Singapore Rental Tenant Rights Guide 2026: Deposits, Stamp Duty, Disputes and Your Legal Protections

- Tenancy agreements in Singapore are governed by contract law; there is no specific landlord–tenant statute equivalent to the UK’s Housing Acts. The key laws are the Conveyancing and Law of Property Act (Cap 61) and common law contract principles.

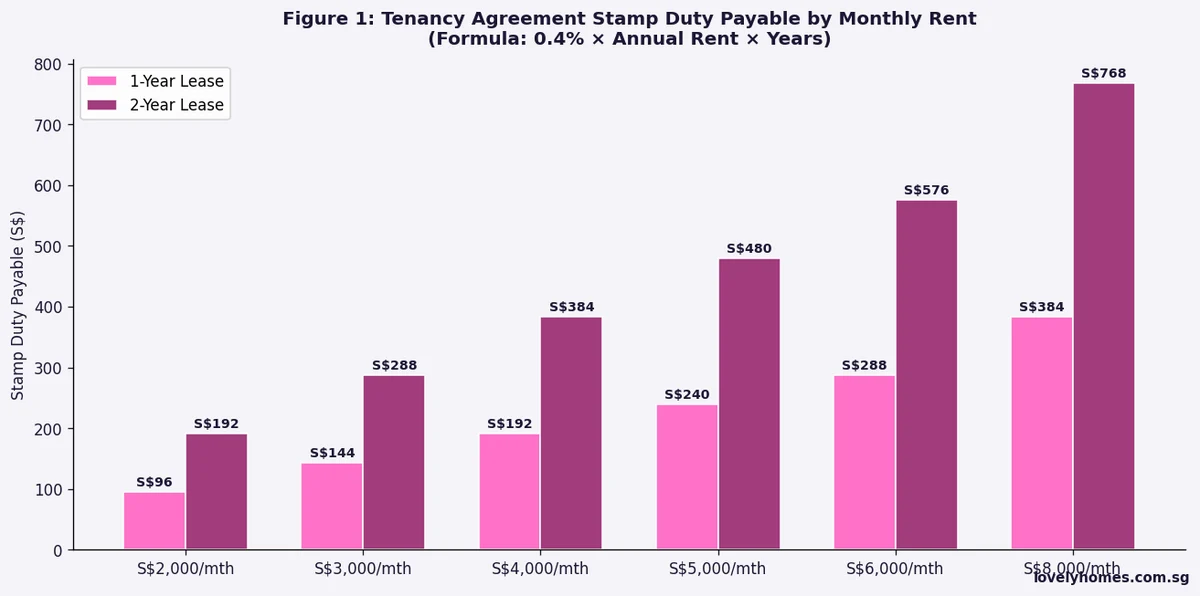

- Stamp duty on a tenancy agreement: 0.4% × annual rent × number of years. Due within 14 days of signing (or 30 days if signed overseas). Payable by the tenant unless otherwise agreed. IRAS administers this.

