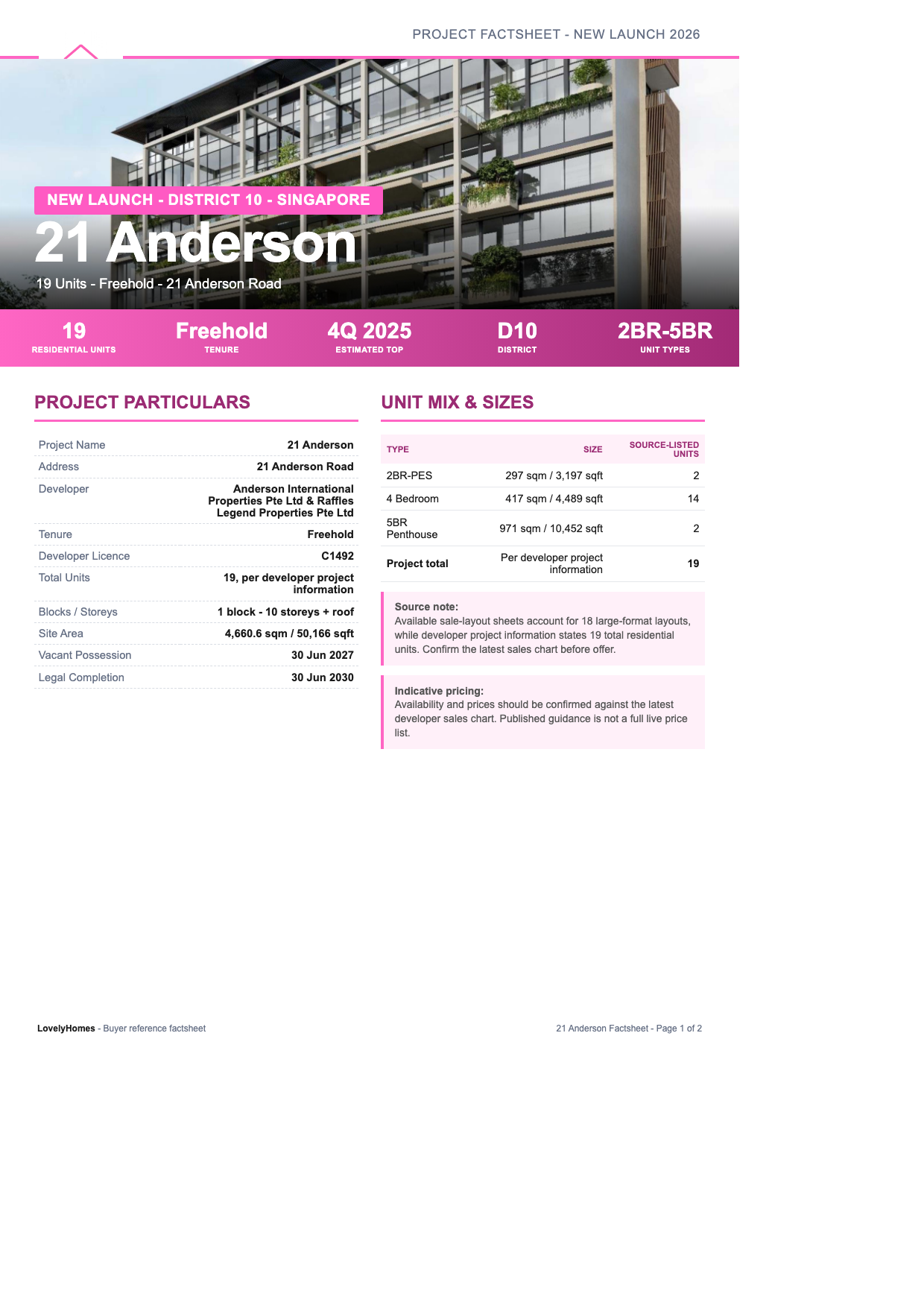

21 Anderson is a freehold boutique residence at Anderson Road, planned as a low-density District 10 address with 19 residential units, large-format homes and private-lift living.

01 – Address

Prime Anderson Road

District 10 location near Orchard, Tanglin, Stevens and the established embassy and lifestyle belt.

02 – Scale

19-Unit Freehold Collection

A rare low-density freehold format with large homes, generous car parking and a private residential setting.

03 – Design

Curated Consultant Team

Project materials identify Ernesto Bedmar Architects, P&T Consultants and Shunmyo Masuno / Japan Landscape Consultants.

