Singapore Property Selling Guide 2026: How to Sell Your HDB, Condo or Landed Property — Step by Step

- There is no capital gains tax in Singapore — profit from a property sale is not taxed unless IRAS deems you a property trader.

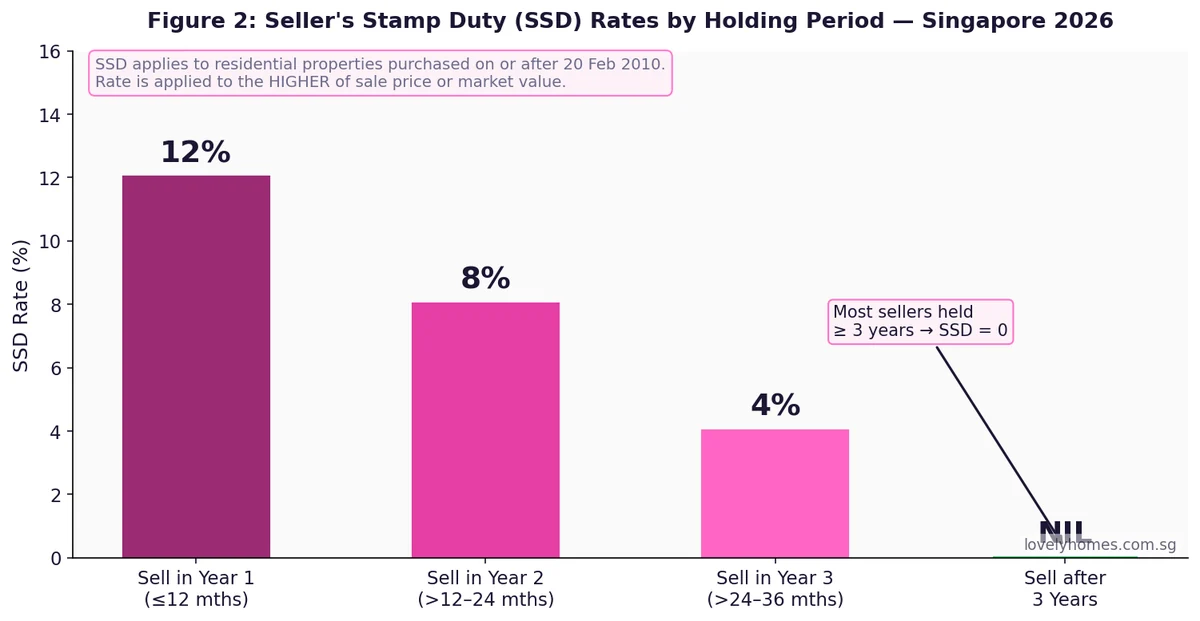

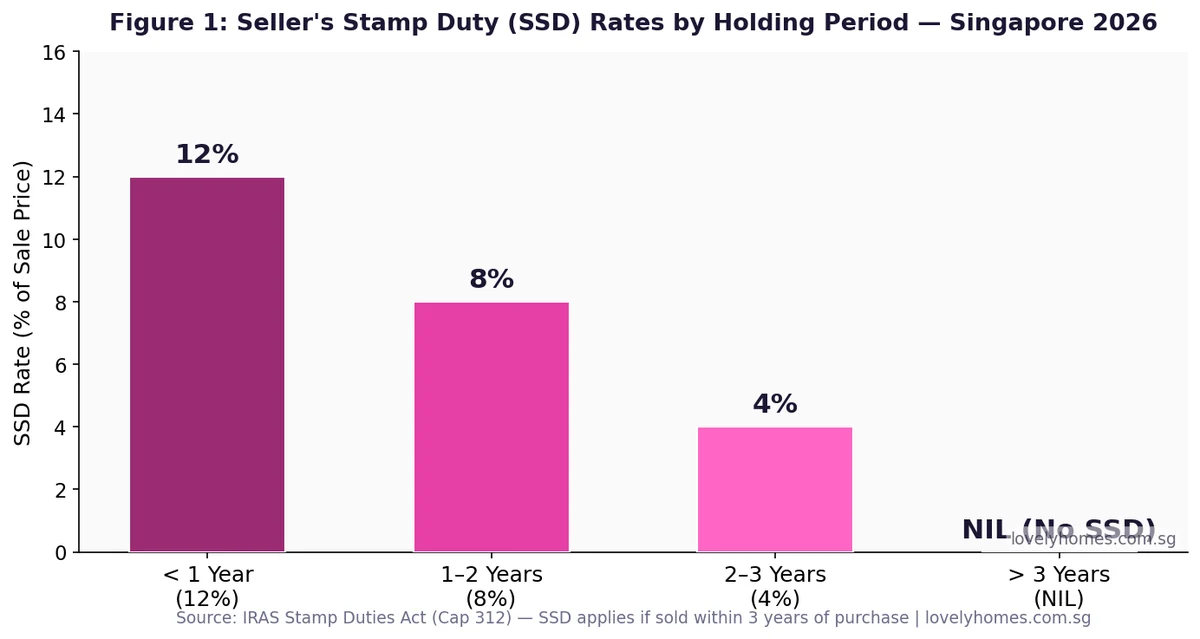

- Seller’s Stamp Duty (SSD) applies if you sell within 3 years of purchase: 12% (under 1 year), 8% (1–2 years), 4% (2–3 years), 0% thereafter.

- HDB flat sellers effectively never pay SSD because the 5-year Minimum Occupation Period (MOP) exceeds the 3-year SSD window.

