Singapore Citizens and Eligible PRs may purchase HDB resale flats; certain restrictions apply to singles and PRs

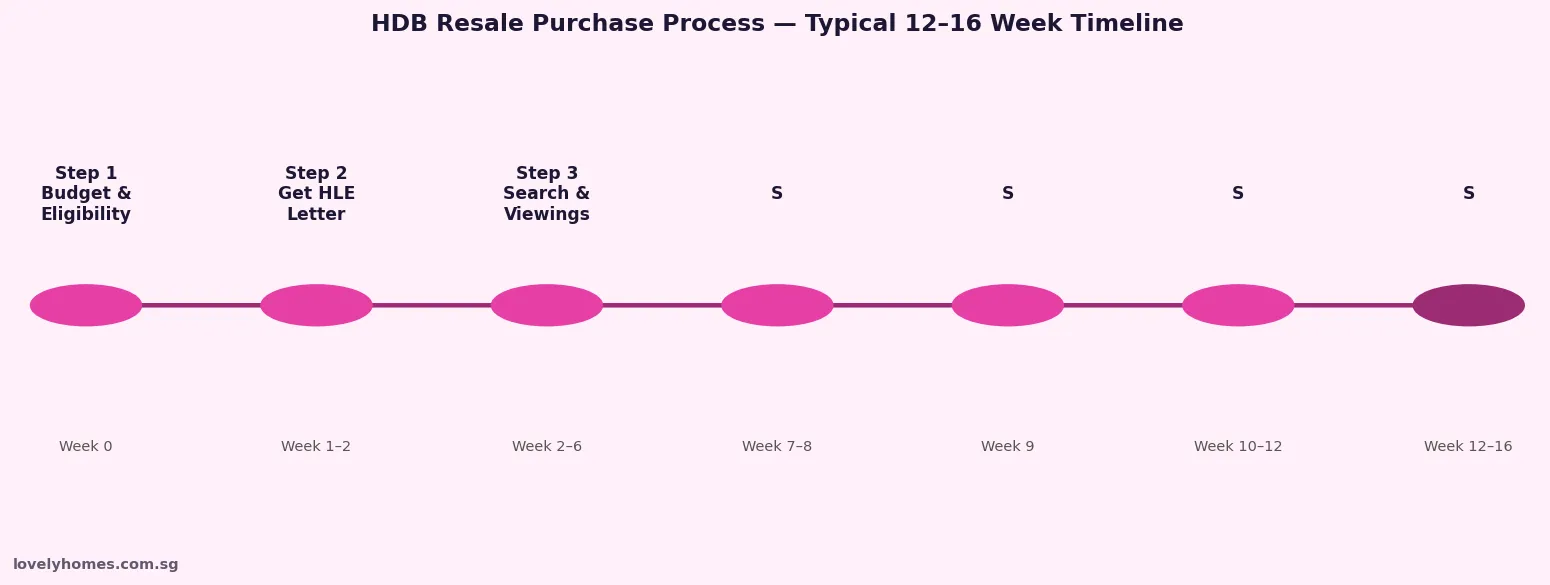

The standard resale process takes 12–16 weeks from Option to Purchase (OTP) to key collection

Resale buyers may tap CPF Housing Grants: Enhanced CPF Housing Grant (EHG), Family Grant, and Proximity Grant — up to S$120,000 combined

HDB Loan Eligibility (HLE) letter or bank Approval-in-Principle (AIP) must be obtained before OTP is exercised

Cash-over-Valuation (COV) must be paid entirely in cash and is no longer disclosed by HDB — buyers and sellers negotiate based on market

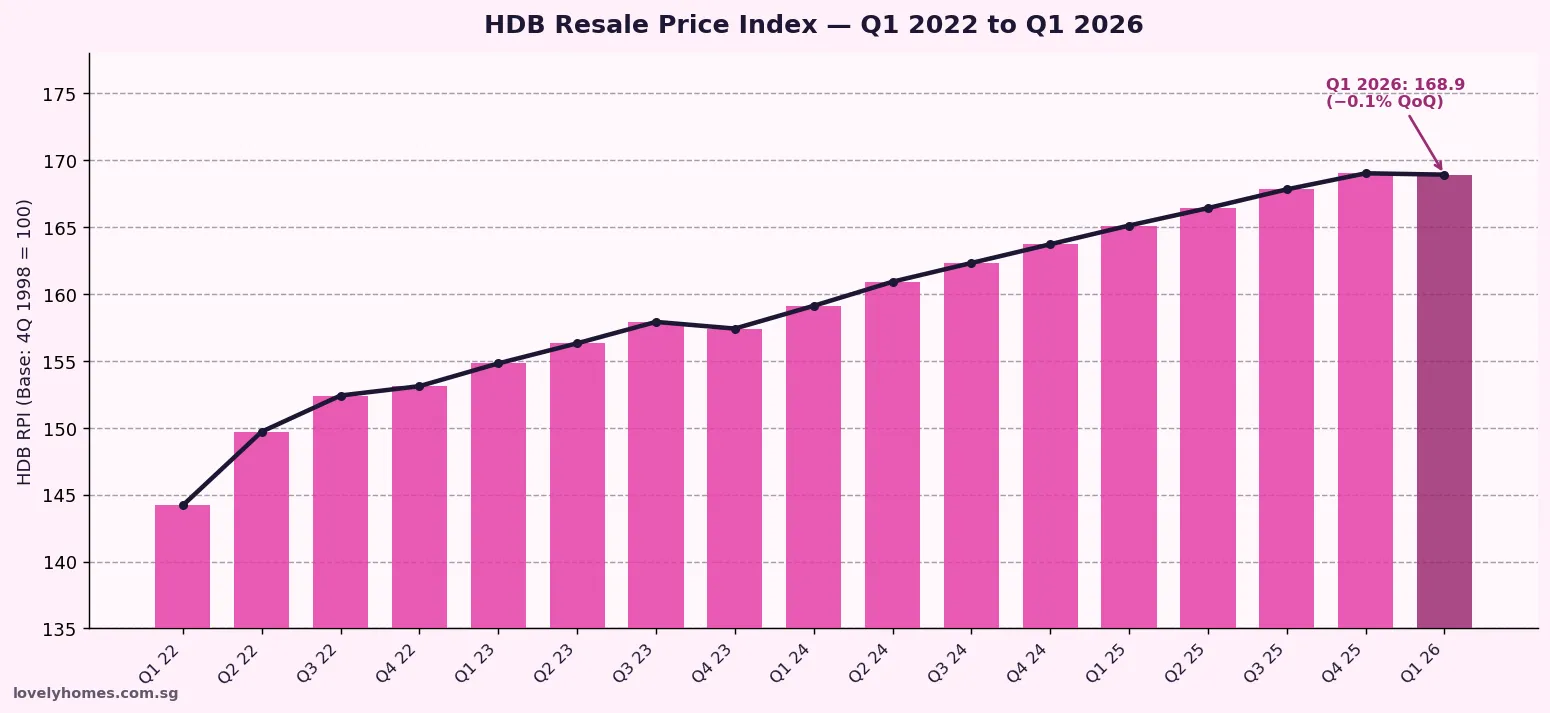

HDB resale prices fell −0.1% QoQ in Q1 2026 (first decline since Q2 2019), though 412 million-dollar transactions set an all-time record

Proximity Housing Grant (S$30,000) available if you live within 4 km of parents/children

What Is an HDB Resale Flat?

A resale HDB flat is a Housing & Development Board flat that has been previously owned by at least one household, has completed its Minimum Occupation Period (MOP) of at least 5 years, and is now available for purchase on the open secondary market through HDB’s resale portal. Unlike a Build-to-Order (BTO) flat — which involves purchasing directly from HDB at a subsidised price with a multi-year wait — a resale purchase is a private transaction between seller and buyer, with HDB administering the eligibility checks and transaction registration.

As of Q1 2026, the HDB Resale Price Index (RPI) stands at 168.9 — representing a rise of approximately 17% from Q1 2022 and a slight moderation of −0.1% quarter-on-quarter, the first quarterly dip since Q2 2019. The resale market remains characterised by sustained demand from upgraders, PRs, and those who cannot wait for BTO completion.

Figure 1: HDB Resale Price Index (RPI) — Q1 2022 to Q1 2026. Source: HDB / URA flash estimates.

Who Can Buy an HDB Resale Flat?

Eligibility for HDB resale flat purchase is governed by HDB’s Ethnic Integration Policy (EIP) and Resale Eligibility Scheme. The primary conditions are as follows:

Buyer Type

Conditions

CPF Grants Available

SC Married Couple (both SC)

May buy any HDB resale flat; MOP 5 years

EHG (up to S$120K) + Family Grant (up to S$50K) + Proximity Grant

SC + PR Family Nucleus

At least 1 SC; can buy any resale flat

EHG (SC portion); reduced Family Grant

SC Singles (≥35 years old)

May only buy 5-room or smaller HDB flat; income ≤ S$7,000

Singles Grant (up to S$25K); EHG Singles

PR Family (no SC)

May buy after PR for 3 years; restricted flat types

No CPF grants; must wait 3 years PR

Foreigners

Not eligible to buy HDB resale flats

N/A

The HDB Resale Purchase Process — Step by Step

Buying an HDB resale flat involves a structured 12–16 week process administered jointly between the buyer, seller, and HDB’s portal. Below is the typical timeline:

Step 1 — Establish your budget and eligibility. Determine your income ceiling, grant eligibility, CPF OA savings, and maximum loan quantum. Use HDB’s e-Services portal to check eligibility. If using an HDB concessionary loan, apply for a Housing Loan Eligibility (HLE) letter. If using a bank loan, obtain an Approval-in-Principle (AIP).

Step 2 — Engage a CEA-registered property agent (optional but recommended). You may transact directly using HDB’s resale portal, or appoint a Council for Estate Agencies (CEA)-licensed agent. All agents must be CEA-registered. Agent commission of 1–2% of the purchase price is typically borne by the buyer on the buyer’s side.

Step 3 — Search and shortlist. Browse HDB Flat Portal or property portals for listings. Factor in HDB’s Ethnic Integration Policy (EIP) quotas — some blocks may have reached their Chinese, Malay, or Indian quota, restricting the sale to certain ethnic groups.

