Singapore HDB Resale Buying Process Guide 2026: Step-by-Step from HFE to Keys

- 10 steps from eligibility check to key collection — typically 8–12 weeks end to end.

- HFE Letter first — apply for the HDB Flat Eligibility letter before searching; it covers loan eligibility, CPF grants, and flat eligibility in one application.

- Option to Purchase (OTP) — option fee S$1–S$1,000; 21 calendar days to exercise; exercise fee S$1–S$5,000.

- Resale application must be submitted by both buyer and seller within 7 days of OTP exercise.

- COV (Cash-Over-Valuation) — if you agree to pay above HDB’s valuation, the excess is cash only; CPF cannot cover it.

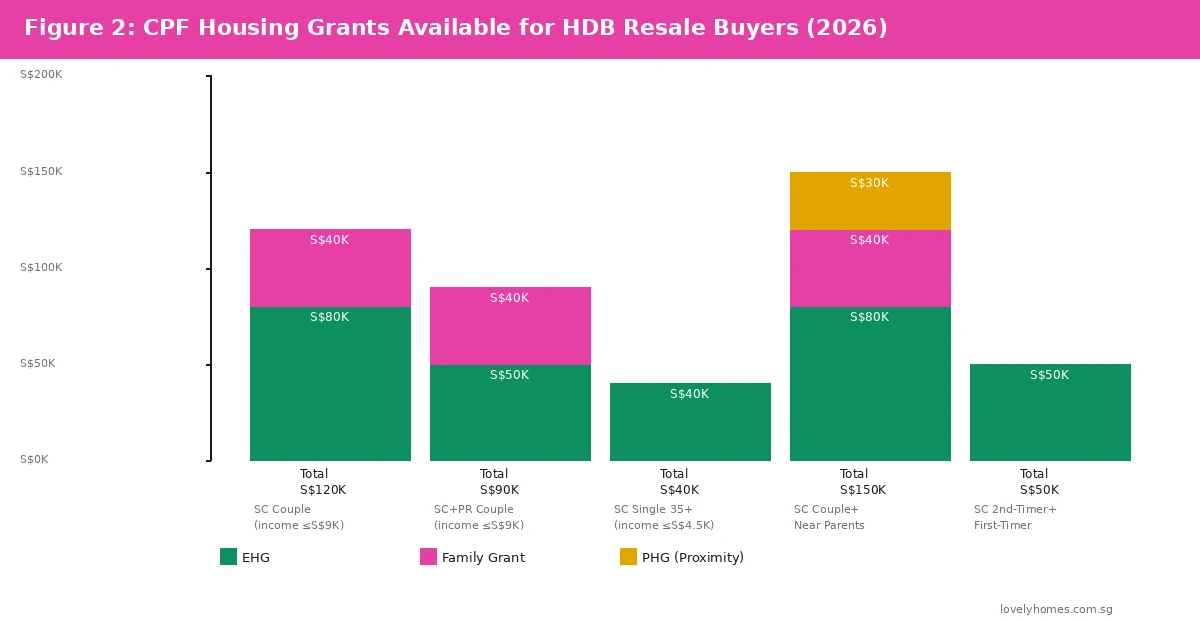

- CPF grants available: EHG (up to S$80K), Family Grant (up to S$80K), Proximity Housing Grant (up to S$30K) — stackable, subject to income ceilings.

- Administering bodies: HDB (eligibility, valuation, approval), MAS (bank loans), IRAS (BSD).

Buying an HDB Resale Flat in 2026: What Has Changed

Purchasing an HDB resale flat remains one of the most common property transactions in Singapore — approximately 27,000–30,000 resale transactions occur each year. But the process has undergone material changes since 2021, most notably the introduction of the HDB Flat Eligibility (HFE) Letter in May 2023 (replacing the prior HDB Loan Eligibility letter and CPF Housing Grant eligibility check with a single, combined application), and the 15-month wait-out period for private property owners effective 30 September 2022.

This guide walks you through every step — from confirming eligibility to collecting your keys — using the current process as at July 2026. It covers who can buy, how to finance the purchase, what grants are available, how to navigate the OTP and resale application, and what costs to budget for.

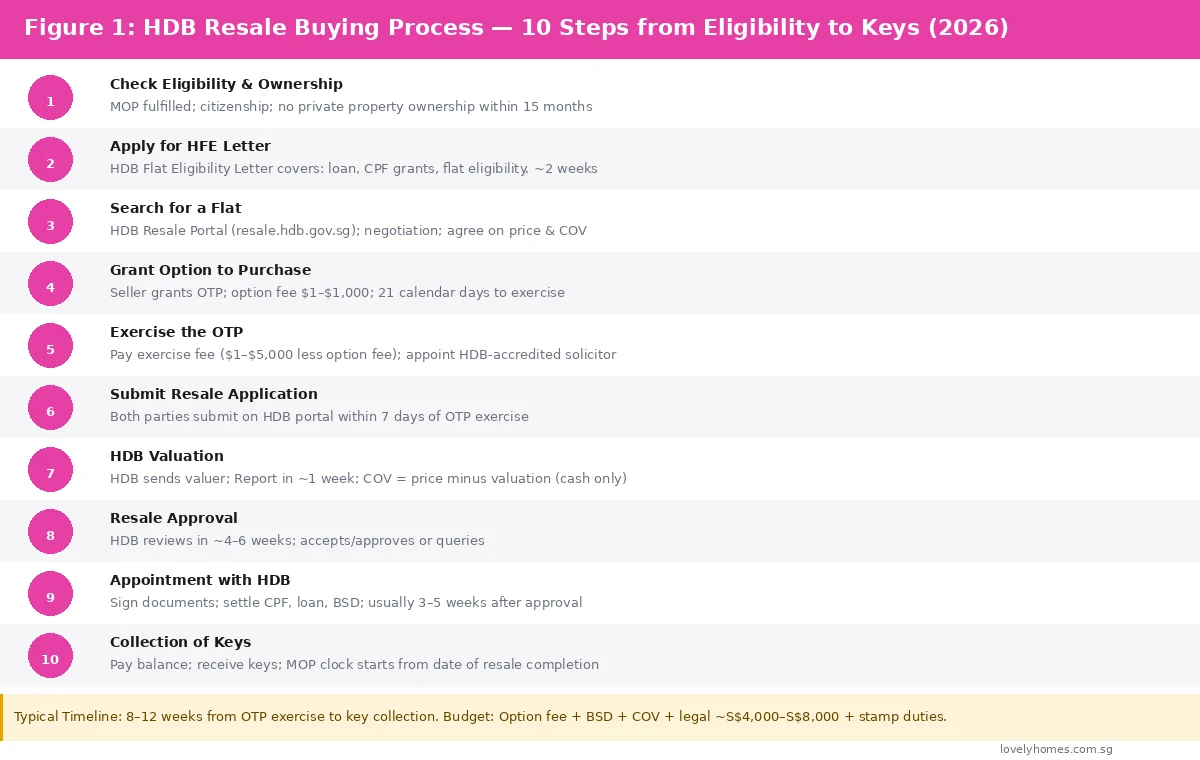

Step 1: Confirm Your Eligibility

Before anything else, you must verify that you and your co-applicant (if any) meet HDB’s eligibility criteria for purchasing a resale flat. The key conditions are:

Citizenship: At least one applicant must be a Singapore Citizen. A Permanent Resident may co-apply, but cannot purchase alone. Singapore Citizens who already own an HDB flat may only purchase a second HDB flat if they dispose of the first within 6 months of completing the resale purchase — they cannot hold two HDB flats simultaneously.

