Singapore Property Investment Strategy 2026: Rental Yields, Capital Gains and Net Returns

Quick Answer: Singapore Property Investment Strategy 2026

- Singapore property gross rental yields range from 2.5% (CCR condos) to 4.8% (shophouse/commercial) — HDB flats offer the highest residential yields in 2026.

- Capital appreciation since 2019 has been strongest in HDB resale (7.2% pa) and landed (6.1% pa), well ahead of CCR condominiums (3.5% pa).

- The biggest drag on investor returns is ABSD: Singapore Citizens buying a 2nd property pay 20% — S$360,000 on a S$1.8M purchase — payable in cash only, not CPF.

- After ABSD amortised over 10 years plus all operating costs, an OCR condo investor nets roughly S$44,000/yr total return — only if the property appreciates at ~4% pa.

- Singapore Citizens on a first property (0% ABSD) and PRs on a first property (5% ABSD) enjoy meaningfully better net returns — estimated at 4.7% and 4.3% pa respectively.

- S-REITs offer property exposure without ABSD or illiquidity, distributing 5.5–6.5% annually in 2026.

- Record GLS supply (9,320 Confirmed-List units for 2026) could soften OCR/RCR prices by 2027 — monitor before committing at today’s entry prices.

Why Singapore Property Remains a Core Investment

Singapore’s property market has delivered consistent long-term returns since the Republic’s founding. Land is finite — the city-state covers just 720 square kilometres — yet it anchors a population approaching six million, a global financial hub, and one of the world’s busiest ports. This structural scarcity underpins values across all residential and commercial segments, and has historically cushioned the market against the deeper corrections seen in comparably-sized cities elsewhere in Asia.

The country’s legal and institutional framework adds a second pillar of confidence. Clear Torrens-system land titles, an independent judiciary, and the absence of capital controls make Singapore one of the few markets where property ownership has proved reliably secure across multiple economic cycles. Foreign institutional capital continues to flow into commercial and luxury-residential segments even at the 65% ABSD rate introduced in April 2023 — a telling signal of long-term conviction despite the punitive entry cost.

For Singapore Citizens and Permanent Residents, however, the investment case has shifted materially since the April 2023 cooling measures. A Singapore Citizen buying a second residential property now pays a 20% Additional Buyer’s Stamp Duty (ABSD), charged on the purchase price and payable entirely in cash within 14 days of exercising the Option to Purchase (OTP). On a S$1.8 million OCR condominium — modest by 2026 standards — that is S$360,000 in upfront tax. The critical question every investor must answer is: do the returns justify this cost?