Project At-a-Glance

Project Name

21 Anderson

Address

21 Anderson Road

District

District 10 – Tanglin

Tenure

Freehold

Developer

Anderson International Properties Pte Ltd & Raffles Legend Properties Pte Ltd

Developer Licence

C1492

Lot / Mukim

TS25 Lots 01519T & 01851T

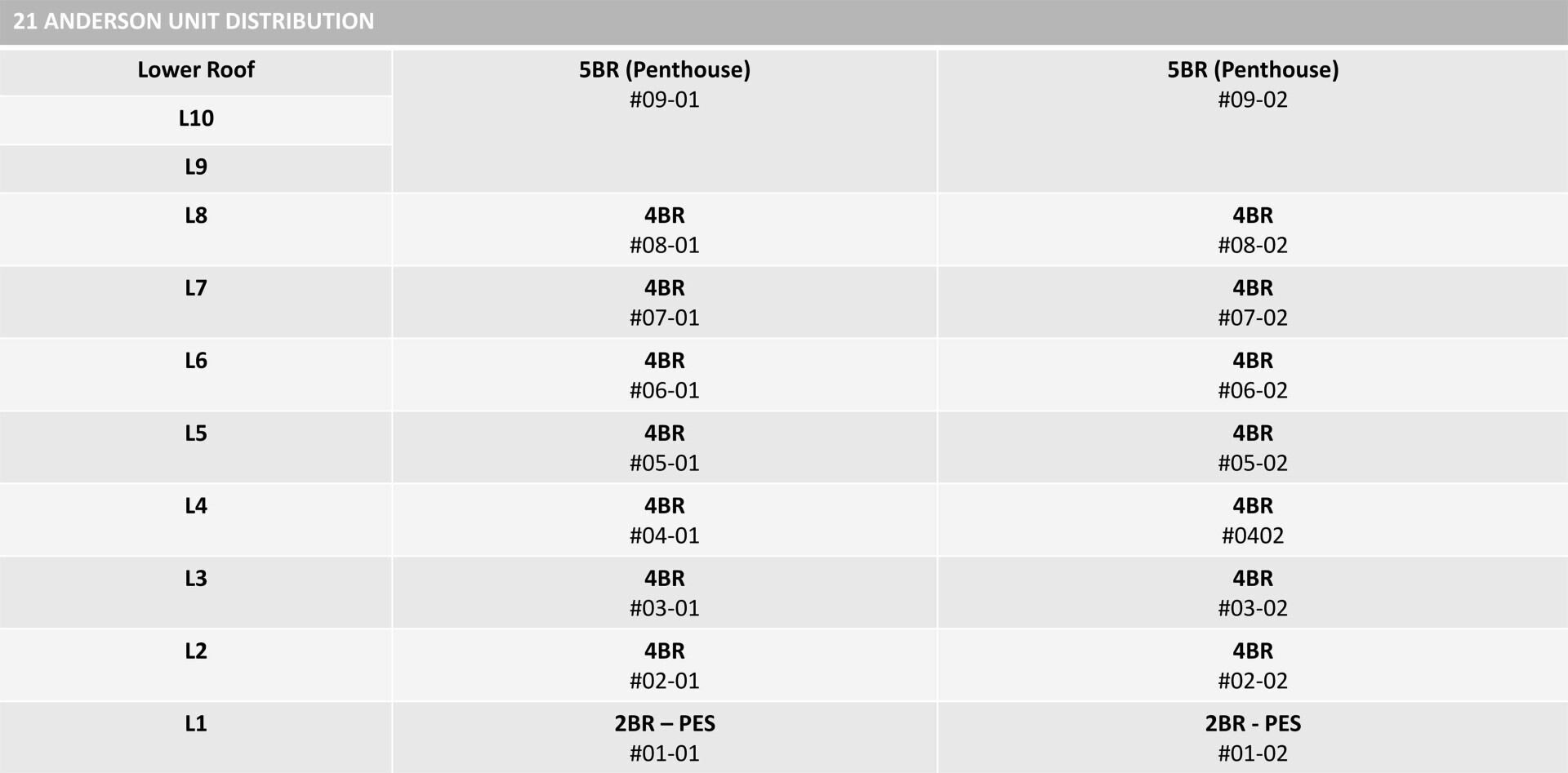

Total Units

19, per developer project information

Blocks / Storeys

1 block – 10 storeys + roof

Site Area

4,660.6 sqm / 50,166 sqft

Carpark

51 lots including EV fast-charging and handicap lots

Estimated TOP

4Q 2025

Vacant Possession

30 Jun 2027

Legal Completion

30 Jun 2030

Unit Mix and Sizes

Type

Approx. Size

Listed Units

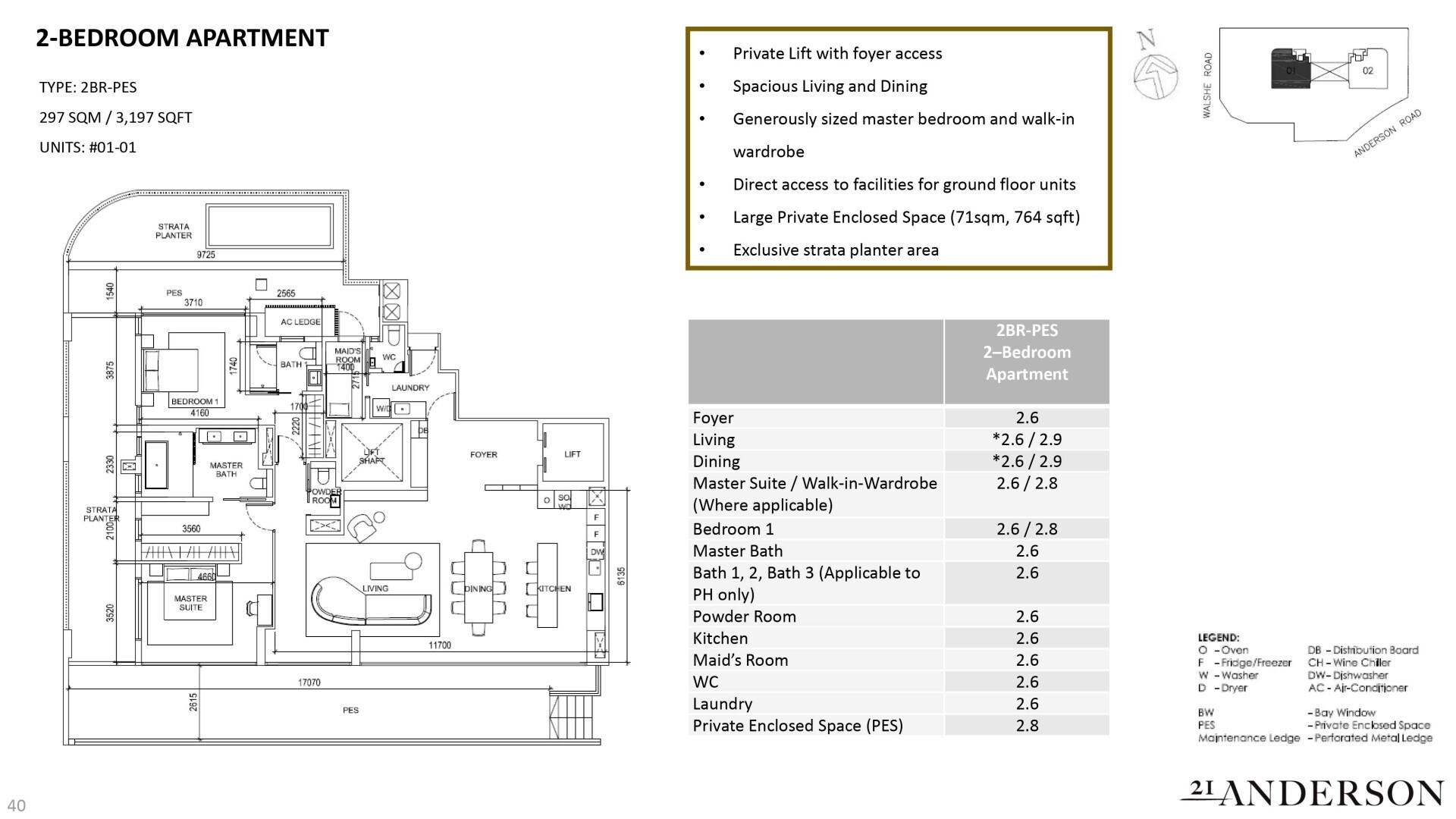

2BR-PES

297 sqm / 3,197 sqft

2

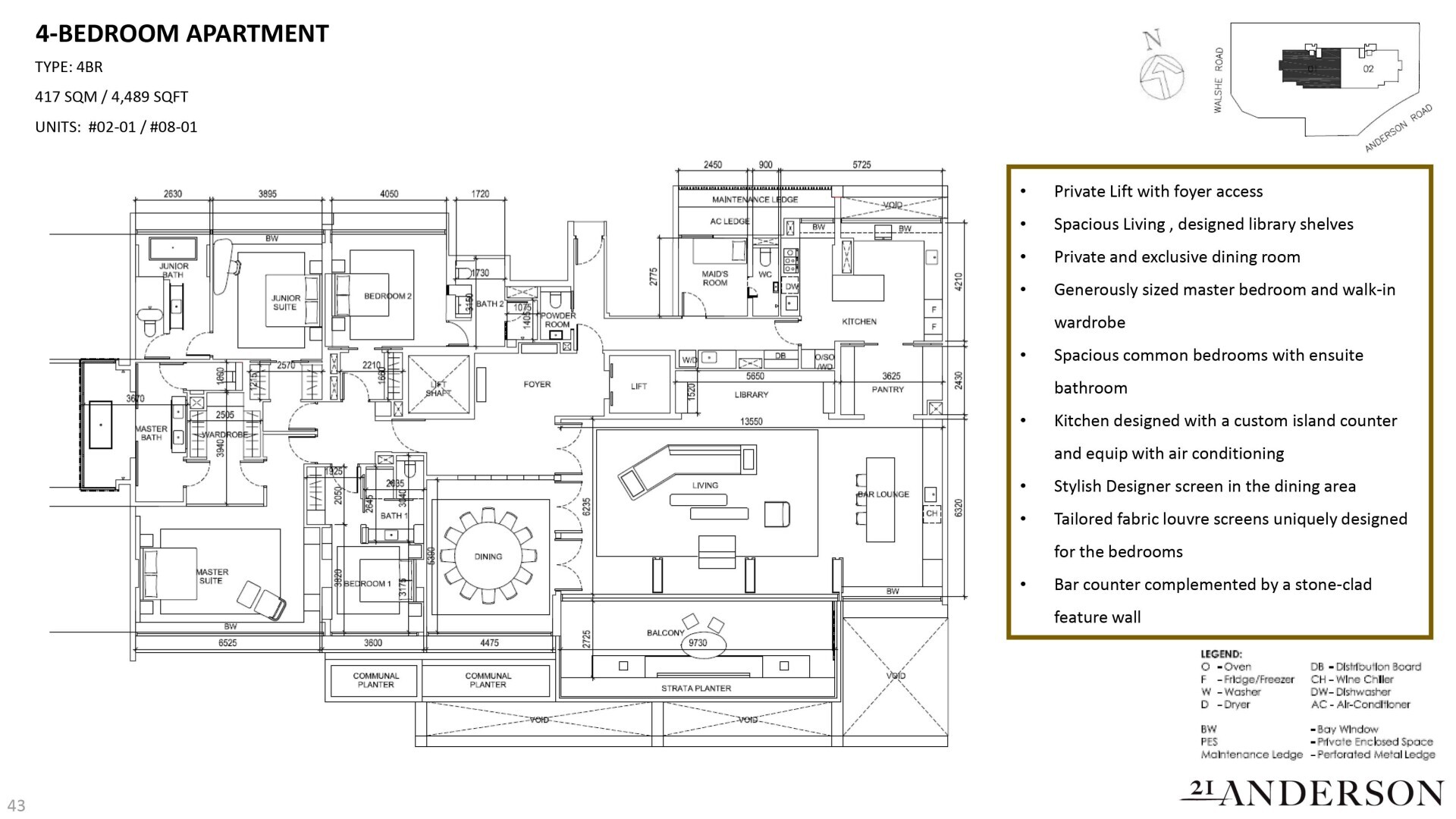

4 Bedroom

417 sqm / 4,489 sqft

14

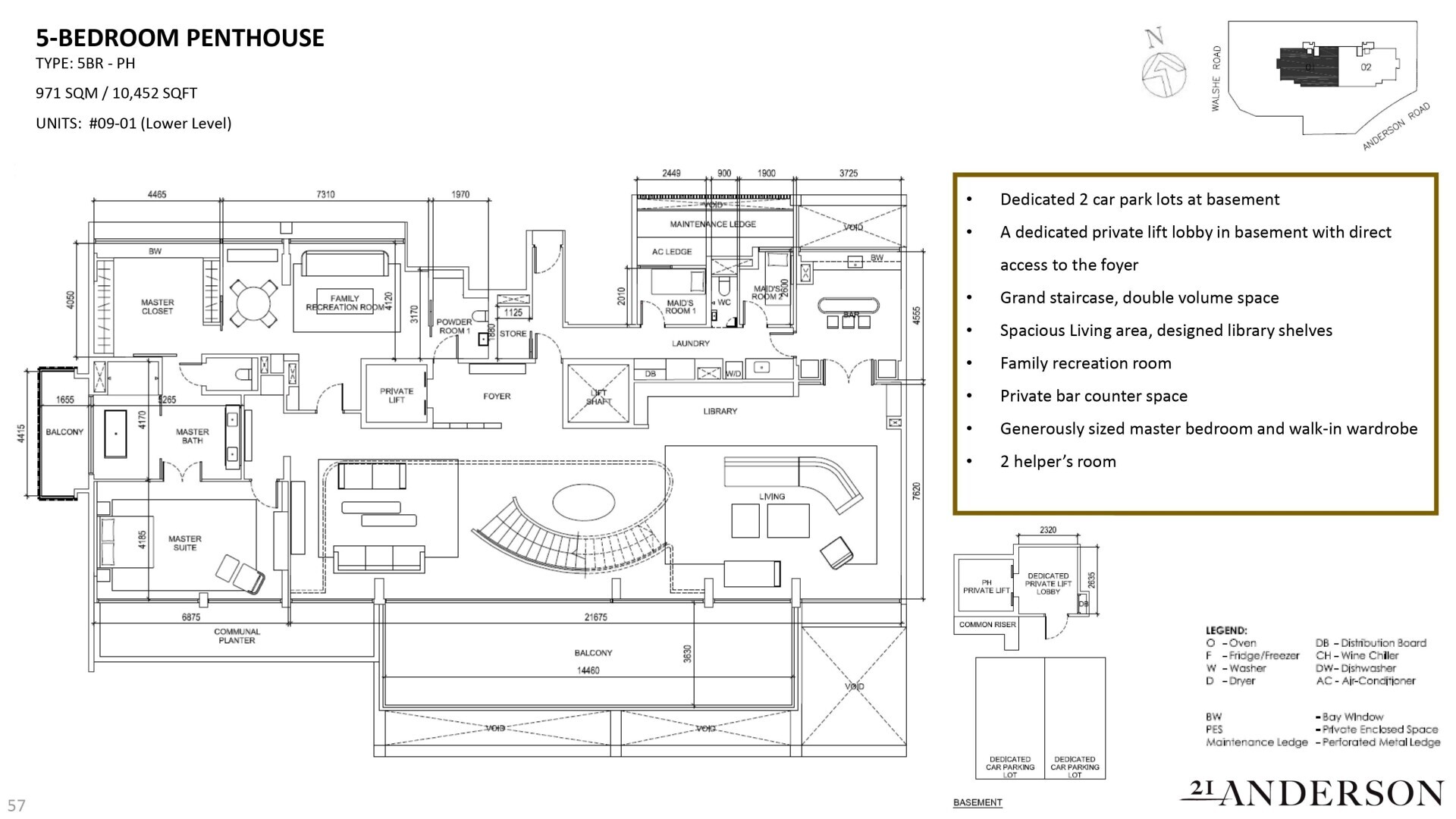

5BR Penthouse

971 sqm / 10,452 sqft

2

Project Total

Per developer project information

19

Unit mix note: Available sale-layout sheets account for 18 large-format layouts, while developer project information states 19 total residential units. Confirm the latest sales chart and balance-unit availability before offer.

Indicative Pricing

2BR-PES

Confirm Latest

4 Bedroom

Confirm Latest

5BR Penthouse

Confirm Latest

Pricing, discounts and availability change with the developer sales chart. No fixed price is stated here unless confirmed against the latest official price list.

Why Buyers Are Watching

01Freehold District 10 rarity. A small-format Anderson Road development with only 19 residential units stated in project information.

02Large homes. Available layout sheets focus on very large 2BR-PES, 4 Bedroom and 5BR Penthouse residences.

03Private-lift living. The project brief positions homes around privacy, premium appliances and generous residential proportions.

04Landscape-led setting. Shunmyo Masuno / Japan Landscape Consultants is listed as landscape architect in the project brief.

05Convenient access. Project materials cite proximity to Stevens MRT, Orchard Road, Tanglin and major expressway connections.

Location and Connectivity

MRT

Stevens MRT

Project brief references approximately 12 minutes’ walk / 800m to Stevens MRT on the TEL and Downtown Line.

Road

Prime Central Access

Near Orchard Road, Tanglin, Stevens Road and central expressway links.

Lifestyle

Orchard and Tanglin

Project materials cite Orchard shopping malls, Tanglin Club, American Club and nearby hotels.

Healthcare

Medical Amenities

Project FAQ references Gleneagles, Mount Elizabeth Orchard, Novena Specialist Center and Tan Tock Seng.

Schools Nearby

Within 1km

Anglo-Chinese School (Primary), Singapore Chinese Girls’ School.

1km to 2km

Anglo-Chinese School (Junior), St. Joseph’s Institution Junior.

Other Nearby References

Raffles Girls’ Secondary School and international school references appear in project location materials.

Lifestyle and Amenities

Shopping

Project materials reference Orchard Road shopping including Forum, Shaw House, ION Orchard, Takashimaya and Wisma Atria.