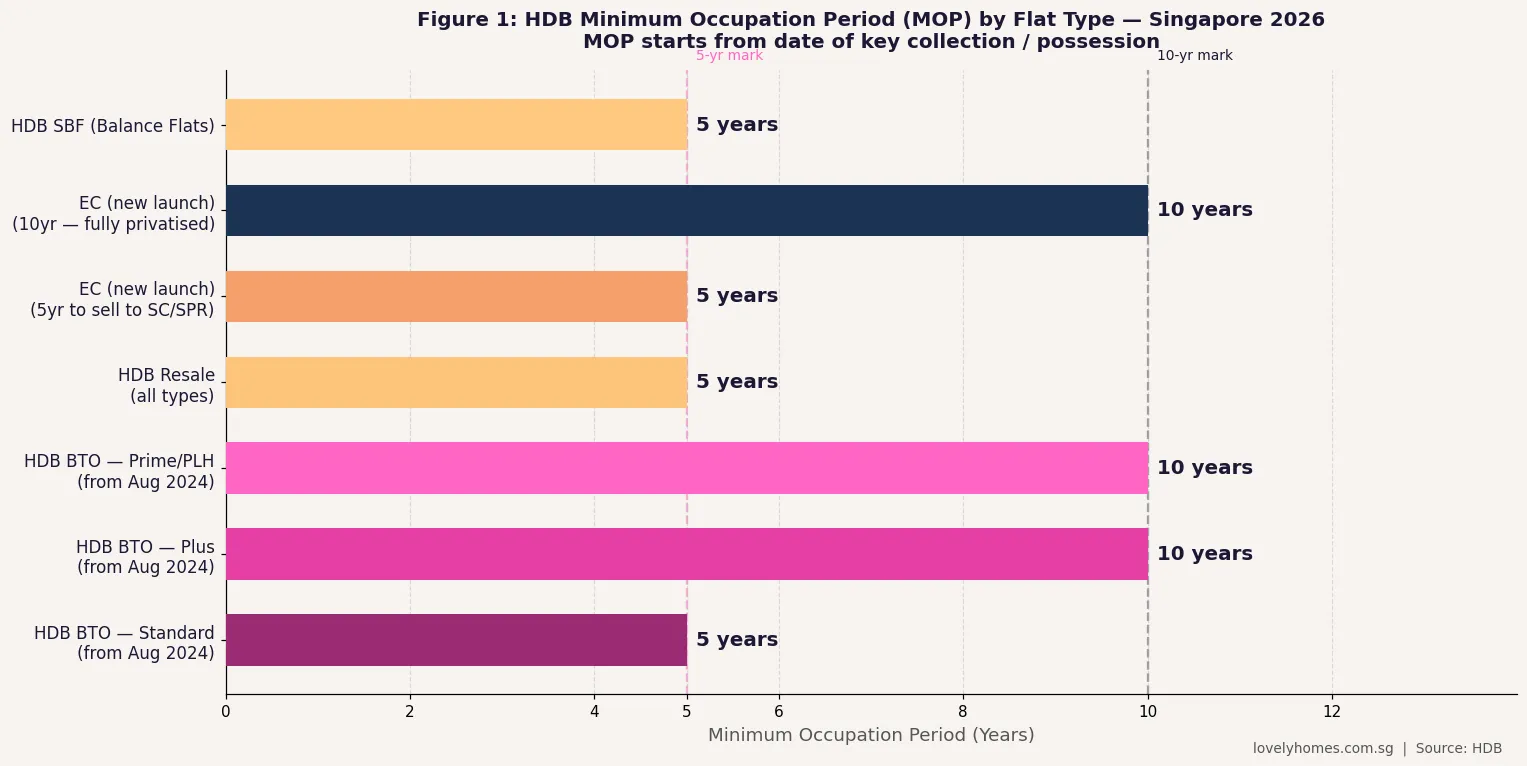

Minimum Occupation Period (MOP): If either applicant currently owns an HDB flat, that flat must have fulfilled its MOP (typically 5 years from date of possession for standard HDB flats; 10 years for Prime or Plus classification flats) before a resale purchase can proceed.

15-Month Wait-Out Period: If either applicant currently owns, or has within the preceding 15 months disposed of, a private residential property, they must wait at least 15 months from the date of disposal before they can purchase an HDB resale flat. This measure was introduced on 30 September 2022 and applies strictly — there are very limited exemptions.

