Singapore Housing Loan Guide 2026: HDB Loan, Bank Loan, TDSR, MSR and Fixed vs Floating Rates

⚡ Quick Answer — Singapore Housing Loan Guide 2026

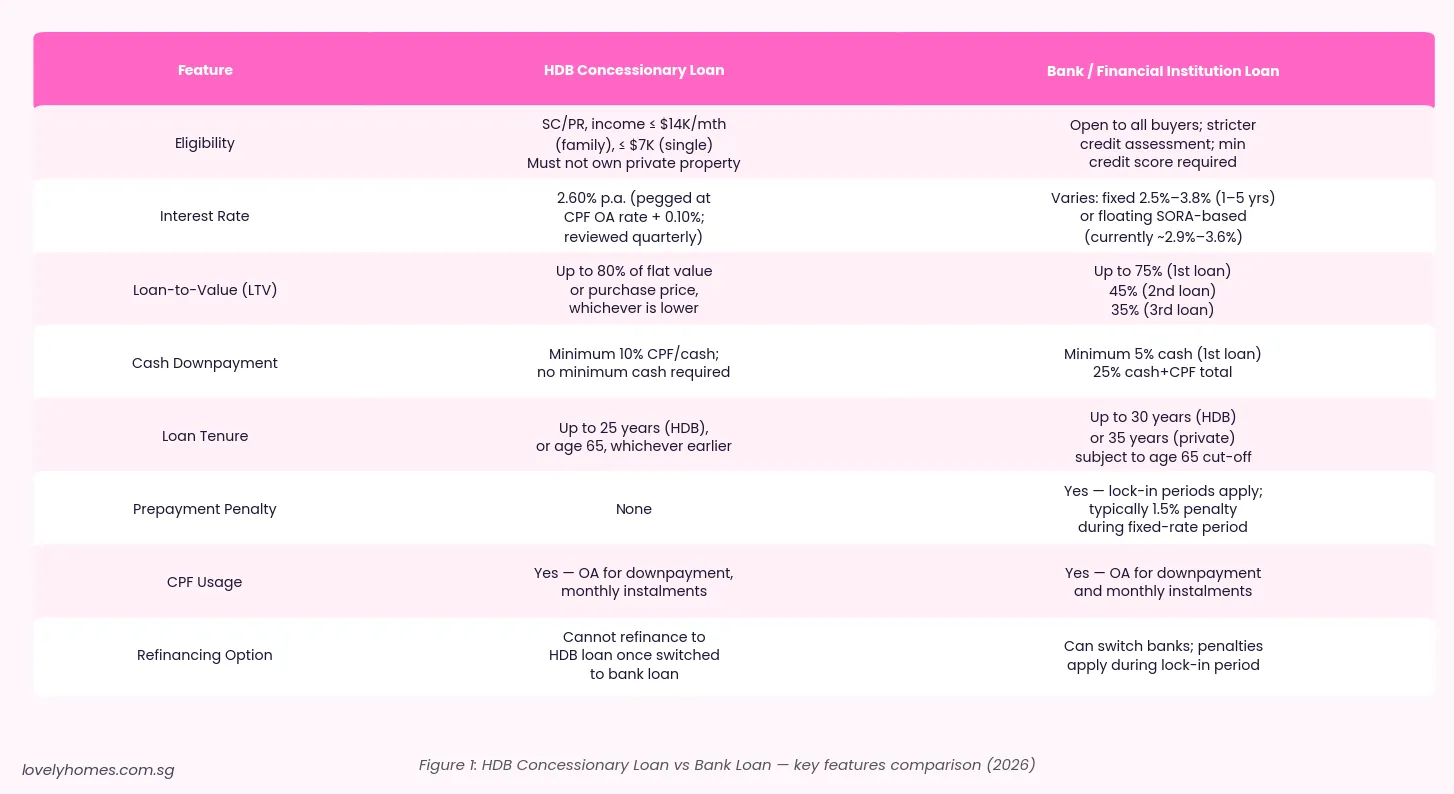

- Two loan types: HDB Concessionary Loan (2.60% p.a., LTV up to 80%) or Bank/FI Loan (variable 2.5%–3.8%, LTV up to 75%). Once you switch to a bank loan, you cannot return to HDB financing.

