Singapore Shophouse Investment Guide 2026: Conservation, Yields and Buyer’s Checklist

Singapore’s conservation shophouses are among the most distinctive and sought-after assets in any property portfolio. Compact in footprint but rich in character, these two- to three-storey heritage buildings — with their distinctive five-foot ways, shuttered windows, and ornate facades — dot the streetscapes of Chinatown, Tanjong Pagar, Kampong Glam, Little India, and Joo Chiat. They are also among the most complex properties to buy, finance, and manage. This guide covers everything an investor needs to know: what drives shophouse values, how yields compare with mainstream residential and industrial assets, the regulatory constraints of URA conservation status, and the real numbers behind a shophouse transaction.

- Commercial shophouses are not subject to Additional Buyer’s Stamp Duty (ABSD) — a significant advantage for investors who already own residential property.

- Price ranges: S$3.5M–S$32M+ depending on location, size, tenure, and conservation grade.

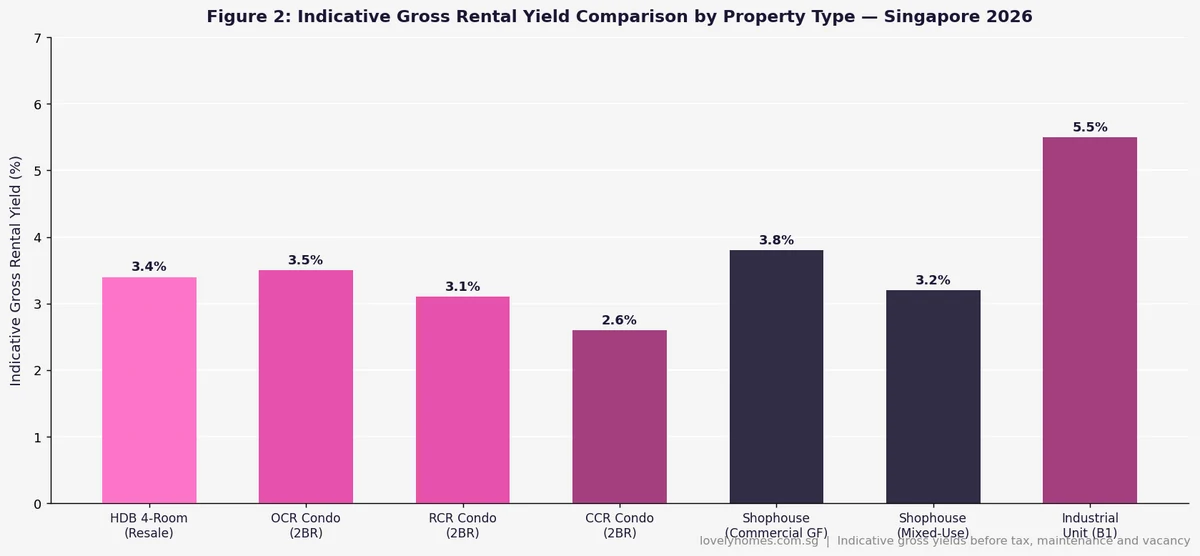

- Gross rental yields for commercial shophouses: 2.5–4.5% (commercial GF tenants pay a premium); mixed-use yields slightly lower at 2.8–3.5%.

- Most conservation shophouses carry 999-year or freehold tenure — offering leasehold decay-free capital preservation.

- URA conservation rules restrict external alterations; internal works are generally permitted with URA’s Written Permission.

- BSD applies at the standard residential/commercial scale on the full purchase price.

- Financing: commercial property loans, typically 80% LTV for pure commercial; some banks apply mixed-use restrictions.

- Corner shophouses command a 30–40% price premium over intermediate units of the same size.

What Is a Singapore Conservation Shophouse?

The term “shophouse” describes a narrow, multi-storey building originally designed for combined commercial and residential use — a shop on the ground floor, living quarters above. Built predominantly during the 19th and early 20th centuries under British colonial rule, Singapore’s surviving shophouses reflect a unique architectural style that blends Chinese, Malay, and European influences: the Straits Chinese (Peranakan), the Early Shophouse, the First Transitional, the Late Shophouse, and the Art Deco styles are the main conservation categories identified by the Urban Redevelopment Authority (URA).

