First-Time Property Buyer Guide Singapore 2026: HDB, EC and Condo — Every Step, Cost and Grant Explained

- Singapore Citizens buying their first property pay zero ABSD on the purchase

- HDB BTO is the most affordable entry point — balloted flats from ~S$180k (non-mature, 2-room Flexi) with Enhanced Housing Grant (EHG) up to S$80,000

- For private condos: minimum 5% cash downpayment + 20% CPF (or cash); TDSR limit = 55% of gross monthly income

- HDB resale: Proximity Housing Grant (PHG) adds S$10k–S$30k for buying near parents/children

- Executive Condominiums (EC): income ceiling S$16,000/month; bank loan only; 5-year MOP; privatises after 10 years

- BSD (Buyer’s Stamp Duty) is payable by all buyers regardless of citizenship — progressive 1–6% on purchase price

- CPF Ordinary Account (OA) can fund downpayment and monthly instalments — up to the Valuation Limit (VL)

- HDB Loan (2.6% p.a.) vs Bank Loan: bank rates lower short-term but variable; HDB offers security and HLE letter approval process

- First-timers have priority balloting at HDB BTO: 95% of flat supply reserved for first-timers (85% for mature estates)

Why First-Time Buyers Have a Significant Advantage in Singapore

Singapore’s public housing framework is deliberately designed to give first-time buyers a material advantage over repeat purchasers. This advantage operates through four channels: zero ABSD on the first residential property for Singapore Citizens (SCs) and a reduced 5% rate for Singapore Permanent Residents (SPRs); substantial cash grants (up to S$80,000 for HDB flat buyers); priority ballot access to subsidised Build-To-Order (BTO) flats; and the ability to deploy CPF Ordinary Account (OA) savings towards both the downpayment and monthly mortgage instalments.

The result is that a married couple of SCs purchasing their first HDB flat at S$550,000 will pay less than S$1,000 in net upfront cash once grants and CPF savings are applied — one of the most government-supported entry pathways to home ownership in the world. This guide, organised by the three main property pathways — HDB flat, Executive Condominium (EC), and private condo — walks through every cost, rule, and decision point a first-time buyer in Singapore needs to know in 2026.

Pathway 1: HDB BTO and Resale Flats

Who Qualifies?

To buy an HDB flat (new BTO or resale), you must satisfy the Public Scheme or one of five other eligibility schemes administered by HDB. The most common for first-timers is the Public Scheme, which requires: at least one Singapore Citizen applicant, plus a Singapore Citizen or Permanent Resident co-applicant (or a single SC aged 35+), and no existing HDB flat or private property ownership (or interest). You must not have previously disposed of an HDB flat.