- All CPF Ordinary Account (OA) monies used for the property must be refunded upon sale — principal plus accrued interest at 2.5% per annum.

- Agent commission is typically 2% for HDB resale and 1–2% for private property (negotiable; no government-mandated rate).

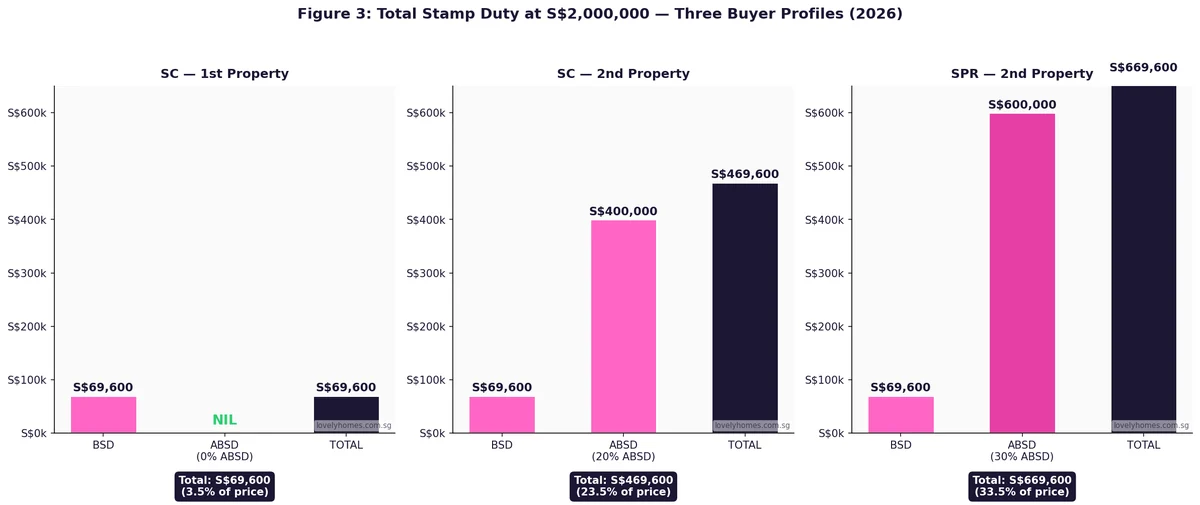

- SC married couples who buy a new private property before selling their HDB flat pay ABSD 20% upfront but may claim a remission if the HDB is sold within 6 months.

- The HDB resale process takes approximately 8–12 weeks; private property completion typically runs 10–16 weeks after OTP exercise.

