13,480 HDB Flats Reaching MOP in 2026: What the Supply Wave Means for Buyers and Sellers

Quick Answer: 13,480 HDB Flats Reaching MOP in 2026 — Key Facts

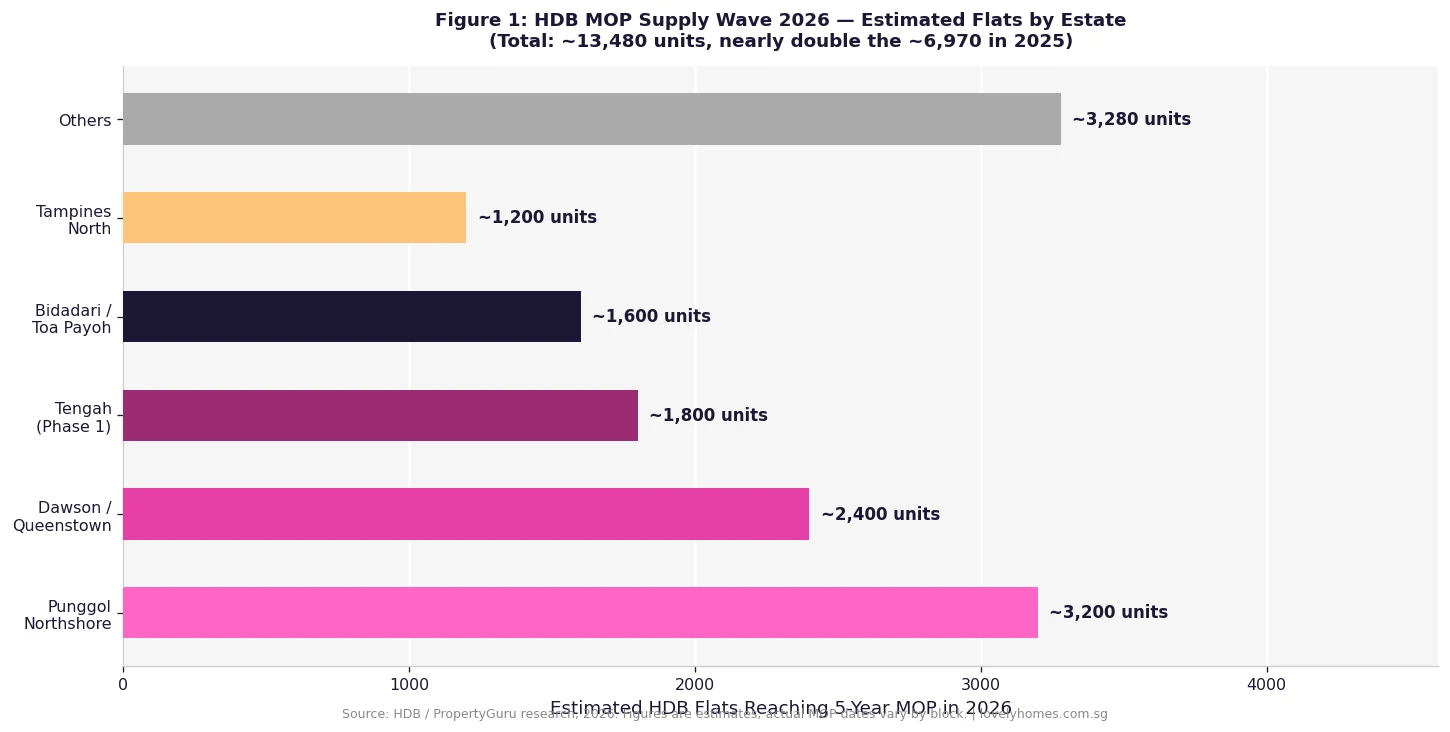

- Scale: An estimated 13,480 HDB flats will reach their 5-year Minimum Occupation Period (MOP) in 2026 — almost double the ~6,970 that reached MOP in 2025.

- Hotspots: Punggol Northshore (~3,200 units), Dawson/Queenstown (~2,400 units), Tengah Phase 1 (~1,800 units), and Bidadari (~1,600 units) are the largest contributors.

