Thomson-East Coast Line Property Guide Singapore 2026: Best Districts & Investment Opportunities

The Thomson-East Coast Line property guide Singapore 2026 is your complete reference for buying, investing, or upgrading along Singapore’s newest MRT trunk line. The TEL, operated by SMRT under the Land Transport Authority’s network, is the first line to run from the deep north of Singapore — Woodlands North — all the way to the eastern seaboard at Sungei Bedok, connecting eight of Singapore’s twenty-eight districts in a single continuous line. For property buyers, the TEL represents both a connectivity premium already priced into northern and eastern districts and a genuine price-growth runway in catchment areas where development is still maturing.

Quick Answer — TEL Property in 2026 at a Glance

- The TEL runs 43 stations across 5 phases; all phases are operational as of November 2024

- North segment (D25–D26): entry prices from S$1.2M–S$1.8M for 1–2 bedroom condos; gross yields 3.8–4.3%

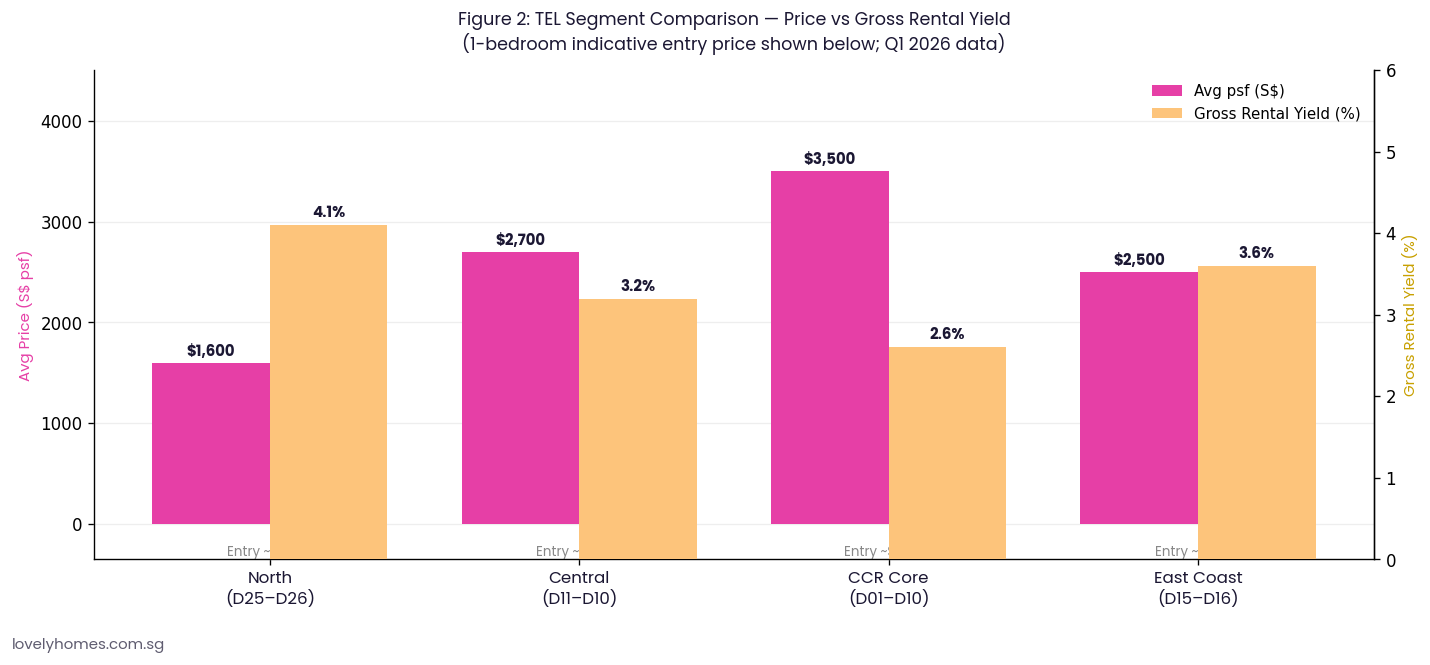

- Prime central segment (D10–D11): average transaction prices S$2,900–S$3,800 psf; yields compress to 2.5–3.2%

