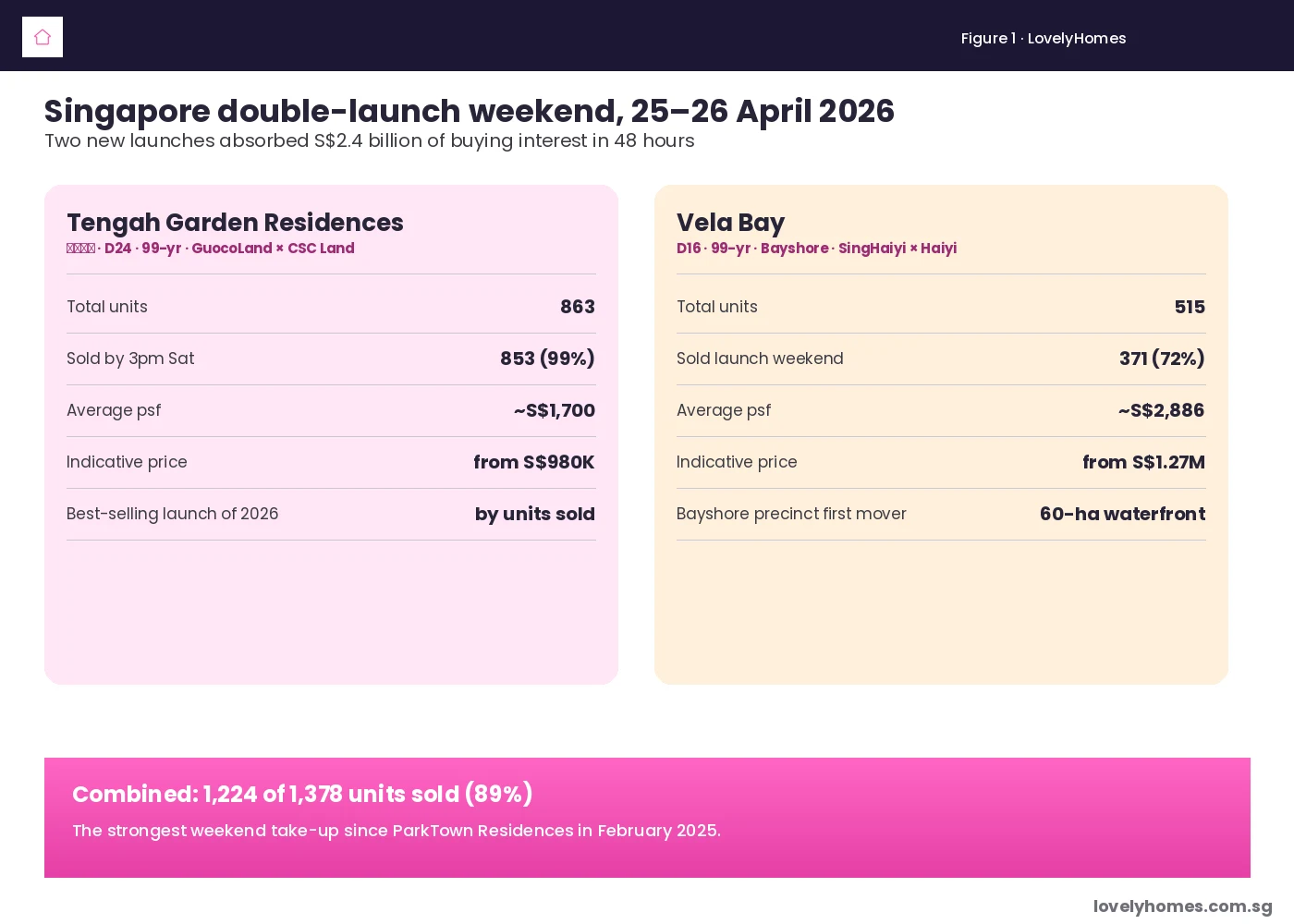

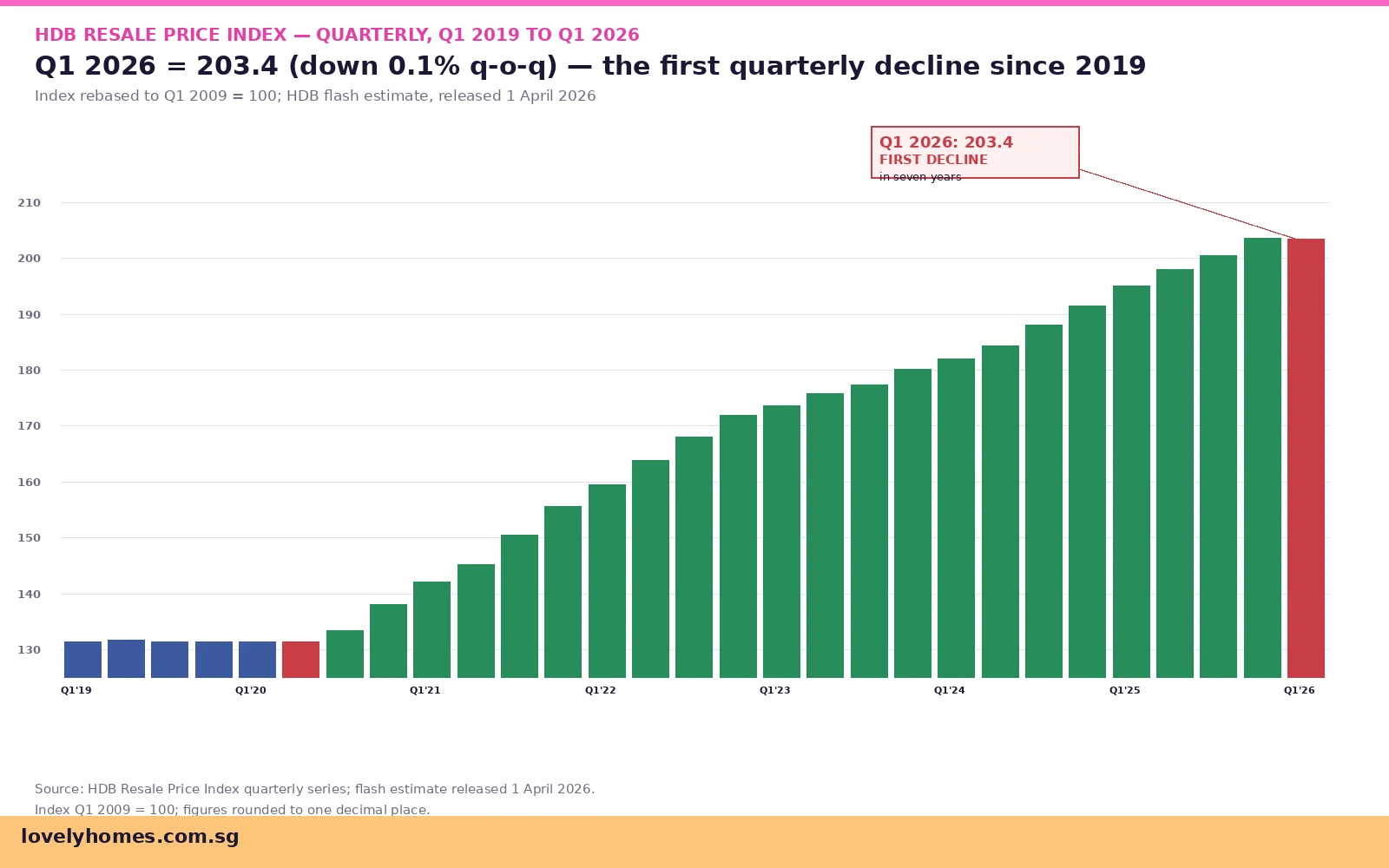

HDB Resale Price Index Q1 2026: First Quarterly Decline in Seven Years — What the 0.1% Dip Actually Means

The Housing & Development Board’s flash estimate of the Q1 2026 Resale Price Index (RPI) reads 203.4 — a 0.1 percent dip from the 4Q 2025 reading of 203.6. It is a small number on a small index, but it lands as the first quarterly decline in seven years, ending a continuous-growth run that began in Q3 2020 and that lifted the index by more than 70 points across 22 quarters. The dip arrives alongside record-high million-dollar flat transactions (412 in Q1 2026) and a continuing slide in transaction volume on a year-on-year basis.

Quick Answer

- HDB RPI Q1 2026 = 203.4, down 0.1 percent from Q4 2025’s 203.6 (HDB flash estimate, released 1 April 2026).

