Singapore 2H2026 GLS Programme Guide: 9 Sites, 4,745 New Homes and What the Pipeline Means

Quick Answer: Singapore’s 2H2026 Government Land Sales (GLS) Confirmed List, announced by URA on 3 June 2026, offers nine sites that can yield 4,745 private homes — including 735 Executive Condo units and 1,200 homes in the landmark Jurong Lake District white site. Full-year Confirmed List supply reaches 9,320 units: 50 per cent above the ten-year annual average. Nine sites span five regions; competition remains robust with an average of 4.6 bidders per GLS tender in 2026.

- Total supply: 4,745 units — 4,010 private + 735 executive condo (EC).

- Sites: Nine Confirmed List sites (eight private residential + one white site), plus a separate Reserve List of thirteen sites.

- Announced: 3 June 2026 by the Ministry of National Development (MND).

- Full-year supply: 9,320 Confirmed List units in 2026 — 50% above the 10-year annual average of approximately 6,200 units.

- Standout plot: Townhall Link white site in Jurong Lake District — 3.72 ha, 1,200 homes + 83,350 sqm commercial GFA; tender opens July 2026.

- First EC in Jurong East in ~30 years: Jurong East Avenue 1 (735 units) under new 10-year MOP rules.

- Orchard Boulevard: Boutique CCR site (110 units); expected top bid up to S$1,700 psf ppr, up to 8 bidders.

- Market temperature: Average 4.6 bidders per GLS tender in 2026 vs 2.4 in 2024 — developer confidence remains firm.

What Is the Government Land Sales Programme?

The Government Land Sales programme is the primary mechanism through which the Singapore government releases state land for private residential and mixed-use development. Administered jointly by URA (for private residential sites) and HDB (for EC sites), the GLS programme is announced twice a year — once for the first half (1H) and once for the second half (2H) of the calendar year. Sites are categorised into two lists: the Confirmed List, which is released unconditionally for tender regardless of market conditions, and the Reserve List, which is released only when a developer submits a minimum bid above URA’s reserve price and triggers an application.

The GLS programme is the government’s single most powerful tool for managing private housing supply. Historically, the annual volume of Confirmed List sites has been calibrated against unsold developer inventory, price trends, and macroeconomic conditions. A high Confirmed List release — as in 2026 — signals a government intent to pre-empt price overheating by ensuring adequate forward supply. Buyers, investors, and developers all watch the programme closely because the sites released today shape the supply of completions three to four years ahead.

The Nine 2H2026 Confirmed List Sites

The nine sites span four broad market segments. Two Core Central Region (CCR) sites — Orchard Boulevard and Holland Plain — introduce 610 units in the city’s most premium residential precinct, continuing the measured release of CCR supply that has characterised government policy since 2023. Four Rest of Central Region (RCR) sites — Marina Gardens Lane, Tanjong Rhu Close, Berlayar Close, and East Coast Road — concentrate development in emerging waterfront and city-fringe precincts with excellent transport connectivity. One Outside Central Region (OCR) site at De Souza Avenue adds mass-market supply in the Bukit Timah planning area. The white site at Townhall Link is the most transformative, anchoring the second phase of the Jurong Lake District’s development as Singapore’s second Central Business District. And the EC site at Jurong East Avenue 1 is the first such site offered in the Jurong East area in nearly three decades.

Unit Supply by Site and Region

Orchard Boulevard (CCR, 110 units)

Situated at the corner of Orchard Boulevard and Tomlinson Road, this 0.34-hectare residential site is described by market observers as “probably one of the last few land plots along Orchard Boulevard”. At a projected top bid of up to S$1,700 per square foot per plot ratio (psf ppr), the site offers a manageable unit yield that limits absolute development risk and is expected to draw up to eight bidders. For context, the most recently awarded CCR site in the vicinity — which became Upperhouse at Orchard Boulevard — was sold in February 2024 at S$1,616 psf ppr and has moved about 80 per cent of units to date, providing developers confidence in the precinct’s demand fundamentals. The boutique scale of the site (likely to yield a 20-storey tower of approximately 110 units) appeals to buyers seeking exclusivity and the proximity to the Thomson-East Coast Line’s Orchard station.