- East Coast segment (D15–D16): sweet spot for yield investors — S$2,200–S$2,600 psf with yields 3.5–4.0%

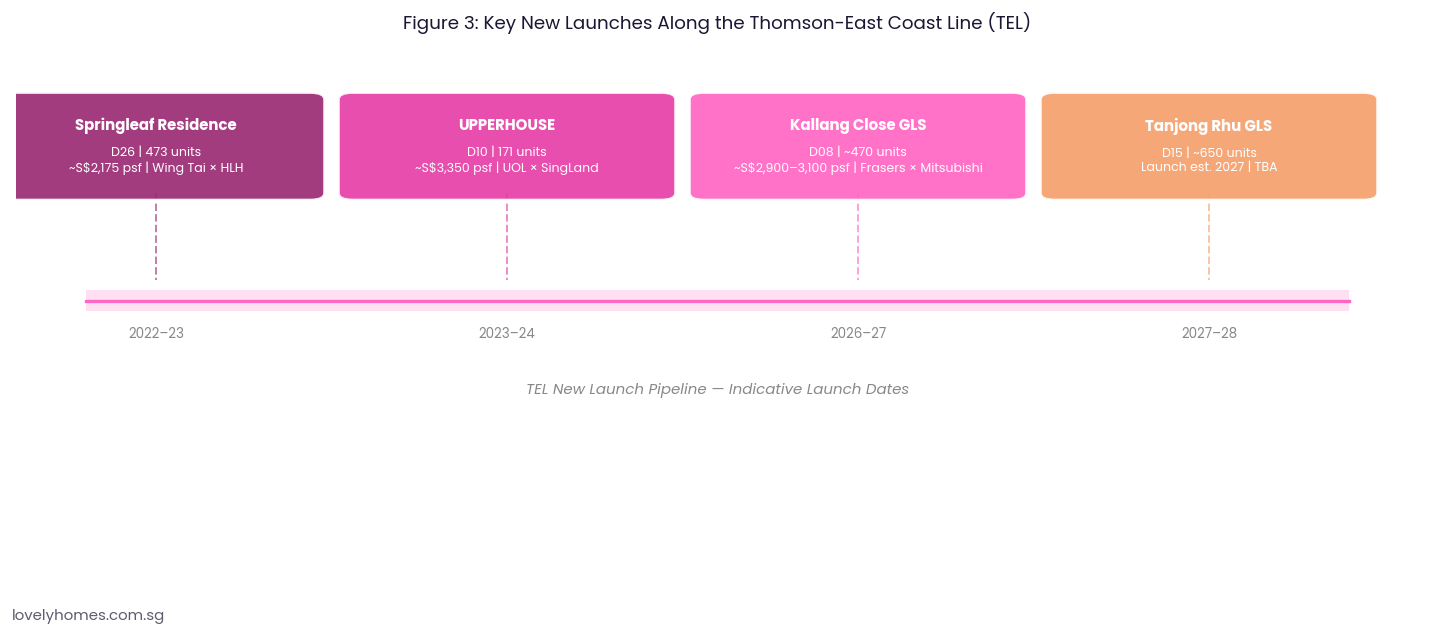

- Three active new launches along the TEL corridor in 2026: Springleaf Residence (D26), UPPERHOUSE (D10), and the Kallang Close GLS

- The TEL’s opening in D15 (Katong, Marine Parade, Tanjong Rhu) added a 6–12% price premium to catchment condos within 500m, per URA caveat analysis

- Investors should note: TEL East Coast properties fall under the Rest of Central Region (RCR) and Core Central Region (CCR) frameworks for ABSD and LTV calculations

- The Tanjong Rhu GLS site (D15) — first new land release in the area in 28 years — signals major upcoming supply in a historically undersupplied waterfront node

What Is the Thomson-East Coast Line?