Step 4 — Grant the Option to Purchase (OTP). The seller grants the buyer an OTP in exchange for an Option Fee of S$1 to S$1,000 (negotiated). The OTP is valid for 21 calendar days. Once the OTP is issued, both parties register their intent on HDB’s resale portal.

Step 5 — Exercise the OTP. Within 21 days, the buyer must exercise the OTP by paying an Exercise Fee (up to S$5,000 minus the Option Fee). At this point, both buyer and seller must submit the resale application to HDB via the portal simultaneously. A conveyancing solicitor is appointed.

Step 6 — HDB Appointment. HDB reviews the application (approximately 4–8 weeks) and schedules a completion appointment. At this appointment, financial documents, CPF pledges, and legal transfers are completed.

Step 7 — Completion and key collection. Keys are handed over, and the transaction is registered with SLA. The buyer officially becomes the registered owner of the flat.

CPF Housing Grants for Resale HDB (2026)

Grant

Maximum Amount

Eligibility Condition

Enhanced CPF Housing Grant (EHG)

S$120,000 (family) / S$60,000 (singles)

First-timer; income ≤ S$9,000 (family) / ≤ S$4,500 (singles); must work continuously for 12 months

Family Grant

S$50,000 (both SC) / S$40,000 (SC+PR)

At least one applicant first-timer; buying for family nucleus

Note: Figures are illustrative. BSD and legal fees (approximately S$9,600 and S$2,500–4,000 respectively) are additional. Verify your specific scenario with HDB or a licensed property consultant.

Key Costs When Buying an HDB Resale Flat

Cost Item

Amount / Rate

Payment Method

Option Fee

S$1–S$1,000

Cash

Exercise Fee

Up to S$5,000 (minus Option Fee)

Cash

Cash-over-Valuation (COV)

Market-determined (if price > HDB valuation)

Cash only

Buyer’s Stamp Duty (BSD)

1–6% progressive on purchase price

CPF OA or cash (14 days)

ABSD (if applicable)

5% (PR 1st property) / 20% (SC 2nd property) etc.

Cash (14 days)

Legal Fees

~S$2,500–S$4,000

CPF OA or cash

Agent Commission (buyer side)

1–2% of purchase price (if appointed)

Cash

Frequently Asked Questions

Can a foreigner buy an HDB resale flat?

No. Only Singapore Citizens and Singapore Permanent Residents (in a family nucleus with at least one SC, and after 3 years of PR status) are eligible to purchase HDB resale flats. Foreigners cannot buy HDB flats under any circumstances.

What is Cash-over-Valuation (COV) and how does it work?

COV is the difference between the agreed purchase price and HDB’s official valuation of the flat. If you agree to pay S$650,000 for a flat valued by HDB at S$620,000, the COV is S$30,000. COV must be paid entirely in cash — it cannot be financed through an HDB or bank loan, and cannot be paid using CPF funds. HDB no longer publishes COV data; buyers and sellers negotiate based on recent transacted prices (available on HDB’s resale flat prices portal).

Can I use CPF to pay for an HDB resale flat?

Yes. You may use your CPF Ordinary Account (OA) savings to pay for the down payment, remaining purchase price (after loan), BSD, and legal fees. However, COV must be paid in cash. CPF usage is subject to the Valuation Limit (you can only use CPF up to the HDB valuation of the flat, not the transacted price). CPF funds used attract Accrued Interest (currently 2.5% per annum), which must be refunded to your CPF account upon sale.

How long does the HDB resale process take?

From the issuance of the OTP to key handover, the HDB resale process typically takes 12 to 16 weeks. The OTP itself has a 21-calendar-day validity period. After both parties register on HDB’s portal, HDB typically takes 4 to 8 weeks to schedule the completion appointment. Delays can occur if eligibility issues arise, if financing takes longer, or if there are outstanding issues with the flat (e.g. renovation works, outstanding season parking).

What is the Ethnic Integration Policy (EIP) and how does it affect buyers?

The Ethnic Integration Policy (EIP) limits the percentage of flats in each HDB block and neighbourhood that can be owned by each ethnic group (Chinese, Malay, Indian/Others). This ensures racial integration. If the EIP quota for your ethnicity in a particular block has been reached, you cannot purchase a flat there — even if the seller is willing. Check EIP quotas using HDB’s online EIP checker before shortlisting a flat.

Disclaimer: Information on this page is published for general reference only and does not constitute professional property, legal, financial, or CPF advice. HDB eligibility rules, grant quantum, and resale procedures may change — verify all details with HDB directly at hdb.gov.sg or through a CEA-registered property consultant before transacting. LovelyHomes.com.sg does not hold a real estate agency licence.

New Launch vs Resale Condo Singapore 2026: Which Should You Buy?

Every Singapore property buyer faces this question. Should you purchase a new-launch condominium directly from the developer — paying a premium for a brand-new unit you will not occupy for two to four years — or buy a resale unit in the secondary market, moving in immediately at a price that reflects market reality rather than developer optimism? The answer is not universal. It depends on your holding horizon, cash-flow situation, rental needs, ABSD position, and how you value certainty of finishes versus flexibility of timing. This guide unpacks every dimension of the new launch vs resale decision for Singapore buyers in 2026.

Quick Answer — Key Takeaways

New launches suit buyers who can wait 2–5 years, want progressive payment to spread cash outlay, and value guaranteed new finishes with a 12-month Defects Liability Period.

Resale condos suit buyers who need immediate occupancy, want rental income from day one, or are targeting specific buildings or locations where no new supply is coming.

ABSD timing matters most for upgraders: a new launch delays the ABSD-remission clock for married SC couples but also delays the resale of an existing property.

Freehold new launches in Districts 9–11 and 15 are rare — when they appear (e.g. Meyer Blue), they typically carry a 10–20% psf premium over leasehold comparable launches but preserve CPF flexibility for future buyers.

Resale condos under 10 years old (sub-5yr from TOP) often price close to new-launch psf but allow immediate occupancy — the best of both worlds, sometimes.

Progressive payment on new launches means loan interest accrues only on drawn amounts — typically saving S$30,000–S$80,000 in interest over a 3-year construction period versus a full drawdown on a resale purchase.

The URA new-launch pipeline for 2026 shows only 17 projects — a 30% year-on-year drop — increasing scarcity pressure on the new-launch segment and potentially supporting resale prices in parallel.

What Is a New Launch Condo in Singapore?

A new launch condominium is a development sold directly by the developer — either off-plan (before construction begins) or during construction under the Progressive Payment Scheme (PPS). Buyers sign the Option to Purchase (OTP), exercise within 3 weeks, and then pay in stages as construction milestones are certified by the Building and Construction Authority (BCA). The buyer does not take vacant possession until the developer issues the Notice of Vacant Possession (also known as TOP — Temporary Occupation Permit) — typically 2.5 to 5 years after launch.

New launches in Singapore are governed by the Housing Developers (Control and Licensing) Act. Developers must maintain a project account at a licensed bank, and all purchase monies flow through that account. The Sales and Purchase Agreement (SPA) must be signed within 3 weeks of OTP exercise, and the SPA locks in price, specifications, and handover timeline.

What Is a Resale Condo in Singapore?

A resale condominium is any private residential unit purchased from a seller in the secondary market — not from the original developer. Resale transactions are governed by standard property law: OTP, caveat lodgement with SLA, 10-week completion timeline, and full payment (loan drawdown + CPF + cash) at completion. The buyer takes vacant possession at legal completion, typically within 10–12 weeks of OTP.

Resale units can range from newly-issued (just received TOP from the developer) to 30-year-old developments. The age, remaining lease (for 99-year developments), MCST condition, and unit condition all factor into the resale price and the true total cost of ownership.

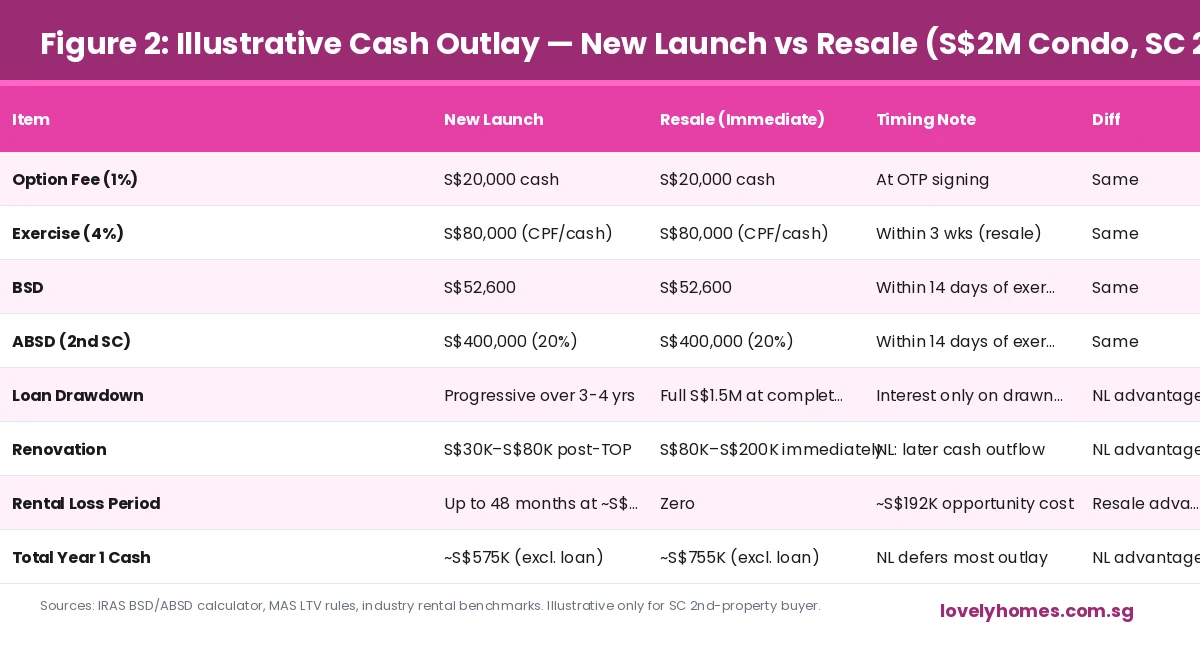

Figure 1: New Launch vs Resale Condo — 10-Factor Comparison, Singapore 2026. Sources: URA, MAS, IRAS. Indicative only.