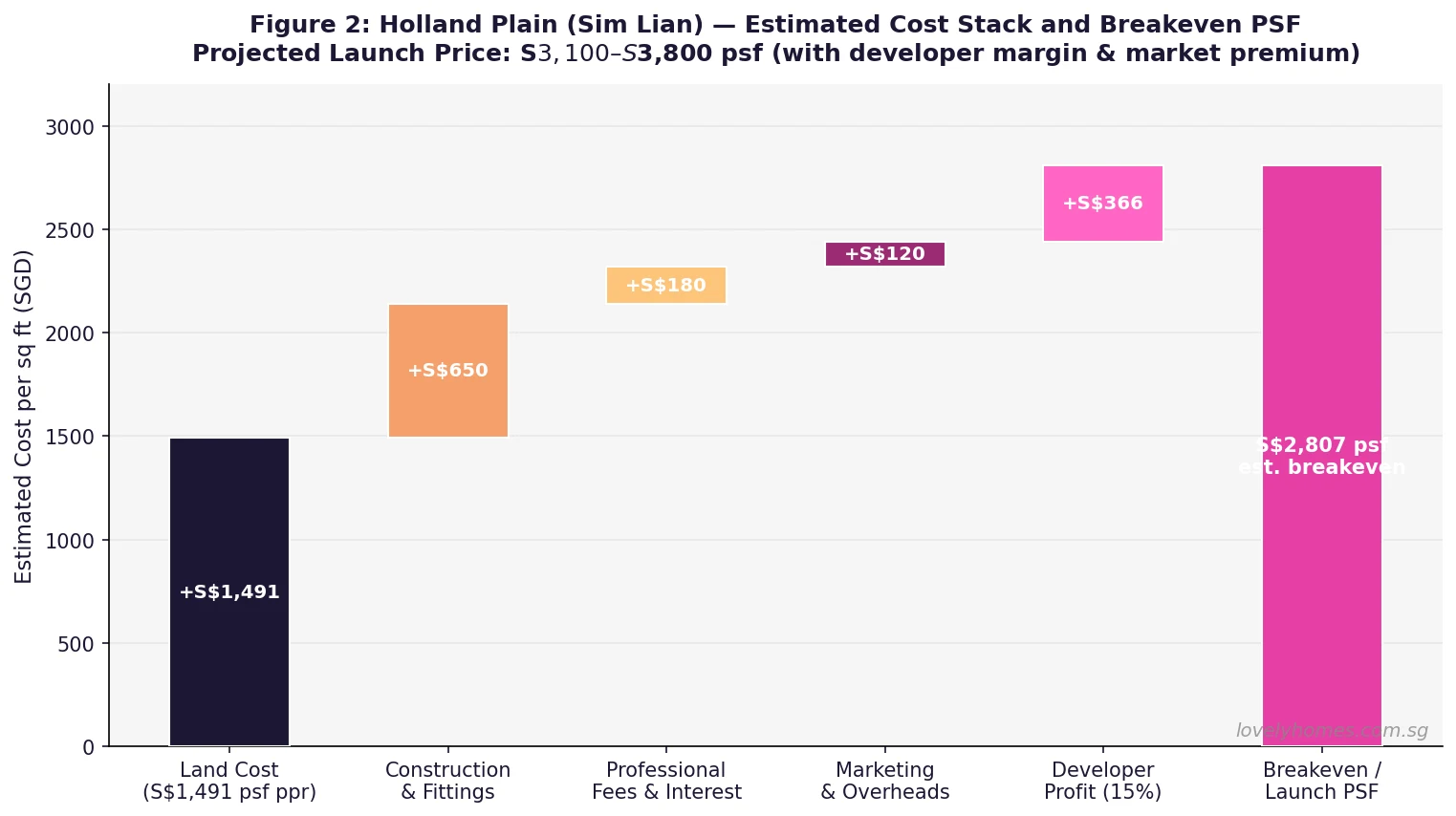

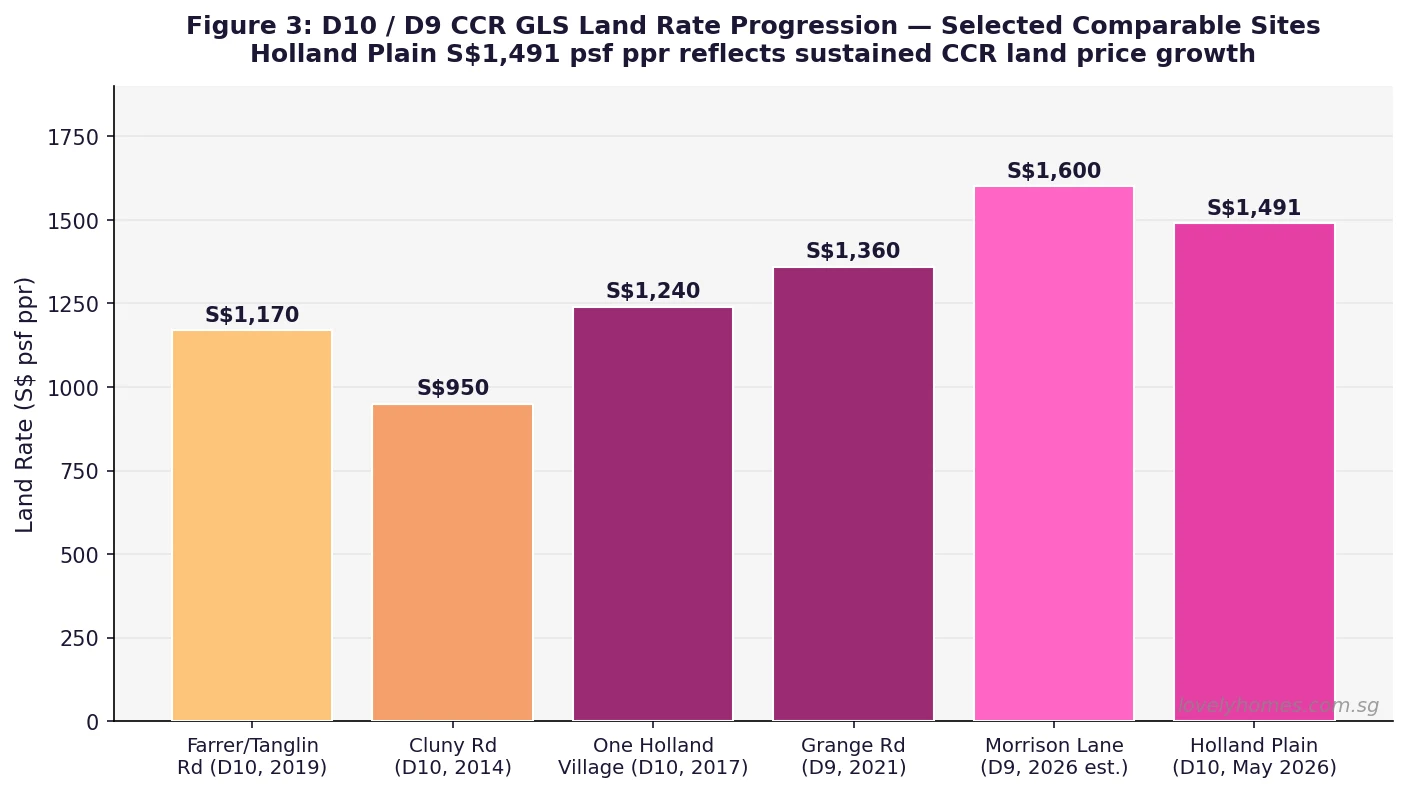

Holland Plain (CCR, ~500 units)

This site is the second CCR site in the 2H2026 Confirmed List and is adjacent to two recently-awarded sites — one at Holland Link awarded to Sim Lian Group at S$1,432 psf ppr in 2025, and a neighbouring Holland Plain site awarded at S$1,391 psf ppr one month prior to the 2H2026 programme announcement. The clustering of three adjacent sites serves a dual purpose: building critical mass in a precinct that is still largely characterised by landed housing and ageing condominiums, while potentially moderating bidding behaviour by reducing the scarcity premium that developers might otherwise price in for isolated plots.

