Singapore Home Insurance Guide 2026: HDB Fire Insurance, Home Contents, MRTA and FDW Cover Explained

Home insurance in Singapore is one of the most consistently misunderstood areas of property ownership. Many HDB flat owners believe they are fully covered by the mandatory HDB Fire Insurance policy that comes with their flat. Most are not. Private condo owners sometimes assume their building’s master policy protects their contents. It typically does not. And across all property types, the gap between what a homeowner thinks they are insured for and what they would actually receive in a claim can run to tens of thousands of Singapore dollars.

This guide explains exactly what each category of Singapore home insurance covers, what it does not cover, how much it costs, and what the appropriate level of coverage looks like for an HDB flat owner, a condominium resident, and a landed property owner in 2026.

Quick Answer — Singapore Home Insurance 2026 at a glance

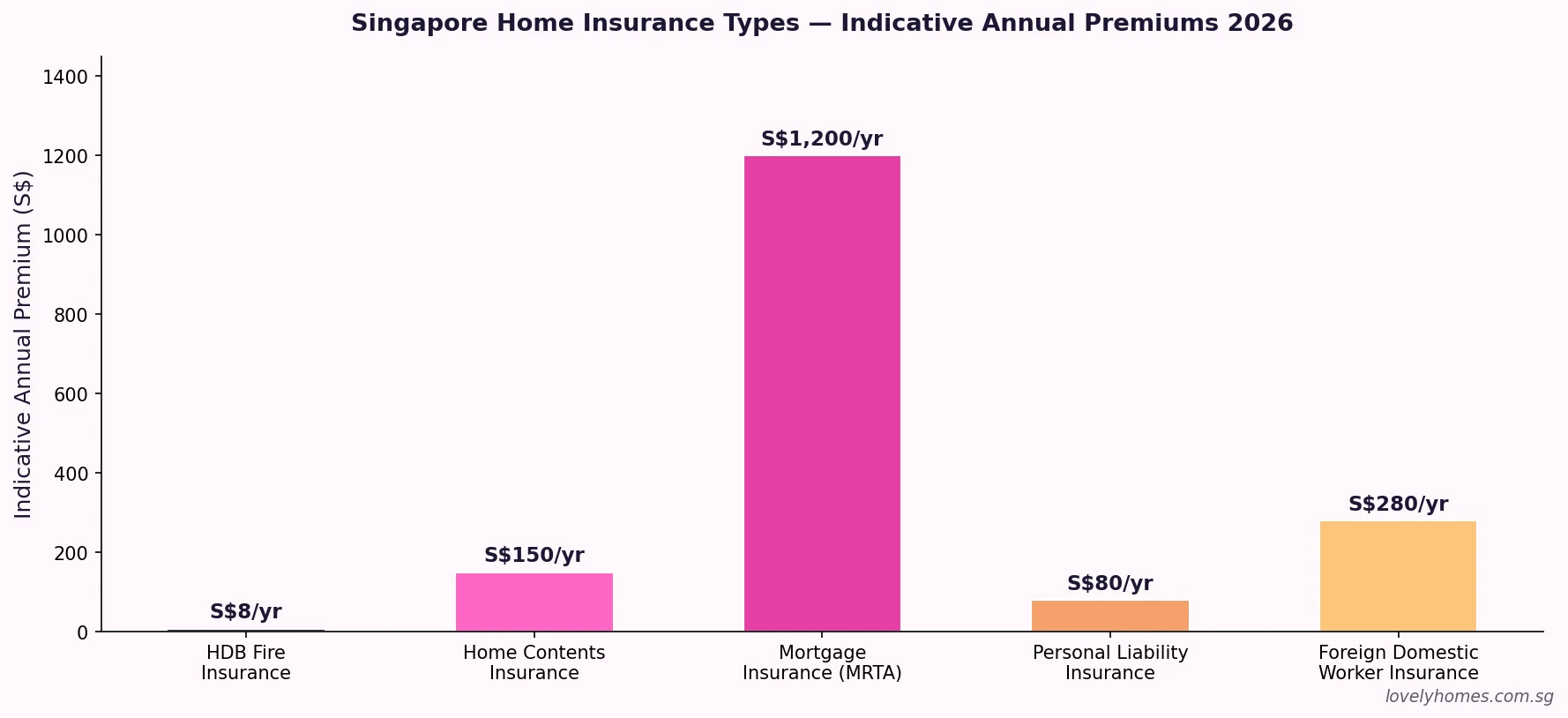

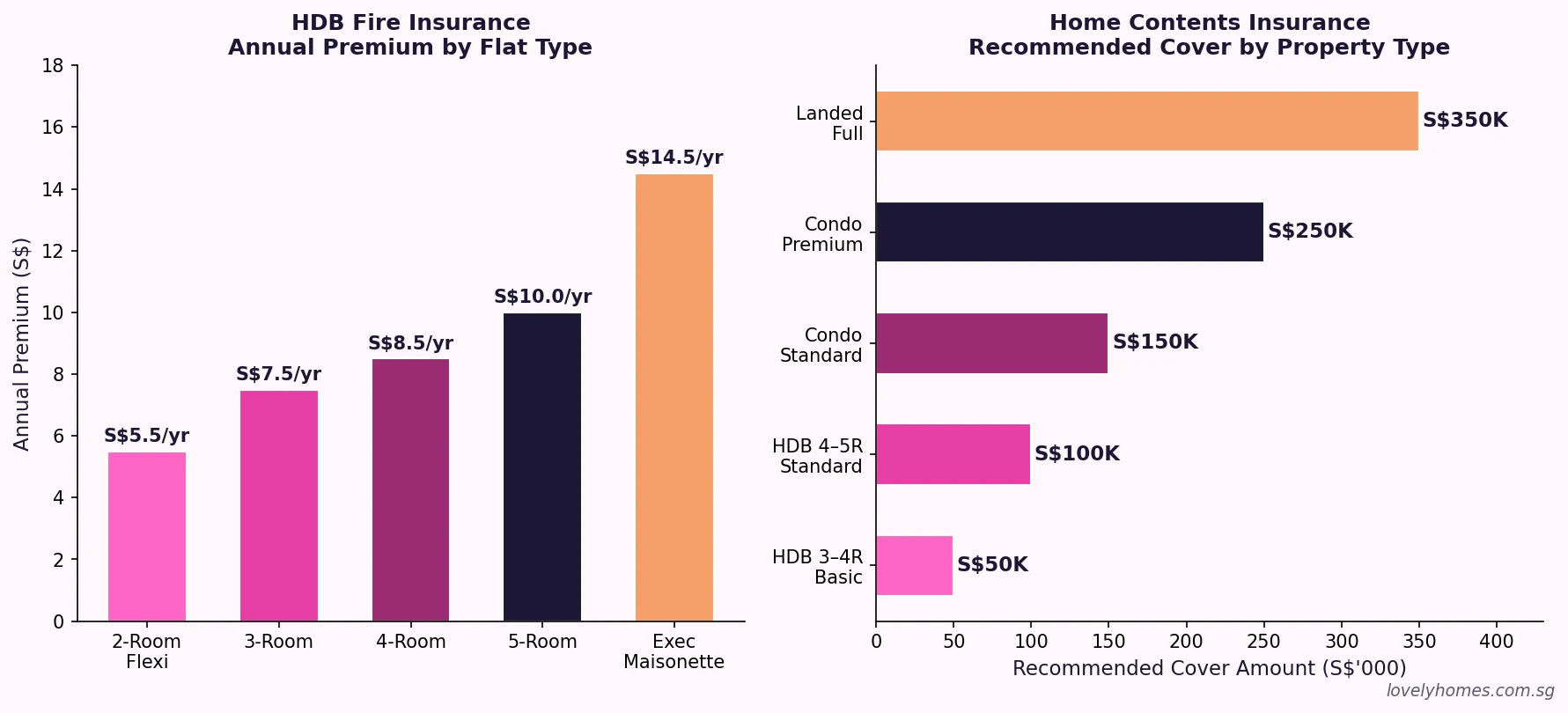

- HDB Fire Insurance is mandatory for HDB flat owners with an outstanding HDB loan. It covers only the building structure, not contents. Annual premiums start from approximately S$5.50 per year for a 2-room flat.

- Home Contents Insurance is optional but highly recommended. It covers furniture, electronics, clothing, and valuables against fire, theft, water damage, and other perils.

- Mortgage Reducing Term Assurance (MRTA) and Mortgage Level Term Assurance (MLTA) are life insurance policies that pay off the mortgage if the borrower dies or becomes totally and permanently disabled.

- Foreign Domestic Worker (FDW) Insurance is mandatory for all households employing a maid in Singapore, administered under the Employment of Foreign Manpower Act.