- TDSR (Total Debt Servicing Ratio): all monthly debt repayments must not exceed 55% of gross monthly income — applies to every borrower.

- MSR (Mortgage Servicing Ratio): for HDB flat purchases only, your property loan repayment must not exceed 30% of gross monthly income.

- Loan tenure: up to 25 years (HDB loan); up to 30 years (bank loan on HDB flat); up to 35 years for private property, subject to age-65 cut-off.

- Minimum cash downpayment: 5% cash for a bank loan (first property); HDB loan requires minimum 10% downpayment, fully payable from CPF OA — no mandatory cash.

- Fixed vs floating: fixed rates lock in certainty for 1–5 years; floating (SORA-based) tracks market rates and benefits from falling rate environments.

- HFE letter required: before exercising an OTP on any HDB flat, you must hold a valid HDB Flat Eligibility (HFE) letter specifying your loan eligibility.

Singapore Housing Loans: The Regulatory Framework

Singapore’s residential mortgage market is governed by the Monetary Authority of Singapore (MAS) through the Financial Advisers Act and the Banking Act, supplemented by the suite of property cooling measures active since 2009. HDB’s own concessionary loan scheme operates in parallel, governed by the Housing & Development Act and administered by HDB.

Two bodies set the lending guardrails every Singapore borrower must work within: MAS (TDSR and LTV limits for bank loans) and HDB (MSR and income-ceiling criteria for the concessionary scheme). Understanding both frameworks before committing to any home purchase is essential, because your borrowing capacity — and the monthly cash-flow required to service the mortgage — depends entirely on which loan type you take.

HDB Concessionary Loan — Who Qualifies and What It Offers

The HDB concessionary loan is available only to buyers of HDB flats and only to households where at least one applicant is a Singapore Citizen. The interest rate is pegged at 0.10 percentage points above the CPF OA rate (2.50% p.a. since 1999), making the HDB loan rate 2.60% p.a. — reviewed quarterly but unchanged since 1 January 1999.

HDB Loan Eligibility (2026)

| Criterion | Requirement |

|---|---|

| Citizenship | At least one Singapore Citizen applicant |

| Gross Monthly Income | ≤ $14,000/mth (families); ≤ $7,000/mth (singles) |

| Private Property | Must not currently own private residential property; none disposed of in preceding 30 months |

| Prior HDB Loans | Maximum two HDB concessionary loans in a lifetime |

| Flat Type | HDB flats only — not ECs, DBSS or private property |

| HFE Letter | Valid HDB Flat Eligibility (HFE) letter required |

A key advantage of the HDB loan is that the minimum 10% downpayment can come entirely from the buyer’s CPF OA — no mandatory cash component is required. For buyers with substantial CPF savings but limited liquid cash, this is a significant advantage over bank loan requirements.

Bank Loans — Flexibility and Market Rates

Bank loans are available from any MAS-licensed bank or financial institution in Singapore. Unlike HDB loans, bank loans are available for all property types — HDB flats, ECs, private condominiums, landed homes, and commercial property. Rates are either fixed for an introductory period or floating, pegged to SORA.

LTV Limits by Outstanding Loan Count (Bank Loans)

| Outstanding Loans | LTV Limit | Minimum Cash Downpayment | Total Minimum Downpayment |