Marina Gardens Lane (RCR, ~390 units)

This is the third site to be offered in the Marina South precinct — Singapore’s emerging waterfront residential neighbourhood on reclaimed land adjacent to Marina Bay. Measuring 0.6 hectares with a residential-with-commercial-at-first-storey zoning, it can yield approximately 390 homes and 150 square metres of commercial space. The site is within walking distance of the upcoming Marina South MRT station on the Thomson-East Coast Line. It is adjacent to One Marina Gardens (937 units), which a Kingsford-led consortium developed and which has sold approximately 68 per cent of units since its April 2025 launch at around S$2,280 psf. The smaller scale of this site is expected to attract mid-sized developers who might otherwise be deterred by the very large plot sizes typical of Marina South.

Tanjong Rhu Close (RCR, ~505 units)

Industry observers consistently rank this as one of the most attractive plots in the 2H2026 programme. Measuring 1.23 hectares, the site is immediately adjacent to a site on Tanjong Rhu Road that was awarded in February 2026 to a City Developments–Woh Hup joint venture at S$1,455 psf ppr — a record land rate for a pure residential site in the Rest of Central Region. The site benefits from its position in a well-regarded enclave close to Marina Bay and the Kallang sports precinct, with the Katong Park and Tanjong Rhu MRT stations approximately ten minutes on foot. Future units are likely to command sea views, adding a premium that historically commands 5–10 per cent above comparable units without such aspects.

Berlayar Close (RCR, ~695 units)

Spanning 2.82 hectares, the Berlayar Close site is the largest of the RCR plots and represents the third site in the Greater Southern Waterfront — a 30-kilometre stretch from Marina East to Pasir Panjang that the government has earmarked for a new waterfront city over the coming decades. The first Greater Southern Waterfront site, at Telok Blangah, was awarded in November 2025 to Kingsford Group at S$1,326 psf ppr and can yield about 745 units. A second Berlayar Drive site (about 415 units) is currently open for tender, closing in August 2026. The Telok Blangah MRT station on the Circle Line is approximately ten minutes on foot.

East Coast Road (RCR, ~85 units)

At 0.55 hectares, this is the smallest of the eight private residential sites, yielding approximately 85 units — a boutique development in the Siglap area, one of Singapore’s last remaining low-density residential enclaves characterised by landed housing and pre-war bungalows. The site carries a minimum unit size requirement of 100 square metres, limiting the ability to create smaller high-yield units and naturally targeting buyers who prioritise space. The site’s distance from the nearest MRT is expected to temper competition, making it more attractive to niche developers focused on landed-style condominium product than to volume builders.

De Souza Avenue (OCR, ~415 units)

Located in the Bukit Timah planning area, this 2.22-hectare site is adjacent to the site of The Sen (347 units), which developer Sustained Land purchased in July 2024 at S$841 psf ppr. The Sen launched in November 2025 and moved about 23 per cent of units on its launch weekend. Interest in De Souza Avenue is expected to be moderate — the site is some distance from an MRT station and lacks a strong HDB upgrader catchment nearby. However, the Bukit Timah address and proximity to good schools, including Pei Hwa Presbyterian, Bukit Timah Primary, and Methodist Girls’ School, give it a defined appeal to families in the primary-school balloting window.

The JLD White Site: Singapore’s Next CBD Pillar

The Townhall Link white site is the most consequential release in the 2H2026 GLS programme. At 3.72 hectares, it is the largest Confirmed List plot and the only mixed-use white site. It can yield up to 1,200 housing units alongside a minimum of 40,000 square metres of office space and 44,000 square metres of additional uses — retail, serviced apartments, hotel, and community facilities — for a total commercial gross floor area of approximately 83,350 square metres.

The site was carved from the former 6.5-hectare master developer plot at Jurong Lake District, which attracted a sole bid of S$640 psf ppr in 2024 that URA rejected as too low. The decision to sub-divide the master plot into smaller parcels reflects a pragmatic acknowledgement that the scale of the original site was deterring competitive bidding and delaying the JLD’s transformation. The Townhall Link site is connected to or in close proximity to four MRT lines: the North-South, East-West, Jurong Region, and the under-construction Cross Island line. It is intended to “spearhead the transformation of JLD into Singapore’s secondary CBD”, in URA’s own words. Its tender opens in July 2026.

The Jurong East EC Site: A 30-Year Gap Closes

The EC site at Jurong East Avenue 1 is the first executive condominium to be offered in Jurong East since Westmere in 1996 — a gap of approximately 30 years. The site can yield 735 units across an area of approximately 2 hectares, making it a large EC development by any measure. It will be the first EC launched under the new ten-year MOP and 15-year privatisation rules announced on 8 May 2026, making its bid result and eventual launch price a critical data point for how the rule changes affect developer land valuations and end-unit pricing.

