Buying Landed Property Singapore 2026: Eligibility, GCB Rules, BSD and Step-by-Step Guide

Quick Answer: Buying Landed Property in Singapore 2026

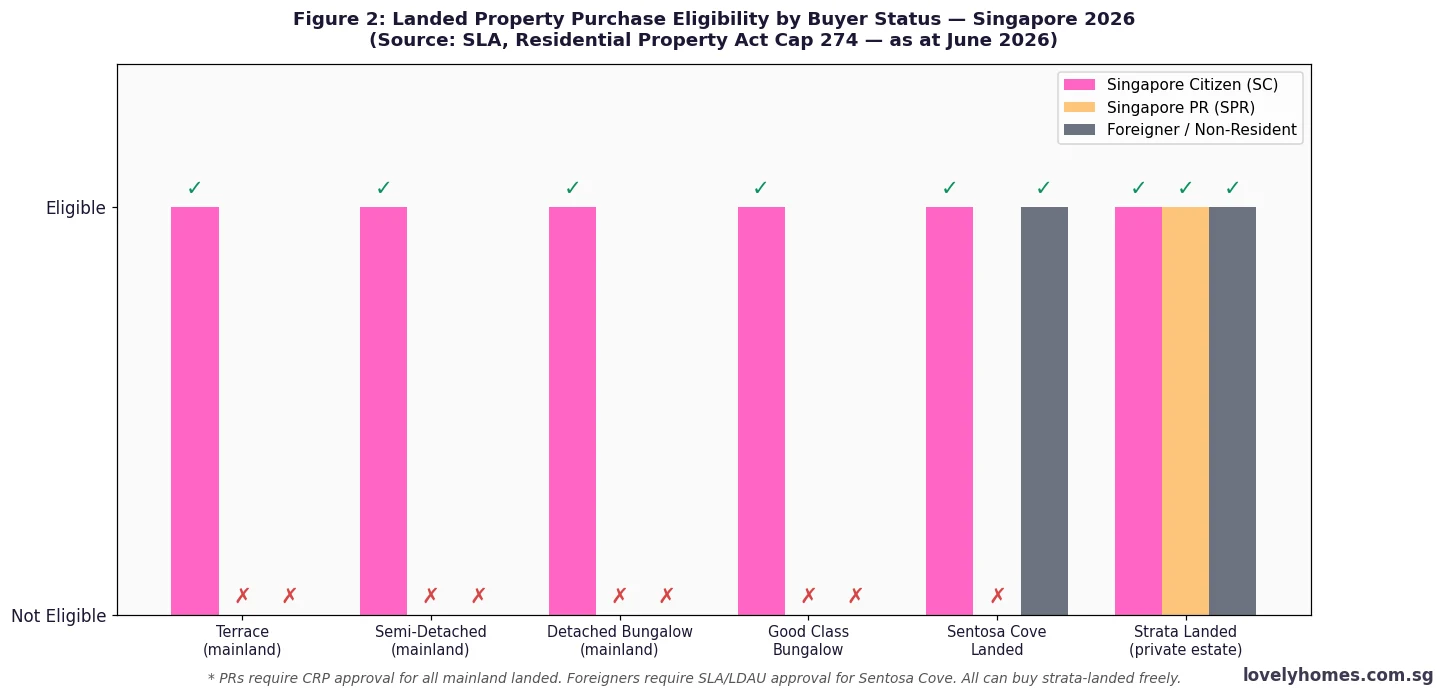

- Who can buy: Singapore Citizens (SCs) may freely purchase all landed property types on the mainland. Singapore Permanent Residents (PRs) require approval from the Controller of Residential Property (CRP). Foreign nationals generally cannot purchase mainland landed property.

- Good Class Bungalows (GCBs): Reserved exclusively for Singapore Citizens — PRs and foreigners are excluded even with CRP or SLA approval. Minimum plot 1,400 sqm; 39 gazetted areas across Singapore.

