Singapore Property Conveyancing Guide 2026: OTP, S&P Agreement, Legal Fees and Timelines Explained

- Conveyancing is the legal process of transferring property ownership in Singapore, handled by licensed Singapore lawyers.

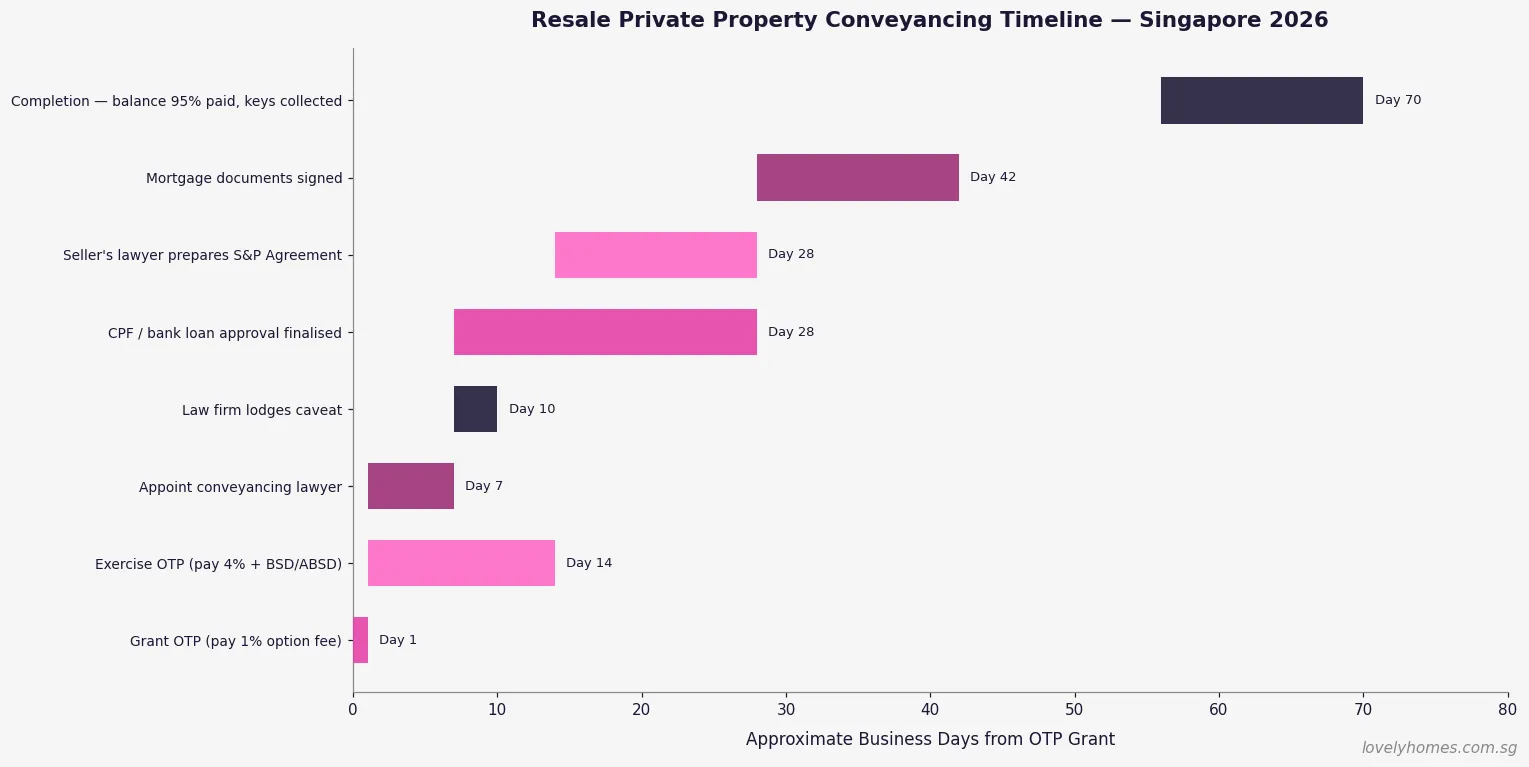

- For private property, it involves an Option to Purchase (OTP), exercise of the OTP, and completion — typically over 8–12 weeks.