Progressive Payment: New Launch’s Biggest Cash-Flow Advantage

The single most misunderstood advantage of buying a new launch is the Progressive Payment Scheme. Under PPS, the S$2 million purchase price is not paid in full at completion. Instead, it is paid in stages as construction milestones are certified — typically 5% at OTP, 15% at SPA (within 3 weeks), and the balance in eight certified tranches as the building rises. This has two significant advantages.

First, the bank loan is drawn progressively. If a buyer takes a S$1.5 million loan on a S$2 million purchase, the bank draws only what is needed for each tranche — meaning interest accrues only on the drawn amount. During a 3-year construction period, a buyer might draw an average of 50% of the loan — saving approximately S$60,000–S$80,000 in interest at current SORA-pegged rates of approximately 3.5–4.0% compared to a full drawdown on a resale purchase. Second, the CPF drawdown is also progressive, meaning CPF balances continue to earn 2.5% per annum on the undrawn amount during the construction period.

Worked Example: S$2M New Launch vs Resale, SC 2nd Property, 75% LTV

Purchase priceS$2,000,000

BSD (new formula from 15 Feb 2023)S$52,600

ABSD (SC 2nd property, 20%)S$400,000

Down payment (25%: 5% cash + 20% CPF/cash)S$500,000

Bank loan (75% LTV)S$1,500,000

New launch: interest saving (3 yr progressive vs full drawdown at 3.7%)~ S$55,500 saved

New launch: renovation cost (post-TOP, year 4)S$40,000–S$80,000

Resale: renovation cost (immediate, 10yr old unit)S$80,000–S$200,000

New launch: rental income foregone (3 yrs at S$4,000/mo)S$144,000 opportunity cost

Total year-1 cash outlay difference (NL vs Resale)NL saves ~S$120,000–S$180,000 in year 1

Figure 2: Illustrative Cash Outlay Comparison — S$2M New Launch vs Resale, SC 2nd-property buyer, April 2026. Sources: IRAS, MAS, industry rental benchmarks. Indicative only.

When a Resale Condo Beats a New Launch

Resale condos are the right answer in several specific scenarios. The most common is immediate occupancy need: a buyer who is relocating, who has just sold their HDB (MOP cleared) and needs housing within 10 weeks, or who has children in school and needs stability, cannot absorb a 3-year construction wait. The rental income argument is also compelling — a resale investor can begin receiving S$3,000–S$5,000 per month from completion day, versus zero income for 3–4 years on a new launch with a carrying cost of approximately S$4,000–S$6,000 per month in loan interest.

Resale condos also allow buyers to physically inspect the unit, the MCST management quality, noise levels, actual view corridors, and defect history before committing. New-launch buyers are buying off a showflat — often a different floor level, a different stack, and a different floor area from the unit they will actually occupy. This risk is non-trivial in Singapore’s high-density developments where a 3-storey difference can mean the difference between an unobstructed sea view and a blocked brick wall.

When a New Launch Beats a Resale

The case for new launches is strongest in three scenarios. First, when a developer has priced the launch below secondary-market comparable transactions (known as a “launch discount”) — this is common in OCR launches competing for HDB upgrader dollars. Second, when the project’s TOP date coincides with a catalyst event (MRT opening, school rezoning, masterplan development) that will lift values by completion. Third, when the buyer has CPF savings that would otherwise earn 2.5% in the OA, and spreads those savings across a 3-year progressive payment — essentially deferring a large purchase while maintaining CPF compound growth.

The 2026 supply pipeline context amplifies the new-launch case: with only 17 new launches scheduled for 2026 (versus 24 in 2025 and a 5-year average of 22), supply is genuinely constrained. Projects like UPPERHOUSE at Orchard Boulevard (301 units, D10), Meyer Blue (226 units, D15), and SORA EC (440 units, D22) represent rare entry points into their respective submarkets. Missing a new launch in a supply-constrained environment often means waiting 2–3 years for the next comparable opportunity.

The ABSD Timing Dimension

For married Singapore Citizens buying a second property, ABSD timing is often the decisive factor in the new launch vs resale debate. Under the ABSD remission rules, a married SC couple where one spouse owns a property may claim an ABSD remission (effectively a refund) if they sell the first property within 6 months of obtaining the second property’s TOP. This remission is not available for resale purchases — the 6-month clock starts from the date of completion, not from TOP.

This asymmetry means that buying a new launch with a 3-year construction period gives the couple approximately 3 years + 6 months to sell their first property before the ABSD refund deadline. Buying a resale means the clock starts immediately at completion — creating pressure to sell within 6 months of moving in. For couples with children or other lifestyle constraints that make a fast first-property sale difficult, the new launch gives meaningfully more breathing room on the ABSD remission timeline.

What This Means for You in 2026

The market context of 2026 favours a nuanced approach. The Singapore private residential price index rose 0.3% in Q1 2026 — modest but positive, with OCR outperforming (+1.3% QoQ). Resale volume is recovering from 2024 lows. New-launch pipeline is compressed. This combination suggests that well-located new launches with 2028–2029 TOPs are capturing forward-looking demand, while quality resale stock in mature estates (D10, D15, D19) is benefiting from genuine occupancy demand. There is no universal winner — but buyers who understand the cash-flow mechanics, ABSD timing, and supply context are better positioned to make the call that fits their specific circumstances.

What Might Come Next

Looking ahead to H2 2026 and 2027, several factors could shift the new launch vs resale calculus. The Jurong Lake District master development (JLD) is expected to see its first major private-sector completions in 2028–2029, potentially lifting demand for nearby new launches in D22. The Thomson-East Coast Line (TEL) full completion in 2026 has already begun repricing D15 and D26 resale stock. And a potential ABSD recalibration — speculation has surrounded the 60% foreigner rate since 2023 — could reignite demand in the CCR resale segment if any relief is announced. Buyers considering new launches with 2029 TOPs should stress-test their hold strategy against these macro scenarios.

Can I use CPF to buy both a new launch and a resale condo?

Yes. CPF Ordinary Account (OA) savings can be used for both new launches (progressive drawdowns as construction milestones are met) and resale condos (full drawdown at completion). For 99-year leasehold properties, CPF withdrawal is subject to the CPF Withdrawal Limit (typically capped at the purchase price or valuation, whichever is lower) and the Valuation Limit rules after the property reaches 30 years’ remaining lease. For freehold properties, there is no lease-related CPF restriction. See our CPF guide for full details.

What happens if a new launch is delayed and TOP is pushed back?

Developers in Singapore are legally required under the Housing Developers (Control and Licensing) Act to deliver TOP by the contractual deadline specified in the Sales and Purchase Agreement (SPA). If TOP is delayed beyond the SPA deadline, buyers are entitled to late delivery compensation at 10% per annum of the purchase price (i.e. approximately 2.74% for every 100 days of delay). This compensation is typically credited against the final payment at completion. Buyers should verify the SPA’s Vacant Possession date and Late Delivery Compensation clause before exercising their OTP.

Is it cheaper to buy a resale condo just after TOP?

Not necessarily. Resale units just after TOP (within 2 years of the development’s Temporary Occupation Permit) are often priced at or above the developer’s launch price — particularly if the project achieved strong initial take-up. Motivated sellers in the sub-2-year resale cohort are typically those who purchased for investment and are seeking early exit, or those who bought speculatively and need to exit before the market moves against them. Buyers seeking a bargain are more likely to find it in resale units 8–15 years from TOP, where the original buyers have either paid down significant loan principal or are willing to negotiate for liquidity reasons.

What is the Defects Liability Period for new launches?

The Defects Liability Period (DLP) for new launches in Singapore is 12 months from the date of TOP. During this period, the developer is legally obligated to rectify any defects in the unit and common areas at no cost to the buyer. Buyers should conduct a thorough defects inspection (also called a “handover inspection”) at TOP and submit a comprehensive defects list to the developer within the DLP. After 12 months, all rectification costs are borne by the MCST (for common areas) or by the individual owner (for within-unit defects).

Can I rent out a new launch condo during construction?

No. You cannot rent out a new-launch unit during construction because vacant possession has not been granted. The unit is legally part of the developer’s project account and does not yet constitute a separate strata lot. Rental income is only possible after TOP is issued and the strata title transfer is completed. For buyers who need rental income during the construction period, a resale condo is the only option — or retaining a separate investment property while the new launch is under construction.

How does ABSD ABSD remission work for new launches vs resale?

For a married SC couple where one spouse holds a property and is buying a second, ABSD remission (clawback of the 20% ABSD paid) is available if the first property is sold within 6 months of: (a) the new property’s TOP date (for new launches), or (b) the legal completion date (for resale purchases). This means a new launch with a 3-year construction period gives the couple approximately 3 years + 6 months to sell their first property — versus just 6 months from completion for a resale purchase. The extended window makes new launches structurally more ABSD-friendly for upgraders who want to retain their first property as long as possible. See our ABSD guide for full remission conditions.

DISCLAIMER: All information in this article is for general informational purposes only and does not constitute legal, financial, or property advice. Property market conditions, stamp duty rates, and CPF rules are subject to change by government policy. All price and yield figures are indicative and based on publicly available data as at 24 April 2026. Buyers should seek independent advice from a licensed property agent, financial adviser, and solicitor before making any property purchase decision. LovelyHomes.com.sg is an independent editorial platform and does not represent any developer, agent, or financial institution. Refer to official sources: URA (ura.gov.sg), IRAS (iras.gov.sg), CPF Board (cpf.gov.sg), MAS (mas.gov.sg), HDB (hdb.gov.sg).

Joint Tenancy vs Tenancy in Common Singapore 2026: Which Is Right for You?

When two or more people purchase a property together in Singapore, they must choose between two legal ownership structures: Joint Tenancy (JT) or Tenancy in Common (TIC). This choice has significant consequences for estate planning, ABSD exposure, CPF usage, and how the property is inherited on the death of one owner. It is also at the centre of several controversial IRAS-flagged property structuring strategies, including the now-notorious “99-to-1” arrangement that attracted an anti-avoidance warning in April 2023. This guide explains each structure clearly, with worked ABSD scenarios and estate-planning implications for Singapore buyers in 2026.