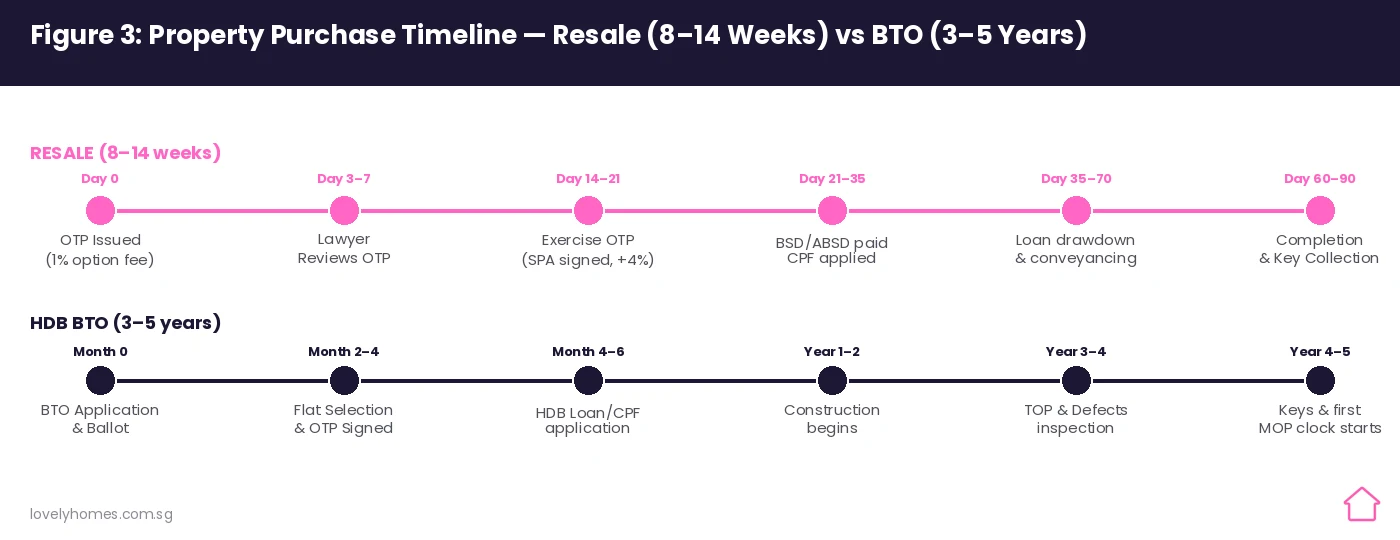

BTO versus Resale

A BTO (Build-To-Order) flat is purchased directly from HDB at a government-subsidised price, but involves a 3–5 year construction wait. A resale flat is purchased from an existing owner in the open market and is ready for immediate occupation, but carries a higher market price. For most first-timers, BTO is considerably more affordable; resale is preferred when location, flat maturity, or timeline constraints make the wait impractical.

HDB Grants Available to First-Timers in 2026

Singapore’s CPF Board and HDB administer three principal grants for HDB flat buyers:

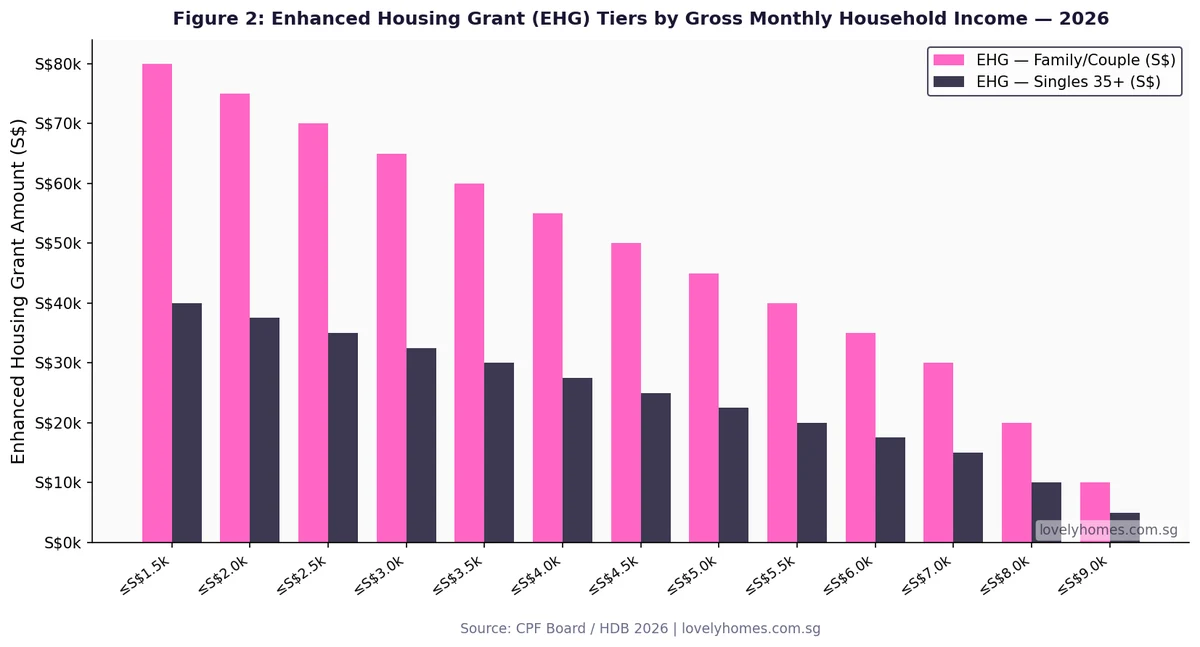

- Enhanced Housing Grant (EHG): Up to S$80,000 for families and S$40,000 for singles (35+). Granted on a sliding scale based on average gross monthly household income (GMHI), with the full S$80,000 available to families earning up to S$1,500/month. EHG applies to both BTO and resale purchases.

