En Bloc Sale Singapore 2026: Complete Guide to Collective Sales, Your Payout and What Owners Need to Know

An en bloc sale — formally called a collective sale under the Land Titles (Strata) Act — is when the majority of owners in a strata development vote to sell the entire site to a single developer, usually at a significant premium over individual unit values. For owners, it can be a life-changing windfall. For developers, it is the primary route to assembling large, contiguous sites in an already built-up city. For the wider market, collective sale cycles signal sentiment at the top of property bull runs. This guide covers every aspect of the en bloc process in Singapore for 2026: the legal framework, the 80% consent threshold, how your payout is calculated, and the tax and CPF implications you must understand before voting.

Quick Answer — En Bloc Sale: 10 Key Points

- An en bloc sale requires 80% consent by share value and strata area for developments over 10 years old; 90% for those aged 10 years or under.

- A Collective Sale Committee (CSC) is elected at an Extraordinary General Meeting (EOGM) before any sale process can begin.

- The CSC must appoint a marketing agent and a lawyer, set a reserve price, and obtain the consent signatures within a 12-month window.

- Minority dissenting owners can be compelled to sell once 80%/90% consent is achieved and the Strata Titles Board (STB) approves the sale.

- Seller’s Stamp Duty (SSD) does not apply to en bloc sales — they are exempt under the Land Titles (Strata) Act provisions.

- Payout is apportioned by share value and strata area per the Sales & Purchase Agreement methodology — not simply unit count.

- CPF principal and accrued interest must be refunded from your payout — as with any residential property sale.

- Any profit above your original purchase price is not subject to capital gains tax in Singapore, but IRAS may assess income tax if trading intent is inferred.

- The typical timeline from CSC formation to completion is 18 to 30 months.

- En bloc activity peaks in property bull markets — Singapore’s last major cycle was 2017–2018, with approximately S$9 billion in deals in 2018 alone.

What Is an En Bloc Sale and Who Governs It?

The en bloc (collective sale) mechanism is governed by Part VA of the Land Titles (Strata) Act (LTSA), administered by the Singapore Land Authority (SLA). The Strata Titles Board (STB), a specialist tribunal under the Ministry of Law, handles disputes and formal approvals when dissenting owners challenge a sale. The Urban Redevelopment Authority (URA) tracks collective sale applications as part of its monitoring of land supply and development pipeline.

The policy rationale for en bloc sales is Singapore-specific: as a city-state with finite land, older low-density developments can unlock significant value through redevelopment at higher plot ratios permitted under the URA Master Plan. A 1980s condominium of 80 units on a 10,000 sqm site might be replaced by a 300-unit development under current planning norms — making the collective value of a developer acquisition substantially greater than the sum of individual units.

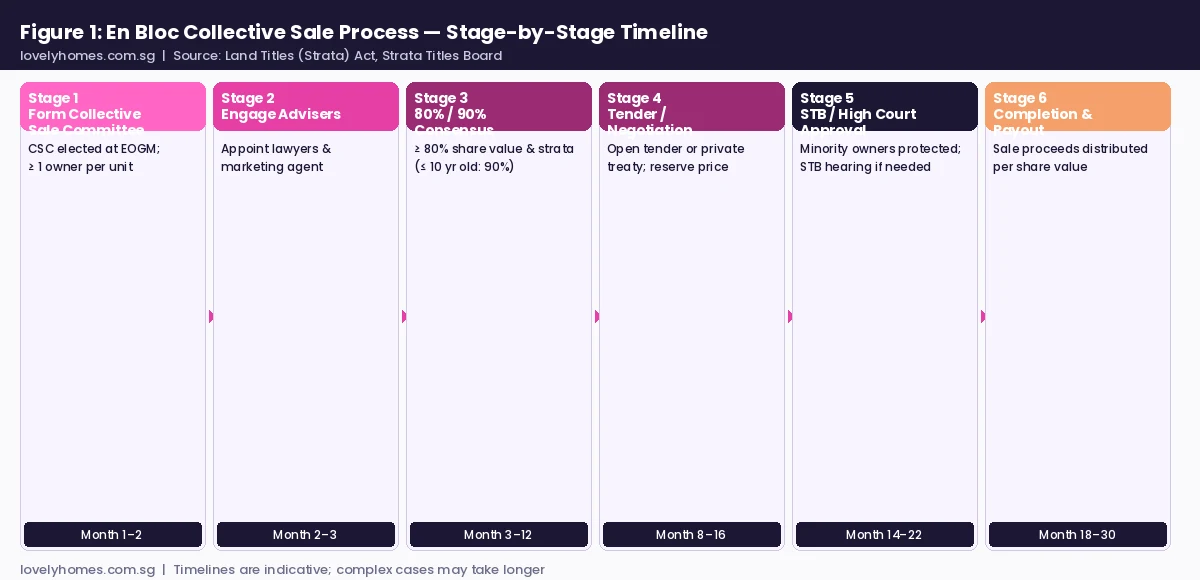

The Six Stages of an En Bloc Sale

Understanding the procedural sequence is essential, whether you are a potential supporter or a dissenting owner. The process is tightly regulated to protect minority rights while enabling the majority to realise the development potential of their land.