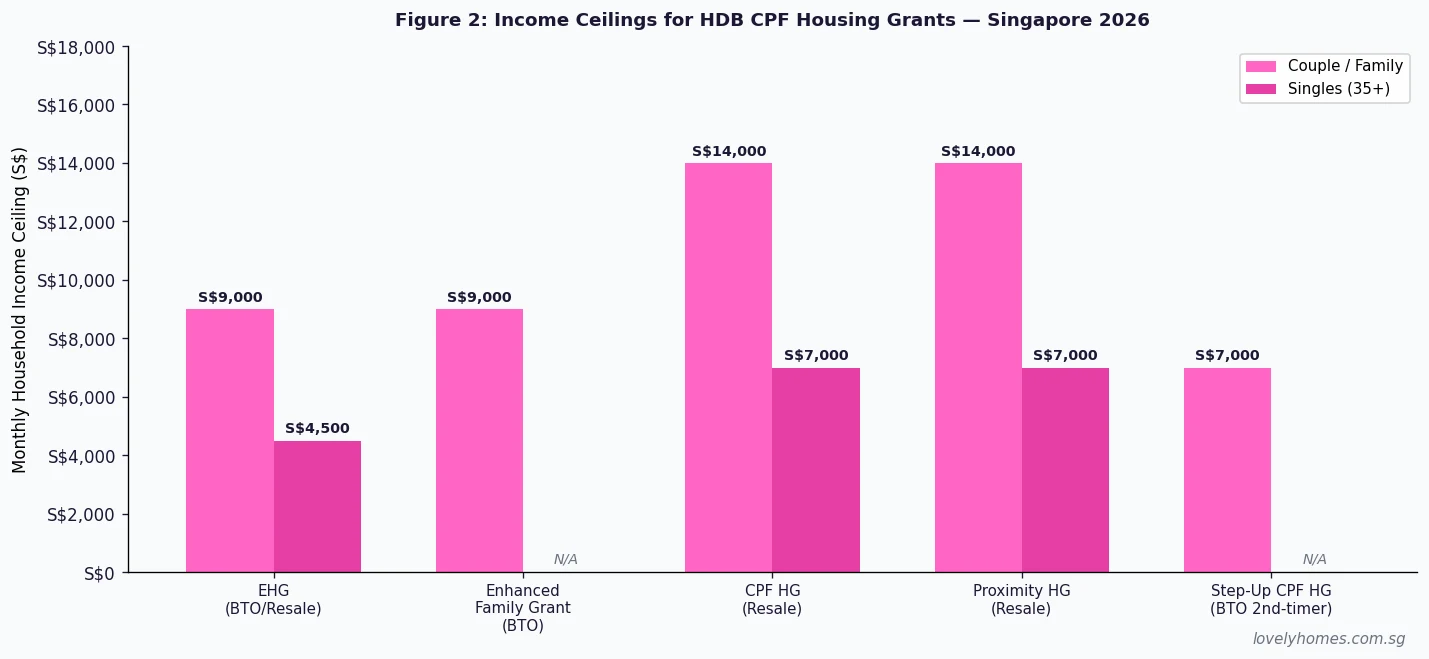

Income ceiling: There is no income ceiling for the purchase of an HDB resale flat itself. Income ceilings apply only to grant eligibility (EHG: S$9,000 household/S$4,500 single; Family Grant: S$14,000; PHG: S$14,000) and HDB loan eligibility (S$14,000 household for concessionary loan).

Step 2: Apply for the HFE Letter

The HDB Flat Eligibility (HFE) Letter, introduced in May 2023, is the single most important document you will obtain before starting your flat search. It is issued by HDB and tells you: (a) whether you are eligible to buy an HDB flat; (b) how much HDB loan you qualify for; and (c) which CPF housing grants you are eligible for and in what amounts.

You apply for the HFE Letter via the HDB Flat Portal (homes.hdb.gov.sg). Processing typically takes 21 business days for HDB loan applicants and about 14 business days if you are seeking a bank loan. The HFE Letter is valid for 6 months from the date of issue. If you plan to take a bank loan rather than an HDB loan, you should also obtain an In-Principle Approval (IPA) from your preferred bank before making an offer — banks do not issue IPAs until after you have the HFE Letter for HDB resale transactions.

HDB strongly recommends — and estate agents have been instructed — that buyers obtain the HFE Letter before signing any OTP. Signing an OTP without a valid HFE Letter exposes you to the risk of being unable to complete the transaction if your financing falls through.

Step 3: Search and Negotiate

HDB resale transactions take place primarily through the HDB Resale Portal (resale.hdb.gov.sg), where sellers list their flats, and through licensed property agents on platforms such as PropertyGuru, 99.co, and the EdgeProp portal. Unlike the BTO process, there is no ballot — you negotiate directly with the seller and agree on a price. HDB does not prescribe or cap resale prices, which are determined entirely by market forces.

Once you identify a flat, check the HDB Resale Price data (available on the HDB and URA websites) to understand recent comparable transactions. Pay attention to the Cash-Over-Valuation (COV) — if you agree to pay more than HDB’s valuation, the excess must be paid in cash only. CPF cannot fund COV. As at July 2026, the median COV in mature estates has been running at S$20,000–S$60,000 depending on flat type and floor level.

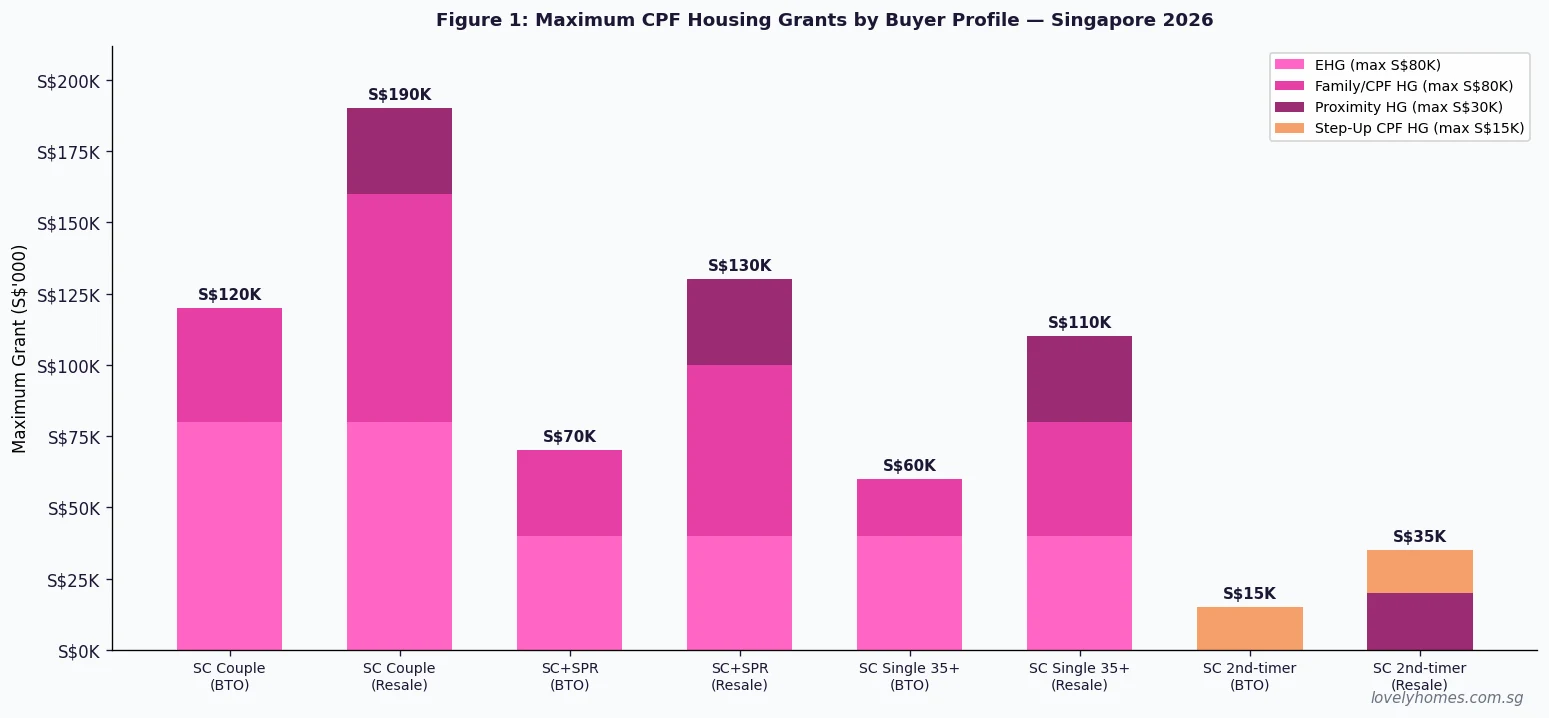

CPF Housing Grants for HDB Resale

HDB resale buyers — particularly first-timers — may be eligible for generous CPF Housing Grants that substantially reduce their effective purchase price. These grants are paid into your CPF Ordinary Account and deducted from the purchase price at completion, reducing the amount you need to borrow.