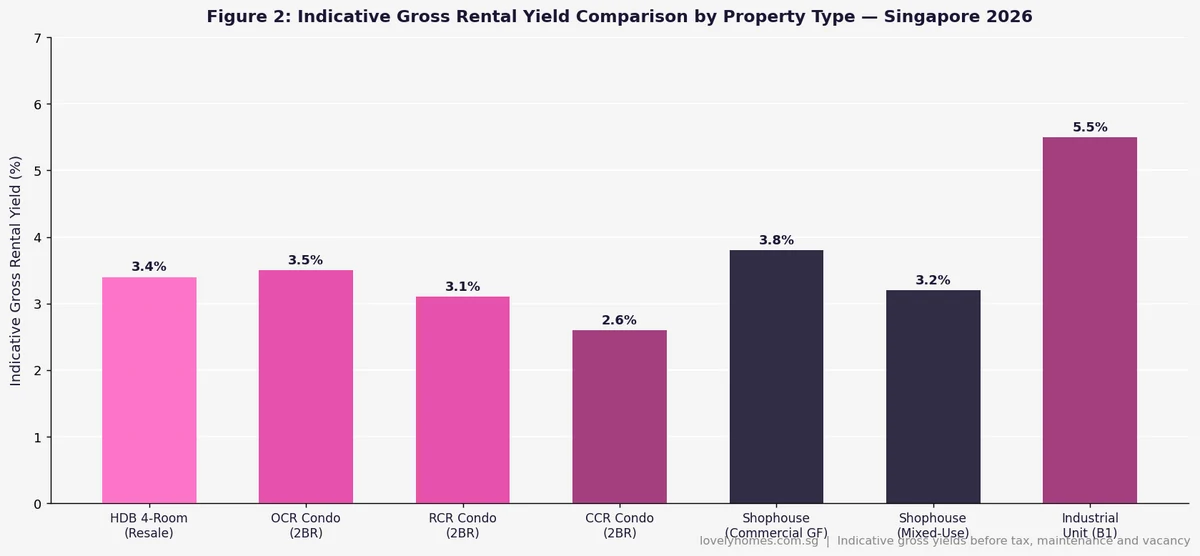

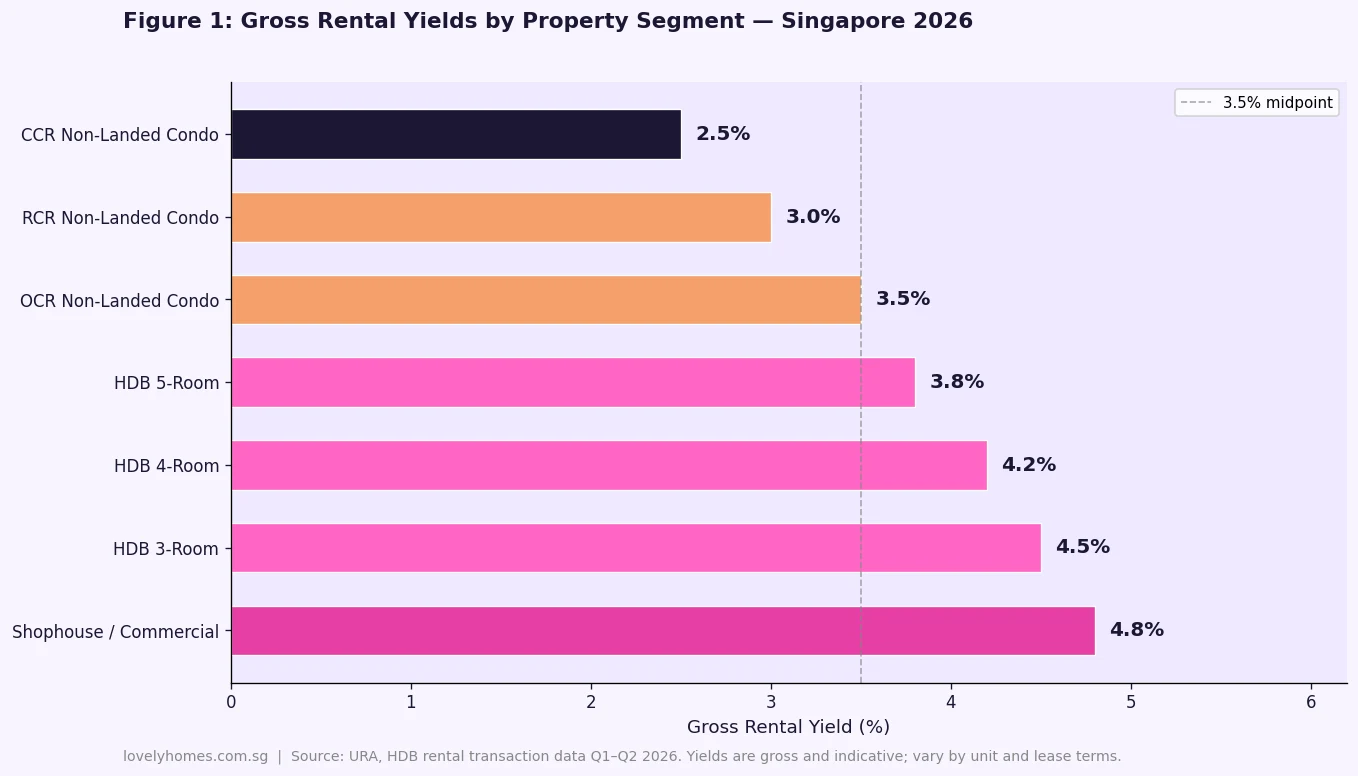

Gross Rental Yields by Segment

Gross rental yield — annual rent divided by purchase price — is the simplest measure of a property’s income productivity before expenses. It varies significantly across Singapore’s property segments, reflecting both the absolute price level of each asset class and the depth and quality of tenant demand.

