≥75% special resolution for capital expenditure above S$200,000.

- Indicative monthly fees: S$280-450 OCR mass-market, S$420-680 mid-tier RCR, S$780-1,400 luxury CCR, S$1,500+ ultra-luxury.

- Renovations affecting common property require written MCST approval before BCA submission (BMSMA s.37).

- Disputes above the council level go to the Strata Titles Boards — not the civil courts in the first instance.

What Is Strata Title and Why Does Singapore Use It?

Strata title is the legal mechanism that makes vertical, multi-owner property possible. When a developer builds a condominium, the Singapore Land Authority registers a strata plan dividing the building into individual lots (the units, plus accessory lots like balconies, planter boxes and air-con ledges) and common property (everything else). Each lot is a separate parcel of land in law, with its own title deed, its own share value, and its own set of rights to the common property.

Without strata title, only the developer or a single co-owner group could hold the title to a multi-storey building — you would be buying a long lease from them, not freehold ownership of a defined unit. Strata title gives you genuine real-estate ownership, the right to mortgage your lot independently, and the right to participate in governance of the building. The trade-off is that you must accept a co-ownership regime: a council elected by other owners, by-laws that bind you, and a duty to contribute to communal expenses whether you use the facilities or not.

Singapore’s strata regime sits inside the Building Maintenance and Strata Management Act 2004 (BMSMA), supplemented by the Land Titles (Strata) Act 1967. Together they cover roughly 12,000 strata-titled developments and over 750,000 strata lots across the island as at the start of 2026. If you own anywhere in Singapore that is not landed-on-its-own-plot, you are almost certainly subject to BMSMA.

The Core Concept: Strata Lot, Common Property, Share Value

Three pieces of paper are issued when your conveyancing completes: the certificate of title for your strata lot, the strata plan for the development, and the schedule of share values. They define everything that follows.

Strata lot

Your physical unit, defined by the centre line of internal walls, the upper surface of the floor, and the under-side of the ceiling slab. Accessory lots include balconies, private enclosed spaces (PES), aircon ledges, and any car-park or storage spaces specifically allocated to your unit on the strata plan. You can renovate inside your strata lot largely as you wish — subject to BCA rules, MCST house rules, and structural integrity.

Common property

Everything outside your strata lot that is not somebody else’s lot. Lifts, lobbies, pools, gyms, gardens, common corridors, the external façade, the roof, the basement carpark, M&E plant rooms, and the structural slabs themselves. Common property is owned collectively by all subsidiary proprietors as tenants-in-common in the proportion of their share values, and managed by the MCST.

Share value

A whole number assigned to each lot in the strata plan that determines (a) your voting weight at general meetings and (b) your contribution to the common funds. Larger units get higher share values. A typical 1,000 sqft 3-bedroom unit might carry 10 share values; a 600 sqft 2-bedroom might carry 6. If your unit’s share value is 10 out of a building total of 5,000, you pay 0.2% of every common-fund expense and cast 10 votes (out of 5,000) on every resolution.