|---|---|---|---|

| 0 (first property loan) | 75% | 5% cash | 25% (5% cash + 20% CPF/cash) |

| 1 (second property loan) | 45% | 25% cash | 55% |

| 2 or more (third+ loan) | 35% | 25% cash | 65% |

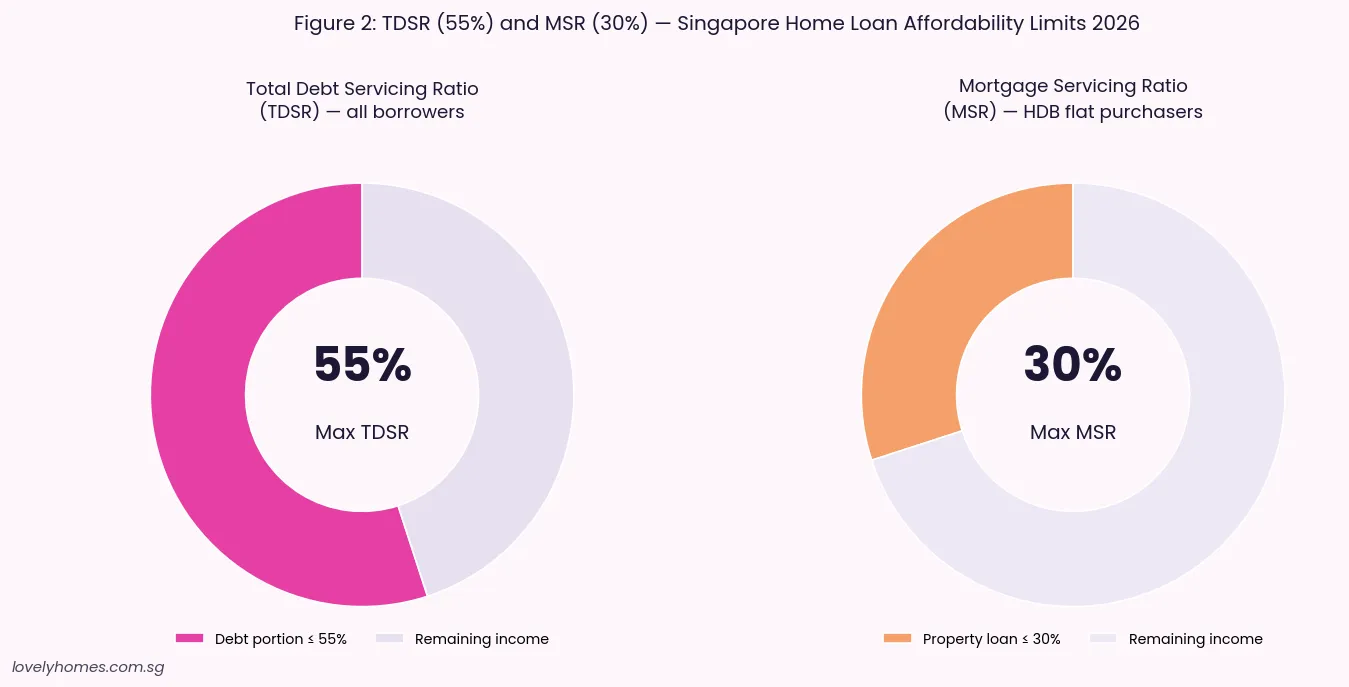

TDSR and MSR: The Two Affordability Tests

Total Debt Servicing Ratio (TDSR), set by MAS at 55%, caps all monthly debt obligations — including car loans, personal loans, credit card minimums and the proposed mortgage — at 55% of gross monthly income. TDSR applies to every property purchase in Singapore, regardless of type or buyer nationality.

Mortgage Servicing Ratio (MSR), at 30%, applies specifically to HDB flat purchases. It limits the monthly mortgage repayment on the HDB loan alone to 30% of gross monthly income. For a household earning $8,000/month, the MSR ceiling is $2,400/month — often the binding constraint when purchasing a larger HDB flat.

The two tests serve different purposes. TDSR prevents households from taking on unsustainable total debt across all borrowings. MSR ensures that HDB — as government-subsidised housing — is not leveraged beyond a prudent level. A buyer can pass TDSR yet fail MSR, requiring either a smaller loan or a higher income.