- Sellers must file the Resale Checklist (HDB) or grant an Option to Purchase (private) as the formal first step — verbal agreements are not binding.

What This Guide Covers

Selling a property in Singapore is a structured, multi-step process governed by the Housing and Development Board (HDB), the Urban Redevelopment Authority (URA), the Inland Revenue Authority of Singapore (IRAS), and the Singapore Land Authority (SLA). Whether you are selling an HDB flat, a private condominium or landed home, understanding your obligations — and your costs — before you sign anything will protect both your timeline and your net proceeds.

This guide walks through every stage of the selling process: from registering your intent to sell through to collecting your sale proceeds. We cover Seller’s Stamp Duty (SSD), CPF Ordinary Account refunds, agent commission, legal fees, the ABSD remission for upgraders, and what the numbers actually look like at three common price points.

Step 1: Confirm Your Eligibility to Sell

HDB Flat Sellers

Before listing your HDB flat, confirm that you have fulfilled the Minimum Occupation Period (MOP). Under HDB rules, the MOP is generally five years from the date of flat collection (key collection) for BTO and resale flats, and 10 years for Prime Location Public Housing (PLH) flats in areas such as Rochor, Central, and River Peaks. Flats under the Plus category (introduced from the October 2024 BTO exercise onwards) also carry a 10-year MOP.

Once your MOP is satisfied, register your Intent to Sell on the HDB Resale Portal at least seven days before granting any Option to Purchase (OTP). HDB uses this window to flag eligibility issues — for example, outstanding upgrading contributions or HDB loan arrears — before any buyer is committed.

Private Property Sellers

There is no waiting period for selling private residential property, but you must check whether SSD applies (see Section 3 below). If you purchased the property as an investment under a corporate entity, the Additional Conveyance Duties (ACD) regime administered by IRAS may also be relevant. Most owner-occupier sellers are unaffected by ACD, which primarily targets equity interest transfers.

Step 2: Appoint an Agent and Set a Price

In Singapore, sellers of private property engage their own agent and pay their own commission. For HDB resale transactions, the seller’s agent is also typically paid by the seller. The Council for Estate Agencies (CEA) licences all property agents in Singapore; you may verify any agent’s registration at the CEA Public Register.

Commission is negotiable — there is no statutory rate. Market practice is approximately 2% of the sale price for HDB flats and 1–2% for private property. For very high-value or difficult-to-move properties, the rate may be negotiated higher. Some sellers opt for a fixed fee arrangement. Always confirm the agreed commission in writing before signing any appointment letter.

Setting the right asking price requires reviewing recent comparable transactions (available free via URA’s REALIS portal and HDB’s public resale flat transaction data). Overpricing slows your sale; underpricing erodes your equity position.

Step 3: Seller’s Stamp Duty (SSD) — Know Your Exposure Before You List

SSD is administered by IRAS under the Stamp Duties Act (Cap 312). It was reimposed in January 2011 and refined in March 2017, when the current three-year, three-tier structure took effect. SSD applies to all residential properties — HDB flats, condominiums, and landed homes alike — sold within three years of purchase.

| Holding Period | SSD Rate | Example: Property Sold at S$1,200,000 | Who This Affects Most |

|---|---|---|---|

| Less than 1 year | 12% | S$144,000 | Short-term flippers; forced sellers |

| 1 year to 2 years | 8% | S$96,000 | Sellers whose circumstances changed |

| 2 years to 3 years | 4% | S$48,000 | Early investors; job relocation sellers |

| 3 years or more | NIL | S$0 | Most owner-occupiers and long-term investors |

SSD is calculated on the higher of the sale price or the market value assessed by IRAS at the time of sale. It is payable by the seller within 14 days of the sale contract date (OTP exercise date for private property, or HDB Resale Application date for HDB transactions). Late payment attracts a penalty of up to four times the unpaid duty.

Practical note for HDB sellers: Because the HDB MOP is five years and SSD applies only within three years, HDB flat sellers who complete their MOP will never be subject to SSD. The SSD window closes at the three-year mark; the MOP does not open until the five-year mark.

