The phrase 99-to-1 Property Purchase Singapore 2026 describes a tenancy-in-common structure where one buyer holds 99 per cent of the property and a second buyer holds 1 per cent. Used legitimately, it is a perfectly valid form of co-ownership recognised under the Land Titles Act. Used as a two-step manoeuvre to add a co-owner after the original purchase, the structure became the subject of one of the most public anti-avoidance probes the Inland Revenue Authority of Singapore (IRAS) has run in the post-2010 cooling-measure era — a probe that recovered an estimated S$60 million in unpaid Additional Buyer’s Stamp Duty (ABSD) and surcharges.

This guide explains how the 99-to-1 structure works, why IRAS has scrutinised it, when a 99-to-1 split is legitimate and when it crosses the line into tax avoidance under the General Anti-Avoidance Rule (Section 33A of the Income Tax Act, with parallel application to stamp duties), and what the practical implications are for any Singapore household considering a tenancy-in-common purchase in 2026. The framework is administered by IRAS under the Stamp Duties Act, with anti-avoidance powers drawn from Section 33A of the Income Tax Act 1947.

Quick Answer — 99-to-1 in Singapore at a glance

What it is: a tenancy-in-common (TIC) ownership split where one party holds 99 per cent and another holds 1 per cent of a single residential property.

Why people use it: to bring a second income onto a bank loan, to plan an estate, or to manage the marital-asset split.

Why IRAS scrutinised it: a two-step variant — Buyer A purchases 100 per cent first, then Buyer B (who already owns property) is added 1 per cent later — was used to dodge ABSD that should have applied at the higher second-property rate.

The 2023 IRAS probe: 166 cases reviewed, an estimated S$60 million in ABSD and surcharge recovered, with a 50 per cent surcharge layered on top of the avoided tax.

Bright-line test: if the 1 per cent share is added after the original purchase, with the only commercial reason being to avoid a higher ABSD bracket, IRAS treats it as one composite transaction and reassesses ABSD on the full price.

Statute of limitations: up to six years backward under Section 33A.

Legitimate use is unaffected: a 99-to-1 split applied at the OTP itself, with both parties paying ABSD on their respective shares from Day 1, is fine.

What 99-to-1 Actually Means in Singapore Property Law

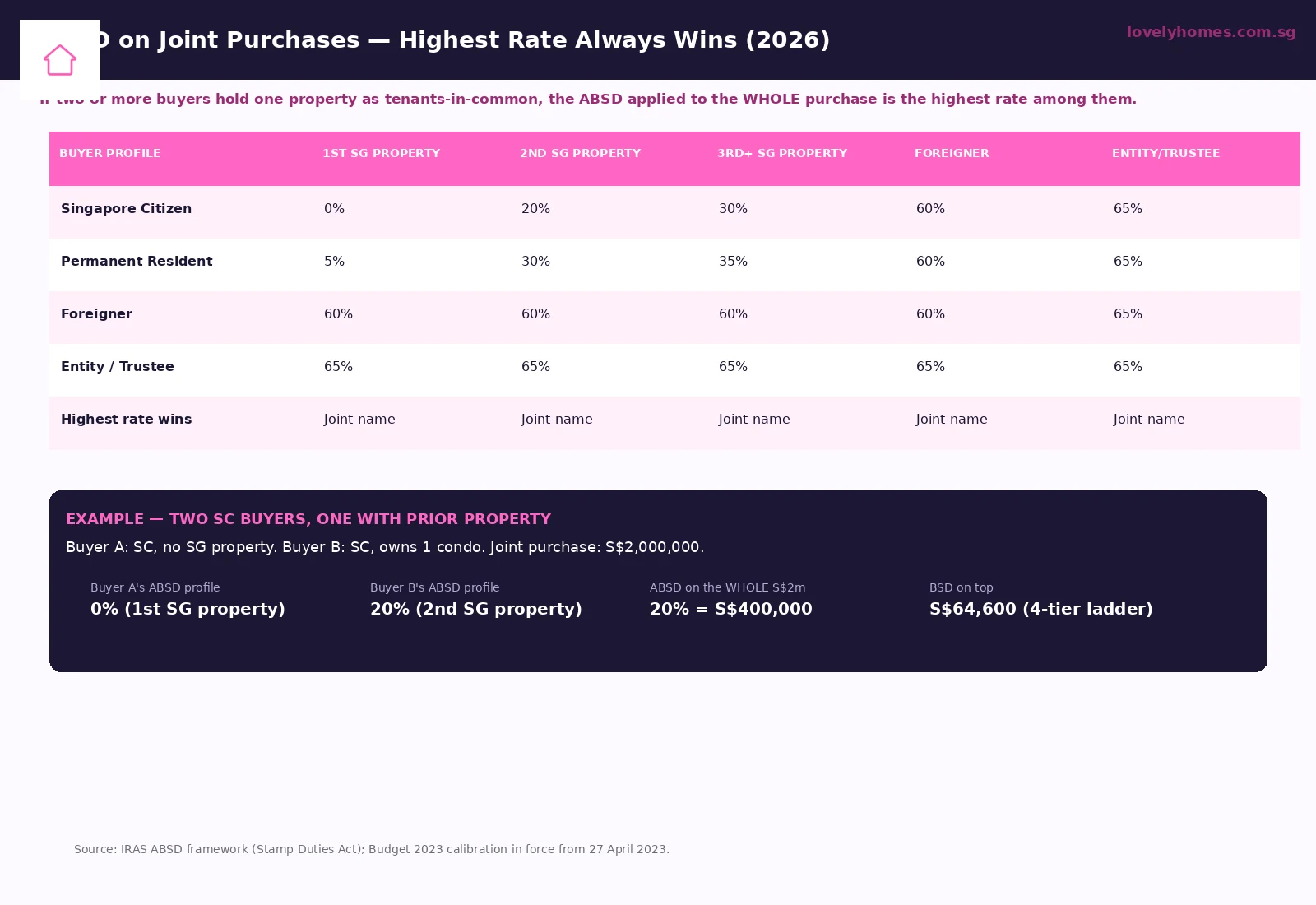

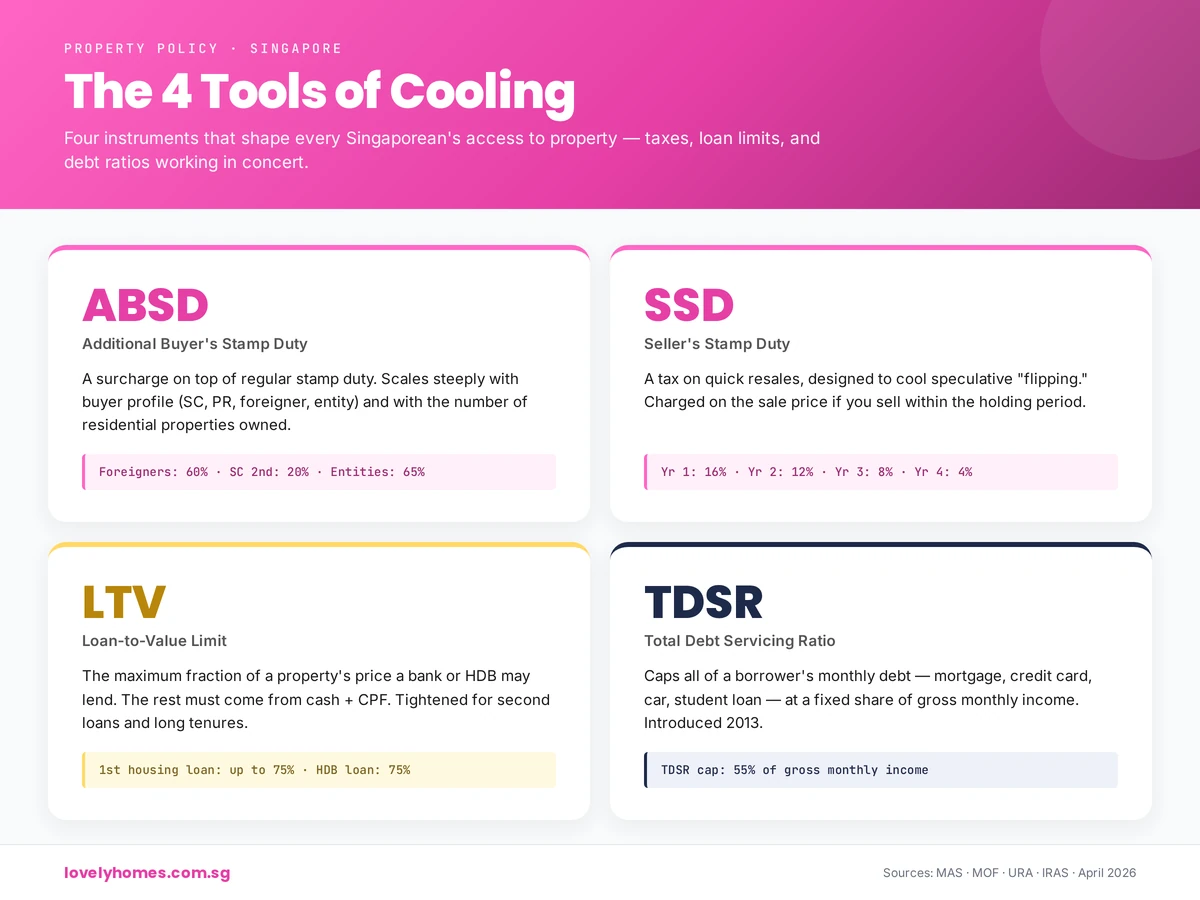

Singapore property co-ownership comes in two legal forms — joint tenancy and tenancy-in-common. Joint tenancy means co-owners share an undivided 100 per cent interest, and the property passes by survivorship to the surviving joint tenant on death. Tenancy-in-common means each owner holds a defined percentage of the property, and that share passes by will (or by intestacy) on death rather than to the other co-owners. Two co-owners as tenants-in-common can hold the property in any split that adds to 100 per cent — 50/50 is the default, but 80/20, 70/30 and 99/1 are all permitted. The Land Titles Act recognises any defined share. The 99/1 split is unusual mathematically but unremarkable legally.

For stamp duty purposes, a tenancy-in-common purchase is treated as a single transaction at the property level. Each co-owner is a “buyer” under the Stamp Duties Act, and ABSD is computed against each buyer’s profile. Where the buyers fall into different ABSD brackets — for example, one with no prior Singapore property (0 per cent) and one with one prior Singapore property (20 per cent) — the rule is unambiguous: the highest ABSD rate among the joint buyers applies to the entire purchase price, not just to the higher-rate buyer’s share.

This rule is what makes the 99-to-1 split structurally different from, say, a 50-50 split. The economic exposure of the 1-per-cent owner is one one-hundredth of the property; but the ABSD effect is the same as if they owned the whole thing. The Government’s logic is straightforward — the rule is meant to plug the obvious workaround of giving a higher-rate buyer a tiny notional share to access a joint loan while ducking the corresponding ABSD.

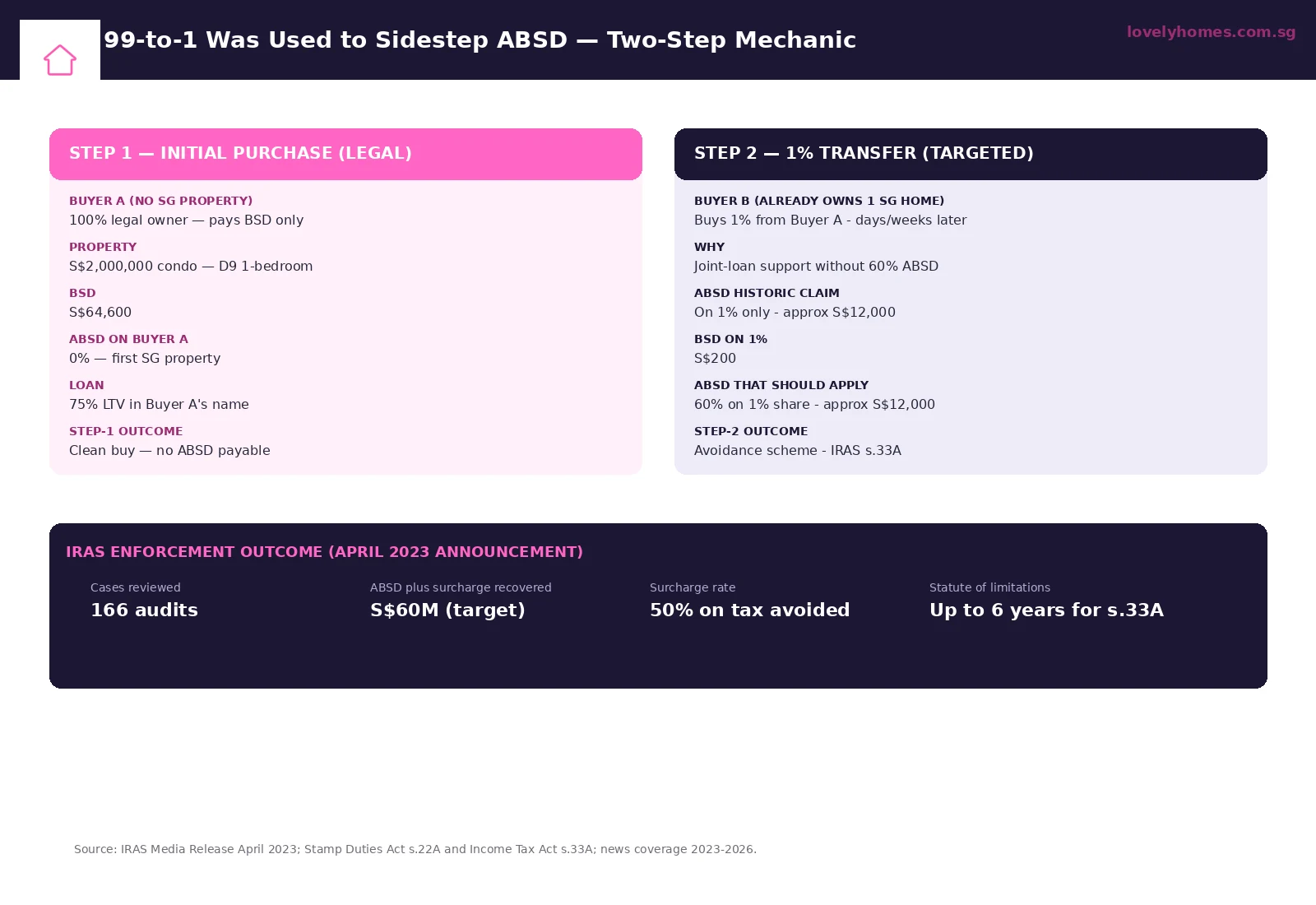

The Two-Step Mechanic IRAS Targeted

The 99-to-1 manoeuvre that IRAS publicly scrutinised in April 2023 was not the upfront 99-to-1 split. Upfront splits, where both buyers appear on the original Option to Purchase, the Sale and Purchase Agreement and stamping documents, were never the issue — the highest-rate ABSD applies cleanly and the tax is paid in full. The structure that drew IRAS’ attention was a two-step purchase:

Figure 1: The two-step pattern targeted by IRAS — original 100% buy by the lower-rate party, followed days or weeks later by a 1% transfer to the higher-rate party.