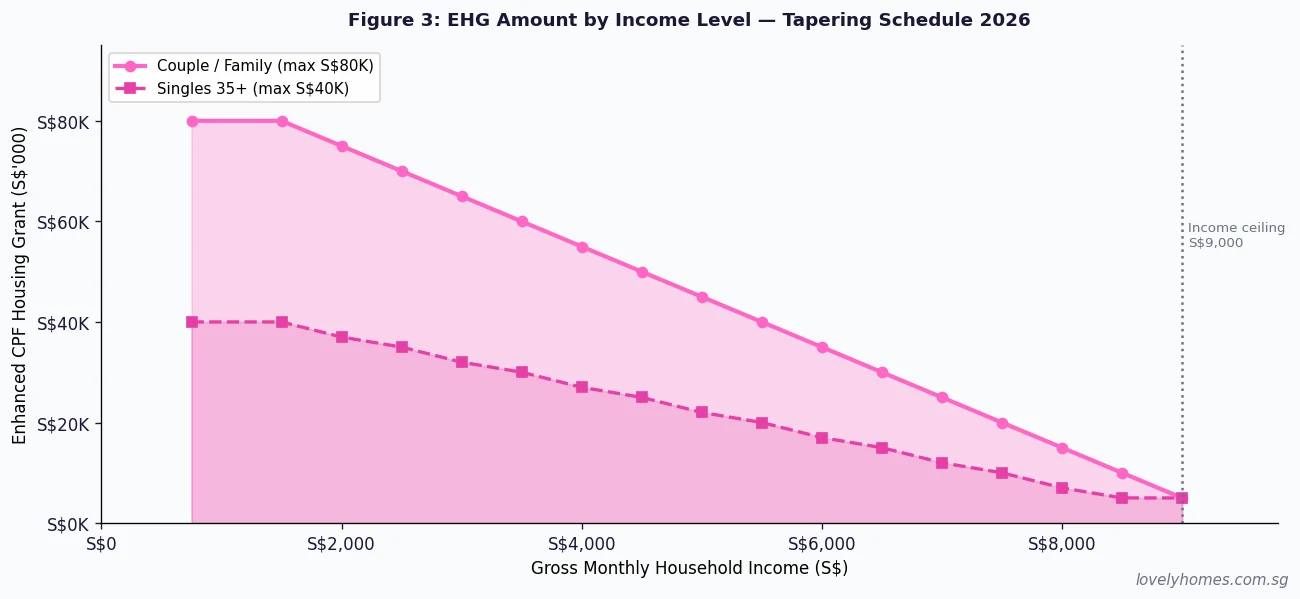

The Enhanced CPF Housing Grant (EHG) is the most substantial: up to S$80,000 for eligible couples (household income ≤S$9,000/month) and up to S$40,000 for singles (income ≤S$4,500/month). The EHG tapers based on income — households earning S$9,000 receive no EHG, while those earning S$1,500 or below receive the full amount. The Family Grant (up to S$80,000 for SC-SC couple buying a 4-room or smaller resale flat) and the Proximity Housing Grant (PHG) (up to S$30,000 if buying within 4km of parents or children, or S$20,000 if buying in the same town) are stackable on top of the EHG, subject to their respective income ceilings of S$14,000 household income.

| Grant | Max (SC-SC Couple) | Max (SC-SPR Couple) | Max (SC Single) | Income Ceiling | Stackable? |

|---|---|---|---|---|---|

| Enhanced CPF Housing Grant (EHG) | S$80,000 | S$60,000 | S$40,000 | S$9,000/mth (couple); S$4,500 (single) | Yes |

| Family Grant (FG) | S$80,000 (4-room or smaller) | S$50,000 | — | S$14,000/mth | Yes |

| Proximity Housing Grant (PHG) | S$30,000 (same town) / S$20,000 (4km) | S$30,000 / S$20,000 | S$15,000 / S$10,000 | S$14,000/mth | Yes |

| Step-Up CPF Housing Grant | S$15,000 (2nd-timer buying 2-room) | — | — | S$7,000/mth | Limited |

Steps 4–6: OTP, Exercise, and Resale Application

Once you and the seller agree on a price, the seller grants you an Option to Purchase (OTP). This is a standardised HDB document (not a private OTP — HDB prescribes the form). The option fee is negotiable between S$1 and S$1,000; this sum is paid to the seller at this stage. You then have 21 calendar days to decide whether to exercise the option.

To exercise the OTP, you pay the seller the exercise fee (negotiable between S$1 and S$5,000, less the option fee already paid). You should appoint an HDB-accredited solicitor at this point — HDB-approved conveyancing firms handle the legal transfer and ensure all conditions are met for a valid resale application. Note that the solicitor fees for an HDB resale are regulated and relatively modest compared to private residential conveyancing.

After exercising the OTP, both the buyer and the seller must each independently submit their portions of the HDB Resale Application via the HDB Resale Portal within 7 days of the OTP exercise date. The application is rejected if either party fails to submit within this window — there are no extensions. The buyer’s portion covers loan details, CPF usage, grant applications, and identity verification; the seller’s portion covers their existing loan redemption, CPF refund computation, and property condition declaration.

Steps 7–10: Valuation, Approval, and Key Collection

After both parties submit, HDB appoints an independent valuer. The valuation report is typically issued within 5–10 business days. If the agreed resale price exceeds the valuation, the difference is the COV — the buyer must pay this entirely in cash. CPF cannot cover COV. If the resale price is at or below valuation, there is no COV issue and the full price can be funded by CPF and/or loan.

HDB then reviews the application — checking buyer and seller eligibility, loan amounts, CPF usage, and grant amounts — and issues its approval in principle (also known as the Letter of Offer for HDB loans, or confirmation of grant disbursement). This review takes approximately 4–6 weeks. Once approved, HDB sets a resale completion appointment (usually 3–5 weeks later), at which both buyer and seller sign the final transfer documents, the seller’s outstanding loan is redeemed, CPF principal and accrued interest are refunded to the seller’s CPF account, and the buyer’s grants are applied to reduce the purchase price.

At completion, the buyer pays the remaining purchase price (after deducting CPF, loan, and grants), and keys are handed over. The HDB MOP clock begins on the date of resale completion, not the date of OTP or application.