- Proximity Housing Grant (PHG): S$30,000 (living with parents/children) or S$20,000 (living within 4km) for buying a resale flat near family members. An additional S$10,000 for singles. PHG is only for resale flats.

- Step-Up Housing Grant: S$15,000 for second-timers from 2-room Flexi flats upgrading to 3-room flats — applies to a specific subset of buyers, not typical first-timers.

HDB Loan vs Bank Loan

First-time HDB buyers may choose between an HDB Concessionary Loan (2.6% p.a., pegged to CPF OA rate + 0.1%) and a commercial bank loan (fixed from ~3.0% p.a. or SORA-based floating). The HDB loan requires a minimum 10% downpayment (all CPF allowed); a bank loan requires 5% cash + 20% total downpayment. The HDB vs bank loan comparison guide shows that bank loans save approximately S$92,000 in total interest over 25 years on a S$500k loan — but carry repricing risk if interest rates rise. First-timers must obtain an HDB Flat Eligibility (HFE) letter before exercising any OTP, confirming their loan eligibility and grant quantum.

Pathway 2: Executive Condominiums (ECs)

Executive Condominiums are a uniquely Singaporean housing type that straddles the HDB-private divide. Built by private developers on government land, ECs are sold at a discount to comparable private condominiums (~10–15% discount), with HDB oversight during the 5-year MOP and 10-year privatisation period. After privatisation, EC owners enjoy the same rights as private property owners and may sell to foreigners.

EC Eligibility in 2026

- Gross monthly household income ceiling: S$16,000

- At least one SC applicant; at least one more SC or SPR

- Cannot own or have disposed of a private property in the 30 months before application

- Must not have previously purchased a subsidised flat or EC as a first-timer (with exceptions)

- EC buyers must take a bank loan (no HDB Concessionary Loan); MSR applies (30% of gross monthly income)

- From 8 May 2026: DPS (Deferred Payment Scheme) abolished for ECs; rental restriction extended to 10 years post-TOP; privatisation milestone extended to 15 years from TOP; 90% of units reserved for first-timers

EC Grants Available

- AHG (Additional Housing Grant): Up to S$30,000 for families with GMHI ≤ S$10,000