Demand for EC in the western region — specifically in Jurong East — has historically been strong, driven by a large pool of young Singaporean families working in the Jurong Industrial Estate, the International Business Park, and the growing Jurong Lake District commercial cluster. The site brings full-year EC supply on the Confirmed List to 1,370 units (635 from 1H2026 + 735 from 2H2026), substantially below the 1,970 EC units supplied in 2025. This measured reduction likely reflects the government’s intent to assess how market participants respond to the new MOP framework before recommitting to higher EC volumes.

Historical Context: 2026 Supply at a 10-Year High

Combining the 1H2026 Confirmed List (4,575 units) with the 2H2026 Confirmed List (4,745 units) yields a full-year total of 9,320 Confirmed List units for 2026. This is 50 per cent above the ten-year annual average of approximately 6,200 units and represents the highest Confirmed List supply since at least 2013. The elevated supply programme is a deliberate policy response to private property price growth that has outpaced income growth in Singapore — the private residential property price index (PPI) reached 208.8 in Q1 2026 (URA data), up from 131.5 at the start of 2020, a 59 per cent increase over six years.

The high supply programme has been accompanied by sustained developer appetite. The average number of bidders per GLS tender (excluding ECs) has risen from 2.4 in 2024 to 4.6 in 2026 year-to-date — close to the 5.6 recorded in 2025, a historically active year. Recent launches such as Pinery Residences, River Modern, and Tengah Garden Residences have moved over 90 per cent of units on their respective launch weekends, confirming that end-user demand remains robust despite the elevated ABSD rates introduced in April 2023.

2H2026 GLS Programme: Summary Table

| Site | Region | Est. Units | Area | Notable Feature |

|---|---|---|---|---|

| Orchard Boulevard | CCR | 110 | 0.34 ha | Boutique; among last Orchard Blvd plots; up to 8 bidders |

| Holland Plain | CCR | ~500 | ~2 ha | Third adjacent site; precinct-building strategy |

| Marina Gardens Lane | RCR | ~390 | 0.60 ha | Third Marina South plot; near future Marina South MRT |

| Tanjong Rhu Close | RCR | ~505 | 1.23 ha | Adjacent to Feb 2026 RCR record; sea views; highly sought-after |

| Berlayar Close | RCR | ~695 | 2.82 ha | Greater Southern Waterfront; third GSW site |

| East Coast Road | RCR | ~85 | 0.55 ha | Boutique Siglap landed enclave; 100 sqm min unit size |

| De Souza Avenue | OCR | ~415 | 2.22 ha | Bukit Timah school belt; some distance from MRT |

| Townhall Link (White Site) | JLD | ~1,200 homes +83,350 sqm GFA |

3.72 ha | Largest site; mega mixed-use; anchors JLD as Singapore’s 2nd CBD |

| Jurong East Ave 1 (EC) | Western | 735 EC | ~2 ha | First EC in Jurong East since 1996; new 10-yr MOP rules apply |

| TOTAL | 9 sites | 4,745 units | 4,010 private + 735 EC | Full-year Confirmed List: 9,320 units | |

Worked Example: What the GLS Programme Means for a Buyer Targeting a Launch in 2027–2028

Mr and Mrs Tan are Singapore Citizens planning to upgrade from their HDB flat in Jurong West to a private condominium. Their combined income is S$15,000 per month. They are watching two sites from the 2H2026 GLS programme: the Jurong East Avenue 1 EC (for its income-ceiling alignment and proximity) and the De Souza Avenue site (for its school catchment and OCR pricing).

Option A — Jurong East EC: Land tender expected mid-2H2026; launch likely 2027. At the 2H2026 land release price, comparable EC units in western Singapore have been pricing at S$1,000–S$1,150 psf. A three-bedroom 95 sqm unit might launch at approximately S$1.1M. BSD: S$24,600. ABSD: 0% (first-time SC couple, EC is first property). If the Tans sell their HDB first, down payment at 25% = S$275,000 (5% cash S$55,000 + 20% CPF S$220,000). Bank loan: S$825,000 at 3.1% 30yr = S$3,527/month. TDSR: 23.5% (PASS). However, the ten-year MOP means this unit cannot be sold until approximately 2037–2038 — a significant illiquidity constraint for a couple in their thirties.