- Strata-landed (cluster housing, townhouses): Generally purchasable by PRs and foreigners as these are classified as private residential (non-restricted) — but ABSD applies at the buyer’s applicable rate.

- Sentosa Cove landed: Foreign nationals may apply to the SLA for approval; 60% ABSD still applies.

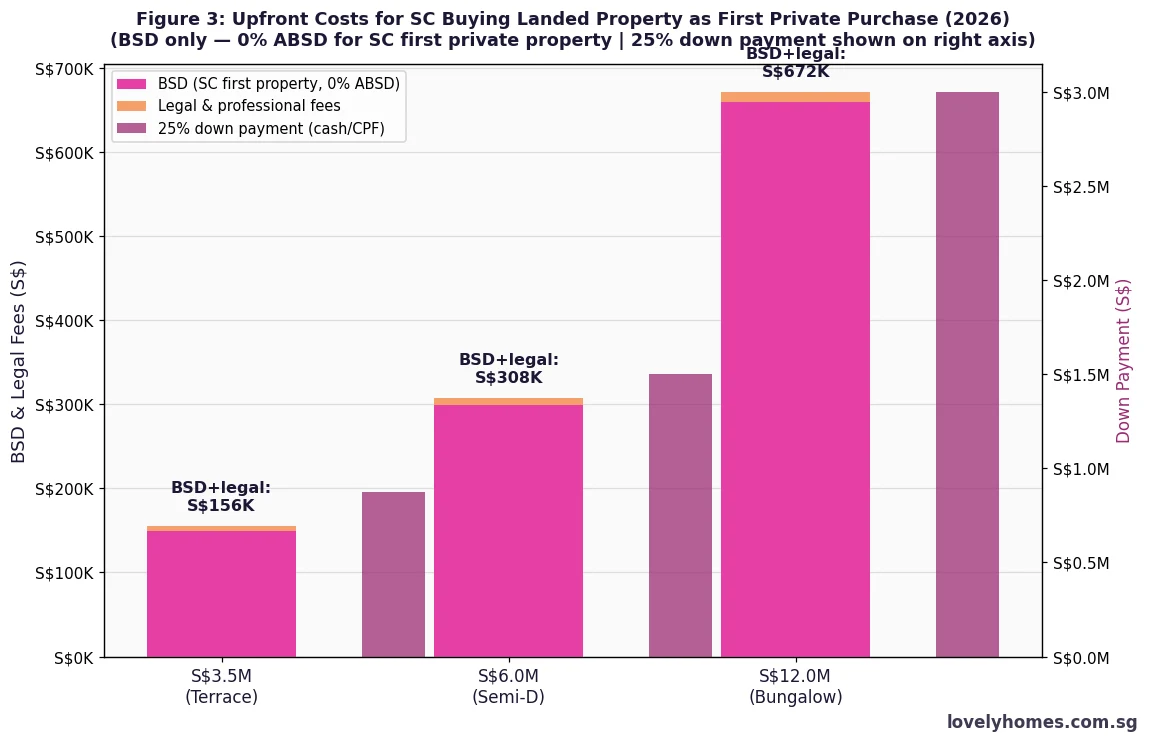

- ABSD: SC first private property purchase: 0% ABSD. SC buying landed while still owning an HDB: 20% ABSD (or use the 6-month remission window). PR: 5% on first private property.

- BSD: Progressive 1–6% on all purchases; for a S$4.2M terrace, BSD is S$191,600.

- Property tax: Owner-occupied landed properties pay progressive property tax on Annual Value; revised rates effective 2023 can exceed S$10,000/year for higher-value landed homes.

- Bank financing: LTV 75% (first property), TDSR 55%. No HDB concessionary loan — bank loans only for private property.

Why Landed Property Remains Singapore’s Most Coveted Real Estate

Singapore has roughly 73,000 landed residential properties — terraces, semi-detached houses, bungalows, and Good Class Bungalows — on an island of just 733 square kilometres. As a share of total housing stock, landed property represents less than 5% of all units. That scarcity, combined with land tenure that is often freehold, makes Singapore landed property one of the most tightly held and appreciating asset classes in Asia-Pacific.