Step 1. Buyer A — a Singapore Citizen or Permanent Resident with no other Singapore property — exercises the Option to Purchase as the sole 100-per-cent owner of, say, a S$2 million condominium. ABSD on Buyer A is 0 per cent (or 5 per cent for a PR). Buyer’s Stamp Duty is computed normally (about S$64,600 for S$2 million). The buy is clean from the stamp-duty perspective.

Step 2. A short period later — sometimes days, sometimes weeks, occasionally a couple of months — Buyer A executes a transfer of 1 per cent of the property to Buyer B, who already owns one or more Singapore residential properties. Buyer B’s ABSD profile sits at 20, 30 or 60 per cent depending on their citizenship and prior holdings. Stamp duty would be paid on the 1-per-cent transfer at face value (BSD on S$20,000 = S$200; ABSD on S$20,000 at 20 per cent = S$4,000). The household has now achieved its real goal — both names on the title — but has paid only a fraction of the ABSD that would have been due if both names had appeared on the original OTP.

The motivation for the two-step structure is almost always financing-related. Banks underwrite home loans against the income of the named borrowers; many households need both incomes to meet the Total Debt Servicing Ratio (TDSR) cap of 55 per cent. If the higher-income borrower already owns property, putting both names on the OTP triggers the higher ABSD bracket on the entire purchase. The 99-to-1 two-step purports to achieve the loan-support outcome without the ABSD outcome.

How IRAS Pulled the Pattern Apart

IRAS announced in April 2023 that it had reviewed 166 cases of 99-to-1 (and similar structures like 95-to-5 or 90-to-10) where there was no commercial reason for the two-step pattern other than ABSD avoidance. The agency invoked Section 33A of the Income Tax Act 1947 — Singapore’s General Anti-Avoidance Rule — together with its parallel powers under the Stamp Duties Act, to recharacterise the two-step transaction as a single composite purchase. Once recharacterised, the ABSD is recalculated as if both buyers had been on the original OTP at the higher rate.

Figure 2: The ABSD rate matrix for joint buyers in 2026. The highest applicable rate among co-owners applies to the whole purchase, not just to that owner’s share.

The reassessment can be material. On a S$2 million joint purchase by an SC with no prior property and an SC with one prior property, the original transaction collected ABSD only on the 1-per-cent transfer (about S$4,000). The composite reassessment applies 20 per cent ABSD to the entire S$2 million — S$400,000 — with the difference (S$396,000) recovered as additional duty. On top, IRAS imposes a 50 per cent surcharge on the avoided ABSD under the surcharge provisions of the Stamp Duties Act. Total exposure: roughly S$594,000 in additional ABSD, surcharge and interest on an originally clean-looking S$2 million buy.

The surcharge is what makes the structure so dangerous in retrospect. A buyer who would have happily paid the full ABSD upfront — perhaps deciding the higher rate was worth paying for joint-name ownership — is now exposed to half-as-much-again-on-top simply because the structure was used to sidestep it.

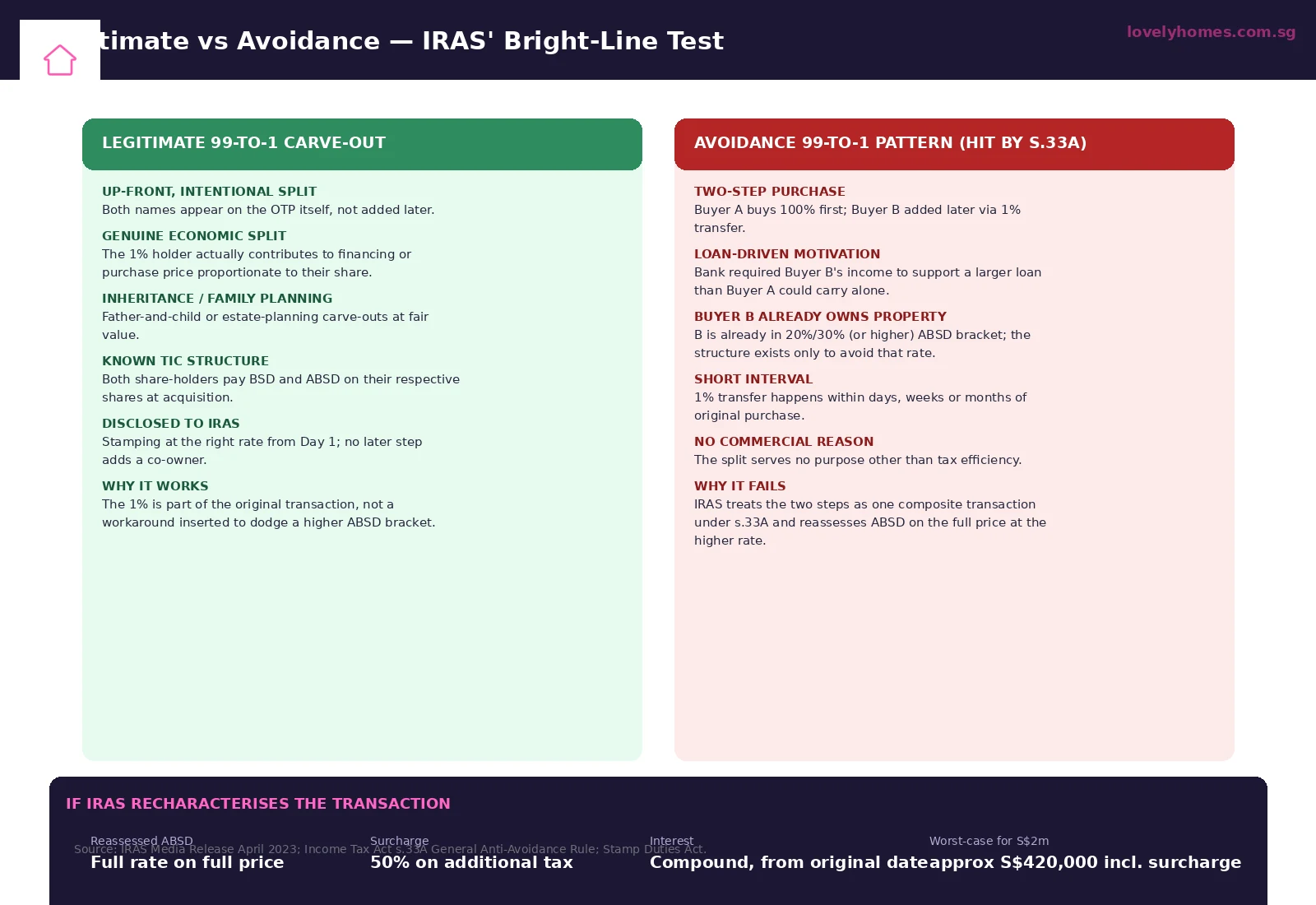

The Bright-Line Test — Legitimate vs Avoidance

IRAS does not publish a closed-list rule on which 99-to-1 structures are acceptable. The framework is principles-based, drawn from the long-established interpretation of Section 33A: a transaction or arrangement is voidable for tax purposes if its sole or dominant purpose is to obtain a tax advantage and there is no genuine commercial reason for it. The case law on Section 33A — including the leading Comptroller of Income Tax v AQQ decision — emphasises substance over form, intent over labels, and the natural commercial reality of what the parties actually did.

Figure 3: The bright-line markers IRAS uses to separate a legitimate 99-to-1 carve-out from an avoidance pattern. Time gap, contribution, intent and disclosure all matter.

Practically, four indicators tend to push a 99-to-1 split into the legitimate column. First, both names appear on the original OTP itself — the 1 per cent is part of the original transaction, not bolted on later. Second, both parties contribute economic value proportionate to their share — for example, a child contributes a small cash deposit and is rightly entered on the title for that contribution. Third, the structure has a non-tax purpose — estate planning, succession, marital-asset planning, or a parent-and-child purchase with a real intent to leave the 1 per cent in the second name. Fourth, disclosure is clean — both parties stamp at their full ABSD rate from Day 1.

Three indicators tend to push a 99-to-1 split into the avoidance column. First, the 1-per-cent owner is added after the original purchase, with no documented commercial trigger for the late addition. Second, the only practical effect of the addition is to bring the higher-rate party’s income onto a bank loan that would otherwise not have qualified at TDSR 55 per cent. Third, the time gap between the original 100-per-cent purchase and the 1-per-cent transfer is short — days, weeks, or a small number of months — and there is no intervening event (such as a marriage, an inheritance, a job change creating a new income source) that explains the delay.

The IRAS audits in 2023 focused on cases where multiple of these markers were present together. A two-step purchase by itself is not automatically voided; what IRAS looks for is the conjunction of the markers — late addition, no commercial reason, financing motivation, short gap, and the higher-rate party already in a prior-property bracket.

What “Legitimate” Looks Like in Practice

Three real-world patterns of 99-to-1 are routinely accepted by IRAS as commercially sound and not subject to anti-avoidance recharacterisation. The first is parent-and-child estate planning: a parent buys a property and includes the child as a 1-per-cent tenant-in-common to facilitate eventual succession at fair value. The 1 per cent is part of the original OTP, ABSD is paid at the parent’s full applicable rate (with the child’s portion stamped at the child’s rate, if different), and the structure has a clear non-tax purpose.

The second is marital asset structuring before divorce: a couple in the late stages of separation may carve out a 99-to-1 split to give one party a residual interest pending the matrimonial settlement, with the larger holder having the operational control to sell. As long as the carve-out is at the OTP itself and ABSD is paid at the highest rate, this is unobjectionable.

The third is commercial co-investment with documentation: a friend-of-friend joint purchase where one party puts up the bulk of the equity and the other contributes a small share for a defined investment purpose (renovation works, future development, occupancy rights). Provided ABSD is fully paid at the highest applicable rate from Day 1, IRAS has no anti-avoidance angle to pursue.

Worked Example — Mr Lee and Mrs Lee on a S$2 Million Tampines Condo

Worked Example. Mr Lee, 36, Singapore Citizen, owns one HDB flat already. Mrs Lee, 33, Singapore Citizen, has no other property. They want to buy a S$2 million private condominium in Tampines. Mr Lee’s gross income is S$14,000 a month; Mrs Lee’s is S$5,000. Mr Lee’s prior HDB will continue to be occupied by his parents. Both names are needed on the bank loan to clear the TDSR 55 per cent test on the S$1.5 million loan they have in mind.

The legitimate joint purchase. Mr and Mrs Lee both go on the OTP as tenants-in-common at any agreed split — 50/50, 99/1, 1/99, whatever. Mr Lee falls into the 20 per cent ABSD bracket (second Singapore property). The highest-rate-wins rule applies the 20 per cent rate to the entire S$2 million purchase. ABSD = S$400,000. BSD = S$64,600. The bank underwrites the S$1.5 million loan against both incomes; TDSR clears comfortably. The Lees write the cheque, take the keys, and IRAS is satisfied.

The avoidance variant (do not do this). Mrs Lee buys 100 per cent of the condo on the OTP at S$2 million. ABSD on Mrs Lee is 0 per cent (first Singapore property). BSD = S$64,600. Six weeks later, Mr Lee is added at 1 per cent for a notional consideration of S$20,000. ABSD on the 1 per cent at his 20 per cent rate = S$4,000. The household has paid roughly S$396,000 less ABSD than it would have under the legitimate joint purchase.

The IRAS reassessment. If IRAS audits the file under Section 33A and finds the financing motivation — the bank loan was sized off both incomes from the start, and there is no commercial reason for the six-week delay other than the ABSD differential — the agency reassesses the original transaction as a composite joint purchase. ABSD becomes S$400,000. The avoided amount of approximately S$396,000 attracts a 50 per cent surcharge of S$198,000. Plus simple interest from the original stamping date to the date of the IRAS notice. Total exposure: around S$594,000 in additional duty and surcharge — most of which would have been zero if the household had simply gone on the OTP together at the start.

The arithmetic is the lesson. Households who can afford to pay the ABSD on a joint purchase should do so. Households who cannot afford it should not be using a 99-to-1 to make themselves “afford” it — the 50 per cent surcharge erases the saving and adds a felt embarrassment to the file.

Summary Table — 99-to-1 Considerations 2026

Question

Answer (2026)

Is a 99-to-1 split itself illegal?

No. Tenancy-in-common at any defined share is recognised under the Land Titles Act.

Is an upfront 99-to-1 acceptable?

Yes. As long as both names are on the original OTP and ABSD is paid at the highest applicable rate.

Is a two-step 99-to-1 acceptable?

Only if there is a documented commercial reason for the delay. If not, IRAS may invoke Section 33A.

What rule applies on joint name?

Highest ABSD rate among the buyers applies to the entire purchase price.

Surcharge if avoidance is found?

50 per cent surcharge on the avoided ABSD, plus simple interest from original stamping date.

Lookback period for IRAS

Up to six years from original stamping under Section 33A.

Legitimate alternatives

Decoupling (sale of one share to the other after MOP), staggered purchases over time, or paying full ABSD upfront.

Cases reviewed in 2023 probe

166 cases; estimated S$60 million in ABSD and surcharge recovered.

Does HDB allow 99-to-1?

Generally not for HDB purchases — HDB applies its own joint-tenancy rules and prohibits decoupling since 10 April 2018.

What This Means for You

The 99-to-1 ABSD episode is one of the clearest illustrations of how Singapore’s tax authorities use a principle-based General Anti-Avoidance Rule rather than a closed-list code. There is no specific rule banning 99-to-1 splits; there is a broader rule that any tax-driven structure with no commercial purpose can be recharacterised. Households making property co-ownership decisions in 2026 should treat this less as a single closed file and more as a continuing posture by IRAS toward stamp-duty avoidance.

The practical advice is simple. If you and a co-buyer want to be on the title, get on the title at the OTP. Pay ABSD at the highest applicable rate from Day 1. Do not invent a delayed structure to manage the bank loan unless there is a real, documentable, non-tax reason for the delay. If you are unsure whether your circumstance qualifies, consult a Singapore conveyancing solicitor before signing the OTP — restructuring is far cheaper than reassessment.

For households who genuinely cannot afford the higher ABSD bracket — for example, an upgrader couple where one spouse already owns property — the legitimate alternative is decoupling after the Minimum Occupation Period on the existing flat (if HDB, subject to the 2018 prohibition), or a staggered purchase strategy over time. These approaches respect the cooling-measure intent and do not invite the 50 per cent surcharge that attaches to recharacterised avoidance.