HDB flats achieve the highest gross yields among residential assets — typically 3.8%–4.5% depending on flat type — because their purchase prices are substantially lower than private condominiums, while rents in mature estates are broadly competitive. A 4-room flat in Toa Payoh, Queenstown, or Bishan renting at S$2,500–S$3,000 per month on a resale price of S$600,000–S$750,000 generates a 4.0%–4.8% gross yield. The caveat is that HDB rental requires HDB approval, and subletting rules — including approved tenant nationalities and minimum lease terms — are more restrictive than private property.

OCR non-landed condominiums sit at approximately 3.5% gross. A 2-bedroom unit in the Tampines, Jurong, or Punggol corridors renting for S$3,200–S$4,000 per month against a purchase price of S$1.1M–S$1.4M falls comfortably in this range. RCR condominiums yield around 3.0%, reflecting higher per-square-foot prices and a somewhat more transient tenant pool. CCR condominiums trail at 2.5%, as their elevated pricing limits the universe of tenants who can afford market-rate rents in the core central region.

Shophouses and commercial units lead all segments at approximately 4.8%, but they come with critical caveats: minimum purchase prices of S$3M–S$15M, limited liquidity, specialist buyer pools, and very different stamp duty treatment — residential ABSD does not apply to commercial purchases, which materially skews headline yield comparisons.

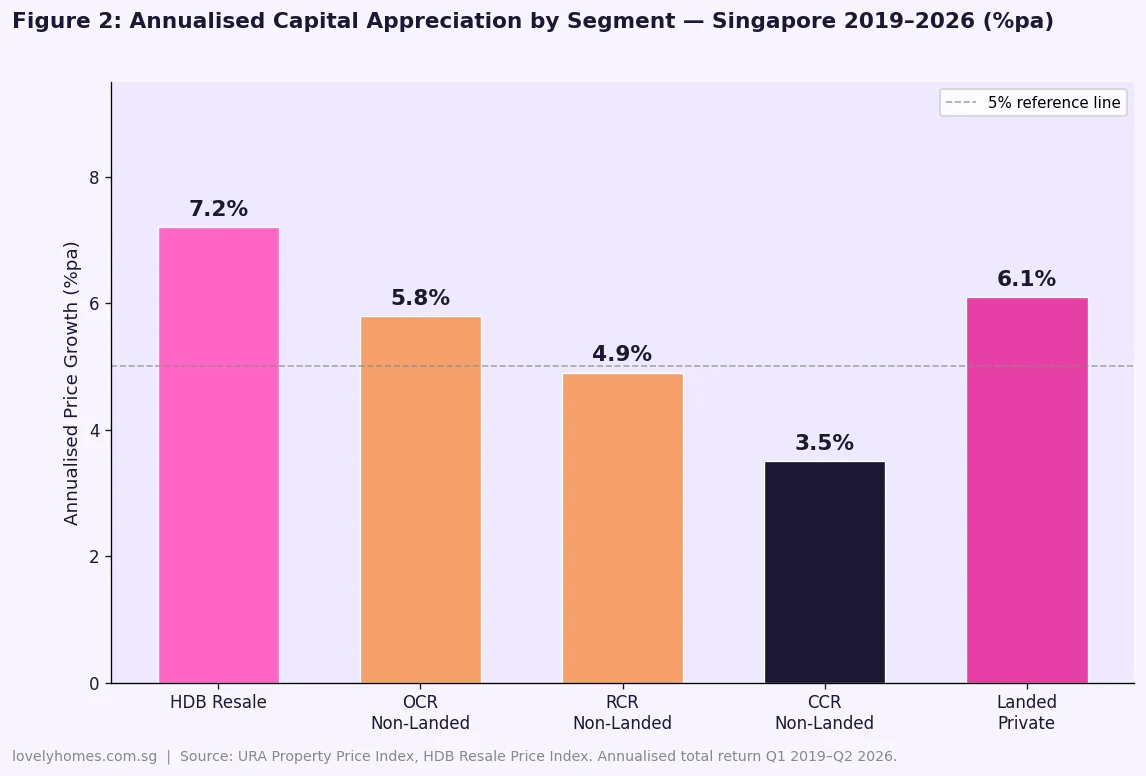

Capital Appreciation by Segment: 2019–2026

Rental income rarely explains why Singaporeans commit such large sums to direct property ownership. The real prize — historically — has been capital appreciation. The chart below shows annualised price growth across segments from Q1 2019 to Q2 2026 flash, covering the post-COVID boom and the subsequent cooling-measure moderation.