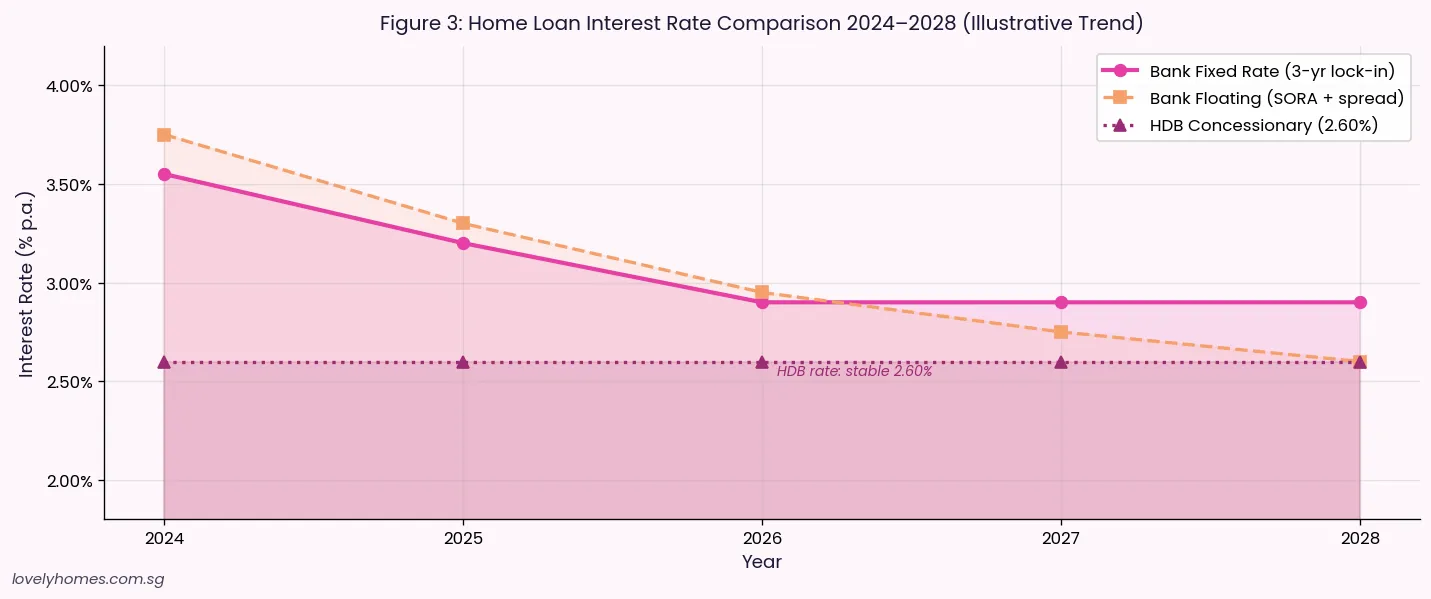

Fixed vs Floating Rate: Which Is Right For You?

The 2022–2023 rate spike, when SORA climbed from near zero to above 3% following global monetary tightening, made this question acutely important for Singapore borrowers. By mid-2026 SORA has moderated; the choice between fixed and floating is less stark but still consequential for monthly cash flow.

| Package Type | Typical Rate (Mid-2026) | Lock-in Period | Best For |

|---|---|---|---|

| Fixed (1-year) | ~2.65%–2.80% p.a. | 1 year | Short-term certainty; expect to refinance |

| Fixed (2-year) | ~2.75%–2.95% p.a. | 2 years | Medium certainty; most popular in 2026 |

| Fixed (3–5 year) | ~2.90%–3.20% p.a. | 3–5 years | Long certainty; premium for stability |

| Floating (SORA + spread) | ~2.85%–3.20% p.a. | None to 1 year | Benefits from rate falls; higher volatility |

| HDB Concessionary | 2.60% p.a. | None | Stable, no lock-in; eligible buyers only |

Worked Example: HDB Loan vs Bank Loan

📺 Case Study — the Lim Household

Profile: Mr and Mrs Lim, SC-SC couple, both first-timers. Combined gross income $9,500/month. Buying a 5-room resale flat in Bishan for $750,000 (HDB valuation $730,000). They have $150,000 in combined CPF OA.

HDB Loan check: Income $9,500/mth exceeds the HDB loan ceiling of $9,000/mth for families. The Lims do not qualify for the HDB concessionary loan — they must take a bank loan.

Bank Loan (LTV 75%): Loan up to $562,500. Downpayment: 25% of $750,000 = $187,500 (mandatory 5% cash = $37,500; CPF $150,000). Loan: $562,500 at 2.85% p.a. (floating), 30 years → monthly repayment ≈ $2,328/month. MSR: 24.5% ✓ PASS. TDSR (no other debts): 24.5% ✓ PASS.