What Might Come Next

The 99-to-1 enforcement was a high-visibility action that has materially shifted market behaviour since 2023. Conveyancing solicitors now flag two-step structures as a matter of course; banks increasingly require ABSD payment confirmation before disbursing on transfers; and IRAS has signalled that anti-avoidance scrutiny extends to other patterns where the form of a transaction differs materially from its substance — for example, trust structures, nominee purchases, and serial divorce-and-remarriage carve-outs in property settlements.

Looking forward, two areas of policy attention deserve watching. First, the Stamp Duties Act may be tightened to make composite-transaction recharacterisation more procedurally straightforward, replacing the case-by-case Section 33A review with a clearer presumption against short-interval transfers. Second, the surcharge level — currently 50 per cent — has historical precedents at higher levels in other Singapore tax regimes, and could be revisited if avoidance patterns continue to surface. The direction of policy travel since 2010 has been toward closing perceived loopholes, not loosening them; households should plan accordingly.

Frequently Asked Questions

Is the 99-to-1 split itself illegal in Singapore?

No. Tenancy-in-common at any defined share — including 99/1 — is a recognised form of co-ownership under the Land Titles Act. What IRAS scrutinises is the two-step pattern where the 1 per cent is added after the original 100 per cent purchase, with no commercial reason other than to avoid the higher ABSD rate that would have applied if both buyers had been on the OTP from the start.

If both names are on the original OTP, do I avoid the IRAS issue?

Yes. The April 2023 IRAS probe focused exclusively on two-step transactions where the second co-owner was added later. An upfront 99-to-1 split where both names appear on the original Option to Purchase, and ABSD is paid at the highest applicable rate from Day 1, is not subject to anti-avoidance recharacterisation.

What is the IRAS surcharge if avoidance is found?

50 per cent on the additional ABSD assessed, plus simple interest from the original stamping date. On a S$2 million purchase where avoided ABSD is S$396,000, the surcharge is S$198,000 — bringing the total reassessment to roughly S$594,000 plus interest. The surcharge is what makes anti-avoidance recharacterisation economically punitive: paying upfront would have been about two-thirds of the post-audit cost.

How far back can IRAS reassess?

Up to six years from the original stamping date under Section 33A. In practice, the 2023 probe looked at transactions over the preceding several years where the two-step pattern was identifiable from records. The lookback window means structures executed in 2020–22 remained exposed when the probe was announced.

Can I do a 99-to-1 for an HDB flat?

Generally not. HDB applies its own joint-tenancy rules — most BTO and resale purchases must be in joint tenancy, not tenancy-in-common — and decoupling has been prohibited since 10 April 2018 to prevent ABSD-avoidance manoeuvres on second properties. The 99-to-1 conversation is largely confined to private property purchases.

My family bought a property in 2021 with a 99-to-1 split. Should I worry?

Read the structure carefully. If both names appeared on the original OTP and ABSD was paid at the highest applicable rate at the time, there is nothing to worry about — that is a legitimate upfront 99-to-1. If the second name was added after the original purchase and the only motivation was financing or ABSD avoidance, the file is potentially exposed under Section 33A’s six-year lookback. Consult a solicitor or tax adviser to assess the position; voluntary disclosure ahead of an audit attracts considerably more lenient treatment than reactive disclosure.

Are there legitimate alternatives that achieve a similar financing outcome?

For households where one party already owns property and the other does not, the cleanest alternatives are: (a) pay the higher ABSD rate upfront on a joint purchase; (b) execute the purchase under the non-owning party’s name with the financing structured to qualify on that party’s income alone; or (c) wait until the existing property is sold (subject to the 30-month decoupling rule for ABSD remission on a Singaporean married couple’s first new property). Each has trade-offs, but none invites a Section 33A reassessment.

Disclaimer

This article is general guidance on Singapore’s stamp-duty framework as administered by the Inland Revenue Authority of Singapore as at the publication date and is not financial, tax or legal advice. Anti-avoidance enforcement under Section 33A of the Income Tax Act 1947 and the corresponding provisions of the Stamp Duties Act is highly fact-specific; the application to any particular transaction depends on the documents, sequence and intent. For the rule that applies to your circumstances, consult IRAS, a licensed Singapore solicitor and a registered tax practitioner. Always rely on official sources — IRAS, the Stamp Duties Act and the Income Tax Act 1947 — for the latest position before transacting.

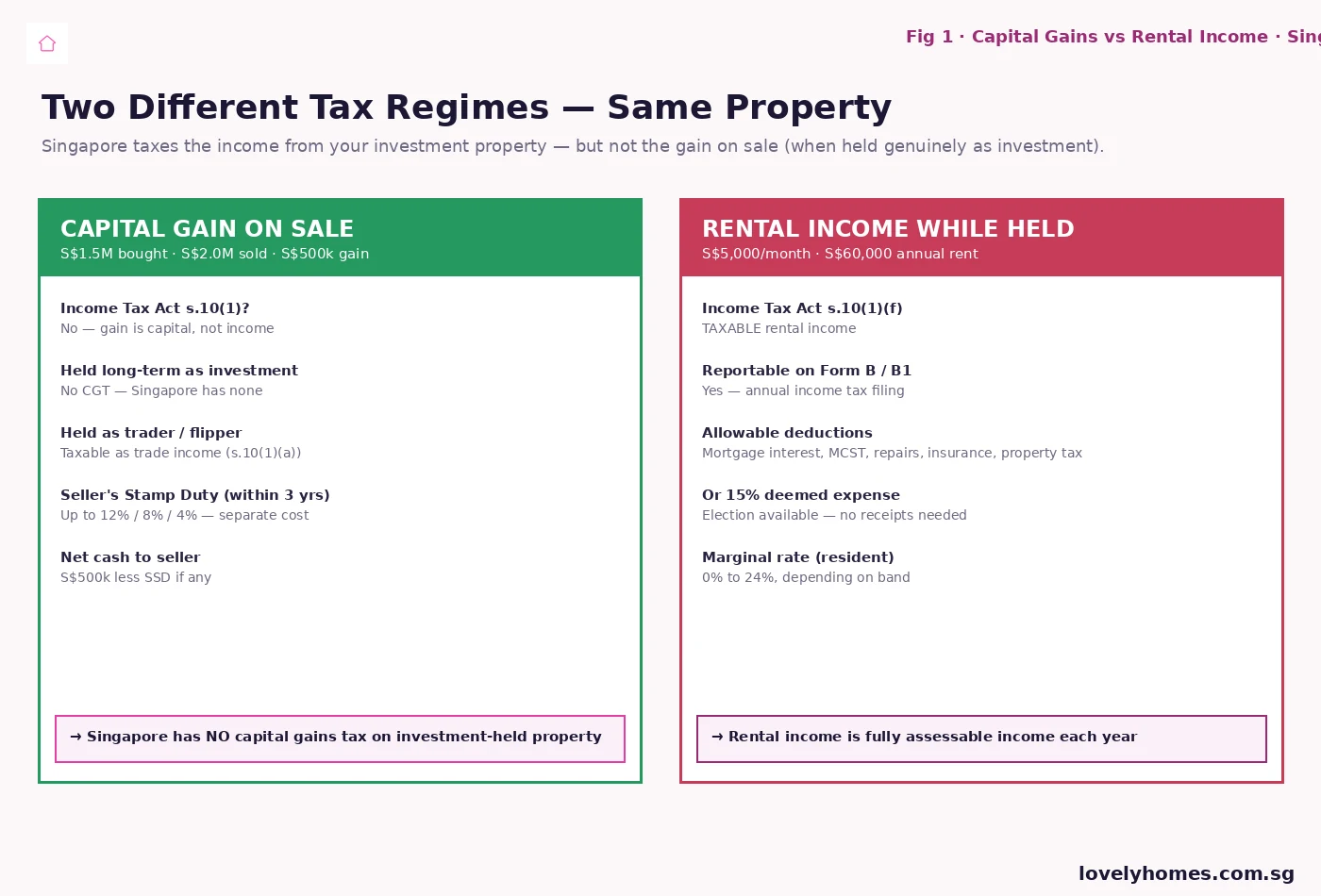

Capital gains tax on property in Singapore 2026 — that is the search every aspiring property investor types into Google before clicking Buy. The short answer is Singapore has no capital gains tax when you sell a property held genuinely as long-term investment. The longer answer is that rental income while you hold the property is fully taxable, and a gain on sale can be reclassified as taxable trade income if IRAS decides you behaved like a property trader rather than an investor. Get either nuance wrong, and you can hand the Inland Revenue Authority of Singapore a tax bill running into six figures.

This guide walks you through both halves of the property-investment tax regime in 2026: the capital-gains side (what you pay on disposal — usually nothing, sometimes everything, depending on intent) and the rental-income side (what you pay every year you let out the property). All figures and rules reflect the framework administered by the Inland Revenue Authority of Singapore (IRAS) under the Income Tax Act 1947.

Quick Answer — Property Tax for Singapore Investors at a glance

Capital gains tax (CGT): none in Singapore. A long-held investment property sold at a profit attracts zero CGT.

Rental income tax: fully assessable income. Rent is reported on your annual Form B / B1 and taxed at your marginal rate (0% to 24% for tax residents).

Deductions: mortgage interest, MCST/management fees, repairs, property tax, agent fees, fire insurance — all deductible against rental income.

15% deemed expense: alternative to actual-expense claims, since YA 2016. Mortgage interest is still claimable on top of the 15%.

“Trader” reclassification: IRAS may treat a gain as trade income taxable at 0–24% if the badges of trade are met (frequency, holding period, financing, intent).

Seller’s Stamp Duty (SSD): separate from income tax. Up to 12% for sales within the first year, 8% within two, 4% within three.

Property Tax: separate annual property tax (4–32% of Annual Value) levied by IRAS regardless of rental status.

Why Singapore Does Not Have a Capital Gains Tax

Singapore is one of a handful of jurisdictions in the world that does not levy a general capital gains tax. The Income Tax Act 1947 taxes income — defined under section 10(1) as gains from a trade, profession, or vocation, plus dividends, interest, rents, royalties, and various other categories. A gain on sale of a long-held asset is, in principle, a capital gain rather than income, and falls outside the section 10(1) net.

This is policy, not oversight. The Singapore government has long taken the view that low capital-mobility costs are a competitive advantage for the financial centre and the housing market. The same principle covers shares, corporate sales, business goodwill, and — critically for property investors — long-held investment properties. The cooling-measure regime taxes property at the buying side (BSD, ABSD) and the disposal side (SSD if disposed within three years), but a clean investment hold-and-sell at year five is untaxed at the gain.

Figure 1: The two-tax framework — Singapore does not tax the capital gain on a long-held investment property, but rental income is taxable income each year.

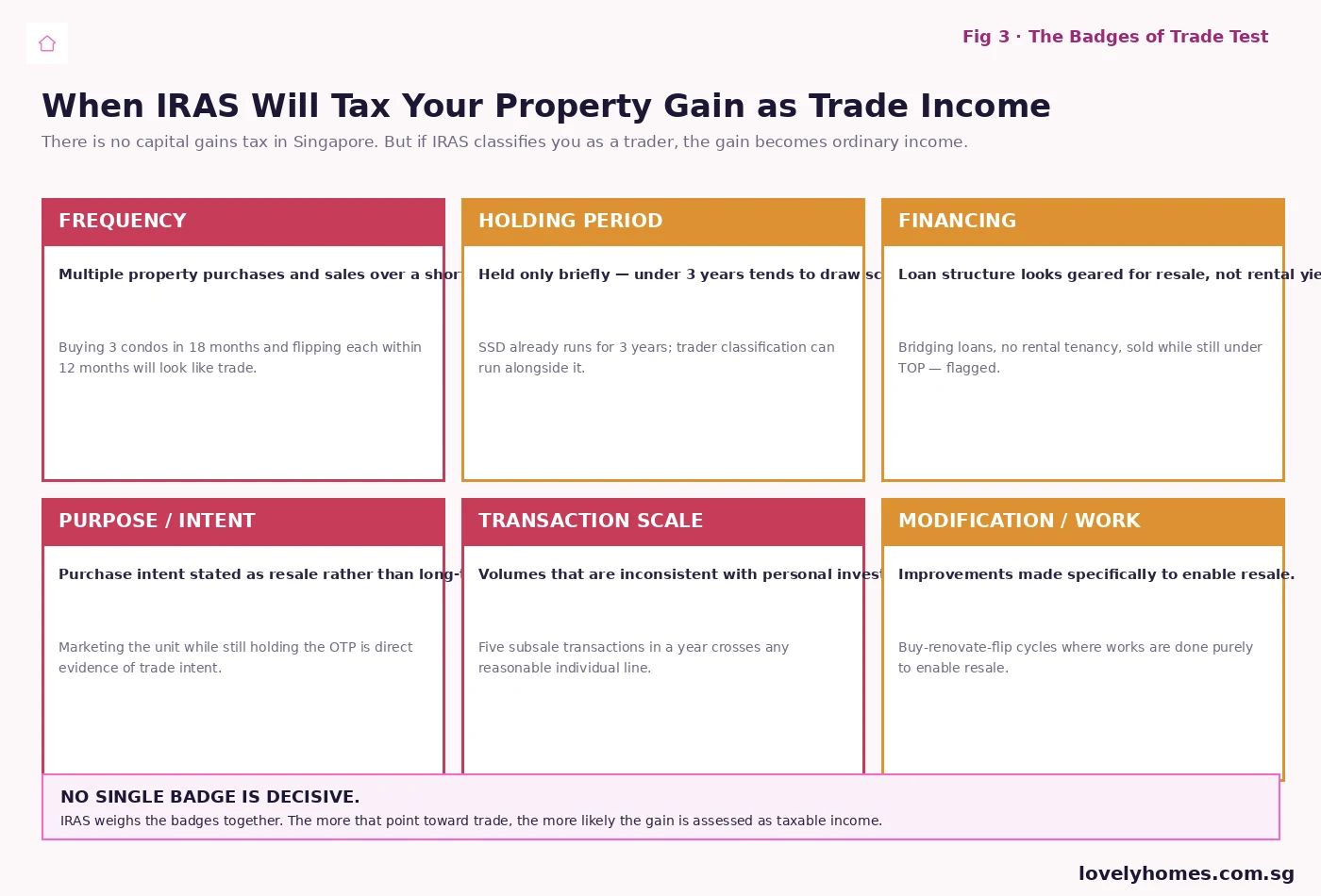

The Trader Trap — When IRAS Reclassifies Your Gain

The capital gains exemption is not unconditional. IRAS reserves the right to reclassify a property gain as trade income if the taxpayer’s behaviour resembles property trading rather than long-term investment. The legal hook is section 10(1)(a) of the Income Tax Act, which taxes “gains or profits from any trade, business, profession or vocation”. Once a gain is reclassified as trade income, it is fully taxable at the individual’s marginal rate (up to 24% for tax residents) or the prevailing 17% corporate rate for entities.