URA has gazetted five primary conservation areas where shophouses are subject to strict conservation guidelines:

- Chinatown (including Tanjong Pagar, Kreta Ayer, Smith Street, and Bukit Pasoh sub-precincts)

- Little India (Serangoon Road corridor, Race Course Road)

- Kampong Glam (Arab Street, Bussorah Street, Haji Lane)

- Joo Chiat / Katong (East Coast corridor)

- Emerald Hill / Cairnhill (CCR, predominantly residential conservation)

Beyond these gazetted areas, some shophouses in Geylang, Serangoon, and Balestier fall under conservation categories but at lower intensities. The conservation status restricts what can be done to the exterior — facades, roofs, five-foot ways, and key internal structural elements must be preserved — but allows substantial internal renovation. This makes shophouses genuinely adaptable assets: refurbished to F&B use, boutique hotels, co-working spaces, or premium retail.

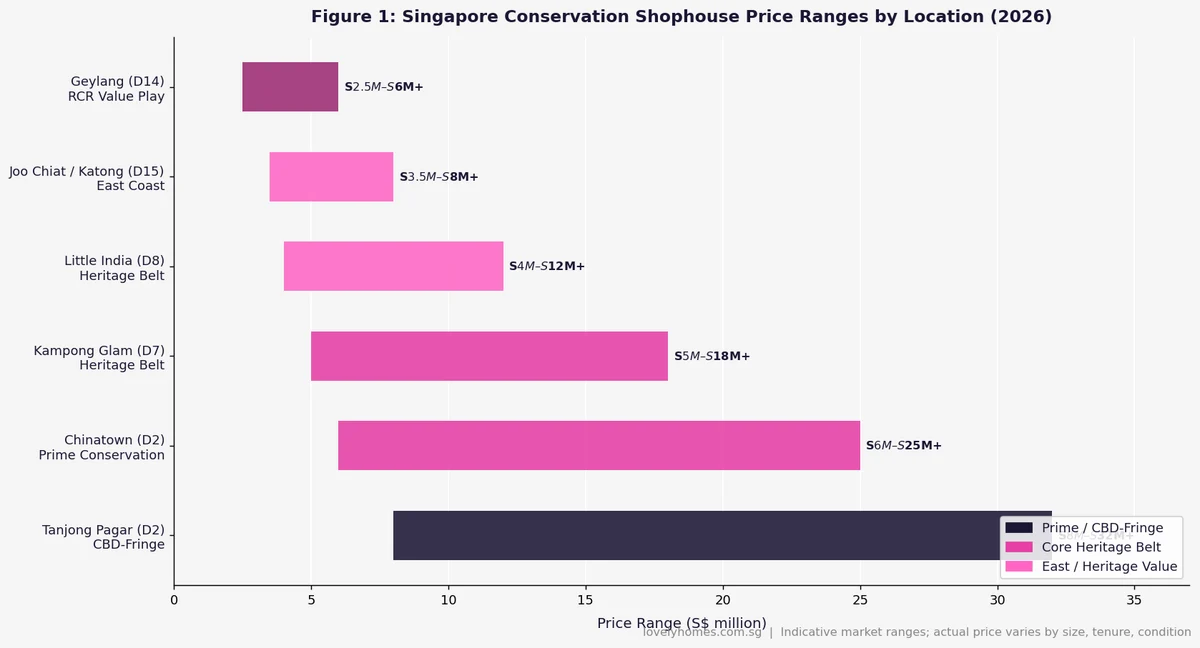

Price Ranges by Conservation Area (2026)

The price gap between precincts is substantial. Tanjong Pagar shophouses — proximity to the CBD, high-end F&B demand, international appeal — trade at S$8M–S$32M+ for larger or corner units. Chinatown prime streets (Club Street, Neil Road, Duxton Hill) can reach S$25M for a sizeable corner unit. Kampong Glam and Little India trade at more accessible entry points (S$4M–S$18M), with strong tourist and lifestyle tenant demand. Joo Chiat remains attractive for investors seeking yield over prestige — units there trade at S$3.5M–S$8M and attract strong F&B, wellness, and boutique retail tenants.