Clubs and Hotels

Tanglin Club, American Club, Shangri-La, Pan Pacific Orchard and Novotel on Stevens Road are cited in the project FAQ.

Green and Dining

Singapore Botanic Gardens and Dempsey are nearby lifestyle references in the project materials.

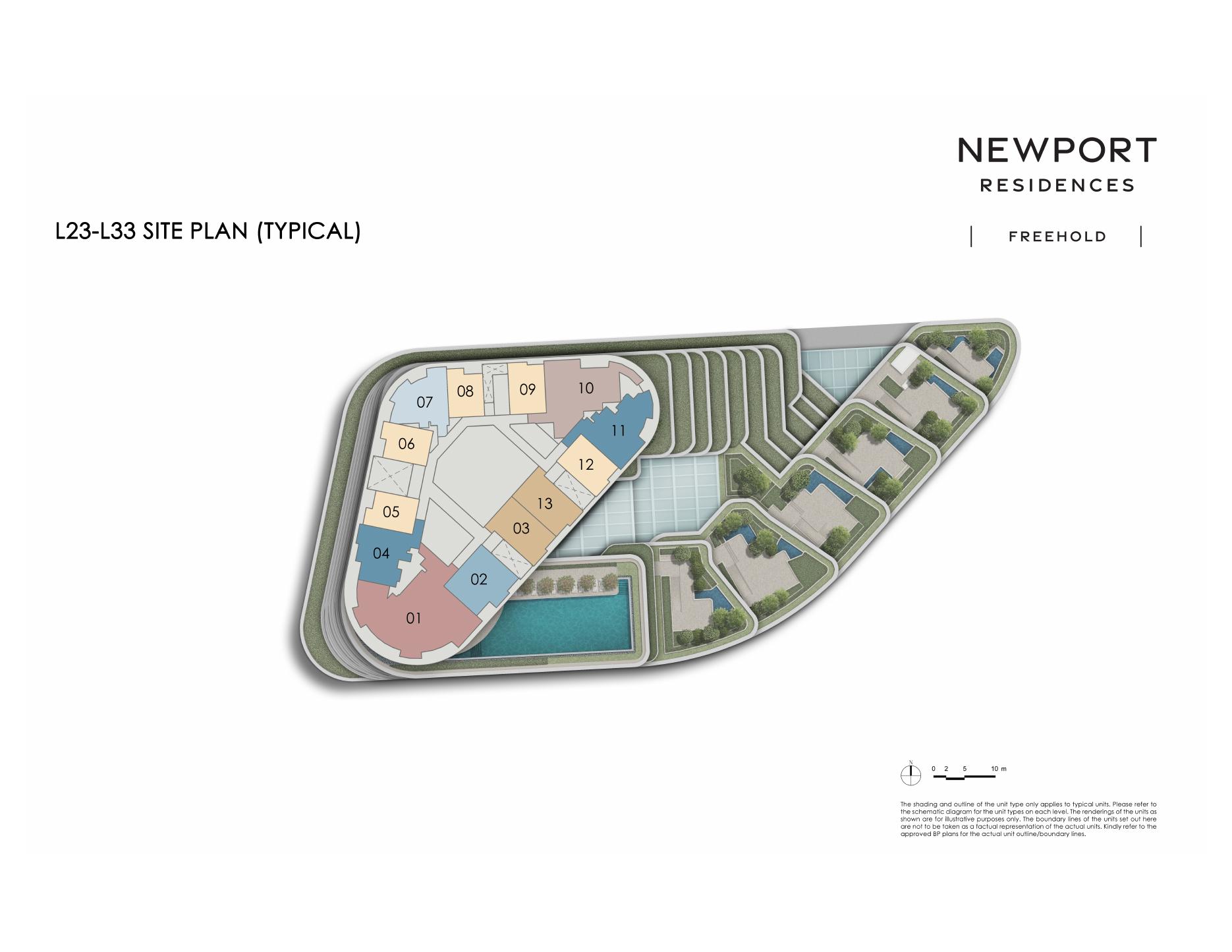

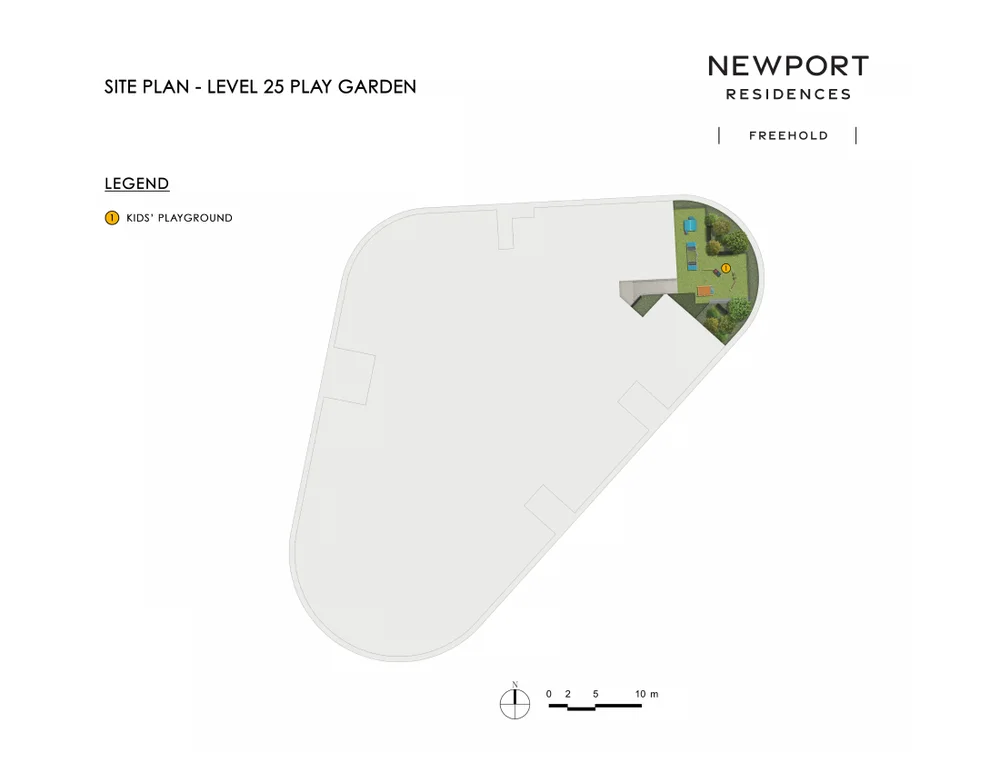

Site Plan

Actual site plan reference from project materials.