Singapore’s courts and the Comptroller of Income Tax apply the badges of trade test, a doctrine inherited from UK case law and refined locally through cases such as Comptroller of Income Tax v IA and the IRAS e-Tax Guide on the matter. The badges are weighed together — no single factor is decisive — and they ask, in essence, “did this taxpayer behave like an investor or like a trader?”

Figure 3: The six classical badges of trade. The more that point toward trade activity, the more likely IRAS will assess the gain as taxable trade income.

The practical implication for the typical Singapore property investor is straightforward: hold the property for at least three to five years, generate genuine rental income during the hold, and document your investment intent (rental tenancies, declared rental income, no immediate resale marketing). For most owner-occupier-then-investor patterns, the badges of trade are not met and the gain is non-taxable. For someone buying multiple units off-plan at a single launch and subsaling within 12 months, the badges of trade are very likely met and the gains will be taxable.

Rental Income — The Annual Tax You Cannot Avoid

Owning an investment property does not get you out of income tax. Whatever rent you collect from a tenant in a Singapore property is fully assessable income in the year it is earned, taxed at your marginal rate. Singapore tax residents face a progressive band running from 0% (first S$20,000) to 24% (income above S$1,000,000) for Year of Assessment 2026. Non-residents pay a flat 24% on rental income, with limited deductions.

The reporting mechanism is your annual income tax return — Form B (self-employed) or Form B1 (employees) — on which rental income from immovable property in Singapore is declared in the “Rent from Property” section. Rental from properties held in joint names is split between the joint owners according to legal share. Rental from a property held in a private trust may be assessed differently — that needs specific tax advice.

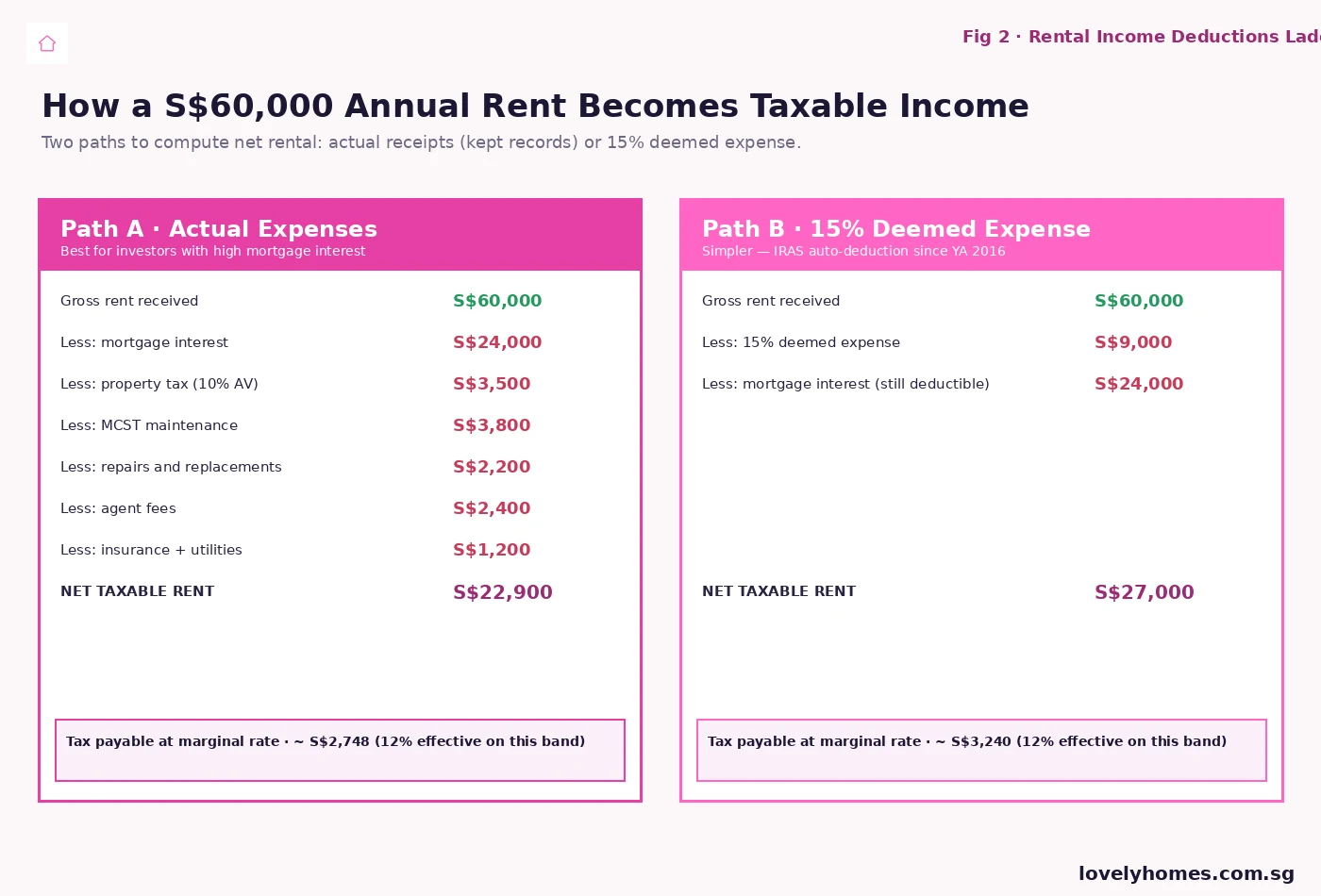

Allowable Deductions — Two Paths

The good news is that net rental income, not gross, is what gets taxed. Singapore allows a generous list of deductions for the costs of producing rental income, with two paths to the calculation.

Figure 2: The two deduction paths for rental income — Path A (actual receipts) usually wins for landlords with a sizeable mortgage; Path B (15% deemed) is administratively simpler.

Path A — Actual expenses. The traditional method requires you to keep receipts and claim the actual expenses incurred. Allowable items include the interest portion of your mortgage instalment (not the principal), property tax, MCST or management corporation fees, repairs and replacements (including replacing furniture and appliances), property agent commission for finding the tenant (capped at the equivalent of one month’s rent for first leases), fire insurance, and utilities you pay directly. You cannot deduct your initial purchase costs, the principal repayment of your mortgage, or capital improvements that extend the property’s life.

Path B — 15% deemed expense. Since Year of Assessment 2016, IRAS has offered an alternative under which you simply deduct 15% of your gross rent as deemed expense, without needing receipts for non-mortgage costs. Critically, you can still claim mortgage interest on top of the 15%. Path B is administratively far simpler and tends to win when your non-mortgage costs are low (newer condos with low MCST, no major repairs, no agent fees in renewal years). Path A wins when your non-mortgage costs are heavy or when you incurred significant repairs in the year. You can switch between the two methods year to year and per property.

Worked Example — Mr Tan’s S$1.5M D15 Investment Condo

Mr Tan, a 42-year-old Singapore Citizen tax resident, bought a S$1.5 million condo in District 15 in 2022 as his second property (paying ABSD of 20% — S$300,000 — at the time). He moved out of his old marital home and rented out the new condo at S$5,500 per month. In 2026 he is filing his Year of Assessment 2026 return covering rental for calendar year 2025. Below is the actual tax he will pay.

Step 1 — Gross rent. 12 × S$5,500 = S$66,000.

Step 2 — Path A (actual expenses). Mortgage interest on the outstanding S$1.05 million loan at an effective 3.4% averaged across the year = approximately S$35,700. Property tax at the non-owner-occupier rate (12% to 36% of Annual Value) on an Annual Value of S$54,000 ≈ S$8,200. MCST at S$420/month = S$5,040. One small repair of S$1,800. Agent fee (re-let in 2025, half-month commission on a renewal) ≈ S$2,750. Fire insurance S$300. Total expenses S$53,790. Net taxable rent = S$66,000 − S$53,790 = S$12,210.

Step 3 — Path B (15% deemed + mortgage interest). 15% × S$66,000 = S$9,900 deemed expense. Plus actual mortgage interest of S$35,700. Total deductions S$45,600. Net taxable rent = S$66,000 − S$45,600 = S$20,400.

Step 4 — Path A wins by S$8,190 of taxable income because Mr Tan’s non-mortgage costs (S$18,090) are well above 15% of gross rent (S$9,900). At Mr Tan’s marginal rate, the difference saves him roughly S$1,560 in tax. He files Path A and keeps his receipts.

Step 5 — When Mr Tan eventually sells. Assume Mr Tan sells the condo in 2030 for S$1.85 million — gain of S$350,000. He held for eight years. He rented continuously (clear investment intent). He has only one investment property. The badges of trade are not met. His S$350,000 gain is a non-taxable capital gain. He pays no tax on the gain itself, although he will have paid SSD if the sale had been within three years (zero SSD beyond year three) and BSD on his original purchase.

What Happens If You Are Classified as a Trader

If IRAS reclassifies a property gain as trade income, the consequences cascade. The gain is taxed at the marginal rate. Prior years may be reopened if the trading pattern goes back further. GST may apply if the trading scale is significant enough to constitute a taxable supply of services (the supply-of-property GST framework is narrow, but it exists). For a high-frequency flipper with a S$300,000 gain on each of three units in a single year, the tax bill at the top marginal rate is meaningful — and the SSD on early disposals adds another layer.

The cleanest defence to a trader-classification challenge is documentation. Keep tenancy agreements and rental receipts for every year of the hold. Keep correspondence showing investment intent. Avoid marketing the unit for resale while the OTP is still outstanding. Avoid bridging loans that scream resale-to-resale. Treat each purchase like a long-term investment, not a 12-month flip.

Property Tax — A Separate Annual Charge

Property tax is sometimes confused with income tax on rental, but it is a different head of tax administered by IRAS. Every owner of immovable property in Singapore pays property tax annually, calculated as a percentage of the Annual Value (AV) of the property — IRAS’ estimate of the market rent the property could fetch in a year, regardless of whether it is actually rented. Owner-occupier rates are progressive from 4% to 32% of AV (Budget 2024 calibration, in force from 2025). Non-owner-occupier rates are higher, running from 12% to 36% of AV. Property tax is paid quarterly or annually and is fully deductible against rental income for income-tax purposes.

For Mr Tan’s S$1.5M condo with an AV of S$54,000 (typical for a mid-D15 condo), the non-owner-occupier property tax in 2026 is in the range of S$8,200 — which is the figure he claimed as a deduction in Step 2 above. Owner-occupied, the same property would attract roughly S$2,200 of property tax — a S$6,000 annual swing that materially affects the holding-cost arithmetic of an investor.

Comparison with Other Asian Markets

Singapore’s no-CGT-on-investment-property position is at one end of the regional spectrum. Hong Kong has no CGT either, treating long-held property gains as capital and taxing only rental income at the standard 15% property-tax rate (with allowable expenses). Japan taxes capital gains on property at 30.63% if held five years or less, and 15.315% if held longer (national portion). South Korea taxes property capital gains at 6–45% with various adjustments and surcharges that can drive the effective rate above 50% for short-term flips of multiple homes. Australia taxes capital gains at the marginal rate with a 50% discount for assets held over 12 months. Singapore’s regime is, on balance, the most investor-friendly in the region — reinforced by the deductibility of mortgage interest and the optional 15% deemed-expense election on the rental side.

What Might Come Next

The Singapore government has periodically reviewed whether to introduce a capital gains tax, with the question raised most recently in the context of the 2022 Wealth Tax Working Group discussions and the post-COVID fiscal review. The Ministry of Finance’s stated position has been that a CGT would conflict with Singapore’s positioning as a regional capital hub and would not raise meaningful revenue from the property segment relative to existing stamp duties (BSD and ABSD already capture transaction-side cooling). The watch-points for 2026–28 are: (a) sustained widening of inequality metrics that make capital-gains taxation politically more urgent; (b) significant rental-yield compression that would invite a tightening of the deemed-expense scheme; and (c) any reform of property tax bands at Budget 2026 (announced February 2026) that reset the AV thresholds. None of these are signalled by MOF as imminent at this writing.

Summary Table — Singapore Property Investment Tax 2026 at a Glance

Tax / Rule

2026 Position

Notes

Capital gains tax — long-held investment

0%

Singapore has no CGT for investment-held property.

Trade income reclassification

0% to 24%

Applies if badges of trade are met (frequency, intent, holding period).

Rental income — tax-resident individual

0% to 24%

Progressive band; YA 2026 schedule. Net of allowable deductions.

Rental income — non-resident individual

24% flat

Limited deductions available.

15% deemed-expense election

Available since YA 2016

Mortgage interest still deductible on top of the 15%.

Property tax — owner-occupier

4% to 32% of AV

Budget 2024 calibration, effective from 2025.

Property tax — non-owner-occupier

12% to 36% of AV

Higher rates for investment property.

Seller’s Stamp Duty

Up to 12% / 8% / 4%

Three-year holding-period schedule, separate from income tax.

Buyer’s Stamp Duty

1% to 6%

Tiered on purchase price; one-off purchase-side cost.

Additional Buyer’s Stamp Duty

0% to 65%

By buyer profile; 27 April 2023 cooling-measures schedule.

Frequently Asked Questions

Does Singapore have a capital gains tax on property?

No, not on property held genuinely as long-term investment. The Income Tax Act 1947 taxes income — gains from a trade, dividends, interest, rents — but not capital gains on long-held assets. A condo bought as investment, rented out for several years, and sold at a profit attracts no income tax on the gain. The exception is when IRAS classifies the taxpayer as a property trader using the badges of trade test, in which case the gain is reassessed as trade income and taxed at the marginal rate.

What are the badges of trade?

The classical six badges, applied by IRAS: (1) frequency of transactions; (2) length of holding period; (3) financing structure (geared for resale or for rental yield); (4) purpose or intent at purchase; (5) scale of transactions; (6) modifications or work done specifically to enable resale. No single badge is decisive — IRAS weighs them together. A pattern of multiple short-hold flips with bridging loans and active resale marketing is heavily indicative of trading; a long-hold, rented-out, single-investment pattern is heavily indicative of investment.

Is rental income taxable in Singapore?

Yes. Rental income from immovable property in Singapore is fully assessable income for tax residents, taxed at the marginal rate (0% to 24% for YA 2026). Non-residents pay 24% flat. You declare rental income on your annual Form B or Form B1, alongside other income sources. Net rental — gross rent less allowable deductions — is what is actually taxed.

What can I deduct from my rental income?

Mortgage interest (not principal), property tax, MCST or management fees, repairs and replacements, fire insurance, agent commission for finding tenants (capped at one month’s rent for first leases), and utilities you pay directly. You cannot deduct your original purchase costs, mortgage principal repayments, or capital improvements that extend the property’s life. You can also elect the 15% deemed-expense option in lieu of itemised non-mortgage deductions, on top of which mortgage interest is still claimable.

