Singapore HDB CPF Housing Grants Guide 2026: EHG, Family Grant, PHG and Every Dollar You Can Claim

Quick Answer: Key Takeaways

- Singapore first-time HDB buyers can receive up to S$230,000 in combined CPF housing grants (resale) or up to S$120,000 for a BTO flat.

- The Enhanced CPF Housing Grant (EHG) is the cornerstone — up to S$80,000 for couples, tapering with income. It applies to both BTO and resale flats.

- The CPF Housing Grant (Family Grant) for resale adds up to S$80,000 on top of EHG; the Proximity Housing Grant (PHG) can add another S$30,000.

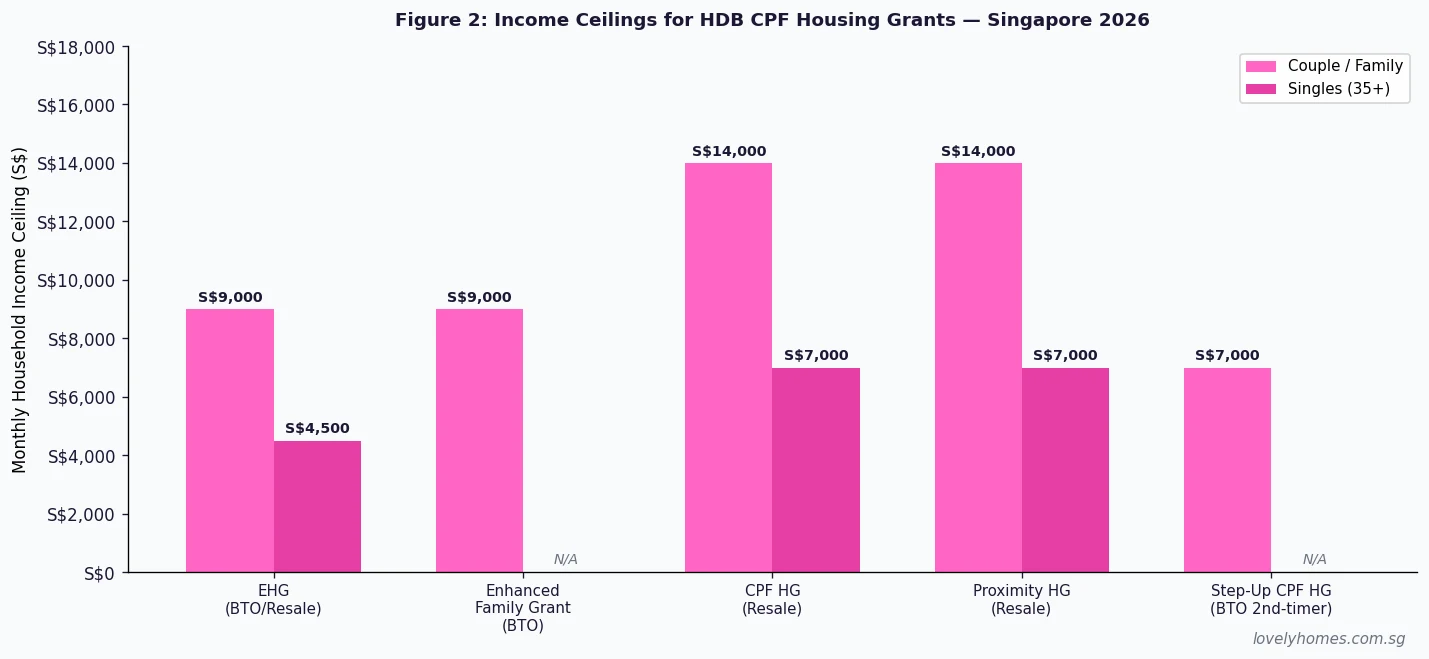

- Income ceilings vary: EHG caps at S$9,000/mth (couples); Family Grant and PHG cap at S$14,000/mth.

- All grants are disbursed into your CPF Ordinary Account and used for the flat purchase — they do not arrive as cash.

- Second-timer families buying BTO flats can access the Step-Up CPF Housing Grant (S$15,000) if upgrading from a 2-room Flexi.

- Apply for grants during the HDB Flat Eligibility (HFE) Letter application process — grants are assessed and confirmed before you book a flat or submit an OTP.

What Are HDB CPF Housing Grants?

Singapore’s CPF housing grant system is one of the most comprehensive homeownership subsidy programmes in the world. Administered jointly by the Housing & Development Board (HDB) and the Central Provident Fund (CPF) Board, these grants reduce the effective purchase price of an HDB flat by transferring funds directly into your CPF Ordinary Account. You then draw on that CPF balance to pay your flat’s downpayment and monthly instalments — effectively cutting your out-of-pocket cash requirements.

Grants apply to Singapore Citizens (SCs) buying HDB flats, whether new BTO or resale. Permanent Residents purchasing resale flats together with an SC spouse are eligible for reduced grant amounts on certain schemes. Grants do not reduce your BSD liability — stamp duty is levied on the full purchase price — but they substantially lower the cash you need to bridge.

As at 1 July 2026, the four active grant schemes are: the Enhanced CPF Housing Grant (EHG), the CPF Housing Grant for resale (sometimes called the Family Grant), the Proximity Housing Grant (PHG), and the Step-Up CPF Housing Grant for eligible second-timers.