Hardship exemptions exist but are rarely granted. IRAS considers genuine financial distress, medical incapacity, or divorce — the applicant must demonstrate that the sale was necessitated by a circumstance beyond their control.

Step 4: CPF Ordinary Account Refund — How Accrued Interest Works

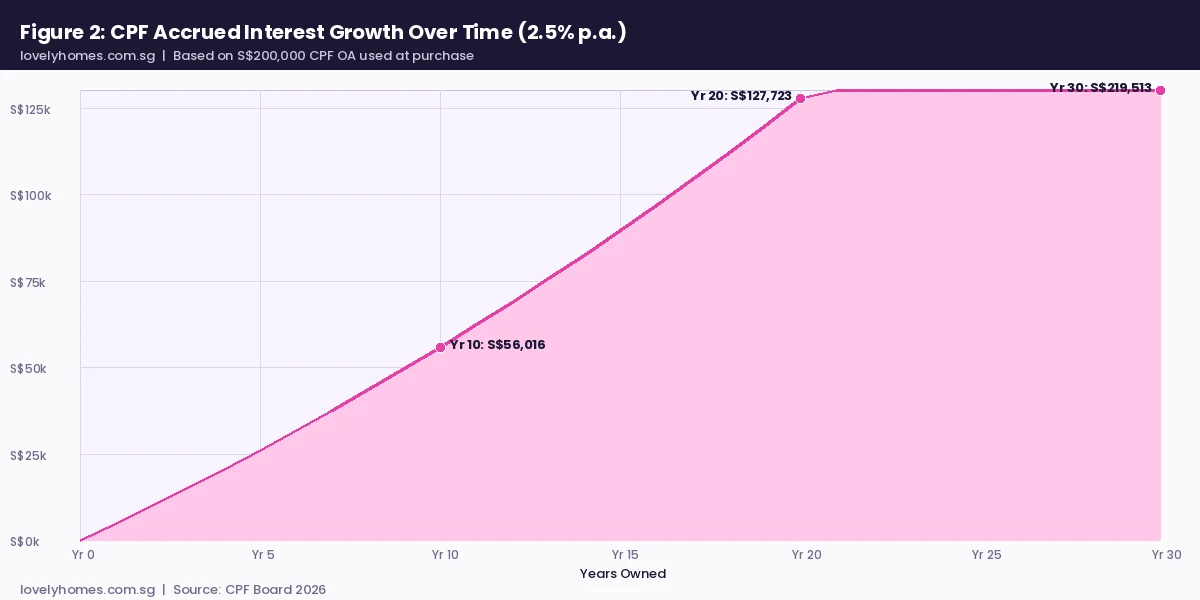

When you use CPF savings to purchase a property, you are borrowing from your own retirement account. To prevent erosion of retirement savings, the CPF Board requires that upon sale, all CPF monies withdrawn for the property are refunded to your CPF OA — including the interest those monies would have earned had they remained in the OA. This “accrued interest” accrues at the prevailing CPF OA interest rate, currently 2.5% per annum (guaranteed floor rate as of 2026).

The refund sequence is: (1) principal CPF withdrawn, (2) accrued interest. Only after this refund do you receive your net cash proceeds. For sellers who purchased many years ago with large CPF drawdowns, the accrued interest component can be substantial.

Illustration: If you drew S$200,000 from CPF OA to purchase a property in January 2019 and sell it in June 2026 (7.4 years), the accrued interest is approximately S$200,000 × 2.5% × 7.4 = S$37,000. Your CPF refund is therefore S$237,000, not S$200,000. This money goes back into your CPF OA and will be available for your next property purchase or for retirement withdrawal at age 55+.

The accrued interest is not a penalty; it is simply the return of the compounded interest your CPF savings would have earned in the OA. Sellers sometimes mistake this for a “profit tax” — it is not. It does, however, reduce your net cash-in-hand on sale, which matters if you need cash for your next purchase’s downpayment.