Quick Answer — Key Takeaways

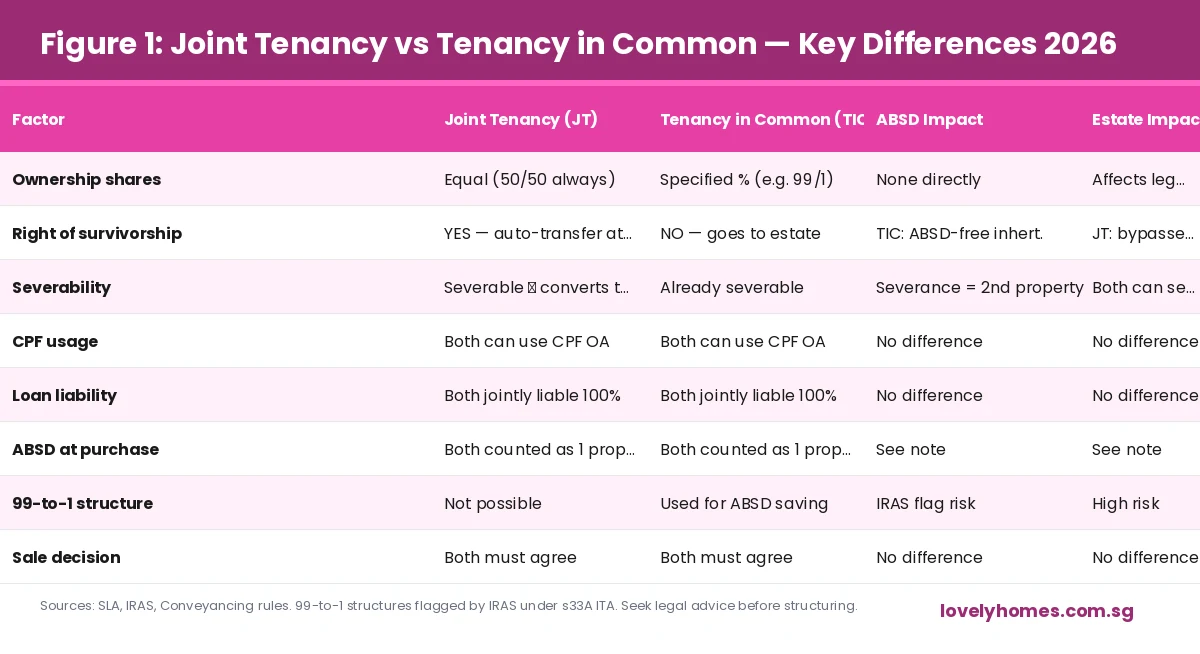

Joint Tenancy (JT): Both owners hold equal undivided shares. On death, the surviving owner automatically inherits the deceased’s share by the right of survivorship — bypassing probate. Commonly used by married couples for matrimonial homes.

Tenancy in Common (TIC): Owners hold specified percentage shares (e.g. 60/40, 99/1). Each owner’s share forms part of their estate on death and is distributed per their will or intestacy laws. More flexible but requires careful estate planning.

ABSD risk for TIC: The IRAS has flagged TIC structures (especially 99/1 and 1/99) as potentially falling within the anti-avoidance provisions of Section 33A of the Income Tax Act if the primary purpose is ABSD avoidance. Seek legal advice before using TIC for tax-saving purposes.

You can convert: A JT can be severed (converted to TIC) by any one owner’s unilateral act of severance. Conversely, TIC owners can merge their interests into a JT by mutual agreement.

CPF usage: Both JT and TIC allow CPF OA usage for the property purchase, subject to the CPF Withdrawal Limit. CPF accrued interest is charged on the amount withdrawn and must be refunded on sale.

Decoupling: TIC is the starting structure for a decoupling exercise, where one co-owner sells their share to the other — but this has ABSD and legal risks. See our decoupling guide for the full analysis.

What Is Joint Tenancy in Singapore?

Joint Tenancy (JT) is an ownership structure in which two or more co-owners hold a property collectively without any specified individual share. Each joint tenant holds an undivided interest in the entire property — not a 50% slice, but a whole-of-property interest held simultaneously with the other joint tenants. The four unities of Joint Tenancy must be present: unity of time (same time of acquisition), unity of title (same instrument of transfer), unity of interest (equal shares), and unity of possession (equal right to possess the whole property).

The defining feature of Joint Tenancy is the right of survivorship (jus accrescendi). On the death of one joint tenant, their interest in the property automatically passes to the surviving joint tenant(s) — regardless of what the deceased’s will says. The property does not form part of the deceased’s estate and does not go through probate. This makes JT the preferred structure for married couples who want a simple, automatic estate outcome without the complexity and delay of probate proceedings.

What Is Tenancy in Common in Singapore?

Tenancy in Common (TIC) is an ownership structure in which co-owners hold specified, separate shares of the property. Unlike JT, TIC owners do not hold the property collectively — each holds a defined percentage (e.g. 70% / 30%, or 99% / 1%) that can be independently dealt with, mortgaged, or bequeathed. Only unity of possession is required — TIC owners need not have acquired the property at the same time or under the same instrument.

On the death of a TIC owner, their share does not pass automatically to the other co-owner(s). Instead, it becomes part of the deceased’s estate and is distributed according to their will (or under the Intestate Succession Act if there is no will). This means TIC ownership requires more deliberate estate planning — but it also provides greater flexibility for owners with different estate objectives, different financial contributions to the purchase, or different intended inheritance outcomes.

Figure 1: Joint Tenancy vs Tenancy in Common — Key Differences, Singapore 2026. Sources: SLA, IRAS, Conveyancing Law. Indicative only — seek legal advice for your specific situation.

ABSD and Ownership Structure — The Critical Interaction

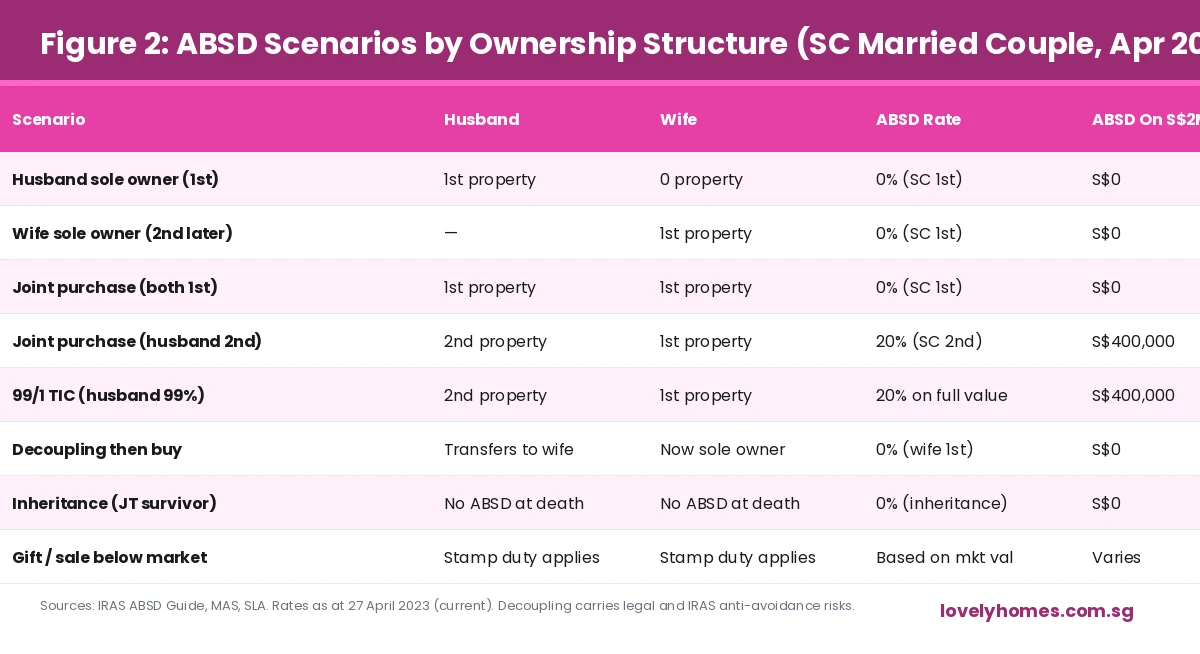

The most important practical difference between JT and TIC for Singapore property buyers in 2026 is how each structure interacts with Additional Buyer’s Stamp Duty (ABSD). ABSD is calculated based on the higher of the two co-buyers’ property count. If a Singapore Citizen (SC) husband who already owns a property buys with his SC wife who has no property, the purchase is treated as a “second property” for ABSD purposes — attracting 20% ABSD on the full purchase price — regardless of whether they use JT or TIC.

The ABSD rules were deliberately designed to prevent ownership structuring from being used as an ABSD avoidance mechanism. A 99/1 TIC arrangement — where the husband holds 1% and the wife holds 99%, ostensibly making the wife the “primary” owner — does not reduce the ABSD payable. IRAS applies ABSD based on each buyer’s property count. If the husband (with existing property) is on the title at all, the purchase is assessed at his higher ABSD rate on the full market value. The IRAS also has Section 33A anti-avoidance powers that can be invoked where an arrangement’s primary purpose is ABSD avoidance — potentially leading to reassessment, penalties, and interest.

Figure 2: ABSD Scenarios by Ownership Structure — SC Married Couple, April 2026. Sources: IRAS ABSD Guide, MAS. Rates as at 27 April 2023 (current). Illustrative only — seek professional advice before structuring.

Summary: Key Differences at a Glance

Dimension

Joint Tenancy

Tenancy in Common

Individual share specified?

No — equal undivided interest

Yes — e.g. 70/30, 99/1

Right of survivorship?

Yes — auto-passes on death

No — goes to estate

Can be bequeathed in will?

No (survivorship overrides will)

Yes

Probate required on death?

No

Yes (for the deceased’s share)

ABSD treatment

Higher count of any co-owner applies

Higher count of any co-owner applies

Convertible to the other?