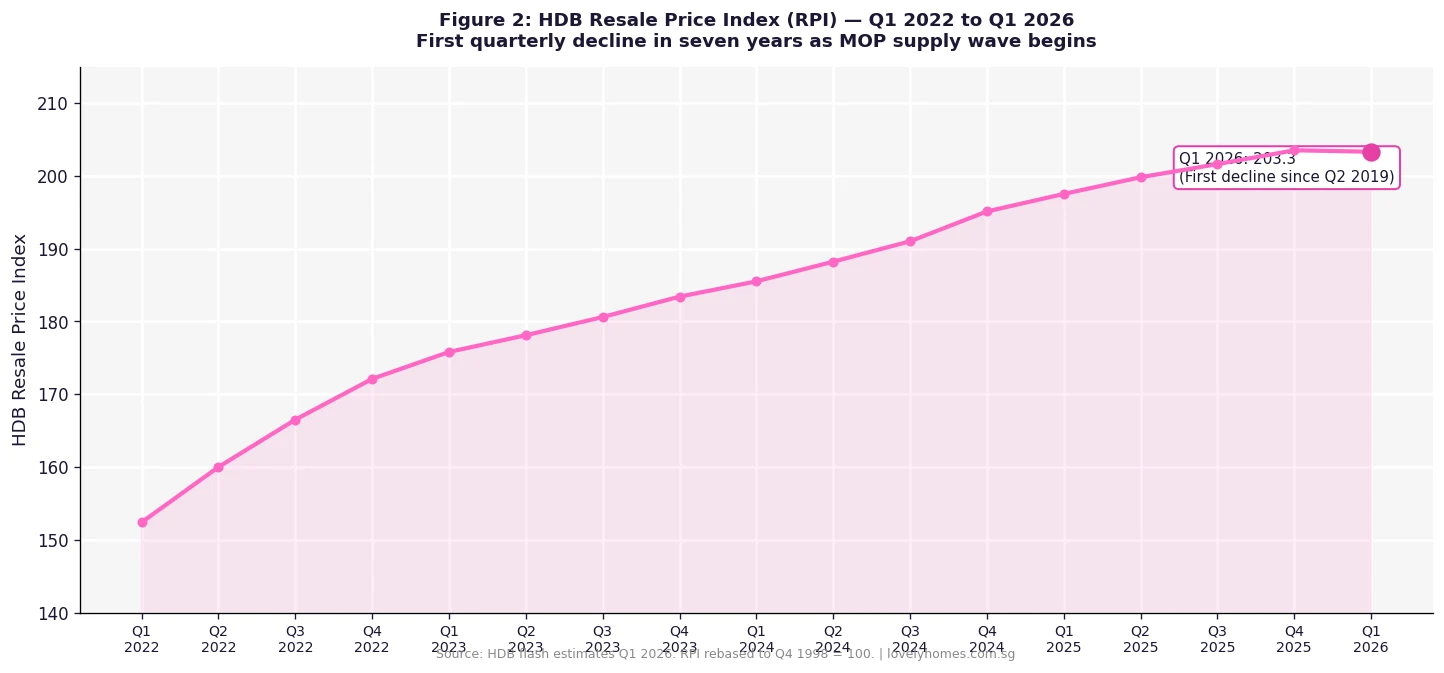

- Market effect: The HDB Resale Price Index (RPI) fell 0.1% in Q1 2026 — its first quarterly decline since Q2 2019, partly attributable to rising MOP-flat supply.

- For buyers: More choices, reduced bidding urgency, and improved negotiating power — especially in estates with cluster supply.

- For sellers: Longer time-on-market expected (up from the typical 6–8 weeks to 10–12 weeks in high-supply estates) and more realistic pricing required.

- For upgraders: Demand for private OCR condos remains firm; OCR prices rose 2.2% in Q1 2026 as MOP-flat sellers redirect proceeds to private property.