Summary of Key Seller Obligations

| Obligation | Administered by | When Due | Penalty for Default |

|---|---|---|---|

| Register Intent to Sell (HDB) | HDB | ≥ 7 days before OTP | Cannot proceed with sale |

| Pay SSD (if applicable) | IRAS | Within 14 days of contract | Up to 4× unpaid duty |

| Repay outstanding HDB loan | HDB | At legal completion | Completion delayed |

| Refund CPF OA principal + accrued interest | CPF Board | At legal completion | Sale proceeds withheld |

| Discharge caveat (if private property) | SLA | At legal completion | Title cannot pass |

| Pay agent commission | CEA-licenced agent | At legal completion | Civil action by agent |

| Pay conveyancing legal fees | Seller’s solicitor | At legal completion | Files withheld |

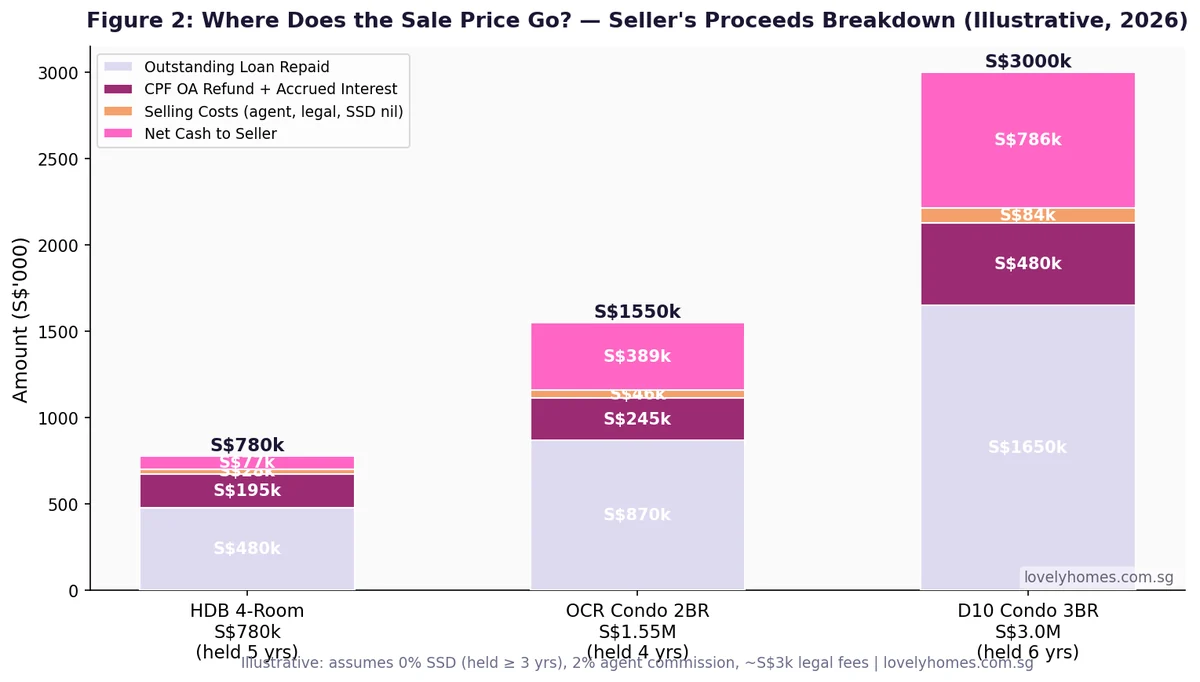

Step 5: Understanding Your Net Proceeds

Your net cash proceeds from a property sale are what remains after repaying all outstanding obligations. Most sellers are surprised to find that the headline sale price bears little resemblance to the cash they actually receive, particularly if the property was heavily financed and CPF funds were used extensively.

The chart above shows three illustrative scenarios for a seller who has held the property for more than three years (SSD = nil). In every case, the outstanding loan repayment is the single largest deduction. The CPF refund (principal plus accrued interest) is the second largest. Net cash to the seller ranges from S$77,000 on an HDB flat to S$786,000 on a prime district condominium — which underscores why understanding your equity position before listing is critical.