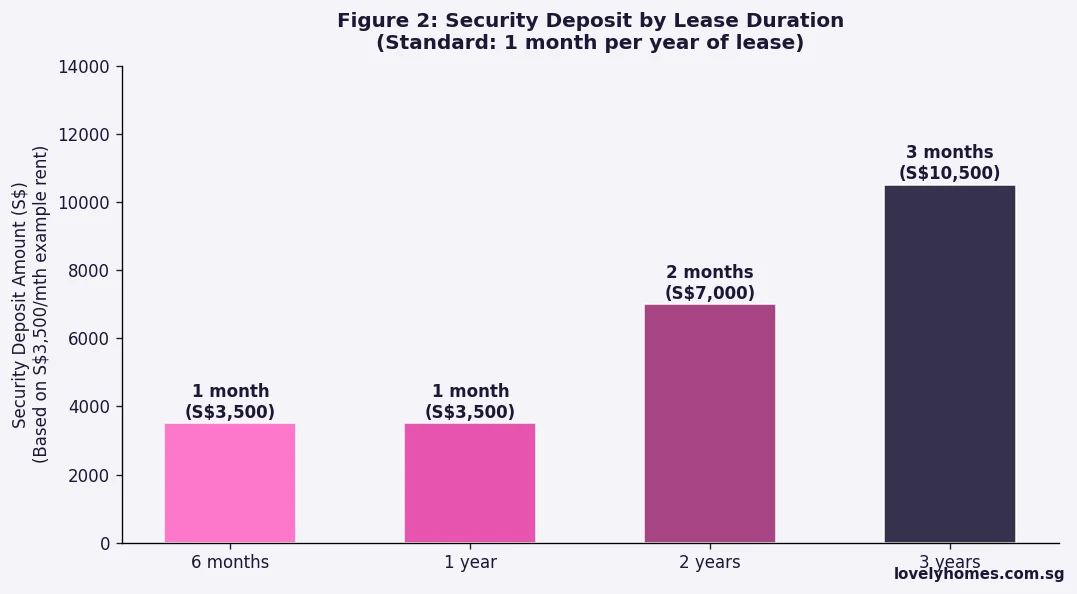

- Security deposit: typically one month per year of lease (a 2-year lease = 2 months’ deposit). Not regulated by law but standard market practice; must be returned within a reasonable period (commonly 14 days) after lease end.

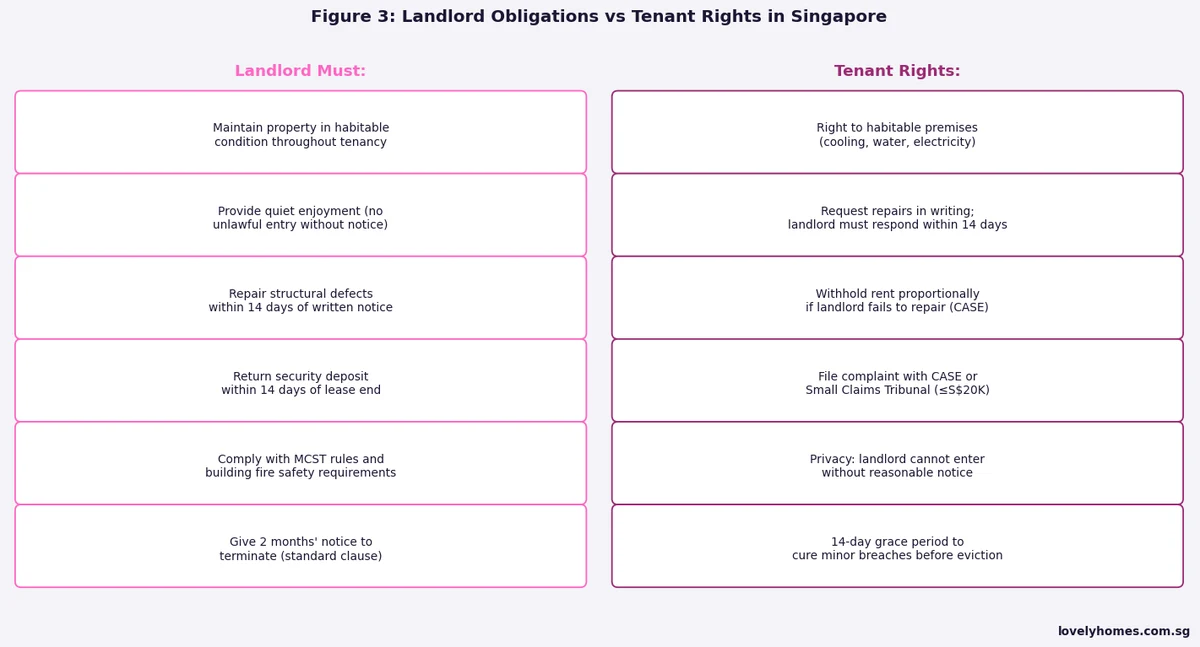

- Landlord obligations: maintain the property in a habitable condition, respect quiet enjoyment, repair structural defects within a reasonable timeframe.