Can I switch between actual expenses and the 15% deemed-expense method?

Yes. The election is annual and per-property, so you can pick whichever method delivers the lower taxable rent each year. Use the actual-expense path when your non-mortgage costs (MCST, repairs, agent fees) are heavy in a particular year. Use the 15% deemed path when those costs are light and the simplicity is worth the small tax difference.

Is property tax the same as income tax on rental?

No. They are two separate taxes administered by IRAS. Property tax is an annual tax on the ownership of immovable property, calculated as a percentage of the Annual Value, and applies whether or not you rent the property out. Income tax on rental is an annual tax on the rent you actually receive. Property tax is itself a deductible expense against rental income for income-tax purposes.

What if I let out my property for short-term stays?

For private residential property, short-term stays under 90 days are not permitted under URA’s residential-zoning rules — running such a lease attracts URA enforcement separate from the tax question. Where short-term lets are legitimate (serviced apartments, certain shophouse zones), the rental income is still assessable in the normal way, and GST can apply if the supplier crosses the registration threshold. Short-stay listings on platforms like Airbnb in standard residential property are non-compliant with URA’s planning rules and should not be assumed to be available as an investment strategy.

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. Singapore’s tax framework is administered by the Inland Revenue Authority of Singapore (IRAS) under the Income Tax Act 1947 and the Property Tax Act, and rules are revised through annual Budgets and IRAS e-Tax Guides. Always verify the current position on the IRAS website and consult a licensed tax adviser, financial planner, or accountant for advice on your specific circumstances.

Seller’s Stamp Duty (SSD) is the Singapore Government’s anti-flipping tax. If you sell a residential property within three years of buying it, you pay a percentage of the sale price — up to 12% — on top of every other selling cost. Get the holding period wrong by even a single day, and a profitable sale can flip into a six-figure loss.

This guide walks you through SSD in 2026: who pays it, how the rate ladder works, when the holding clock starts and stops, who is exempt, and the strategies sellers actually use to manage it. All rates reflect the framework in force since 11 March 2017, which remains current. For the authoritative figures, always check the IRAS Seller’s Stamp Duty page.

Quick Answer — SSD at a glance

SSD applies only to residential property sold within 3 years of acquisition.

The clock starts on the date you signed the OTP or accepted the S&P — not the day you collected the keys.

Payable within 14 days of contract for sale, on the higher of price or market value.

Most short-term sales are caught: divorce sales, job relocations, second properties — SSD applies to nearly all of them.

Industrial property has a separate (shorter) ladder; commercial property is exempt.

What Is SSD and Why Does It Exist?

SSD is a transaction tax levied on the seller of a residential property in Singapore when the property is sold within a defined holding period. It is administered by the Inland Revenue Authority of Singapore (IRAS), calculated on the higher of the sale price or the market value, and payable within 14 days of the contract for sale.

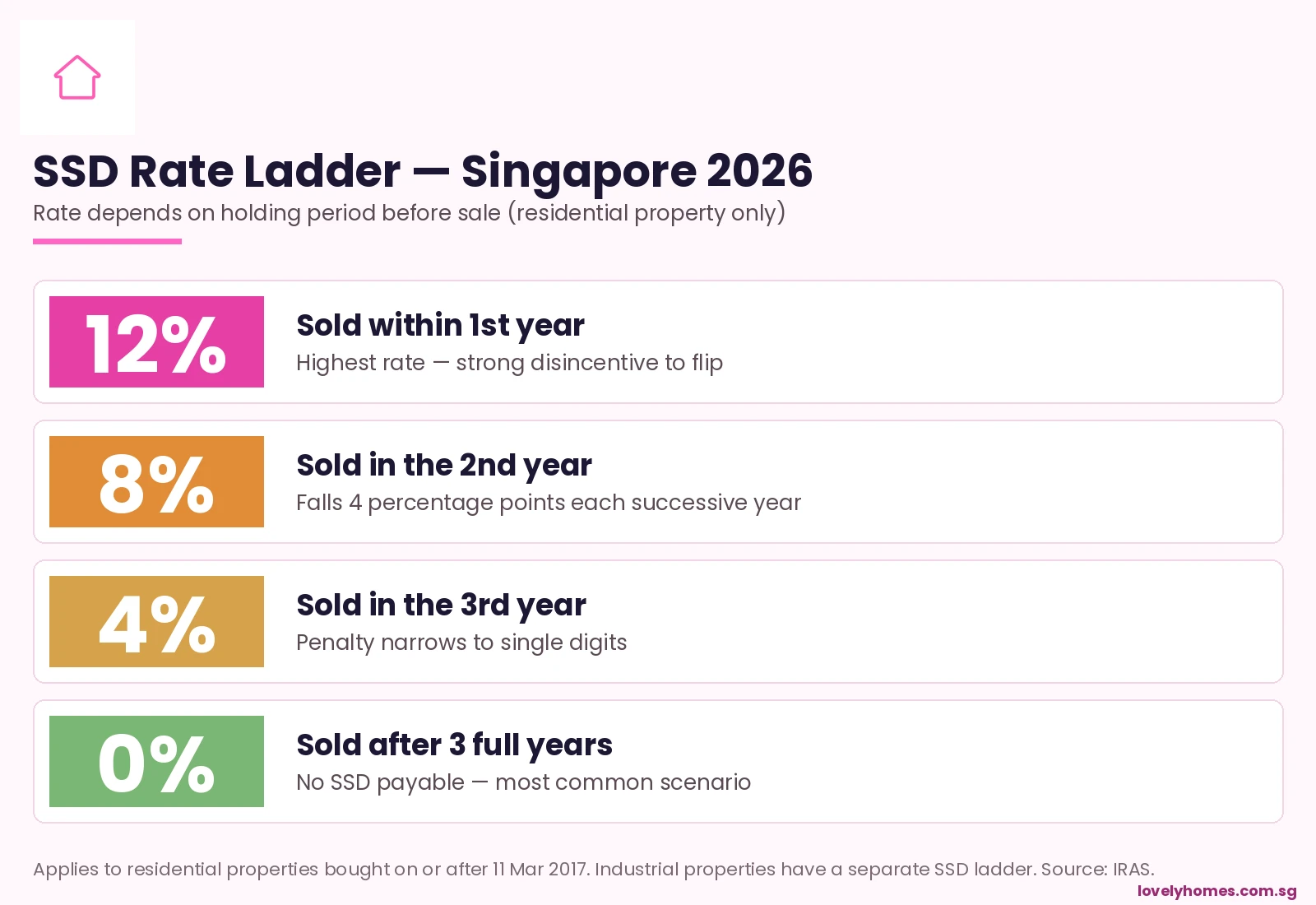

The tax was first introduced in February 2010 and progressively widened in 2011 and 2013 as part of the Government’s suite of property cooling measures. The most recent recalibration was in March 2017, which shortened the SSD holding period from four years to three and lowered the headline rate from 16% to the present 12% — a deliberate easing aimed at supporting genuine homeowners rather than speculators. The 2017 framework is still the live rule book in 2026.

The policy goal is simple: discourage speculative flipping while leaving genuine end-users untouched. By the time you have held a private condo or HDB flat for three full years, the cooling-measure case for taxing your sale is gone, and SSD falls to zero.

Seller’s Stamp Duty Singapore 2026 — the cost of selling too soon.

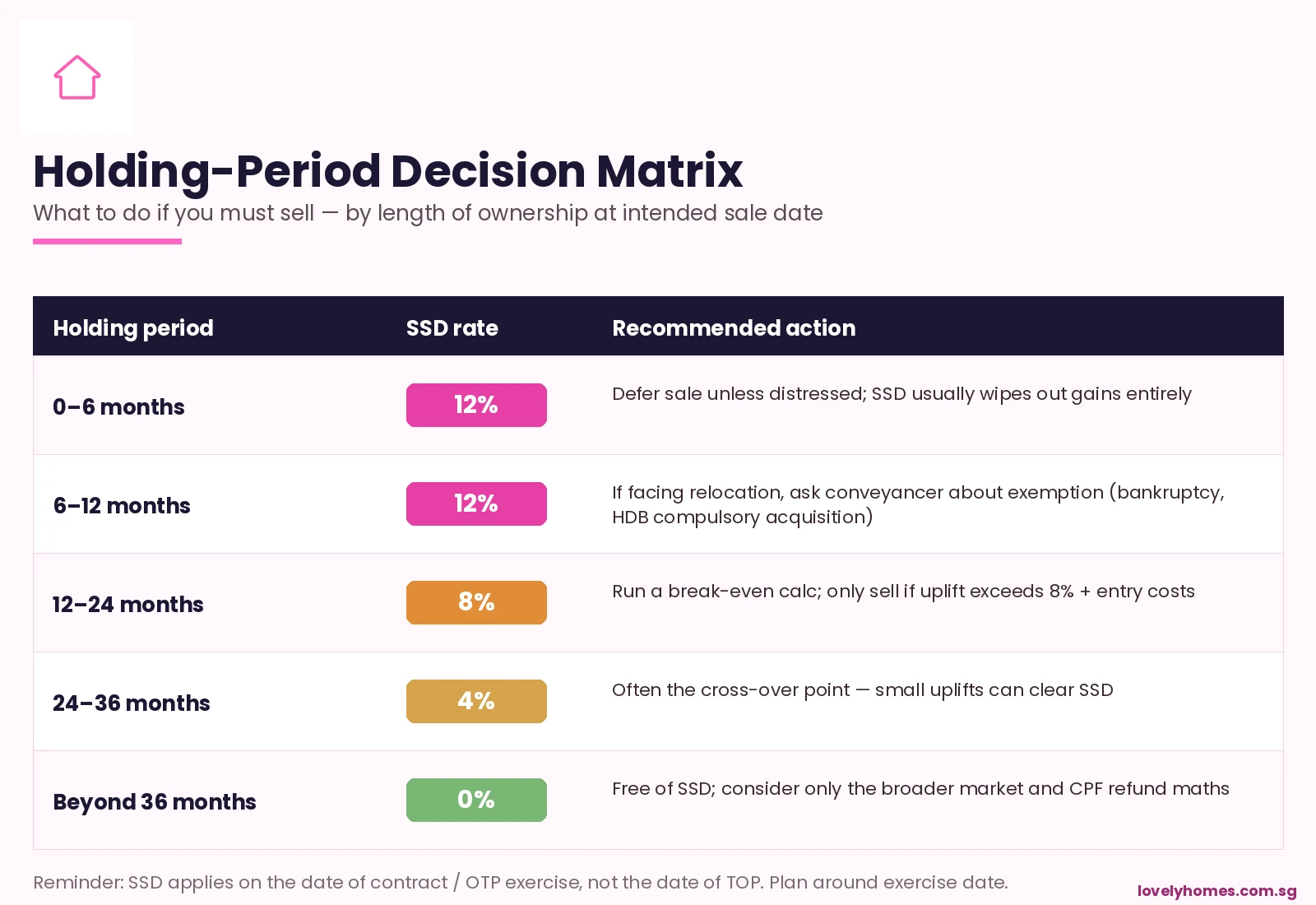

The 2026 SSD Rate Ladder

The rate you pay depends entirely on how long you held the property before signing the contract for sale. The ladder is steep at the top and falls four percentage points each subsequent year:

Figure 1: SSD rate ladder by holding period — residential property, 2026.

Holding period at sale

SSD rate

Apparent on a S$1.5M sale

Up to 1 year (within 1st year)

12%

S$180,000

More than 1 to 2 years

8%

S$120,000

More than 2 to 3 years

4%

S$60,000

More than 3 years

0%

Nil

The rate is applied to the higher of the contracted sale price or IRAS’s assessed market value — sellers cannot lower their SSD bill by deliberately under-pricing a transaction.

When Does the Holding Clock Start — and Stop?

This is where most disputes arise, because the holding period is calculated to the day. The general rule is:

Start: the date the buyer signs the Option to Purchase (OTP) or, if there is no OTP, the date of the Sale & Purchase Agreement (S&P).

End: the date the buyer signs the next OTP or S&P when reselling.

Note carefully — the keys handover (TOP for new condos, vacant possession for resale) is irrelevant to SSD. A buyer who signs an OTP on 1 March 2024 and signs the next OTP on 28 February 2027 has held for one day under three years — SSD at 4% applies. Sign on 2 March 2027 and SSD drops to zero. Conveyancers routinely time exercise dates around this calendar boundary.

For new launches under construction, the start date is the OTP exercise date, not the TOP date. This means a buyer who signed an OTP in early 2023 for a project that only TOP’d in 2026 is already past the SSD window when they collect the keys.

Who Is Exempt or Remitted?

The exemptions list is narrow. SSD remission is granted only in specific situations, including:

HDB flats — not subject to SSD because HDB has its own Minimum Occupation Period (MOP) regime, which generally bars resale within five years.

Compulsory acquisition by the State (for example, road or MRT line widening).

Bankruptcy of the owner, with proof of insolvency proceedings.

Owners required by HDB to sell on grounds of policy violation.

Inherited property — the holding period is reckoned from the original purchase by the deceased, not the date of inheritance.

Property transferred between spouses as part of a court-ordered division on divorce, in some cases.

Standard life events — relocation overseas for work, family expansion, or financial difficulty — are not grounds for SSD remission. The tax applies even if the seller is selling at a loss.