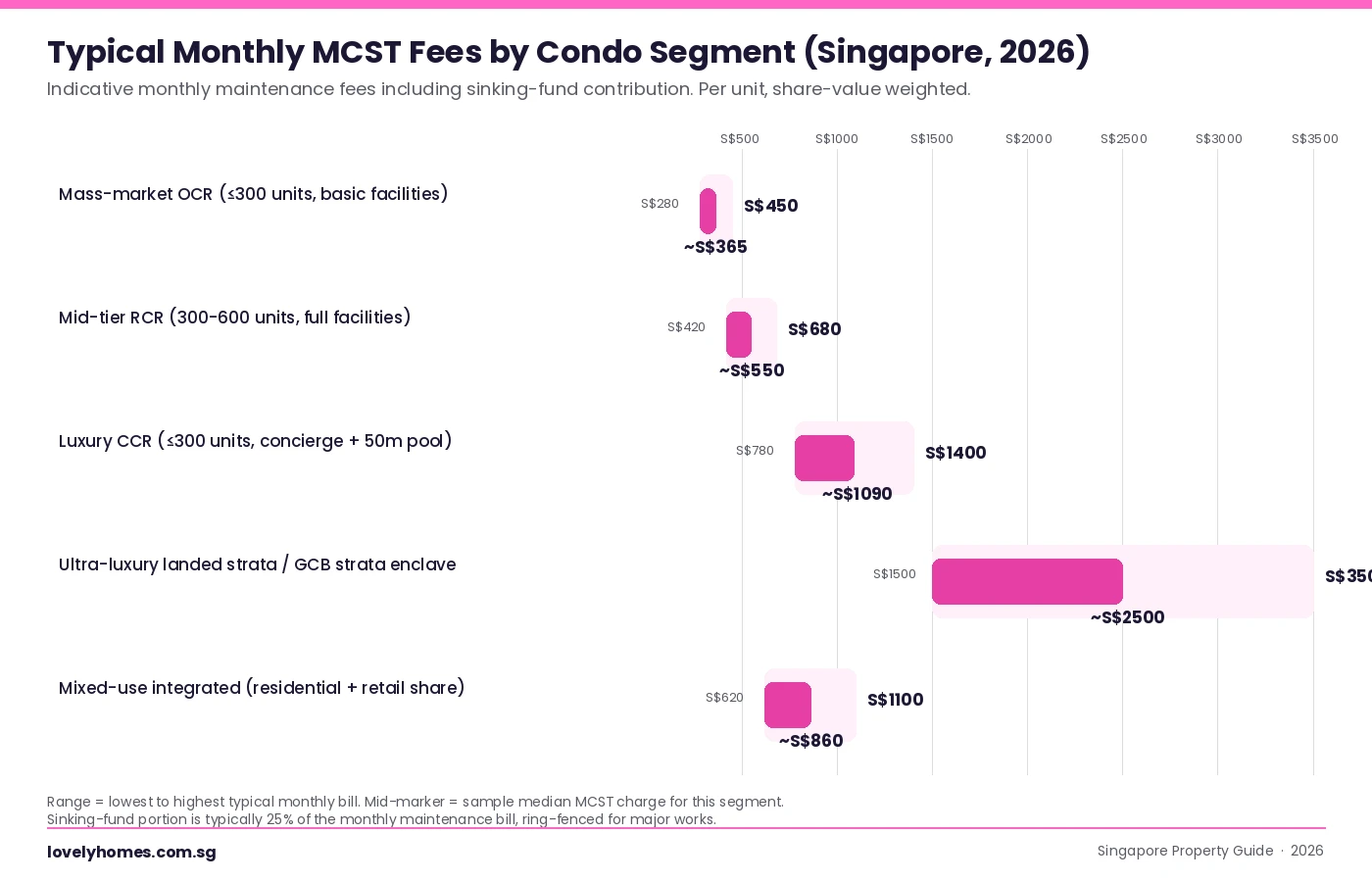

Indicative MCST Fees by Condo Segment (2026)

Before you commit to a unit, look at the monthly maintenance bill. It is the single biggest variable holding cost of ownership and varies enormously by segment. The figure below sets out what most owners actually pay across five common segments of the Singapore market in 2026.

| Segment | Typical monthly fee (per unit) | Sinking fund share | Drivers of cost |

|---|---|---|---|

| Mass-market OCR | S$280-450 | ~25% | Basic facilities, lower headcount, fewer lifts, surface carparks |

| Mid-tier RCR | S$420-680 | ~25% | Full facilities suite, multi-deck basement carpark, larger landscape |

| Luxury CCR | S$780-1,400 | ~25-30% | 24-hr concierge, valet, branded F&M for plant, smaller lot count to share costs |

| Strata landed / GCB enclave | S$1,500-3,500 | ~30% | Few lots, large land area, perimeter security, private roads |

| Mixed-use integrated | S$620-1,100 | ~25% | Shared cost-allocation with retail/commercial component, dual-MCST structures |

One important nuance: integrated developments often have two MCSTs — one for the residential strata, one for the entire development. Your monthly bill is therefore the sum of both layers. Always ask the marketing agent for the dual-MCST cost breakdown before signing.