Rental Yields and How They Compare

Shophouses with a commercial ground floor tenanted by F&B, retail, or lifestyle operators typically generate gross yields of 3.5–4.5% — higher than most private residential condos and competitive with industrial units when you factor in capital appreciation. Mixed-use shophouses (where the upper floors are residential) yield slightly less (2.8–3.5%) because residential rents per sqft are lower than prime commercial. The attraction of shophouses lies not just in current yield but in the scarcity premium: URA does not permit new conservation shophouses to be built, and the total stock is finite. Capital appreciation over 10- and 20-year periods has consistently outperformed OCR residential condos in the same time frames, according to industry data.

The No-ABSD Advantage

This is the single most compelling reason property investors look at shophouses. Under Singapore’s ABSD regime, commercial property is entirely excluded from the ABSD count. A Singapore Citizen who already owns a private condominium would normally pay 20% ABSD on a second residential purchase. On a S$6M shophouse, that would amount to S$1.2M — which simply does not apply. The BSD still applies on the shophouse purchase at the standard BSD scale, but the ABSD zero is a substantial advantage.

The same principle applies to foreigners: a non-resident foreigner buying a Singapore residential property pays 60% ABSD. Buying a commercial shophouse? Zero ABSD. For foreign investors with capital to deploy in Singapore real estate, prime commercial shophouses have become a preferred structure precisely because of this ABSD exemption. For a full breakdown of ABSD and how it affects different buyer profiles, see our ABSD Singapore 2026 Complete Guide.

Conservation Rules — What You Can and Cannot Do

Before purchasing a shophouse, investors must understand exactly what URA’s conservation guidelines permit:

| Element | Permitted | Restricted / Prohibited |

|---|---|---|

| Facade | Restoration, repainting in period-appropriate colours | Alteration of external profile, removal of ornamental features |

| Five-Foot Way | Public pedestrian access must be maintained | Enclosure or privatisation of the five-foot way |

| Internal Layout | Extensive alteration with Written Permission; floor plan changes | Removal of original load-bearing walls without approval |

| Roof | Replacement of roof tiles in original style; skylights in rear | Raising roof height or changing roof profile |

| Extensions | Rear extensions with URA approval and setback compliance | Front extensions, significant height increases |

| Use Change | Change of use with planning permission (e.g. residential to hotel) | Uses incompatible with conservation area character |

The practical implication: internal renovations and fit-outs can be comprehensive — new MEP systems, open-plan ground floors, boutique hotel conversions, co-working fit-outs — but all external work requires URA’s Written Permission. A qualified architect familiar with conservation guidelines is essential for any significant Additions and Alterations (A&A) works.

Financing a Shophouse Purchase

Shophouse financing differs meaningfully from residential mortgage financing:

- Commercial property loans (not housing loans) apply — typically from the same major Singapore banks but under different terms. Some banks classify mixed-use shophouses as commercial for loan purposes.

- Loan-to-Value (LTV): Most banks will lend up to 80% LTV on pure commercial shophouses. For mixed-use (residential upper floors), some banks apply a blended LTV of 70–75% depending on their internal classification. Unlike residential mortgages, there is no HDB or MAS-mandated minimum LTV floor for commercial — terms are at the bank’s discretion.

- TDSR applies — the 55% Total Debt Servicing Ratio applies to shophouse purchases as it does to all Singapore property financing. You must demonstrate sufficient income to service the loan.

- Loan tenure: Typically 25–30 years, but some banks cap shophouse loans at 20–25 years, particularly for older buildings where remaining structural life is a concern.

- Interest rates: Shophouse commercial loans are generally priced at SORA + a margin, typically 1.5–2.5% margin, resulting in effective rates of 3.5–4.5% in the current environment — higher than residential mortgage rates.