The Thomson-East Coast Line is the sixth MRT line on Singapore’s Mass Rapid Transit network. Planned by the Land Transport Authority and built in five phases, the TEL broke ground in 2015 and reached full network connection in November 2024 when the final phase linking Bedok South to Sungei Bedok opened, completing the 43-station, approximately 43-kilometre corridor. Unlike older lines that were retrofitted through existing urban fabric, the TEL was master-planned as a north-south-east spine: it reaches previously MRT-unserved residential catchments in Woodlands, Upper Thomson, and the East Coast, while also adding new stations in the premium central districts of Stevens, Napier, and Orchard Boulevard.

The LTA’s long-term transport planning has established a clear correlation between MRT station proximity and private residential price premiums. Researchers at the National University of Singapore’s Institute of Real Estate and Urban Studies have documented average premiums of 5–15% for private properties within 500 metres of a station, with new lines generating the strongest uplift in the two to three years around opening. The TEL’s staged opening created sequential pricing events across its catchments, and property investors who tracked the LTA’s construction timeline were able to position ahead of each phase.

The TEL in Five Segments: A Property Investor’s Map

For analytical purposes, the TEL’s 43 stations divide into five investment segments, each with distinct supply, pricing, and yield characteristics.

Segment 1 — The North (D25–D26): Woodlands to Springleaf

The northern anchor of the TEL serves Woodlands (D25) and Upper Thomson/Mandai (D26). This is the most affordable segment on the line, with median condo transaction prices in the S$1,300–S$1,800 psf range as of Q1 2026 (URA caveats). The key residential projects here are Woodlands-area condos such as The Woodleigh Residences and Canberra Crescent developments, alongside the more recent Springleaf Residence at Upper Thomson. Springleaf Residence — a Wing Tai Holdings and Hong Leong Holdings joint venture — launched at an average S$2,175 psf and achieved 92% sold at launch, validating strong homebuyer demand in the D26 corridor.

Investment fundamentals for the north segment: rental yields are the highest on the TEL, typically 3.8–4.3% gross for 1-bedroom and 2-bedroom units, driven by the presence of international school catchments (Woodlands International School, Singapore Sports School), and the Woodlands Regional Centre transformation under URA’s long-range master plan. Entry prices for 1-bedroom units start from approximately S$850,000–S$1,000,000, making this the most accessible entry point on the line for investors under S$1M. The Woodlands–Johor Bahru RTS Link, due to complete in end-2026, is an additional demand catalyst: cross-border workers commuting from Singapore to the Johor Bahru Bukit Chagar terminus will increasingly seek rental accommodation at or near Woodlands MRT.