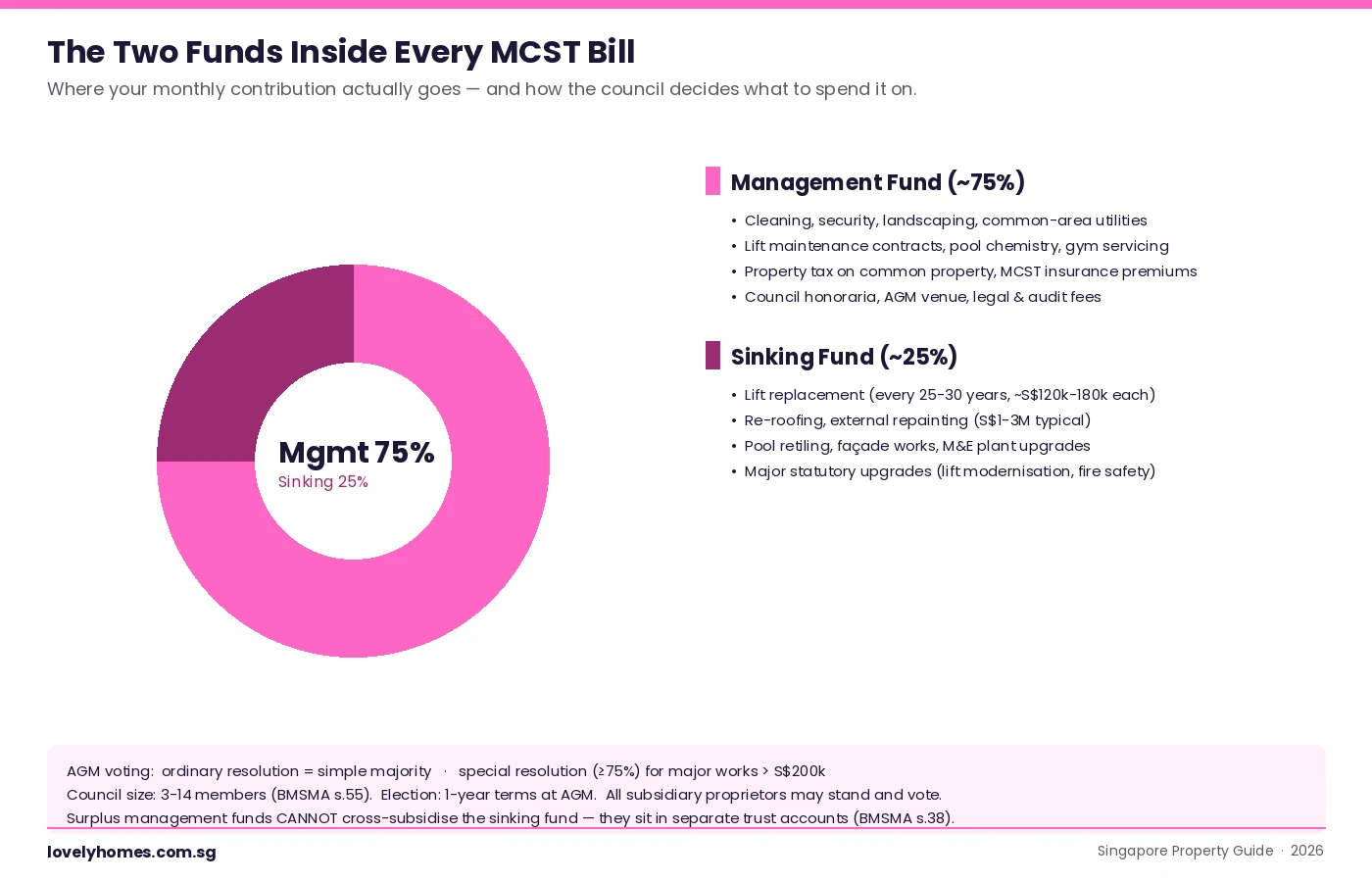

The Two Funds Inside Every MCST Bill

Your monthly maintenance fee is not a single pot of money. By law it splits into two ring-fenced trust accounts — the Management Fund (general operations) and the Sinking Fund (capital reserves) — and the council cannot move money freely between them.