Grant 1: Enhanced CPF Housing Grant (EHG)

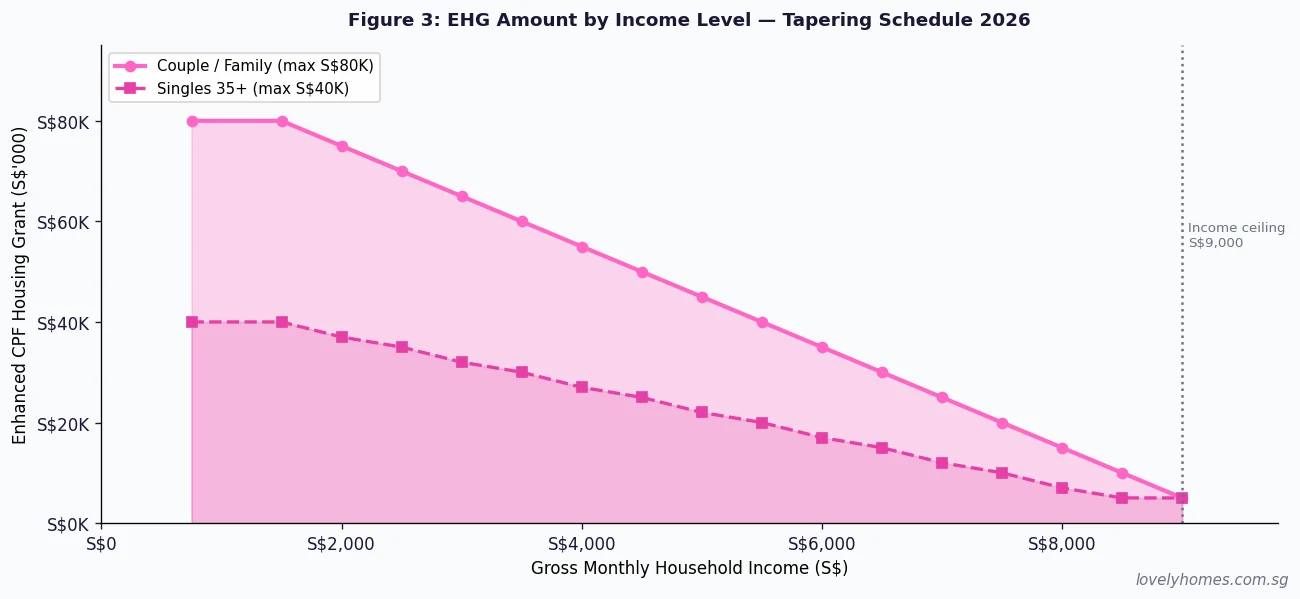

The EHG is the flagship grant available to first-timer families and singles buying their first subsidised home — applicable to both BTO and resale HDB flats. It was introduced in September 2019, replacing the earlier Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG), and is designed to taper sharply with household income so that the lowest-income buyers receive the most support.

EHG eligibility

- At least one applicant must be a Singapore Citizen.

- All applicants and occupiers must not own or have disposed of any private property (locally or overseas) in the 30 months before the flat application.

- All applicants and essential occupiers must have been in continuous employment for at least 12 months before the application, or be self-employed for 12 months with CPF contributions.

- Gross monthly household income must not exceed S$9,000 for families (or S$4,500 for singles aged 35 and above).

- Buying a flat with a remaining lease of at least 20 years that covers the youngest buyer to age 95.