Segment 2 — Upper Thomson to Caldecott (D20, D11): The Middle Ground

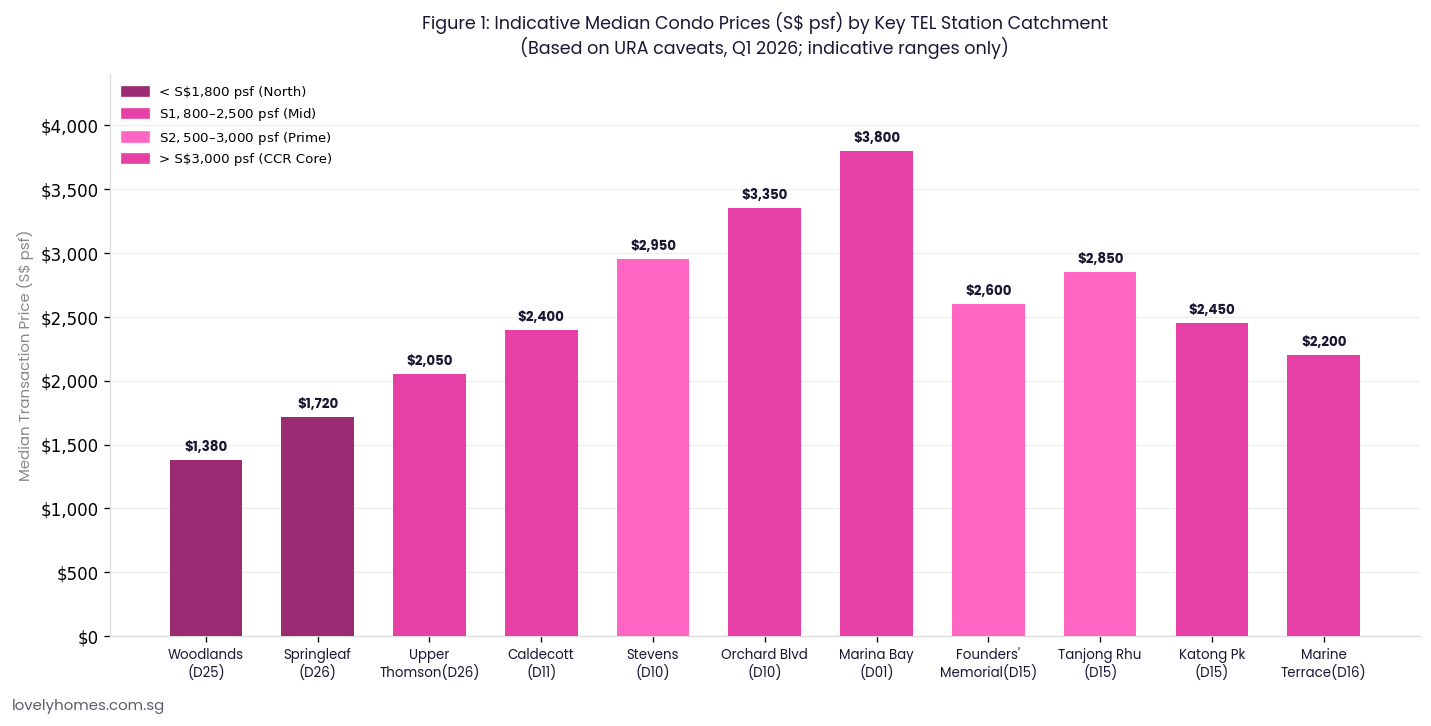

Between Springleaf and the Orchard stretch, the TEL passes through Upper Thomson Road, the Caldecott interchange (linking to the Circle Line), and Stevens (linking to the Downtown Line). This segment includes Districts 20, 11, and the western edge of D10. Caldecott and Stevens are immediately adjacent to premium private residential estates including Bukit Timah, Holland Road, and the Nassim/Tanglin clusters — traditionally among the most expensive residential districts in Singapore.

The Stevens station, in particular, serves as a gateway to the Good Class Bungalow belt in D10 and the UOL-SingLand UPPERHOUSE at Orchard Boulevard development (101 units, 99-year leasehold, average S$3,350 psf, launched 2024). The connectivity addition of the TEL here — bringing a direct one-seat ride from Stevens all the way to Marina Bay and the East Coast — solidified premium pricing in a corridor that was already well-served by car ownership. For buyers, the TEL has made D10–D11 properties accessible to a broader pool of non-car-owning tenants, improving rental sustainability for high-end CCR units.

Segment 3 — The CCR Core (D01–D10): Orchard to Marina Bay

The TEL’s central stations — Napier, Orchard Boulevard, Great World, Havelock, Outram Park (interchange), Maxwell, Shenton Way, and Marina Bay — traverse the very heart of Singapore’s Core Central Region. Median transaction prices in this segment range from S$2,900 psf (Havelock/Great World catchment) to S$3,800 psf (Orchard Boulevard environs), with top CCR addresses in Orchard exceeding S$4,500 psf. The key driver here is not yield — gross rental yields compress to 2.4–3.0% as capital values are elevated — but capital preservation and long-run appreciation in freehold or near-freehold assets.