Option B — De Souza Avenue private condo: Land tender expected 3Q2026; launch likely 2027–2028. Comparable OCR condominiums near Bukit Timah are launching at S$1,900–S$2,200 psf. A three-bedroom 90 sqm unit might launch at S$1.75M. BSD: S$54,600. ABSD: S$350,000 (20%, SC second property — payable upfront if HDB not yet sold; eligible for remission upon HDB sale within six months). Bank loan: S$1,312,500 at 3.1% 30yr = S$5,619/month. TDSR: 37.5% (PASS under 55%). The private condo has no MOP (Sellers’ Stamp Duty applies for three years post-purchase: 12%/8%/4%), giving far greater flexibility.

Conclusion: The EC route offers substantially lower upfront cost and zero ABSD for a first-time buyer, but the ten-year MOP creates a fifteen-year horizon to liquid resale that requires careful long-term planning. The private condo route demands significantly more cash and ABSD outlay but provides full flexibility and an open buyer pool upon privatisation from day one. For the Tans, if they are highly confident about remaining in the western region for at least fifteen years and do not anticipate significant financial changes, the EC represents better value for money. If their circumstances are likely to change — relocation, family expansion, employment shifts — the private condo’s liquidity premium is well worth paying.

Why the 2H2026 Programme Matters for Singapore’s Property Market

Singapore’s approach to GLS supply management has historically been counter-cyclical: the government releases more land when prices are rising and less when they are correcting. The 2026 Confirmed List total of 9,320 units — the highest in at least a decade — is a clear signal that the government views the prevailing price trajectory as requiring active supply-side management. Private residential prices rose 2.63 per cent year-on-year in Q1 2026 (URA PPI), and the broader context of elevated ABSD rates since April 2023 has not fully dampened demand from genuine owner-occupiers and local investors.

The concentration of RCR sites (Marina Gardens Lane, Tanjong Rhu Close, Berlayar Close, East Coast Road) reflects a deliberate policy to develop Singapore’s waterfront precincts — Marina South, Tanjong Rhu, and the Greater Southern Waterfront — as premium residential addresses that can absorb demand from residents upgrading from ageing RCR stock. The JLD white site, by contrast, is an economic-development play as much as a housing play: the combined residential and commercial component at Townhall Link is intended to accelerate the transformation of Jurong into a self-sufficient live-work-play district.

Peer cities have drawn different supply-side lessons. Hong Kong’s chronic supply shortage and sky-high prices are a cautionary tale for what happens when GLS supply lags consistently behind demand for decades. Sydney’s experience with developer-driven oversupply in the mid-2010s showed that excessive releases can cause sharp short-term corrections. Singapore’s managed approach — calibrated half-yearly, responsive to data — has broadly achieved its goal of a stable market, though at the cost of perpetually high price levels relative to household income.

What Might Come Next

With the 2H2026 Confirmed List sites feeding into the launch pipeline for 2027 and 2028, buyers watching the GLS programme should expect a well-supplied private residential market for the next two to three years. The key swing factor will be the outcome of the JLD Townhall Link tender: if multiple developers bid competitively, it signals robust institutional confidence in the Singapore market; if the tender attracts few bidders or a below-reserve outcome, it may prompt URA to revise the Reserve List strategy. URA Q2 2026 Flash Estimates — expected in the first week of July 2026 — will be the next major data point for whether the elevated supply programme is having the intended moderating effect on prices.

The 1H2027 GLS programme, likely to be announced in December 2026, will also be closely watched. If unsold developer inventory remains elevated (42,561 units in the pipeline as at Q1 2026, of which 17,032 remain unsold), the government may maintain or marginally reduce Confirmed List supply. If take-up continues at the robust pace seen in H1 2026, the supply programme may be sustained or expanded.

Frequently Asked Questions

What is the difference between the Confirmed List and the Reserve List?