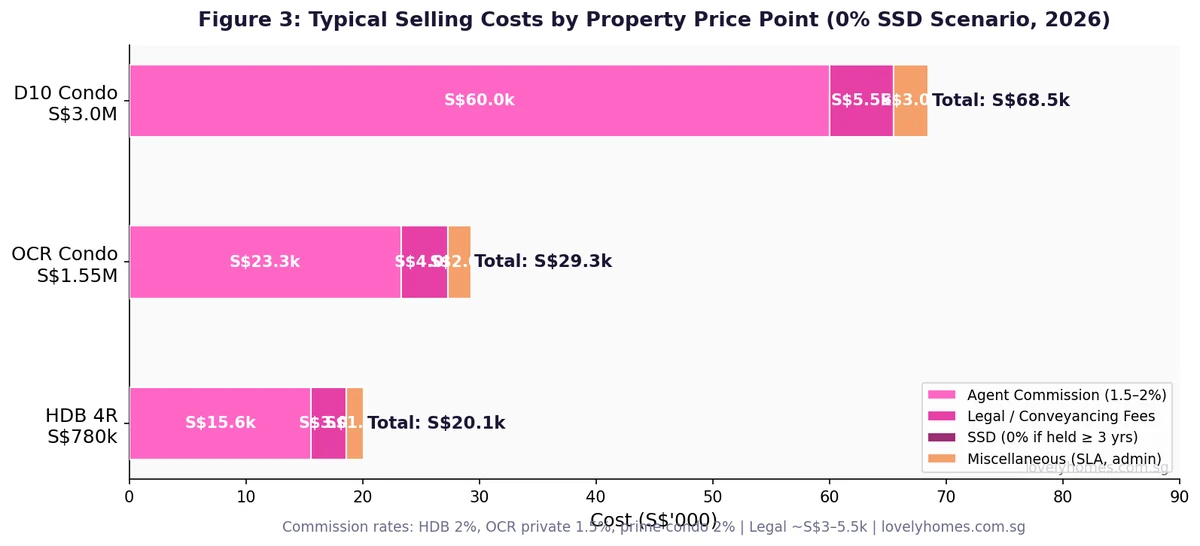

Step 6: Selling Costs — Agent, Legal, and Sundry Fees

Selling costs in Singapore are modest by regional standards, but they still add up:

- Agent commission: The dominant selling cost. Typically 2% of the sale price for HDB (both seller and buyer each pay their own agent). For private property, 1–2% is standard. On a S$3 million condominium at 2%, commission is S$60,000.

- Conveyancing legal fees: S$2,000–S$4,500 for most standard transactions. Solicitors in Singapore generally follow the Law Society scale but are free to quote fixed fees. Complex transactions (e.g., partial CPF pledging, foreign seller, multiple mortgagees) may cost more.

- HDB administrative fees: For HDB resale, an administrative fee of S$80 is charged at the Resale Completion Appointment.

- SLA caveat withdrawal: If you lodged a caveat as buyer (common for private property), the caveat must be withdrawn at sale. Fee: S$64.45 via the SLA e-filing portal.

- SSD (if applicable): As described above — 0% if held ≥ 3 years, up to 12% for sub-one-year sales.

Worked Example: Mr & Mrs Goh — Selling HDB, Upgrading to Private

Mr and Mrs Goh are Singapore Citizens, married, with a combined monthly income of S$15,000. They purchased a 5-room Bishan HDB flat in January 2019 at S$600,000 via an HDB concessionary loan (80% LTV). They have fulfilled their MOP (January 2024) and wish to sell in June 2026 and purchase an Outside Central Region (OCR) condominium unit.