For buyers who qualify — primarily Singapore Citizens — purchasing a landed home represents not just a lifestyle upgrade but a substantive long-term wealth accumulation strategy. URA data shows that the landed residential property price index has risen approximately 73% from Q1 2019 to Q1 2026, outpacing even the robust gains in the private non-landed segment.

This guide covers who may buy landed property in Singapore, the types of landed homes available, eligibility rules under the Residential Property Act (Cap 274) administered by the Singapore Land Authority (SLA), how stamp duties are calculated, and what a realistic transaction looks like from start to finish. All rules and figures reflect the position as at June 2026.

Types of Landed Property in Singapore

Singapore’s landed residential market is divided into five principal categories, each with its own planning parameters, price band, and ownership rules:

1. Terrace Houses (Intermediate and End-Lot)

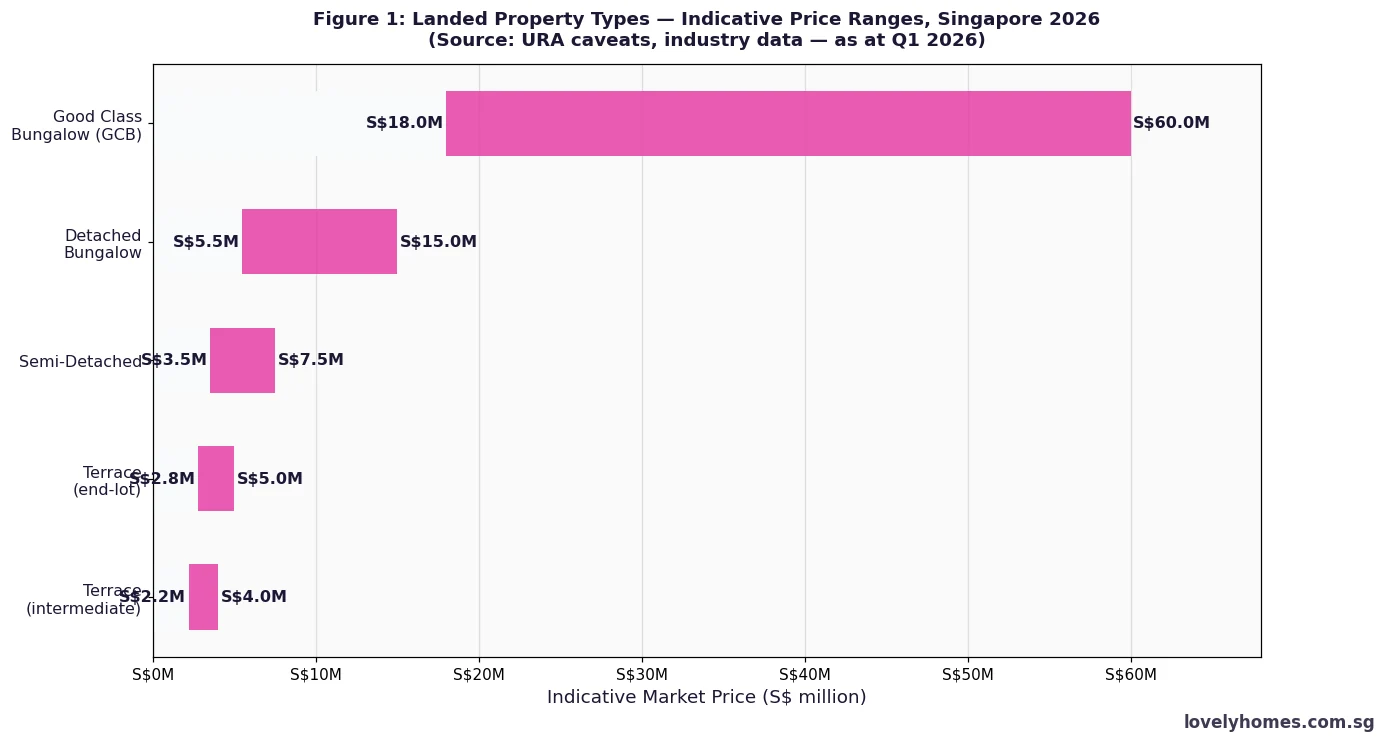

Terrace houses are the most accessible entry point into Singapore’s landed market. An intermediate terrace sits between two other units in a row; an end-lot terrace has one open side and typically commands a 10–20% premium. Standard terraces cover a land area of roughly 150–300 sqm (about 1,600–3,200 sqft). Prices range from approximately S$2.2 million for an older intermediate terrace in a non-prime district to S$5 million or more for a renovated freehold end-lot in a desirable estate like Serangoon Gardens (D19), Frankel Estate (D15), or Joo Chiat (D15).

2. Semi-Detached Houses

A semi-detached house shares one party wall with an adjacent unit; the other three sides are free-standing. Land areas typically range from 250 to 500 sqm. Semi-Ds in prime freehold estates (Bukit Timah D11, Holland Road D10) can fetch S$6–9 million, while newer leasehold developments in the north may trade at S$3.5–5 million.

3. Detached Bungalows

A detached bungalow stands on its own plot with no shared walls. Singapore’s Urban Redevelopment Authority (URA) stipulates minimum plot sizes for new detached dwellings, typically 400 sqm and above. Bungalows range widely: a mid-size freehold bungalow in D21 might list at S$6–8 million, while a trophy bungalow in prime D10 or D11 can exceed S$20 million.

4. Good Class Bungalows (GCBs)