- FHG (Family Housing Grant): S$10,000 for families; available on top of AHG

Pathway 3: Private Condominiums

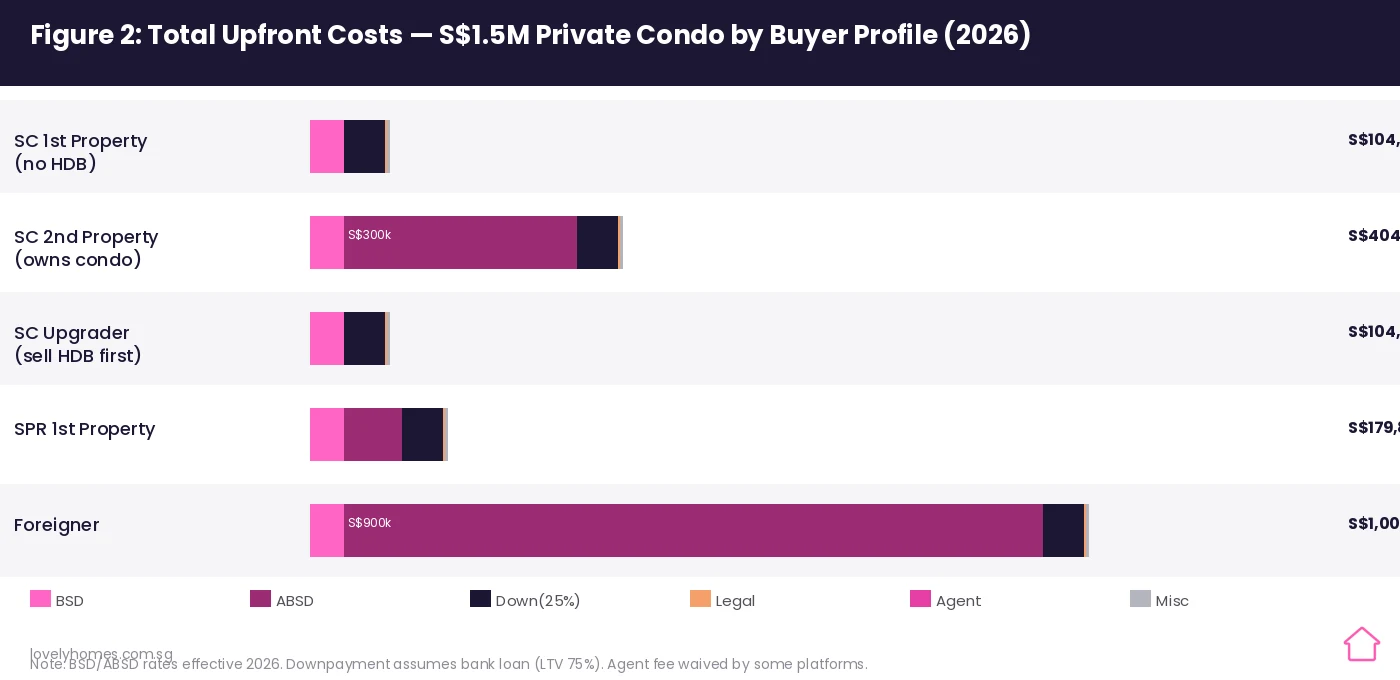

SCs buying a private condo as their first and only property pay zero ABSD — but BSD still applies. For a S$1.3M OCR condo, BSD is S$37,400. The minimum downpayment for a bank loan (LTV 75%) is 5% cash (S$65,000) + 20% CPF or cash (S$260,000) = S$325,000, assuming the buyer has enough CPF savings. The Total Debt Servicing Ratio (TDSR) of 55% applies; for a S$1.3M purchase with a S$975,000 loan at 3.0% over 25 years, the monthly instalment is approximately S$4,627, requiring a minimum gross household income of ~S$8,413/month to satisfy TDSR.