Yes — by severance (any 1 owner)

Yes — by agreement (all owners)

Typical use

Matrimonial home, equal-share investment

Unequal contributions, estate planning

Decoupling suitability

Must sever to TIC first

Directly usable (with risks)

Worked Example: Estate Planning with TIC vs JT

Scenario: Mr Tan (60%) and Mrs Tan (40%) own a S$3M condo in TIC

Mr Tan passes away (no will)His 60% share → estate

Under Intestate Succession Act (married, 2 adult children)Wife gets 50% of 60% = 30%; children share remaining 30%

Mrs Tan now owns40% (original) + 30% (inheritance) = 70%

Each child now owns15% of the condo

Children’s ABSD position if they buy their own propertyThey “own” 15% — counts as a property for ABSD

If JT had been used insteadMrs Tan inherits 100% automatically. Children inherit nothing.

Key lessonTIC requires a carefully drafted will to avoid unintended outcomes

How to Convert Between Joint Tenancy and Tenancy in Common

Converting from Joint Tenancy to Tenancy in Common (severance) can be done unilaterally by any one joint tenant — it does not require the consent of the other co-owner(s). A joint tenant serves written notice of severance on the other co-owner(s), and a declaration is registered with the Singapore Land Authority (SLA). Upon registration, the JT converts to a TIC in equal shares (e.g. 50/50 for two former joint tenants). If the severing party wants unequal shares, they must transfer the relevant portion of their interest to the other co-owner — which may attract stamp duty and ABSD if the recipient thereby “acquires” an additional property interest.

Converting from Tenancy in Common back to Joint Tenancy requires the agreement of all co-owners and the re-execution of a transfer instrument, registered with SLA. The four unities must be re-established. This is less common but may be appropriate when co-owners who originally split their shares for estate planning purposes later want to consolidate for simplicity.

The 99-to-1 Structure and IRAS Anti-Avoidance

The “99-to-1” or “1-to-99” TIC structure gained notoriety in Singapore around 2021–2022 as a mechanism purportedly used by married couples to reduce ABSD. The arrangement involves one spouse (who already owns a property) purchasing just 1% of a new property, while the other spouse (who owns nothing) purchases 99%. The intended logic was that the 99% owner — being a “first-time buyer” — would attract 0% ABSD on their 99% share, with only 1% of the value attracting the higher ABSD rate.

IRAS expressly addressed this in April 2023, clarifying that ABSD applies to the full value of the property for each buyer, based on the buyer’s property count — not proportionate to their ownership share. A husband who buys even 1% of a property where he already owns another property is treated as a “second property” buyer on the full purchase price. Additionally, IRAS warned that 99-to-1 arrangements could be subject to the general anti-avoidance provision in Section 33A of the Income Tax Act, which empowers IRAS to disregard or reconstruct transactions that are not entered into for bona fide commercial reasons, or that are primarily for the purpose of obtaining a tax advantage. Buyers who have entered into such arrangements are advised to seek a legal opinion on their exposure.

What This Means for You in 2026

For most married couples buying their first home together, Joint Tenancy remains the simpler and more appropriate structure. The right of survivorship provides automatic estate protection without the cost or complexity of probate, and the equal share assumption aligns with the typical matrimonial home context. For investors, business partners, or co-owners with meaningfully different financial contributions or different estate objectives, Tenancy in Common with a clearly drafted will is the more appropriate structure — but it requires professional legal advice to ensure the intended outcome.

The ABSD landscape of 2026 has made property ownership structuring significantly more fraught. The 60% ABSD on foreign purchases, the 20% on SC second properties, and IRAS’s active anti-avoidance posture mean that creative structuring carries real legal risk. The safest path is to engage a conveyancing solicitor and a property tax advisor before executing any co-ownership arrangement, particularly where one of the buyers already holds a residential property.

What Might Come Next

There is ongoing industry discussion about whether Singapore’s ABSD regime will be relaxed for specific categories — particularly the 60% foreign-buyer rate, which has significantly reduced CCR transaction volumes since 2023. Any reduction in foreign ABSD could trigger a wave of CCR resale activity, changing the dynamics for TIC investors who hold CCR properties jointly with foreign spouses. On the estate-planning side, Singapore does not currently impose inheritance tax or estate duty (abolished in 2008) — meaning TIC inheritance of property is tax-free. Should Singapore ever reintroduce estate duty as part of a broader fiscal package, TIC structures with careful will-drafting could become even more strategically important.

Can a husband and wife hold a property in different ownership structures for different properties?

Yes. Each property is a separate legal transaction. A married couple can hold their matrimonial home under Joint Tenancy while holding an investment property under Tenancy in Common (with different specified shares). The ownership structure for each property is chosen independently at the time of purchase and can be changed subsequently through the appropriate legal processes (severance for JT→TIC, or mutual transfer for TIC→JT).

Does Tenancy in Common affect the CPF usage rules?

No. Both Joint Tenancy and Tenancy in Common allow each co-owner to use their CPF Ordinary Account (OA) savings for the property purchase, subject to the CPF Withdrawal Limit and Valuation Limit. In a TIC arrangement, each owner’s CPF contribution is typically proportionate to their ownership share — though the CPF Board does not strictly enforce this proportionality. On sale, each owner must refund their own CPF OA withdrawals plus accrued interest (at 2.5% per annum) from their respective sale proceeds.

Can a foreigner co-own a Singapore private condo as a Tenancy in Common co-owner?

Yes. Foreign nationals can co-own Singapore private condominiums (not landed property or HDB flats) under either Joint Tenancy or Tenancy in Common. A foreigner co-owner will attract the 60% ABSD on their proportionate share of the purchase price. In a 50/50 TIC with a foreigner, ABSD applies at 0% for the SC co-owner’s 50% (assuming first property) and 60% for the foreigner’s 50% — resulting in a blended ABSD rate of 30% on the full purchase price. This is significantly lower than a sole foreigner purchase at 60% but still a substantial cost.

What happens to a joint tenancy when the parties divorce?

Divorce does not automatically sever a Joint Tenancy. The JT continues in force until the Family Court issues an ancillary order dealing with the matrimonial property, or until one party serves a notice of severance. In practice, the Family Court’s ancillary order will typically either direct the sale of the property (with proceeds distributed as ordered) or award the property to one spouse with a transfer obligation. Once the Family Court order is made, the property is usually transferred to sole ownership or sold, effectively terminating the JT. During the divorce proceedings, neither party can unilaterally sell the property without the other’s consent or a court order.

Is there stamp duty payable when converting from Joint Tenancy to Tenancy in Common?

Severance of a Joint Tenancy (converting from JT to TIC in equal shares) does not involve a transfer of ownership and generally does not attract stamp duty, as no beneficial interest changes hands. However, if the severance results in unequal shares (e.g. one co-owner transferring 10% of their interest to the other), Buyer’s Stamp Duty (BSD) and potentially ABSD will apply to the transferred portion. For example, if the recipient already owns a property, ABSD at the applicable rate applies to the market value of the interest transferred. This is a key consideration in decoupling structures. See our decoupling guide for the full analysis.

Can I leave my Tenancy in Common share to anyone I choose in my will?

Yes, subject to Singapore’s intestacy and family provision laws. A TIC owner can bequeath their share to any person — family member, friend, charity, or trust — provided they have a valid, witnessed will. Singapore does not currently have forced heirship rules (unlike some civil law jurisdictions), so a TIC owner has broad testamentary freedom over their property share. However, the Inheritance (Family Provision) Act allows certain family members (spouses, children) to apply to court for a greater share of the estate if the will does not adequately provide for them. Executors should seek legal advice when a TIC property forms a significant part of the estate.

DISCLAIMER: All information in this article is for general informational and educational purposes only and does not constitute legal, tax, or financial advice. Ownership structuring decisions have significant stamp duty, estate, and legal implications. The IRAS anti-avoidance provisions under Section 33A of the Income Tax Act can apply to arrangements entered into for the purpose of obtaining a tax advantage. Readers should consult a qualified conveyancing solicitor and a property tax advisor before making any ownership structuring decisions. LovelyHomes.com.sg is an independent editorial platform. Refer to official sources: IRAS (iras.gov.sg), SLA (sla.gov.sg), CPF Board (cpf.gov.sg), Ministry of Law (mlaw.gov.sg).

Upgrading from an HDB flat to a private condominium is the most common property milestone in Singapore. For a Singapore Citizen couple who bought their HDB in the early 2010s, the combination of substantial HDB appreciation, accumulated CPF savings, and rising household income has made condo upgrading more achievable than it has ever been — but the transaction is still the most financially consequential decision most families will make. Getting the sequencing wrong can cost S$300,000 or more in avoidable Additional Buyer’s Stamp Duty (ABSD). This guide walks you through every step, from checking your eligibility to collecting your new keys.

Quick Answer — HDB to Condo Upgrade at a Glance

Minimum Occupation Period (MOP): You must have fulfilled 5 years’ MOP before selling your HDB flat

ABSD — Sell First: Zero ABSD if you sell your HDB before purchasing the condo

ABSD — Buy First: 20% ABSD upfront, claimable if you sell the HDB within 6 months (SC couples only)

LTV for second property: 45% maximum loan-to-value (55% down payment required) if you still hold the HDB at the time of condo purchase

CPF usage: Your CPF OA (refunded from HDB sale + current balance) can fund the new condo’s down payment and monthly mortgage

2026 market context: Private prices up 0.3% q-o-q in Q1 2026; just ~8,100 new launch units in the 2026 pipeline — act with research but without panic

Step 1 — Check Your HDB Eligibility: Has Your MOP Been Met?

The first gateway to upgrading is the Minimum Occupation Period. For most HDB flats (BTO and resale), the MOP is 5 years from the date you collect the keys. You cannot sell your HDB flat, rent out the entire flat, or purchase a private property — whether in Singapore or overseas — until your MOP has been fulfilled. This applies to both joint owners.

Exceptions exist for certain special categories (e.g., divorce, death of owner, financial hardship), but these require HDB approval. For the vast majority of upgraders, the path is straightforward: wait out the MOP, then proceed. Check your MOP completion date on the HDB website or via the My HDBPage portal.