EHG amounts

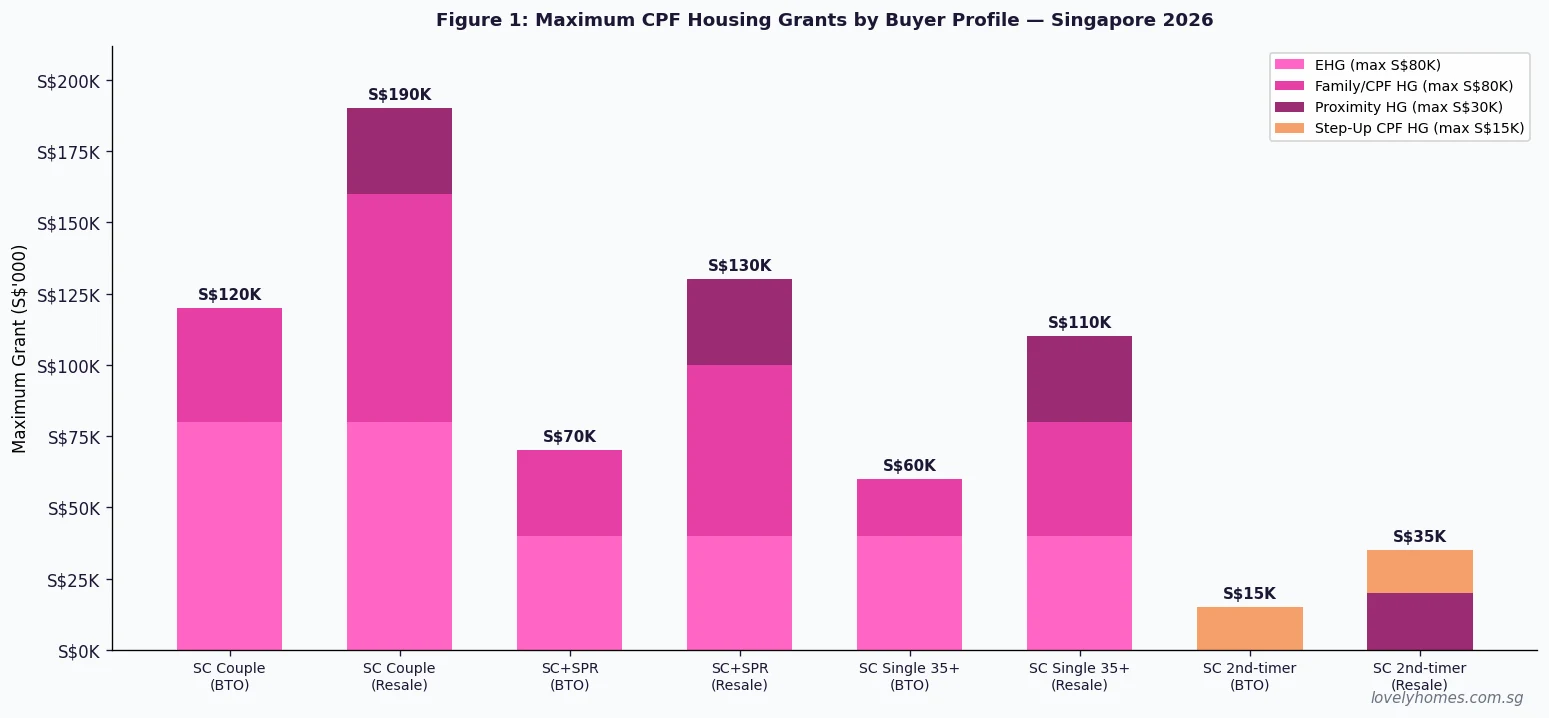

The EHG is income-progressive. The lower your household income, the higher your grant. For a couple or family, the maximum is S$80,000 (for households earning S$1,500 per month or less), tapering in roughly S$5,000 increments as income rises, to a minimum of S$5,000 for households earning S$8,501–S$9,000 per month. For singles aged 35 and above, the amounts are halved: maximum S$40,000 at income ≤ S$1,500, down to S$2,500 at ≤ S$4,500. Note that the EHG applies for every flat type — a couple buying a 2-room BTO in Tengah receives the same EHG as one buying a 5-room resale flat in Bishan, as long as income and other criteria are met.

Grant 2: CPF Housing Grant — Family Grant (Resale Flats)

The CPF Housing Grant for resale flats — commonly called the Family Grant — applies exclusively when you buy a resale HDB flat from the open market. It is layered on top of the EHG and brings the total potential subsidy to well over S$100,000 for eligible buyers.

Family Grant amounts

| Buyer Profile | 2-room / 3-room flat | 4-room flat and above |

|---|---|---|

| SC couple or family (both SC) | S$50,000 | S$80,000 |

| SC + SPR couple (one SC, one PR) | S$40,000 | S$60,000 |

| SC singles (35 and above) | S$25,000 | S$40,000 |

Family Grant eligibility

- At least one applicant must be an SC.

- For couples: at least one must have been working and making CPF contributions continuously (or self-employed) for at least 12 months immediately before the OTP date.

- Gross monthly household income must not exceed S$14,000 (couples/families) or S$7,000 (singles).

- First-timer families only (you must not have previously received any CPF housing grant).

Grant 3: Proximity Housing Grant (PHG)

Singapore’s Proximity Housing Grant incentivises multigenerational living — or at least living close to family. Administered by HDB, it applies when you buy a resale flat to live near or with your parents, children, or in-laws. The PHG recognises that family proximity reduces social isolation and supports informal caregiving, and it is stacked on top of EHG and the Family Grant.

PHG amounts

| Living arrangement | Grant |

|---|---|

| Living WITH parents / child (in the same flat, at time of application) | S$30,000 |

| Living NEAR parents / child (within 4 km, different flat) | S$15,000 |

PHG eligibility

- The applicant and the relevant family member (parent/child) must both be SCs or PRs.

- The family member being lived near/with must be in a qualifying flat (HDB, EC, or private).

- Income ceiling: S$14,000/month (couples/families).

- Applies to resale flats only — not BTO.

- The applicant’s flat and the parent’s/child’s flat must each be in Singapore, and the 4 km radius is measured door-to-door (straight line) by HDB.

Grant 4: Step-Up CPF Housing Grant

The Step-Up CPF Housing Grant was introduced to help Singapore Citizens who are second-timers but from lower-income backgrounds make the jump from a 2-room Flexi BTO flat to a larger subsidised flat. It is specifically designed for households that may have missed the first-timer grant window or have more modest means.

Step-Up Grant criteria

- Both applicants must be SCs, and at least one must be currently living in a 2-room Flexi BTO flat (built by HDB after 2017).

- Household income must not exceed S$7,000/month.

- Buying a 3-room BTO flat or larger from HDB.

- Grant amount: S$15,000.