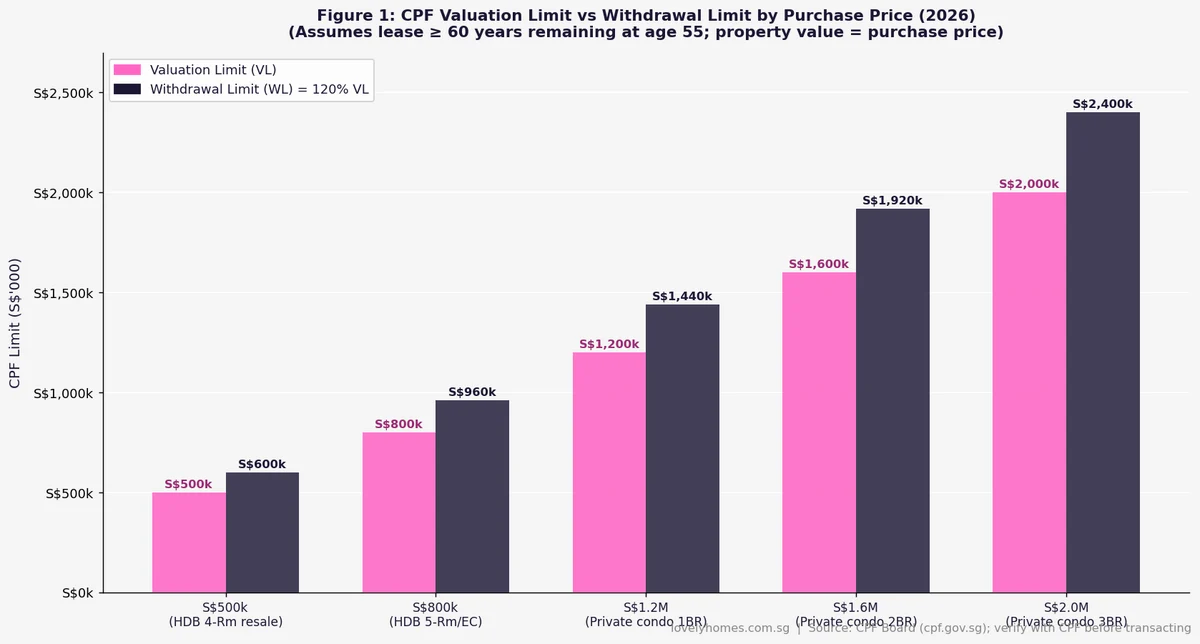

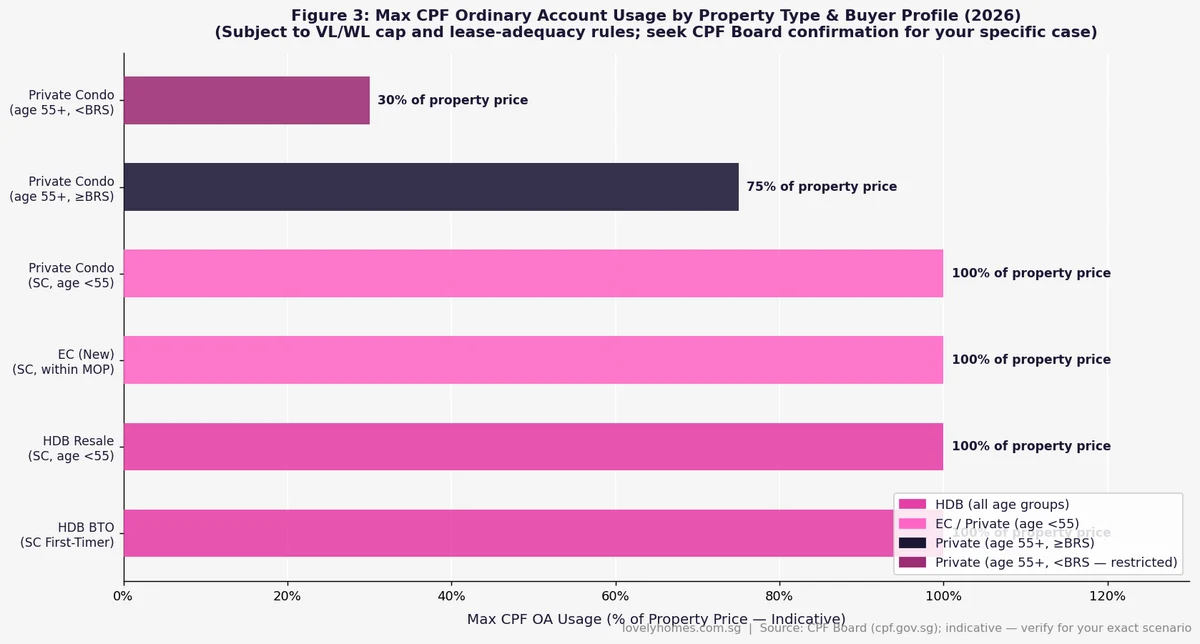

CPF Usage for Private Property

CPF OA savings may be used for the downpayment and monthly instalments of a private property, up to the Valuation Limit (VL) — equal to the lower of purchase price or market valuation. Once CPF usage reaches VL, further CPF withdrawals require the flat’s remaining lease to cover the buyer to age 95, and are capped at the Withdrawal Limit (WL) of 120% of VL. For buyers aged under 55 purchasing a property with a 99-year lease, the VL and WL constraints are typically non-binding at normal private condo price levels.