The HDB resale segment’s 7.2% annualised gain is the most striking figure in the landscape. This reflects a chronic undersupply of resale flats in mature estates, persistent demand from first-time buyers who did not win a BTO ballot and are paying market price, and the government grant structure that pulls purchasing power from a wide income band into the same finite pool of homes.

Landed property at 6.1% pa reflects equally constrained supply — Singapore’s landed housing stock is constitutionally protected in most districts, and titles cannot be subdivided below minimum plot sizes. OCR non-landed private property at 5.8% has been propelled by the HDB upgrader pipeline: Singapore Citizens who have served their Minimum Occupation Period and graduated to private ownership. That demographic funnel, fed by BTO completions from 2018–2022 and the elevated HDB resale market of 2021–2024, has proved remarkably durable.

CCR’s more modest 3.5% pa gain reflects both the segment’s higher price base and the disproportionate impact of the 65% foreign ABSD — raised from 30% in April 2023 — on CCR demand, which had historically skewed towards foreign investors and expatriate purchasers.

The ABSD Impact: Quantifying the Investor’s Hurdle

For Singapore Citizens already owning property, the 20% ABSD on a second residential purchase is the dominant variable in any investment analysis. It is not merely an upfront cost: it is a 20% return hurdle the investment must clear before any real profit begins to accumulate.

| Buyer Profile | ABSD Rate | ABSD on S$1.8M | Est. Net Yield | Cap. Gain (4% pa) | Total Return pa |

|---|---|---|---|---|---|

| SC — 1st property (owner-occupier buying only) | 0% | S$0 | +0.7% | +4.0% | ~4.7% |

| PR — 1st property | 5% | S$90,000 | +0.3% | +4.0% | ~4.3% |

| SC — 2nd property | 20% | S$360,000 | -1.3% | +4.0% | ~2.7% |

| PR — 2nd property | 25% | S$450,000 | -1.6% | +4.0% | ~2.4% |

| SC — 3rd property | 30% | S$540,000 | -2.5% | +4.0% | ~1.5% |

| Foreigner | 65% | S$1,170,000 | Deeply negative | +4.0% | ~2.0%* |

*Foreigner total return assumes 10yr hold and 4% pa capital appreciation; ABSD amortised at S$117K/yr. Estimates only; not financial advice. ABSD rates effective 27 April 2023 per IRAS.