- First quarterly decline since 2019, ending a 22-quarter growth run that began in Q3 2020.

- Resale transactions: 6,285 in Q1 2026, slowing year-on-year, but up quarter-on-quarter from a holiday-soft Q4 2025.

- Million-dollar flats: 412 transactions in Q1 2026 — a record quarterly figure, concentrated in mature estates like Bukit Merah, Toa Payoh and Queenstown.

- Top-end stays hot, mass-market softens. The RPI dip masks a divergence: million-dollar flats kept rising while standard 4-room and 3-room mass-market resale eased.

- Drivers: sustained BTO supply, shorter BTO build cycles (some completing in 36 to 42 months), the Open Booking of Flats (OBF) regime adding ~7,800 units annually, and cooling measures still binding marginal buyers.

- Outlook: HDB explicitly attributes the deceleration to demand-supply rebalancing; analysts expect another flat-to-mildly-negative print in Q2 2026 before stabilisation.

The Number Itself

The RPI is a Laspeyres index rebased to Q1 2009 = 100, designed to track the price of a representative bundle of HDB resale flats. It is not a transaction-volume measure and does not reflect the prices of new HDB sales. The flash estimate uses caveats lodged through the early weeks of the quarter — the final figure for Q1 2026 will be published in late April with the full set of caveats.

The flash reading of 203.4 is 0.1 percent below the Q4 2025 print of 203.6. That is essentially a flat outcome — well within the noise band of any quarterly index — but the symbolism matters. The previous quarterly dip was in Q1 2019 (RPI 131.5, down from Q4 2018’s 131.5 — i.e. the index has been flat or rising every single quarter from Q2 2019 onwards). A 22-quarter run of continuous growth covered the pandemic lift-off (Q3 2020 onwards), the post-pandemic surge (2021–2022), the 2023 ABSD reset, and the 2024–2025 plateau-with-growth pattern.