Step 2 — The Critical Decision: Sell First or Buy First?

This is the most consequential decision in the entire upgrader journey. It determines whether you pay S$0 or potentially hundreds of thousands of dollars in ABSD, and it shapes your entire financing plan. There is no universally right answer, but there is a framework for making the decision.

Option A — Sell First (Recommended for most upgraders)

You sell your HDB flat first, collect the proceeds, clear your HDB loan (if any), and receive your CPF refund (principal drawn plus accrued interest). You are then in the position of a first-time private property buyer: clean title history, 75% LTV (25% down payment), and zero ABSD as a Singapore Citizen buying your first private property. The trade-off is a temporary housing gap — you need somewhere to stay between selling the HDB and moving into the new condo. Options include renting privately, staying with family, or timing the HDB sale to coincide with a condo’s TOP date.

Option B — Buy First (ABSD Remission Route)

An SC couple can purchase a replacement private home while still owning the HDB flat, pay the 20% ABSD upfront, and then apply for a remission from IRAS after selling the HDB — provided the HDB is sold within 6 months of the condo’s purchase date (or 6 months after the condo’s TOP date for uncompleted projects). If the conditions are met, IRAS refunds the full 20% ABSD. The advantage is continuity of housing with no displacement. The risks are: (1) LTV drops to 45% because you hold two properties; (2) the 6-month sale deadline creates pressure; (3) if you miss the deadline for any reason, the ABSD is forfeited.

Important: Only SC-SC or SC-SPR couples qualify

The ABSD remission for replacement property purchases applies only to married couples where at least one spouse is a Singapore Citizen. Single buyers and SPR-SPR couples do not qualify for this remission. Always verify your eligibility with your conveyancing lawyer before relying on this route.

Sell First vs Buy First — Side-by-Side Comparison

Factor

Sell First

Buy First (with Remission)

ABSD payable upfront

S$0

S$370,000 (20% on S$1.85m)

ABSD recoverable?

N/A — no ABSD paid

Yes, if HDB sold within 6 months of new purchase

Interim housing needed?

Likely yes — bridge gap between sale and move-in

No — can stay in HDB until new condo TOP or handover

Bridging loan required?

Possibly (for IPA lapse or timing gap)

Usually no; but servicing 2 mortgages concurrently is a risk

Financial flexibility

Full sales proceeds available before next purchase

Tie-up of capital; dual mortgage risk

Ideal for

Buyers who want a clean break; financial discipline preferred

Families who need continuity of housing; confident of selling HDB within 6 months

Risk

Temporary displacement; may miss specific launch

ABSD remission application not guaranteed; timing pressure

Key Takeaway

For most HDB upgraders, Sell First eliminates ABSD entirely and reduces financial risk. Buy First suits families who cannot afford temporary displacement and are confident in selling their HDB within 6 months.

Source: IRAS / CPF Board — 24 April 2026

lovelyhomes.com.sg

Step 3 — Understanding Your Finances: How Much Can You Afford?

The upgrader’s budget equation has three inputs: net HDB sale proceeds, current CPF OA balance, and borrowing capacity. Here is how each works.

Net HDB proceeds: Your gross HDB sale price minus (a) the outstanding HDB loan balance (if any), (b) the CPF principal withdrawn plus accrued interest at 2.5% per annum (this is refunded back to your CPF OA, not paid in cash), (c) legal and conveyancing costs, and (d) agent commission (typically 1–2% of sale price). The cash proceeds are what remains after all of the above — in a fully-paid-up HDB bought in 2010, this could be substantial cash plus a large CPF refund.

CPF OA balance (post-refund): Once your HDB is sold, all CPF OA monies drawn for the purchase (plus 2.5% p.a. accrued interest) are returned to your OA. This refreshed CPF balance can be applied toward the down payment and monthly instalments of the new condo. Note: the CPF Usage Rules for private property limit how much you can use depending on the remaining lease of the property and your age at the time of purchase. For a 99-year leasehold condo with >60 years remaining, the full Valuation Limit applies.

Loan eligibility (TDSR): Your Total Debt Servicing Ratio must not exceed 55% of your gross monthly income across all outstanding debt obligations. For most salaried couples in dual-income households, this is not the binding constraint. The loan quantum for a private property is subject to a 75% LTV (Sell First) or 45% LTV (Buy First while HDB still held). At 75% LTV, a S$1.85 million condo requires a S$462,500 down payment (25%), of which at least 5% (S$92,500) must be in cash.

Step 4 — Buyer’s Stamp Duty: What You Will Pay

BSD is payable by every buyer — it applies regardless of whether you hold any other property. It is calculated on the higher of the purchase price or the market value of the property, using the progressive table below.

BSD Rates in Singapore 2026

Purchase Price Band

BSD Rate

BSD on That Band

First S$180,000

1%

S$1,800

Next S$180,000 (S$180k–S$360k)

2%

S$3,600

Next S$640,000 (S$360k–S$1m)

3%

S$19,200

Next S$500,000 (S$1m–S$1.5m)

4%

S$20,000

Next S$1,500,000 (S$1.5m–S$3m)

5%

S$75,000 max in this band

Above S$3,000,000

6%

Variable

Key Takeaway

BSD on a S$1.85 million condo = S$1,800 + S$3,600 + S$19,200 + S$20,000 + (S$350,000 × 5%) = S$1,800 + S$3,600 + S$19,200 + S$20,000 + S$17,500 = ~S$62,100.

Source: IRAS — iras.gov.sg/taxes/stamp-duty — 24 April 2026

lovelyhomes.com.sg

Step 5 — New Launch vs Resale: Which Route for Upgraders?

New launch condos offer the Progressive Payment Scheme (PPS), where you pay in stages as construction milestones are reached. This creates a natural cash-flow buffer: you do not need the full loan amount drawn down on day one, giving you time to sell your HDB and rebuild savings before full monthly instalments begin. The trade-off is a 3–4 year wait for TOP, during which you may need to rent. New launches in Singapore’s 2026 pipeline are heavily subscribed — popular projects such as Pinery Residences achieved a 92.5% launch-weekend take-up rate in early 2026 — so acting decisively at launch is important for choice units.

Resale condos offer immediate occupation, avoiding the rental gap entirely. You can time the HDB sale to coincide with resale condo completion in as little as 8–12 weeks. The full loan amount is drawn down from day one, so your monthly commitment is immediate. Resale units in popular districts (15, 19, 23, 26) may command a premium over new launches on a per-square-foot basis, but you avoid the risk of TOP delays and the uncertainty of unit quality before handover.

Step 6 — Executive Condominiums: The Upgrader’s Middle Ground

Executive Condominiums (ECs) are a hybrid product developed by private developers but sold at subsidised prices to HDB upgraders. They are subject to an eligibility framework (Monthly Household Income ceiling: S$16,000; you must not have owned private property in the preceding 30 months; at least one applicant must be SC or PR), but if you qualify, ECs offer condo-standard facilities at prices typically 20–30% below comparable private condos in the same area. ABSD is not payable when buying a new EC directly from the developer, even if you still own your HDB flat — a significant advantage over the private condo route.

The 2026 EC pipeline includes Rivelle Tampines EC and projects in Sembawang and Plantation Close. These are worth considering for eligible upgraders who prioritise value over prime CCR address.

Step 7 — Getting Your In-Principle Approval (IPA)

Before signing any Option to Purchase (OTP), secure an In-Principle Approval (IPA) from your bank. An IPA gives you a formal indication of the loan quantum, interest rate, and tenure the bank is willing to offer, based on your income documents and credit profile. Having an IPA in hand at the showflat means you know your exact budget envelope and can make a confident, irreversible decision when the OTP is presented. Note that an IPA is not a formal Letter of Offer — the bank will conduct a full assessment when you submit a formal loan application — but it is the closest proxy available before a specific unit is identified. Most banks issue IPAs within 2–3 business days. Compare rates across at least 3 banks, including fixed-rate (typically 2.5–3.5% in 2026), floating SORA-linked, and fixed-SORA hybrid packages.

Step 8 — The Legal Process: From OTP to Keys

For a new launch condo, the process runs: (1) exercise the OTP (1% booking fee) → (2) sign the Sale & Purchase Agreement within 3 weeks (typically 4–9% more paid) → (3) engage a conveyancing lawyer → (4) pay BSD (and ABSD if applicable) within 14 days of OTP exercise → (5) progress payments as per the PPS schedule over the construction period → (6) collect keys at TOP → (7) complete final payment and receive Certificate of Statutory Completion. The conveyancing lawyer handles stamp duty payments, title searches, bank loan drawdown, and final completion. Budget S$3,000–S$5,000 in legal fees for a standard new-launch purchase.

2026 Market Context — Is Now the Right Time?

The Q1 2026 URA flash estimate showed a modest 0.3% quarter-on-quarter increase in private residential prices, with the OCR (where most upgrader condos are priced) leading at +1.3% q-o-q. The 2026 launch pipeline is significantly constrained at approximately 8,100 units across 17 projects, down 30% from 2025. This supply tightness tends to sustain prices and take-up rates at quality launches, as seen in the strong weekend sales figures at Pinery Residences (92.5% sold) in Q1 2026.

For upgraders, the current environment suggests a window of stable prices with limited new supply — not a runaway market, but also not a buyer’s market in the traditional sense. Prioritise location, unit type, and fit-for-purpose over speculation. The best condo purchase for an upgrader family is one they can comfortably afford and intend to occupy for at least 5 years.

Frequently Asked Questions

Can I own an HDB and a condo at the same time?

Yes, but only after fulfilling the HDB MOP. An SC or SPR can hold both an HDB flat and a private property simultaneously after MOP, subject to paying 20% ABSD (SC) or 30% ABSD (SPR) on the private purchase. You must then sell the HDB within the prescribed timeframe to claim ABSD remission (SC couples only). You cannot own an HDB and a private property at the same time before MOP — this would breach HDB ownership rules.

Does CPF need to be returned when I sell my HDB?

Yes. All CPF monies withdrawn for the HDB purchase (including the principal and accrued interest at 2.5% p.a.) are automatically returned to your CPF OA upon sale. You do not get this cash in hand; it goes back into your CPF OA. However, you can then re-use this CPF OA balance for the new condo purchase, subject to CPF usage rules for private properties.