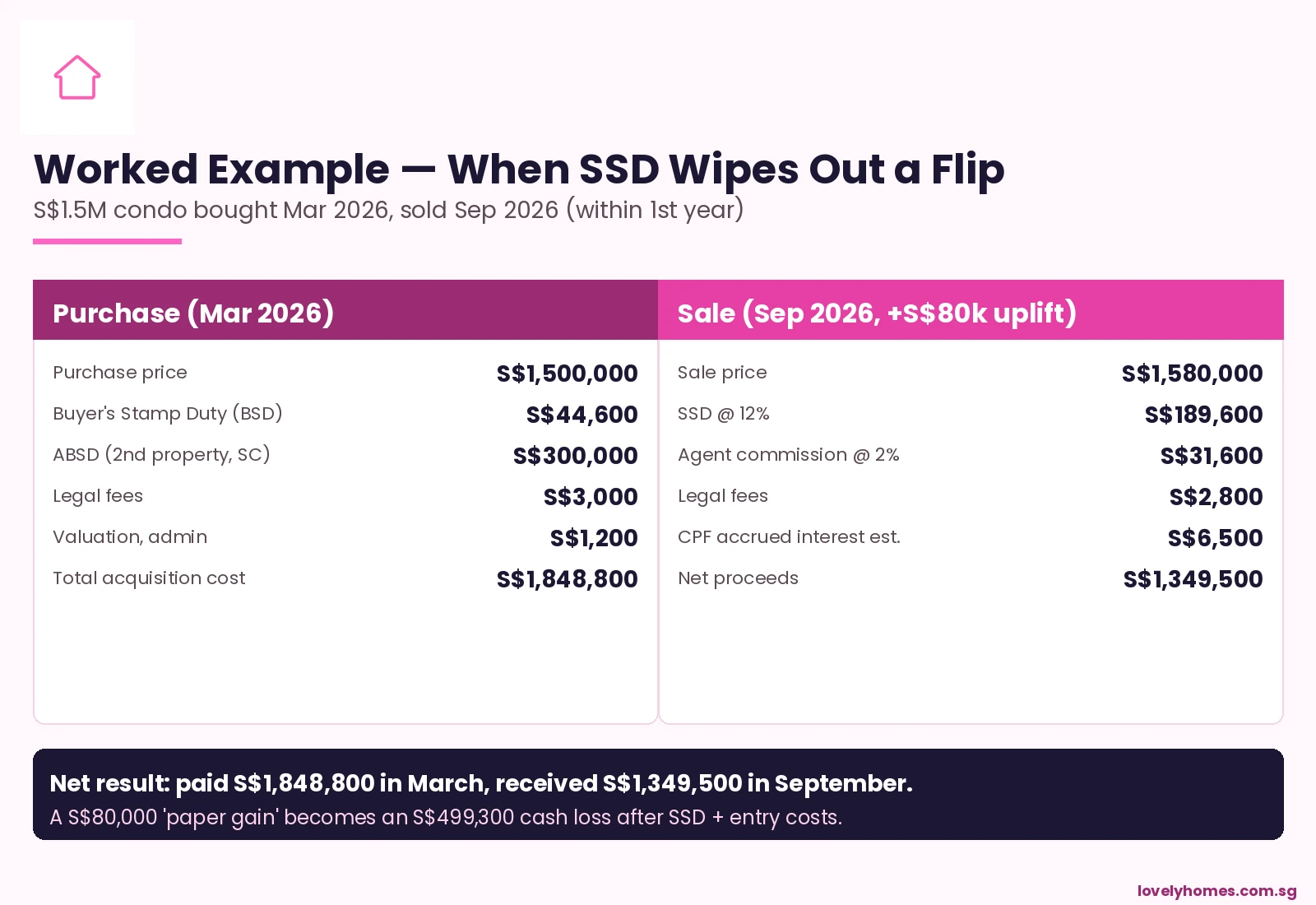

Worked Example — A S$1.5M Condo Flipped in 6 Months

Imagine a Singapore Citizen who buys a S$1.5M private condo as a second property in March 2026, then receives a job offer in Hong Kong six months later and decides to sell at S$1.58M (a S$80,000 paper gain). Here is what the maths actually looks like:

Figure 2: Worked example — an apparent S$80k gain becomes an S$499k cash loss when SSD is applied.

Acquisition costs (BSD, ABSD on the second property at 20%, legal fees) total S$348,800. The owner has paid S$1,848,800 to take possession. Six months later, the sale at S$1,580,000 attracts SSD at 12% (S$189,600), broker commission, legal fees, and CPF accrued interest. Net proceeds: S$1,349,500. Cash loss: S$499,300.

The lesson is brutal: SSD is designed to make short-term residential property sales economically unattractive even when the underlying market has moved up. For most second-property buyers, the only way to make the maths work is to stay invested for at least three years.

Strategies Sellers Actually Use

If you find yourself needing to sell within the SSD window, there are a small number of strategies practitioners commonly consider:

1. Run the holding-period calendar to the day

Conveyancers often time the OTP issue and exercise so that the sale falls just outside the next rate band. Selling on day 365 versus day 367 of the second year can mean a four-percentage-point swing on the sale price.

Figure 3: Decision matrix — what to do if you must sell, by length of ownership.

2. Rent out instead of selling

If holding-period maths do not work, leasing the unit until SSD falls to zero can preserve value. Singapore rental yields on private condos run 3.0–3.8% gross in 2026, which often covers the carrying cost of the mortgage during the wait.

3. Decoupling within marriage

Where one spouse needs to free up ABSD allowance for a future purchase, transferring a property between spouses (a Part-Disposal arrangement) may attract SSD on the transferred share. Practitioners check carefully whether the holding clock survives the transfer.

4. Swap residential for commercial

Commercial property (offices, shops) is not subject to SSD. Investors with a short horizon sometimes pivot from residential plays to commercial plays specifically to avoid the SSD window. Commercial does carry GST, however, so the trade-off is real.

SSD on HDB — Yes, Technically — But MOP Comes First

Strictly, SSD does not apply to HDB flats sold during the SSD window because the HDB Minimum Occupation Period (MOP) usually prevents resale within five years anyway. The rare exceptions — flats sold under HDB’s compulsory-sale rules, or flats where MOP has been waived by HDB — are also exempt from SSD.

For practical purposes, most HDB sellers should treat MOP as the binding constraint and ignore SSD entirely.

SSD on Industrial Property — A Different (Shorter) Ladder

SSD on industrial property uses a separate, shorter ladder introduced in January 2013: 15% within the first year, 10% in the second year, 5% in the third year, and 0% thereafter — harsher in headline terms but with the same three-year horizon. Commercial property (offices, shops, hotels) attracts no SSD at all.

What This Means for You as a Buyer in 2026

The 2026 environment makes the holding-period calculus even more important. With ABSD at 20% on the second property for Singapore Citizens and 60% for foreigners, entry costs are already punishing. Adding a 12% SSD on a quick exit means roughly one-third of an investment property’s purchase price is consumed by transaction taxes if the holding period is mismanaged.

For buyer-occupiers, the practical advice is unchanged: buy what you can hold through three full years and a typical Singapore property cycle (roughly 7 to 10 years). For investors, the calculus is whether the projected three-to-five-year capital appreciation comfortably exceeds the entry-cost stack — not just SSD but BSD, ABSD, conveyancing, agent commission, and CPF accrued interest combined.

Frequently Asked Questions

Does SSD apply if I bought before 11 March 2017?

Yes, but at the older rate ladder applicable on the date of acquisition. Properties bought between 14 January 2011 and 10 March 2017 use the four-year, 16% / 12% / 8% / 4% ladder. Properties bought between 20 February 2010 and 13 January 2011 use a three-year, 3% / 2% / 1% ladder. IRAS publishes the historical rate tables for cross-reference.

Is SSD payable on the sale of a property at a loss?

Yes. SSD is calculated on the higher of the contracted sale price or the assessed market value, regardless of whether the seller realised a profit or loss on the transaction. Loss-making short-term sales remain fully taxable.

How is SSD different from ABSD?

ABSD (Additional Buyer’s Stamp Duty) is paid by the buyer at purchase based on residency status and number of properties already owned. SSD (Seller’s Stamp Duty) is paid by the seller at sale based on how long the property was held. They are independent taxes and can both apply to the same transaction at different ends.

What if I co-own a property with my spouse and only my spouse’s share is sold (decoupling)?

SSD applies to the share being transferred, calculated on the value of that share. The holding period for the transferred share is reckoned from the original date of acquisition. Conveyancers will typically structure the transfer documentation so that SSD exposure is calculated correctly for the share at issue.

Can I deduct SSD against my income tax?

No. SSD is a transaction tax, not a deductible business expense for an individual seller. Property held by a corporate vehicle may treat SSD differently — consult a Singapore tax adviser for any company-held holding.

Does SSD apply to gifts or transfers within the family?

Generally yes, where the transfer is treated as a sale at market value. There are limited remissions for transfers between spouses incident to divorce or for inherited property where the holding period is reckoned from the deceased’s original acquisition. Always verify with IRAS directly for non-arm’s-length transfers.

When exactly is SSD due?

SSD must be paid within 14 days of the contract for sale — that is, the date the buyer exercises the OTP or signs the S&P. Late payment attracts penalty interest of 5% on the unpaid duty per annum, plus possible additional charges. The seller’s conveyancer typically pays SSD out of the sale proceeds at completion.

This article is intended as general information about Seller’s Stamp Duty in Singapore as at May 2026 and does not constitute tax, legal, or financial advice. Rates, exemptions, and procedures are set by the Inland Revenue Authority of Singapore and may be amended at any time without notice. For authoritative figures, refer to IRAS, the Housing & Development Board, the Monetary Authority of Singapore, the Urban Redevelopment Authority, and CPF Board for related procedures. For transactions of any size, engage a licensed Singapore conveyancing solicitor and, if relevant, a chartered accountant or tax practitioner before signing an OTP or S&P.

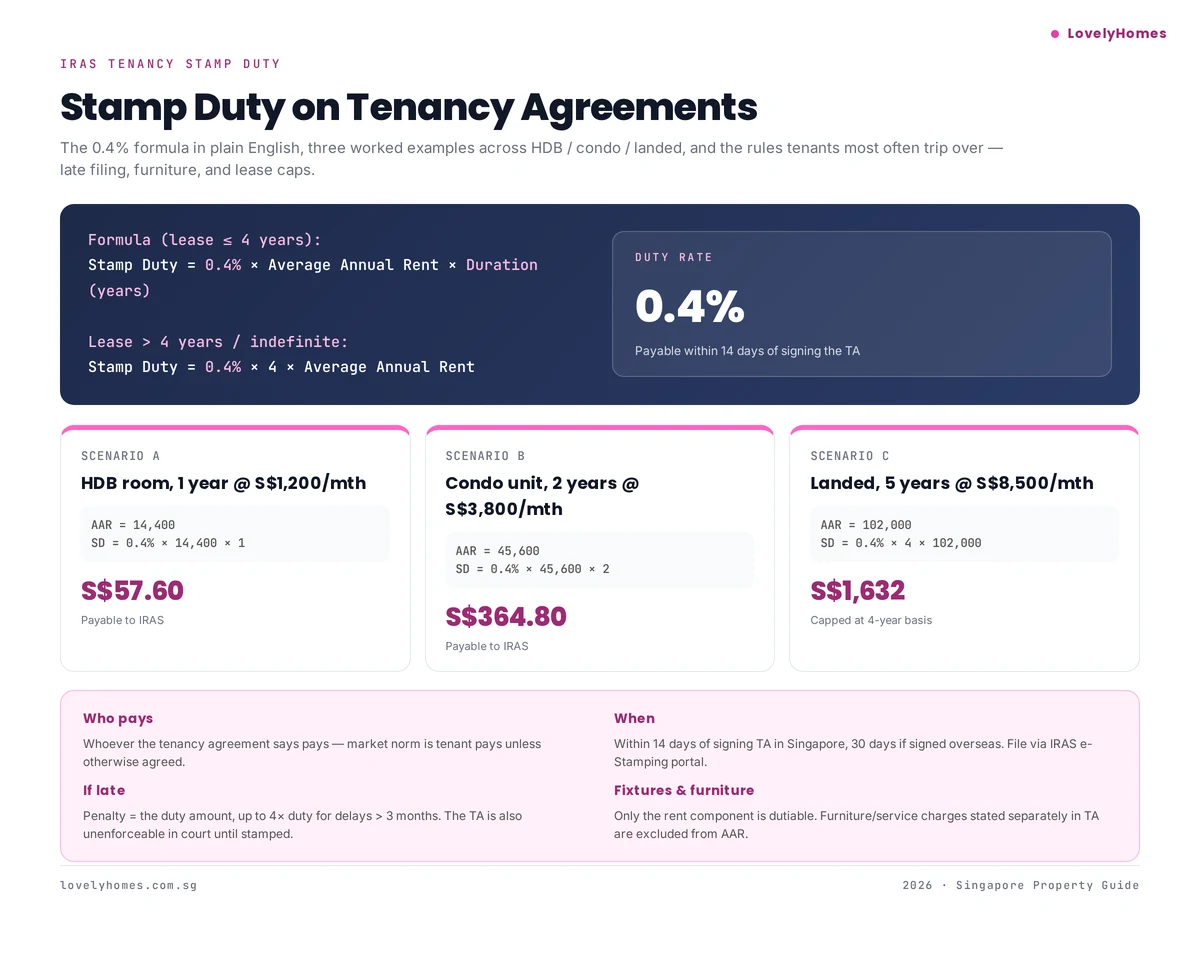

Rental stamp duty in Singapore is 0.4% of the Average Annual Rent (AAR) for leases up to 4 years. Leases longer than 4 years or indefinite are capped at 0.4% × 4 × AAR. Pay within 14 days of signing the TA (30 days if signed overseas). Most TAs have the tenant pay. Late filing penalty: up to 4× the duty if delay exceeds 3 months.

Rental stamp duty trips up more first-time tenants in Singapore than any other rental rule. The formula itself is simple — 0.4% of average annual rent — but the 14-day filing deadline, overseas-signed exception, and what counts as dutiable rent (furniture excluded, service charge maybe) create confusion. This guide explains the rules in plain English with three worked examples.

The 0.4% formula with three worked examples across HDB, condo, and landed

The formula

For a tenancy agreement with a fixed term:

Stamp Duty = 0.4% × Average Annual Rent (AAR) × Duration (in years) Where AAR = Total rent over lease period ÷ Lease length in years

If the lease is longer than 4 years, or is indefinite/renewable, the multiplier is capped at 4:

Stamp Duty = 0.4% × 4 × Average Annual Rent

Three worked examples

Example 1 — HDB room, 1-year lease at S$1,200/month

AAR = S$1,200 × 12 = S$14,400

Duty = 0.4% × S$14,400 × 1 year = S$57.60

Example 2 — Condo unit, 2-year lease at S$3,800/month

Under the Stamp Duties Act, either party can pay — the TA dictates who. Market convention in Singapore is tenant pays, but always check the clause. If the TA is silent, the party presenting it for registration pays.

Within 14 days of signing if the TA is executed in Singapore.

Within 30 days if signed overseas.

You’ll need SingPass or a CorpPass login. IRAS sends the stamp certificate by email — store it with your TA.

Late payment penalties

Delay

Penalty

Up to 3 months late

S$10 or the duty amount (whichever is higher)

More than 3 months late

S$25 or 4× the duty amount (whichever is higher)

Beyond the fine, an unstamped TA cannot be used as evidence in court — so if you ever dispute a deposit refund or breach claim, your unstamped TA is worthless until you stamp it (and pay the late penalty).

What is and isn’t dutiable

Component

Dutiable?

Rent

Yes

Maintenance fee (if stated separately in TA)

No

Furniture rental (stated separately)

No

Utility estimates bundled in rent

Yes (if not separated)

Security deposit

No (it’s refundable)

Agent commission

No

To lower the dutiable amount, ensure the TA separately itemises rent, furniture rental, and maintenance charges. Bundling them into “all-in rent” means everything becomes dutiable.

Enter the property address, landlord and tenant details, TA signing date, lease start and end dates.

Enter the monthly rent or annual rent — portal auto-calculates the AAR and duty.

Pay by PayNow, eNETS, GIRO, or credit card (surcharge applies).

Download the stamp certificate PDF — attach to your TA and keep for records.