GCBs are the pinnacle of Singapore’s residential hierarchy. Regulated by URA’s Good Class Bungalow Areas planning rules, these properties must sit on plots of at least 1,400 sqm (approximately 15,000 sqft), be capped at two storeys above ground plus one basement, and may not subdivide below the minimum plot size. There are 39 gazetted GCB areas across Singapore — concentrated in districts 10, 11, and 21 — including Nassim Road, Bishopsgate, Dalvey Estate, Swiss Club Road, Ridgewood, Caldecott Hill, and Frankel Estate. GCBs are reserved exclusively for Singapore Citizens; PRs and foreigners are ineligible regardless of wealth or residency track. Prices range from approximately S$18 million to over S$60 million, with the rarest Nassim Road GCBs occasionally transacting at S$3,500–S$5,000 psf of land.

5. Strata-Landed Housing

Strata-landed properties — cluster housing, townhouses, and similar formats that sit within a private condominium development on a strata title — occupy a unique middle ground. They are landed in appearance (each unit has its own ground floor and outdoor space) but are legally classified as strata units within a development, placing them outside the Residential Property Act’s “restricted residential property” regime. This means PRs and foreign nationals may purchase strata-landed homes without CRP or SLA approval (subject to the applicable ABSD). Prices are typically lower than equivalent standalone landed: a cluster terrace in a popular development might list at S$2.5–4 million.

Who Can Buy Landed Property: Eligibility by Buyer Status

Singapore Citizens (SC): Full Access to All Mainland Landed Types

Singapore Citizens may purchase any landed residential property on the Singapore mainland — terrace, semi-detached, bungalow, or GCB — without any prior approval from the SLA or CRP. The only constraint is financial: stamp duties, financing limits, and the HDB ownership rules discussed below. SC buyers who already own an HDB flat face an important restriction: under HDB rules, a flat owner who acquires a private residential property (including landed) must dispose of the HDB flat within six months of completing the private purchase, unless they qualify for the married-couple ABSD remission scheme and choose to retain the HDB temporarily.

Singapore Permanent Residents (PRs): Approval Required

PRs wishing to purchase mainland landed property must first obtain approval from the Controller of Residential Property (CRP), a statutory position within the SLA established under the Residential Property Act (Cap 274). Applications are assessed individually, with the CRP considering factors such as the length of PR status, economic contributions to Singapore (including taxes paid and businesses run), family ties, and the applicant’s immigration trajectory. There is no guarantee of approval, and processing typically takes several months. If approval is granted, conditions may be attached — for example, a prohibition on subletting the property.