Total cash at completion: $37,500 mandatory cash + ~$5,000 legal fees. BSD $17,100 payable from CPF. Total cash outlay ≈ $42,500.

Key takeaway: The Lims must take a bank loan due to the income ceiling. The 5% cash minimum ($37,500) is manageable; CPF covers the balance of the downpayment and BSD. At a 24.5% MSR, they have headroom if rates rise modestly. If SORA falls in 2027, their floating-rate repayment will reduce automatically.

Why Singapore’s Mortgage Rules Are Structured This Way

The dual-layer TDSR/MSR framework reflects MAS and HDB’s shared objective: ensuring home ownership does not become a source of financial distress. TDSR at 55% was introduced in 2013 in direct response to rising household leverage during the post-2008 low-rate period, when lenders were extending mortgages to buyers whose total debt obligations far exceeded sustainable levels. By standardising a hard ceiling across all lenders, MAS established a consistent affordability floor across Singapore’s banking system.

MSR at 30% is deliberately tighter for HDB purchases because HDB flats are government-subsidised public housing. The 30% threshold is calibrated so that most HDB buyers can continue servicing their mortgage even if one income earner loses employment — preserving the social objective of housing stability. Singapore’s approach contrasts with markets like Australia (individual serviceability tests without hard regulatory caps) or the UK (soft loan-to-income ratios). The result is a structurally lower mortgage default rate.

Rate Outlook and Refinancing

The trajectory of the US Federal Reserve and the Singapore overnight lending market will determine whether floating-rate packages remain competitive through 2027. Market consensus as at mid-2026 places the next Fed rate cut in late 2026 or early 2027, which would pull SORA lower. Buyers entering floating-rate packages now may benefit from falling monthly repayments. Those on 2-year fixed packages locked in 2024–2025 at higher rates should review refinancing options as their lock-in period expires.

FAQ: Singapore Housing Loans 2026

Can I use CPF OA to pay monthly mortgage instalments for a bank loan?

Yes. CPF Ordinary Account savings can service monthly mortgage instalments for both HDB loans and bank loans on eligible property, subject to the Valuation Limit and accrued-interest rules. The bank deducts the instalment from your CPF OA monthly, with any shortfall requiring cash top-up. CPF withdrawals for property accrue interest at 2.5% p.a., which must be refunded to CPF on sale.

What is SORA and how does it affect my floating-rate mortgage?

SORA (Singapore Overnight Rate Average) is the volume-weighted average rate of unsecured overnight interbank SGD transactions, published daily by MAS. Most Singapore bank mortgage packages moved from SIBOR-based to SORA-based pricing since 2021. A typical floating package might be “1-month SORA + 1.00% spread” — your rate moves monthly with SORA. When the Fed cuts rates, SORA tends to follow with a short lag, reducing your repayment. The risk is the reverse: the 2022–2023 spike demonstrated how sharply obligations can rise.

Can I refinance from a bank loan back to an HDB loan?

No. Once you switch from an HDB concessionary loan to a bank loan, you cannot refinance back to HDB financing. The switch is permanent. You can refinance between banks — subject to lock-in penalties — or switch between rate types with the same bank. This makes the initial loan-type decision particularly consequential.