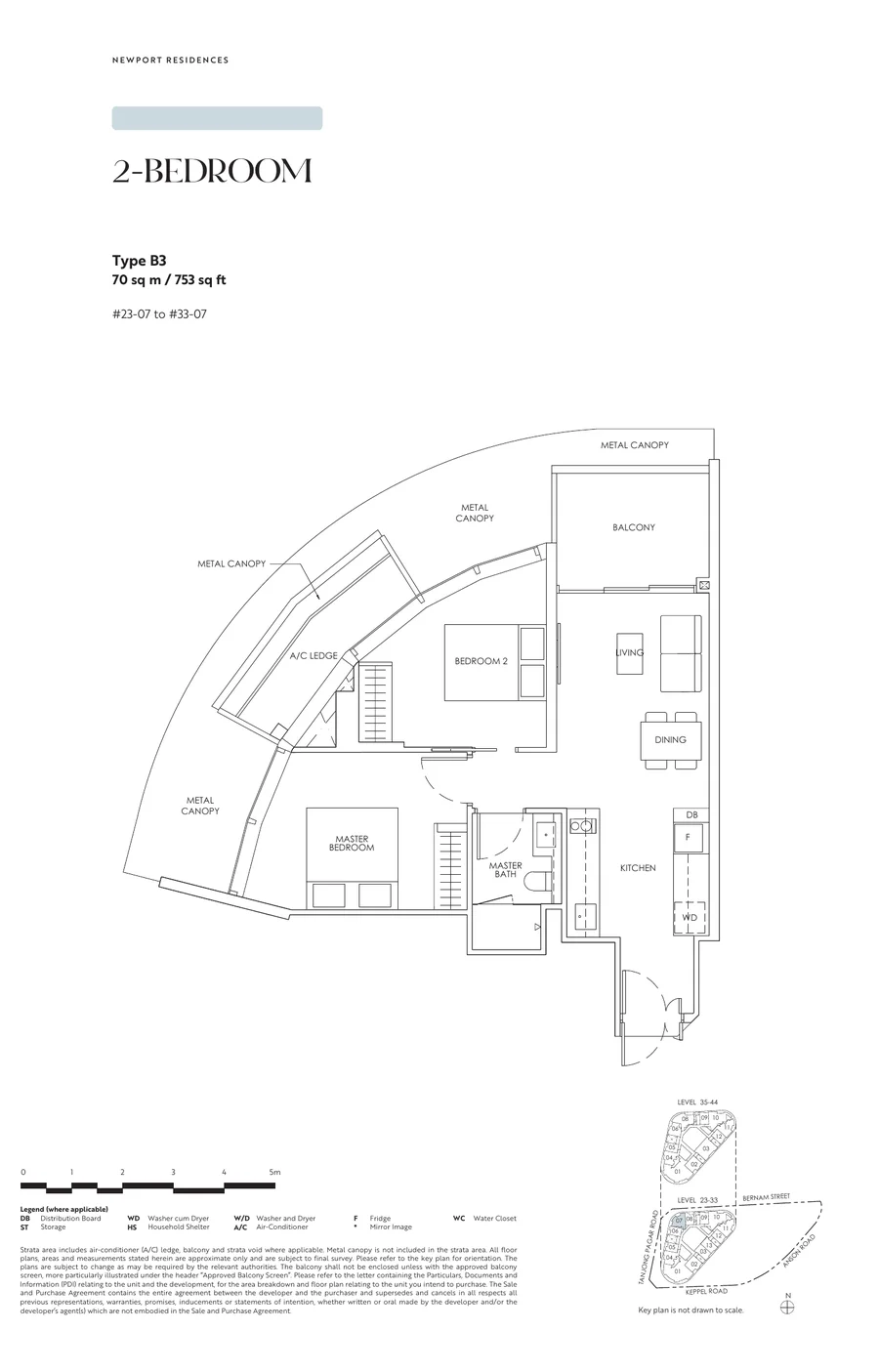

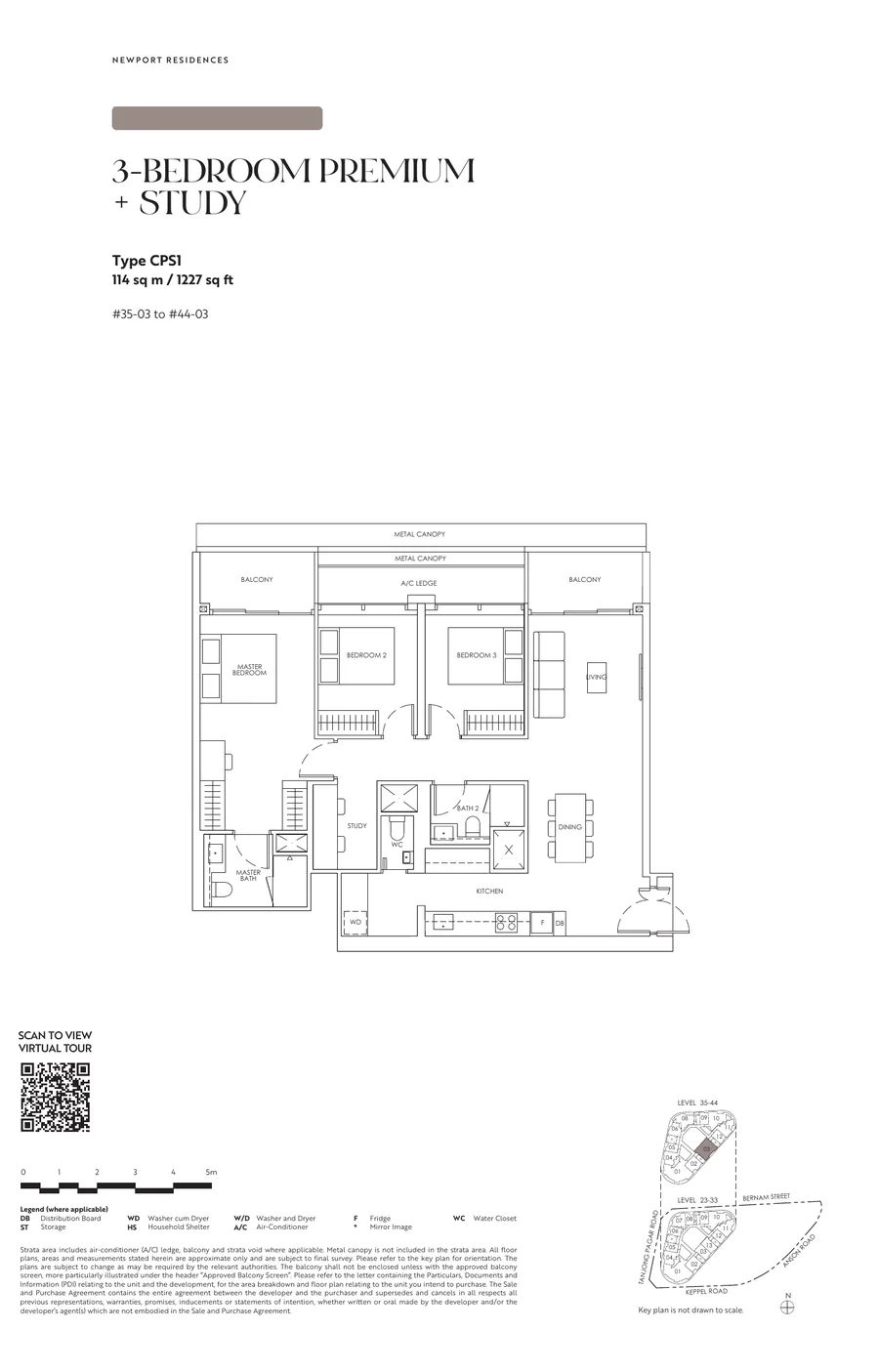

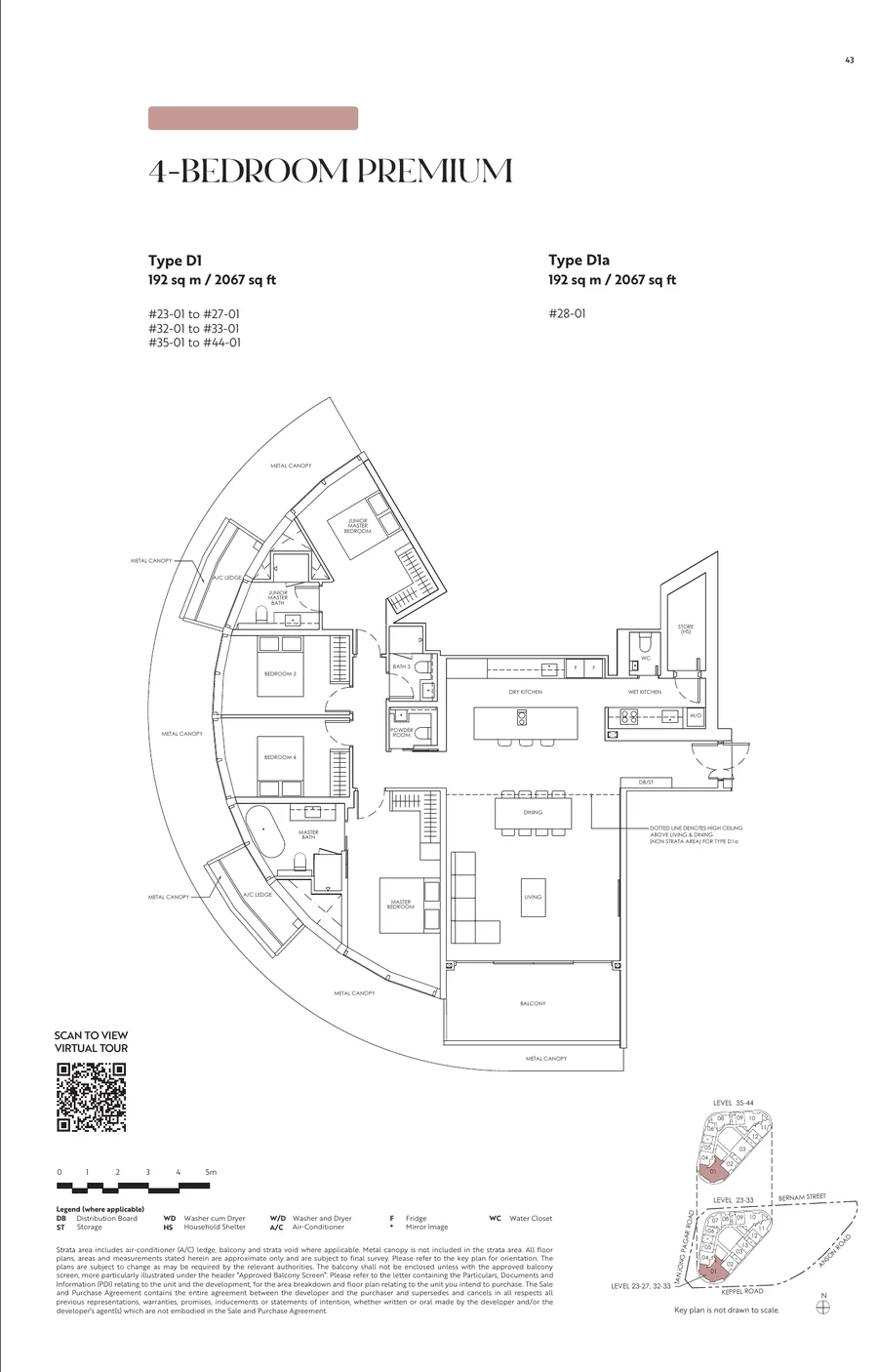

Floor Plans (Selected)

2BR-PES – 297 sqm / 3,197 sqft

4 Bedroom – 417 sqm / 4,489 sqft

5BR Penthouse – 971 sqm / 10,452 sqft

Source note: The available 21 Anderson e-brochure starts at 2-bedroom layouts; no 1-bedroom or 3-bedroom plan is included in the local source set, so selected thumbnails show the representative 2-bedroom, 4-bedroom and penthouse layouts only.

Full Floor Plans and E-Brochure

Download the source e-brochure for full layout references and project information.

Layout note: Available unit mix does not list 1 Bedroom or 3 Bedroom types for 21 Anderson.

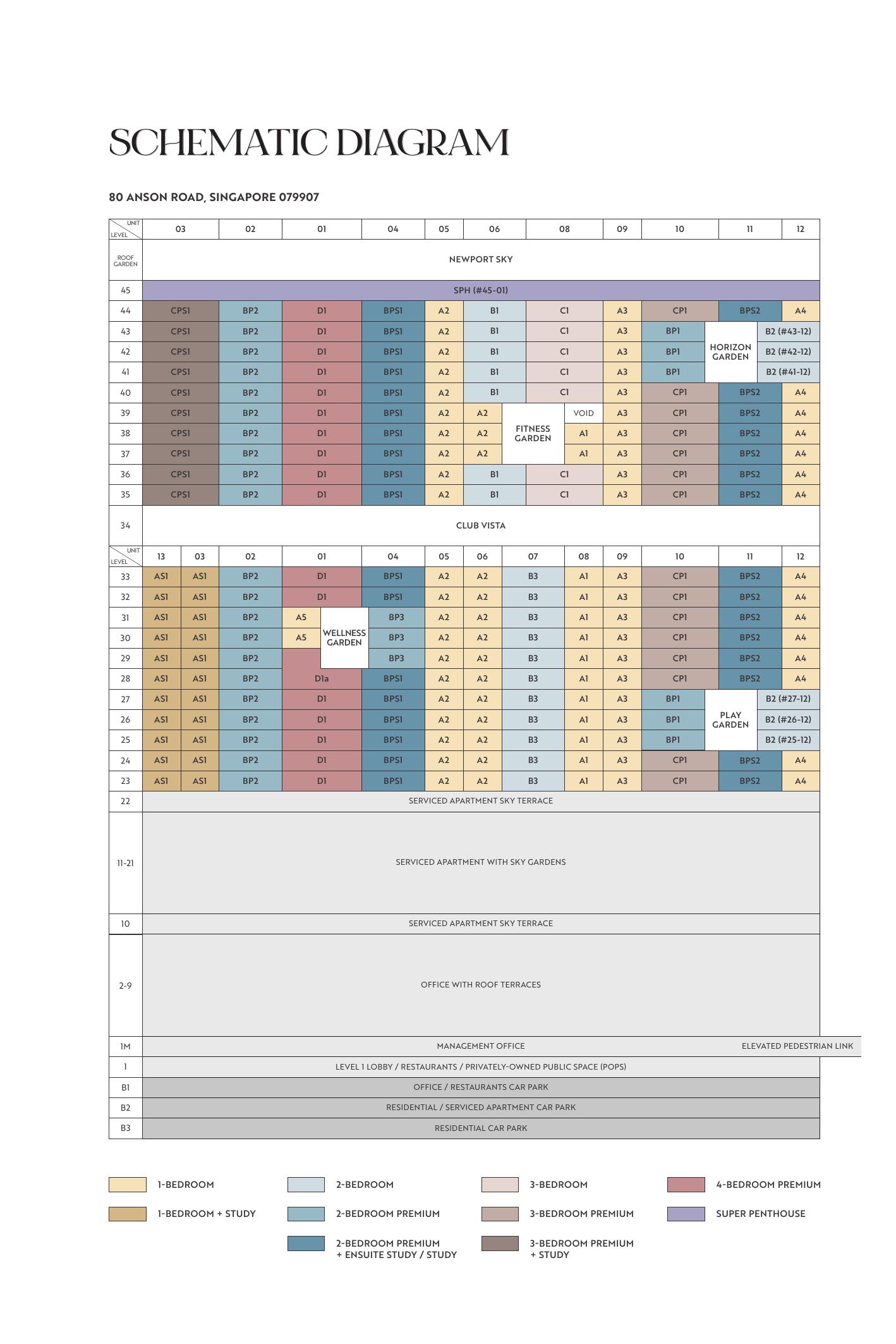

Elevation and Stack Chart

Elevation and stack chart reference from project materials.

