HDB Prime, Plus and Standard Flats Singapore 2026: Complete Classification Guide

- Three tiers introduced August 2024 BTO onwards, replacing the earlier Prime Location Public Housing (PLH) scheme. All new BTO launches from August 2024 use this classification.

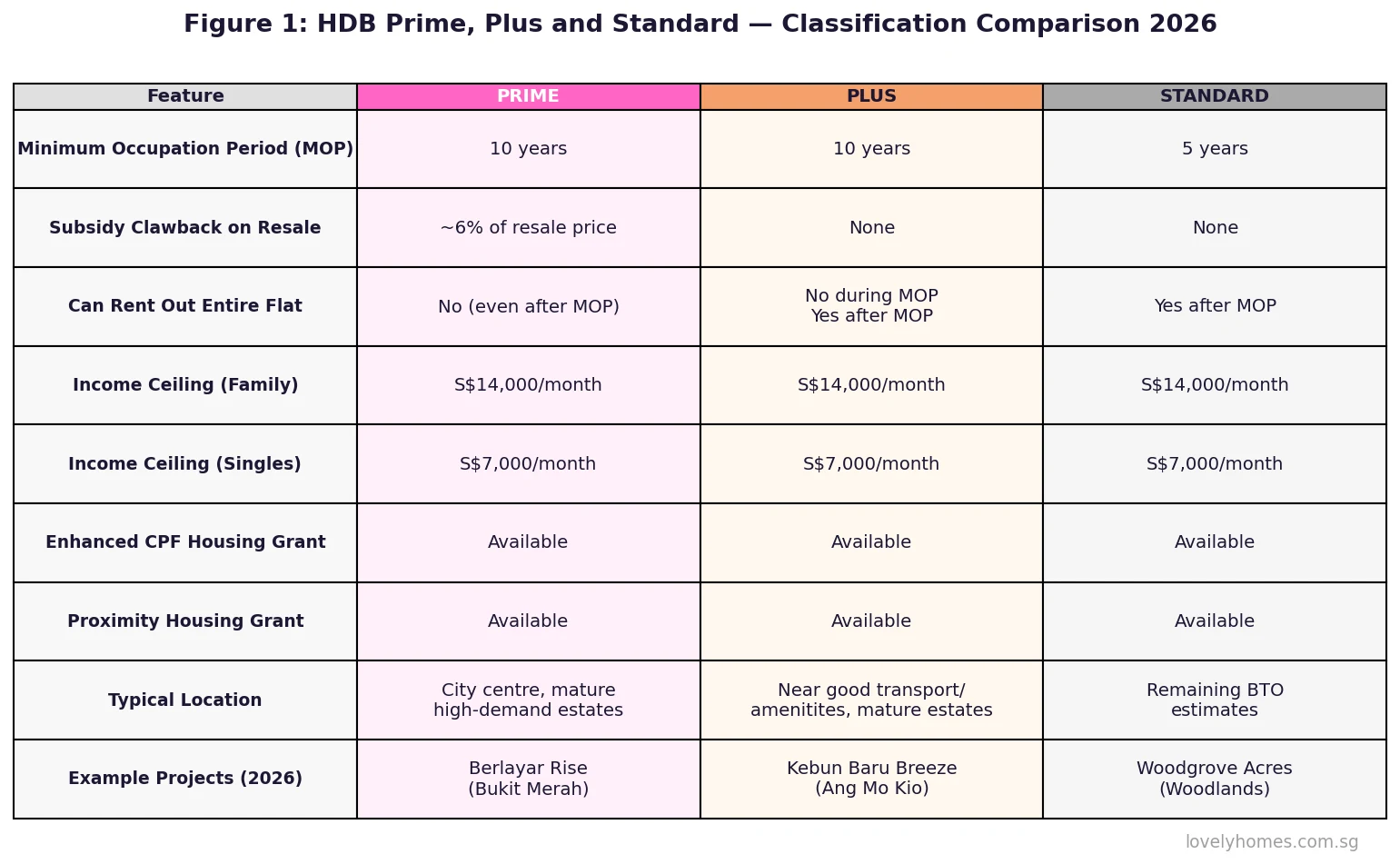

- Prime: highest-demand locations (city fringe, mature estates near MRT/amenities). 10-year MOP. Subsidy clawback of approximately 6% of resale price payable to HDB when reselling. Cannot rent out entire flat even after MOP.