Management Fund

Pays for everything that recurs: cleaning contracts, security guarding, lift maintenance, pool chemistry, gym servicing, common-area utilities, landscaping, MCST insurance premiums, property tax on common property (yes — the building itself is taxed on the rental value of its common areas), council members’ honoraria, AGM venue, audit and legal fees, and the salary of the appointed managing agent. If the toilet roll runs out in the lobby, the management fund replaces it.

Sinking Fund

Funds large, infrequent capital works that would otherwise hit owners with sudden special levies. Lift modernisation (typically required at 25-30 years and costing S$120k-180k per lift), exterior repainting, re-roofing, façade re-cladding, pool retiling, M&E plant replacement, and statutory upgrades (e.g. lift safety upgrades mandated by BCA, fire-system retrofits required by SCDF). A well-run building should hold roughly 2-3 years of operating expenditure in the sinking fund at any time.

Why the wall between them matters

Section 38 of the BMSMA prohibits using management-fund money to pay for sinking-fund items, and vice versa. This protects future owners: if the council were free to spend the sinking fund on day-to-day items, you would arrive at the 25-year mark with no money for the lift modernisation, and the council would have to issue a one-off levy of, say, S$15,000 per unit to make up the gap. Always read the audited accounts before bidding on a resale unit — a depleted sinking fund is a hidden liability the buyer inherits.

Governance: Council, AGMs, Voting

The MCST is the body corporate; the council is its elected board. Owners (subsidiary proprietors) elect a council of 3 to 14 members at the AGM, each serving one-year terms. The council appoints office-bearers (chair, secretary, treasurer) and engages a managing agent — a licensed property-management firm that runs the day-to-day operation.

Annual General Meeting (AGM)

Must be held within 15 months of the previous one. Owners receive at least 14 days’ written notice with the agenda, audited accounts, the proposed annual budget, and any resolutions for vote. Standard agenda items: receive the audited accounts, fix the next year’s budget and contribution rates, elect the council, appoint the auditor, transact special resolutions.

Resolution thresholds

- Ordinary resolution — simple majority of the share values voted. Used for routine business: budget approval, council elections, day-to-day spending decisions within budget.

- Special resolution — ≥75% of share values voted in favour, with ≤25% against. Required for capital expenditure exceeding S$200,000 (s.40 BMSMA), variation of by-laws, and certain by-law-affecting matters.

- 90% resolution — required to vary common property boundaries or transfer common property.

- Unanimous resolution — required for any change that affects an individual lot owner’s title or rights.

Extraordinary General Meetings (EGM)

Called between AGMs for urgent matters — usually a special-resolution capital project (e.g. lift modernisation), an unplanned major repair, or to vote on a collective sale resolution. Owners holding ≥20% of share values can requisition an EGM directly.