PRs may, however, purchase strata-landed housing freely, without CRP approval, as it falls outside the “restricted residential property” definition. PRs are also ineligible for GCBs even if they obtain CRP approval for other landed types.

Foreign Nationals: Mainland Landed Prohibited

Foreign nationals (including those on Employment Passes, Dependent Passes, Long-Term Visit Passes, or any other Singapore immigration status short of PR or citizenship) may not purchase any mainland landed property in Singapore. This prohibition is absolute under the Residential Property Act and does not vary based on wealth, tenure in Singapore, or the type of visa held. The only exceptions are Sentosa Cove landed properties (purchasable with SLA/LDAU approval, with the 60% ABSD still applying) and strata-landed homes in private estates, which foreigners may purchase freely as private residential property.

Stamp Duties on Landed Property: BSD and ABSD

Stamp duty on landed property transactions works identically to other residential purchases — BSD is payable by all buyers, ABSD is layered on depending on buyer status and property count. The key difference is that the transaction values are significantly higher, which means BSD in the 5% and 6% brackets applies to a large portion of the purchase price.

ABSD and Landed Property: Critical Points for Upgraders

Many landed buyers in Singapore are HDB flat owners upgrading to private residential property. For a Singapore Citizen purchasing their first private residential property (having either sold the HDB first, or qualifying under the married-couple remission window), ABSD is 0%. However, a SC who buys landed before selling their existing HDB or private property must pay 20% ABSD upfront on the second property and may apply for a remission of this ABSD if the first property (HDB or private) is sold within six months of the second purchase’s completion date. This remission applies to married SC couples only; single buyers are not eligible.

PRs buying their first private residential property (including landed with CRP approval) pay 5% ABSD. A second PR purchase attracts 30% ABSD. Foreigners buying strata-landed or Sentosa Cove landed pay 60% ABSD.

Financing Landed Property: LTV, TDSR and Practical Considerations

Landed property purchasers in Singapore must use bank financing — there is no HDB concessionary loan option for private residential property. The MAS-regulated parameters are the same as for condominiums: LTV cap of 75% for the first property loan, subject to TDSR of 55% of gross monthly income. For a S$5 million semi-detached property, a 75% LTV loan equals S$3.75 million — carrying a monthly repayment of approximately S$15,800 at 3.0% over 30 years, requiring a household income of at least S$28,700/month to pass TDSR (with no other debts). This reflects the buyer demographic typical of the Singapore landed market.

One practical consideration specific to landed property transactions is the use of CPF. While SC buyers may use CPF Ordinary Account savings for the down payment and monthly loan instalments on private property (subject to the Valuation Limit and Withdrawal Limit rules), the higher absolute values involved mean that CPF often covers only a fraction of the total cost. Most landed buyers also deploy significant savings or proceeds from prior property sales.

Property Tax on Landed Homes

Property tax is levied annually by IRAS on the Annual Value (AV) of a property — the estimated gross annual rent it could command in the open market. AV for landed homes depends on the property type, size, location, and condition. A terrace in Serangoon Gardens might carry an AV of S$60,000–80,000; a Nassim Road bungalow might have an AV of S$200,000 or more.

Owner-occupied residential property tax rates (revised upward from 1 January 2024) are progressive:

| Annual Value (AV) | Owner-Occupied Rate | Non-Owner-Occupied Rate |

|---|---|---|

| First S$8,000 | 0% | 10% |

| S$8,001–S$30,000 | 4% | 12% |

| S$30,001–S$40,000 | 6% | 14% |

| S$40,001–S$55,000 | 10% | 16% |

| S$55,001–S$70,000 | 14% | 18% |

| S$70,001–S$85,000 | 18% | 20% |

| S$85,001–S$100,000 | 22% | 22% |

| Above S$100,000 | 32% | 36% |

For an owner-occupied terrace with an AV of S$72,000, annual property tax would be approximately S$8,160. A non-owner-occupied landed home (i.e., one that is tenanted or vacant) is taxed at the higher non-owner-occupied rate, which could result in an annual property tax bill of S$11,400 or more on the same AV.