Facilities (30+)

32m x 5m swimming poolKids poolJacuzziClubhouseGarden pavilionTechnogym-equipped gymBasement arrival lobbyConciergeSide gate to Walshe RoadEV fast-charging lots

Gallery

Developer and Consultant Team

Anderson International Properties Pte Ltd & Raffles Legend Properties Pte Ltd

The developer entities above are stated in the official project information. The project brief also associates the lifestyle concept with Kheng Leong Group.

Design Architect

Ernesto Bedmar Architects

Project Architect

P&T Consultants Pte Ltd

Landscape Architect

Shunmyo Masuno / Japan Landscape Consultants

Developer Licence

C1492

Tenure

Freehold

Sustainability and Specifications

EV charging: Project brief states 51 carpark lots including 2 EV fast-charging lots and handicap lots.

Premium fittings: Gaggenau appliances are listed in the project brief, with enhanced penthouse provisions.

Security: Project FAQ states audio/video intercom and card access provisions.

Private residential format: Project brief positions 21 Anderson around large-format homes, private lift access and landscaped common spaces.

21 Anderson is located at 21 Anderson Road in prime District 10, within the Tanglin planning area.

Who is the developer for 21 Anderson?

The developer entities stated in the project information are Anderson International Properties Pte Ltd and Raffles Legend Properties Pte Ltd. The lifestyle and design concept is associated with Kheng Leong Group in the project brief.

What is the tenure of 21 Anderson?

21 Anderson is a freehold residential development.

How many units are there?

Developer project information states 19 total residential units. Available layout sheets show large-format 2BR-PES, 4 Bedroom and 5BR Penthouse layouts.

What is the expected TOP for 21 Anderson?

The project brief states an estimated TOP of 4Q 2025. The e-brochure states expected vacant possession on 30 Jun 2027 and expected legal completion on 30 Jun 2030.

What unit types are available?

Available layout sheets include 2BR-PES at 297 sqm / 3,197 sqft, 4 Bedroom at 417 sqm / 4,489 sqft, and 5BR Penthouse at 971 sqm / 10,452 sqft. No 1 Bedroom or 3 Bedroom unit type is listed in the available unit mix.

What facilities are planned?

Facilities listed in the project brief include a 32m x 5m swimming pool, kids pool, jacuzzi, clubhouse, garden pavilion, Technogym-equipped gym, concierge and basement arrival lobby.

Are floor plans available for download?

Yes. The selected floor-plan section shows representative layouts by available unit type, and the full e-brochure / floor-plan PDF is available from the download button.

Ready to see 21 Anderson in person?

Request the latest price list, balance units, floor-plan pack and viewing slots before comparing against other District 10 options.

Compare boutique and large-scale launches across Singapore districts.

DISCLAIMER: All information is compiled from developer-issued and publicly available project materials for informational purposes only. Prices, unit mix, specifications, timelines and availability are subject to change without notice. This page does not constitute an offer to buy or sell. Seek advice from a licensed property agent and legal counsel. LovelyHomes.com.sg is an independent editorial platform. Agency Licence: L3010858B.

Landed property in Singapore is the apex of local real estate — a scarce, tightly regulated asset class that accounts for just 5% of residential dwellings, occupies about 80 sqkm of the island, and is almost entirely reserved for Singapore Citizens. For buyers who qualify, landed homes deliver three things that condominiums cannot: private land ownership, multi-generational living space, and freehold tenure on the overwhelming majority of stock. This 2026 guide explains the four main landed typologies (Detached, Semi-Detached, Terrace and Cluster/Strata-Landed), the Residential Property Act rules that govern foreign and PR ownership, typical pricing by district, and the structural demand drivers that have made landed property Singapore’s most consistent long-term outperformer.

Figure 1: Singapore landed property — Good Class Bungalow, Detached, Semi-Detached, Terrace and Cluster.

Quick Answer

Landed property = Detached, Semi-Detached, Terrace, and Cluster/Strata-Landed.

Good Class Bungalow (GCB): detached on ≥ 1,400 sqm in one of 39 gazetted GCB areas.

Ownership: Singapore Citizens only (landed non-Sentosa); PRs and foreigners need LDAU approval.

Tenure: majority freehold; some 99-year and 999-year stock in specific estates.

Share of housing stock: approx. 5% of Singapore’s residential dwellings.

Median price (2026): Semi-D S$5.8M–S$7.5M; Terrace S$4.2M–S$5.8M; GCB S$25M+.

Sentosa Cove: the only landed enclave open to non-resident foreigners, subject to LDAU approval.

What Counts as Landed Property in Singapore

Under the Residential Property Act (RPA), “landed residential property” comprises detached, semi-detached and terrace houses, and — for legal purposes — vacant residential land. Strata-landed (cluster) housing sits in a hybrid zone: it is physically a landed house but legally a strata lot under the Building Maintenance and Strata Management Act.

Typology

Definition

Key Characteristics

Detached / Bungalow

Standalone house on its own plot; minimum 400 sqm plot by URA.

Full privacy; highest price point. GCB sub-category at 1,400+ sqm.

Semi-Detached

Pair of houses sharing one party wall; minimum 200 sqm per plot.

Second most expensive typology; balances space and price.

Terrace

Row houses sharing two party walls; minimum 150 sqm per plot.

Most affordable landed entry; concentrated in older estates.

Cluster / Strata-Landed

Gated enclave of landed units sharing common facilities (pool, gym, guardhouse).

Body-corporate-managed; foreigners eligible without LDAU approval (as strata).

Good Class Bungalow (GCB)

Detached on ≥ 1,400 sqm in a gazetted GCB Area (39 areas).

Singapore’s most exclusive housing; SC buyers only.

Shophouse (conservation)

Historically residential/commercial; zoned on a case-by-case basis.

Commercial-dominant usage today, but some remain residential.

The 39 Good Class Bungalow Areas

Good Class Bungalows — the pinnacle of Singapore residential — are concentrated in 39 gazetted areas. Each plot must meet four criteria: (1) minimum 1,400 sqm plot size, (2) minimum 18.5m plot width, (3) no more than two storeys plus an attic, and (4) at least 3m side setback. The best-known GCB areas include Tanglin, Nassim, Queen Astrid, Bishopsgate, Chatsworth, Cluny, Cornwall, Dalvey, Gallop, White House Park and Holland Park.

Key takeaway

There are approximately 2,800 GCB plots in Singapore — a fixed, non-expandable pool. The scarcity alone has driven GCB prices to compound at 7%–9% p.a. over the last two decades, outpacing the broader residential index.

Who Can Buy Landed Property in Singapore?

Singapore Citizens

SCs have the fewest restrictions: they can purchase any landed property on the mainland, in Sentosa Cove, or in strata form, subject only to ABSD rules (0% on 1st, 20% on 2nd, 30% on 3rd+ property) and standard financing rules.

Singapore Permanent Residents (PR)

PRs cannot purchase landed property on the mainland without specific approval from the Land Dealings (Approval) Unit (LDAU) of the Singapore Land Authority. In practice, LDAU approval for PRs is rare — usually granted only for PRs of at least 5 years’ standing who demonstrate substantial economic contribution to Singapore. PRs may freely purchase strata-landed (cluster) housing and Sentosa Cove landed (subject to LDAU).

Foreigners (Non-Resident)

Non-resident foreigners may purchase Sentosa Cove landed property (subject to LDAU approval, typically granted for 1 plot with owner-occupation conditions), and may freely purchase strata-landed cluster housing. Mainland landed is effectively closed to foreign buyers.

Entities (Companies, Trusts)

Entities are generally prohibited from owning landed residential property. Certain family-office and LDAU-approved trusts have been granted exceptions, but these are the minority. Entities face a 65% ABSD rate across the board.

Buyer Type

Mainland Landed

Strata-Landed (Cluster)

Sentosa Cove

Singapore Citizen

Yes

Yes

Yes

PR (≥ 5 yrs)

LDAU approval (rare)

Yes

LDAU approval

PR (< 5 yrs)

Effectively No

Yes

Rare

Foreigner

No (mainland)

Yes

LDAU approval

Entity

No

Yes (subject to ABSD 65%)

No

Tenure: Freehold, 999-Year and 99-Year Landed

Most landed stock in Singapore is freehold, a product of colonial-era land grants. A material minority is 999-year leasehold — functionally equivalent to freehold for all planning purposes. A smaller segment is 99-year leasehold, typically in newer developments such as Sentosa Cove and specific GLS strata-landed projects.

Freehold / 999-year command a 5%–12% price premium over 99-year peers. At the 60-year leasehold mark, CPF usage begins to taper (by the 30-year remaining point, CPF is materially restricted), which structurally caps the buyer pool for older leasehold landed — and compresses prices.

Price Benchmarks by Typology and District (2026)

Typology

Representative Districts

Tenure Mix

2026 Price Band

Detached (GCB)

D10 Tanglin / D11 Nassim

Freehold

S$25M – S$80M+

Detached (non-GCB)

D10 / D11 / D15

Freehold

S$8M – S$18M

Semi-Detached

D10 Holland / D11 Novena / D15 Katong

Freehold

S$6.5M – S$9M

Semi-Detached

D13 Potong Pasir / D14 Eunos / D19 Hougang

Freehold / 999-yr

S$4.5M – S$6M

Terrace (Inter / Corner)

D10 / D11 / D15

Freehold

S$5M – S$7.5M

Terrace (Inter / Corner)

D13 / D14 / D19 / D25

Freehold / 999-yr / 99-yr

S$3M – S$5M

Cluster / Strata-Landed

D10 / D11 / D16 / D19

Freehold / 99-yr

S$3.5M – S$7M

Sentosa Cove Bungalow

D4 Sentosa

99-yr

S$15M – S$40M+

Cluster Housing: The Strata-Landed Alternative

For buyers who want a landed lifestyle without the upkeep burden — and for PRs and foreigners whose mainland landed options are effectively zero — cluster (strata-landed) housing offers a compromise. Cluster developments are gated enclaves of terraces or semi-detached units, managed under a body corporate with shared facilities (swimming pool, gym, tennis court, 24/7 security). Because the units are legally strata lots rather than landed titles, they fall outside the RPA’s landed-ownership restrictions.

Flagship cluster developments include The Shaughnessy (Holland), Victoria Park Villas (Bukit Timah), Jardin (Bukit Timah) and Archipelago (Bedok Reservoir). Pricing typically runs at a 15%–25% discount to comparable freehold detached landed within the same district.

Financing Landed Property

Landed purchases are subject to the same LTV, TDSR and MSR frameworks as condominiums — up to 75% LTV for first housing loan, stepped down for second and subsequent loans. Because absolute quantums are higher, the cash requirement is significant. For a S$6M terrace:

Line Item

Amount

Purchase Price

S$6,000,000

Buyer’s Stamp Duty (BSD)

S$229,600

ABSD (SC 1st property)

S$0

Legal fees

S$5,000

Minimum Cash Downpayment (5%)

S$300,000

CPF + Cash Downpayment (20%)

S$1,200,000

Loan Quantum (75%)

S$4,500,000

Monthly Mortgage (4.0%, 25-yr)

Approx. S$23,750

Total Cash Upfront

S$534,600

Stress-test your borrowing envelope using our TDSR/MSR guide. Most banks will require comfort on both household income resilience and liquid asset reserves for landed quantums > S$5M.

The Landed Investment Case

Scarcity

Singapore’s landed stock is capped. URA’s Master Plan does not meaningfully add new landed zoning — the only additions are small infill sites and occasional en-bloc redevelopments. The approximately 72,000 landed units on the island represent a finite pool that cannot grow in line with population or wealth.