The CCR core is where the ABSD differential matters most acutely. Foreigners buying in this segment pay 60% ABSD, which has materially shifted the buyer mix since April 2023 towards Singapore Citizens and PRs on investment purchases. URA Q1 2026 caveats show that CCR transactions remain below their 2021–2022 peak volumes, but median prices have held firm, suggesting that existing CCR owners are not distressed and are holding for long-term appreciation rather than selling at discounts.

Segment 4 — East Coast (D15): Katong to Marine Terrace

The TEL’s East Coast segment — from Tanjong Rhu to Marine Parade and Siglap — is arguably the most exciting investment corridor on the line in 2026. This is a historically low-supply, high-demand residential area. The East Coast has long commanded rental and lifestyle premiums driven by the concentration of international schools (SAS, CIS, UWCSEA East, EtonHouse), the East Coast Park, and a café-and-food-culture character that attracts young expatriate and local professional tenants. Before the TEL, the area had no MRT connectivity at all — residents relied entirely on buses and private transport. The arrival of Katong Park, Marine Parade, and Marine Terrace stations in 2023 was transformative.

URA caveat analysis shows that East Coast condos within 500 metres of the new TEL stations transacted at S$2,400–S$2,700 psf in Q1 2026, representing a 6–12% premium over comparable units further from the stations. Gross rental yields for 1-bedroom units in Katong and Marine Parade run at 3.5–4.1%, benefitting from high expatriate rental demand. The 2025 Tanjong Rhu GLS — the first government land sale in the area in 28 years — will eventually add supply, but the timeline to completion is 3–5 years, leaving the existing stock to absorb near-term rental demand.

Segment 5 — Far East (D16): Bedok to Sungei Bedok

The terminal segment, from Bedok South through Siglap, Bayshore, and Sungei Bedok, represents the TEL’s newest frontier. Bayshore Road — the subject of a significant GLS tender launched by the URA in March 2026, with a S$1.9–2.1B bid estimate and a 1,280-unit mixed-use integrated development — will be the anchor new launch for this segment. This site has MRT integration built into the development brief, meaning future residents will have a covered walk directly from their lobby to Bedok South MRT. The catchment here currently trades at S$1,900–S$2,300 psf, offering the best price-to-TEL-connectivity value on the entire line for medium-term investors who are comfortable with a 2–3 year supply wait.

Summary Table: TEL Segments at a Glance

| Segment | Districts | Median psf (Q1 2026) | Gross Yield | Entry 1BR (~S$) | Best For |

|---|---|---|---|---|---|

| North (Woodlands–Springleaf) | D25–D26 | S$1,300–1,800 | 3.8–4.3% | S$850K–1.0M | Yield-focused; RTS uplift play |

| Mid-North (Thomson–Caldecott) | D20–D11 | S$2,050–2,400 | 3.0–3.5% | S$1.2M–1.5M | Balanced; school proximity |

| CCR Core (Orchard–Marina Bay) | D01–D10 | S$3,000–3,800 | 2.5–3.0% | S$2.2M–3.5M | Capital preservation; prestige |

| East Coast (Katong–Marine Parade) | D15 | S$2,400–2,700 | 3.5–4.1% | S$1.5M–1.8M | Expat rental; lifestyle premium |

| Far East (Bayshore–Sungei Bedok) | D16 | S$1,900–2,300 | 3.6–4.0% | S$1.1M–1.4M | Medium-term upside; Bayshore GLS |

Worked Example: Comparing Two TEL Investment Scenarios

To illustrate how the TEL’s price geography affects investor outcomes, consider two hypothetical purchasers buying in April 2026, each with a S$1.8M budget for a 2-bedroom investment unit (Singapore Citizen, first private property, no ABSD).

