Buying Property Near Top Schools in Singapore 2026: Complete Guide

📌 Quick Answer: Buying Property Near Top Schools in Singapore 2026

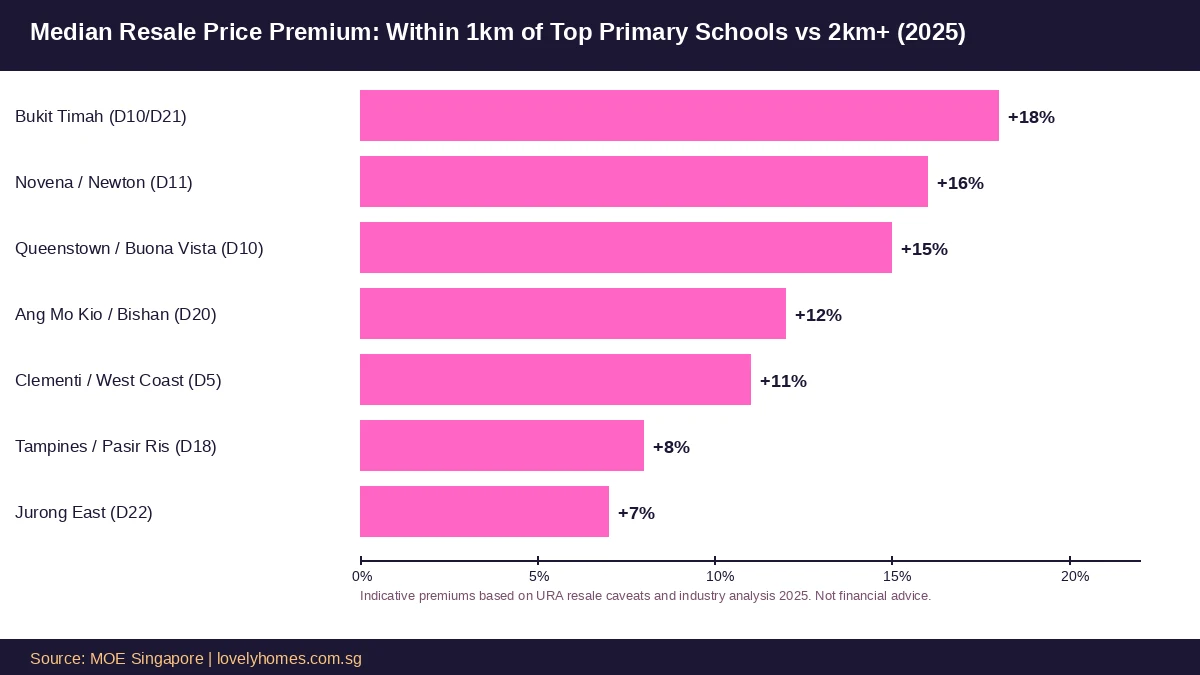

- School proximity drives property premiums: homes within 1 km of an oversubscribed primary school can command 8–18% higher prices than comparable homes 2 km away, depending on the district.

- MOE’s Phase 2C priority gives Singapore Citizens living within 1 km of a school priority registration places before those living within 2 km — making the 1 km radius the most prized zone.

- Bukit Timah, Novena, and Queenstown carry the largest school-proximity premiums; Jurong and Tampines carry the smallest, though still meaningful.

- Not all popular schools are equally scarce: a school oversubscribed at Phase 2C is the one that matters for the proximity premium. Schools that regularly have vacancies at Phase 2C generate no meaningful price premium.

- HDB resale flats near top schools are significantly cheaper entry points than condos and still qualify for Phase 2C priority as long as your registered address is within the distance cut-off.

- The premium is time-limited: once your child has secured a place, the school-proximity rationale diminishes and you may be able to upsize or relocate without premium pricing.

- Distance is measured straight-line from the main gate of the property to the school’s main gate using MOE’s official measurement tool — not Google Maps driving distance.