Demand: Second-Generation Singaporean Wealth

A generation of Singaporeans who benefited from the 1998–2008 and 2013–2023 property cycles are now handing down wealth. Landed is the preferred destination for that capital: it is stable, defensible, and tax-efficient (no capital gains tax on primary residence). The “upgrade ladder” — HDB → condo → landed — is a real phenomenon driving steady demand at the mid-tier.

Underperformance in Weak Markets

The counter-argument: landed prices are less liquid than condominiums. In the 2008–2009 GFC drawdown and the 2014–2017 cooling-measures cycle, landed stock took 18–30 months longer than the condo market to clear at the new equilibrium. Buyers with time horizons shorter than 10 years should consider this liquidity premium.

Landed vs Condominium: Trade-offs

Dimension

Landed

Condominium

Privacy

Full

Shared common areas

Land ownership

Yes (freehold / 99-yr)

No (strata lot)

Maintenance

Owner’s responsibility

Managed by MCST

Facilities

None unless built by owner

Pool, gym, security, lounges

Renovation flexibility

High (subject to URA GFA)

Low (interior only, MCST rules)

Price entry (2026)

S$3.5M – S$80M+

S$1.2M – S$20M+

Typical absolute quantum

S$4.5M+ mid-tier

S$1.8M+ mid-tier

Foreign/PR eligibility

Restricted (mainland)

Open to all

Annual property tax (AV)

Generally higher (land)

Lower per sqft

Capital growth 2000–2024

Approx. 6.2% p.a.

Approx. 4.8% p.a.

Regulatory and Planning Considerations

Envelope Control

URA enforces an “Envelope Control” regime across most landed estates, capping building height (typically 2 storeys plus attic; 3 storeys in designated zones), setback distances (at least 2m front, 2m side for terraces), and GFA. Reconstruction or redevelopment must comply with the prevailing envelope.

Conservation Areas

Certain shophouse and black-and-white bungalow zones are gazetted conservation areas, subject to URA’s Conservation Guidelines. External alterations require URA written approval and must preserve heritage character.

Drainage Reserves and Plot Ratio

Some landed plots carry URA drainage reserves or setback obligations that effectively reduce buildable GFA. Always confirm with URA’s Master Plan zoning map and the developer’s Schedule of Conditions before offering.

Frequently Asked Questions

Can a foreigner buy landed property in Singapore?

Not on the mainland — the Residential Property Act restricts mainland landed to Singapore Citizens. Foreigners can purchase strata-landed (cluster) housing freely, and Sentosa Cove landed with LDAU approval.

What is the minimum plot size for a bungalow?

400 sqm under URA guidelines. A Good Class Bungalow requires a minimum 1,400 sqm plot in one of 39 gazetted GCB areas.

Is a cluster house considered landed?

Physically yes, legally no. Cluster units are strata lots under BMSMA and are not subject to the RPA’s landed restrictions. Foreign and PR buyers can purchase them without LDAU approval.

Can a PR buy a mainland terrace house?

Only with LDAU approval, which is granted selectively to PRs with substantial economic contribution to Singapore. Most PR applications for mainland landed are declined.

How is property tax calculated on landed?

Based on Annual Value (AV) set by IRAS, which reflects the market rental value of the property. Owner-occupier rates range from 0% to 32% (progressive); non-owner-occupier rates from 12% to 36%. See our property tax guide.

What is the difference between GCB Area and GCB?

A GCB Area is a gazetted zone (one of 39) in which GCB controls apply. A GCB is a specific detached bungalow within a GCB Area that meets the plot-size and setback criteria. A house in a GCB Area that does not meet GCB criteria is simply a detached house within that zone.

Can I convert a terrace into a semi-detached?

In theory yes, subject to URA planning approval and sufficient GFA, side setback and party-wall agreements. In practice, such conversions are rare and require consent from the neighbouring unit owner.

Is Sentosa Cove a good buy?

Sentosa Cove is Singapore’s only waterfront landed enclave and the only mainland-adjacent landed market open to foreign buyers (with LDAU approval). It has underperformed the broader landed index since 2014 due to cooling measures and limited tenant pool, but has recently re-rated on non-resident demand.

Disclaimer: Specifications, price bands and eligibility rules are current as at the time of writing. Always verify regulatory positions with URA, SLA and a qualified conveyancing lawyer before committing to a landed purchase. Nothing on this page is financial, tax, or legal advice.

Newport Residences is a 246-unit freehold residential development in District 02, Singapore, developed by CDL with an estimated TOP of 2028.

01 · Location

District 02 Address

Well-connected neighbourhood with access to public transport, schools, and lifestyle amenities.

02 · Scale

246 Residences

Freehold development with quality fittings, smart-home provisions, and full condominium facilities.

03 · Value

New-Launch Advantage

Progressive payment schedule, 12-month Defects Liability Period, and modern specifications throughout.

Project At-a-Glance

Project Name

Newport Residences

Developer

CDL

District

D02

Tenure

Freehold

Total Units

246

Est. TOP (VP)

2028

Est. Legal Completion

2031

Unit Mix and Sizes

Bedroom Type

Size (sqft)

Units

% of Total

Download the project factsheet for the full unit mix breakdown and confirmed sizes.

Refer to the developer’s official sales kit for confirmed unit types, sizes, and availability. Download factsheet (PDF).

Indicative Pricing

1BR

From S$1.359M

431-474 sqft

2BR

From S$2.076M

753 sqft

3BR

From S$3.460M

980 sqft

Current public balance-unit snapshot shows 1BR from S$1.359M, 2BR from S$2.076M, 3BR from S$3.460M and 4BR Premium from S$8.280M. Source: Newport Residences NewLaunches price list updated 4 Mar 2026, accessed 29 Apr 2026.

Why Buyers Are Watching

1

District 02 location — well-connected address with MRT access, expressways, and lifestyle amenities in an established residential corridor.

2

Freehold — Freehold title with no lease decay — perpetual ownership ideal for long-term holds and estate planning.

3

246 residential units — boutique scale ensuring exclusivity and a curated ownership community.

4

Developer pedigree — CDL brings a track record of quality residential development across Singapore’s private property market.

5

Progressive payment advantage — staggered cash outlay during construction typically saves S$30,000–S$60,000 in loan interest compared to a full resale drawdown.

6

12-month Defects Liability Period — legally binding developer obligation to rectify defects at no cost within 12 months of TOP.

Location and Connectivity

Transport

MRT Access

Conveniently located near MRT stations connecting to the wider Singapore rail network.

Expressways

Road Connectivity

Access to major expressways for quick connections to the CBD, Changi Airport, and key destinations.

Lifestyle

Shopping & Dining

Nearby malls, hawker centres, supermarkets, and F&B within the immediate neighbourhood.

Schools

Education Belt

Primary and secondary schools within 1–2 km, with tertiary institutions in the broader district.

Newport Residences elevation and stack chart from source schematic diagram.

Facilities (30+)

Swimming PoolGymnasiumFunction RoomsBBQ PavilionsChildren’s PoolJacuzziClub LoungeGarden PavilionSky TerraceYoga LawnSmart Home SystemEV Charging24-Hour SecurityBicycle BaysPneumatic Waste System

Gallery

Developer and Consultant Team

CDL

Developer of Newport Residences with residential development expertise in Singapore’s private property market. Consultant team details are available in the project factsheet.

Developer

CDL

District

D02

Estimated TOP

2028

Sustainability and Specifications

BCA Green Mark: Designed to meet BCA Green Mark standards with energy-efficient envelope and water-efficient fittings.

Smart Home: Smart home management provisions across all units for access control and utilities.

EV Infrastructure: Electric vehicle charging provisions in basement carpark.

Quality Finishes: Premium materials and fittings in line with developer specifications throughout.

Project Timeline

2023–2024

Land Award & Licence

2024–2025

Sales Launch

2025–2028

Construction Phase

2028

Estimated TOP (VP)

2031

Legal Completion

Project Factsheet

A shareable 2-page PDF snapshot — bring it to viewings, share with family.

DISCLAIMER: All information is compiled from publicly available sources and developer-issued materials for informational purposes only. Prices, unit mix, specifications, and timelines are indicative and subject to change without notice. This page does not constitute an offer to buy or sell. Seek advice from a licensed property agent and legal counsel. LovelyHomes.com.sg is an independent editorial platform. Agency Licence: L3010858B.

Figure 1: The three tenure classes in Singapore real estate — with freehold at ~4% of the housing stock, 999-year a rare pre-1960s relic, and 99-year the dominant form.

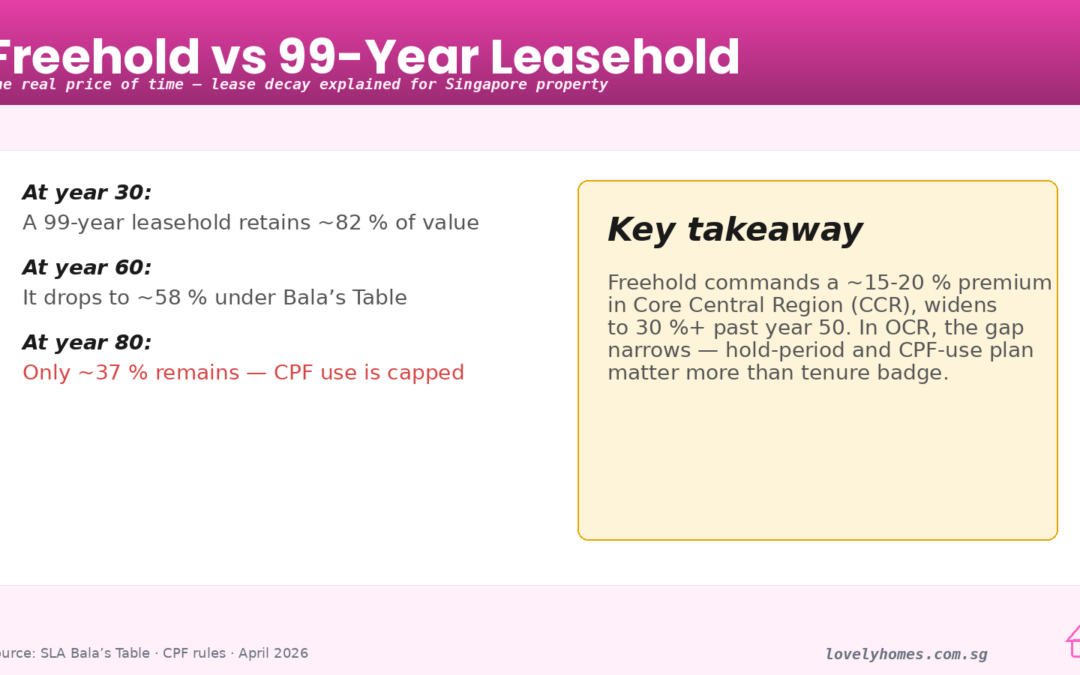

Every Singapore property conversation eventually turns to tenure. Is the extra 10–15% for a freehold condo actually worth it? Will a 99-year leasehold unit hold its value if I plan to hold for 20 years? Do banks and CPF really pull the plug on an ageing lease? These are not academic questions. The tenure decision shapes your long-run return more than almost any other call you make at the point of purchase, and the rules that govern it — CPF usage, bank LTV caps, HDB loan eligibility, lease-top-up policy — change in sharp steps rather than smoothly.