Option A — East Coast (D15), near Marine Parade MRT: 2BR, 700 sqft at S$2,500 psf = S$1.75M. BSD payable to IRAS: ~S$55,600. Monthly mortgage (75% LTV, S$1.31M at SORA+0.75% = ~3.70%, 25 years): ~S$6,720. Monthly rental income at 3.7% gross yield: ~S$5,390. Net monthly cash flow (before management fee, property tax, sinking fund): −S$1,330 per month. Capital appreciation target: 4–6% per annum over a 7-year hold. Total return (conservative 4% p.a. appreciation + cumulative rental income): estimated IRR of approximately 8–10% over a 7-year hold.

Option B — North (D26), near Springleaf MRT: 2BR, 800 sqft at S$1,850 psf = S$1.48M. BSD payable to IRAS: ~S$43,000. Monthly mortgage (75% LTV, S$1.11M at 3.70%, 25 years): ~S$5,700. Monthly rental at 4.1% gross: ~S$5,060. Net cash flow: −S$640 per month (significantly better than Option A). Capital appreciation at a more conservative 3% p.a. over 7 years. IRR: approximately 7–9%, with a stronger monthly cash flow during the hold period. Option B also leaves S$320K of the budget unused, which could service emergencies or fund a second property later.

Neither option is inherently superior — the trade-off is between location prestige and rental resilience (Option A) versus cash-flow comfort and lower entry risk (Option B). Both outperform a typical fixed deposit or Singapore Savings Bond over a 7-year horizon on a total return basis, based on current market data.

Why the TEL Matters for Property Investors in 2026

Singapore’s MRT network has historically been the single most reliable infrastructure driver of residential price premiums. The TEL is unique in that it opened across a decade (2019–2024), meaning different catchments are at very different stages of the price-uplift cycle. The north segment is still absorbing the connectivity premium as the Johor Bahru RTS Link nears completion; the East Coast is in the early-mid stage of its premium maturation; and the CCR core stations are fully priced in. For investors, the implication is clear: the North and East Coast segments still offer the better forward-looking return profile relative to entry price.