- Verify distance before transacting: even 50 metres can determine whether you fall inside or outside the 1 km cutoff, so always use the MOE School Finder to confirm.

Why School Proximity Matters in Singapore Property

Singapore’s Primary 1 (P1) registration system is one of the most consequential drivers of residential property demand in the country. Unlike many education systems where school admission is determined purely by merit or choice, Singapore’s Phase 2C priority system gives automatic preference to children living closest to a school when balloting places are contested. This policy — administered by the Ministry of Education (MOE) — has created a predictable and enduring link between residential addresses and primary school access, making the 1 km radius around any oversubscribed primary school one of the most reliably valued assets in the Singapore property market.

For parents weighing their next property purchase, understanding how the P1 registration phases work, which schools generate meaningful premiums, and how to quantify the value of proximity is not a luxury — it is a core part of the buying decision. For investors who do not have school-going children, the same proximity premium represents a defensible demand floor that tends to support property values even through softer markets.

This guide explains the MOE priority phase system in full, maps the districts and schools that generate the largest premiums, provides a worked example of the financial implications, and offers a framework for deciding whether the school-proximity premium is worth paying for your specific situation.

MOE Primary 1 Registration Phases — How Proximity Works

The P1 registration exercise is structured in phases that proceed in order of priority. A school only opens to later phases if vacancies remain after earlier phases are filled. The relevant phases for proximity are Phase 2B and Phase 2C.

Phase 2B gives priority to children whose parents are active volunteers at the school (40 hours per year for at least the preceding year), who have community or CCA connections to the school, or whose parents are of the relevant religious affiliation for mission schools. Within Phase 2B, if there are more applicants than places, children living within 2 km of the school are given priority over those living further away. Distance matters even here.

Phase 2C is the general registration phase for all Singapore Citizens. This is where proximity becomes most critical. If the number of Phase 2C applicants exceeds the remaining vacancies, MOE ballots first among children living within 1 km of the school, then — if vacancies remain — among those living within 2 km, and finally — if still not full — among those living further away. For the most oversubscribed schools, the ballot has historically been decided entirely within the 1 km tier, meaning that a family living at 1.1 km may receive no priority whatsoever.

Phase 2C Supplementary covers Singapore Permanent Residents after all Singapore Citizen applicants have been processed. Phase 3 covers non-PR foreigners and is only relevant if the school still has vacancies after all citizen and PR phases are complete — an unusual scenario for popular schools.

Which Schools Generate the Largest Property Premiums?

Not every primary school generates a proximity premium. The premium is driven by two factors working together: the school’s perceived academic and co-curricular reputation, and its level of oversubscription at Phase 2C. A school that clears all its places by Phase 1 or Phase 2A1 (alumni parents’ children) before Phase 2C is even reached is effectively inaccessible via proximity alone — distance does not help if the school fills up before the distance-based phases. Conversely, a school with consistent Phase 2C balloting in the 1 km zone generates a hard, measurable demand for nearby addresses.