Net Annual Return: The Full Breakdown

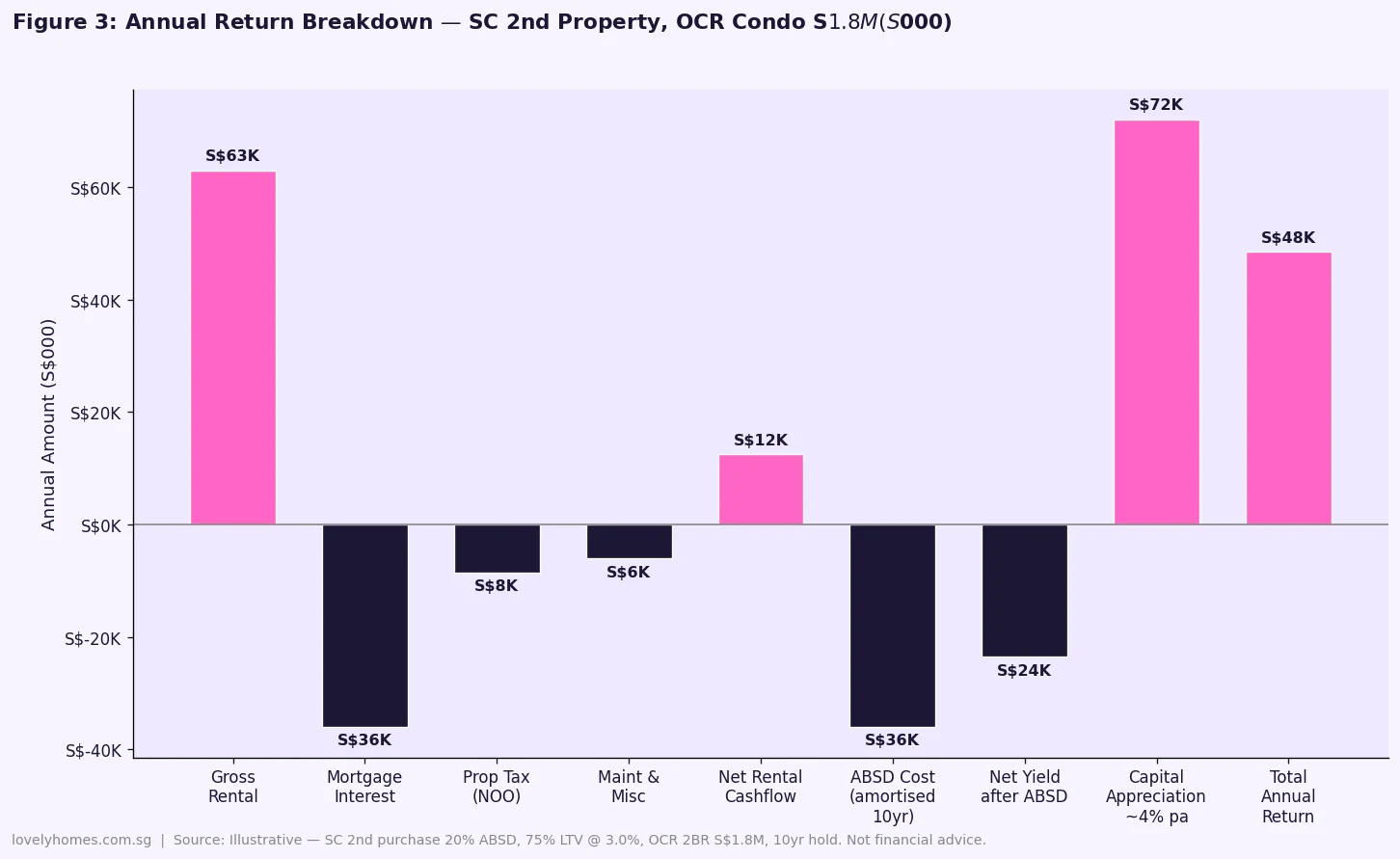

The chart below deconstructs every component of annual return for a Singapore Citizen buying a second property — a 2-bedroom OCR condominium at S$1,800,000 — showing precisely where income is earned and where costs erode it.

Gross rent at 3.5% yields S$63,000 per year. Mortgage interest on a S$1.35 million loan at 3.0% costs S$40,500. Non-owner-occupied property tax on an annual value of approximately S$63,000 costs around S$8,500. Maintenance fees and miscellaneous outgoings run another S$6,000 per year. That leaves a net rental cashflow of S$8,000 — barely 0.5% of the purchase price — before ABSD is factored in.

Amortised over a 10-year hold, the S$360,000 ABSD costs S$36,000 per year in opportunity cost. Subtracted from the S$8,000 net rental cashflow, the investor is running at S$28,000 negative annually from operations. Capital appreciation at 4% per annum on S$1.8M generates approximately S$72,000 per year in theoretical gain — rescuing the total return to roughly S$44,000 per year, or about 2.5% on purchase price. For comparison, the 10-year SGS bond yield in mid-2026 stood at approximately 3.0%, and S-REITs were distributing 5.5%–6.5% per annum. The risk-adjusted case for a second-property investment in Singapore demands real conviction in the capital-appreciation story.

Investment Strategies for 2026

Four broad strategies align with different investor profiles and risk appetites in the current environment.

Buy-to-let for income: Best suited to HDB flats (SC first purchase, mature estates near MRT) or OCR condominiums (first-time private buyer). Mature-estate HDB flats in Queenstown, Toa Payoh, and Bishan generate 4.0%–4.5% gross yields with low vacancy risk. Private condos in high-demand OCR rental catchments — near international schools, tech corridors, or major employment hubs — support consistent 3.3%–3.8% gross yields.

Capital-gain strategy via HDB-to-private upgrade: SC couples who sell their HDB flat and buy a private condominium as their primary residence pay zero ABSD on the private purchase and face no LTV penalty from an existing loan. This is structurally the most efficient entry into private property appreciation, and has driven OCR capital gains for over two decades.

En bloc positioning: Buying into an older, low-plot-ratio freehold property in a redevelopment-ready location — Greater Southern Waterfront fringe, Orchard/Newton corridor, or established OCR growth nodes — can deliver outsized capital gains if a collective sale proceeds. The trade-off is timeline uncertainty of 12–24 months and the 80% or 90% consent threshold. See our En Bloc Sale Guide 2026 for the full process and legal framework.