Summary: Key Rules for Buying Landed Property in Singapore 2026

| Parameter | Singapore Citizen | Singapore PR | Foreigner |

|---|---|---|---|

| Terrace / Semi-D / Bungalow (mainland) | ✓ Free to buy | CRP approval needed | ✗ Prohibited |

| Good Class Bungalow (GCB) | ✓ Free to buy | ✗ Ineligible | ✗ Prohibited |

| Strata-landed (cluster housing) | ✓ Free to buy | ✓ Free to buy | ✓ Free to buy |

| Sentosa Cove landed | ✓ Free to buy | ✓ Free to buy | SLA/LDAU approval needed |

| ABSD (first private property) | 0% | 5% | 60% |

| BSD | Progressive 1–6% | Progressive 1–6% | Progressive 1–6% |

| SSD (if sold within 3 years) | 12%/8%/4% | 12%/8%/4% | 12%/8%/4% |

| LTV cap (first property loan) | 75% | 75% | 75% (bank only) |

| Minimum cash down payment | 5% cash + CPF | 5% cash + CPF | 5% cash only (no CPF) |

| HDB ownership: must dispose | Within 6 months of private purchase | Within 6 months | N/A (no HDB ownership) |

Worked Example: Mr & Mrs Tan (Singapore Citizens) — Upgrading to a Serangoon Gardens Terrace at S$4,200,000

Profile: Mr Tan (46) and Mrs Tan (42), both Singapore Citizens, joint gross income S$28,000/month. They currently own a Tampines HDB 5-room flat that they sell for S$950,000. After repaying the outstanding HDB loan (S$150,000) and refunding CPF accrued interest (S$220,000 principal + S$32,000 interest = S$252,000), they net approximately S$548,000 in cash proceeds. They have additional savings of S$550,000. Combined liquid assets: S$1,098,000.

Step 1 — BSD calculation on S$4,200,000:

- 1% × S$180,000 = S$1,800

- 2% × S$180,000 = S$3,600

- 3% × S$640,000 = S$19,200

- 4% × S$500,000 = S$20,000

- 5% × S$1,500,000 (S$1.5M–S$3.0M) = S$75,000

- 6% × S$1,200,000 (S$3.0M–S$4.2M) = S$72,000

- Total BSD = S$191,600

Step 2 — ABSD: The Tans sell their HDB before exercising the OTP on the terrace, so this is their first private residential purchase — ABSD = 0%.

Step 3 — Bank loan and TDSR:

- LTV 75%: loan = S$4,200,000 × 75% = S$3,150,000

- At 3.0% p.a. over 30 years: monthly instalment ≈ S$13,280

- TDSR = S$13,280 ÷ S$28,000 = 47.4% — PASS (below 55% threshold)

- Stressed at 4.0%: S$15,037/month ÷ S$28,000 = 53.7% — borderline; lender may require 25-year tenure instead

Step 4 — Cash outlay summary:

| Item | Amount (S$) | Funding Source |

|---|---|---|

| 25% down payment (incl. 5% cash minimum) | S$1,050,000 | 5% cash S$210k + CPF S$420k + cash S$420k |

| BSD | S$191,600 | CPF OA (if sufficient) / cash |

| Legal fees (conveyancing + bank) | S$7,500 | Cash |

| Property valuation fee | S$800 | Cash |

| Total upfront (excl. ABSD) | S$1,249,900 | Cash available: S$1,098,000 + CPF used |

CPF OA balance (combined) assumed at S$380,000 — covers BSD and part of down payment. The Tans’ total cash and CPF resources of approximately S$1,478,000 comfortably cover the S$1,249,900 needed, leaving a liquidity buffer of approximately S$228,100 plus ongoing CPF contributions. Monthly instalment S$13,280 at 3.0%/30yr.