What is the maximum loan for a condo if I still own my HDB?

If you hold an existing property (including an HDB flat) at the time of the condo purchase, the maximum LTV for a bank loan is 45% — meaning a 55% down payment is required, of which 25% must be in cash. This is a significant constraint and one of the key reasons most upgraders prefer the Sell First strategy.

Can I use my CPF to pay for the condo if the remaining lease is short?

CPF usage for private property is subject to the Lease Remnant Restriction: the property’s remaining lease must cover the youngest buyer to age 95. For most new-launch 99-year leasehold condos, this requirement is easily satisfied. Shorter-lease or older resale properties may restrict CPF usage or trigger a pro-rated cap. Check the CPF online calculator or consult your conveyancing lawyer.

What if I miss the 6-month ABSD remission deadline?

If you fail to sell your HDB within the 6-month window, the ABSD is not refunded. It is permanently forfeited. IRAS does grant extensions in exceptional circumstances (e.g., death of a co-owner), but these are discretionary and not guaranteed. If you are buying first, build in a buffer and engage a property agent to market your HDB promptly after exercising the condo OTP.

Disclaimer: This guide is for general information only and does not constitute financial, legal, or tax advice. ABSD rates, LTV limits, CPF rules, and HDB eligibility conditions are subject to change. Always verify current figures on the IRAS website and CPF Board, and consult a licensed property agent and conveyancing solicitor before proceeding.

HDB’s May 2026 Build-To-Order launch is expected to open for application in the first week of May, the second launch of the year after the February 2026 exercise. Based on the sites gazetted through URA Government Land Sales in late 2024 and 2025, and on pre-launch developer briefings released by HDB, we preview the likely site mix, expected application rates, and the first-timer vs second-timer allocation picture.

At a glance

May 2026 BTO is expected to launch approximately 6,800 flats across Standard, Plus and Prime categories.

Confirmed launch sites include Bukit Merah (Henderson), Tampines (Tampines North), Tengah (Garden District) and Woodlands (Woodlands North Coast).

Bukit Merah Henderson is the category headliner — Prime location classification; expect application rates above 10x for 4-room.

Family grant framework (Enhanced CPF Housing Grant, Family Grant, Proximity Housing Grant) applies; first-timer ballot weights unchanged.

Applications typically close 7 days after opening; ballot results announced 4–6 weeks later.

What a Plus / Prime BTO classification means for May buyers

The Plus and Prime classifications — introduced under the revised 2024 HDB framework — replace the legacy Mature / Non-Mature framework for new BTO launches. Standard flats follow the traditional BTO rules. Plus flats, typically in choice non-mature locations, carry a 10-year Minimum Occupation Period (up from 5) and subsidy clawback on resale. Prime flats, in the most central and amenity-rich locations, carry the same 10-year MOP plus a resale income ceiling that applies when the flat is eventually sold.

Buyers should model the full hold cycle before ballot. A Prime classification delivers an under-market purchase price and exceptional location, but the 10-year MOP plus resale-income-ceiling combination narrows the eventual buyer pool at exit. For households expecting to stay in the flat 15–20 years, the Prime route is straightforward. For households planning a shorter trade-up, the Standard category is typically the better fit.

Site-by-site expectations

Bukit Merah (Henderson) — Prime classification

Estimated launch: approximately 1,200 flats, 4-room and 5-room mix. The site sits on Henderson Road, about a 5-minute walk from Redhill MRT (East-West Line) and within walking distance of Dawson Estate and Bukit Merah Central. The Prime designation is expected to deliver a substantial price discount vs the adjacent resale market, where four-room flats are transacting in the S$850–S$1,050k band. Expect application rates for 4-room flats above 10x on the first-timer pool.

Tampines (Tampines North) — Plus classification

Estimated launch: approximately 1,600 flats, full mix from 2-room Flexi to 5-room. The site is adjacent to the Tampines North MRT (Cross Island Line Stage 1, opened late 2024) and sits in a growing mixed-use district bracketed by Tampines Regional Centre and Tampines North Park. The Plus classification carries a 10-year MOP but no resale-income ceiling. Expect application rates of 4–6x on 4-room flats.

Tengah (Garden District) — Standard classification

Estimated launch: approximately 2,400 flats, the largest single-site batch of the May 2026 launch. The Tengah Garden District is the western master-planned town pioneered as Singapore’s first car-free town centre. The Jurong Region Line MRT is under construction with stations expected to open progressively from 2027 through 2029. Expect application rates of 2–3x on 4-room flats given the larger supply and the longer MRT wait.

Woodlands (Woodlands North Coast) — Standard classification

Estimated launch: approximately 1,600 flats. The Woodlands North Coast site benefits from the recently opened Thomson-East Coast Line terminus at Woodlands North, cross-border connectivity via the under-construction Johor Bahru-Singapore Rapid Transit System, and the still-developing Woodlands Regional Centre. Expect application rates of 2–3x on 4-room flats.

First-timer, second-timer and quota mechanics

HDB ring-fences a majority of every launch for first-time applicant families — specifically, at least 85% of four-room and larger Standard flats are reserved for first-timer families. Two-timer applicants (families who already own or have previously owned an HDB flat, EC or private property) compete for the remaining quota and typically face ballot odds 2–4x longer than first-timers. Singles and first-timer families under the joint application framework are balloted separately under the 2-Room Flexi scheme.

Prime and Plus flats have the same general first-timer preference but with a further stratification: households with household income under the relevant bracket receive the CPF Housing Grant stack, which can add up to S$80,000 in grants depending on income-group position.

Application tactics for a strong ballot position

Three behavioural points the HDB system rewards. First, ballot entry across multiple launches does not compound — each launch is a fresh lottery. But second-timers who roll over their application to a next launch do receive a small priority-weighting uplift, capped at two rollovers. Second, the Proximity Housing Grant (S$30,000 for applying to live with or near parents) is a strong signal to the ballot system and materially improves odds at Bukit Merah Henderson and Tampines North. Third, the Enhanced CPF Housing Grant is income-tiered — the lowest income tier receives the largest grant, which influences eligibility for Standard categories.

Expected timeline

What May 2026 means for the resale market

A May launch of approximately 6,800 flats is a moderate supply pulse into the BTO pipeline, but the immediate effect on resale is indirect. In the short term, first-timer applicants who commit to a BTO ballot typically withdraw from active resale viewings while waiting for the result, which softens resale transaction volume for 4–6 weeks. If ballot rates are high (as expected for Bukit Merah Henderson), disappointed applicants often re-enter the resale market in late June, which typically produces a small transaction bounce in July. This pattern has been consistent across the last six BTO launch cycles.

Frequently asked questions

When exactly does the May 2026 BTO open for application?

HDB typically announces the exact launch window approximately two weeks before applications open. Based on past May launches, the window usually falls in the first 10 days of May, with applications closing roughly 7 days after opening.

Can I apply for both a BTO and a resale flat at the same time?

You can apply for a BTO while viewing resale flats, but you cannot hold a BTO booking and simultaneously enter a resale HDB agreement. Most applicants use the BTO ballot window to continue resale research; successful balloters decline at booking if they have already committed to a resale.

How much is the ABSD and BSD on a BTO flat?

BTO flats are sold directly by HDB under the Housing & Development Act. Buyers’ Stamp Duty applies on the purchase price at the standard schedule. Additional Buyer’s Stamp Duty does not apply to first-timer BTO applicants buying their first residential property.

What is the difference between Plus and Prime?

Both carry a 10-year MOP and subsidy clawback on sale. Prime adds a resale-income-ceiling constraint at exit — the eventual resale buyer must meet an income ceiling. Plus has no such eventual-buyer constraint.

Can PRs apply for BTO flats?

PR-only households cannot apply for a BTO. A Singapore Citizen applying with a PR spouse or family nucleus can apply under the HDB Fiancé/Fiancée, Family or Joint Singles scheme.

What happens if I decline the allocated BTO flat?

Declining a BTO selection appointment has consequences for future applications: after two non-selections in a 12-month period, HDB may debar the applicant from applying for BTO for a period of up to 12 months. Plan your ballot portfolio carefully.

Source

Source: HDB public information on the BTO launch framework and 2024 revised category system, URA GLS announcements, and public site-gazetting records. Full documentation: HDB BTO flat selection and URA GLS current sites.

Editorial note. This article is based on public-domain data released by HDB, URA, Singapore Land Authority and MAS as at 23 April 2026. All analysis is our own. No marketing-agency research is cited. Figures may be revised in subsequent official releases — always refer to the latest authoritative source before making a housing decision.

The Progressive Payment Scheme (PPS) is the default payment structure for new-launch private residential property in Singapore. Under the scheme, you pay a small deposit on booking, incremental tranches as construction reaches each milestone, and the final balance only when the keys are handed over at TOP. This 2026 guide walks through each stage, the CPF and cash flow at every milestone, and the practical cash-flow implications for a typical Singapore buyer.

Quick Answer

The Progressive Payment Scheme spreads purchase payments across seven construction milestones, from OTP booking to CSC (final 12-month defect period).

On launch day you pay 5% in cash (the Option fee). Within 8 weeks you pay a further 15% on Sale & Purchase signing — of which up to 5% may be from your CPF Ordinary Account.

The remaining 80% is drawn progressively from your home loan as construction reaches foundation, walls, ceiling/roof, TOP and CSC.

Monthly mortgage payments begin after the first drawdown — not on the day you sign the OTP.

PPS is the default for new-launch condominiums. The Deferred Payment Scheme (DPS), where available, pushes the bulk of payments to TOP but typically carries a price premium and stricter eligibility.

What is the Progressive Payment Scheme?

The Progressive Payment Scheme is the payment structure prescribed by the Urban Redevelopment Authority for property sold in the primary market under the Housing Developers (Control and Licensing) Act. Under PPS, the purchase price is paid in incremental tranches timed to construction milestones, rather than in a single lump sum at handover. The structure exists for two reasons: it reduces the buyer’s financing burden during the 3–4 year build period, and it gives the developer progressive cash-flow to fund construction without requiring 100% escrow.