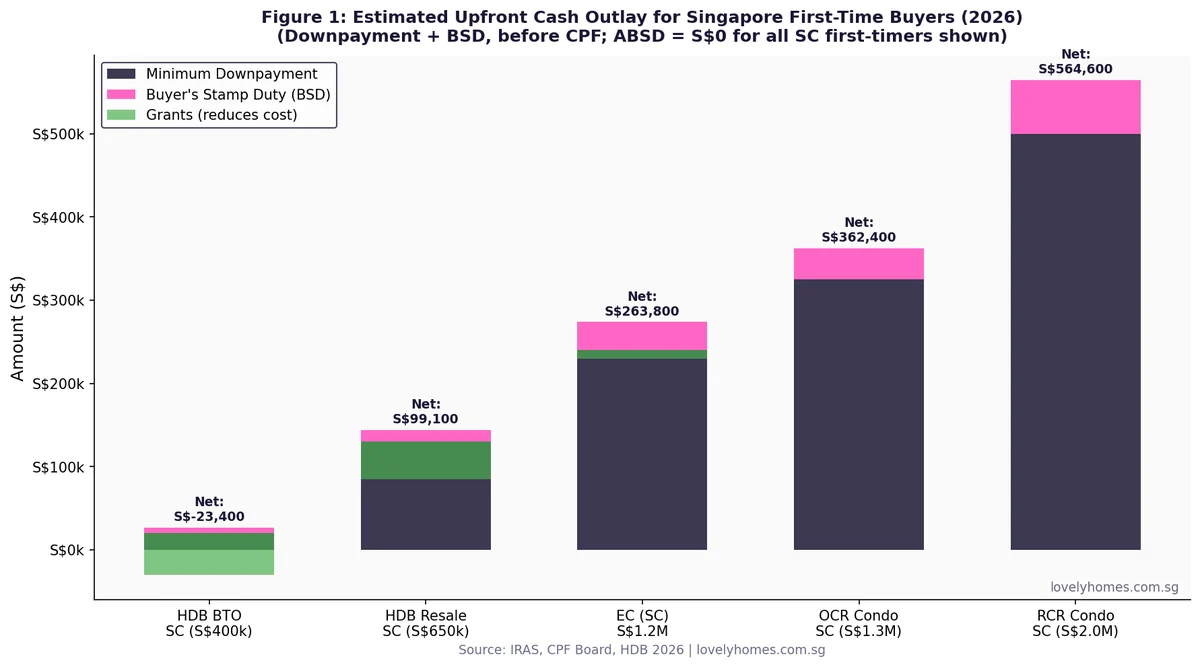

Upfront Cost Comparison: HDB vs EC vs Private Condo

| Parameter | HDB BTO (S$400k) | EC (S$1.2M) | OCR Condo (S$1.3M) |

|---|---|---|---|

| BSD | S$6,600 | S$33,800 | S$37,400 |

| ABSD (SC 1st purchase) | Nil | Nil | Nil |

| Min. downpayment | 10% (all CPF ok) | 5% cash + 20% CPF | 5% cash + 20% CPF |

| Min. cash downpayment | S$0 (if CPF sufficient) | S$60,000 | S$65,000 |

| Grants available | EHG up to S$80k | AHG+FHG up to S$40k | None |

| Loan type | HDB 2.6% or bank | Bank loan only | Bank loan only |

| Income test | MSR 30% | MSR 30%; ceiling S$16k | TDSR 55% |

| MOP / Restriction | 5-year MOP | 5-year MOP; 15-yr privatisation | None |

| Can buy jointly with SPR? | Yes | Yes | Yes |

Worked Example: Mr & Mrs Tan’s First Home

Mr Tan (SC, 31) and Mrs Tan (SC, 29) are newly married, renting a room in Queenstown. Mr Tan earns S$5,800/month; Mrs Tan earns S$4,200/month — combined gross S$10,000/month. They have S$80,000 in combined CPF OA savings and S$35,000 in cash savings.