- Tenant disputes: CASE (Consumers Association of Singapore) for mediation; the Small Claims Tribunal handles claims up to S$20,000; the General Division of the High Court handles larger claims.

- Subletting an HDB flat requires HDB approval and is subject to quota rules; subletting a private condo requires landlord and MCST consent.

- There is no “right to rent” certificate required in Singapore; however, foreign nationals must hold a valid pass (EP, S Pass, LTVP, etc.) to legally rent accommodation.

- From 2024, URA requires all private residential rentals to be listed at minimum 3 months’ duration (short-term rental of under 3 months is illegal for private homes).

Understanding Tenant Rights in Singapore’s Rental Market

Singapore’s private rental market is large — over 160,000 private residential units are estimated to be tenanted at any given time, housing a mix of Singapore Citizens and Permanent Residents who have not yet purchased their own home, Employment Pass and S Pass holders, and long-term visitors. Yet unlike many jurisdictions, Singapore has no unified residential tenancy act. Tenant protections derive from general contract law, the Conveyancing and Law of Property Act (Cap 61), and, for HDB flat rentals, specific HDB regulations.

This guide explains what tenants are entitled to, what landlords are obligated to do, how security deposits work, how to stamp a tenancy agreement correctly, and how to resolve disputes — from the Consumer Association of Singapore (CASE) all the way to the Small Claims Tribunal.

The Tenancy Agreement: What It Must Cover

A tenancy agreement (TA) is a legally binding contract between landlord and tenant. While there is no statutory form, a well-drafted TA for a Singapore private property should cover: the property address and description, the lease commencement and expiry dates, the monthly rent and payment date, the security deposit amount, permitted use (residential only), utility responsibility, pet policy, maintenance obligations, break clause (if any), diplomatic clause (if any), and the landlord’s and tenant’s notice periods.

The TA should be signed by both parties and two witnesses. The tenant then has an obligation — though in practice the cost is often borne by the tenant — to stamp the agreement with IRAS within 14 days. The stamp duty formula is straightforward: 0.4% × annual rent × number of years. For a S$4,000/month flat on a 2-year lease, that is 0.004 × S$48,000 × 2 = S$384. Failure to stamp does not render the agreement void, but it cannot be used as evidence in court until it is stamped with any late penalty paid.

A diplomatic clause (also called a break clause) allows a tenant to terminate the lease early — typically after the first 12 months on a 24-month lease — by giving 2 months’ written notice. This clause is especially important for expatriates on employment passes, whose work assignment may change. Landlords will often resist including it but will accept a modest rent premium in exchange.

Security Deposits: Your Rights and How They Work

Singapore law does not prescribe a maximum security deposit. Market practice has settled on one month’s deposit per year of lease (a 2-year lease = 2 months, a 3-year lease = 3 months). At S$3,500/month, a 2-year lease means the tenant hands over S$7,000 upfront before even taking the keys.

The landlord holds this deposit throughout the tenancy and must return it at lease end, typically within 14 days, less any legitimate deductions. Legitimate deductions include unpaid rent, cost of repairing damage beyond fair wear and tear, and unpaid utility bills that were the tenant’s responsibility. Fair wear and tear is a critical concept: fading of paint, worn carpets, and minor scuffs to walls from normal use are NOT deductible. A hole in a wall, a broken fitting, or a pet scratch on a wooden floor may be deductible.

If a landlord deducts more than is justified, or refuses to return the deposit, the tenant may file a claim at the Small Claims Tribunal (SCT) for amounts up to S$20,000, or the Magistrate’s Court for larger claims. The SCT is accessible, relatively fast (typically resolved within 2–3 months) and does not require legal representation. CASE also offers mediation services — useful if both parties prefer to avoid the tribunal.