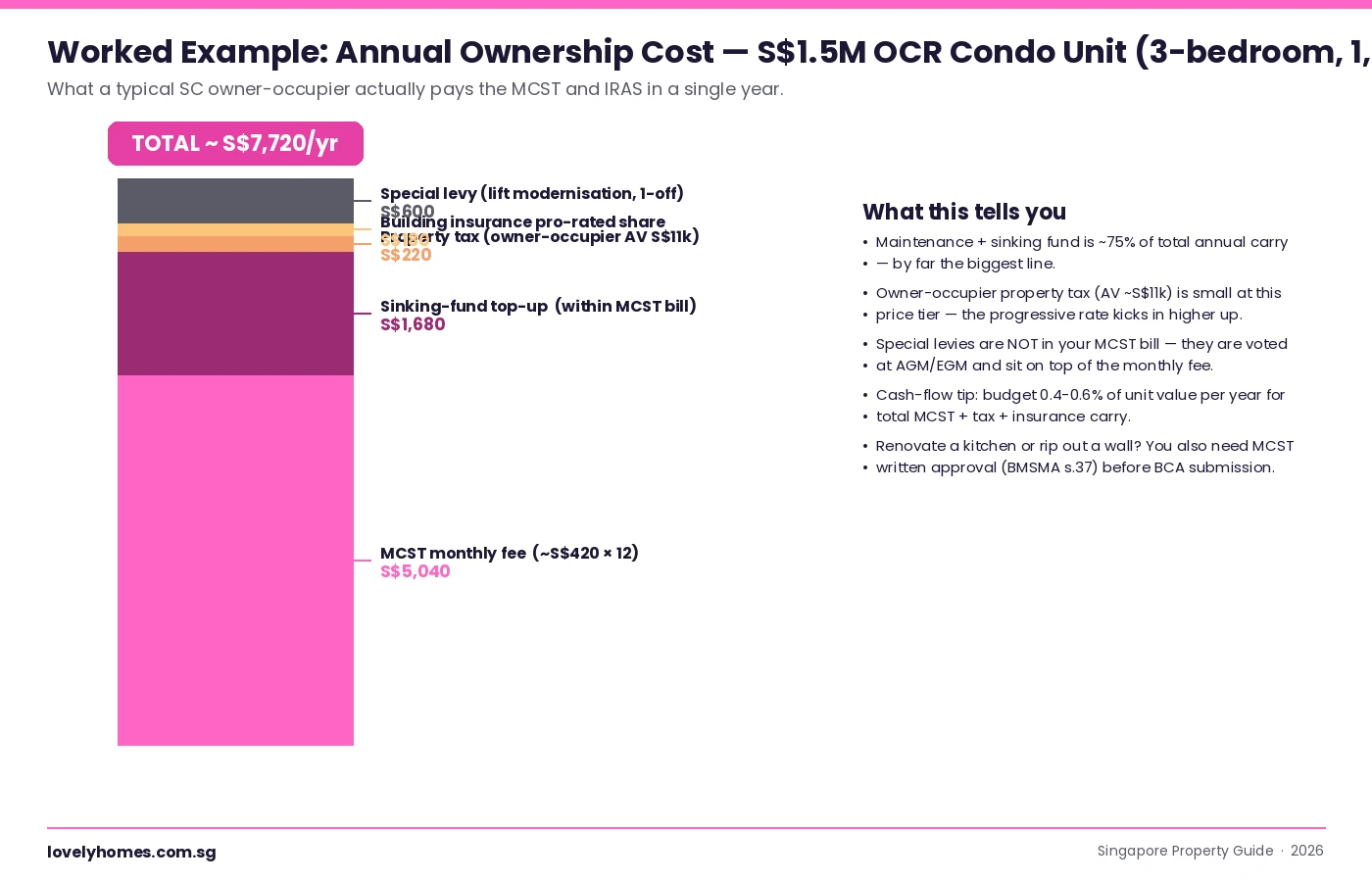

Worked Example: What a S$1.5M OCR Condo Owner Pays in a Year

Numbers ground the abstract. Here is what a typical Singapore Citizen owner-occupier of a 1,000-sqft, 3-bedroom unit in a mid-tier OCR development worth S$1.5 million actually pays the MCST and IRAS over a year, assuming no leasehold-related issues and no rental income.

Three observations stand out. First, the recurring carry on a S$1.5M unit is a real number — about S$5,000-7,000 per year, or 0.4-0.5% of unit value, before any one-off special levies. Second, the property-tax line at this AV tier is genuinely small; most of your tax burden was paid up front as BSD when you bought. Third, special levies are not in the monthly bill — they are voted at AGM/EGM and sit on top, often with 3-6 months’ notice. Plan a 1-2% capital reserve of unit value over a 10-year horizon if you want to avoid surprises.

Your Rights and Obligations as a Subsidiary Proprietor

Buying a strata lot binds you to a contract you may never have read — the by-laws of the development, set out in the First Schedule of the BMSMA (the prescribed by-laws) and in any additional by-laws passed by special resolution at the AGM. Key obligations every owner has:

- Pay contributions on time — arrears attract interest (often 10% p.a.) and the MCST may register a charge on your title under s.34 BMSMA after 30 days, blocking refinancing or sale until paid.

- Get written approval before altering common property — even private balcony tinting or aircon-ledge enclosures usually need MCST consent under s.37.