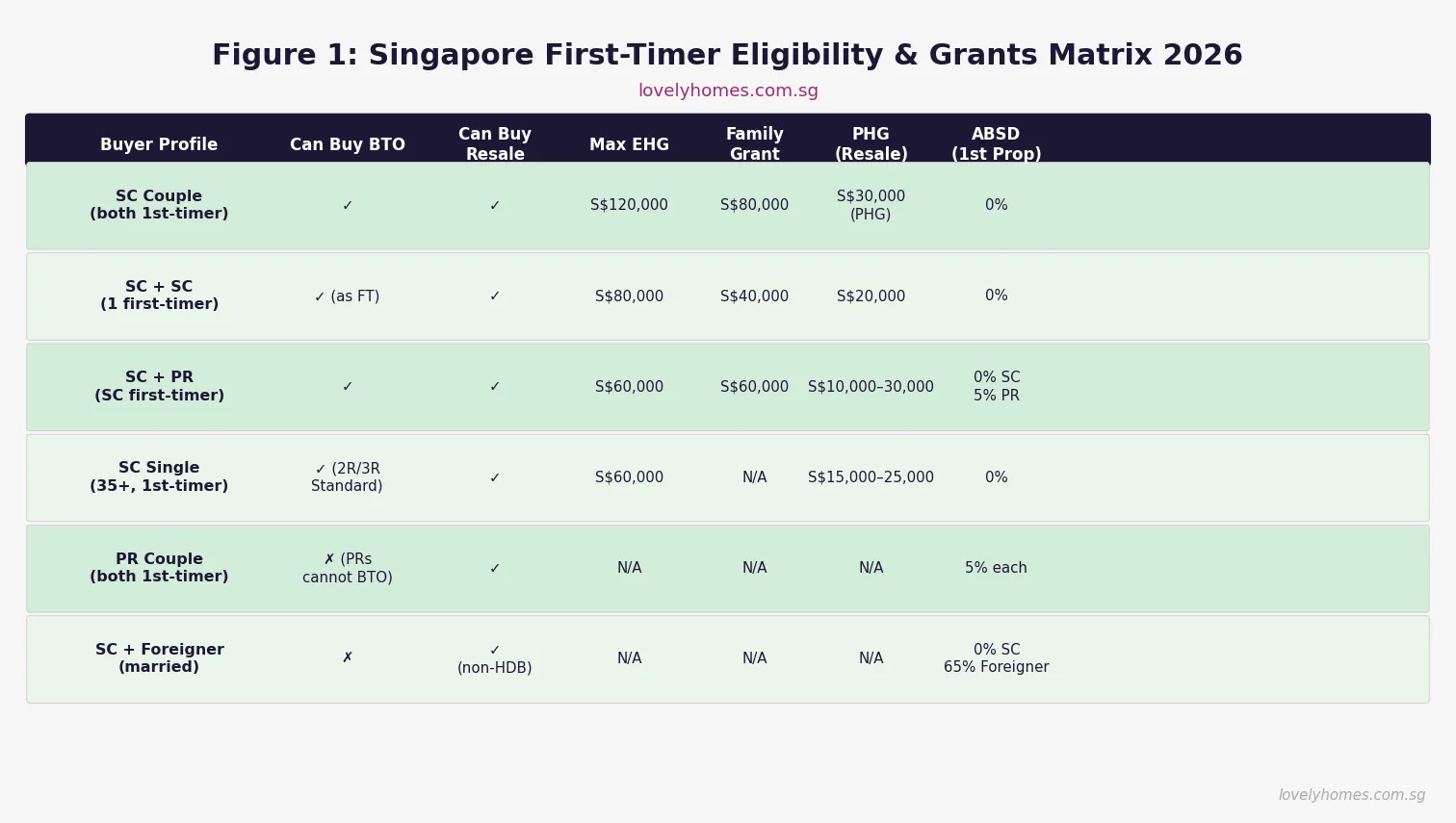

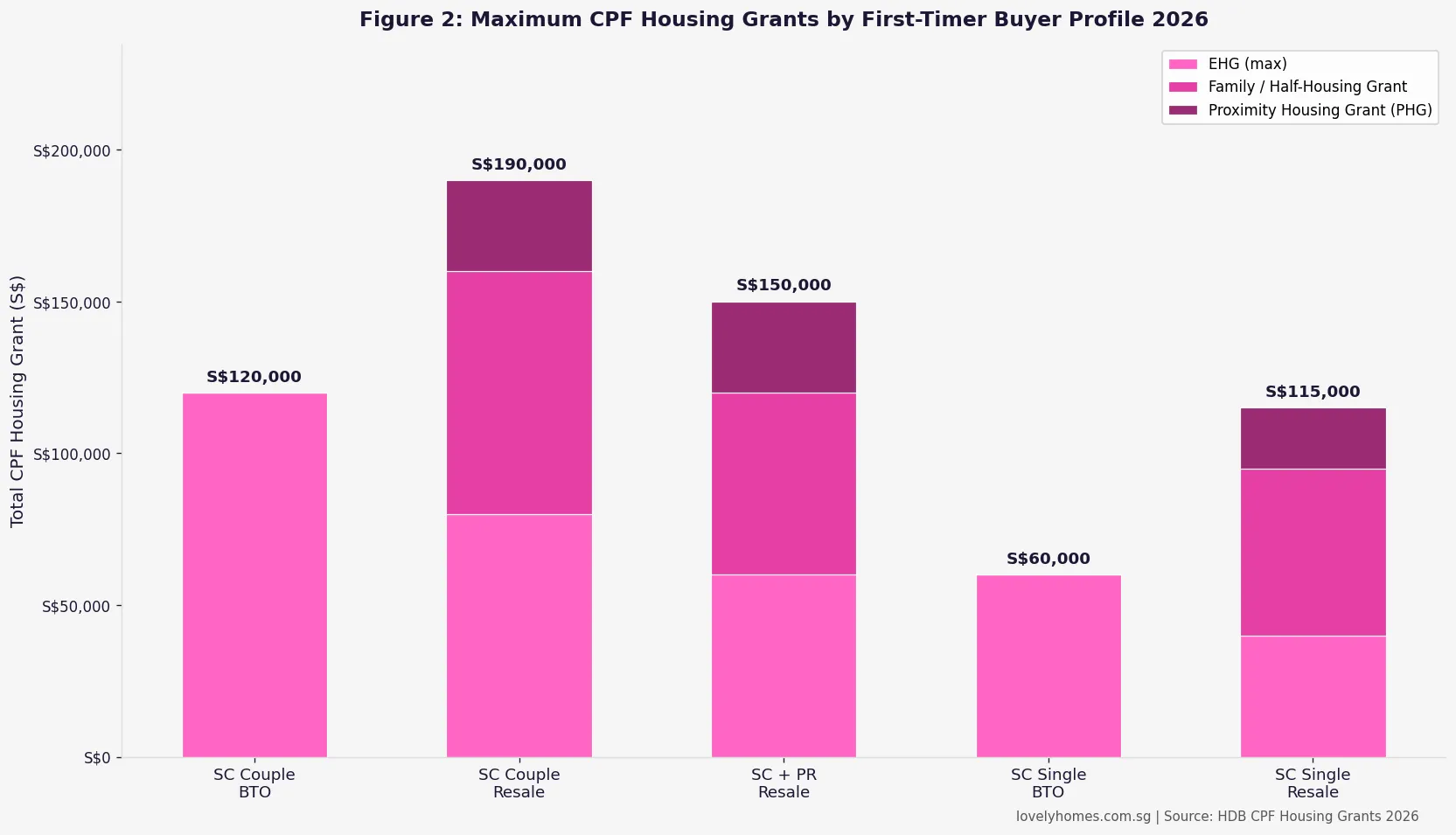

How the Grants Stack: A Summary Table

| Grant | BTO / Resale | Max Amount (SC Couple) | Income Ceiling | Stackable With |

|---|---|---|---|---|

| EHG | Both | S$80,000 | S$9,000/mth | Family Grant, PHG |

| Family Grant | Resale only | S$80,000 | S$14,000/mth | EHG, PHG |

| Proximity HG (PHG) | Resale only | S$30,000 | S$14,000/mth | EHG, Family Grant |

| Step-Up CPF HG | BTO only (3-room+) | S$15,000 | S$7,000/mth | EHG (limited) |

| Maximum (Resale, SC Couple) | Resale | S$190,000 | S$9,000/mth (EHG) + S$14,000/mth (others) | All stacked |

| Maximum (BTO, SC Couple) | BTO | S$80,000 | S$9,000/mth | EHG only (+ Step-Up if 2nd-timer) |

Worked Example: The Lim Family

Mr and Mrs Lim are a Singapore Citizen couple, both aged 29, with a combined gross monthly income of S$5,500. They have been continuously employed for over 12 months. Their CPF OA balance is S$28,000 combined. They are buying a 4-room resale HDB flat in Tampines for S$620,000. Mrs Lim’s parents live in Tampines, approximately 1.8 km away.

Step 1 — Determine EHG. Income S$5,500, SC couple, first-timers. EHG taper table: at S$5,001–S$5,500, the grant is approximately S$45,000.

Step 2 — Determine Family Grant. 4-room resale flat, SC couple, income below S$14,000 → Family Grant = S$80,000.

Step 3 — Determine PHG. Mrs Lim’s parents are within 4 km but not in the same flat → Near-parents PHG = S$15,000.

Total grants: S$140,000.

Step 4 — Work out the purchase.

Purchase price: S$620,000

BSD: S$620,000 × (1% × S$180K + 2% × S$180K + 3% × S$260K) = S$15,000 (paid from CPF OA)

HDB loan (80% LTV): S$496,000 (assuming they take HDB loan)

CPF contribution: S$620,000 − S$496,000 = S$124,000 needed (grants S$140,000 disbursed into CPF OA — covers this entirely)

Cash outlay: approximately S$0 for downpayment (CPF + grants cover it); cash needed for legal fees ~S$2,000.