Frequently asked questions

Does the stamp duty increase if rent changes mid-lease?

Only if there’s a written variation to the TA. Automatic CPI-linked increases written into the original TA are captured in the AAR calculation when you stamp at signing.

Do I need to stamp a room-only rental?

Yes — any tenancy agreement, including for a single room, is dutiable. The duty amount will just be smaller.

Can I deduct stamp duty from my income tax?

If you paid the stamp duty as a landlord, it’s a deductible rental expense. If you paid as a tenant (and the property isn’t used for business), it’s not deductible.

What if both parties refuse to pay?

Either party can pay and recover from the other. The TA itself cannot be enforced in court until stamped, so the party needing legal enforcement usually ends up paying.

Disclaimer

This guide is for general information only. Singapore’s rental rules, HDB policies, and IRAS stamp duty rates change periodically. Always verify against the HDB, URA and IRAS websites before signing a lease or filing with IRAS. LovelyHomes is not a licensed property agent or tax adviser. For personalised advice, please engage a registered CEA agent or a qualified tax professional.

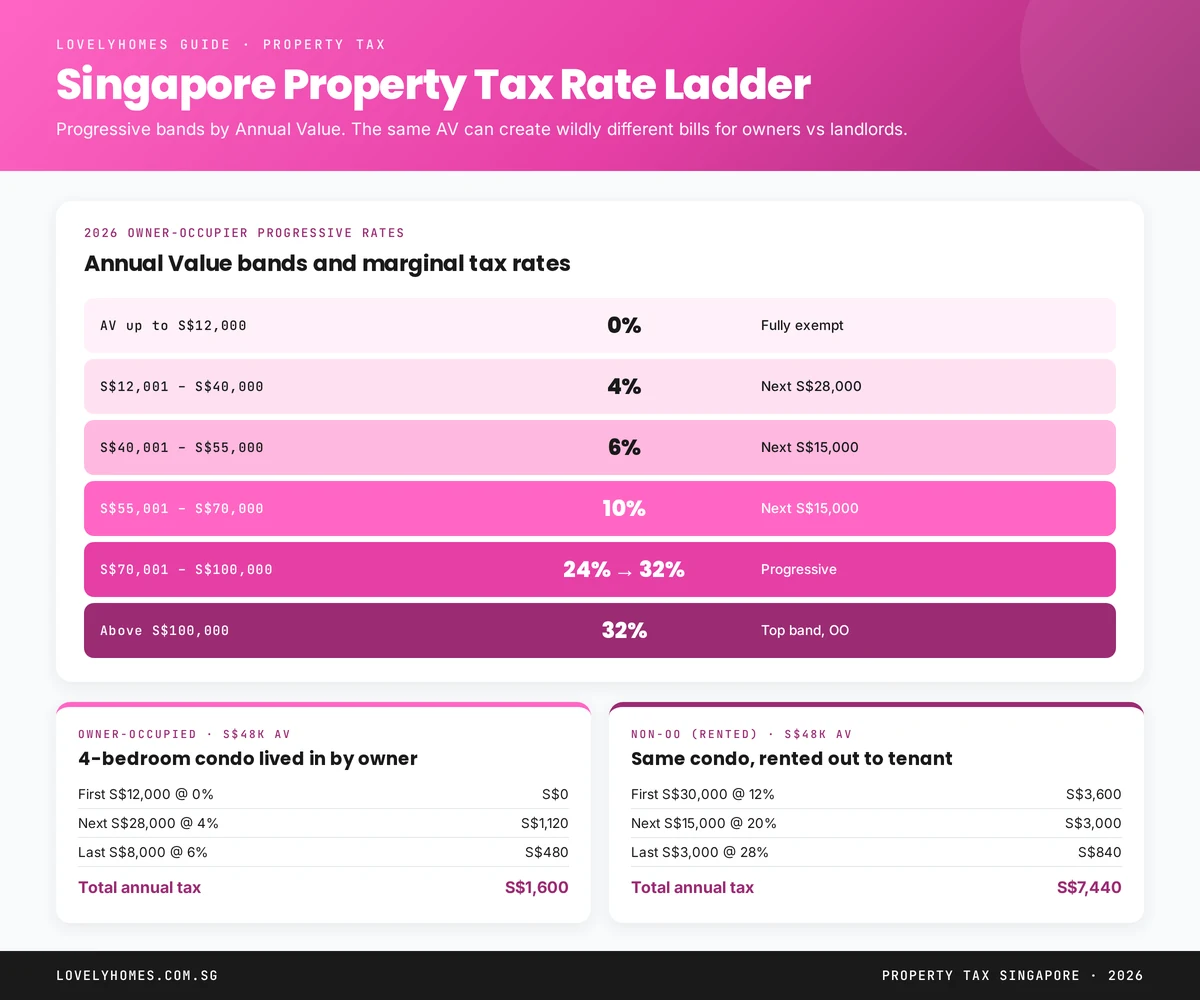

Property tax Singapore is a recurring annual tax levied by IRAS on all immovable property in Singapore. It is not based on your purchase price or your income — it is based on the Annual Value (AV) of the property, an IRAS estimate of what it would rent for on the open market. This design means even an owner who paid for their home decades ago faces a tax bill that rises with the rental market.

This 2026 guide walks through how Annual Value is set, the progressive rate bands for owner-occupiers and non-owner-occupiers, when the bill falls due, and a worked example that shows how the same property can create radically different tax bills depending on whether the owner lives in it or rents it out. For the official tables, see the IRAS Property Tax Rates page.

Quick Answer — Property Tax 2026

Based on: Annual Value (AV), not purchase price or income.

Owner-occupier rates: 0% on the first S$12,000, rising progressively to 32% on AV above S$100,000.

Non-owner-occupier rates: 12% on first S$30k, rising to 36% above S$60k.

Payable annually: bill issued in December, due 31 January. GIRO allows 12 monthly instalments.

Late payment: 5% penalty, then additional 1% per month of delay.

What is Annual Value and How Is It Set?

Annual Value is IRAS’s estimate of the gross annual rent your property could fetch on the open market, excluding furniture, fittings and service charges. IRAS revises AVs periodically based on actual rental transactions in the area, demographic trends, and condition of the building.

AV has nothing to do with:

Your purchase price

The actual rent you may receive (if renting out)

Your occupancy status (IRAS sets AV once; your occupancy decides which rate table applies)

The mortgage outstanding

You can check your property’s current AV at any time via myTax Portal using your Singpass. If you believe the AV is wrong, you have 30 days from the date of notification to object and supply rental evidence.

The 2026 Owner-Occupier Rate Ladder

Figure 1: Singapore’s progressive property tax rates for owner-occupied residential property in 2026.

Owner-occupiers pay the lowest rates because the scheme is designed to encourage home ownership. The progressive bands as at 2026:

First S$12,000 of AV: 0%

Next S$28,000 (S$12,001–S$40,000): 4%

Next S$15,000 (S$40,001–S$55,000): 6%

Next S$15,000 (S$55,001–S$70,000): 10%

Next S$15,000 (S$70,001–S$85,000): 14%

Next S$15,000 (S$85,001–S$100,000): 24%

Above S$100,000: 32%

Owner-occupier rates apply to the property you physically live in and where you are the legal owner. You cannot claim owner-occupier status on two properties simultaneously — the second (and subsequent) is taxed at non-owner-occupier rates.

The 2026 Non-Owner-Occupier Rate Ladder

If your property is rented out or vacant, the higher non-OO rates apply. These were raised significantly in 2023 and 2024:

First S$30,000 of AV: 12%

Next S$15,000 (S$30,001–S$45,000): 20%

Next S$15,000 (S$45,001–S$60,000): 28%

Above S$60,000: 36%

These rates apply to all forms of non-owner-occupation, including rental to tenants, use by family members who are not joint owners, and vacancy.

Worked Example: Same Condo, Two Tax Bills

Take a 3-bedroom condo in District 15 with an Annual Value of S$48,000.

Scenario A: Owner lives in it

Band

Amount

Rate

Tax

First S$12,000

S$12,000

0%

S$0

Next S$28,000

S$28,000

4%

S$1,120

Next S$8,000

S$8,000

6%

S$480

Total

S$48,000

—

S$1,600

Scenario B: Owner rents it out

Band

Amount

Rate

Tax

First S$30,000

S$30,000

12%

S$3,600

Next S$15,000

S$15,000

20%

S$3,000

Next S$3,000

S$3,000

28%

S$840

Total

S$48,000

—

S$7,440

The non-OO bill is 4.7× the OO bill on identical property with identical AV. That gap is exactly what the Government intends — a deliberate wedge against holding residential property as pure investment.

When the Bill is Due

Property tax for the calendar year is billed in December of the preceding year and due on 31 January.

Payment options:

GIRO — recommended. Split into 12 monthly instalments automatically. No interest.

Lump sum. Pay in full by 31 January via PayNow, AXS, or credit card (fees may apply).

Late payment: 5% penalty on the unpaid amount, plus 1% additional per month of delay (capped at 12%).

Reliefs and Rebates

Several reliefs can reduce your property tax bill:

Owner-occupier rates are automatic for the property that IRAS’s records show you living in. Update the records if you move.

Property Tax Rebate (introduced in 2023 Budget and repeated in 2024, 2025, 2026) has provided up to 100% rebate on the first S$1,000–S$2,000 of tax for owner-occupied HDB flats. Check current year for details.

Vacancy refund: historically available for vacant units; fully abolished from January 2014.

Frequently Asked Questions

Is property tax deductible for rental income tax?

Yes. Property tax is an allowable expense when computing taxable rental income on your annual personal income tax return.

What happens to the tax when I sell?

Property tax for the calendar year remains your obligation through the date of completion. The completion statement typically pro-rates the tax between seller and buyer based on occupancy days.

How does AV for new launches get set?

New launches are assigned a provisional AV based on comparable rentals in the area. Once the property is physically completed and rental evidence accumulates, the AV is reassessed.

Is there property tax on commercial or industrial property?

Yes, at a flat 10% of AV for most commercial and industrial categories. The progressive residential bands do not apply.

Can I reduce property tax by keeping the property vacant?

No. Vacancy attracts non-OO rates and AV remains based on market rental potential. There is no vacancy discount since 2014.

Disclaimer: This guide is general information, not tax advice. Rate bands and rebate schemes change annually via the Budget. Always verify current rules at iras.gov.sg and consult a tax professional for material decisions.

Wait-Out Period: Private property owners must wait 15 months before buying HDB resale without grant.

What are Singapore’s Property Cooling Measures?

Singapore’s property cooling measures are a suite of policy tools designed to moderate demand, curb speculation, and ensure housing remains affordable. They exist because rapid property price growth can outpace wage growth, lock first-time buyers out of the market, and create unsustainable bubbles. Four key agencies administer these measures: the Monetary Authority of Singapore (MAS), the Urban Redevelopment Authority (URA), the Inland Revenue Authority of Singapore (IRAS), and the Housing and Development Board (HDB). Together, they apply tools such as stamp duties, loan limits, affordability tests, and holding periods to regulate the market and protect both buyers and the broader economy.

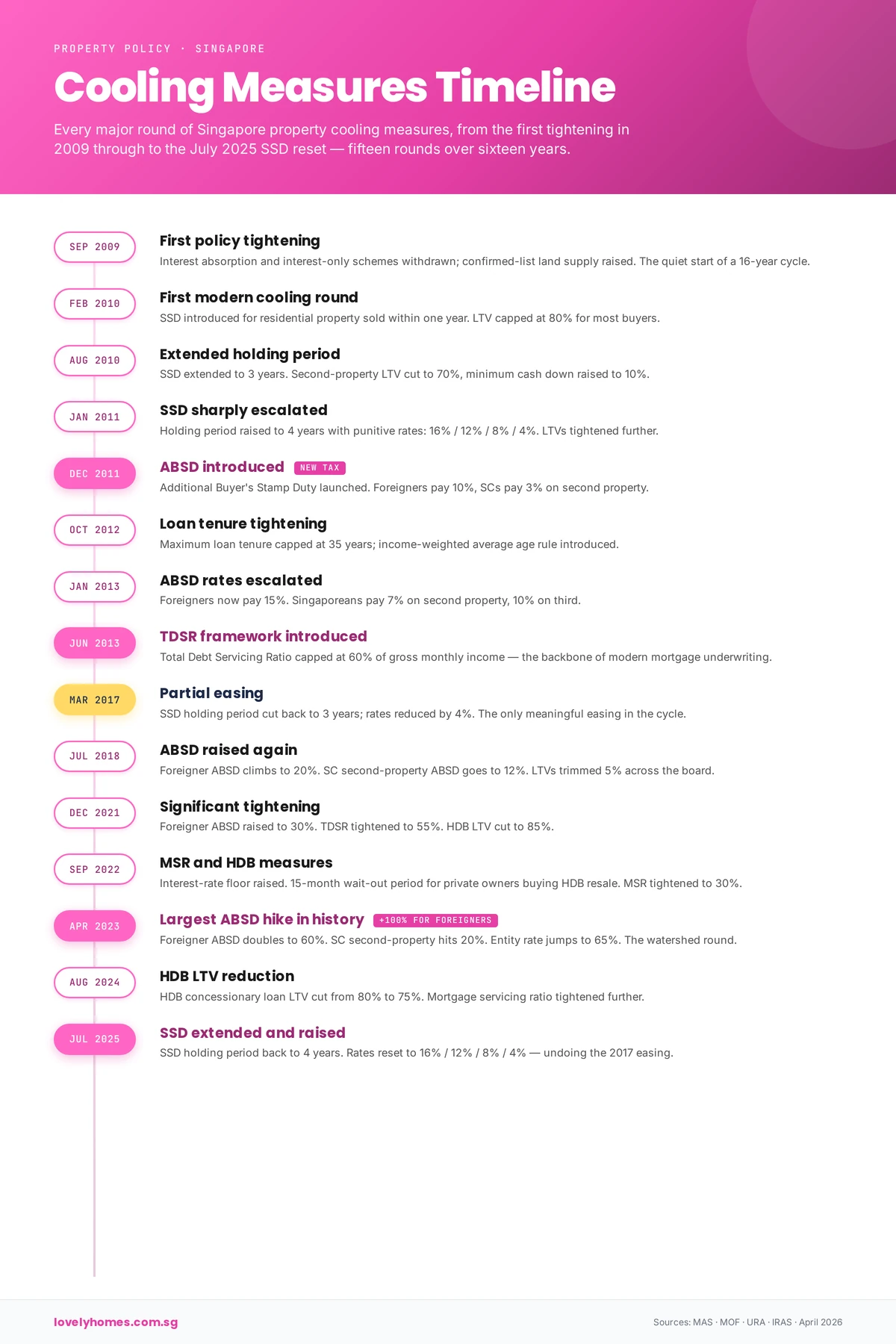

Figure 1: The 15 major rounds of Singapore property cooling measures, 2009–2026.