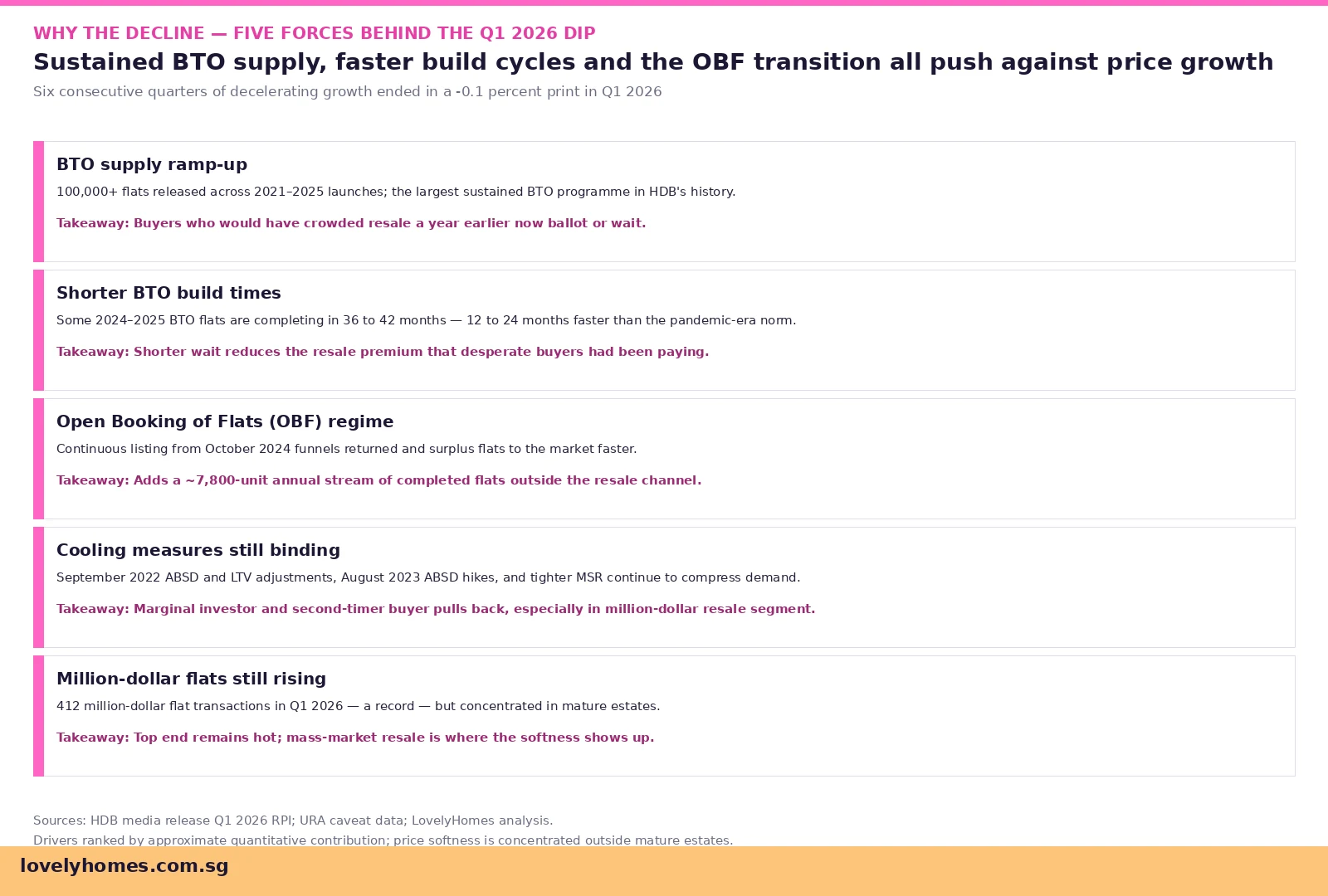

Why It Happened — Five Pressures

HDB’s own commentary points to a structural rebalancing of supply and demand. Five forces stand out.

BTO supply ramp-up. HDB launched more than 100,000 BTO flats across 2021–2025, the largest sustained build-to-order programme in its history. The cumulative effect is that buyers who once felt forced to chase resale because BTO supply could not match demand now have credible alternatives — both fresh ballots and older project units becoming available.

Shorter BTO build cycles. Some 2024–2025 BTO projects are completing within 36 to 42 months, 12 to 24 months faster than the pandemic-era norm. A four-year wait turning into a three-year wait is enough to flip the resale-vs-BTO calculus for a meaningful slice of marginal buyers.

Open Booking of Flats (OBF). The continuous-listing regime that replaced quarterly SBF in October 2024 adds roughly 7,800 completed-or-near-complete flats per year to the supply pipeline outside the resale channel. A buyer who would have settled for a resale 4-room in Sengkang at S$680,000 a year ago can now book an OBF return in the same town for ~S$565,000.

Cooling measures still binding. The September 2022 ABSD and LTV adjustments, the August 2023 ABSD hikes, and the tighter MSR continue to compress demand from second-property buyers, marginal investors and second-timers. The resale market — especially the high-quantum end — feels this most.

The million-dollar segment is an outlier. 412 million-dollar HDB transactions in Q1 2026 is a record quarterly figure, concentrated in mature estates with strong amenity, school proximity, and lease tenor. The top end is hot. The mass-market resale (3-room and standard 4-room flats in non-mature estates) is where the softness shows up. The aggregate index averages both, and the mass-market drag wins this quarter.

Summary — Key Q1 2026 Indicators

| Indicator | Q4 2025 | Q1 2026 | Change |

|---|---|---|---|

| RPI | 203.6 | 203.4 | -0.1% q-o-q |

| Resale Transactions | ~6,070 | 6,285 | +3.5% q-o-q (-y-o-y) |

| Million-Dollar Transactions | ~370 | 412 | Record quarterly |

| Median 4-Room Resale Price (Mature) | S$760,000 | S$758,000 | -0.3% |

| Median 4-Room Resale Price (Non-Mature) | S$612,000 | S$608,000 | -0.7% |

Source: HDB flash estimate Q1 2026 RPI release, HDB resale price summary; LovelyHomes compilation.

Worked Example — A Buyer Looking at a 4-Room Resale Right Now

Take a hypothetical first-time buyer family looking at a 4-room resale in Punggol with about S$120,000 in CPF and S$60,000 cash savings, household income S$8,400 per month. Twelve months ago, the same flat traded at roughly S$632,000. Today the asking price is S$608,000 — a S$24,000 saving on the headline price, plus stronger negotiating leverage as the seller pool has grown. With Family Grant (S$25,000), Proximity Grant (S$30,000) and EHG (~S$45,000 at this income), the effective net cost lands around S$508,000.