- CPF cannot be used to fund a shophouse purchase. The 20% downpayment (assuming 80% LTV) and all BSD/legal costs must be in cash or business funds.

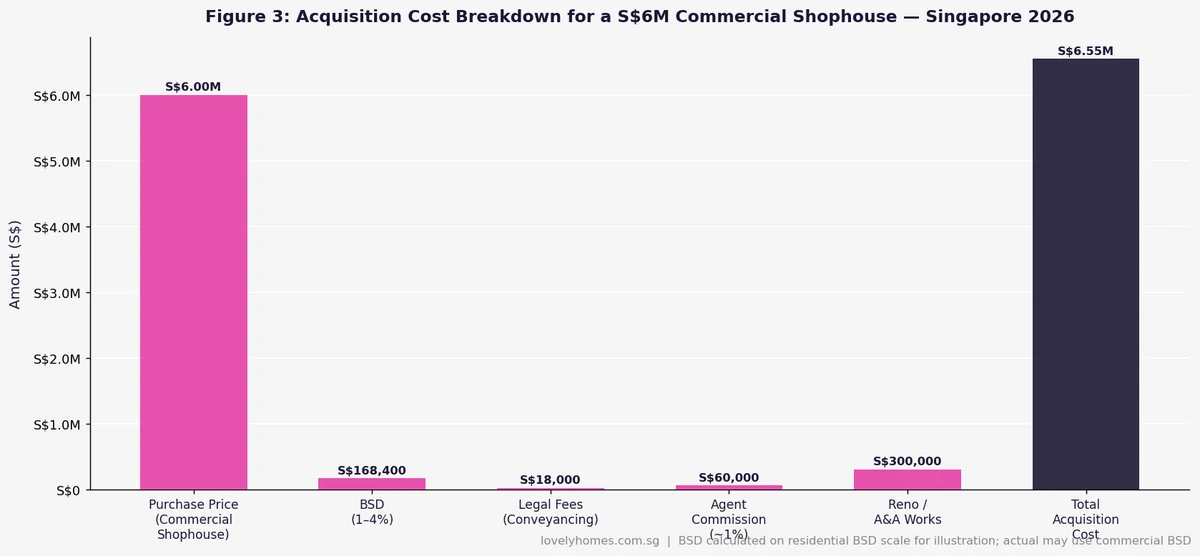

Worked Example — Buying a S$6M Joo Chiat Shophouse

Mr Tan is a Singapore Citizen who already owns a private condominium in Bishan (his principal residence). He wishes to acquire a 2.5-storey intermediate shophouse on East Coast Road, Joo Chiat, for S$6,000,000. The shophouse has a commercial ground floor (approx. 800 sqft) and two residential upper floors (approx. 1,200 sqft each). Tenure is 999-year leasehold from 1840 (effectively freehold in practice).

| Cost Item | Amount | Notes |

|---|---|---|

| Purchase Price | S$6,000,000 | Agreed with seller |

| BSD (approx.) | S$168,400 | 1%/2%/3%/4%/5%/6% progressive on S$6M |

| ABSD | S$0 | Commercial property — ABSD does not apply |

| Legal Fees (buyer) | ~S$18,000 | Conveyancing for commercial transaction |

| Agent Commission | ~S$60,000 | Typically 1% of price (negotiable) |

| A&A / Renovation | ~S$300,000 | Commercial GF fit-out + residential refresh |

| Total Acquisition Cost | ~S$6,546,400 | Before financing costs |

Financing: Mr Tan arranges a commercial property loan at 80% LTV — borrowing S$4,800,000 at SORA + 1.8% (approximately 3.8% effective rate, 25-year term). Monthly instalment: approximately S$25,000/month.

Income: Ground floor (commercial): S$8,000/month from an F&B tenant. Upper floors (residential): S$6,500/month combined from two tenants. Total: S$14,500/month gross rent.

Net position: Gross yield: 14,500 × 12 / 6,000,000 = 2.9%. After property tax (~S$7,200/year on residential NOO + 10% commercial AV), maintenance, and occasional vacancy, net yield settles at approximately 2.2–2.5%. The real case rests on capital appreciation — Joo Chiat shophouses have seen strong transactional demand and supply scarcity since 2021, with industry figures showing 15–25% value growth over 5-year periods in prime Joo Chiat streetscapes.