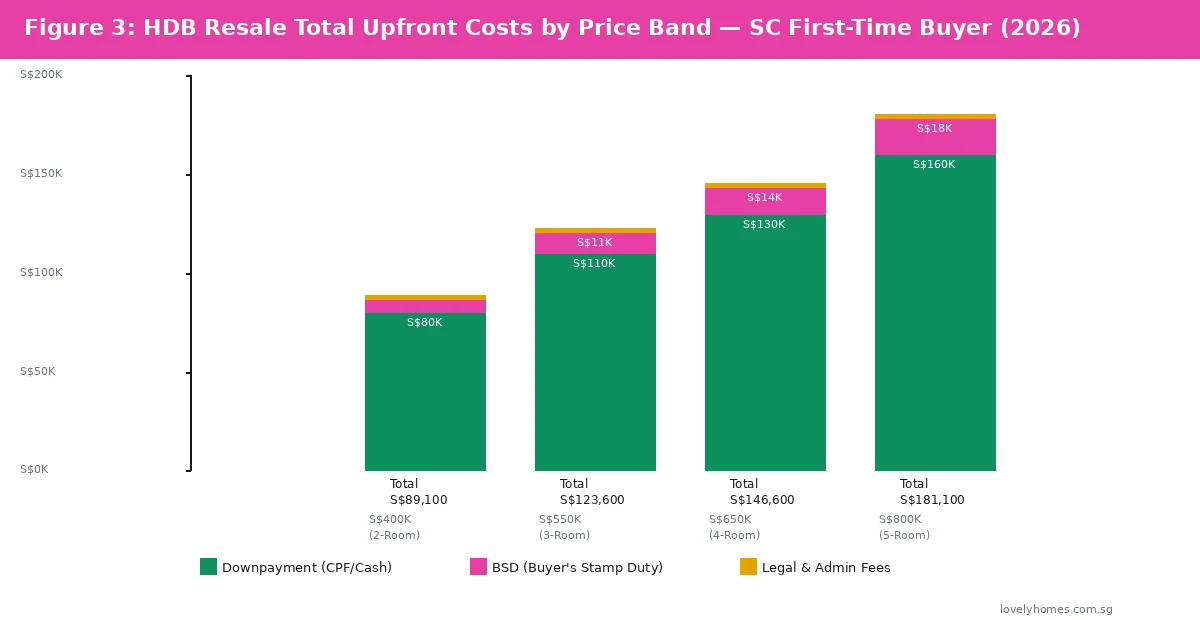

Worked Example: The Tan Family Buying a 4-Room Resale in Tampines

Mr and Mrs Tan are both Singapore Citizens, both first-timers, with a combined gross monthly income of S$7,200. They wish to buy a 4-room resale flat in Tampines. They identify a unit at S$650,000 — the HDB valuation comes in at S$630,000, meaning COV of S$20,000 in cash.

Grants: EHG: household income S$7,200 → approximately S$45,000. Family Grant (SC couple, 4-room resale): S$80,000. PHG (buying in same town as Mrs Tan’s parents): S$30,000. Total grants: S$155,000.

Financing: HDB Loan (at valuation S$630,000); HDB Loan LTV 80% = S$504,000. Monthly repayment at HDB concessionary rate 2.60% p.a. over 25 years: approximately S$2,287/month. MSR check: S$2,287 / S$7,200 = 31.8% — slightly above the 30% MSR. The loan tenure would need to be extended to 27 years to reduce the monthly payment to S$2,147 (29.8%, within MSR).

Cash required: 20% downpayment on S$630,000 = S$126,000 (CPF/cash); COV S$20,000 cash; BSD on S$650,000: first S$180K × 1% + next S$180K × 2% + balance S$290K × 3% = S$1,800 + S$3,600 + S$8,700 = S$14,100 BSD (payable from CPF); Legal fees ~S$2,500. After grants of S$155,000 applied to purchase price, effective loan reduces further. Total cash required on completion day: approximately S$20,000 COV + S$2,500 legal = S$22,500 cash. The downpayment and BSD can be funded entirely from CPF OA.

HDB Resale Buying Process: Summary Checklist

| Step | Action | Key Deadline | Portal / Body |

|---|---|---|---|

| 1 | Confirm eligibility (MOP, citizenship, WOP) | Before everything else | HDB / self-check |

| 2 | Apply for HFE Letter | ~2–3 weeks processing | homes.hdb.gov.sg |

| 3 | Search, view flats, check RPI and COV | HFE valid 6 months | resale.hdb.gov.sg / portals |

| 4 | Receive OTP from seller; pay option fee | OTP valid 21 days | HDB standard form |

| 5 | Exercise OTP; appoint solicitor | Within 21 days of OTP | HDB-accredited law firm |

| 6 | Both parties submit Resale Application | Within 7 days of OTP exercise | resale.hdb.gov.sg |

| 7 | HDB valuation issued | ~5–10 business days | HDB-appointed valuer |

| 8 | HDB resale approval | ~4–6 weeks | HDB |

| 9 | Completion appointment: sign & pay | ~3–5 weeks after approval | HDB Hub / solicitor |

| 10 | Key collection; MOP clock starts | Completion date | HDB |

Why the HFE Letter Changed the Process

Before May 2023, buyers had to separately apply for an HDB Loan Eligibility (HLE) letter (for loan quantum) and individually check grant eligibility through the CPF Board. These were separate processes with separate documentation requirements. The HFE Letter consolidated all three determinations — eligibility to buy, loan quantum, and grant amounts — into a single application with Myinfo integration that pre-populates most fields from government databases. This has reduced the administrative burden significantly and means that by the time a buyer reaches Step 3 (searching for a flat), they already have a comprehensive view of their purchasing power.

The practical implication is that the HFE Letter has become the de facto pre-qualification document for HDB resale transactions. Sellers and their agents increasingly request to see it before entertaining an offer — much like how banks request an IPA before accepting a purchase offer in private transactions. Buyers who have not yet obtained their HFE Letter are at a disadvantage in competitive situations.

What Might Change: HDB Resale in 2H 2026

This section is analytical and speculative; it does not represent government policy.