Why Landed Property Holds a Special Place in Singapore’s Wealth Architecture

Singapore’s land constraints are structural and permanent. The Government has stated that no new landed residential land will be released through the Government Land Sales programme — landed supply growth comes only from existing plots being redeveloped or amalgamated. This fixed supply, combined with relentless demand from Singapore’s growing population of high-net-worth Citizens, underpins the asset’s long-run outperformance. Industry data suggests that freehold landed property has appreciated at approximately 5–7% per annum over two decades in prime districts, with GCBs in particular serving as wealth-preservation vehicles for Singapore’s wealthiest families.

Unlike condominiums, landed homes generate no management fee or sinking fund contributions (for standalone properties), offer true ground-floor living, and permit significant customisation through rebuilding or A&A (additions and alterations) works subject to URA guidelines. The combination of scarcity, control, and customisation makes landed property a distinct asset class rather than simply “a more expensive condo”.

What Might Come Next for Landed Property Policy?

This section represents editorial analysis and should not form the basis of any investment decision. The core restrictions on PR and foreign purchases of mainland landed property have been in place since the Residential Property Act’s enactment in 1976 and are unlikely to change materially. There has been no policy signal of any relaxation. The GCB rules in particular — which restrict purchases to SCs only — reflect a deliberate policy to preserve the nation’s most prestigious residential stock for citizens.

Looking further ahead, some observers speculate that as Singapore’s population of long-tenured, economically integrated PRs grows, there may be gradual liberalisation of the CRP approval process for PR buyers in the mid-tier landed market. Others have suggested that the Government could use landed property supply to reward exceptional talent (through a fast-tracked CRP approval linked to an enhanced-tier talent scheme). For now, however, the policy stance is unchanged: landed ownership on the Singapore mainland remains principally a citizen prerogative.

Frequently Asked Questions

Can a Singapore PR apply to buy a landed property on their own?

Yes — a Singapore Permanent Resident may apply to the Controller of Residential Property (CRP) at the Singapore Land Authority (SLA) for approval to purchase mainland landed residential property. The application is assessed individually. Key factors include the applicant’s length of PR status, economic contribution to Singapore (employment, taxes paid, business ownership), family ties to Singapore Citizens, and whether the applicant has applied for or is eligible to apply for citizenship. There is no published approval rate, and decisions are at the CRP’s discretion. PRs who are granted approval may purchase terrace houses, semi-detached houses, and detached bungalows, but not Good Class Bungalows (which are restricted to SCs only). The CRP approval does not reduce or waive the applicable ABSD — a PR buying a first private property still pays 5% ABSD.

What is the minimum plot size for a Good Class Bungalow?

A Good Class Bungalow (GCB) must sit on a plot of at least 1,400 sqm (approximately 15,069 sqft), as stipulated in URA’s Good Class Bungalow Areas planning rules. The building envelope is limited to two storeys above ground plus one basement storey. GCBs may not be subdivided below this minimum plot size, and amalgamation (combining two or more plots) is permitted only if the resulting plot meets the minimum size requirement. The 39 gazetted GCB areas are concentrated primarily in Districts 10, 11, and 21, with pockets in Districts 15 and 16. Any redevelopment or rebuilding on a GCB plot requires BCA and URA approval and must comply with the GCB planning parameters. Singapore Citizens wishing to purchase a GCB do not need any special government approval beyond the standard conveyancing process.

Can an SC who owns an HDB flat buy a landed property without selling the HDB first?

Yes, but with significant stamp duty consequences. A Singapore Citizen who owns an HDB flat and purchases a private residential property (including landed) without first selling the HDB will pay 20% ABSD on the private property. This ABSD is payable within 14 days of the OTP exercise. However, if the HDB flat is sold — and the sale is completed — within six months of the private purchase’s completion date, the SC (or married SC couple) may apply to IRAS for a remission of the 20% ABSD. This is the “married couple ABSD remission” scheme under the Stamp Duties Act. Note: the remission requires the couple to be lawfully married, and both spouses must be Singapore Citizens to qualify. Single SCs are not eligible for this remission and must sell their HDB first to avoid ABSD.