- Plus: intermediate tier near good transport and amenities in mature/non-mature estates. 10-year MOP. No subsidy clawback. Cannot rent entire flat during MOP; eligible to do so after MOP.

- Standard: all other BTO flats. 5-year MOP (unchanged). No clawback. Can rent out entire flat after MOP. Same rules as before the new classification.

- Income ceiling: S$14,000/month (family) or S$7,000/month (singles) across all three tiers.

- Why it matters: buying a Prime flat commits you to a 10-year lock-in period and reduces your net proceeds on eventual resale. Model the clawback before you ballot.

Why HDB Introduced a New Flat Classification System

On 31 October 2023, the Housing & Development Board (HDB) and the Ministry of National Development (MND) announced a new classification framework for all HDB BTO flats from the August 2024 exercise onwards. The move replaced the then-two-year-old Prime Location Public Housing (PLH) model — which had been introduced in November 2021 to manage the sharp price premium commanded by BTO flats in the most sought-after city-fringe locations — with a cleaner three-tier structure: Prime, Plus, and Standard.

The rationale was equity and consistency. Under the old system, only a handful of projects in places like Rochor, Kallang, and Queenstown were designated PLH, leaving buyers of well-located “regular” BTO flats in mature estates facing few additional restrictions despite capturing significant locational subsidies. The new system extends graduated restriction to all HDB flats according to their locational advantage, creating a more systematic calibration of subsidy, restriction, and resale price.

For buyers, the practical implication is significant: choosing a Prime BTO flat in Bishan or Bukit Merah over a Standard flat in Woodlands is not just a lifestyle decision — it is a decision to accept a 10-year minimum occupation period, forgo the ability to rent out the entire flat, and repay approximately 6% of the eventual resale price to HDB as subsidy recovery. Understanding these trade-offs before balloting is essential.

The Three Tiers Explained

Figure 1: HDB Prime, Plus and Standard flats — complete classification comparison. Source: HDB, Ministry of National Development, 2026.

Prime flats occupy HDB’s most desirable locations: city fringe and high-demand mature estate zones where the locational subsidy is highest. The June 2026 BTO exercise illustrates this clearly — Berlayar Rise in Bukit Merah attracted 4.5 times more applications than units available, with 4-room units indicatively priced from S$580,000. Lakeview Cascadia in Bishan recorded a 4.7 times oversubscription rate. Both are Prime-classified.

Prime restrictions are the most restrictive in the HDB spectrum:

- 10-year Minimum Occupation Period (MOP) — you must physically occupy the flat for 10 continuous years before you can sell it on the open market or apply for another flat.

- Subsidy clawback: when you sell a Prime flat after MOP, you must return approximately 6% of the resale price to HDB. On a Prime flat reselling at S$900,000, this means a clawback of S$54,000 payable to HDB on the day of completion.

- No subletting entire flat: even after the 10-year MOP, Prime flat owners may not sublet their entire flat. You may sublet individual rooms (subject to HDB approval) but not vacate and fully lease out the property.

- Priority schemes: flat-type-specific application priority schemes (Married Child Priority, Ageing Parents Priority, etc.) still apply within the Prime tier.

Plus flats sit between Prime and Standard. They are located near good transport infrastructure (typically an MRT station within 500m) or significant amenities in mature or non-mature estates, but do not command the highest premium of Prime locations. The June 2026 BTO exercise included Kebun Baru Breeze and Kebun Baru Ridge in Ang Mo Kio as Plus-classified, with 4-room units from around S$310,000.

Plus restrictions are intermediate:

- 10-year Minimum Occupation Period (MOP) — same as Prime.

- No subsidy clawback: unlike Prime, Plus flat owners do not repay a percentage of the resale price to HDB. You keep the full net proceeds.

- Subletting during MOP: Plus flat owners cannot sublet the entire flat during the 10-year MOP period. After MOP, full subletting is permitted subject to HDB approval and standard subletting conditions.