- Comply with the by-laws on noise hours, pet keeping, short-let restrictions (typically minimum 3 months for residential), commercial use limitations, and exterior-facade alterations.

- Allow access for the MCST or its contractors to perform repairs to common property running through your lot, on reasonable notice.

Conversely, the rights you can enforce:

- Inspect the records — minutes, accounts, contracts. Owners are entitled to see anything in the corporate register on reasonable notice (a small fee may apply).

- Stand for council, attend and vote at general meetings, and propose resolutions.

- Requisition an EGM if you can muster 20% of share values.

- Apply to the Strata Titles Boards if the council acts unreasonably, refuses by-law-approved alterations, or makes invalid decisions.

Disputes: The Strata Titles Boards

The Strata Titles Boards (STB) — constituted under the BMSMA and the Building Maintenance Act — are the specialised tribunal that hears strata disputes. Most owner-vs-MCST or owner-vs-owner strata disputes cannot go to the High Court in the first instance; they must come through the STB. Common applications:

- Section 92 applications to compel the MCST to take a specific action (e.g. carry out a long-overdue repair).

- Section 31 applications to vary or invalidate a by-law that is unreasonable or oppressive.

- Collective-sale applications under the Land Titles (Strata) Act — the 80%/90% en-bloc consent threshold mechanic is litigated here.

- Disputes over share values, accessory-lot rights, and exclusive-use grants over common property.

STB filing fees are modest (S$500-1,000 typically) and the process is faster and lighter than the High Court — expect 6-9 months from filing to determination on most matters.

What to Watch When Buying Resale

If you are buying a strata-titled resale, the MCST is going to be your landlord-of-sorts. A few things to inspect before exercising the OTP:

- Last 3 years of audited accounts. Look for a healthy sinking fund, no qualified audit opinions, and no pattern of outsized recurring deficits.

- Latest AGM minutes. Check for upcoming capital works that may trigger a special levy. Lift modernisation, repainting, and façade works in the pipeline will hit your wallet.

- Outstanding maintenance arrears on the lot. Ask your conveyancer to obtain a section 50 certificate from the MCST — arrears transfer with the lot.

- By-laws. Read the additional by-laws — some buildings restrict pet weight, prohibit short-lets entirely, ban exterior changes, or impose dress codes in common areas.

- Legal disputes. Ask whether the MCST is currently in any STB or High Court proceedings — ongoing disputes can mean a deteriorating building or financial drain.

How Strata Title Differs From Other Tenure Forms

Singapore’s strata regime is similar in principle to Hong Kong’s multi-storey buildings regime, the Australian strata title system (from which the term originates), and US condominium ownership — but the BMSMA framework is more prescriptive than most. By comparison:

- vs HDB ownership — HDB flat owners are not subsidiary proprietors of an MCST. The HDB itself manages the estate. Town councils handle the day-to-day common-property functions, funded by service-and-conservancy charges (S&CC).

- vs landed property — A standalone landed home on a freehold or 99-year leasehold parcel has no MCST and no shared common property. You bear all costs and decisions yourself, but you also have full autonomy.

- vs strata-landed — Cluster housing and strata-landed enclaves do have an MCST, but with a much smaller lot count (often 30-100). Their fees are correspondingly higher per unit because fixed costs are spread thin.

What Might Come Next: Strata Reform Watch

BCA and the Ministry of National Development have been quietly consulting on a third tranche of BMSMA amendments since 2024. The most-talked-about proposals as at April 2026:

- Mandatory minimum sinking-fund balance tied to building age (e.g. 18 months of opex once the building is over 10 years old). Aimed at preventing under-funded sinking funds.

- Compulsory professional MCST chairs for buildings of over 500 lots, in response to dispute volumes from large integrated developments.

- Streamlined STB process for routine repairs — a fast-track procedure to compel obvious common-property maintenance.

- Stricter rules on short-term lets — aligning the BMSMA with URA’s 3-month minimum-let regime to give MCSTs cleaner enforcement teeth.

None of the above is yet law. We will update this guide when the next round of amendments is gazetted.

Frequently Asked Questions

Can the MCST force me to renovate or repair my own unit?