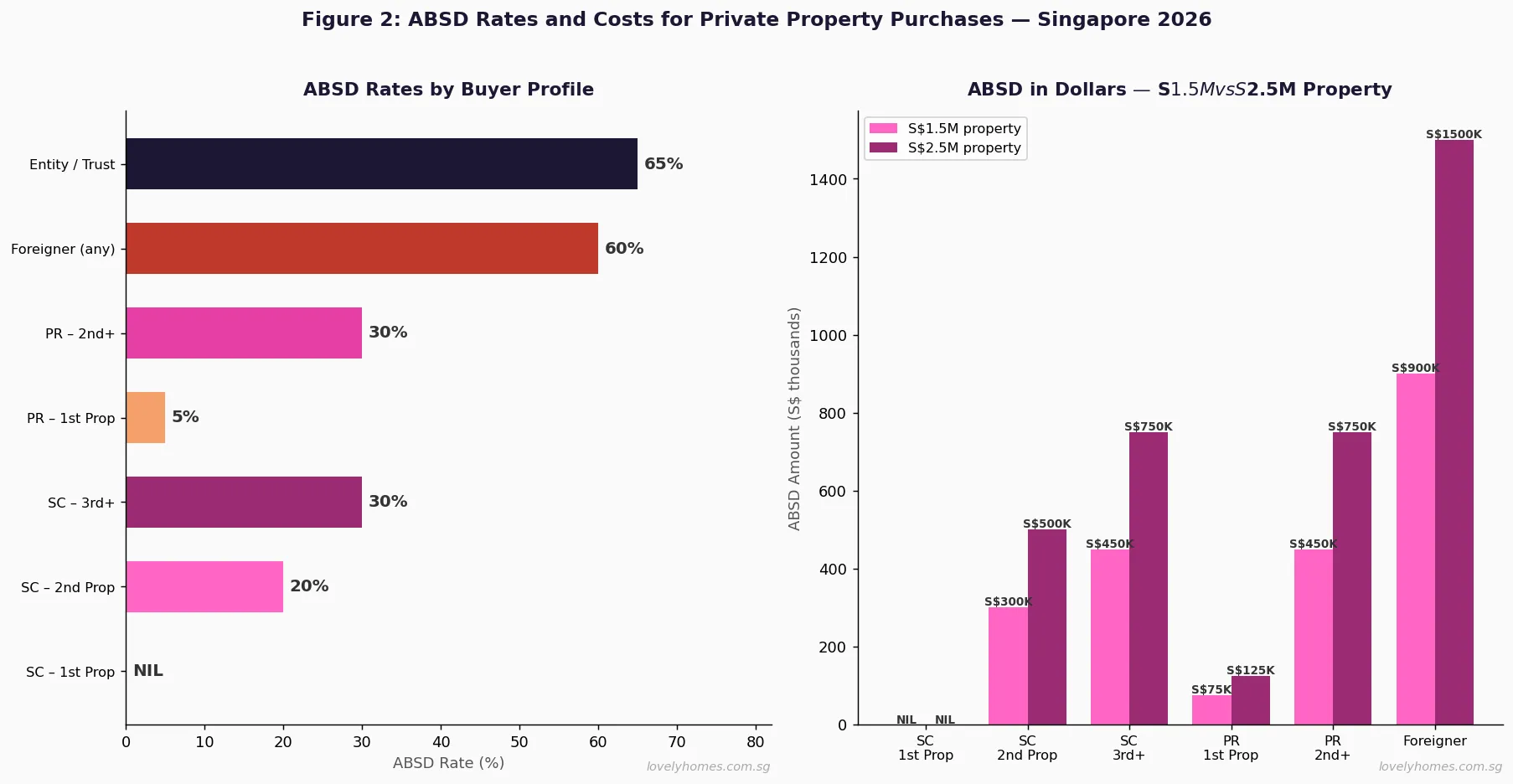

Does a larger loan affect ABSD?

The loan amount does not directly affect ABSD. Additional Buyer’s Stamp Duty is calculated on the purchase price (or market value, whichever is higher) and must be paid in cash within 14 days of signing the S&P Agreement. ABSD cannot be financed or paid from CPF; it requires a separate cash outlay. A higher purchase price implies higher ABSD, but the financing structure is irrelevant to the ABSD computation.

What happens if I cannot meet my mortgage repayments?

For HDB loans, HDB has an arrears management framework with grace periods and restructuring options before enforcement. For bank loans, lenders may issue a Letter of Demand and, ultimately, commence foreclosure if repayments remain delinquent beyond the contractual default period (typically 3 months). Borrowers in difficulty should contact their lender early — most banks have hardship assistance programmes, and MAS expects lenders to engage proactively. HDB also operates a Financial Assistance Scheme for eligible borrowers.

Can foreigners take bank loans for Singapore property?

Yes. Foreigners and PRs can obtain bank mortgages from Singapore-licensed banks for eligible property types. LTV limits, TDSR and tenure rules apply equally. Foreigners are not eligible for HDB loans. Some banks apply additional credit assessments or require larger downpayments for non-residents — particularly for borrowers with income in volatile currencies.