Key Risks and Due Diligence Checklist

Shophouse investment is not without risk. Buyers must assess:

- Structural condition: Conservation buildings are old. An independent building survey by a professional engineer (PE) is essential before purchase. Termite damage, foundation settlement, and roof condition are the most common issues.

- Encumbrances: Check the SLA title search thoroughly — some shophouses carry restrictive covenants, outstanding charges, or right-of-way easements that affect use and redevelopment potential.

- Rent roll and tenant quality: Verify actual rent, lease term, security deposit held, and tenant’s business licence (particularly for F&B tenants — NEA and SFA licences must be current).

- URA approval history: Check whether prior owners obtained Written Permission for any works. Unauthorised structures must be regularised or removed — at the buyer’s cost.

- Zoning: The URA Master Plan zoning determines permitted uses. Most shophouses are zoned Commercial or Commercial & Residential — but some edge-area shophouses have mixed zoning that restricts certain business activities.

- Tenure and title: 999-year shophouses are near-equivalent to freehold for practical purposes, but verify the exact commencement date and remaining lease (e.g. a shophouse on a 999-year lease commencing 1840 has approximately 813 years remaining as of 2026).

Summary Table — Shophouse vs Residential Condo Investment (2026)

| Parameter | Conservation Shophouse | Private Residential Condo |

|---|---|---|

| ABSD (2nd property, SC) | S$0 | 20% of price |

| Entry Price Range | S$3.5M–S$32M+ | S$600K–S$5M+ (OCR to CCR) |

| Gross Yield | 2.5–4.5% | 2.6–3.8% |

| Tenure | Mostly 999yr/freehold | Mix: 99yr, 999yr, freehold |

| CPF Eligible | No | Yes (SC/PR) |

| Financing LTV | Up to 80% (commercial loan) | Up to 75% (housing loan) |

| Property Tax | 10% (commercial) + NOO residential | NOO rates: 12–36% |

| Supply Constraint | Absolute — no new stock possible | Ongoing GLS supply adds new units |

| Conservation Constraints | External alteration restricted; URA WP required | Subject to strata by-laws only |

What Might Come Next for Singapore Shophouses

The shophouse market has been resilient through multiple cooling-measure cycles precisely because it sits outside the residential ABSD framework. Looking ahead:

- Demand remains structurally strong from family offices and ultra-high-net-worth individuals (UHNWIs) who find 60% ABSD on residential property prohibitive but can access shophouses without that burden.

- The URA 2023 Master Plan has not significantly changed shophouse zoning — conservation areas remain designated, and no new shophouse supply is on the horizon.

- F&B and wellness operators remain the most active commercial tenants, drawing on Singapore’s strong food culture and tourist footfall in heritage precincts.

- Risk to watch: If the Government were ever to extend ABSD to commercial property acquisitions (speculative and without current policy indication), shophouse demand from the residential-ABSD-averse investor class would moderate significantly. This is a tail risk — not current policy — but worth monitoring.

Frequently Asked Questions

Can foreigners buy Singapore shophouses?

Yes — commercial shophouses may be purchased by foreigners and foreign entities without ABSD, as they fall outside the Residential Property Act’s restrictions on foreign ownership of residential property. However, if a shophouse has residential upper floors (mixed-use), the Residential Property Act may apply to those floors, requiring SLA approval for foreign ownership of the residential portion. In practice, most investors purchasing mixed-use shophouses hold the property through a Singapore-incorporated company or structure it commercially. Always obtain qualified legal advice on the exact SLA classification of any shophouse before committing to purchase.

How much rental income can I earn from a S$6M shophouse?