What are the typical costs to rebuild a landed property in Singapore?

Rebuilding a landed property in Singapore — demolishing the existing structure and constructing a new home — typically costs between S$2.5 million and S$5 million or more depending on the plot size, the architectural specification, the quality of finishes, and the contractor selected. Rebuilding a standard two-storey terrace on a 200 sqm plot might cost S$1.5–2.5 million for a mid-range build (around S$500–900 psf of built-up area). A GCB rebuild to a high specification can cost S$5–15 million. Before any demolition or reconstruction, the owner must obtain Planning Permission from URA and a Building Plan approval from BCA. Typically the entire process from appointment of an architect to receipt of a Temporary Occupation Permit (TOP) takes 2–4 years. During the rebuild period, the owner must either rent alternative accommodation or — if they have not yet moved in — remain patient.

Are landed property gains subject to capital gains tax in Singapore?

No — Singapore does not impose a general capital gains tax. Gains realised on the sale of landed (or any other) residential property are not taxable under the Income Tax Act, as long as the seller is not considered to be carrying on a trade or business in property. IRAS may assess an individual as a property trader — and therefore liable for income tax on gains — if they demonstrate a pattern of frequent buying and selling with the intention of profit rather than genuine long-term ownership. In practice, IRAS’s scrutiny is most intense for buyers who flip properties shortly after purchase and for those with professional connections to the property industry. For most individual landed property owners who hold their home for several years, there is no capital gains liability on a sale. The Seller’s Stamp Duty (SSD) at 12%/8%/4% for sales within the first three years of ownership is a deterrent to short-term flipping, but this is a stamp duty obligation rather than a capital gains tax.

Can foreigners who become PRs apply for CRP approval immediately?

Technically, an applicant may apply for CRP approval as soon as they are granted PR status. However, in practice the CRP’s assessment places significant weight on the duration of PR status as evidence of genuine long-term residence commitment. A fresh PR applicant applying immediately after receiving their PR is unlikely to succeed unless there are exceptional circumstances. Most approved applicants have held PR status for several years and have additional compelling ties to Singapore. The CRP does not publish a minimum qualifying period, and decisions are made on a case-by-case basis. Would-be PR buyers of landed property are generally advised by solicitors to wait at least three to five years after receiving PR before applying, and to build a strong profile of economic and social contributions to Singapore in the meantime.

What is “strata-landed” property and is it a good substitute for a standalone landed home?

Strata-landed housing — cluster houses, townhouses, and similar formats within a private estate — offers a landed-style living experience (ground-floor access, small garden, no unit above or below) within a condominium’s legal framework. They are generally more affordable than equivalent standalone landed homes, often located in suburban or newer estates, and available to PRs and foreigners without CRP approval. However, strata-landed homes come with condominium management fees (covering common facilities and security), are subject to the strata title’s collective management and by-laws, and may carry restrictions on exterior modifications. The land beneath a strata-landed unit is held collectively, unlike the exclusive freehold or leasehold land title of a standalone landed property. For buyers who prioritise the lifestyle of a landed home but face eligibility constraints (PRs, foreigners) or budget constraints (strata-landed is often S$500k–S$1.5M cheaper than comparable standalone), strata-landed can be an attractive alternative — albeit one that does not carry the same scarcity premium as a true standalone landed property in a prime estate.

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or taxation advice. Eligibility rules, stamp duty rates, property tax schedules, and planning regulations are subject to change by the Government at any time. The information reflects the position as at June 2026. Before making any property transaction — particularly one involving the Residential Property Act, ABSD remission applications, or CRP approvals — readers should consult a Singapore-licensed solicitor, MAS-licensed financial adviser, and the relevant authorities: SLA (sla.gov.sg), IRAS (iras.gov.sg), URA (ura.gov.sg), and HDB (hdb.gov.sg). LovelyHomes does not accept liability for any loss arising from reliance on this article.