September 2009: The First Policy Tightening

Before the modern cooling era, the government moved to restrict lending practices. In September 2009, the Monetary Authority of Singapore (MAS) disallowed two risky loan products: the Interest Absorption Scheme (IAS) and Interest-Only Housing Loans (IOL). These products had allowed borrowers to defer principal repayment during the early years of a mortgage, increasing default risk during rate rises. By banning them, the government signalled a preference for prudent, full-amortising loans and set the stage for the more comprehensive cooling measures that would follow.

February 2010: The First Modern Cooling Round

On 20 February 2010, Singapore introduced its first comprehensive cooling package, reflecting rapid price growth and surging demand. The government introduced two major tools:

Seller’s Stamp Duty (SSD): Properties sold within one year were hit with a 3% SSD. The intent was to discourage “flipping”—rapid resale for short-term gain.

Loan-to-Value (LTV) limit: Reduced from 90% to 80%, requiring buyers to put down at least 20%. This reduced lender exposure and made buyers more cautious.

These measures reflected a key insight: when buyers can leverage heavily and exit quickly, prices can spiral. By raising the entry cost and the holding cost, the government aimed to attract only genuine buyers.

August 2010: Extended Holding Period

By mid-2010, demand remained strong. On 19 August 2010, the government extended the SSD holding period from 1 year to 3 years, raising the cost of short-term resale. For those with existing loans, the LTV limit tightened further to 70%, and cash downpayment requirements rose, particularly hurting leveraged investors.

January 2011: Sharp SSD Escalation

Recognising that the market was still overheating, the government on 8 January 2011 escalated the SSD significantly. The new structure was:

Year 1: 16%

Year 2: 12%

Year 3: 8%

Year 4: 4%

The rationale was unmistakable: hold for less than a year and lose a sixth of your sale price. LTV limits were also tightened to 60% for those with existing loans, making it much harder for property investors to string together multiple mortgages.

December 2011: ABSD Introduced

On 8 December 2011, Singapore introduced the Additional Buyer’s Stamp Duty (ABSD), its most powerful tool. ABSD was a second layer of stamp duty on top of the normal Buyer’s Stamp Duty (BSD), calibrated to buyer type:

Singapore Citizens buying a 2nd+ property: 3%

Singapore Citizens buying a 3rd+ property: 3%

Permanent Residents buying a 2nd+ property: 3%

Foreigners: 10%

Corporate entities: 10%

ABSD was revolutionary because it directly attacked investment demand, particularly from overseas. It signalled that Singapore prioritised homeownership for citizens over investment returns for outsiders.

October 2012: Loan Tenure Tightening

The Monetary Authority of Singapore further tightened lending on 19 October 2012. The maximum loan tenure was capped at 35 years, with a penalty: if LTV remained above 60% after 30 years, the LTV would be capped at 40% in year 31 onwards. This forced borrowers to repay principal faster, reducing their borrowing power and making loans less attractive.

January 2013: ABSD Escalation

On 11 January 2013, the government raised ABSD across the board:

Singapore Citizens (2nd property): 7%

Singapore Citizens (3rd+ property): 10%

Permanent Residents (2nd+ property): 10%

Foreigners: 15%

Entities: 15%

The hike reflected continued demand, particularly from foreign investors and corporate buyers. Cash downpayment requirements also rose, targeting multiple-property owners and entities.

June 2013: TDSR Framework Introduced

On 28 June 2013, the Monetary Authority of Singapore introduced the Total Debt Servicing Ratio (TDSR) framework. TDSR capped total monthly debt repayments (mortgage, car loan, credit cards, personal loans, etc.) at 60% of gross monthly income. The intention was to prevent over-leverage: even if house prices were rising, a banker couldn’t lend to someone whose entire income was going to debt service.

This was a game-changer because it wasn’t about house prices directly—it was about borrower health. It also forced banks to stress-test loans, assuming interest rates would rise, to ensure borrowers could survive a shock.

March 2017: Partial Easing

By 2016–2017, prices had stabilised and growth had slowed. On 5 March 2017, the government eased some measures:

SSD holding period reduced from 4 years to 3 years, though rates remained steep (12%/8%/4% for years 1–3).

TDSR and ABSD eased slightly for refinancing.

This signalled a shift: the government was confident the market was no longer overheating and could afford marginal relief.

July 2018: ABSD Raised Again

By mid-2018, there were signs of renewed speculative interest, particularly from foreign and corporate buyers. On 6 July 2018, the government raised ABSD sharply:

LTV limits also tightened by 5 percentage points across all categories, making down payments larger and borrowing power lower.

December 2021: Significant Tightening

After years of near-zero interest rates post-COVID, demand surged again. On 16 December 2021, the government announced a comprehensive tightening:

ABSD raised again: foreigners to 30%; entities to 35%; PR 2nd property to 20%.

TDSR tightened from 60% to 55% of gross monthly income.

Interest-rate floor for TDSR/MSR calculations raised to 3.5% for private bank loans (previously 3%).

HDB LTV limits reduced across the board.

This was a significant hardening, reflecting real concern about affordability following three years of price growth.

September 2022: MSR and HDB Measures

On 30 September 2022, the government introduced new measures targeting the HDB resale market, where first-time buyers (and upgraders) primarily shop:

Mortgage Servicing Ratio (MSR) introduced: For HDB and Executive Condominium (EC) loans, monthly mortgage payments cannot exceed 30% of gross income—stricter than TDSR’s 55%.

15-month wait-out period: Private property owners must wait 15 months after selling before buying an HDB resale flat, curbing investor demand for subsidised public housing.

Interest-rate floor for TDSR/MSR raised from 3% to 3.5% for private loans; 3% for HDB loans.

These moves directly sheltered first-time HDB buyers from investor competition.

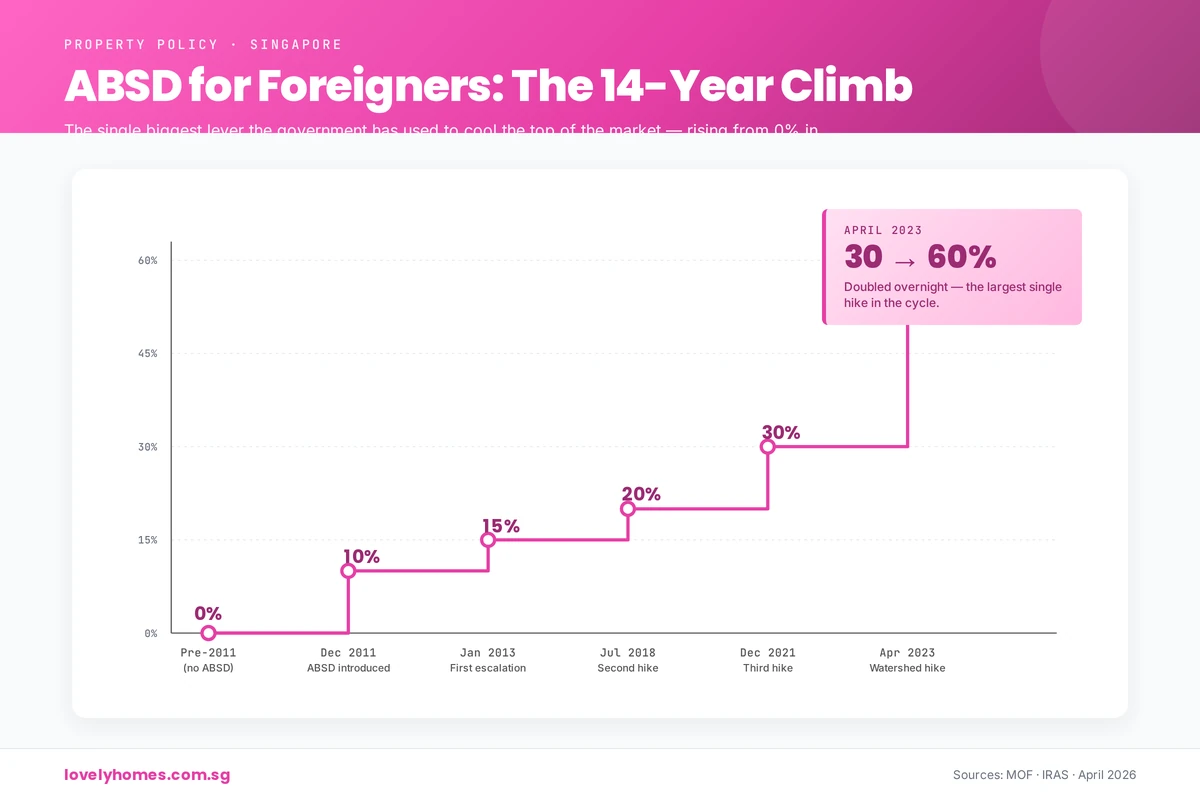

Figure 3: Foreigner ABSD climbed from 0% in 2011 to 60% in April 2023 — the largest single hike in the cycle.

April 2023: Largest ABSD Hike in History

On 27 April 2023, faced with renewed price acceleration in Q1 2023 (especially among owner-occupiers), the government announced its largest ABSD increase:

This was the most aggressive escalation since ABSD’s introduction, reflecting the government’s determination to prioritise homeownership for citizens and slow speculation. A foreign buyer purchasing a S$2 million condo now faced S$1.2 million in ABSD—an enormous barrier.

August 2024: HDB LTV Reduction

On 20 August 2024, the government reduced the Loan-to-Value (LTV) limit for HDB-granted housing loans from 80% to 75%. This meant HDB buyers now needed a 25% down payment instead of 20%, directly reducing borrowing power for this segment. Concurrently, higher CPF Housing Grants were introduced for first-time buyers to offset the impact, retaining affordability.

July 2025: SSD Extended and Raised

On 3 July 2025, the government responded to a spike in “flipping”—buyers purchasing uncompleted units (off-plan) and reselling before completion or soon after. The SSD holding period was extended from 3 years to 4 years, and rates were raised across the board by 4 percentage points:

Year 1: 20% (from 16%)

Year 2: 16% (from 12%)

Year 3: 12% (from 8%)

Year 4: 8% (from 4%)

This further discouraged short-term speculation while allowing long-term owners to exit penalty-free after four years.

Current Cooling Measures Framework (April 2026)

The current cooling-measures framework, established by the 27 April 2023 ABSD hike and subsequently adjusted by the 20 August 2024 HDB LTV reduction and the 4 July 2025 SSD restructure, remains in force as at April 2026. MAS, MND, URA and HDB jointly review the framework regularly and have repeatedly indicated they will recalibrate the measures — either tightening or easing — in response to market conditions.

Figure 2: The four core cooling tools — taxes (ABSD, SSD), loan limits (LTV) and debt ratios (TDSR) working in concert.

Let’s illustrate the impact with a hypothetical Singapore Citizen (SC) buying a second property valued at S$2 million:

Year

ABSD Rate

ABSD Cost (S$)

BSD + ABSD Total

2010 (Feb)

0%

S$0

~S$20,000 (BSD only)

2013 (Jan)

7%

S$140,000

~S$160,000

2018 (July)

7%

S$140,000

~S$160,000

2023 (April)

20%

S$400,000

~S$420,000

2026 (April)

20%

S$400,000

~S$420,000

Notice the leap from 2013 to 2023: the cost of buying a second home more than doubled in stamp duty alone, while the property value remained constant. This is the direct impact of cooling measures: they make property ownership more expensive, not by changing the property itself, but by raising friction and entry costs.

Why Have Cooling Measures Worked?

Singapore’s housing market has not crashed, despite aggressive cooling measures—a fact some cite as evidence of failure. But that misses the point. Cooling measures are designed to slow, not stop, price growth; to reduce speculation, not eliminate it; and to align prices with incomes, not freeze them.

Consider the evidence:

Slower growth: Private residential property annual price gains have typically stayed in the 2–5% range post-2013, compared to double-digit growth in the early 2010s. This moderation reflects a market rebalancing, where price appreciation has settled into a more sustainable trajectory aligned with economic fundamentals such as wage growth and rental yields.

Affordability preserved: First-time buyers, particularly HDB upgraders, have continued to buy; median house prices have not become so extreme relative to median incomes that the market has fractured. The price-to-income ratio in Singapore remains among the most manageable in developed Asia, allowing younger buyers to enter the market without undue hardship.

Comparison to global peers: Hong Kong, Vancouver, and Sydney have seen much steeper price-to-income ratios despite less stringent cooling measures. In Hong Kong, for example, a property may cost 20–30 times annual median household income; in Vancouver and Sydney, the ratio exceeds 12–15. Singapore’s pragmatic approach has kept the ratio at a more sustainable 8–10 times, making the market more accessible.

Investor activity moderated: The share of property transactions by investors (vs. owner-occupiers) has declined, indicating cooling measures are successfully crowding out speculative demand. This shift is crucial: when investors withdraw, price volatility typically decreases and stability improves.

Market resilience: The market has absorbed multiple rounds of tightening—seven major cooling packages since 2009—without experiencing a crash. This speaks to the underlying strength of Singapore’s economy and the government’s ability to calibrate policy precisely, neither so tight as to stifle the market nor so loose as to permit excess.

In short, cooling measures have succeeded in their core mission: managed, sustainable growth that preserves homeownership as an achievable goal for Singaporeans whilst safeguarding financial stability.

What Might Come Next?

Predicting future cooling measures is speculative, but several potential levers exist if the market overheats again. The government has shown it is willing to adjust policy swiftly when conditions warrant, and the following measures are within the realm of possibility:

Further LTV tightening: LTV could drop below 75% for HDB and 70% for private, forcing larger down payments. This would particularly affect HDB first-time buyers, though offsetting grants could mitigate the impact.

ABSD escalation on entities: Corporate and foreign entity purchases could face rates exceeding 70%, further discouraging institutional investors and offshore funds from treating Singapore residential property as an alternative asset class.

TDSR reduction: The 55% threshold could tighten to 50%, limiting borrowing power even further. This would reduce the quantum of debt banks could extend and force buyers to increase down payments or reduce property search prices.

Extended hold periods: SSD holding could extend beyond four years; MSR wait-out could lengthen beyond 15 months. A 5–7 year SSD period would effectively end short-to-medium-term flipping as an investment strategy.

Targeted HDB measures: Given HDB’s social mission, the government could ring-fence HDB buying further (e.g., longer wait-out periods for private owners, stricter owner-occupancy rules for upgrade purchases).

Differentiated ABSD by property type: Separate ABSD rates for landed (houses, land) vs. non-landed (condos, ECs) to focus cooling where prices are most extreme. Landed property prices have historically appreciated faster than condominiums, making them a natural target for stricter cooling.

Interest-rate floor adjustments: The MAS could raise the notional interest-rate floor used in TDSR/MSR calculations from the current 4% (private) to 4.5% or 5%, making loans seem more expensive during qualification, thereby reducing lending volumes.