The same buyer’s BTO option (next launch, October 2026) carries a ~3.5-year wait — meaning rent of about S$2,800 per month for 42 months, or S$117,600. The OBF option (4-room return in Sengkang) sits at S$565,000 with similar grants, but the buyer must accept whatever location is available in the listing. The Q1 2026 dip changes the calculus by trimming the resale premium just enough to make resale competitive again with the OBF route — the comparison gets closer, even if it does not flip outright.

Why This Matters For You

For buyers, the dip is mildly good news but does not change strategy. A 0.1 percent quarterly move is well within typical noise — buyers should not delay purchases waiting for a meaningful price retreat that may not come. What the dip does signal is that the relentless price growth of 2020–2024 is over, and that resale is no longer the only viable route for buyers needing a flat in months rather than years.

For sellers, the message is to price realistically. The Q1 2026 evidence is that listings priced ahead of valuation are sitting longer; price-to-value listings still clear within standard timeframes. Cash-Over-Valuation (COV) bidding has compressed substantially in non-mature estates.

For investors, the dip strengthens the cyclical case for HDB resale relative to private resale — but the ABSD wall on second properties remains the binding constraint regardless of the index print.

What Comes Next

Three things to watch over the coming quarters. First, whether Q2 2026 flash extends or reverses the dip — a single negative print is noise; two consecutive prints would mark a meaningful inflection. Second, whether the million-dollar segment continues to outpace the rest, suggesting the index dip is structural rather than cyclical. Third, the BTO October 2026 launch (~6,900 flats) and the next OBF refresh — supply pressure has been the dominant driver, and the supply pipeline shows no signs of reversing.

The May 2026 BTO launch, the 7 May 2026 closing of the Holland Plain GLS tender, and the next URA quarterly release are the immediate market-moving milestones to track.

Frequently Asked Questions

Is the Q1 2026 RPI dip the start of a crash?

No. A 0.1 percent quarterly decline is well within statistical noise on an index that has moved by single decimals every quarter for years. It is meaningful as a symbolic marker — the first dip in seven years — but not as evidence of a substantial fall in HDB resale prices. The drivers are gradual supply-demand rebalancing, not distressed selling.

If the index fell, why are million-dollar flats hitting records?

Two different segments. The RPI averages all resale flats, weighted by volume. Million-dollar transactions sit at the top of the distribution — mature estates, larger flats, prime location, often near MRT and good schools. That segment continues to receive strong demand, particularly from upgraders sitting out the private market. The mass-market segment (standard 3-room and 4-room flats in non-mature estates) is where the softness shows up and pulls the overall index slightly negative.

Should I delay buying because prices might fall further?

Generally no. A 0.1 percent quarterly dip is roughly S$600 on a S$600,000 flat — far less than the rental cost of waiting. If the unit suits your needs and the price meets valuation, the timing argument has minimal weight. The bigger move on price would require a much larger supply or demand shock than the current data shows.

How does the OBF regime affect resale prices?

Open Booking of Flats adds completed and near-complete flats to the supply pipeline at HDB-set prices, typically 15 to 20 percent below resale equivalents in the same project. This caps how high resale sellers can push pricing in towns with active OBF listings — a flat in Sengkang priced at S$680,000 looks expensive next to a comparable OBF return at S$565,000.

When does the final Q1 2026 RPI come out?

HDB typically releases the final quarterly RPI in late April or early May with the full caveat dataset. The flash estimate (203.4) was published on 1 April 2026; revisions are usually within 0.1 to 0.3 index points. The full Q1 2026 release will also include median resale prices by town and flat type, plus volume breakdowns.