Option A: HDB Resale 4-room, Bishan — S$720,000

- EHG: S$35,000 (income S$10k → upper tier; max S$35k)

- PHG: S$0 (not buying near parents in same town)

- BSD: S$16,800 (progressive on S$720k)

- ABSD: Nil (SC first property)

- HDB loan (80% LTV): S$576,000 at 2.6% p.a., 25yr = S$2,607/month — MSR 26.1% ✓

- Downpayment 20%: S$144,000 (paid: S$80,000 CPF OA + S$64,000 cash)

- BSD paid via CPF OA: S$16,800

- Less EHG offset to CPF: −S$35,000

- Net cash outlay: S$64,000 − S$35,000 (grant to CPF) ≈ S$29,000 cash

- Monthly payment (CPF OA deduction): S$2,607 — fully funded by CPF contributions (~S$2,700/month combined for salaries S$10k)

Option B: OCR Condo 2BR, Tampines — S$1,300,000

- BSD: S$37,400

- ABSD: Nil (SC first property)

- Bank loan (75% LTV): S$975,000 at 3.0% p.a., 25yr = S$4,627/month — TDSR 46.3% ✓

- Downpayment: 5% cash (S$65,000) + 20% CPF/cash (S$195,000) = S$260,000 total; but CPF OA only S$80,000 → cash shortfall of S$115,000

- Shortfall vs available savings: S$65,000 + S$115,000 − S$35,000 cash available = S$145,000 cash required vs S$35,000 available

- Verdict: Not feasible at current savings. Mr & Mrs Tan should buy the HDB resale first, build equity over 5 years, and upgrade to a private condo once CPF and capital appreciation allow.

This is a textbook application of Singapore’s HDB-first, upgrade-later strategy — the single most common path for Singaporean households to accumulate property wealth over their lifetime.

Why the First-Timer Advantage Matters for Long-Term Wealth

Singapore’s property framework rewards patience and sequential upgrading. The first-timer’s zero ABSD status — worth S$0 now but S$260,000 on a S$2M purchase if purchasing a second property — is a one-time use entitlement. Preserving it by making the right first purchase is critical. A first-timer who buys a S$650,000 resale HDB flat at age 28 and sells at age 33 (MOP completed) can potentially walk away with S$150,000–S$200,000 in equity and CPF proceeds, enough to fund the downpayment on an OCR condo — all without ever having paid a cent of ABSD. This sequential pathway is not available to foreigners (65% ABSD from purchase 1) or even to SPRs (5% ABSD on first purchase).

What Might Change for First-Time Buyers in 2026 and Beyond

The HDB June 2026 BTO exercise — covering approximately 6,900 flats across Ang Mo Kio, Bishan, Bukit Merah, Sembawang, and Woodlands — is expected to release ballot results in late June or early July 2026. Successful applicants in mature estates (Bishan, Bukit Merah) will benefit from the 85% first-timer priority allocation. The HDB’s ongoing review of the Prime Location Public Housing (PLH) classification boundaries — particularly as the definition of what constitutes a “prime” location has attracted debate — may affect grant eligibility and resale restrictions for upcoming BTO exercises. First-timers considering a BTO application in 2026–2027 should watch MND announcements closely.

Frequently Asked Questions

Do I pay ABSD as a Singapore Citizen buying my first property?

No. Singapore Citizens purchasing their first residential property are fully exempt from Additional Buyer’s Stamp Duty (ABSD) — effective 27 April 2023 and ongoing. You will still pay Buyer’s Stamp Duty (BSD) at the standard progressive rates (1–6% of purchase price). The BSD is unavoidable for all buyers regardless of citizenship. ABSD at 20% kicks in only from the second property for SCs; the rate rises to 30% for a third and subsequent property. SPRs pay 5% ABSD even on their first property.

How much CPF can I use to buy a flat or condo?

You may use CPF Ordinary Account (OA) savings for both the downpayment and monthly mortgage instalments, up to the property’s Valuation Limit (VL) — which is the lower of the purchase price and the property’s market valuation. Once your total CPF withdrawals reach VL, further CPF usage is subject to the property’s remaining lease covering you to age 95. In practice, for most buyers under 45 purchasing 99-year-leasehold properties, the VL cap is non-binding until the CPF balance is exhausted. An upper Withdrawal Limit (WL) of 120% of VL applies as an absolute ceiling. Check your CPF OA balance and projected contributions at cpf.gov.sg.