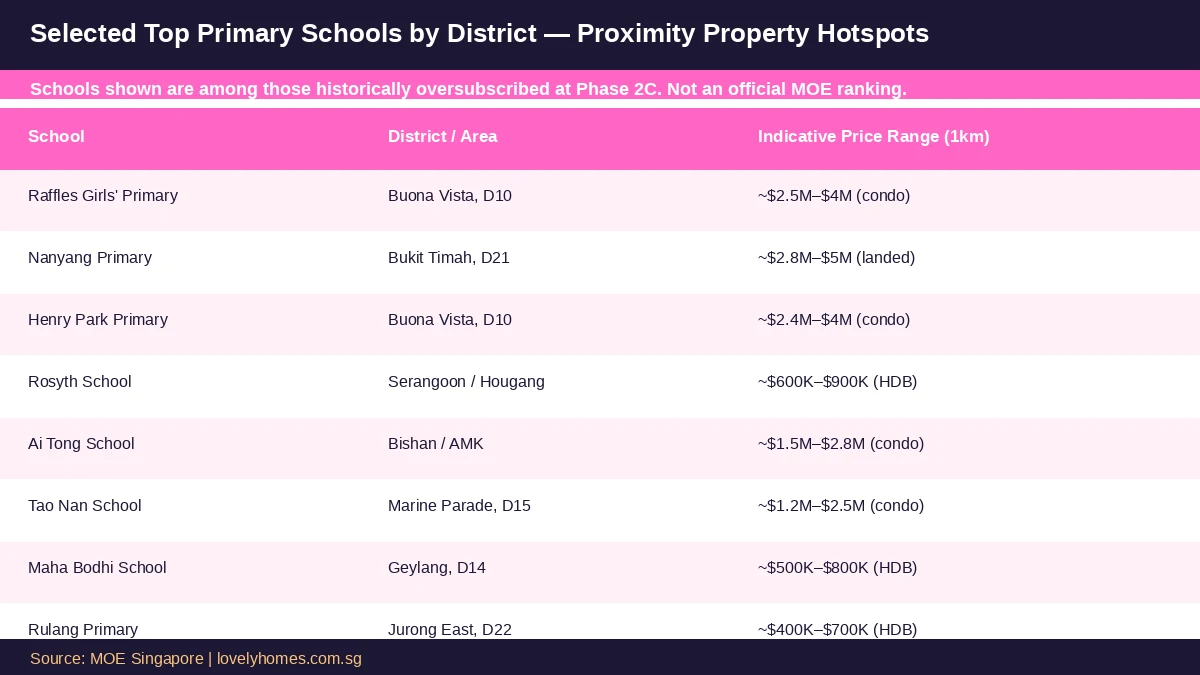

The schools that have historically generated the most sustained proximity premiums — based on their consistent oversubscription at Phase 2C and their reputation — cluster in the following districts: Bukit Timah (District 21), Novena and Newton (District 11), Queenstown and Buona Vista (District 10), Bishan and Ang Mo Kio (District 20), and Marine Parade (District 15). These areas also happen to be among Singapore’s most expensive residential districts for reasons beyond schools alone, which makes it challenging to isolate the school premium precisely.

Key Districts and Their School-Proximity Premium Characteristics

| District | Notable Schools | Typical Premium (1km vs 2km+) | Property Type |

|---|---|---|---|

| Bukit Timah (D21) | Nanyang Primary, Methodist Girls’ Primary | 15–20% | Landed, high-end condo |

| Novena / Newton (D11) | Anglo-Chinese School (Primary), Saint Joseph’s Institution Junior | 14–18% | Condo, terrace |

| Queenstown / Buona Vista (D10) | Raffles Girls’ Primary, Henry Park Primary | 13–17% | Condo, HDB (older) |

| Bishan / Ang Mo Kio (D20) | Ai Tong School, Catholic High Primary, Pei Hwa Presbyterian | 10–14% | Condo, HDB |

| Marine Parade (D15) | Tao Nan School, CHIJ Katong Primary | 10–13% | Condo, shophouse |

| Clementi / West Coast (D5) | Nan Hua Primary, Clementi Primary | 9–13% | HDB, condo |

| Tampines / Pasir Ris (D18) | Poi Ching School, Elias Park Primary | 7–10% | HDB, EC |

| Jurong East (D22) | Rulang Primary, Fuhua Primary | 6–9% | HDB, EC |

Worked Example: The Tan Family’s School-Proximity Purchase

🏫 Scenario: Tan Family, Child Entering P1 in 2028

Target school: Ai Tong School, Bishan (historically oversubscribed at Phase 2C within 1 km)

Budget: S$1.8 million for a condominium

Without school premium: A comparable 3-bedroom condo 2.5 km from Ai Tong in Ang Mo Kio averages S$1.55 million in 2025 resale.

With school premium: A comparable 3-bedroom condo within 1 km of Ai Tong averages S$1.78 million — a premium of approximately S$230,000 (14.8%).