Generally no — renovations inside your strata lot are your decision, subject to BCA structural rules and any by-law restrictions (e.g. flooring requirements above the second storey). The MCST can however require you to remedy a condition inside your lot that is causing damage to common property or to neighbouring lots — a leaking bathroom waterproofing membrane, for example, where moisture is reaching the unit below. If you fail to act, the MCST can perform the works and charge them back to your lot under s.41 BMSMA.

What happens if the council goes broke?

If the management fund runs out, the MCST cannot pay contractors or salaries. The council must call an EGM to pass a special levy (a one-off contribution from all owners pro-rata to share value) to recapitalise. Repeated insolvency is a sign of either chronic under-budgeting or council misconduct — in extreme cases the STB can appoint an interim manager to run the MCST under s.85.

Can I rent out my parking space to non-residents?

It depends on whether your parking lot is an accessory lot, an exclusive-use common-property right, or a transient-use right. Accessory lots can typically be sublet to anyone in some buildings but most modern by-laws restrict carpark sub-letting to residents of the development only for security reasons. Always check the additional by-laws and house rules — sub-letting to non-residents in breach of by-laws is enforceable by the STB.

How are votes weighted — one-lot-one-vote or by share value?

Share-value votes apply by default. So a penthouse with a share value of 24 has roughly 4 times the voting weight of a 1-bedroom unit with a share value of 6. This is intentional: larger units pay more to the common funds and bear more of the financial impact of decisions, so they vote in proportion. Some routine matters (e.g. council elections) may also be conducted on a one-vote-per-lot basis under the BMSMA’s voting rules.

If I am buying a brand-new condo, when does the MCST actually come into existence?

The MCST is constituted automatically on the date the strata-title plan is registered with the SLA. In practice, the developer manages the building from TOP onwards under an “interim period” with an interim management committee (often staffed by the developer and a few early-mover owners). The first AGM — where the permanent council is elected — must be held within 13 months of the first lot being conveyed (s.27 BMSMA). Until then, your monthly fee is charged at developer-set rates, which may be re-budgeted up or down at the first AGM.

Do I need MCST consent for a kitchen renovation?

If the renovation is purely cosmetic and stays within your lot — new countertops, replacement appliances, repainting — you usually only need to notify the managing agent and pay any renovation deposit / debris fee under house rules. If you are touching any wet area, structural element, exterior, or anything that could affect a neighbouring lot or common property, you need written MCST approval before submitting plans to BCA. Most buildings require approved-contractor lists, work-hour windows (typically 9am-6pm Monday-Saturday, no Sundays/public holidays), and a renovation deposit of S$1,000-3,000.

How do collective sales fit into the strata regime?

Collective sale (en-bloc) is the process by which the MCST as a whole sells the entire development to a redeveloper, with proceeds distributed among lot owners. Under the Land Titles (Strata) Act, an 80% share-value-and-floor-area consent threshold applies to developments over 10 years old (90% for younger ones). The STB hears applications and may approve, vary, or reject the sale. Successful collective sales effectively dissolve the MCST on completion. We cover the process in detail in our En-Bloc Sale Process Guide.

Related Articles

- Property Conveyancing Guide Singapore 2026 — how the strata title transfer happens at completion.

- En-Bloc Sale Process Guide — how MCSTs and lot owners trigger a collective sale.

- Freehold vs 99-Year Leasehold Singapore 2026 — tenure interacts with strata sinking-fund liabilities.