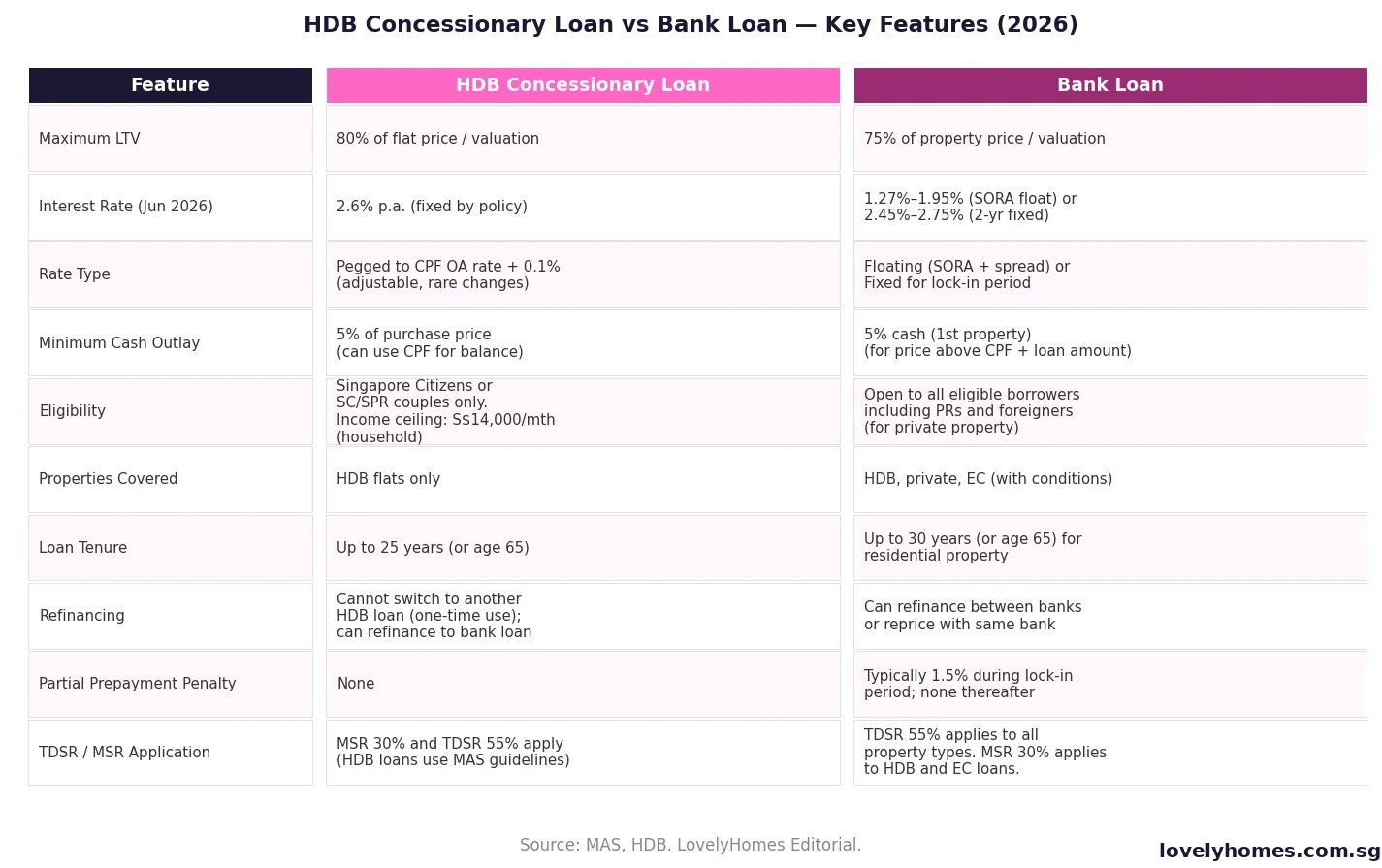

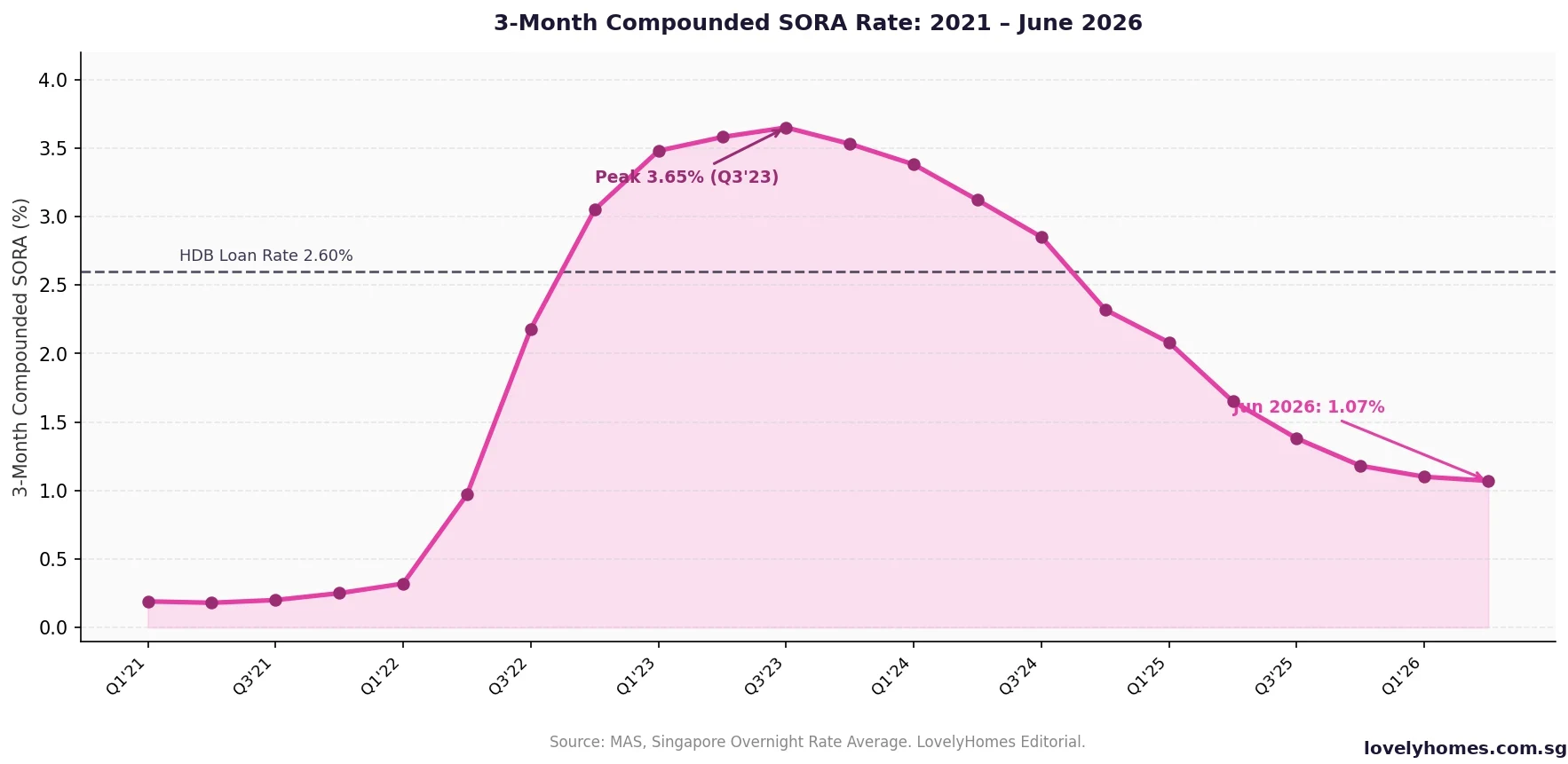

Monthly instalment: S$496,000 at 2.6% over 25 years ≈ S$2,255/mth, within HDB’s 30% MSR rule on S$5,500 income (MSR = 41% — slightly over; they may consider a bank loan at lower rate or extend tenure to reduce instalment).

Why Singapore’s Grant System Is Designed This Way

The tiered grant structure reflects HDB’s policy objective: to ensure that housing affordability scales with means. Lower-income households receive proportionally larger subsidies, while higher-income households approaching the ceiling still receive meaningful support. The separation between BTO and resale grants — with resale grants being substantially higher — is deliberate: it reflects the higher market price of resale flats and provides a counterweight to the price premium that resale commands over BTO. Singapore’s model is unusual globally in that subsidies are not means-tested as one-time eligibility checks; rather, the progressive tapering of EHG mirrors the progression of income in a household’s early career.

What Might Come Next

The grant framework has been broadly stable since the 2019 EHG introduction and the 2023 cooling-measure adjustments. Looking forward, analysts expect the income ceiling for the Family Grant (S$14,000) to remain unchanged through 2026–2027 given that median household incomes in Singapore are still well below this level. There is some speculation — given rising resale prices, particularly in mature estates — that the EHG maximum for resale buyers could be revised upward before the next major budget cycle. Any revision would likely be announced in the Singapore Budget (typically February) or as a standalone HDB policy announcement.

Frequently Asked Questions

Can I receive both EHG and Family Grant for the same resale purchase?

Yes — the EHG and the Family Grant are stackable for resale purchases. For a first-timer SC couple buying a 4-room or larger resale flat, you can receive up to S$80,000 EHG (subject to income) + S$80,000 Family Grant = up to S$160,000 in combined grants, before the PHG. This is the “full stack” for resale purchasers and represents the most generous scenario in the HDB grant system.

Can a SC buying with a foreigner (non-PR) spouse receive any grants?