PPS applies to all uncompleted private residential property purchased directly from the developer. For completed-and-TOP-issued stock sold in the primary market, the payment structure is different — typically the full balance is due within 12 weeks of OTP.

The seven PPS milestones

Stage 1 — Option to Purchase (5% in cash)

On launch day, you pay a 5% Option fee to the developer in cash or cashier’s order. This secures your right to purchase the specific unit for a 3-week Option period. During this window, you finalise financing, commission a conveyancing lawyer and decide whether to proceed. If you do not exercise the Option, you forfeit 1.25% of the Option fee (one-quarter of the 5%) and the developer returns the balance 3.75%.

Stage 2 — Sale & Purchase Agreement (15% within 8 weeks)

Within 8 weeks of Option exercise, you sign the Sale & Purchase Agreement and pay a further 15% of the purchase price. A typical split is 5% in additional cash and 10% from CPF Ordinary Account, though this varies by buyer. At this stage, you also pay Buyer’s Stamp Duty and, if applicable, Additional Buyer’s Stamp Duty to IRAS — due within 14 days of S&P signing.

Stage 3 to 5 — Construction-linked draws (45% total)

Once construction reaches each milestone, the developer issues a payment notice. Your home-loan bank draws down against your loan facility to pay the developer directly. Monthly mortgage instalments begin on the bank side after the first drawdown. The three construction-linked milestones are: foundation complete (10%); reinforced concrete framework, carpark and partition walls complete (10%); ceiling, roof and external wall complete with windows installed (25%). Typical elapsed time between Stage 2 and Stage 5 is 24–30 months for a mid-size project.

Stage 6 — TOP and key handover (25%)

When the Temporary Occupation Permit is issued, the developer notifies the buyer. You pay the next 25% tranche and receive the keys. You can now occupy the unit, lease it out, or commission renovation work. The MCST (management corporation strata title) is also constituted at or shortly after this milestone, and your monthly maintenance-fee obligation begins.

Stage 7 — Certificate of Statutory Completion (10%, within 12 months)

The final 10% is held back and released when the Certificate of Statutory Completion is issued — typically within 12 months of TOP. CSC confirms that all building works conform to the approved plans and that the defects-liability period has been honoured. This hold-back is the buyer’s main leverage during the first-year defects period, and you should work through your defects snag list methodically before authorising the final tranche.

How the CPF + cash + loan split actually works

The payment split varies by buyer, but a common structure for a Singapore Citizen first-time buyer is:

The 5%/15% split at the front of the scheme is not legally fixed — it is the default under URA rules. A buyer with additional CPF headroom may redirect more of Stage 2 from cash to CPF. A buyer with limited CPF but strong cash flow may pay Stage 2 entirely in cash. Your conveyancing lawyer will confirm the precise split on your S&P, and your bank’s mortgage specialist will coordinate the CPF withdrawal application.

Worked example — S$2,000,000 purchase

Consider a Singapore Citizen first-time buyer purchasing a S$2 million new-launch condominium under PPS. Total BSD is S$64,600, ABSD is nil on a first property.

BSD (paid in 14 days): S$ 64,600 (from cash or CPF)

Upfront total (weeks 0-8):

Cash required: S$ 200,000 – 264,600

CPF required: S$ 200,000 – 264,600

Stages 3-7 (24-48 months):

80% loan drawdown: S$1,600,000 (monthly instalment from first drawdown)

Approx. monthly mortgage at 3.5% / 30 yrs on S$1.6M:

Full-loan equivalent: S$ 7,184 per month

Starts: After Stage 3 first drawdown, scales as loan balance grows

Note two things. First, the BSD payment at Stage 2 is often overlooked in cash-flow planning. A S$2 million purchase carries approximately S$64,600 of BSD due within 14 days of S&P — a buyer who has budgeted only the 5% cash at OTP is likely to be caught short. Second, the monthly mortgage payment ramps up over the construction period: from roughly S$900 per month after Stage 3 (10% of loan drawn) to the full S$7,184 once all drawdowns are complete at TOP.

How monthly mortgage payments scale across milestones

This ramp is the single most important cash-flow feature of PPS. A buyer who qualifies on the full-loan TDSR check still has a much lighter monthly burden in the first 18–24 months of construction, which can be useful for offsetting stamp duty and renovation savings.

PPS vs Deferred Payment Scheme (DPS)

For completed inventory of some developments — particularly foreign-developer-owned assets and late-cycle unsold stock — developers sometimes offer a Deferred Payment Scheme as an alternative. Under DPS, the buyer pays 20% at OTP and S&P combined, defers the remaining 80% to TOP (or up to 3 years later for completed units), and takes no home-loan drawdowns during the deferral period.

DPS improves short-term cash flow at the cost of a slightly higher purchase price. For a buyer expecting a large cash event (bonus, asset sale, parental gift) at TOP, DPS can make sense. For a buyer with steady cash flow through the construction period, PPS is materially cheaper on a total-cost basis.

Common pitfalls to avoid

Pitfall 1 — Budgeting only the 5% at OTP

The 5% OTP is not the upfront cost. You need 20% plus BSD/ABSD in the first 8 weeks. Add renovation, agent, legal and moving costs and you are looking at 22–25% of purchase price in the first 12 weeks, not 5%.

Pitfall 2 — Forgetting BSD is due 14 days after S&P

BSD is not paid at TOP. It is due within 14 days of S&P signing. On a S$2M purchase that is S$64,600 — budgeted separately from the 20% downpayment.

Pitfall 3 — Mixing up loan disbursement schedule with own cash flow

The bank draws your loan on the developer’s notice — you do not pay the developer directly. But the bank’s monthly instalment on the drawn loan balance comes out of your account from the first drawdown.

Pitfall 4 — Releasing the CSC tranche before defects are fixed

The final 10% is your main leverage during the 12-month defects-liability period. Work through the snag list methodically and only authorise CSC release when outstanding defects are resolved or formally noted.

The PPS stamp-duty timing gotcha

Buyer’s Stamp Duty and Additional Buyer’s Stamp Duty are payable within 14 days of the dutiable instrument. For a new-launch PPS purchase, the dutiable instrument is the Sale & Purchase Agreement signed at Stage 2 — not the Option to Purchase signed at Stage 1. This timing nuance matters for three reasons.

First, you have a measurable planning window — roughly 10 weeks from launch day — to assemble the cash to pay both the Stage 2 downpayment and the stamp duty. Second, the ABSD exemption application window (for married couples claiming spousal ABSD remission, for example) opens at the S&P stage, not at OTP. Third, if the government announces a cooling-measure change between OTP and S&P, the stamp-duty rate that applies is the rate in force on the S&P date, not the OTP date. This has historically been a source of significant buyer anxiety during cooling-measure cycles.

Frequently asked questions

1. Do all new-launch private condominiums in Singapore follow PPS?

Yes. PPS is the default payment structure prescribed by URA for uncompleted private residential property sold in the primary market. Deferred Payment Scheme alternatives are available only for completed or late-cycle inventory at the developer’s discretion.

2. When does my monthly mortgage payment start?

Your monthly mortgage payment starts after the first loan drawdown — typically at Stage 3 (foundation complete), which is usually 6–12 months after S&P signing. Until the first drawdown, you pay no mortgage instalment.

3. Can I pay the whole purchase price upfront?

No. URA rules require the developer to collect payment against milestones under PPS, and a lump-sum upfront payment is not permitted on a new-launch uncompleted unit. You can, of course, make an agreed partial pre-payment on your home loan at any time once the loan has been drawn.

4. What happens if I cannot meet a progress-payment milestone?

Your loan facility covers the milestone drawdowns automatically — the bank pays the developer against your loan balance. The mortgage instalment comes out of your bank account monthly. A genuine default scenario would only arise if your monthly cash flow cannot service the mortgage instalment. Speak to your bank immediately if this looks likely; options typically include a short-term restructure or, in extreme cases, a resale exit.

5. Can I use CPF for the 5% OTP booking fee?

No. The 5% OTP must be paid in cash or cashier’s order. CPF can be used from Stage 2 onwards, subject to the Valuation Limit and Withdrawal Limit framework.

6. When is ABSD payable under PPS?

ABSD (and BSD) is payable within 14 days of signing the Sale & Purchase Agreement at Stage 2, not at OTP. Budget the stamp duty separately from the Stage 2 downpayment.

7. What is the Option fee forfeiture if I do not exercise the OTP?

One-quarter of the 5% Option fee — 1.25% of the purchase price — is forfeited to the developer. The remaining 3.75% is returned within a reasonable period. This is the standard URA-prescribed position and cannot be waived.

8. Does PPS apply to Executive Condominiums?

Yes. Executive Condominiums follow the same PPS milestones as private condominiums. The main EC-specific difference is eligibility and resale-restriction rules on the buyer side, not on the payment-schedule side.

9. Does PPS apply to HDB BTO flats?

No. HDB BTO flats follow a different payment schedule: 10% Option fee at booking (mostly from CPF), then the balance at key collection. Construction-linked progressive drawdowns do not apply to BTO.

10. How long does the full PPS cycle take?

Typically 3–4 years from OTP to CSC for a mid-size project: 2–3 months from OTP to S&P, then 24–36 months through construction to TOP, then a further 12 months to CSC.

11. Can I sell the unit before TOP?

Yes, subject to the standard resale rules for private property. You can sell the uncompleted unit to another buyer via a ‘sub-sale’ arrangement, with the original buyer’s obligations novated to the new buyer. The Seller’s Stamp Duty framework applies on the gain, and Additional Buyer’s Stamp Duty applies to the new buyer — both on the sub-sale price, not the original purchase price.

12. What happens if the developer delays TOP?

The Sale & Purchase Agreement specifies a contractual TOP deadline. If the developer misses it, liquidated damages are payable to the buyer per the S&P terms — typically a fraction of the purchase price per month of delay. Review your S&P clauses carefully; liquidated damages are not uniform across developers.

Disclaimer. This article is for general information only and does not constitute legal, financial or tax advice. Figures referenced reflect the position as at 23 April 2026 and are subject to change without notice. Always verify the latest rates and policies with the official authority — IRAS, HDB, URA, CPF or MAS — before making any property decision. Consult a qualified lawyer, mortgage broker or accountant for advice specific to your circumstances.