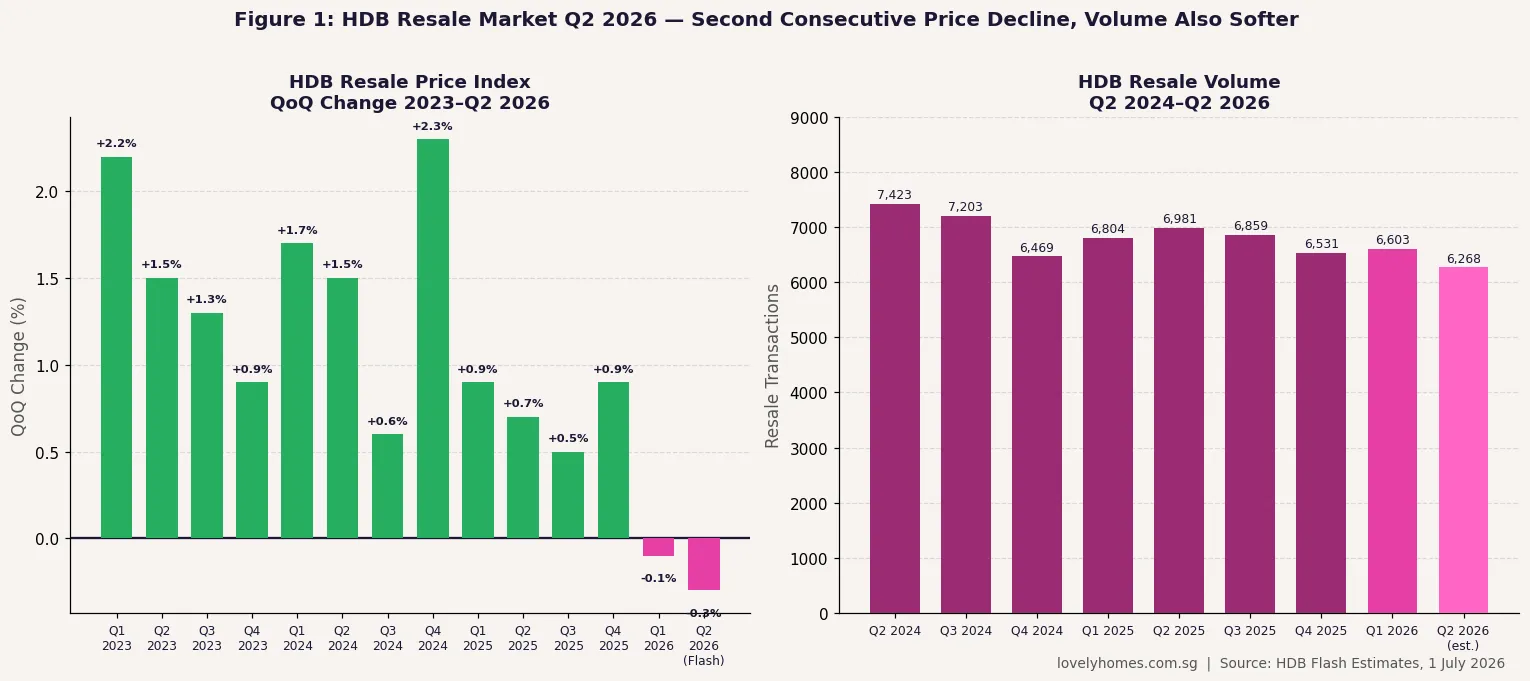

HDB resale prices fell by 0.3% in Q2 2026 — the second consecutive quarterly decline. Volumes were also down approximately 10% year-on-year. The moderation has been attributed to a combination of the 15-month wait-out period (removing a significant pool of upgrader demand), the large cohort of BTO completions in 2025–2026, and higher mortgage rates. If the moderation continues through 2H 2026, there may be political pressure to consider relaxations such as easing the wait-out period for specific buyer segments or adjusting the EC income ceiling to divert some demand from the resale market. These are speculative — HDB has not signalled any imminent changes. Full Q2 2026 resale transaction data is expected from HDB around 23 July 2026.

Frequently Asked Questions

Do I need to sell my current HDB flat before buying a resale?

You cannot own two HDB flats simultaneously (with limited exceptions for concurrent subletting). If you own an HDB flat and wish to buy a resale flat, you must either sell the existing flat within 6 months of the new resale completion, or ensure the existing flat’s MOP has been met and proceed under HDB’s approved conditions. Singapore Citizens who own a private property and wish to buy an HDB resale must also comply with the 15-month wait-out period from the date of disposing of the private property.

What is Cash-Over-Valuation (COV) and how much should I budget?

COV is the difference between the agreed resale price and HDB’s valuation of the flat. It must be paid entirely in cash — it cannot be covered by CPF, grants, or loans. As at mid-2026, COV in mature estates such as Tampines, Bishan, and Toa Payoh typically ranges from S$20,000 to S$80,000 for 4-room and 5-room flats, with premium units (high floors, well-maintained, near MRT) attracting COV at the upper end or beyond. In non-mature estates, COV is generally lower or even nil. Budget at least S$20,000–S$40,000 in liquid cash specifically for potential COV when considering a mature estate purchase.

Can I use CPF to pay BSD for an HDB resale flat?

Yes. Buyer’s Stamp Duty for an HDB resale flat can be paid from your CPF Ordinary Account. The BSD is assessed on the higher of the purchase price or valuation. For a flat priced at S$650,000 (with valuation at S$630,000), BSD is assessed on S$650,000: 1% on first S$180,000 + 2% on next S$180,000 + 3% on balance S$290,000 = S$14,100. This amount can be deducted from your CPF OA balance and paid directly to IRAS by your conveyancing solicitor. Note that Additional BSD (ABSD) does not apply to most HDB resale purchases by first-time buyers.

My HFE Letter has expired. Can I still exercise the OTP?

No — a valid HFE Letter is required at the point of submitting the HDB Resale Application (Step 6). If your HFE Letter expires before you submit the application, you will need to apply for a fresh one. The HFE Letter is valid for 6 months from the date of issue. Given that the HDB resale process from HFE application to key collection can take 3–6 months in total, it is best to time your HFE application so it remains valid through to at least the expected date of resale application submission. If you expect to search for a flat for several months, consider applying for the HFE Letter approximately 2–3 months before you plan to make serious offers.

Is a property agent required to buy an HDB resale flat?

No. HDB’s resale portal (resale.hdb.gov.sg) is designed to allow buyers and sellers to transact directly without agents. HDB provides standard OTP forms, step-by-step guided submissions, and appointment scheduling through the portal. That said, many buyers choose to engage a licensed property agent for negotiation support, flat search assistance, and procedural guidance — particularly first-timers unfamiliar with the process. If you engage an agent, ensure they hold a valid CEA practitioner licence. Agent commission for a buyer is negotiable; it is often 1% of the purchase price, sometimes waived or subsidised by the co-broking arrangement with the seller’s agent.

What happens if I back out after exercising the OTP?

Once you exercise the OTP, you are legally bound to complete the purchase on the agreed terms. If you withdraw after exercising, the seller is entitled to forfeit your option and exercise fees and may seek further damages depending on the circumstances. Unlike private residential transactions (which involve a more complex contractual structure under the Sale and Purchase Agreement), HDB resale OTPs are relatively straightforward — but the principle of contractual commitment applies equally. If you are genuinely uncertain about proceeding, it is better to let the OTP lapse (forfeiting only the option fee of up to S$1,000) rather than exercise it and then withdraw.

Related Articles

- Singapore HDB CPF Housing Grants Guide 2026: EHG, Family Grant, PHG and Every Dollar You Can Claim