This is the 2026 edition of our tenure guide. It walks through the legal substance of freehold, 999-year and 99-year titles; the SLA “Bala’s Table” that dictates how lease-decay is valued; the financing cliffs at 95, 60 and 30 years remaining; and a Singapore-specific worked example that puts a dollar figure on the freehold premium. We close with a forward view on what the SERS / VERS pipeline means for older leaseholds.

Quick Answer: The 10 Things Every Tenure-Sensitive Buyer Should Know

Freehold ≈ ~4% of SG residential stock. The vast majority of private homes and all HDB flats are 99-year leasehold. 999-year titles are a rare pre-1960 relic but, in valuation terms, behave like freehold.

The freehold premium is ~10–15%. In comparable micro-markets, a fresh-lease 99-year condo typically trades at 85–90% of the freehold equivalent — a narrower gap than many buyers expect.

Bala’s Table is the ruler. SLA’s published valuation table is the single authoritative source for how a leasehold interest is valued at any years-remaining. It is a non-linear curve, steepening materially below 60 years.

60 years is the financing cliff. CPF usage and bank LTVs compress sharply once a lease drops below 60 years remaining.

30 years is the exit wall. Below 30 years remaining, almost no bank will finance the unit and CPF usage is effectively nil — the buyer pool collapses to cash-rich owner-occupiers.

SERS is discretionary, not guaranteed. HDB’s Selective En bloc Redevelopment Scheme is offered to a very small minority of ageing flats; the 99 years ends and the land reverts regardless.

VERS is the policy hedge. The Voluntary Early Redevelopment Scheme (legislated 2018, rolling out for the oldest HDB towns in the late 2020s) gives residents a vote on early redevelopment in exchange for a lower pay-out than SERS.

Lease top-ups exist for private land. URA allows lease extensions via upgrading premium payments for selected private freehold/leasehold sites — used routinely by en-bloc developers.

HDB’s 99-year clock starts at award. A BTO completed in 2018 will, in 2117, revert to the state regardless of whether the flat has been sub-sold or renovated.

Tenure affects renter demand less than you’d think. Rental yields on comparable freehold and 99-year properties tend to be within 10–20 basis points of each other; the rental market is insensitive to tenure in a way the sales market is not.

What Tenure Actually Means in Singapore Law

Under the Land Titles Act, freehold in Singapore is what the Common Law calls an “estate in fee simple” — the fullest form of private ownership available, running in perpetuity and capable of being transmitted by will or gift without reverting to the state. 999-year leasehold is functionally indistinguishable from freehold during the lifetime of anyone reading this article; valuers treat it at par with freehold for discounting purposes, and both CPF and bank lenders do the same. Its rarity reflects early colonial-era land grants, most of them pre-1960.

99-year leasehold is the modern default. The State (via the Singapore Land Authority, SLA) retains reversionary title; the leasehold owner holds what is technically a “term of years absolute”. When the lease expires, title reverts without compensation unless the land is re-granted. This is the deal that underpins every HDB flat, every Executive Condominium (from its initial sale onwards), and the majority of private condos and landed properties released from the Government Land Sales (GLS) programme since the 1970s.

How Lease Decay Is Valued: Bala’s Table

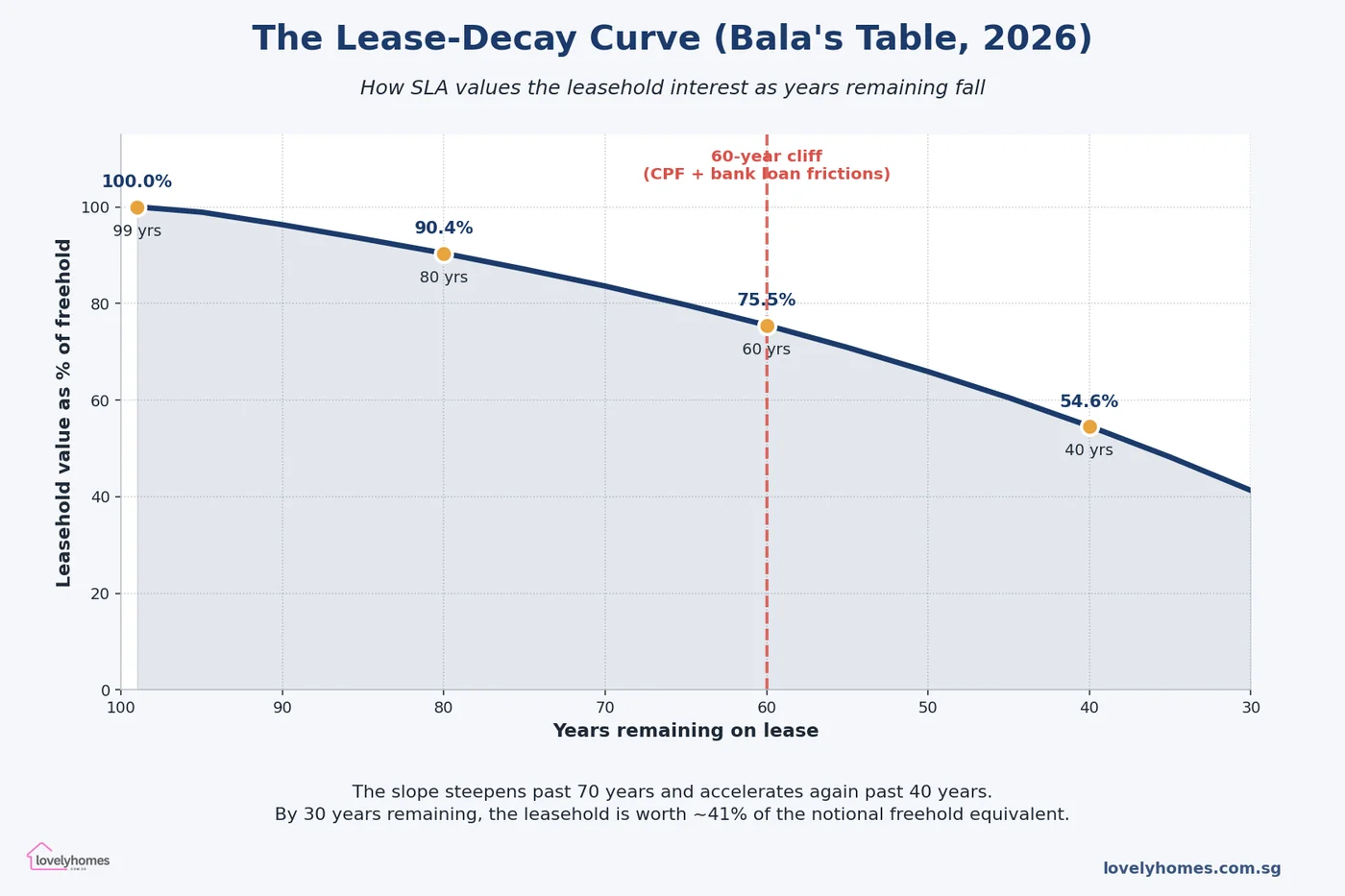

Figure 2: The Bala’s Table lease-decay curve as maintained by SLA. A 99-year leasehold retains 90% of its freehold-equivalent value at 80 years remaining, but only 75% at 60 years and 55% at 40 years.

Every Singapore valuer — including IRAS, SLA, CPF, banks and private surveyors — uses the SLA’s “Bala’s Table” as the reference for lease-hold-to-freehold value conversion. The table was named after Mr. Bala Subramaniam, then Chief Valuer, who introduced it in the early 1980s. It expresses the leasehold interest as a percentage of the equivalent freehold value at each remaining-years figure from 99 down to zero. The curve is not linear — depreciation accelerates as years remaining shrinks.

Key reference points from the 2026 version of the table:

99 years remaining: 100.0% of freehold

80 years remaining: ~90.4%

70 years remaining: ~83.6%

60 years remaining: ~75.5%

50 years remaining: ~65.9%

40 years remaining: ~54.6%

30 years remaining: ~41.3%

20 years remaining: ~26.6%

Two practical implications flow from this curve. First, the “depreciation drag” on a 99-year lease over the first 20 years is only about 10 percentage points — which in a market where underlying land values are rising 2–3% annually is easy to out-run. Second, the drag compounds rapidly past the 40-year mark, and by the time a lease is under 30 years remaining the leasehold interest is a fraction of the notional freehold and financing options have all but disappeared.

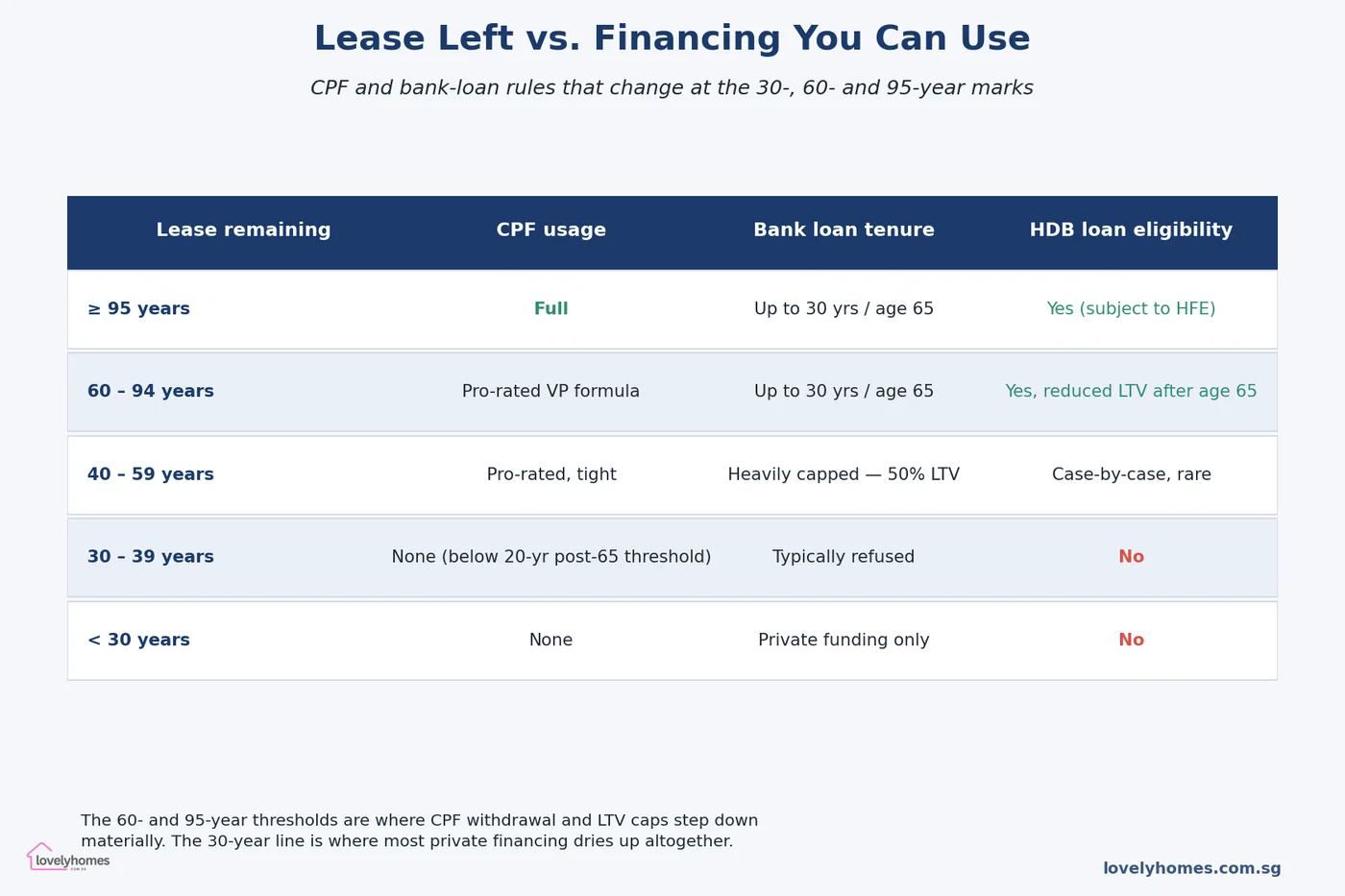

The Financing Cliffs: 95, 60 and 30 Years

Figure 3: The step changes in CPF usage, bank-loan tenure and HDB-loan eligibility as the years remaining on the lease decline.