Standard flats are all remaining BTO flats — those not classified Prime or Plus. The majority of BTO supply by volume falls into the Standard tier. In the June 2026 BTO exercise, Woodgrove Acres in Woodlands and Sembawang Portico and Sembawang Brook were Standard-classified, with some projects recording application rates below 1 times (meaning not all units were balloted for), particularly in the family segment.

- 5-year Minimum Occupation Period (MOP) — unchanged from the pre-2024 HDB norm.

- No clawback, no subletting restriction: after the 5-year MOP, owners may sublet the entire flat, sell on the open market, or use it as a base for upgrading to private property.

- Same grants available: Enhanced CPF Housing Grant (EHG), Family Grant, Proximity Housing Grant (PHG), and Step-Up Grant all apply to Standard flats at their standard quantum, subject to income and eligibility criteria.

MOP Duration and Subsidy Clawback: The Numbers That Matter

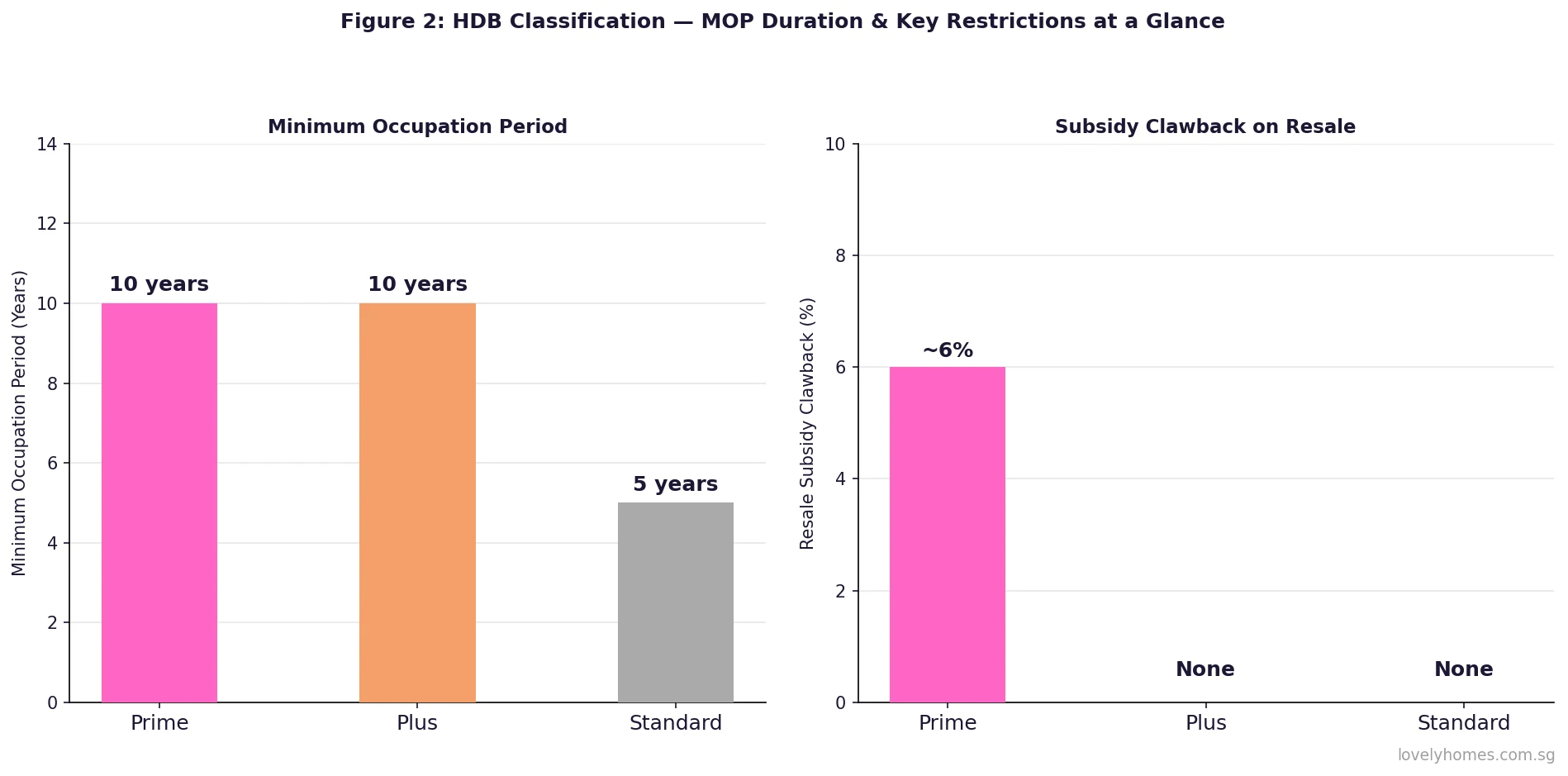

Figure 2: HDB flat tier MOP comparison (left) and subsidy clawback on resale (right). Prime and Plus share the 10-year MOP; only Prime has a resale clawback. Source: HDB, 2026.

The 10-year MOP for Prime and Plus flats is not merely a procedural inconvenience — it is a structural commitment that affects household planning. Buyers who purchase a Prime BTO at age 30 cannot legally sell their flat or purchase a second property until age 40 (assuming continuous occupation from the grant of keys, which itself typically comes 3–5 years after balloting). Add the application-to-key-collection lead time and the effective lockout from the private market can stretch to 13–15 years from the date of balloting.

The 6% clawback for Prime flats deserves careful modelling. HDB calculates the clawback on the resale price — not on the grant quantum or the original purchase price. If a Prime 4-room flat bought at S$580,000 in 2026 appreciates to S$900,000 by 2036, the clawback would be S$54,000. If it appreciates to S$1,100,000 (a scenario not unreasonable for a Prime Bishan or Bukit Merah address given historical flat appreciation in mature estates), the clawback would be S$66,000. On a nominal S$900,000–S$1.1M resale, the clawback represents 5–7% of your gross proceeds.