The MOP Supply Wave: How We Got Here

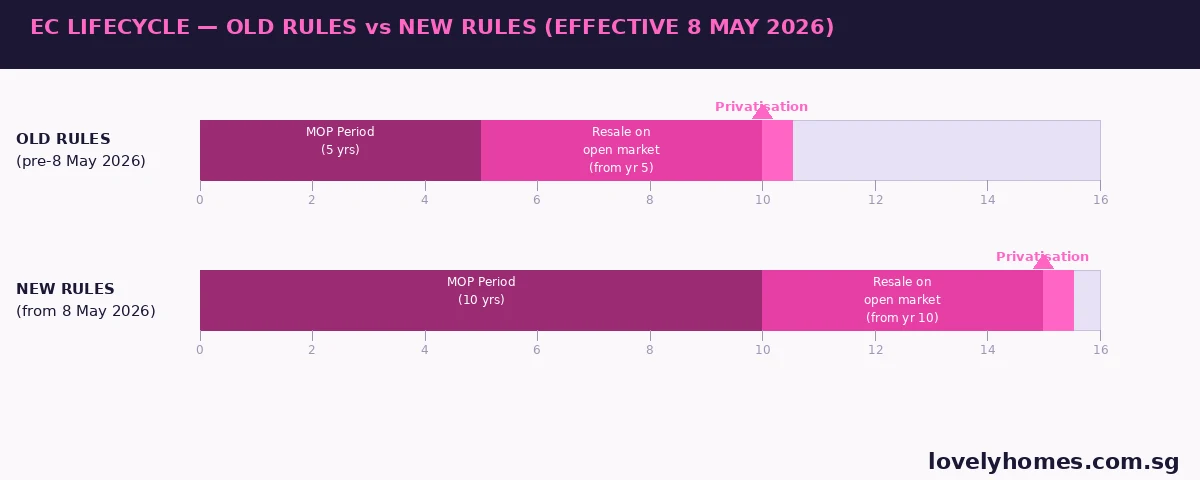

The Minimum Occupation Period is the mandatory period — typically five years for standard HDB flats, now extended to ten years for certain Plus and Prime classification flats under HDB’s 2024 reclassification framework — during which an HDB flat owner cannot sell their unit on the open resale market. The MOP clock starts from the date of flat key collection, not the date of purchase application or ballot.

The surge in MOP-eligible supply in 2026 is a direct consequence of the unprecedented BTO construction and completion activity that took place between 2019 and 2021. During those years, HDB launched and completed tens of thousands of flats in new growth areas — particularly Tengah, Punggol Northshore, Bidadari, and the rejuvenated Dawson/Queenstown estates — most of which had key collection dates between late 2020 and mid-2021. Five years later, those keys have become resale eligibility certificates.

Industry data compiled by PropertyGuru and HDB estimates the 2026 cohort at approximately 13,480 MOP-eligible flats — a volume not seen since the BTO ramp-up years of 2013–2015. The comparison with 2025’s ~6,970 MOP-eligible units illustrates just how dramatic the step-change is.

What the Supply Wave Is Doing to HDB Resale Prices

The most immediate market signal came from HDB’s flash estimate for Q1 2026: the Resale Price Index (RPI) fell by 0.1% quarter-on-quarter, registering 203.3 from 203.5 in Q4 2025. This was the first quarterly decline in the RPI since Q2 2019 — ending a 29-quarter streak of quarterly gains or flat readings that had carried the index from around 131 to its recent high.

To put the decline in context: 0.1% is modest, and the RPI remains 33% higher than its pre-pandemic Q1 2020 level. But the direction of travel is significant. Several forces are converging simultaneously: the MOP supply wave, shorter BTO build times reducing the wait for new flats (increasing substitution options), residual effects of the ABSD cooling measures, and a gradual easing of the buyer urgency that characterised the 2021–2023 market.

Worked Example: What the MOP Wave Means for a Punggol Seller

Mr Tan bought a 4-room BTO flat in Punggol Northshore in 2021, collecting keys in February 2021. His MOP expires in February 2026, giving him the right to list on the open market from that date onwards.