S-REITs — indirect exposure without ABSD: Singapore-listed REITs provide diversified property exposure across industrial, retail, logistics, and hospitality sectors, currently yielding 5.5%–6.5% annually. They are listed on SGX, liquid, and accessible from one lot. For income-focused investors who cannot justify the ABSD cost of direct second-property ownership, a portfolio of S-REITs is a compelling alternative — though it sacrifices the leverage and direct asset-selection advantages of physical property.

Financing: TDSR, LTV, and the Second-Property Rules

The Monetary Authority of Singapore (MAS) enforces the Total Debt Servicing Ratio (TDSR) across all property-linked loans. Monthly debt obligations — the new mortgage plus all existing commitments — must not exceed 55% of verified gross monthly income. For second-property investors, the binding constraint is often TDSR rather than ABSD alone.

Loan-to-Value rules compound this. With no outstanding loan, the bank LTV is 75% (meaning 25% downpayment, of which minimum 5% must be cash). With one outstanding loan — a common scenario for SC investors still servicing an HDB mortgage — the LTV on the new private loan drops to 45%, requiring a 55% downpayment. On a S$1.8M property, that is S$990,000 in equity required before ABSD, BSD, or legal fees are counted.

Note that ABSD cannot be paid with CPF. Only cash funds may be used. BSD may be paid from CPF Ordinary Account. These rules constrain the investable universe to buyers with substantial liquid savings beyond their CPF holdings.

What Might Come Next

The record GLS Confirmed List of 9,320 units for 2026 — the largest in the programme’s modern history — will translate into completions primarily in 2028–2030. Rental yields may compress modestly in 2027 as this wave of new supply enters the leasing market, particularly in the OCR and RCR segments where GLS activity is heaviest. Short-term investors entering at today’s prices face this headwind.

Interest rates are trending lower. The US Federal Reserve is expected to cut two to three times in 2026, pulling SORA from approximately 3.6% toward 2.8% by year-end. Lower financing costs improve net yields and could re-activate demand across all private segments. The full Q2 2026 URA private residential statistics, expected on 24 July 2026, will provide the most comprehensive data signal of whether the flash +0.5% figure holds across all sub-segments.

There is no credible expectation that ABSD rates will be reduced in the near term. MND has consistently signalled that housing affordability remains a priority concern, and any ABSD reduction risks reigniting the demand surge the 2023 measures were designed to prevent.

Frequently Asked Questions

Can I use CPF Ordinary Account funds to pay ABSD?

No. ABSD must be paid entirely in cash within 14 days of exercising the Option to Purchase. CPF Ordinary Account funds may be used for BSD, downpayments, and monthly mortgage instalments, but not for ABSD. This is a material liquidity constraint — buyers must hold sufficient cash above and beyond their CPF balances before committing to a second-property purchase.

Is there any ABSD remission for investors selling an existing property?

The ABSD remission for SC married couples allows a full ABSD refund on a second property if the first is sold within six months of the new property’s purchase date (completed property) or TOP (new launch). This is designed for the buy-before-sell upgrade path, not for investors who intend to retain both properties. There is no investor-specific ABSD waiver as at July 2026. Married SC/PR couples may apply for ABSD remission at the SC rate if the SC spouse is the sole or joint purchaser.

How does the TDSR apply to investment properties?

The TDSR applies equally to investment and owner-occupied residential properties. All monthly loan obligations must not exceed 55% of verified gross monthly income. Rental income from the investment property may be counted at a 70% haircut if you have evidence of existing rental receipts, but prospective rent from a newly purchased property is generally excluded. The TDSR is enforced by the MAS and applies to all financial institutions regulated in Singapore.

Is rental income from Singapore property taxable?

Yes. Net rental income is taxable as part of your assessable income under the Income Tax Act administered by IRAS. Net rental income is gross rent less allowable deductions: mortgage interest, agent commissions, property maintenance, fire insurance, property tax, and statutory depreciation on furniture and fittings (at 25% of monthly rent). Singapore residents pay progressive rates from 0% to 24%; non-residents pay a flat 24%. Rental income must be declared in your annual IRAS tax return by 15 April each year. Full guidance is available at iras.gov.sg.

Can foreigners buy investment property in Singapore?