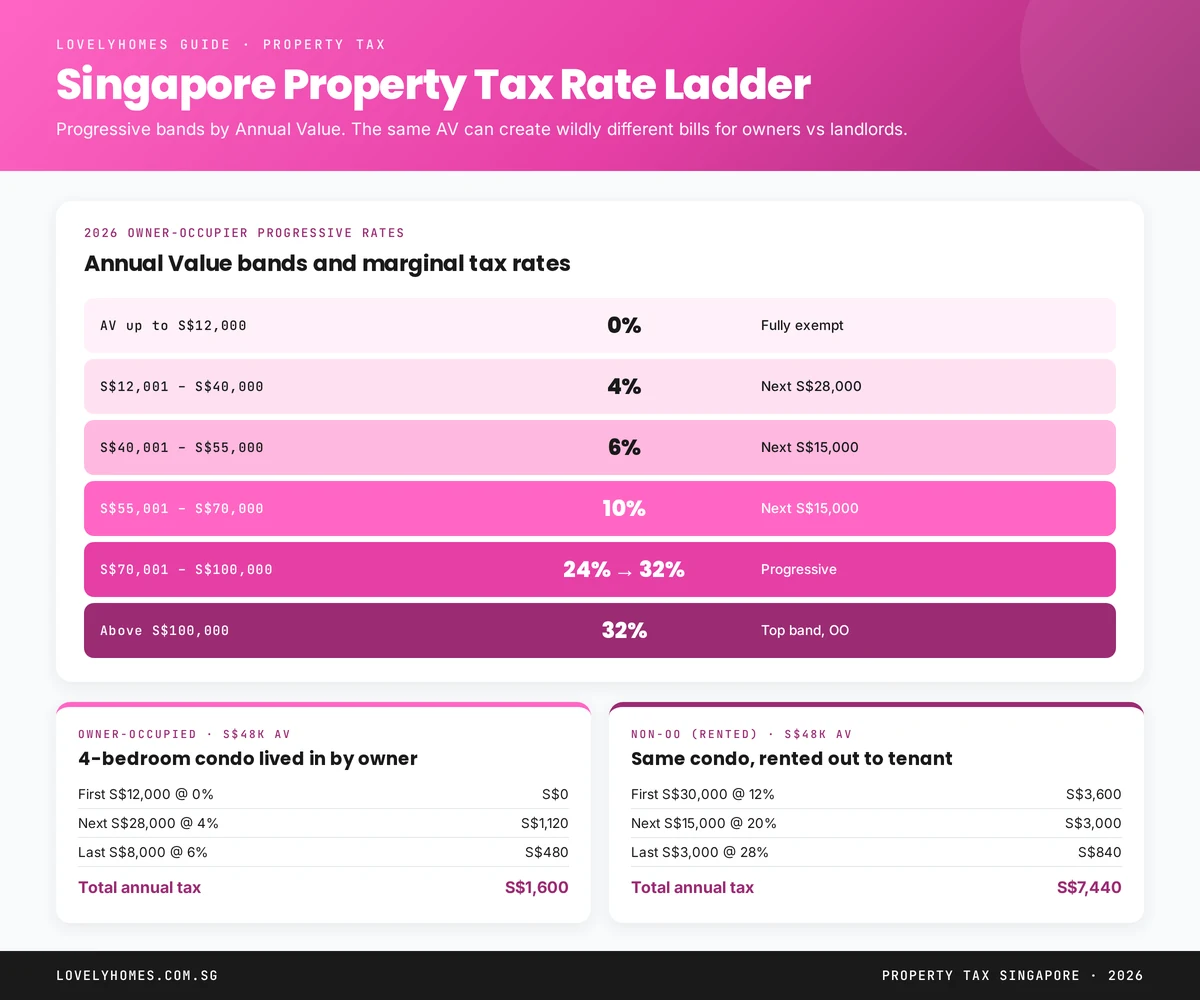

- Property Tax Singapore 2026 — how owner-occupier vs investor AV bands feed your annual carry.

- Singapore Property Insurance Guide 2026 — the MCST’s master policy and what it does not cover for you.

- New Launch vs Resale Condo 2026 — resale buyers must inherit the existing MCST balance sheet.

- Joint Tenancy vs Tenancy in Common Singapore 2026 — how you hold the strata lot itself.

Disclaimer

This guide is for general information only and does not constitute legal, tax, or financial advice. The Building Maintenance and Strata Management Act, the Land Titles (Strata) Act, and associated subsidiary legislation are the authoritative sources of strata-title law in Singapore and have been amended several times since 2004. Always verify the current position with the Building and Construction Authority, the Singapore Land Authority, the Ministry of Law, and the Inland Revenue Authority of Singapore — and consult a licensed conveyancing or strata-management lawyer before acting on any specific matter.