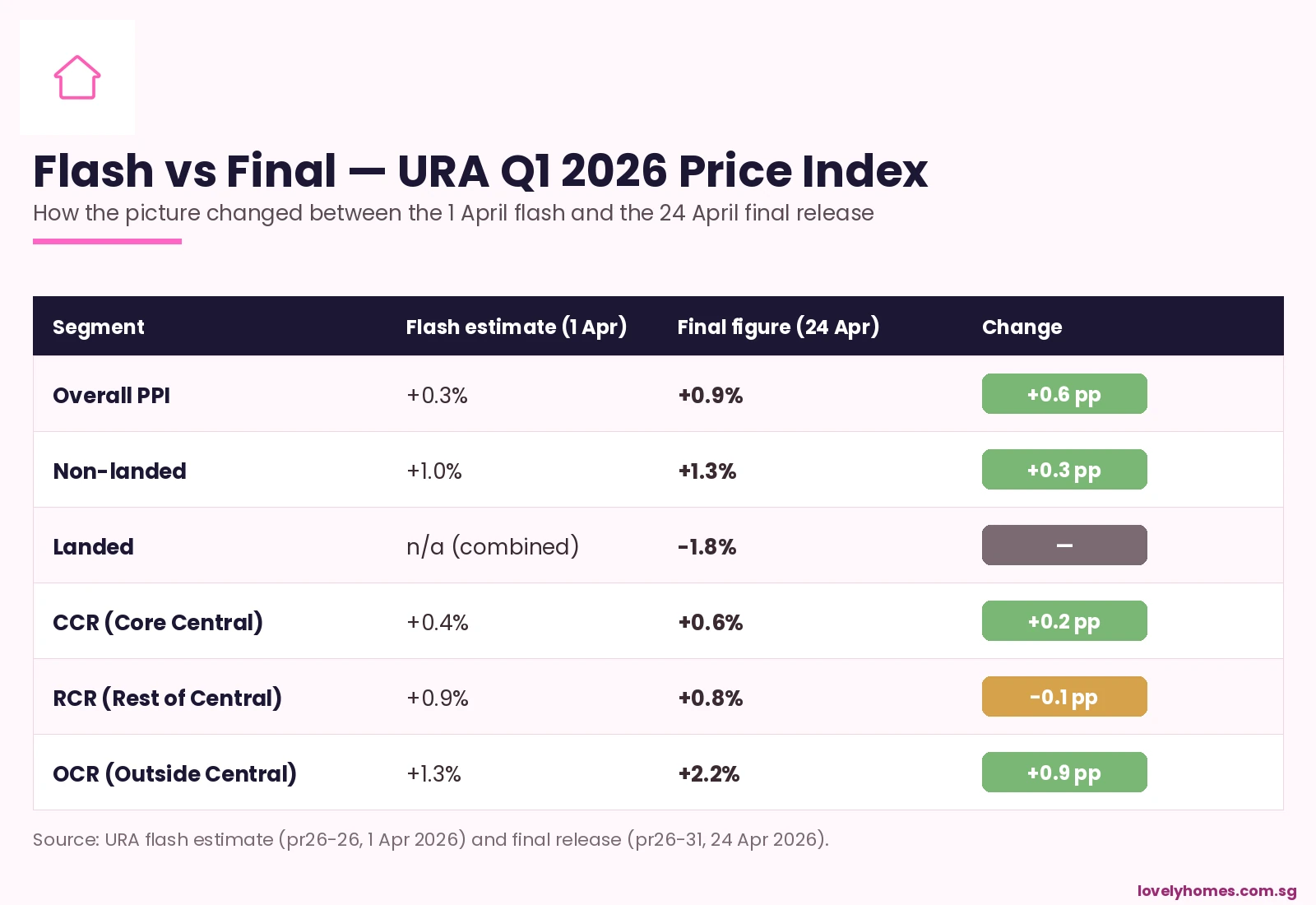

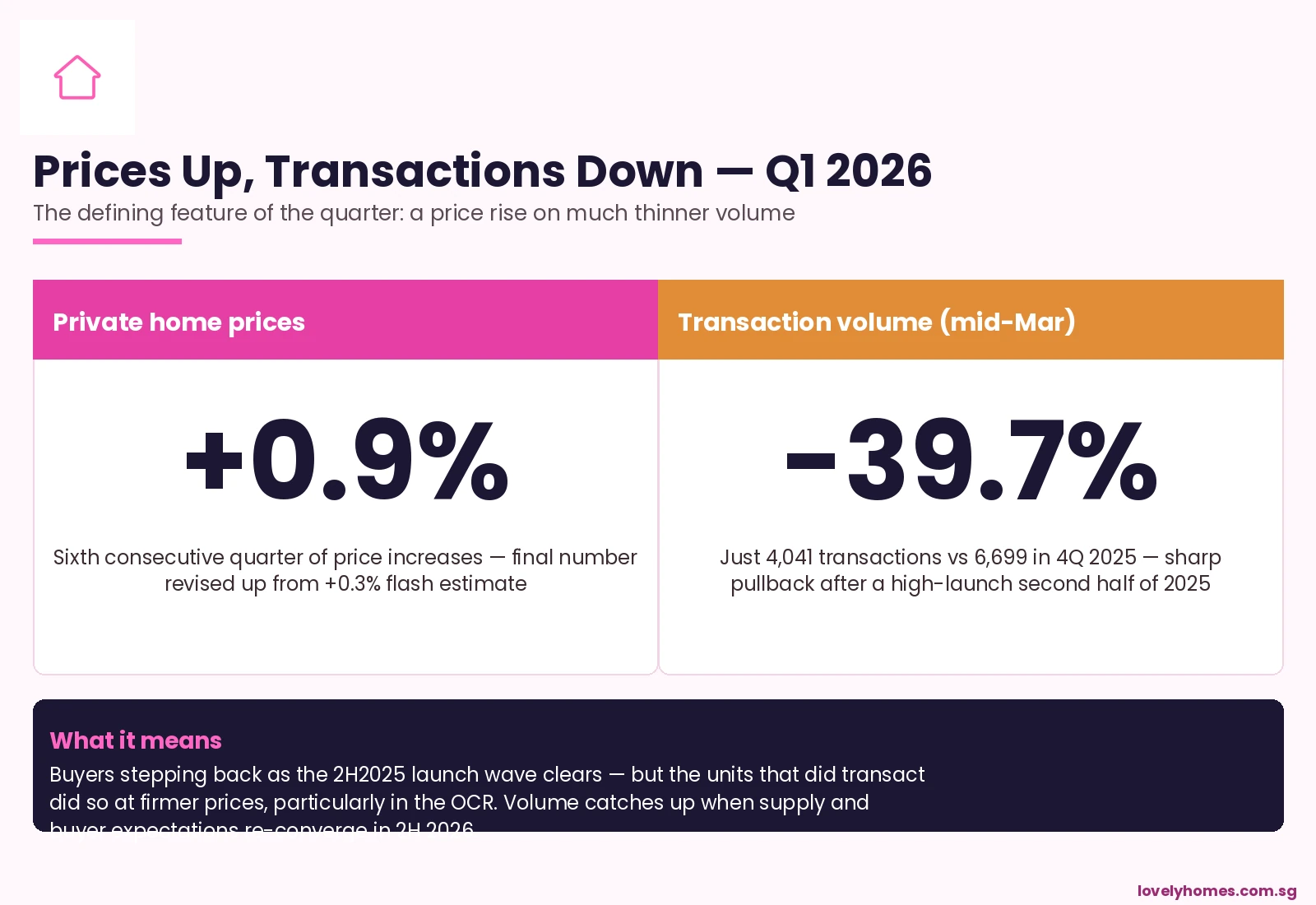

Are private home prices doing the same thing?

No — the URA private residential price index rose 0.9 percent q-o-q in Q1 2026 (revised up from a flash 0.3 percent), led by a 2.2 percent OCR increase. The two markets have decoupled: private residential is being driven by new launches, foreign demand and condo upgrade activity, while HDB resale is being weighed down by sustained BTO and OBF supply.

Related Articles

- Sale of Balance Flats Singapore 2026: Open Booking, Eligibility and How They Differ from BTO

- HDB MOP Supply Bumper 2026: How 13,484 Newly-Eligible Flats Are Reshaping Resale and Rentals

- HDB Million-Dollar Flats Singapore 2026: Where, Why, and Whether One Is Worth Buying

- URA Q1 2026 Private Home Prices Rise 0.9% — Revised Up from +0.3% Flash, OCR Leads at +2.2%

- June 2026 BTO Launch Preview: 6,900 Flats Across 7 Projects in 5 Towns

- Plus and Prime Flats Singapore 2026: 10-Year MOP, Subsidy Clawback and the S$14,000 Income Ceiling Explained

Disclaimer

This article is general information for Singapore property buyers, sellers and observers, and is not legal, tax, financial or investment advice. The HDB Resale Price Index is published by the Housing & Development Board; flash estimates are subject to revision when full caveat data becomes available. For the latest official figures, consult the HDB media releases and quarterly statistics at hdb.gov.sg. Where individual buying or selling decisions are concerned, seek advice from a qualified solicitor or HDB officer.