- Most comprehensive home insurance packages for a 4-room HDB flat with S$100,000 contents cover cost approximately S$120–S$200 per year in 2026.

- Premiums are not regulated by MAS — shop around and compare at least three insurers before buying.

- ABSD and stamp duties do not apply to insurance premiums; see our ABSD Singapore 2026 guide for property transaction costs

The Four Main Categories of Singapore Home Insurance

Singapore’s home insurance market is structured around four distinct insurance categories, each addressing a different layer of financial risk. Understanding which category applies to your situation is the essential first step before comparing policies or premiums.

The first category, HDB Fire Insurance, is a government-mandated basic policy administered under the HDB’s Fire Insurance Scheme. The second category, Home Contents Insurance, is a commercial product sold by private insurers to cover the movable assets inside your home. The third category encompasses Mortgage Insurance products (MRTA and MLTA), which are life-insurance instruments designed to discharge a mortgage on death or total permanent disability. The fourth category, FDW Insurance, is a mandatory cover for employers of foreign domestic workers.

HDB Fire Insurance: What It Covers and What It Does Not

The HDB Fire Insurance Scheme is administered by the Housing & Development Board and is compulsory for all HDB flat owners with an outstanding HDB loan. Private bank loans on HDB flats do not legally require HDB Fire Insurance, but most banks impose an equivalent building insurance requirement as a loan condition. The scheme is underwritten by a single insurer appointed by HDB through a tender process — as at 2026, Etiqa Insurance Pte Ltd holds the mandate.

What HDB Fire Insurance covers: The policy insures the structural components of the flat, including the original fixtures, internal walls, floors, ceilings, and the built-in fittings that were installed by HDB when the flat was first built (kitchen cabinets, bathroom fittings, electrical wiring). The insured sum is the estimated cost to rebuild the structural elements in the event of fire or an allied peril (smoke, explosion, lightning, impact).

What HDB Fire Insurance does NOT cover: It does not cover any renovations, additions, or alterations made by the flat owner after purchase. It does not cover furniture, electrical appliances, clothing, jewellery, art, or any other movable contents. It does not cover accidental damage, water damage from external sources (such as a burst pipe in the unit above), theft, or public liability. For most HDB owners, the renovation work they commission after purchase — which can cost S$30,000–S$100,000 for a 4-room flat — is entirely uninsured under the HDB Fire Insurance Scheme.

Home Contents Insurance: What It Is and How Much You Need

Home Contents Insurance is a private commercial product sold by insurers including NTUC Income, AIA, AXA, Sompo (formerly Sompo Japan), Great Eastern, and Etiqa, among others. Policies are not standardised, so coverage, exclusions, and premiums vary significantly between providers. Buyers should compare policy wordings carefully, not just premium prices.

A standard Home Contents Insurance policy typically covers: furniture and fittings (including renovation works), electronic appliances, clothing and personal effects, and jewellery (subject to per-item and aggregate sub-limits). Perils covered typically include fire, lightning, explosion, theft, vandalism, water damage from burst pipes or overflowing tanks, and in some policies, accidental damage. Most policies exclude flood, earthquake, and subsidence, though Singapore’s geography makes these perils relatively rare.

The key figure to determine is your sum insured — the amount of cover you are purchasing. Many homeowners significantly underestimate the replacement value of their contents. A practical exercise is to walk through your home and estimate the current replacement cost (not original purchase price) of every item: bedroom furniture, mattresses, wardrobe and clothing, kitchen appliances, television, computer equipment, power tools, jewellery, and children’s toys and equipment. For a 4-room HDB flat with moderate furnishings and a mid-range renovation, the replacement cost of contents and renovation works combined often exceeds S$100,000–S$150,000.

Mortgage Insurance: MRTA vs MLTA

Mortgage insurance addresses a different risk: the risk that the borrower dies or becomes totally and permanently disabled (TPD) before the mortgage is paid off, leaving the surviving family with a property but no capacity to service the loan.

Mortgage Reducing Term Assurance (MRTA) is the simpler instrument. It provides a death/TPD benefit that reduces over time in line with the outstanding mortgage balance. If you borrow S$500,000 and die in Year 5, the MRTA pays out approximately S$460,000 (the remaining balance), discharging the mortgage. MRTA does not pay out a lump sum beyond the mortgage balance; there is no residual benefit to the estate. Premiums for MRTA are typically paid as a single lump sum at loan inception, often capitalised into the loan amount itself. Indicative single-premium MRTA for a S$500,000 loan over 25 years for a 35-year-old non-smoker is approximately S$15,000–S$25,000.