In early 2024, comparable 4-room resale flats in Punggol Northshore (then still pre-MOP and transacting via sub-sale with special conditions) were fetching around S$720,000–S$740,000. When Mr Tan lists in March 2026, he faces a materially different supply environment: an estimated 200–300 comparable units in the same estate are also newly MOP-eligible in Q1–Q2 2026.

| Scenario | Indicative Price | Time-on-Market |

|---|---|---|

| Q1 2024 (pre-MOP cluster, limited supply) | ~S$730,000 | ~5–6 weeks |

| Q2 2026 (post-MOP wave, clustered supply) | ~S$695,000–S$710,000 | ~10–12 weeks |

| Indicative price softening (2024 vs 2026) | ~S$20,000–S$35,000 | +4–6 weeks |

| Original BTO purchase price (2021) | ~S$410,000 | — |

| Estimated capital gain (even at lower price) | ~S$285,000–S$300,000 | — |

Mr Tan’s capital gain, even after the supply-induced price moderation, remains substantial — roughly 69–73% above his original purchase price over five years. The MOP wave reduces margins at the margin, but does not eliminate them. The more important implication for him is patience: in a supply-heavy quarter, chasing the last S$20,000 with an overpriced listing will cost more in time and negotiating leverage than pricing realistically from day one.

What the MOP Wave Means for HDB Buyers

For buyers in 2026, the supply wave is largely positive. More resale supply in desirable, well-located estates — Dawson, Bidadari, Tengah — means genuine choice where previously the listings were sparse and asking prices aggressive. Buyers who were priced out or crowded out of these estates in 2023–2024 may find that the 2026 MOP cohort opens affordable windows.

Notably, many of the MOP-eligible flats are in mature or near-mature estates with established amenities and shorter HDB wait times (since they are resale, not BTO, there is no wait). For young families who need a flat quickly, the MOP wave is creating the most compelling resale market conditions seen since 2019.

What the MOP Wave Means for Private Property and EC Upgraders

Every MOP-eligible seller is a potential upgrader. The strong demand for Outside Central Region (OCR) private condominiums — OCR prices rose 2.2% in Q1 2026, the strongest regional performer — is partly explained by this upgrader flow. MOP sellers, sitting on capital gains of S$200,000–S$400,000 from their BTO purchases, are redeploying proceeds into OCR condos in the S$900,000–S$1.4M range, often as a second property with ABSD implications or as their primary home after selling the HDB flat.

The new 10-year MOP rules for Plus and Prime classification BTO flats (effective from launches from May 2024 onwards) will throttle a future wave of upgrader supply in those categories — but the current 2026 MOP cohort predates those rules, and almost all are standard 5-year MOP flats that feed directly into the upgrader pipeline.

What Might Come Next

The MOP wave is likely to remain elevated through 2026 and into early 2027, as BTO completions from 2021–2022 continue to roll through. HDB’s accelerated build programme — driven by the post-pandemic construction catch-up — means further tranches of completed flats entering the 5-year MOP window. Analysts broadly expect HDB resale price growth to be in the 0–2% range for full-year 2026, a sharp deceleration from the 8–10% growth seen in 2022. The supply-induced softening is a policy success by design — HDB has explicitly timed BTO ramps to moderate resale inflation. Whether prices resume growth in 2027 and 2028 will depend heavily on the pace of upgrader absorption into the private market and any further policy interventions.

Frequently Asked Questions

When exactly does the 5-year MOP start and end?

The MOP clock starts from the date of key collection — not from the date of flat application, ballot, or signing of the Sales of Balance Flat agreement. For BTO flats, this is the date on the key collection acknowledgement letter issued by HDB. The MOP ends exactly five years from that key collection date. Flat owners can check their specific MOP expiry date through the HDB e-Service portal.

Can I rent out my entire flat before MOP?

No. During the MOP, you must physically occupy your HDB flat. You cannot rent out the entire flat. You may, subject to HDB approval, rent out individual bedrooms while continuing to live in the flat. Subletting the entire unit without meeting the post-MOP and quota requirements is a serious breach of HDB’s tenancy rules and can result in compulsory acquisition of the flat.