The Confirmed List is released for tender by URA regardless of market conditions — developers can submit bids at any time once the site is listed. The Reserve List is held back: a developer must submit a minimum-price application to trigger an official tender for a Reserve List site. The government uses this structure to maintain supply certainty (Confirmed List) while keeping optionality for responsive releases (Reserve List). In practice, a strong Reserve List application signals developer appetite and is often seen as a leading indicator of market activity.

How long does it take from a GLS award to a new launch?

Typically, a developer needs six to twelve months after land award to complete design planning, obtain approvals, and prepare sales materials before launching the project. Construction then takes three to four years from launch before TOP is achieved. So a 2H2026 GLS site awarded in late 2026 or early 2027 would likely launch in mid-2027 to mid-2028 and reach TOP around 2030–2032. Buyers planning to purchase on the primary market should factor in this timeline when deciding whether to buy a new launch or a completed resale unit.

What does “psf ppr” mean and why does it matter?

PSF ppr stands for “price per square foot per plot ratio” — the standard land-value metric used in Singapore GLS tenders. It is calculated as (bid price ÷ land area in sqft ÷ plot ratio). Plot ratio is the zoning parameter that determines how much total floor area a developer may build on a given site. A higher psf ppr means the developer paid more for each unit of developable floor area, which generally flows through to higher end-unit launch prices. Comparing psf ppr across adjacent sites is the most reliable way to track land cost trends across a precinct over time.

Can foreigners buy units launched from 2H2026 GLS sites?

Yes — private residential units launched from all 2H2026 GLS sites (excluding the EC) are open for purchase by foreigners. However, the Additional Buyer’s Stamp Duty for foreigners purchasing any residential property in Singapore is 60 per cent of the purchase price (as at June 2026), making foreign purchases of new private condominiums extremely expensive. The EC at Jurong East Avenue 1 is subject to the standard EC rules: foreigners may not purchase new ECs at all, and can only enter the EC market after full privatisation (15 years from TOP under the new rules).

Does a high GLS supply programme necessarily mean lower prices?

Not necessarily, at least not in the short term. GLS supply translates into completions three to four years after the land award date, meaning the pipeline from 2H2026 will add meaningful inventory only around 2030–2032. In the interim, the supply of completed private homes available for immediate purchase is relatively thin, which can sustain price levels even when forward supply is high. The government’s primary intent is to prevent a structural undersupply from driving prices to extreme levels — as has occurred in Hong Kong — rather than to engineer a price correction. Whether 2026’s elevated supply pipeline produces meaningful price moderation will depend heavily on interest-rate trends, immigration policy, and overall economic growth through 2030.

When can I buy a unit in the 2H2026 GLS sites?

Units in 2H2026 GLS sites will only be available for sale once developers have been awarded the land and prepared their sales launches. Based on the typical timeline, most 2H2026 sites will tender in Q3–Q4 2026, with awards following in early 2027. Launches are likely between mid-2027 and end-2028, depending on developer readiness. The JLD Townhall Link white site tender opens in July 2026 and is likely to be awarded later in 2026; given its complexity, the launch of its residential component may be 2028 or later. Keep an eye on URA’s new sale launches page and the official project showroom announcements for confirmed launch dates.

Related Articles

- Singapore Property Market Mid-Year Outlook 2026: Prices, Trends and What the Second Half Holds

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore New Launch Condo Buying Guide 2026: Everything You Need to Know Before You Sign

- Singapore Executive Condo Guide 2026: Eligibility, New MOP Rules and EC vs BTO vs Condo

- Singapore Property Cooling Measures Guide 2026: ABSD, TDSR, LTV and SSD Explained

- River Valley Green Parcel C GLS 2026: Top Bid S$1,730 psf ppr Sets New River Valley Benchmark

- Singapore Property Portfolio Guide 2026: ABSD, Yields & Strategy

Disclaimer: This article is for general informational and educational purposes only. GLS programme details, site unit yields, and timeline estimates are based on the URA press release of 3 June 2026 and subsequent market commentary. Actual tender outcomes, launch prices, unit counts, and development timelines are subject to change depending on market conditions, regulatory requirements, and developer decisions. Readers should verify all information directly with the Urban Redevelopment Authority (ura.gov.sg), the Housing and Development Board (hdb.gov.sg), and the Ministry of National Development (mnd.gov.sg), and consult a licensed property agent or financial adviser before making any investment or purchase decision.