- The Tans have a child born in 2021, meaning P1 registration is in 2027 (for entry in January 2028).

- They need to be registered at the address before the Phase 2C registration exercise, which typically opens in July 2027 and requires the address to be active at least 30 months before the exercise for Phase 2B purposes.

- Break-even analysis: The S$230,000 premium represents approximately S$19,200 per year over a 12-year horizon (primary through secondary school). If the school-proximity effect sustains the property’s relative value through resale, the net cost may be substantially less — or even zero if the 1 km zone appreciates faster than the 2.5 km zone.

- ABSD: As Singapore Citizens buying a second property, the Tans pay 20% ABSD on S$1.78 million = S$356,000. If this is their first property, no ABSD applies.

Is the School-Proximity Premium Worth Paying?

The answer depends on three variables: the school in question, the phase at which you expect to compete, and your time horizon. If you are a Phase 2B volunteer parent, you may already enjoy priority within 2 km — paying the 1 km premium may not be necessary. If you have no Phase 2B connection and the school is consistently balloted within the 1 km zone at Phase 2C, then the 1 km address is effectively a prerequisite for reasonable access, and the premium reflects a real, functional benefit rather than pure sentiment.

From a resale perspective, the proximity premium tends to be self-reinforcing in areas with good overall fundamentals (MRT access, amenities, estate quality). It is weakest in areas where the school is the sole driver of demand — in those cases, the premium may erode once your child has completed primary school and you decide to sell. The strongest investment case is therefore found where school proximity overlaps with strong general demand: Bukit Timah, Queenstown, and Bishan all fit this profile.

First-time buyers and HDB upgraders should note that HDB resale flats in the 1 km catchment area of oversubscribed schools can represent excellent value. A 4-room HDB flat in Bishan within 1 km of Ai Tong or Catholic High Primary typically transacts at S$700,000–S$900,000 in 2025 — a fraction of the condo price while qualifying for exactly the same Phase 2C priority. The trade-off is flat size, lease remaining, and the absence of condominium facilities.

What Investors Should Know About the School-Proximity Premium

For property investors without school-going children, the school-proximity premium is a demand-side floor to understand rather than a purchasing criterion. The premium is most durable in schools that are oversubscribed consistently year after year, such as those on the MOE’s School Information Service with Phase 2C balloting records visible at MOE’s P1 registration results page. Schools that recently became popular due to merger or re-branding may not sustain the same premium. URA’s transaction data, accessible at ura.gov.sg, allows investors to overlay resale transaction prices against school catchment boundaries to quantify the premium empirically for any school they are considering.

One structural risk to the school-proximity premium is MOE policy change. In 2019, MOE capped the number of children who can benefit from Phase 2B volunteerism, and has periodically adjusted how distance tiers are applied. Any future change to Phase 2C that removes or reduces the distance priority would directly erode the 1 km premium. Buyers who are paying a large premium on the basis of school access alone should keep this policy risk in mind.

🔮 Looking Ahead: Will the School-Proximity Premium Persist?

Singapore’s P1 registration system has been broadly stable for decades, and the government has shown little appetite for eliminating the distance-based priority — it is seen as a reasonable community-based principle. However, MOE has been expanding school capacity at the primary level and has encouraged parents to consider neighbourhood schools as credible alternatives to branded schools. If these efforts succeed in reducing the prestige gap between schools, the Phase 2C premium for any individual school may narrow. The safest bet remains properties in estates with multiple oversubscribed schools within range, so that the premium is supported by a cluster of demand rather than a single school. These are speculative observations — official policy may change without notice.

Frequently Asked Questions

How exactly does MOE measure the 1 km distance?

MOE measures the straight-line distance from the main entrance of your home to the main gate of the school. This is not walking distance or driving distance — it is the straight-line (crow flies) measurement. MOE uses its own GIS system to calculate this; the result may differ from Google Maps or other mapping tools by up to 100–200 metres in some cases. You can check your address against any school using the MOE School Finder tool. Always verify using MOE’s official tool before relying on any proximity claim made by a property agent or listing.