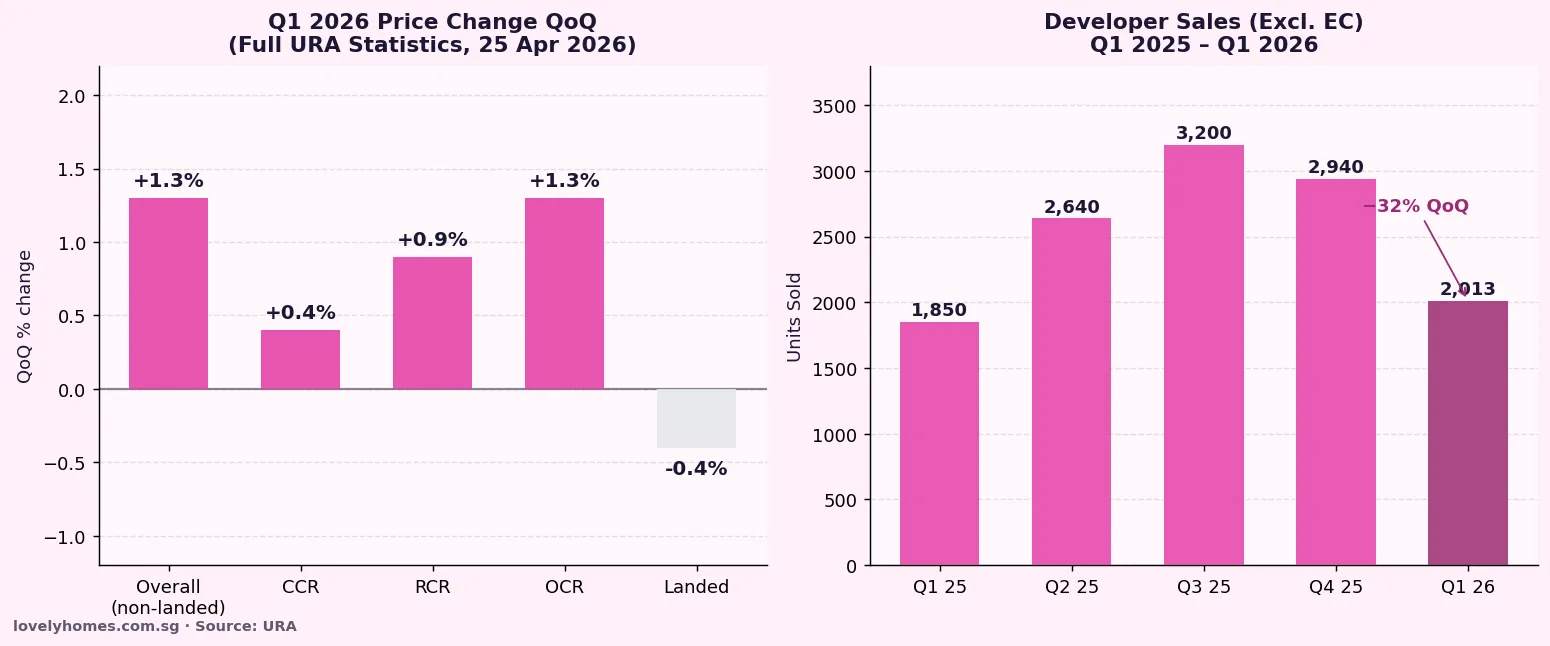

URA’s Q1 2026 full statistics (released 25 April 2026) showed that private residential prices rose 0.9% quarter on quarter, with the Rest of Central Region — which encompasses much of the East Coast TEL corridor — outperforming the Core Central Region in transaction volume. This divergence suggests that RCR properties, including East Coast condos, are currently absorbing more buyer demand than the premium CCR market, consistent with a pricing cycle where affordability-conscious buyers are moving down the price curve from CCR into RCR catchments along connective infrastructure like the TEL.

What Might Come Next Along the TEL

Looking forward, three developments warrant investor attention. First, the Bayshore Drive GLS (URA tender, closing July 2026) will be the defining new launch for the Far East segment. With 1,280 units and an MRT-integrated brief, the eventual project will set a new price benchmark for D16, potentially pushing neighbouring resale values upward in anticipation. Second, the Tanjong Rhu GLS — where the site was awarded in late 2025 — will bring the first new private development to the Tanjong Rhu waterfront in three decades; market estimates place the launch price at S$3,200–3,500 psf, consistent with D15 premium waterfront comparable transactions. Third, URA’s ongoing Draft Master Plan 2025 consultations include proposals to intensify the East Coast Park corridor and the Katong precinct, which, if implemented, could further bolster lifestyle premiums in the Marine Parade and Siglap catchments.

Frequently Asked Questions

Which TEL station has the best investment value in 2026?

For yield-focused investors, the Upper Thomson and Springleaf catchments (D26) currently offer the best combination of gross yield (3.8–4.3%), reasonable entry price (from S$1.2M for 2BR), and near-term demand catalysts from the Johor Bahru RTS Link. For capital appreciation, Marine Parade and Katong Park (D15) are the standout stations — still absorbing the TEL connectivity premium with a supply shortage that will persist until the Tanjong Rhu GLS project completes circa 2029–2030. For lifestyle owner-occupiers, Stevens and Orchard Boulevard (D10) offer unsurpassed centrality and school proximity at a premium entry point.

How much of a premium do TEL station properties command over non-MRT units?

Research from the Institute of Real Estate and Urban Studies at NUS estimates that properties within 500 metres of a new MRT station command a 5–15% price premium over comparable properties 800–1,500 metres away, with the premium being largest in the first two to three years after the station opens and in areas with low existing MRT coverage (such as the East Coast before the TEL). Properties integrated directly with a station (ground-level covered link) command a further 3–7% premium, per URA caveat analysis. For the East Coast segment, which had zero prior MRT coverage, the observed premium has been at the higher end of the 8–12% range for 500m-radius properties.