Financing rules, not sentiment, drive most of the tenure-based price gap. CPF and bank underwriting both step down abruptly rather than smoothly. The three thresholds every buyer should know:

95 years remaining and above — Full CPF Ordinary Account usage, bank loan tenure up to 30 years or age 65, HDB loan eligible (subject to HDB Flat Eligibility letter). This is the baseline scenario for any brand-new launch.

60 years remaining — The first major cliff. CPF switches to a pro-rated Valuation Limit formula (the property must last the buyer until at least age 95, otherwise CPF usage is capped proportionally). Banks remain willing to lend but the 75% LTV may compress to 55% if the tenure extends past age 65. HDB loans remain available but with reduced LTV for older buyers.

30 years remaining — The exit wall. Most banks will decline to finance the purchase; those that do offer sub-50% LTV at punitive rates. CPF usage is effectively nil. HDB loans are not available. The market for the unit shrinks to cash-rich, typically older, buyers who are treating the purchase as a lifestyle-until-death asset.

The non-linearity is what makes tenure so consequential. A leasehold condo at 65 years remaining looks like a bargain on a pure price-per-square-foot basis — until the buyer realises they have a 5-year runway before the 60-year CPF cliff begins biting, which compresses the future pool of buyers who can take the unit off their hands.

A Fully-Worked Example: Freehold vs 99-Year in District 15

Consider two comparable 3-bedroom condo units in the Marine Parade area, both completed in 2026:

Unit A (99-year leasehold): S$2.3 million purchase price. 99 years at award — so the buyer gets 99 years of tenure starting from 2024 (when the plot was awarded).

Unit B (freehold): S$2.65 million purchase price. 15% premium to Unit A.

Assume both appreciate at 3% per annum nominal (a rough median for the Marine Parade submarket over a 20-year horizon). What does the tenure decision look like at the 20-year mark (2046)?

Unit A (now 79 years remaining): On Bala’s curve at 79 years, the leasehold interest is worth ~90% of the notional freehold equivalent. If the freehold equivalent has compounded at 3% for 20 years, it would be worth S$2.3m × 1.03^20 = S$4.15 million. The leasehold interest is then 90% of that “freehold equivalent” — but wait: the Bala curve already expresses value relative to freehold. So the 99-year unit in 2046 is worth roughly S$2.3m × 1.03^20 × (90%/100%) = S$3.74 million. Gain: ~63% over 20 years.

Unit B (still freehold): S$2.65m × 1.03^20 = S$4.79 million. Gain: ~81% over 20 years.

At the 20-year mark, the freehold unit has outperformed by about S$1.05 million in absolute terms and 18 percentage points in percentage gain. Adjust for the S$350,000 premium paid upfront (which could alternatively have earned ~4% in risk-free assets: S$350k × 1.04^20 = S$767k of opportunity cost), and the net advantage of the freehold is closer to S$300,000–S$400,000 over the period.

Is that worth it? For a buyer with a 20-year hold and no liquidity pressure, plausibly yes. For a buyer whose realistic hold is 8–10 years, the freehold premium may not recoup — the decay drag on a fresh 99-year lease is small over that horizon and the opportunity cost on the premium is live. This is the central trade-off: tenure mattered most for very long holds, very aged leases, or illiquid micro-markets.

SERS, VERS and the End-of-Lease Question

The elephant in the room for ageing 99-year stock is what happens at expiry. Three scenarios exist:

Lease runs its full 99 years and reverts. This is the default. The land returns to the state and the leasehold owner receives no compensation. For HDB flats the owner-occupier gets to live there until expiry (subject to upkeep and lease conditions). For private condos the same applies but the economic value in the final years approaches zero.

SERS (Selective En bloc Redevelopment Scheme). HDB identifies a small number of ageing blocks with high redevelopment potential and offers residents a replacement flat plus ex gratia compensation. Fewer than 5% of HDB blocks have been selected for SERS since the programme began in 1995. The policy framing is deliberately narrow — SERS is a planning tool, not a tenure safety net.

VERS (Voluntary Early Redevelopment Scheme). Legislated in 2018 and first offered to flats around the 70-year-remaining mark in the late 2020s, VERS is an opt-in mechanism: residents of an eligible precinct vote on whether to accept a negotiated pay-out in exchange for early redevelopment. Payouts are explicitly flagged as lower than SERS compensation. Our full VERS guide walks through the mechanics.

For private leaseholds, the equivalent mechanism is the en bloc (collective) sale, where 80% of owners by value (90% if the development is less than 10 years old) can force a sale to a developer who pays SLA a topping-up premium to reset the 99-year clock. The economics of en bloc sales change materially once a development crosses 60 years remaining — the topping-up premium escalates and developer IRRs tighten.

What Might Come Next — Policy Signals to Watch

Three forward-looking data points to monitor over 2026–2028:

The first VERS offers. The first precincts eligible for VERS are the 1970s HDB estates in Tiong Bahru, Queenstown and Marine Parade, now crossing the 55-year-remaining mark. The terms of the first offer (how much is paid, how much choice the resident has in replacement housing) will set the template for the next two decades. HDB has signalled a 2027–2028 rollout window.

Bala’s Table updates. SLA reviews the table periodically. The last meaningful revision was in 2019, when decay rates were nudged upward to reflect data from transactions in older leases. Another revision would have knock-on effects on CPF and bank LTV decisions.

Lease top-up policy for older private estates. A handful of pre-1970s private freehold estates have approached URA for lease-top-up schemes to extend or recalibrate tenure. If a standardised top-up mechanism emerges, the value of ageing 99-year private leaseholds could rise materially.

How Singapore’s Tenure System Compares Globally

Singapore is not alone in using long leaseholds for residential land. Hong Kong’s typical residential lease is also 99 years, with far more aggressive lease-modification and top-up activity (land premiums are a major source of government revenue). London uses a mix of long leaseholds (typically 99 or 125 years) on ex-local-authority and conversion flats, and reformed the Leasehold Reform, Housing and Urban Development Act in 2002 to allow leaseholders to compel freehold purchase (a process called “enfranchisement”) under specific conditions. Vancouver has true freehold in most of the metro area but faces its own lease-renewal issues with First Nations reserve land.

The distinctive feature of Singapore’s framework is the tightness of its financing-tenure coupling: HDB and CPF rules shape the buyer pool in a way that is more formulaic than in most peer jurisdictions. That makes Singapore’s Bala-Table decay an underwriting reality, not just a valuation convention — which is why it moves prices in step-changes around the 60- and 30-year thresholds.

Frequently Asked Questions

1. Is paying a 15% premium for a freehold condo ever worth it?

It depends almost entirely on your holding period and the opportunity cost of the premium. For a 25+ year hold in a supply-constrained micro-market, the math usually favours freehold — the Bala decay on the 99-year unit starts to bite after year 20, the buyer pool for the freehold unit remains wider, and the reinvested-premium scenario struggles to keep pace with property inflation. For a 5–10 year hold, the 99-year unit will typically outperform net of the premium: the Bala decay over that window is less than the opportunity cost of parking an extra S$300,000–S$500,000 in a lower-yielding asset.

2. Can I get a bank loan for a flat with less than 30 years remaining?

In practice, very rarely. Two or three private banks specialising in high-net-worth lending will consider it on bespoke terms — typically capped at 50% LTV, premium rates, short tenure and often secured against other assets. For standard retail buyers, the answer is effectively no. This is why the 30-year mark is called the exit wall: the market shrinks to a niche of cash-rich buyers and the price discount can be severe. The same logic drives why a 99-year unit sold at year 65 clocks a bigger-than-Bala discount — the market is already pricing in the financing thinning that bites at 60.

3. Does CPF allow me to buy an ageing leasehold flat?

Yes, but pro-rated. The CPF Board’s rule of thumb is that the property must be able to last the owner until at least age 95. If the remaining lease does not cover that, CPF usage is capped proportionally via the Valuation Limit/Withdrawal Limit formula. A 40-year-old buyer looking at a 65-year lease on a flat can usually still use full CPF. The same buyer at 55 looking at a 50-year lease will face a material haircut. Always run the CPF calculator before committing.

4. Are all HDB flats 99-year leasehold?

Yes. Every HDB flat — BTO, resale, SBF, DBSS — is 99-year leasehold from the date the block was first awarded (or in some older blocks, re-dated for the current lease commencement). The 99-year clock is set in stone; HDB does not sell freehold, and there is no mechanism to convert an HDB flat to freehold. The compensation schemes (SERS, VERS) are the only policy routes around the expiry, and they are discretionary.

5. How does tenure affect rental yields?

Less than most people expect. Rental markets price comparable units on amenity, location and unit quality; tenure is a distant factor because tenants are paying for the right to occupy, not to own. Comparable freehold and 99-year condos in the same submarket typically show rental yields within 10–20 basis points of each other. The yield difference is usually in favour of the leasehold (because the leasehold trades at a lower capital value), but the gap is small enough that investors optimising for yield rarely pick tenure as the decision variable.

6. What is the difference between lease commencement date and Temporary Occupation Permit (TOP) date?

The lease commencement date is the date on which the 99-year clock begins — typically when the land was awarded to the developer via the GLS programme. The TOP date is when the building is ready for occupation, usually 3–5 years after lease commencement for a condo and 6–8 years for an HDB BTO. The lease clock does not reset at TOP; a buyer moving into a newly-completed 2026 condo may already have only 95 years remaining on the lease because the plot was awarded in 2022. Always check the lease commencement date in the Sale & Purchase Agreement, not just the TOP.

7. Can a 99-year lease be extended?

For private residential land, yes — via the URA’s lease top-up scheme, which en bloc developers use routinely. The developer pays a topping-up premium to SLA and the lease resets to 99 years. Individual flat owners cannot unilaterally request a top-up; it must be done at the collective/development level. For HDB flats there is no top-up mechanism available to flat owners; the 99 years runs to expiry with only the SERS/VERS escape hatches as exceptions.

This article is an editorial guide for general information only and does not constitute legal, financial or valuation advice. The Bala’s Table figures and policy references used are illustrative and reflect the position as published by the Singapore Land Authority (SLA) and the Housing & Development Board (HDB) at the time of writing (April 2026); figures are periodically revised. For authoritative guidance consult the Singapore Land Authority, the HDB, the URA, a licensed property valuer and a qualified conveyancing lawyer before any property decision. Worked-example numbers are illustrative; actual outcomes depend on market conditions, the specific property, and financing available at the time of purchase.