HDB Sale Proceeds Breakdown (Sale price S$920,000):

| Item | Amount | Notes |

|---|---|---|

| Sale price | S$920,000 | Agreed transacted price |

| Less: Outstanding HDB loan | (S$376,000) | Approx balance after 7.5 years at 2.6% p.a. |

| Less: CPF OA principal refund | (S$120,000) | Total CPF drawn for downpayment + instalments |

| Less: CPF accrued interest | (S$22,200) | ~2.5% p.a. on S$120k × 7.4 years |

| Less: Agent commission (2%) | (S$18,400) | Seller pays own agent |

| Less: Legal / conveyancing fees | (S$2,800) | Seller’s solicitor |

| Less: SSD | NIL | Held > 3 years; MOP confirmed cleared |

| Net cash to Mr & Mrs Goh | S$380,600 | Available for next purchase + cash savings |

Next Step — OCR Condo Purchase (S$1,350,000): After selling the HDB first, Mr and Mrs Goh own zero residential properties. As Singapore Citizens purchasing their first private property, ABSD is nil. BSD on S$1.35M is S$37,200 (progressive rates up to 4% above S$1M). Bank loan at 75% LTV = S$1,012,500 at 3.0% p.a. over 25 years = S$4,800/month. TDSR: S$4,800 ÷ S$15,000 = 32% — comfortably within the 55% threshold. Cash upfront: S$337,500 (downpayment) + S$37,200 (BSD) = S$374,700 — funded from the S$380,600 net HDB sale proceeds. The transaction is feasible without additional savings.

ABSD Remission for SC Married Couples — The “Buy First, Sell Later” Option

Some upgraders prefer to secure their new private property before selling the HDB to avoid a gap period where they are without a home. Under the current rules (effective April 2023), a Singapore Citizen married couple buying a second residential property must pay ABSD at 20%. However, they may apply to IRAS for an ABSD remission if the HDB flat is sold within six months of the purchase of the private property (for a completed unit) or within six months of the private property’s Temporary Occupation Permit (TOP) date (for an uncompleted unit).

This is a powerful option but carries risk: if the HDB sale falls through or is delayed beyond the six-month window, the ABSD is forfeited. On a S$1.35 million purchase, ABSD at 20% is S$270,000. Couples considering this route must maintain sufficient liquidity to fund the ABSD upfront while awaiting the refund.

What This Means for Property Sellers in 2026

Singapore’s property market in Q1 2026 recorded private residential price growth of 0.9% (URA), with the Outside Central Region leading at 2.2% gains. HDB resale prices remain elevated, with a five-room flat at Henderson Road transacting at S$1.728 million in April 2026 — the highest-ever HDB resale price. In this environment, sellers generally hold the advantage, but the SSD and ABSD frameworks mean that timing your sale matters enormously. Selling within the three-year SSD window destroys value fast; holding beyond three years and structuring your purchase correctly (sell first or use remission carefully) preserves it.

What Might Come Next

The MAS Financial Stability Review (November 2025) flagged property market resilience but noted that elevated interest rates and slowing transaction volumes in the CCR warranted monitoring. Industry analysts suggest that the government is unlikely to ease cooling measures in 2026 absent a material correction in prices — meaning the SSD and ABSD frameworks should be treated as fixed parameters for planning purposes at least through 2027. Any revision to the ABSD remission window (currently six months) would require a formal policy announcement from the Ministry of Finance and IRAS.

Frequently Asked Questions

Can I use CPF to pay agent commission or legal fees when selling?

No. CPF savings cannot be used directly to pay agent commission or legal fees for a property sale. These costs must be paid in cash. CPF can only be used for property-related purposes at the point of purchase — specifically downpayment, monthly instalments, and BSD/ABSD (subject to timing rules). Upon sale, your CPF OA receives the principal refund plus accrued interest, which then becomes available for future property purchases or CPF-approved uses.

Is there any tax on the profit I make from selling my property?

Singapore does not levy a capital gains tax. Profit from the sale of a private residential property or HDB flat is generally not taxable. However, IRAS retains the discretion to treat gains as income if you are deemed to be carrying on a business of property trading — characterised by a pattern of frequent, short-hold purchases and sales with profit intent. Owner-occupiers and genuine long-term investors are almost never subject to this treatment. SSD is the government’s primary disincentive against short-term speculation and is entirely separate from income tax.