Can a single Singapore Citizen buy an HDB flat alone?

Yes — a single Singapore Citizen aged 35 or above may buy an HDB flat (resale) or apply for a BTO flat (2-room Flexi units in non-mature estates or Prime/Plus locations via the Single Singapore Citizen (SSC) scheme). Singles below 35 cannot buy an HDB flat on their own. Singles purchasing HDB flats are eligible for the EHG at half the family quantum (up to S$40,000) and may qualify for PHG of S$10,000 for buying near parents. Private condominiums and ECs have no age or single/married restrictions — a single SC of any age may purchase a private property with zero ABSD.

What is the Minimum Occupation Period (MOP) and why does it matter?

The MOP is the minimum period a HDB flat or EC buyer must physically occupy the property before selling it in the open market or buying another HDB flat. For standard HDB flats, the MOP is 5 years from the date of key collection. For Plus and Prime Location Public Housing (PLH) flats — introduced under the new HDB classification framework effective October 2023 — the MOP is 10 years. For ECs (from the 8 May 2026 cooling measures), the MOP remains 5 years but privatisation is extended to 15 years from TOP. The MOP prevents short-term speculation and ensures that subsidised housing goes to genuine owner-occupiers. An owner who violates MOP conditions (e.g., by subletting the entire flat before MOP completion) risks compulsory acquisition of the flat by HDB.

What is the TDSR and how does it affect my borrowing capacity?

The Total Debt Servicing Ratio (TDSR) is a MAS-mandated framework limiting total monthly debt obligations to 55% of the borrower’s gross monthly income. It applies to all loans secured on private residential properties. For HDB flats, the Mortgage Servicing Ratio (MSR) applies instead, capping the home-loan instalment (only) at 30% of gross monthly income. TDSR includes all existing loan obligations — car loans, personal loans, credit card minimum payments — not just the property mortgage. For example, a couple earning S$12,000/month combined with a S$500/month car loan payment has a remaining TDSR capacity of S$6,100/month (55% × S$12,000 − S$500), which at 3.0% p.a. over 25 years translates to a maximum loan of approximately S$1,285,000.

Should I buy HDB first and upgrade, or go straight to a private condo?

For most Singaporean households, buying HDB first and upgrading later is the mathematically superior strategy — but it depends on your income, savings, and goals. The HDB route gives you access to grants (up to S$80,000 EHG), a subsidised purchase price, and the CPF usage advantage. After the 5-year MOP, you can sell the HDB flat and use the proceeds plus CPF accrued value to fund the downpayment on a private condo — still with zero ABSD (as it is your first private property purchase). The alternative — buying a private condo directly at age 25–30 — requires substantially more upfront cash and eliminates access to HDB grants entirely. However, if you have the savings and income, a direct private condo purchase avoids the 5-year illiquidity of HDB ownership and offers better rental income flexibility from day one. A worked comparison for upgraders is available on LovelyHomes.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Complete Guide 2026: BSD, ABSD, SSD and ACD Explained

- HDB Loan vs Bank Loan Singapore 2026: Complete Comparison Guide

- CPF Housing Grant for Resale Singapore 2026: Complete Guide to EHG, PHG and Step-Up Grant

- Condo vs HDB Singapore 2026: The Upgrader’s Complete Decision Framework

- Singapore Property Buying Checklist 2026: 12 Steps from IPA to Key Collection

- Singapore Property Rental Guide 2026: Renting, Landlord Rules and Market Rates Explained

Disclaimer: The information in this guide is for general educational purposes only and does not constitute legal, tax, or financial advice. Property grant eligibility, loan limits, ABSD rates, and HDB policies change regularly. Always verify current rules at the official government portals — hdb.gov.sg, cpf.gov.sg, iras.gov.sg, and mas.gov.sg — and consult a licensed property agent or conveyancing solicitor before signing any Option to Purchase. LovelyHomes is an independent editorial platform and is not affiliated with any property agency.

Click anywhere outside to close