BTO Prices by Tier: What You Pay for Location

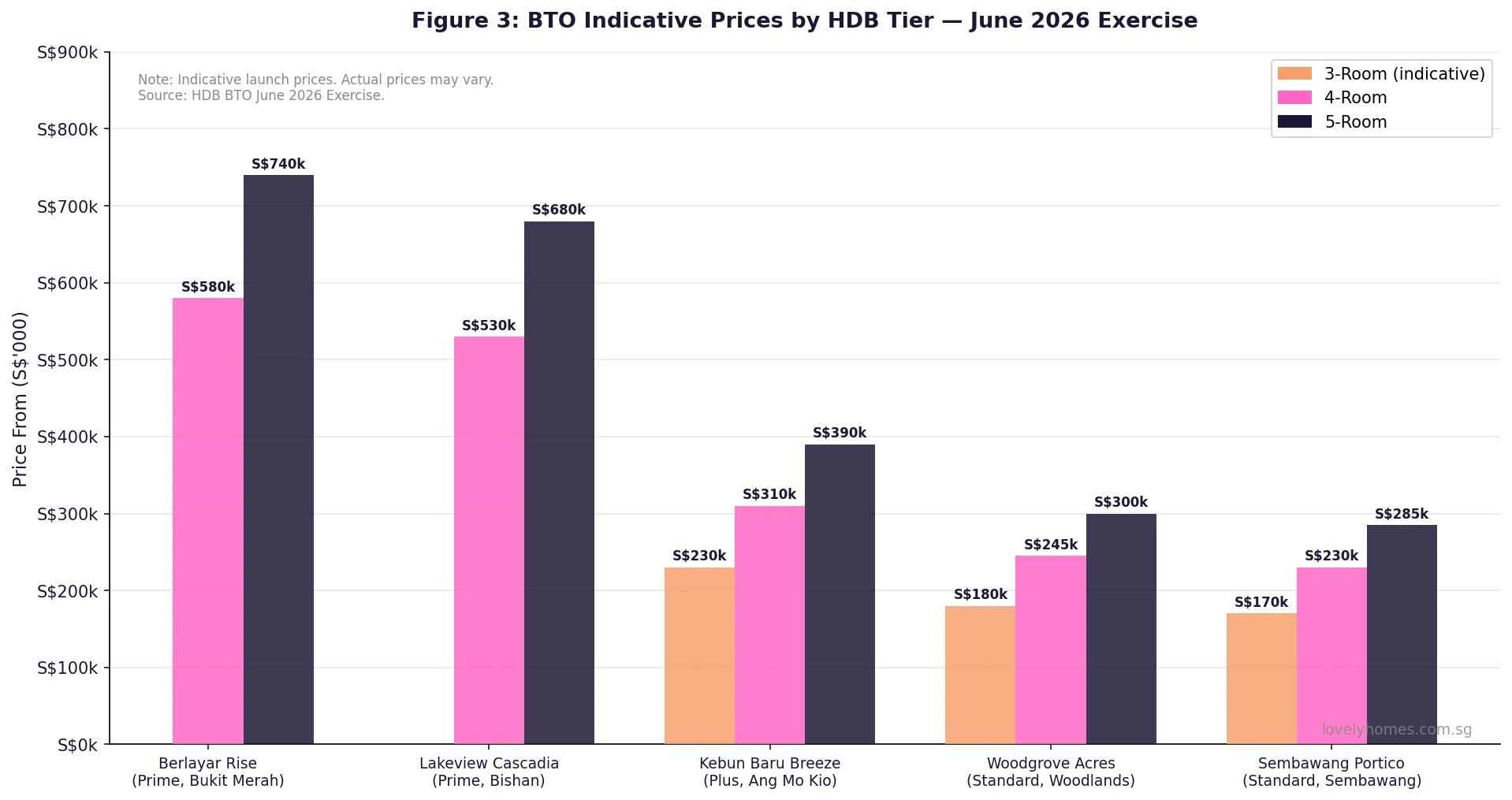

Figure 3: Indicative BTO prices by HDB classification tier — June 2026 Exercise. Note: Actual prices vary; figures are indicative launch prices published by HDB. Source: HDB, June 2026 BTO Exercise.

Figure 3 illustrates the pricing differential across the three tiers in the June 2026 BTO exercise. A Prime 4-room flat in Bukit Merah (Berlayar Rise) was priced from S$580,000 — approximately 2.4 times the entry price for a Standard 4-room flat in Woodlands (from S$245,000). The Plus-classified Kebun Baru Breeze (Ang Mo Kio) fell in between at around S$310,000 for a 4-room.

This pricing differential is HDB’s deliberate mechanism to keep BTO flats affordable relative to their locational value — the market-based price for a comparable 4-room flat near Bukit Merah on the open resale market would likely approach S$900,000–S$1.1M. The S$300,000–500,000 difference represents the “HDB subsidy” that the clawback is designed to partially recover on resale.

| Feature | Prime | Plus | Standard |

|---|---|---|---|

| MOP | 10 years | 10 years | 5 years |

| Subsidy clawback on resale | ~6% of resale price | None | None |

| Can sublet entire flat after MOP | No (rooms only) | Yes | Yes |