What happens to my CPF accrued interest when I sell? Is it lost?

The accrued interest is not lost — it goes back into your CPF OA, where it continues to earn the 2.5% guaranteed rate (with the additional 1% on the first S$60,000 of combined CPF balances). If you are below 55, you can use the CPF OA funds for your next property purchase. If you are 55 or above, the refund first tops up your Retirement Account to the Full Retirement Sum (S$213,000 in 2026), and any excess in the OA can be used for property or withdrawn. The accrued interest does reduce your cash-in-hand at sale, which is why planning your equity position before listing is important.

If I sell my HDB flat, can I buy a private property immediately?

Yes. Once your HDB flat is sold and the legal completion has taken place, you no longer own an HDB flat and your residential property count drops accordingly. Singapore Citizens purchasing their first private property pay no ABSD. Singapore Permanent Residents purchasing their first private property pay 5% ABSD. However, note that CPF proceeds from the HDB sale are returned to your CPF OA and are not accessible as cash on the day of completion — they typically post to your OA within a few working days. Ensure your cash flow for the new property’s downpayment is sourced accordingly.

What is the difference between the Option to Purchase (OTP) and the Sale & Purchase Agreement (S&P)?

The OTP is a contractual right granted by the seller to the buyer, giving the buyer a period (typically 14 days for private property) to decide whether to exercise the option. The option fee (typically 1% of the purchase price) is paid when the OTP is granted. If the buyer exercises the OTP, they pay the exercise fee (typically 4%), bringing the total deposit to 5%. The Sale & Purchase Agreement (S&P) is the binding contract executed upon exercise of the OTP, setting out all terms of the transaction including the completion date (usually 8–12 weeks). For HDB resale, the equivalent process uses a standardised OTP issued by HDB and submitted through the HDB Resale Portal — there is no separate S&P document.

How does SSD apply if I inherited the property?

SSD is based on the original purchase date of the property, not the date of inheritance. If the deceased purchased the property in March 2024 and you inherited it and sell it in May 2026 (approximately 2 years), SSD at 8% would apply. This catches many beneficiaries off guard. The SSD holding period is not reset by the change in ownership via inheritance. Beneficiaries who inherit property that is within the SSD window should factor this into their estate planning and timing decisions. There is no automatic exemption for inherited properties.

Do I need to pay property tax up to the day of completion?

Yes. Property tax is levied on an annual basis by IRAS and is the seller’s liability up to the date of legal completion. Your solicitor will apportion the property tax between seller and buyer in the completion account — the buyer reimburses the seller for property tax from the completion date to the end of the calendar year (or whatever period the annual tax covers). This apportionment is standard practice and will appear in your completion account prepared by your conveyancing lawyer. Owner-occupier rates (0% on the first S$8,000 AV, 4% on the next S$47,000 AV) typically mean property tax is modest for residential sellers.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Complete Guide 2026: BSD, ABSD, SSD and ACD Explained

- Singapore CPF Property Withdrawal Limits 2026: OA Valuation Limit, Withdrawal Limit and Accrued Interest Explained

- First-Time Property Buyer Guide Singapore 2026: HDB, EC and Condo — Every Step, Cost and Grant Explained

- Singapore Property Rental Guide 2026: Renting, Landlord Rules and Market Rates Explained

- Condo vs HDB Singapore 2026: The Upgrader’s Complete Decision Framework

- Singapore Bridging Loan Guide 2026: How to Bridge the Gap Between Selling and Buying Property

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, tax, or property advice. Property transactions in Singapore are governed by a complex and evolving framework of legislation and regulations administered by HDB, URA, IRAS, CPF, MAS, CEA, and SLA, among others. All figures, rates, and timelines cited are accurate as at 1 June 2026 based on publicly available sources, but may change. Always consult a licensed property agent, conveyancing solicitor, and financial adviser before proceeding with any property transaction. For official guidance, refer to: hdb.gov.sg, iras.gov.sg, cpf.gov.sg, ura.gov.sg.