- HDB resale transactions use the HDB Resale Portal and take approximately 8–10 weeks after HDB approval.

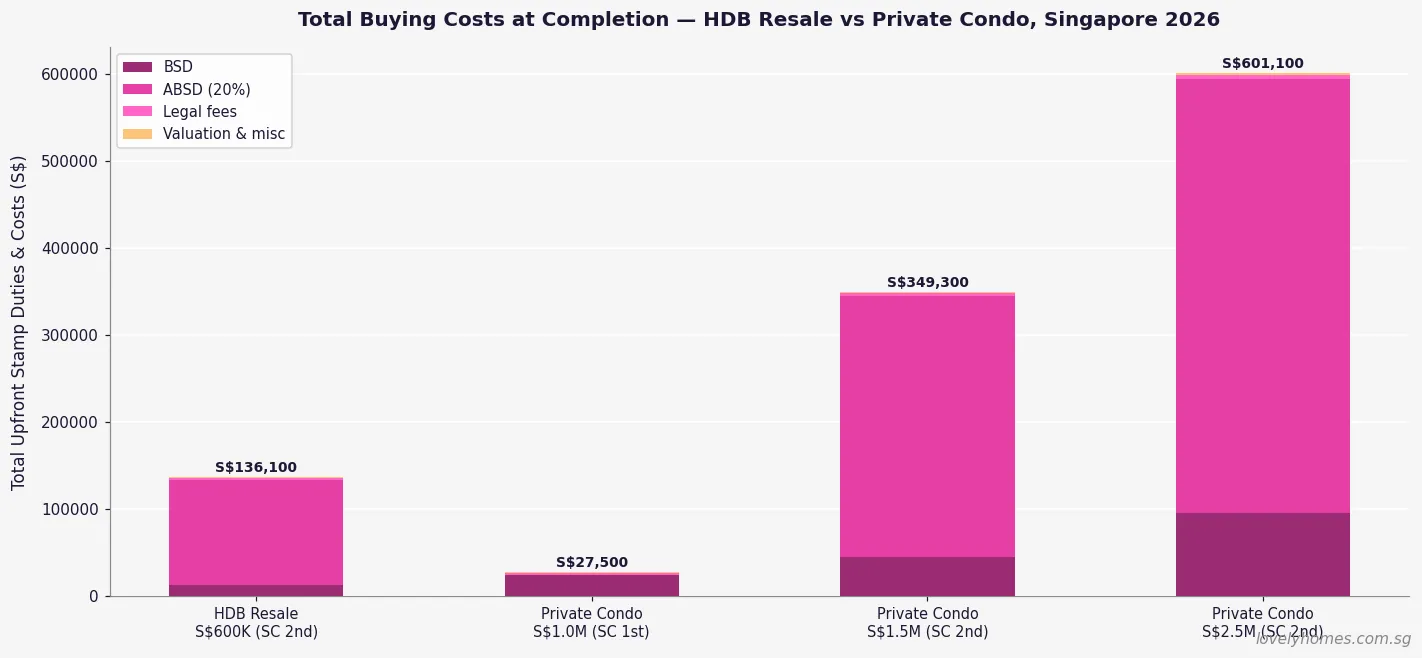

- Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD, if applicable) must be paid within 14 days of signing the OTP or S&P Agreement.