Can I use a relative’s address to get the 1 km priority?

No. MOE requires you to be genuinely registered and residing at the address provided. Using a relative’s or friend’s address to claim proximity priority is considered fraudulent and may result in the child’s application being rejected, even after a school place has been allocated. MOE conducts checks including cross-referencing with NRIC records, HDB or URA records, and utility bills. Parents found to have provided false addresses face disqualification from the registration exercise and potential legal consequences. The address must be your genuine principal place of residence at the time of registration.

Does the school-proximity premium apply to secondary schools too?

Not in the same way. Secondary school admission in Singapore is primarily determined by PSLE results (Direct School Admission aside), so residential proximity plays no formal role in secondary school access. The property premium phenomenon is therefore primarily a primary school effect. That said, some parents choose to live near certain secondary schools for practical convenience (shorter commute), and a cluster of good primary and secondary schools in the same area can create a compounding “educational belt” effect on property values — as seen in the Bishan–Ang Mo Kio corridor.

Will buying an HDB flat near a top school get me the same Phase 2C priority as a condo?

Yes. MOE’s Phase 2C priority is based on the registered residential address and its distance from the school — it does not distinguish between property types. An HDB flat within 1 km of Ai Tong School receives exactly the same Phase 2C ballot priority as a private condominium within 1 km. The key is that the address must be your genuine place of residence and registered in the HDB or URA records. For HDB buyers, note that the MOP (Minimum Occupation Period) means you must already own or purchase an HDB flat that is within 1 km — you cannot simply rent a nearby property to claim proximity.

How long before the P1 registration exercise must I live at the address?

For Phase 2C, MOE requires the child to be residing at the registered address. There is no explicit minimum duration stated for Phase 2C, but MOE may request supporting documentation. For Phase 2B (volunteer parent priority), the volunteerism must be completed in the year before registration, typically requiring at least 40 hours of actual service at the school. If you purchase a property specifically for school access, moving in at least several months before the registration exercise (which typically opens in July for January the following year) is strongly advisable to avoid any documentary issues.

What if I rent a property near the school rather than buying?

Renting is a legitimate and often lower-cost strategy for securing the proximity priority without paying the purchase premium. A tenancy agreement and utility bills in your name at a 1 km address are typically accepted as evidence of residence for MOE purposes. However, renting near a top school can itself be expensive — landlords in these catchment areas are aware of the demand and price accordingly. Rental premiums of 10–15% over comparable properties outside the catchment are not uncommon in Bukit Timah and Queenstown. If you only need the proximity for one registration year, renting for 12 months may be materially cheaper than paying the purchase premium over a longer horizon.

Are international schools affected by the same proximity rules?

No. International schools in Singapore operate under different admission frameworks set by the individual school and the Ministry of Education’s International Schools Unit. They are not subject to the MOE P1 Phase 2C priority system, so residential proximity to an international school creates no formal priority advantage. Property premiums near international schools do exist in some cases — particularly near the American School, United World College, and the German European School — but these are driven by the convenience of expatriate communities rather than any formal regulatory priority linked to the address.

Related Articles

- Singapore Property Buying Checklist 2026: 50 Things to Check Before You Commit

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Home Loan Complete Guide 2026

- Singapore HDB Resale Guide 2026: Buying a Resale Flat Step-by-Step

- Singapore Property Investment Guide 2026

- Singapore Prime District Property Guide 2026

- Condo vs HDB Singapore 2026: Which Should You Buy?

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or educational advice. Property prices, school admission policies, and MOE phase criteria are subject to change; always verify current rules directly with the Ministry of Education and Urban Redevelopment Authority. Price premiums cited are indicative estimates based on publicly available URA transaction data and industry analysis — they are not financial advice. Consult a licensed financial adviser and property professional before making any property decision. School names and reputations are referenced for informational purposes only; LovelyHomes does not endorse or rank any school.