No. The CPF housing grants require that the co-applicant be at least a Singapore Permanent Resident. A SC buying with a foreign national (non-PR) does not qualify for the EHG, Family Grant, or PHG. The SC buyer would also be subject to ABSD at 60% on the non-citizen co-buyer’s share. In this situation, the SC typically purchases the flat in their own name, without the foreign spouse as a co-applicant — which means only one income is assessed for the MSR/TDSR, and the flat may not be co-owned by the foreigner.

Are BTO buyers eligible for the Proximity Housing Grant?

No. The PHG applies to resale flats only. When you buy a BTO flat, there is no equivalent proximity grant. This is one of the reasons why resale buyers in proximity to their parents can receive substantially more total grants than BTO buyers — resale buyers can access EHG + Family Grant + PHG simultaneously, while BTO buyers only receive the EHG (plus Step-Up Grant for eligible second-timers).

How are the grants disbursed — do I receive cash?

Grants are not paid in cash. HDB disburses the approved grant amount into your CPF Ordinary Account (OA). Once in your OA, the funds can be used to pay the flat’s downpayment, BSD, and monthly loan instalments — but they remain in the CPF ecosystem until the flat is sold or the CPF balance reaches a withdrawal limit. This means grants directly reduce your cash outlay (by building up your CPF OA balance), but they do not arrive in your bank account.

Does receiving grants affect my CPF accrued interest obligation when I sell?

Yes, indirectly. The more CPF you draw on for the flat (including grant monies credited to your OA and subsequently withdrawn for the flat), the larger the CPF refund — principal plus 2.5% p.a. accrued interest — due upon sale. The grants increase your CPF OA balance, which you then draw down. Upon sale, the full CPF drawn amount plus accrued interest is refunded to your CPF accounts first. This can significantly reduce your net cash proceeds, particularly if you hold the flat for 15–20 years and have drawn heavily on CPF. Always model this in your net-proceeds calculation before deciding whether to maximise CPF usage.

Can I use my grants to pay Buyer’s Stamp Duty (BSD)?

Indirectly, yes. The grants are credited to your CPF OA, and you may use your CPF OA balance to pay BSD on the flat. So while the grants themselves do not directly pay BSD, they boost your OA balance from which BSD can be paid, reducing the cash you need to set aside. BSD is capped at the amount the CPF Board allows you to use based on the flat’s valuation, so very low-valuation flats may require some cash top-up for BSD regardless.