Landlord Obligations Under Singapore Law

Singapore landlords have several implied obligations that exist regardless of what the tenancy agreement says, derived from common law and the Conveyancing and Law of Property Act:

Quiet enjoyment. The landlord must not interfere with the tenant’s reasonable use of the property. This means no entering without advance notice, no removing appliances mid-lease, no harassing behaviour, and no changing locks without consent.

Habitability. While Singapore law does not define a statutory minimum standard, common law implies that the property must be fit for residential use at commencement. A landlord who knowingly rents a property with a serious defect (e.g., a collapsed ceiling, non-functioning plumbing, pest infestation) may be liable for breach of the implied covenant of fitness.

Structural repairs. Landlords are generally responsible for structural maintenance — roofing, major plumbing, external walls. Tenants are typically responsible for minor repairs and maintenance of fixtures they use daily. The tenancy agreement should specify this division clearly. Where it is silent, the party that caused the damage is responsible.

Notice before entry. There is no statutory notice period in Singapore, but the general expectation — and what CASE recommends — is that landlords give at least 24–48 hours’ advance notice before entering, except in genuine emergencies (gas leak, burst pipe). Entering without notice may constitute a breach of the quiet enjoyment covenant.

Resolving Disputes: CASE, SCT and Beyond

When landlord–tenant relations break down, Singapore offers a tiered resolution pathway that tenants should be aware of:

Step 1 — Written notice. Always put complaints in writing (email is sufficient). A clear written record of when a defect was reported, what was requested, and whether the landlord responded is critical evidence for any later tribunal proceeding. Give the landlord a reasonable timeframe — typically 14 days for non-urgent repairs — and state what action you expect.

Step 2 — CASE mediation. The Consumers Association of Singapore offers free and low-cost mediation for landlord–tenant disputes. CASE mediators are neutral and their service is voluntary (both parties must agree to participate). Mediation outcomes, if reached, are binding and can be filed with the court as a consent order. CASE’s contact is 1800 773 3163 or case.org.sg.

Step 3 — Small Claims Tribunal (SCT). For monetary claims up to S$20,000, the SCT (part of the State Courts) is the primary forum. Filing is done online via the State Courts e-Services portal. Both parties appear in person; legal representation is generally not permitted at the SCT, making it accessible for self-represented claimants. Filing fees are modest (S$10–S$30 depending on claim amount).

Step 4 — Magistrate’s Court or District Court. For claims above S$20,000 (up to S$60,000 for Magistrate’s, up to S$250,000 for District Court), a more formal court process applies. Legal representation becomes advisable at this stage.

Renting HDB Flats: Additional Rules That Apply

HDB flats are subject to additional rental regulations that do not apply to private property. Key rules as at 2026 include: the whole flat may only be rented out after the 5-year Minimum Occupation Period (MOP) has been fulfilled (the MOP clock starts from the date the keys are collected); the owner must obtain HDB’s prior approval before renting out the entire flat; renting out individual rooms does not require HDB approval for SC/PR owners of flats that have met MOP, but the Ethnic Integration Policy (EIP) quota still applies to the composition of occupants in the flat.

HDB’s Non-Citizen Quota limits the proportion of non-citizen tenants (excluding Malaysian nationals) at both the neighbourhood and block level. A block may have no more than 8% of non-citizen non-Malaysian tenants; the neighbourhood cap is 5%. Landlords are responsible for checking quota headroom before committing to a non-citizen tenant — failure to comply results in HDB enforcement action against the owner, not the tenant.

Worked Example: Ms Lim’s Dispute over Her Security Deposit

Ms Lim, a Singapore Permanent Resident, rented a 2-bedroom apartment in D15 (East Coast) at S$3,800/month on a 2-year lease from January 2024 to December 2025. She paid a S$7,600 security deposit (2 months) and S$152 in stamp duty (0.4% × S$45,600 × 2).

At lease end in December 2025, the landlord deducted S$3,200 from the deposit, citing: (a) repainting of all walls — S$1,800; (b) replacement of kitchen tap — S$150; (c) professional carpet cleaning — S$400; (d) replacement of a cracked bathroom basin — S$850. Ms Lim disputed items (a) and (c), arguing the walls had only minor normal-use scuffs (fair wear and tear) and that carpet cleaning was the landlord’s routine maintenance cost.