| Income ceiling (family) | S$14,000/month | S$14,000/month | S$14,000/month |

| Income ceiling (singles) | S$7,000/month | S$7,000/month | S$7,000/month |

| EHG available | Yes | Yes | Yes |

| Proximity Housing Grant | Yes | Yes | Yes |

| June 2026 example (4-room from) | S$580,000 (Berlayar Rise) | S$310,000 (Kebun Baru Breeze) | S$245,000 (Woodgrove Acres) |

Worked Example: Prime vs Standard — The 10-Year Financial Horizon

📋 Case Study: Lim Family (SC/SC, first-timers) — Comparing Prime in Bishan vs Standard in Woodlands

Profile: Singapore Citizens, married couple both in their late twenties, combined gross income S$9,200/month. First-timer applicants. Considering either Lakeview Cascadia (Prime, Bishan) or Woodgrove Acres (Standard, Woodlands).

Option A: Lakeview Cascadia (Prime, Bishan) — 4-room, S$530,000

- EHG (income S$9,200/mth): S$15,000 (income-tested — max EHG is S$80,000 for incomes ≤S$1,500/mth; at S$9,200/mth household, EHG quantum is approximately S$15,000)

- Family Grant: S$50,000 (resale grant — not applicable for BTO; for BTO no Family Grant, only EHG)

- Note: For BTO, the applicable grant is EHG only (up to S$80,000 based on income). Family Grant applies to resale flats.