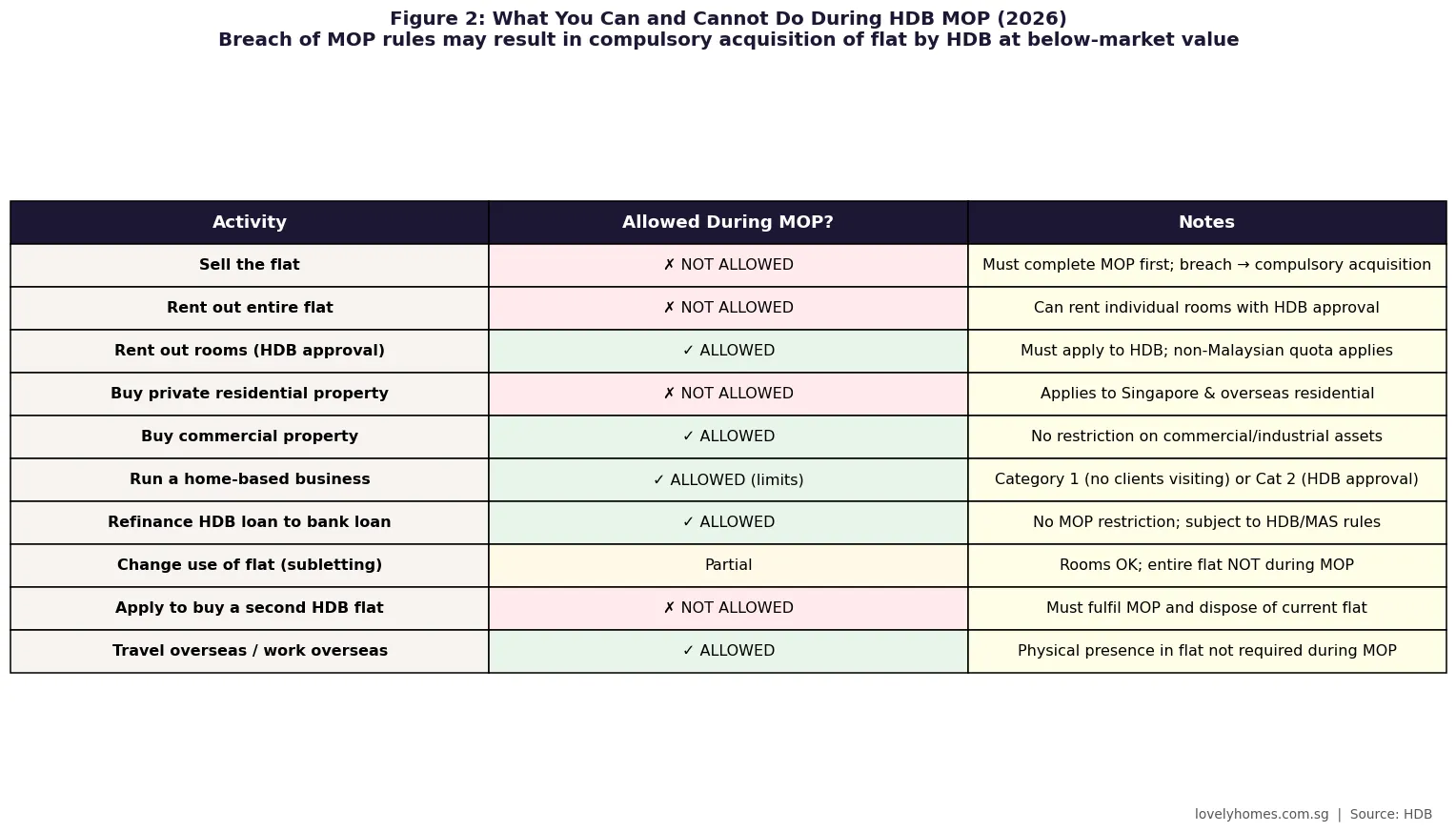

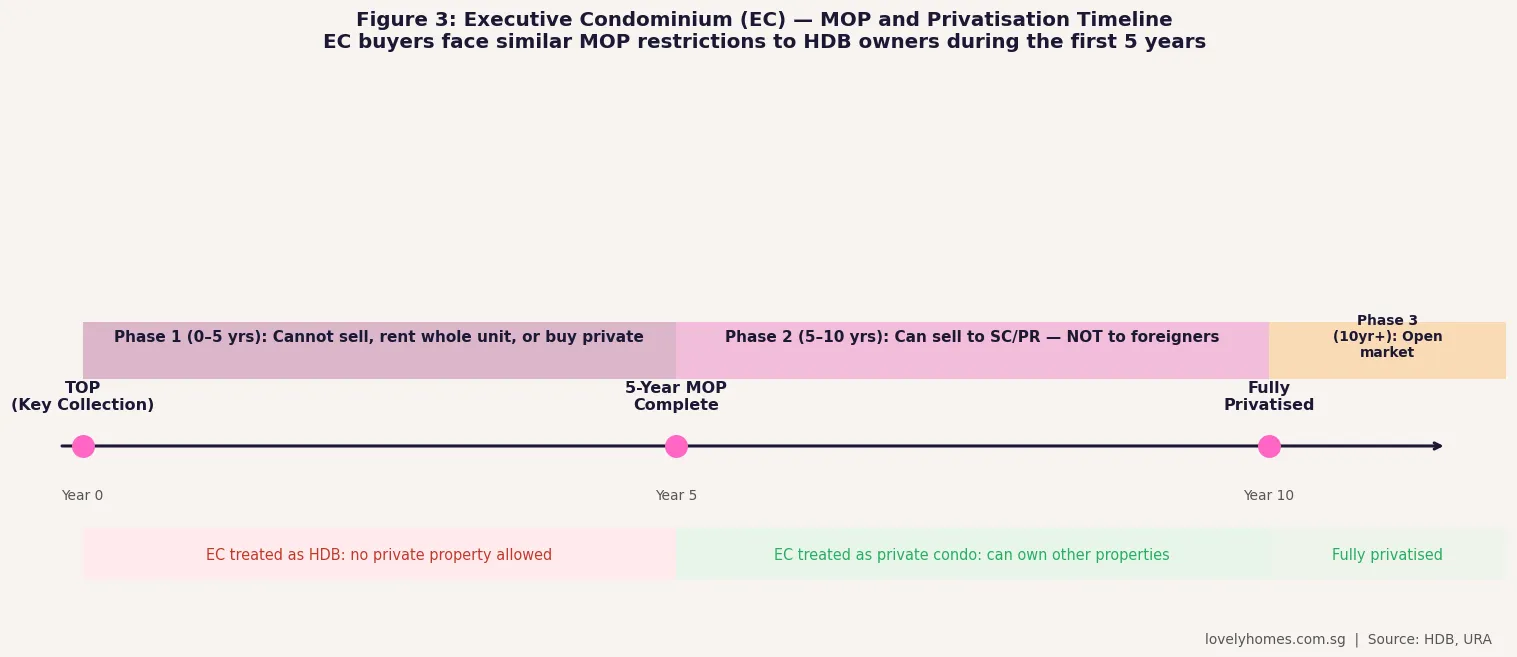

- Singapore HDB Minimum Occupation Period (MOP) 2026: Complete Guide

- Singapore First-Timer Home Buyer Complete Guide 2026

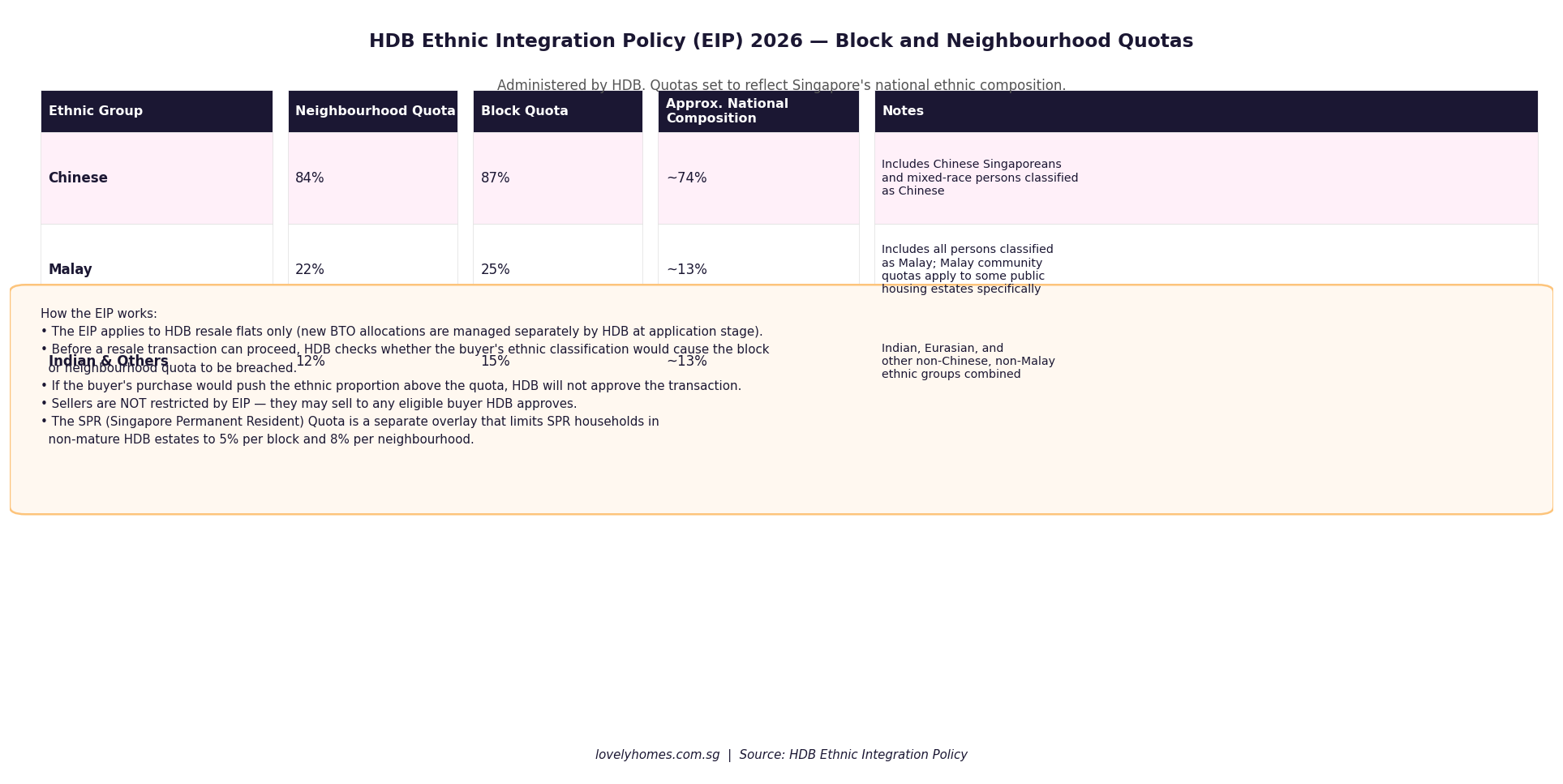

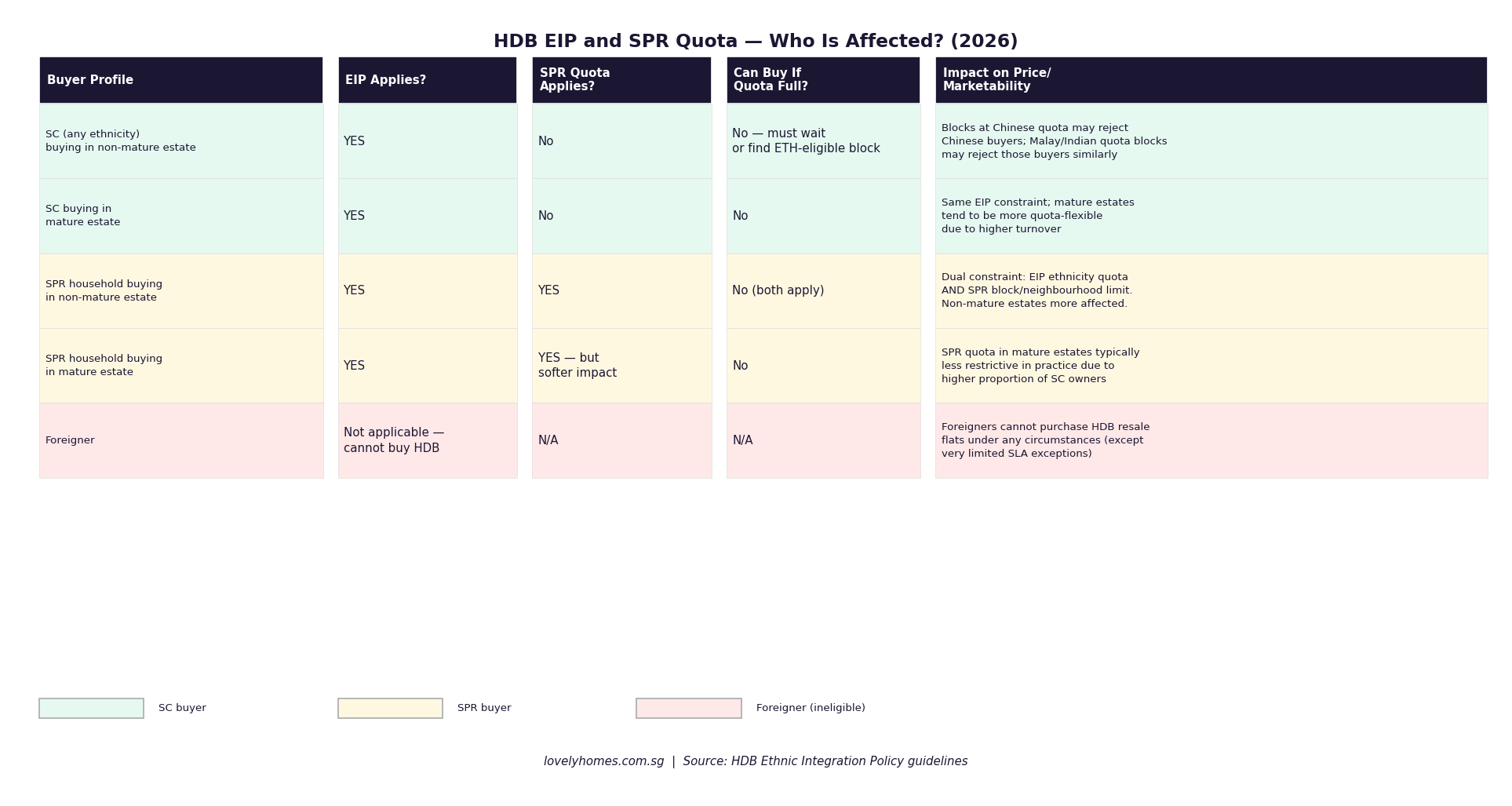

- HDB Ethnic Integration Policy (EIP) 2026: Quotas, SPR Limits and How It Affects Your Purchase

- Singapore HDB Downpayment Guide 2026: How Much Cash Do You Need?

- Singapore Property Cooling Measures 2026: Complete Guide to ABSD, TDSR, LTV and SSD

Disclaimer

This article is for general informational purposes and does not constitute legal, financial, or professional advice. HDB eligibility rules, CPF grant amounts, loan limits, and stamp duty rates are subject to change. All figures cited are accurate as at 3 July 2026. Readers should verify current rules with HDB (hdb.gov.sg), IRAS (iras.gov.sg), MAS (mas.gov.sg), and the CPF Board (cpf.gov.sg) before making any decisions. LovelyHomes is not a licensed property agent, financial adviser, or legal practitioner.