Mortgage Level Term Assurance (MLTA) is a level-sum-assured life policy that provides a fixed death/TPD benefit (e.g. S$500,000) throughout the policy term regardless of the outstanding mortgage balance. If the insured dies in Year 20 and the mortgage balance is S$200,000, the MLTA pays S$500,000 — S$200,000 discharges the mortgage and S$300,000 goes to the estate. MLTA premiums are paid monthly or annually and are higher than MRTA on an equivalent sum-assured basis, but the policy accrues surrender value and provides greater financial protection for the family.

The Monetary Authority of Singapore (MAS) regulates both MRTA and MLTA as insurance products. HDB Home Loan borrowers are required to have adequate life insurance covering the loan amount, but are not required to purchase any specific product. Buyers who take a bank loan for a private property are typically not legally required to purchase mortgage insurance, though banks may offer (and recommend) these products as part of the loan package.

Foreign Domestic Worker (FDW) Insurance

Any household employing a Foreign Domestic Worker in Singapore must purchase FDW Insurance as a condition of the work permit, administered under the Employment of Foreign Manpower Act and enforced by the Ministry of Manpower (MOM). The mandatory minimum coverage includes personal accident insurance of S$60,000, hospitalisation and surgical expenses of S$15,000 per year, and a security bond of S$5,000 (waived if the employer meets certain criteria).

MOM-approved FDW Insurance policies are available from a range of insurers at annual premiums of approximately S$220–S$350, depending on the insurer, the coverage level, and whether optional add-ons (such as repatriation costs, maternity cover, or third-party liability) are included. Premiums have risen modestly since 2022 due to increased hospitalisation cost claims. Employers must renew FDW Insurance annually and cannot allow it to lapse without risking permit revocation and MOM sanctions.

Summary Table: Singapore Home Insurance Types 2026

| Insurance Type | Mandatory? | What It Covers | What It Does NOT Cover | Indicative Annual Cost |

|---|---|---|---|---|

| HDB Fire Insurance | Yes (HDB loan) | Structure, original HDB fixtures & fittings | Renovation, contents, accidental damage, water ingress from outside | S$5.50–S$14.50 |

| Home Contents Insurance | No | Furniture, appliances, renovation, clothing, jewellery | Flood, earthquake, wear & tear, high-value items above sub-limit | S$80–S$350+ |

| MRTA (Mortgage) | No | Outstanding mortgage balance on death/TPD | Critical illness, income protection, residual estate benefit | Single premium ~S$15K–S$25K total |

| MLTA (Mortgage) | No | Fixed life sum assured on death/TPD | Critical illness unless rider added | S$800–S$1,800/yr (monthly premiums) |

| FDW Insurance | Yes (maid employers) | PA, hospitalisation, security bond | Employer liability unless optional add-on purchased | S$220–S$350 |

| Personal Liability | No | Third-party bodily injury/property damage from your home | Intentional acts, business use, motorised vehicles | S$60–S$120 |

Worked Example: How Much Should a 4-Room HDB Owner Spend on Home Insurance?

Mr and Mrs Lim own a 4-room HDB flat in Tampines, purchased for S$580,000 with an outstanding HDB loan of S$380,000. They spent S$65,000 on renovation (kitchen, bathrooms, built-in wardrobes, flooring). Their home contents include furniture (S$15,000), electronics and appliances (S$12,000), clothing and personal effects (S$8,000), and Mrs Lim’s jewellery (S$25,000). They employ a Foreign Domestic Worker.

Mandatory insurance they already have: HDB Fire Insurance (approximately S$8.50/year for a 4-room flat), covering the original HDB structure. FDW Insurance for their domestic worker (approximately S$260/year). Total mandatory: approximately S$269/year.

What they need but do not yet have: The HDB Fire Insurance does NOT cover their S$65,000 renovation, S$55,000 in contents, or the S$25,000 jewellery. A Home Contents Insurance policy with S$150,000 sum insured (covering renovation and contents) with a jewellery rider up to S$30,000 would cost approximately S$170/year from a typical Singapore insurer. Personal Liability cover (S$500,000 limit for accidental injury to a third party in their home) would add approximately S$80/year.