Outcome: CASE mediation ruled that repainting of all walls after a 2-year lease was standard fair wear and tear unless there was evidence of deliberate damage; the landlord was directed to refund S$1,800 for repainting. The carpet cleaning deduction of S$400 was upheld because the tenancy agreement expressly stated the tenant must return the premises in professionally cleaned condition. The tap (S$150) and basin (S$850) deductions were upheld as verifiable damage. Net outcome: Ms Lim received S$1,800 back, retaining a total refund of S$5,400 of the original S$7,600 deposit.

Why Knowing Your Tenant Rights Matters in 2026

Singapore’s rental market has tightened considerably since 2021, with median rents for private 2-bedroom units rising over 35% between 2021 and 2023. While rental rates have moderated since the 2023 peak — median rents for non-landed private property fell approximately 1.2% quarter-on-quarter in Q1 2026 per URA data — the total cost of renting remains elevated relative to pre-pandemic levels. At the same time, vacancy rates in some sub-markets (notably CCR 1-bedroom and 2-bedroom units) have risen as the expat population adjusts to hybrid work models and some employers reduce Singapore headcount.

In this environment, tenants are in a somewhat stronger negotiating position than during the 2022–2023 peak, and understanding your legal rights means you are less likely to accept unfair deductions from security deposits or sub-standard maintenance from landlords who rely on tenant ignorance. Equally, understanding what landlords are legally entitled to — and what the practical limits of your rights are — helps you navigate tenancy disputes without litigation where avoidable.

What Might Come Next: Calls for a Residential Tenancy Act

Speculation: Singapore’s property market commentators and some civil society groups have periodically called for a codified residential tenancy law — similar to what exists in the UK (the Housing Act), Australia (state-level residential tenancy acts) or New Zealand (the Residential Tenancies Act). Such a law would standardise notice periods, define maximum security deposit multiples, mandate habitability standards, and create an independent dispute resolution tribunal specialising in tenancy disputes.

As of mid-2026, no such legislation has been announced by the Ministry of National Development (MND) or the Ministry of Law. The government’s stated preference is to allow the market to self-regulate with CASE mediation and SCT as backstops. Tenants and landlords should continue to operate under the current common-law framework and ensure their tenancy agreements are comprehensive, clearly drafted and properly stamped.

Singapore Tenancy: Key Rules at a Glance

| Topic | Rule / Standard | Governing Body |

|---|---|---|

| Stamp duty on TA | 0.4% × annual rent × years; due 14 days from signing | IRAS |

| Security deposit | Market standard: 1 month per year of lease (no statutory cap) | Contract law |

| Minimum rental duration | 3 months for private residential (URA rule since 2024) | URA |

| HDB whole-flat rental | Post-MOP (5yr from key collection); HDB approval required | HDB |

| HDB room rental | SC/PR owner post-MOP; non-citizen quota (8% block/5% neighbourhood) | HDB |

| Quiet enjoyment | Landlord must give advance notice before entry (≥24hrs recommended) | Common law |

| Structural repairs | Landlord responsible; minor maintenance typically tenant’s responsibility | TA + common law |

| Security deposit return | Within 14 days of lease end; deductions must be itemised | Contract + CASE |

| Dispute resolution (small claims) | CASE mediation → Small Claims Tribunal (up to S$20,000) | CASE / State Courts |

| Subletting (private) | Requires landlord + MCST consent; not a tenant’s automatic right | TA + strata titles rules |

Frequently Asked Questions

Can a landlord increase rent mid-tenancy?

No. Once a tenancy agreement is signed and stamped, the rent is fixed for the lease term. A landlord cannot unilaterally increase rent mid-lease without the tenant’s written agreement. Any rent increase must be negotiated — typically at renewal time — and the tenant has the right to reject any increase and leave at the end of the existing lease term, provided correct notice is given.