What is the HDB Flat Eligibility (HFE) Letter and how does it relate to grants?

The HFE Letter is the entry point to both the HDB loan and the grants system. Introduced in 2023, it replaced the HDB Loan Eligibility (HLE) letter and the older grant assessment process. You apply for the HFE letter on the HDB Flat Portal before booking a flat or submitting an OTP for a resale purchase. HDB assesses your eligibility for an HDB loan AND all applicable grants simultaneously, so you know upfront exactly what financial support you qualify for. The HFE letter is valid for 6 months, after which you must reapply if you have not completed the purchase.

Related Articles

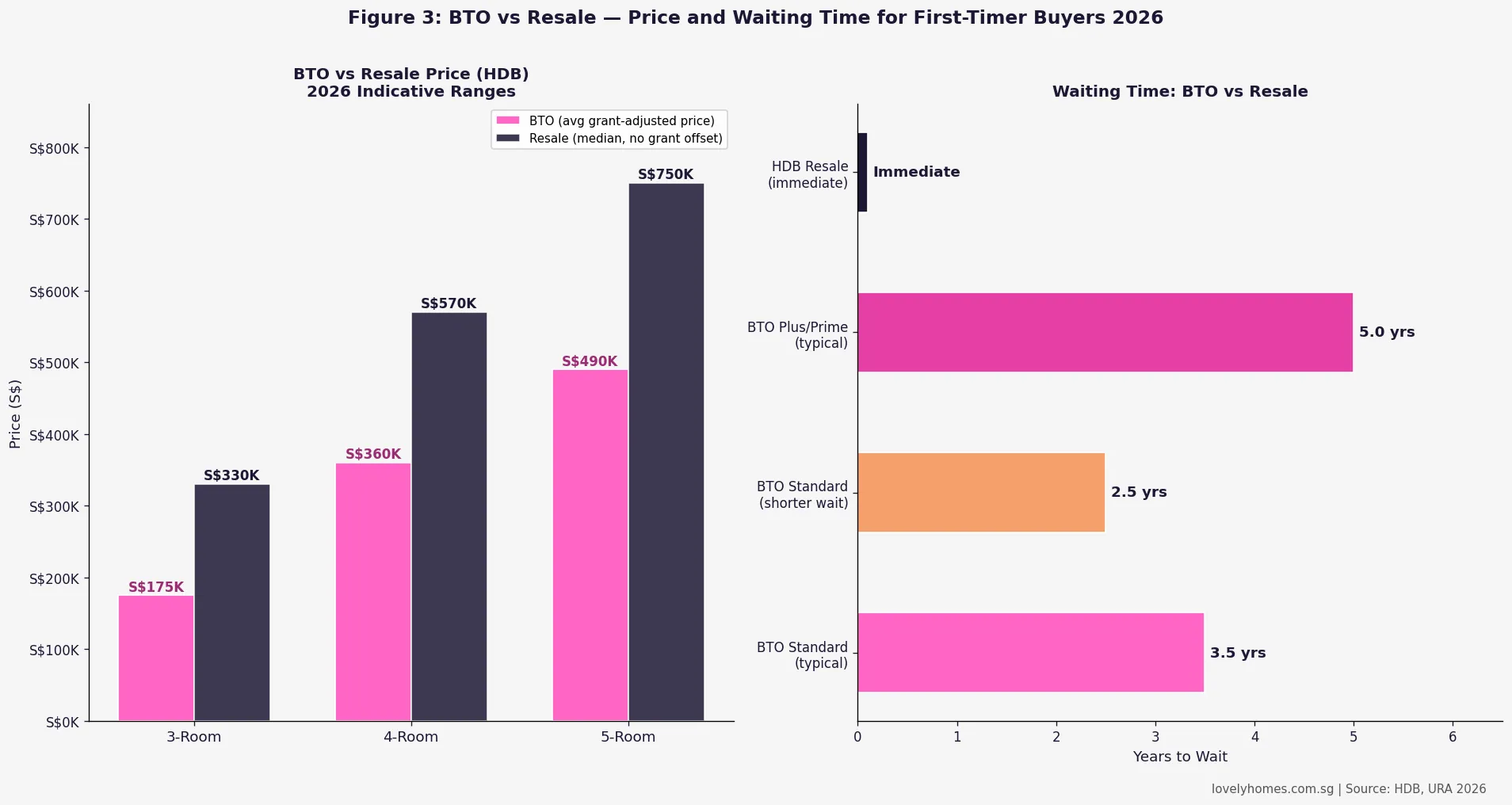

- HDB BTO vs Resale Flat 2026: Complete Comparison

- Singapore First-Timer Home Buyer Complete Guide 2026

- HDB BTO October 2026 Guide: All 7 Projects and Application Tips

- Singapore HDB Resale Buying Process 2026: Step-by-Step

- CPF Property Usage Guide 2026: OA Withdrawal and Accrued Interest

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer

This article is for general information only and does not constitute financial, legal, or property advice. Grant amounts, income ceilings, and eligibility conditions are subject to change; always verify current rules with the Housing & Development Board (HDB) and the Central Provident Fund (CPF) Board before making any purchase decision. Stamp duty figures are indicative only. Please consult a licensed financial adviser or HDB-registered solicitor for advice tailored to your circumstances.