Does the 10-year MOP apply to all HDB flats bought in 2026?

No. The 10-year MOP applies only to Plus and Prime classification BTO flats launched from May 2024 onwards (under HDB’s new flat classification framework). Standard classification BTO flats retain the 5-year MOP. All resale HDB flats have no MOP obligation for the buyer (the original MOP is with the seller, not the resale purchaser). The current 2026 MOP wave consists entirely of 5-year MOP flats from the pre-2024 launch cohort.

Are the MOP flats from mature or non-mature estates?

The 2026 MOP wave is mixed. Dawson (Queenstown) and Bidadari (Toa Payoh) are in mature estates with strong locational attributes. Punggol Northshore and Tengah are in newer, non-mature estates. The distinction matters for resale pricing: mature estate MOP flats typically command a premium due to established transport, amenities, and school catchments, while non-mature estate flats benefit from newer build quality and larger layouts at lower absolute prices.

Will the MOP wave cause HDB prices to fall significantly?

Industry consensus as at May 2026 expects HDB resale price growth of 0–2% for full-year 2026 — not a significant decline. The Q1 2026 dip of 0.1% is a moderation, not a crash. Singapore’s tight land supply, ongoing population household formation, and strong upgrader demand underpin a structurally supported HDB resale market. A supply wave of 13,480 units — spread across multiple estates over twelve months — is material but not large enough to overwhelm a market that transacts approximately 25,000–27,000 resale flats per year.

Related Articles

- Minimum Occupation Period (MOP) Singapore 2026: HDB, EC and Private Property Rules