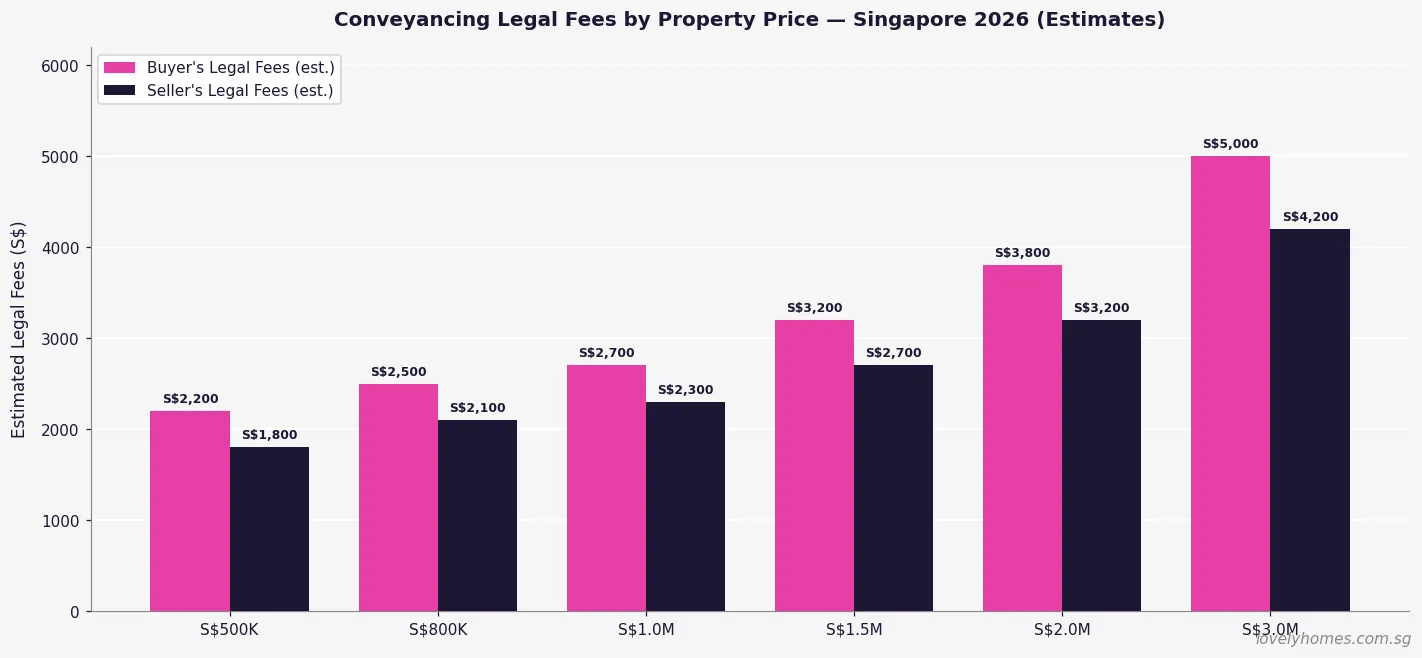

- Legal fees for buyers typically range from S$2,200 to S$5,000 depending on property price; sellers pay S$1,800–S$4,200.

- Disbursements (search fees, caveats, IRAS e-Stamping) add a further S$500–S$1,500 per transaction.

- A conveyancing lawyer lodges a caveat on the title to protect the buyer’s interest between OTP exercise and completion.

- CPF funds used for the purchase are refunded with 2.5% per annum accrued interest upon sale — factor this into your net proceeds calculation.

What Is Property Conveyancing?

Conveyancing is the Singapore legal process by which ownership of land or property is formally transferred from seller to buyer. Every private residential transaction — whether a new launch, resale condominium, landed property, or executive condominium — requires a conveyancing lawyer admitted to the Singapore Bar under the Legal Profession Act (Cap. 161). No individual may conduct their own conveyancing in Singapore; you must appoint a licensed law firm.

The Singapore Land Authority (SLA) maintains the land register under the Land Titles Act (Cap. 157). Separately, the Inland Revenue Authority of Singapore (IRAS) collects Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD) via its e-Stamping portal. Your lawyer interfaces with both agencies on your behalf, making the choice of conveyancing firm a meaningful decision — not just a rubber stamp on your property purchase.