- EHG (BTO): ~S$15,000 at household income S$9,200/mth

- Purchase price after EHG: S$515,000

- HDB loan (80% LTV): S$412,000 at 2.60% p.a., 25 years → monthly repayment S$1,872

- MSR check: S$1,872 / S$9,200 = 20.3% — PASS (must be ≤30%)

- BSD: 1% on S$180k + 2% on S$180k + 3% on S$170k = S$1,800 + S$3,600 + S$5,100 = S$10,500

- Total upfront (5% cash down = S$26,500 + BSD S$10,500 + legal ~S$3,000): ~S$40,000

- Clawback risk (Year 10 horizon): If the flat resells at S$900,000 in 2036, clawback = S$54,000 payable to HDB. Net proceeds = S$900,000 − outstanding loan − S$54,000.

- Subletting after Year 10: rooms only — cannot generate full rental income from entire flat.

Option B: Woodgrove Acres (Standard, Woodlands) — 4-room, S$245,000

- EHG: ~S$15,000 (same income, same quantum)

- Purchase price after EHG: S$230,000

- HDB loan (80% LTV): S$184,000 at 2.60% p.a., 25 years → monthly repayment S$836

- MSR check: S$836 / S$9,200 = 9.1% — PASS

- BSD: 1% on S$180k + 2% on S$65k = S$1,800 + S$1,300 = S$3,100

- Total upfront: S$12,250 + S$3,100 + S$3,000 = ~S$18,350

- After 5-year MOP: can sublet entire flat (rental income ~S$2,500–3,000/mth in Woodlands), or sell and upgrade to private property.

- No clawback on resale.

Summary: The Prime flat gives the Lim family a Bishan address with long-term capital appreciation potential — but at a significantly higher upfront cost, a 10-year lock-in, and an eventual resale clawback. The Standard flat in Woodlands is dramatically cheaper, frees up the family in 5 years, and leaves full subletting optionality intact. The right choice depends on the family’s employment location, school proximity preferences, and long-term upgrading strategy.

What This Means for You: Choosing the Right HDB Tier

The Prime/Plus/Standard framework is HDB’s attempt to give buyers a clear signal about the trade-off between locational subsidy and mobility restrictions. For first-timers who are genuinely committed to a specific estate for the long term — families with elderly parents in Bishan, or professionals working in Alexandra who want a Queenstown address — Prime may be a rational choice despite the 10-year MOP. The subsidy is real: you are buying a S$900,000–S$1M asset for S$530,000–580,000. Even after the 6% clawback on resale, the financial gain is substantial.

But for households where both spouses may change jobs, relocate, or eventually want to upgrade to private property, the 10-year MOP is a genuinely constraining commitment. Singapore’s residential property cycle historically runs in 5–8 year windows; a buyer locked into a 10-year MOP will miss at least one full upgrading cycle. Plus flats offer a middle ground — the locational premium without the clawback penalty — but still carry the 10-year MOP.

Peer-country perspective: Hong Kong’s public housing scheme has a 2-year minimum tenancy with no transferability at all for subsidised flats; purchasers must go through a buyback scheme at an administered price. By contrast, Singapore’s HDB resale market — even for Prime flats post-MOP — remains open, liquid, and market-priced (minus the 6% clawback for Prime). This market-based exit mechanism, uncommon in global public housing systems, is part of what makes Singapore’s public housing model distinctive.

What Might Come Next: HDB Classification Beyond 2026

Industry observers and housing researchers have raised two forward-looking questions about the new framework. First: will the Prime tier clawback rate be adjusted? The current ~6% was set as a rounded approximation of average subsidy quantum relative to estimated resale price at the 10-year horizon. If Prime flat prices appreciate faster than modelled (as Bishan and Bukit Merah historically have), the effective subsidy recovery at 6% understates the actual subsidy received. HDB may review this rate at its next major policy revision.

Second: could the tier boundaries shift over time? Estates classified as Plus today may, through new MRT lines or amenity upgrades, reach the threshold for Prime reclassification in a future BTO exercise. Buyers who purchased Plus flats in Ang Mo Kio or Bedok in 2024–2025 retain their Plus designation for their specific flat — reclassification does not apply retroactively to existing flat owners. But future BTO buyers in the same estate may face Prime rules if HDB upgrades the zone.