Total recommended insurance spend: Mandatory S$269 + Home Contents S$170 + Personal Liability S$80 = approximately S$519/year for comprehensive home insurance protection. This represents approximately 0.09% of the flat’s purchase price annually — a modest cost relative to the financial risk of being uninsured against a fire, water damage event, or theft.

Mortgage insurance: For an outstanding loan of S$380,000, a single-premium MRTA would cost approximately S$12,000–S$18,000 capitalised into the loan, or an MLTA at S$500,000 sum assured would cost approximately S$1,200/year in monthly premiums for Mr Lim aged 38. Whether to choose MRTA or MLTA depends on their broader financial planning, life insurance coverage from existing policies, and whether they value the surrender value and estate planning aspects of MLTA.

Why This Matters for Singapore Homeowners

Singapore’s property prices mean that most homeowners’ single largest financial asset is their property. The paradox is that many of these same homeowners carry inadequate insurance against the events most likely to cause a partial or total loss of that asset — fire, water damage, and theft. Insurance penetration for home contents in Singapore has historically been low relative to the value of assets at risk, a fact that the General Insurance Association of Singapore (GIA) has repeatedly flagged in its annual market reports.

The situation is compounded by two misunderstandings. First, HDB flat owners conflate the mandatory HDB Fire Insurance with comprehensive home protection, and feel covered when they are not. Second, strata condo owners assume their MCST’s building insurance covers the interior of their unit and its contents, when in fact the building policy typically covers only the structure and common areas — not renovations, fittings, or personal property within individual units. Understanding precisely what your current insurance does and does not cover is the critical first step.

From an investment standpoint, home insurance also protects rental income. If a flood or fire damages a tenanted property and makes it uninhabitable, most comprehensive policies include Loss of Rent cover (typically 10–15% of the sum insured) to compensate the landlord for the rental income lost during the repair period. Without this cover, a landlord faces both repair costs and lost income simultaneously — a double financial impact that can take years to recover from.

What Might Come Next for Singapore Home Insurance

Several developments are likely to shape the home insurance market over the medium term. Rising renovation costs — up an estimated 20–30% since 2019 due to supply chain disruptions and labour shortages — mean that sum-insured amounts set several years ago may be materially inadequate today. Homeowners who have not reviewed their Home Contents Insurance policy since completing their renovation should reassess their sum insured.

Climate-related risks are also receiving increasing attention from Singapore’s insurance regulators. The MAS’s climate risk framework has prompted insurers to review their underwriting models for flood and extreme weather events. While Singapore’s drainage infrastructure is among the world’s best, flash flooding in low-lying residential areas has caused property damage in recent years, and some insurers have introduced flood exclusions or sub-limits in their home policies. Buyers should read policy wordings carefully for flood coverage.

Finally, the increasing value of jewellery, watches, and art collections in Singapore homes — driven in part by the Ultra High Net Worth influx since 2021 — has prompted specialist insurers to develop dedicated high-value personal property floaters that sit above standard home contents policies. For homeowners with individual items worth more than S$10,000–S$15,000, a standard Home Contents policy’s per-item sub-limit (typically S$1,500–S$5,000) may be inadequate, and a specialist all-risks policy should be considered.

Frequently Asked Questions

Is HDB Fire Insurance compulsory if I take a bank loan instead of an HDB loan?

The HDB Fire Insurance Scheme is legally mandatory only for HDB flat owners with an outstanding HDB loan. If you take a bank loan for your HDB flat, you are not legally required to purchase HDB Fire Insurance specifically. However, most banks impose their own building insurance requirement as a loan condition — they typically require you to purchase a fire insurance policy covering at least the reinstatement value of the structural components. You may purchase this from any MAS-licensed insurer, not only the HDB scheme provider. In practice, most bank-loan HDB buyers do purchase fire insurance, and some also purchase comprehensive home contents insurance on top. Confirm your bank’s specific requirement in your loan letter of offer.

Does my condo’s MCST master policy cover my unit’s contents and renovation?

No. The MCST’s master building insurance policy covers the common areas, external structure, and the original building components — the concrete structure, lift shafts, roof, corridors, and shared facilities. It does not cover any renovations, fittings, furniture, appliances, or personal effects inside individual units. It also typically does not cover accidental damage or water ingress originating within your own unit (as distinct from structural ingress through the building envelope). As a condo owner, you need your own Home Contents Insurance policy to cover your interior renovations, contents, and personal effects. The MCST policy exists to protect the collective asset — not the individual unit owner’s possessions.