Foreigners may purchase non-landed private residential property (condominiums and apartments). However, the 65% ABSD rate makes this prohibitively expensive for most investment theses — on a S$2M condominium, ABSD alone is S$1.3M. Foreigners cannot purchase HDB flats and require SLA written approval for landed property. Commercial property (shophouses, office, retail, industrial) is exempt from residential ABSD and remains fully open to foreign ownership, which is why shophouses continue to attract significant foreign institutional capital.

Are S-REITs a better investment than direct property?

S-REITs offer higher current yields (5.5%–6.5% in 2026), full liquidity (SGX-listed), no ABSD, and no minimum investment beyond one lot. The trade-off is that you do not select individual properties, you bear equity market volatility and interest-rate sensitivity, and capital appreciation is driven by unit-price movements rather than specific deals. For income-focused investors who cannot justify the ABSD cost of direct second-property ownership, a diversified S-REIT portfolio typically produces better risk-adjusted returns than a single leveraged property — though it sacrifices the leverage and bespoke asset-selection advantages of direct ownership.

Should I buy now or wait for the GLS supply to affect prices?

The record 9,320-unit GLS Confirmed List for 2026 translates into completions primarily in 2028–2030 — not an immediate price shock. Rental markets may soften from 2027 as supply arrives, particularly OCR/RCR. Short-term investors (3–5 year horizon) face elevated risk of entry-price headwinds from this supply wave. Long-term investors (8–10+ years) have historically found most Singapore entry points acceptable, as prices have recovered from every supply-driven moderation since 2013. Monitor the full Q2 2026 URA statistics (24 July 2026) and the October 2026 GLS announcement before committing.

Worked Example: SC Upgrader Buys OCR Investment Condo

Mr Tan, SC, 45, earns S$18,000 per month. He and his wife own a fully paid-up HDB flat in Bishan. He wishes to purchase an OCR 2-bedroom condominium in Tampines at S$1,800,000 as a 10-year investment.

Upfront costs: BSD S$56,600 (CPF OA) • ABSD 20% S$360,000 (cash only) • 25% downpayment: S$90,000 cash + S$360,000 CPF • Bank loan 75% LTV S$1,350,000 @ 3.0% 30 years = S$5,691/mth • TDSR 31.6% ✓ • Legal fees S$5,500. Total outlay: approximately S$455,500 cash + S$416,600 CPF.

Annual returns: Gross rent 3.5% = S$63,000 • Less mortgage interest (3.0% × S$1.35M) = S$40,500 • Less NOO property tax = S$7,560 • Less maintenance S$450/mth = S$5,400 • Less insurance and misc = S$1,200. Net rental cashflow: S$8,340/yr (0.5%). Less ABSD amortised over 10 years = S$36,000. Net yield after ABSD: −S$27,660/yr. Assumed capital appreciation 4% pa = S$72,000/yr. Estimated total annual return: S$44,340 (~2.5% pa on purchase price).

At a 10-year exit (no SSD having held more than three years), assuming 4% pa compound growth, the property is worth approximately S$2.66M — a S$860,000 gross capital gain. Less total ABSD (S$360,000), less selling costs (~S$36,000), less cumulative negative operating cashflow (approximately S$276,000 over 10 years): net 10-year return roughly S$188,000 on S$455,500 cash outlay. That is approximately 41% cumulative or 3.5% CAGR on cash invested. Compelling only if the 4% capital appreciation assumption holds across the entire decade.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Seller’s Stamp Duty (SSD) Guide 2026

- Singapore Private Property Buying Guide 2026

- Singapore Property Tax Guide 2026: IRAS Annual Value and Owner-Occupied Rates

- Singapore Housing Loan Guide 2026: TDSR, MSR and HDB vs Bank Loan

- En Bloc Sale Singapore 2026: Collective Sales, 80% Consent and Owner Rights

Disclaimer: This article is for general information only and does not constitute financial, investment, or legal advice. Property investment involves risk, including possible loss of capital. Yield and appreciation figures are illustrative estimates based on historical and current market data; future performance may differ materially. ABSD rates, BSD schedules, and financing rules are correct as at 11 July 2026 but are subject to change by the relevant Singapore authorities. Readers should consult a licensed financial adviser or mortgage broker and conduct independent due diligence before making any investment decision. For official ABSD/BSD rates, refer to IRAS at iras.gov.sg. For market transaction data and GLS information, refer to URA at ura.gov.sg.

Click anywhere to close