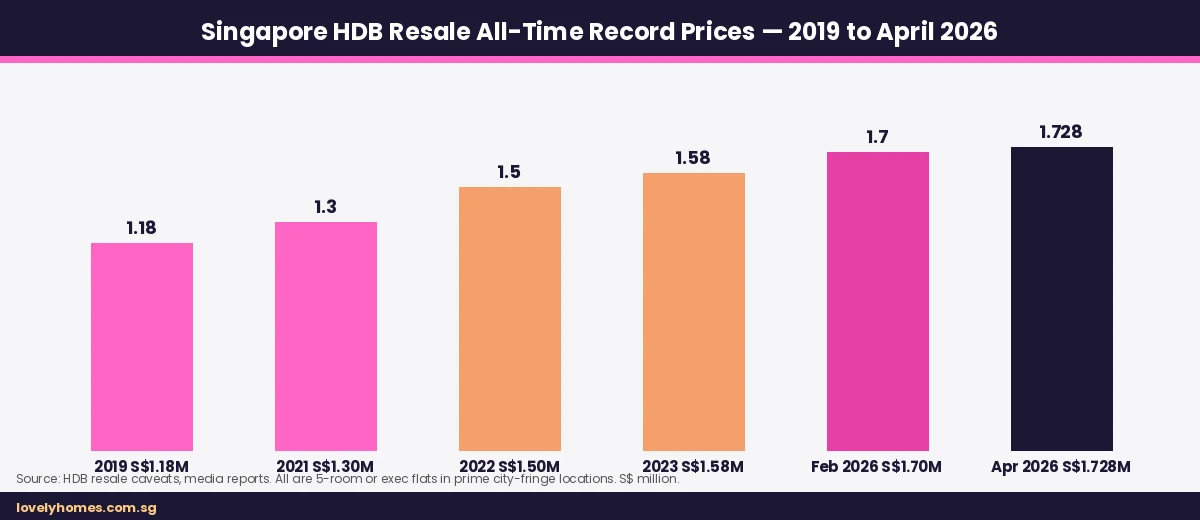

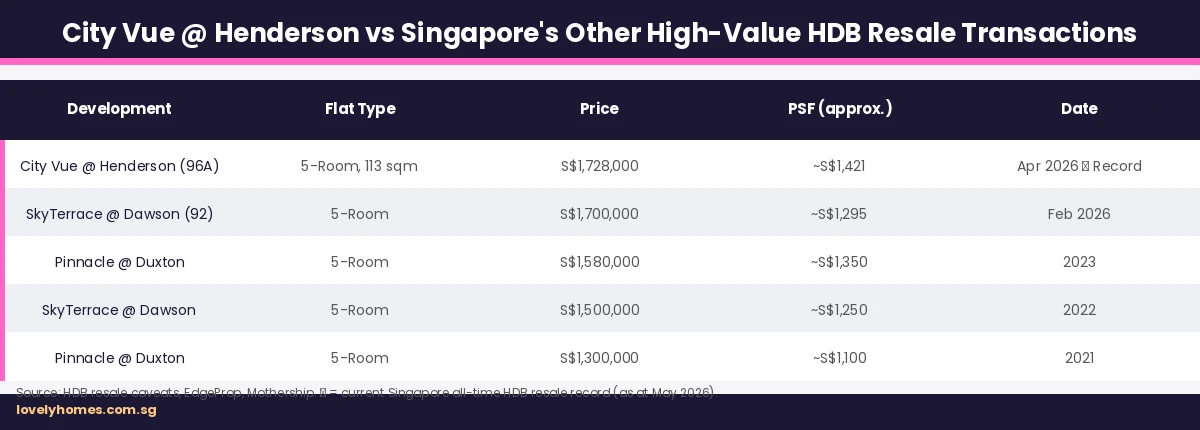

- S$1.728M HDB Resale Record: City Vue @ Henderson Sets New All-time High

- HDB Resale Price Index Q1 2026: First Quarterly Decline in Seven Years

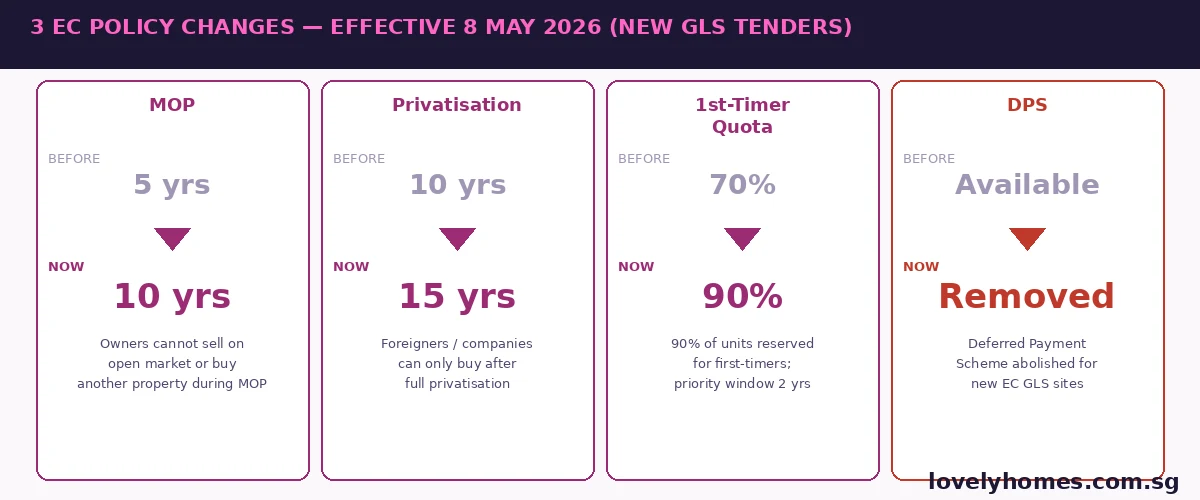

- Singapore EC Cooling Measures May 2026: 10-Year MOP, 90% First-Timer Quota

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- HDB Income Ceiling Singapore 2026: BTO, EC, EHG and Resale

Disclaimer: This article is for informational purposes only and does not constitute financial or property advice. MOP unit estimates are based on publicly available industry data and HDB records; exact figures vary by flat and block. Property price data sourced from HDB flash estimates (Q1 2026). Readers should verify MOP expiry dates with HDB directly at www.hdb.gov.sg and consult a licensed property agent or financial adviser before making any purchase or sale decision. References: HDB Q1 2026 Flash Estimates; URA; PropertyGuru; Stacked Homes, May 2026.