Are there new launch condos available along the TEL right now?

As of April 2026, active new launches along the TEL corridor include Springleaf Residence (D26, near Springleaf MRT, 473 units, 92% sold at launch at ~S$2,175 psf by Wing Tai and Hong Leong Holdings) and UPPERHOUSE at Orchard Boulevard (D10, near Orchard Boulevard MRT, 171 units at ~S$3,350 psf by UOL and Singapore Land Group). The Kallang Close GLS site (near Bendemeer MRT, an adjacent north-south TEL interchange station) is expected to launch circa 2027–2028 at S$2,900–3,100 psf by Frasers Property and Mitsubishi Estate. For the East Coast, the Tanjong Rhu waterfront site is in development and expected to preview approximately 2027.

How does ABSD apply to TEL property purchases by foreigners?

Foreigners purchasing any residential property in Singapore — including condos along the TEL — pay 60% ABSD on the full purchase price, regardless of whether it is their first or subsequent property. This applies equally to CCR Orchard Boulevard units and to more affordable East Coast apartments. The 60% rate, introduced in April 2023, has effectively priced most foreign investors out of the Singapore residential market. Singapore Permanent Residents buying their first private property pay 5% ABSD; their second residential property attracts 30% ABSD. Singapore Citizens pay 0% on a first private purchase and 20% on a second. All ABSD is administered by the Inland Revenue Authority of Singapore and is payable within 14 days of exercising the Option to Purchase.

What is the Johor Bahru RTS Link and why does it matter for TEL D25–D26 properties?

The Rapid Transit System (RTS) Link is a cross-border rail connection between Woodlands North MRT (the TEL’s northernmost station) and Bukit Chagar in Johor Bahru, Malaysia, scheduled for completion in late 2026. The RTS Link will allow commuters to travel between Singapore and Johor Bahru in approximately 5 minutes by rail, replacing a congested road crossing that currently takes 30–90 minutes in peak hours. For property investors, the RTS Link is a demand multiplier: Singaporeans working in Johor Bahru’s rapidly developing Iskandar Malaysia economic region, as well as Malaysians working in Singapore who choose to commute rather than rent, both anchor rental demand at or near Woodlands North and Woodlands MRT. Industry data suggests rental demand for 1BR and 2BR units within a 10-minute walk of Woodlands MRT could increase 15–25% once the RTS Link is fully operational.

How do I find resale condos near a specific TEL station?

The most reliable data source for resale condo transactions near any TEL station is the Urban Redevelopment Authority’s real estate information system at URA REIS. You can search by postal district or project name to see actual caveated transaction prices, floor area, and date of transaction. For a broader property search including current listings, URA’s public portal at ura.gov.sg provides planning information and the latest approved development details for each district. Cross-referencing URA caveats with listing prices gives you a reliable indication of the price gap (or premium) being applied by sellers in each catchment.

Related Articles

- Singapore Rental Yield Guide 2026: Where to Find 4%+ Gross Yields

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Greater Southern Waterfront Singapore Guide 2026

- Integrated Developments Singapore Guide 2026

- Singapore Private Property Q1 2026: Full URA Statistics

- Kallang Close GLS: Frasers & Mitsubishi S$610.8M Waterfront Condo

- Freehold vs 99-Year Leasehold Singapore 2026: The Real Price of Time

Disclaimer

This article is for general informational purposes only and does not constitute financial, legal, or property investment advice. All price per square foot figures, yield estimates, and transaction data referenced are indicative, based on publicly available URA caveat records and industry analysis, and are subject to change. Property values may go up or down. ABSD and stamp duty rates are administered by IRAS and are subject to revision. Consult a licensed property professional and a qualified financial adviser before making any investment decision.