HDB flat transactions follow a slightly different route: they use the HDB Resale Portal and require HDB’s administrative approval, but buyers and sellers still appoint separate law firms (or use HDB’s approved conveyancing panel) to handle legal documents.

Step 1 — The Option to Purchase (OTP)

The OTP is a unilateral contract granting the buyer an exclusive right to purchase the property at an agreed price within a specified period. Under the Law Society of Singapore’s Conditions of Sale 2012, the standard OTP gives the buyer a 14-day option period from the date of grant. During this window, the property is effectively taken off the market.

Option fee: Typically 1% of the agreed purchase price, paid by cheque or cashier’s order to the seller (or seller’s lawyer). This fee is forfeited if the buyer does not exercise the option. It is not part of BSD — it is consideration for the option contract.

Exercising the OTP: The buyer exercises by paying a further 4% exercise fee (bringing the deposit to 5% total). BSD and ABSD are due within 14 days of exercising the OTP. Failure to pay on time attracts a late payment penalty of 5% per annum on the unpaid amount plus a flat 1% penalty.

Completion: Standard completion is 8–10 weeks after exercise. The buyer pays the remaining 95% of the purchase price (less any CPF utilised and bank loan disbursement) on completion day, and receives the keys and certificate of title.

Step 2 — The Sale and Purchase Agreement

Once the OTP is exercised, the seller’s lawyers typically issue a formal Sale and Purchase (S&P) Agreement within 2–4 weeks. The S&P Agreement sets out all conditions of sale including: completion date, vacant possession, included fixtures and fittings, representations and warranties on title, and risk allocation between exchange and completion.

For HDB resale flats, there is no separate S&P Agreement — instead, the parties register their Intent to Sell and Intent to Buy via the HDB Resale Portal, and HDB issues the resale completion letter setting the completion appointment.

Step 3 — Stamp Duties: BSD and ABSD

Stamp duties are collected by IRAS under the Stamp Duties Act (Cap. 312). They are the buyer’s obligation. The Buyer’s Stamp Duty (BSD) rates as at 7 June 2026 are:

| Purchase Price Bracket | BSD Rate |

|---|---|

| First S$180,000 | 1% |

| Next S$180,000 | 2% |

| Next S$640,000 | 3% |

| Next S$500,000 | 4% |

| Next S$1,500,000 | 5% |

| Remainder above S$3,000,000 | 6% |

Additional Buyer’s Stamp Duty (ABSD) applies on top of BSD for second and subsequent properties (Singapore Citizens), all purchases by Singapore Permanent Residents, and all purchases by foreigners and entities. For a complete ABSD table, see the LovelyHomes ABSD Singapore 2026 Guide.

Step 4 — Appointing Your Conveyancing Lawyer

You should appoint your conveyancing lawyer before you sign the OTP, so that they can advise you on the option terms and perform preliminary title searches. The Law Society of Singapore’s Conveyancing Practice Directions require lawyers to advise clients on conflicts of interest — the same law firm generally cannot act for both buyer and seller in the same transaction.

Your lawyer’s duties as buyer’s solicitor include: conducting all title searches; preparing or reviewing the S&P Agreement; handling BSD/ABSD payment to IRAS; lodging a caveat at SLA to protect your interest; liaising with your bank’s lawyers on mortgage documentation; requisitioning CPF funds from CPF Board; and attending completion to receive title from the seller.

Legal Fees and Disbursements

Law Society scale fees for residential conveyancing were abolished in 2009, meaning firms now charge freely. As a buyer, expect to pay S$2,200–S$5,000 in professional fees depending on transaction price and complexity. On top of professional fees, your lawyer will pass through disbursements — out-of-pocket costs charged at cost. Typical disbursements include:

- SLA title search: approx. S$30–S$80

- SLA caveat registration: approx. S$64.45 (includes GST)

- Bank mortgage registration: approx. S$350–S$500

- SLA transfer lodgement fee: approx. S$28–S$38 per instrument

- CPF requisition fee: approx. S$15–S$25 per utilisation

- Property valuation fee: S$300–S$1,200 depending on property type

Budget approximately S$500–S$1,500 in disbursements for a straightforward private resale transaction, in addition to professional fees.