What is the difference between MRTA and MLTA, and which should I choose?

MRTA (Mortgage Reducing Term Assurance) is a pure protection product — the sum insured reduces over time in line with the outstanding loan balance. If you die or become totally and permanently disabled, the insurer pays out the remaining mortgage balance, clearing the debt. MRTA has no surrender value and no residual benefit beyond the mortgage discharge. It is typically cheaper than MLTA, especially when the premium is calculated at loan inception on a single-premium basis. MLTA (Mortgage Level Term Assurance) is a level-sum life policy. The sum assured remains constant throughout the term. If the insured dies in Year 20 and the remaining mortgage is S$150,000, the MLTA pays the full sum assured (e.g. S$500,000), clearing the mortgage and leaving S$350,000 for the estate. MLTA accrues surrender value and typically includes whole-of-life or extended coverage options. The choice between MRTA and MLTA depends on your broader life insurance holdings, estate planning objectives, and budget. Consult a licensed Financial Adviser before deciding.

How much Home Contents Insurance do I actually need?

The correct sum insured is the current replacement cost of everything in your home that is not part of the building structure — furniture, electronics, appliances, clothing, books, children’s equipment, sports gear, and jewellery — plus the full reinstatement cost of any renovation works you have carried out (new flooring, built-in wardrobes, kitchen cabinets, bathroom fittings, lighting, painting). For a 4-room HDB flat with a moderate renovation (S$50,000–S$70,000) and standard furnishings, the total replacement cost typically falls in the S$120,000–S$180,000 range. Many homeowners significantly underestimate this figure by forgetting to include renovation costs, systematically undervaluing their belongings, and failing to account for appreciation in replacement costs since the items were purchased. Reviewing and updating your sum insured every two to three years is advisable.

Can I use CPF to pay for home insurance premiums?

No. CPF funds may not be used to pay general insurance premiums, including Home Contents Insurance, HDB Fire Insurance, or FDW Insurance. CPF OA funds may be used for the purchase of a home (down payment, BSD, monthly loan instalments for certain loan types) but not for ongoing insurance premium payments. MLTA (Mortgage Level Term Assurance) premiums may be payable from CPF OA funds in certain approved schemes — verify this directly with the insurer and CPF Board. MRTA premiums capitalised into the loan amount are funded by the loan itself, not directly from CPF. For most home insurance products, premiums must be paid by GIRO, credit card, or cheque from a bank account.

What happens if my neighbour causes a fire that damages my flat?

If a fire originates in a neighbouring unit and spreads to damage your flat, your recourse depends on the specific facts and whether your neighbour was negligent. Under Singapore tort law, you may have a civil claim against a negligent neighbour for damage to your property. In practice, pursuing such claims can be lengthy and uncertain. The practical protection is to ensure you have your own Home Contents Insurance (and where applicable, Houseowner Insurance) that covers fire damage regardless of origin — your insurer will then subrogate against your neighbour’s insurer if negligence is established, relieving you of the burden of pursuing the claim directly. Never rely solely on a third party’s insurance to protect your assets.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Housing Loan Guide 2026: HDB Loan, Bank Loan, TDSR, MSR and Fixed vs Floating Rates

- Singapore HDB Resale Buying Process Guide 2026: Step-by-Step from HFE to Keys

- Singapore Landlord Guide 2026: Rental Income Tax, Tenancy Agreements, Property Tax and Landlord Rights

- Singapore Strata Title and MCST Guide 2026: Management Fees, Sinking Fund, By-Laws and En Bloc Rights

- Singapore CPF for Property Guide 2026: How to Use Your OA, Valuation Limits and Accrued Interest Explained

- Singapore Property Tax Guide 2026: IRAS Annual Value, Owner-Occupied Rates and How to Pay

Disclaimer

All insurance premium figures in this article are indicative and based on publicly available market information as at July 2026. Actual premiums depend on the insurer, policy terms, property type, sum insured, and individual risk factors. The MAS’s Financial Institutions Directory at mas.gov.sg lists all licensed insurers operating in Singapore. HDB Fire Insurance scheme details are published at hdb.gov.sg. FDW Insurance requirements are administered by MOM at mom.gov.sg. This article is for general information purposes only and does not constitute financial, legal, or insurance advice. Readers should consult a licensed Financial Adviser or insurance professional before purchasing any insurance product. LovelyHomes is an independent editorial property information platform and does not receive commissions from or recommend any specific insurer.