Who is responsible for paying the stamp duty — landlord or tenant?

IRAS rules are silent on who bears the cost — it is a matter of agreement between the parties. Market custom in Singapore is that the tenant pays the stamp duty. However, for landlord-furnished premium units, it is sometimes split or borne by the landlord. The obligation to ensure stamping happens within 14 days rests on both parties: if the agreement is not stamped it cannot be used in court, putting both at risk. Practically, the tenant typically stamps the agreement immediately upon receiving it.

What happens if the landlord sells the property during the tenancy?

In Singapore, a properly registered tenancy (where a caveat has been lodged by the tenant with SLA) binds the new owner. The new owner steps into the landlord’s shoes and must honour the tenancy agreement until its natural expiry. If the tenancy was not caveated, the position depends on whether the new buyer had constructive or actual notice of the tenancy. Tenants in high-value properties or long leases should consider instructing a solicitor to lodge a caveat to protect their leasehold interest.

Can a landlord evict a tenant without a court order in Singapore?

No. Self-help eviction — changing locks, removing a tenant’s belongings, cutting utilities to force a tenant out — is illegal in Singapore. A landlord who believes a tenant has breached the tenancy agreement must apply to the court for a Writ of Distress (for unpaid rent) or commence civil proceedings for possession. Unlawful eviction can expose the landlord to damages claims. Tenants who are physically locked out or whose utilities are cut off against their will should report the matter to the police and contact CASE immediately.

Is there a limit on how much a landlord can deduct from the security deposit?

There is no statutory cap on deductions — a landlord can deduct the entire deposit if verifiable damages and unpaid rent justify it. However, deductions must be reasonable, itemised, and documented (receipts, photographs, contractor quotes). Deductions for fair wear and tear — normal deterioration of paint, carpets, and furnishings through ordinary use over the lease term — are not legally defensible. The key test is whether the damage goes beyond what would reasonably be expected from a tenant in ordinary use, based on the property’s age and the duration of the tenancy.

Can I sublet a room in my rented condo without the landlord’s permission?

Almost certainly not. Most standard Singapore tenancy agreements for private property prohibit subletting without the landlord’s prior written consent. Subletting without consent is a breach of the tenancy agreement and can be grounds for termination. Even with landlord consent, you should check whether MCST by-laws (if you are in a strata development) impose any additional restrictions on occupation numbers or subletting. Short-term subletting on platforms like Airbnb for less than 3 months is illegal for private residential property under URA rules.

What is the diplomatic clause and how do I invoke it?

A diplomatic clause (break clause) allows a tenant to terminate a lease early — typically after the first 12 months of a 24-month lease — by giving 2 months’ written notice. It must be explicitly included in the tenancy agreement; it does not arise automatically. To invoke it, you send the landlord a written notice stating your intention to terminate and the proposed last day of tenancy, ensuring the notice complies exactly with the clause’s terms (timing, form, mode of delivery). You remain liable for rent through the 2-month notice period. The security deposit is refunded normally, subject to standard deduction rules.

Related Articles

- Singapore Private Property Rental Guide 2026: How to Rent Out Your Condo

- Singapore Property Agent Guide 2026: CEA Rules, Commissions and Your Rights

- Singapore Home Loan Refinancing Guide 2026

- Singapore Property Conveyancing Guide 2026

- Singapore HDB Flat Eligibility Guide 2026

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer: This article is for general informational and educational purposes only. It does not constitute legal advice. Singapore’s landlord–tenant law is based on common law principles and contract, not a codified residential tenancy statute; outcomes in any dispute depend on the specific terms of the tenancy agreement and the facts of the case. Tenants and landlords with specific disputes should seek legal advice from a qualified Singapore solicitor. Stamp duty obligations should be verified with IRAS (iras.gov.sg). HDB rental rules should be verified directly with HDB (hdb.gov.sg). CASE mediation can be accessed at case.org.sg or by calling 1800 773 3163.