Summary: Key Conveyancing Facts at a Glance

| Item | HDB Resale | Private Resale | New Launch |

|---|---|---|---|

| OTP / booking fee | S$1 (HDB prescribed) | Typically 1% of price | Booking fee 5% on S&P day |

| OTP exercise fee | N/A — HFE/portal process | 4% within 14 days | Further progress payments |

| BSD payment deadline | 14 days from HDB flat offer letter | 14 days from exercise | 14 days from S&P date |

| Standard completion period | 8–10 weeks (HDB schedule) | 8–12 weeks from exercise | On TOP or CSC date |

| Caveat filed by | HDB portal (automatic) | Buyer’s lawyer | Developer’s panel lawyer |

| Buyer legal fees (indicative) | S$1,500–S$2,200 | S$2,200–S$5,000 | S$2,200–S$3,500 |

| Seller legal fees (indicative) | S$1,000–S$1,800 | S$1,800–S$4,200 | N/A (developer pays) |

| CPF accrued interest on refund | 2.5% p.a. on OA withdrawn | 2.5% p.a. on OA withdrawn | 2.5% p.a. on OA withdrawn |

Worked Example: Mr and Mrs Koh Buy a Resale Condominium in Queenstown

Mr and Mrs Koh are Singapore Citizens purchasing their second property — a resale 2-bedroom condominium in Queenstown (District 3) for S$1,600,000. They are selling their HDB flat simultaneously (see our HDB Upgrader Guide 2026 for ABSD remission timing).

- Option fee (1%): S$16,000 — paid by cashier’s order on grant of OTP.

- BSD at exercise: 1% × S$180,000 + 2% × S$180,000 + 3% × S$640,000 + 4% × S$500,000 + 5% × S$100,000 = S$1,800 + S$3,600 + S$19,200 + S$20,000 + S$5,000 = S$49,600

- ABSD remission: If HDB sold within the stipulated window, ABSD is remitted for SC joint first-time private purchase. If outside the window, ABSD at 20% = S$320,000 — manage this timing carefully.

- Buyer’s legal fees: Approx. S$3,400 professional + S$900 disbursements = S$4,300

- Valuation fee: S$700

- Bank loan: S$1,200,000 at 3.0% p.a. over 30 years = S$5,058/mth; TDSR 36.1% on joint income S$14,000/mth — PASS.

- Completion cash balance: S$1,600,000 − S$80,000 (deposit) − S$1,200,000 (bank) − S$100,000 (CPF) = S$220,000 cash

The entire conveyancing process, from OTP grant to completion, spans approximately 10 weeks — aligning with the typical resale timeline shown in Figure 1 above.

What to Watch in 2026 and Beyond

Singapore’s conveyancing framework has remained largely stable since the Land Titles Act was modernised in 1994, but two pressure points are worth watching. First, the Ministry of Law has periodically reviewed whether HDB flat conveyancing should be further streamlined through the portal — licensed lawyers remain mandatory as at 2026. Second, the SLA has been progressively digitalising title documents towards a fully electronic land registry, which reduces search turnaround times and potentially disbursement costs.

For buyers, the practical implication is that while stamp duties remain the dominant cost item (dwarfing legal fees for most transactions), shopping for a competitive legal fee quote matters more the larger your transaction. For a second-property private condominium purchaser, ABSD is typically 20–60 times larger than legal fees — making ABSD remission timing the single most important conveyancing consideration of all.

Frequently Asked Questions

Can I use the same lawyer as the seller?