HDB has stated its intention to review the framework periodically and adjust classifications as estates evolve. The transparency of the three-tier public announcement prior to each BTO launch is designed to give buyers full information before balloting — a significant improvement over the more opaque PLH designation system it replaced.

Frequently Asked Questions: HDB Prime, Plus and Standard

Does the new classification apply to all existing HDB flats on the resale market?

No. The Prime/Plus/Standard classification applies only to BTO flats offered from the August 2024 exercise onwards. Flats on the resale market that were purchased before August 2024 retain their original designation — either as a regular HDB flat or (if purchased under the 2021–2024 PLH scheme) as a PLH flat with the associated PLH restrictions. Resale buyers should check which designation applies to the specific flat they are buying, as PLH flats carry their own clawback and subletting rules.

Can a Prime or Plus flat owner buy a second property before the MOP ends?

No. HDB flat owners — regardless of tier — cannot own any other residential property (including private property, DBSS, or EC) while still within the MOP period. Purchasing a second residential property before the MOP ends is a breach of HDB ownership rules, subject to compulsory acquisition of the flat by HDB. This 10-year lock-out effectively prevents Prime and Plus flat buyers from participating in the private property market until a decade after receiving their keys — which may be 13–15 years after the ballot date.

What happens if I need to sell my Prime flat before the 10-year MOP?

You cannot sell a Prime or Plus flat on the open resale market during the 10-year MOP. The only options are: (1) returning the flat to HDB (at HDB’s valuation, which may be below open-market value); or (2) demonstrating to HDB a qualifying exceptional circumstance (e.g. divorce, financial hardship) for which HDB may grant a waiver on a case-by-case basis. Buyers facing genuine hardship may apply through HDB’s appeals process, but approvals are discretionary and not guaranteed. This is why financial stress-testing before balloting is so important.

Are CPF housing grants different for Prime, Plus and Standard flats?

The types of grants available — Enhanced CPF Housing Grant (EHG), Proximity Housing Grant (PHG), and (for resale flats) the Family Grant — are the same across all three tiers. The EHG quantum depends on your household income, not the flat’s tier: it ranges from S$5,000 (at household income S$9,001–S$9,500/month for families) up to S$80,000 (at household income ≤S$1,500/month). Singles applying for a 2-room Flexi BTO may receive EHG up to S$40,000. The tier does not affect grant eligibility, only the MOP, clawback, and subletting rules.

If I ballot for a Plus flat in 2026 and my estate gets reclassified to Prime in 2030, do I lose my Plus status?

No. Your flat’s classification is locked in at the time of the BTO exercise in which you balloted. If you successfully ballot for a Plus flat in Ang Mo Kio in 2026 and HDB reclassifies that zone as Prime for future BTO launches in 2030, your flat retains Plus-tier restrictions — not Prime. The 6% clawback would not apply to you. However, new BTO buyers in the same estate from 2030 onwards would face Prime rules. This distinction is important when modelling resale value: your Plus flat in a subsequently-Prime-zoned estate may attract buyers willing to pay a premium for the same locational advantage without the clawback cost.

Can I rent out rooms in my Prime flat during the MOP?

Yes, subject to HDB approval. Prime flat owners may sublet individual rooms (not the entire flat) during the MOP, provided they continue to occupy the flat themselves. You must apply to HDB for room subletting approval, meet the eligibility criteria (Singapore Citizen or Permanent Resident owner), and comply with occupancy cap rules (maximum number of tenants based on flat type). Room rental in Bishan, Bukit Merah, and Kallang in mid-2026 ranges from S$900–S$1,800/month per room depending on location and furnishing, providing partial rental income during the 10-year MOP.

Is there any way to avoid the Prime clawback on resale?

No. The approximately 6% clawback is a mandatory condition attached to all Prime flats from the date of purchase. It cannot be waived, negotiated, or avoided through any transaction structure. The clawback is calculated on the resale price at the time of the sale — not on a fixed nominal amount — and is payable to HDB at completion. Sellers must factor this into their net proceeds calculation before listing. There is no mechanism to “pay off” the clawback obligation early; it only crystallises (and extinguishes) upon the resale transaction.