At indicative gross yields of 2.5–4.5%, a S$6M shophouse generates approximately S$150,000–S$270,000 in gross annual rental income (S$12,500–S$22,500/month). The actual figure depends on the tenant mix, lease terms, and whether the commercial ground floor is currently tenanted. Top-quality F&B tenants in prime Chinatown or Tanjong Pagar shophouses have been known to pay S$18,000–S$25,000/month for a ground floor alone. Deduct property tax, maintenance, insurance, and occasional vacancy to arrive at net income. Rental income is taxable at your marginal personal income tax rate (for individual owners) or corporate tax rate (for companies), with allowable expense deductions including property tax, interest, depreciation, and repair costs.

What is the difference between a conservation shophouse and a non-conservation shophouse?

A conservation shophouse has been gazetted by URA under the Planning Act as a conservation building. This means it is legally protected — demolition is prohibited, and any external alterations require URA’s Written Permission. In return, conservation shophouses carry significant cachet and scarcity value that non-conservation shophouses do not. Non-conservation shophouses (sometimes called “walk-up” shophouses) can be found in areas like Geylang or parts of Balestier where URA conservation designation does not apply. These can be demolished and redeveloped within the planning parameters, which may offer more flexibility — but they lack the heritage premium that conservation status confers. Most of the market premium and investor demand is concentrated in gazetted conservation shophouses.

Can I convert a shophouse into a boutique hotel?

Yes — change of use from commercial/residential to hotel use is possible with the relevant planning approvals. You need URA Written Permission for the change of use (which involves demonstrating the proposal meets conservation guidelines for the external treatment), Singapore Tourism Board (STB) licensing for hotel operation, and compliance with fire safety regulations from SCDF. Several conservation shophouses in Chinatown and Kampong Glam have been successfully converted into boutique hotels with 4–12 rooms, commanding premium nightly rates. The conversion capex is significant — typically S$400,000–S$800,000+ depending on the extent of works — but successful boutique hotel operators have demonstrated gross revenue yields well above standard residential tenancy.

What is Seller’s Stamp Duty on shophouses?

Singapore’s Seller’s Stamp Duty (SSD) applies only to residential property. Commercial shophouses (pure commercial GF + upper floors) are not subject to SSD — you can sell at any time without a holding-period penalty. This is another advantage over residential investment properties, where SSD of 4% (sold within 1 year), 3% (within 2 years), or 2% (within 3 years) of purchase can erode gains on short-to-medium holds. The SSD exemption makes shophouses attractive for investors who may need liquidity flexibility. For mixed-use shophouses with residential upper floors, seek specific legal advice on whether the residential SSD applies to the residential portion of the transaction value.

How do I find out the URA conservation grade and permitted uses of a specific shophouse?

The URA SPACE map portal shows planning parameters, conservation categories, and approved use for every plot in Singapore. Enter the address or street name to view the URA Master Plan zoning, GPR, and conservation designation. The SLA’s INLIS (Integrated Land Information Service) provides detailed title search information including tenure, encumbrances, and registered easements. For the conservation guidelines specific to your shophouse’s style and location, the URA Conservation Guidelines publications (available on URA’s website) set out exactly what is and is not permitted. Always engage a qualified architect and conveyancing lawyer familiar with conservation properties before committing to any shophouse transaction.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Tax 2026: Complete Guide for Homeowners and Investors

- Rental Income Tax Singapore 2026: Complete IRAS Guide for Landlords

- Rental Yield Singapore 2026: District-by-District Guide for Property Investors

- Singapore Landed Property Buying Guide 2026: Terrace, Semi-D, Bungalow and GCB

- Seller’s Stamp Duty Singapore 2026: Rates, Holding Periods and Exemptions

- Singapore Prime District Property Guide 2026: D9, D10 and D11 Buyer’s Guide

Disclaimer: This guide is for general information only and does not constitute legal, financial, or investment advice. Shophouse prices, rental yields, and financing terms are indicative and subject to market conditions. URA conservation guidelines, planning parameters, and BSD/ABSD rules are subject to change. Always engage a licensed conveyancing lawyer and qualified architect before any shophouse transaction or renovation. Verify all planning permissions and title information with the relevant authorities (URA, SLA, IRAS) before proceeding. Past capital appreciation is not indicative of future returns.

Click anywhere outside to close