Generally no. The Law Society’s Conveyancing Practice Directions prohibit a single law firm from acting for both buyer and seller in the same residential transaction — a conflict-of-interest rule designed to protect both parties. Exceptions exist for new launch sales where developer panel lawyers act for the developer, but you as the buyer still engage your own firm. Having separate representation ensures your lawyer’s duty runs exclusively to you.

What happens if I miss the BSD payment deadline?

BSD and ABSD must be paid within 14 days of signing the OTP or S&P Agreement. Late payment attracts a penalty of 5% per annum on the unpaid stamp duty, plus a flat penalty of 1% of the unpaid duty under the Stamp Duties Act. Your conveyancing lawyer will typically pay stamp duties on your behalf immediately on instruction — ensure you have sufficient cleared funds in your account by the day of exercise.

What is a caveat and why does my lawyer lodge one?

A caveat under the Land Titles Act is a formal notice lodged at the Singapore Land Registry (via SLA) once you have exercised the OTP. It signals to the world — including any subsequent buyer, mortgagee, or judgment creditor — that you have a legal interest in the property. This prevents the seller from dealing with the property inconsistently with your purchase contract during the period between exercise and completion. The caveat lodgement fee is approximately S$64 and is a standard disbursement.

How does CPF work in a property purchase?

Singapore Citizens and PRs may use their CPF Ordinary Account (OA) savings towards the purchase price and monthly mortgage instalments, subject to a Valuation Limit (VL) of 100% of the lower of purchase price or valuation, and a Withdrawal Limit (WL) of 120% of VL for properties with at least 30 years remaining lease. CPF monies withdrawn for property must be refunded with 2.5% p.a. accrued interest upon sale — returned to your own CPF account. See our HDB Upgrader Guide for worked CPF refund calculations.

What is the difference between new launch and resale conveyancing?

New launch transactions involve a developer under a Housing Developers (Control and Licensing) Act licence. Instead of an OTP, you sign a Standard Sale and Purchase Agreement in the prescribed form under the Housing Developers Rules, and pay a booking fee (typically 5%) on the day of signing. Stamp duties are payable within 14 days. Completion occurs on the issue of the Temporary Occupation Permit (TOP) or Certificate of Statutory Completion (CSC), which may be 2–5 years from booking. Your CPF usage and bank loan terms must be structured to accommodate drawdowns aligned with the developer’s progress billing schedule.

Can a foreigner buy Singapore property and what additional steps apply?

Foreigners may purchase private condominium units, executive condominiums that have reached their 10-year privatisation mark, and Sentosa Cove landed properties — subject to the Residential Property Act (Cap. 274). The conveyancing process is identical, except that ABSD at 60% of the purchase price is payable by foreigners on any residential property purchase as at 2026. US, Swiss, Icelandic, Norwegian, and Liechtenstein nationals benefit from Free Trade Agreement (FTA) exemptions and are treated at Singapore Citizen rates for ABSD purposes. See our Singapore Foreign Buyer Property Guide 2026.

What happens on completion day?

Completion is typically conducted at the seller’s lawyer’s office. Your bank disburses the loan directly to the seller’s lawyers; your CPF Board requisition is remitted; and you or your lawyer presents cashier’s orders for any remaining cash. The seller hands over keys and access cards. Title transfers on completion — your lawyer registers the transfer at SLA (typically processed within 1–3 business days). You will receive a Land Register printout confirming your name as the registered proprietor.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Seller’s Stamp Duty (SSD) 2026: New 4-Year Holding Period and Rates

- Singapore Home Loan Complete Guide 2026: HDB Loans, Bank Loans, TDSR and MSR

- Singapore HDB Upgrading Guide 2026: Costs, ABSD and Step-by-Step Process

- Singapore Property Decoupling Guide 2026: Save ABSD, Costs and Risks

- Singapore Foreign Buyer Property Guide 2026: ABSD 60%, Eligibility and Costs

- Singapore HDB Resale Guide 2026: Buying and Selling HDB Resale Flats