Stage 1 — Forming the Collective Sale Committee: Any owner may propose an en bloc sale at an EOGM convened under the LTSA. If the resolution passes, a Collective Sale Committee of at least 3 (and typically 5–12) elected owner-representatives is constituted. The CSC is a fiduciary body — its members must act in the collective interest and maintain records of all deliberations.

Stage 2 — Engaging Professional Advisers: The CSC appoints a licensed real estate marketing agent (to conduct the tender or private treaty negotiation) and a law firm experienced in collective sales. A professional valuer must provide an independent valuation of the site — a key input for setting the reserve price. These appointments require approval from the general body of owners at a general meeting.

Stage 3 — Achieving 80% or 90% Consent: This is typically the longest and most contentious phase. Owners sign a Collective Sale Agreement (CSA) — a legally binding contract — setting out the reserve price, the apportionment methodology, and their agreement to proceed. The consent threshold is 80% by share value and 80% by strata area for developments over 10 years old, rising to 90% for younger developments. The CSC has 12 months from the first signature to collect the required percentage.

Stage 4 — Tender or Private Treaty: Once the threshold is met, the CSC launches a public tender or negotiates privately. Developers submit bids; the CSC and its agent evaluate offers against the reserve price and qualitative criteria (developer track record, conditions precedent). The preferred bid goes to a general meeting for ratification.

Stage 5 — Strata Titles Board / High Court Approval: If all owners agree, a private sale can proceed directly to the High Court for sanction. Where there are dissenters, the CSC files an application with the STB. The STB adjudicates whether the sale is in good faith (price is fair, minority interests are not unduly prejudiced) and may order the sale over objections. Complex or challenged cases escalate to the High Court.

Stage 6 — Completion and Payout: On completion of the sale (typically 6 to 12 months after signing the S&P Agreement), each owner receives their allocated share of the net proceeds, with CPF refunds and outstanding mortgage settled by the conveyancing lawyers before the cash balance is disbursed.

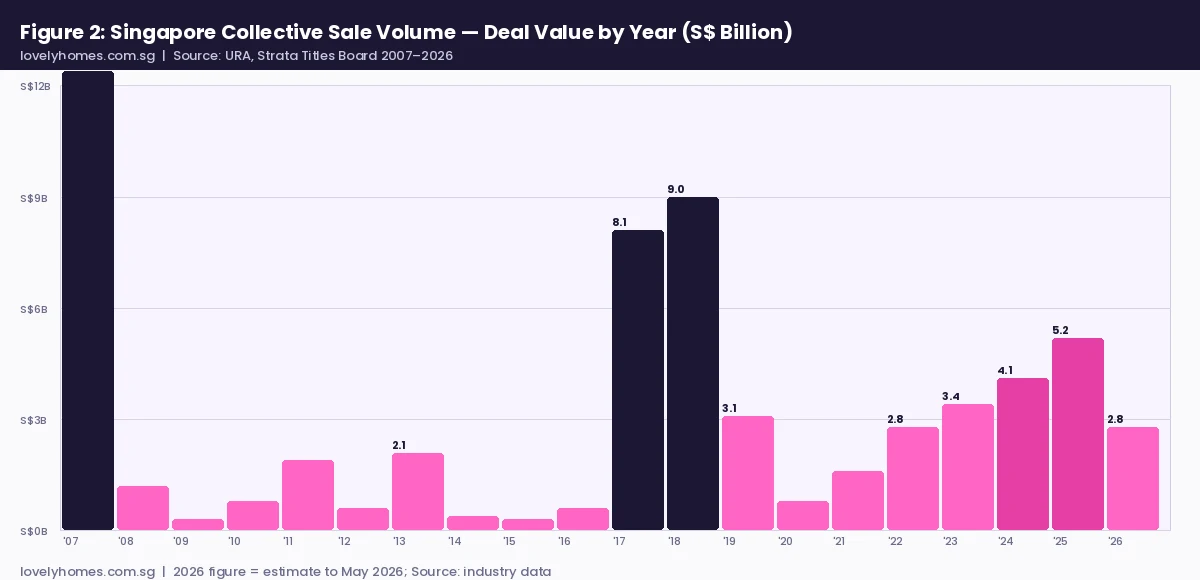

Historical En Bloc Volume in Singapore

Singapore has experienced two major en bloc cycles since 2000. The first peaked in 2007 with approximately S$12.4 billion in collective sale transactions, driven by the pre-GFC property boom. The second — and larger by deal count — ran from 2017 to 2019, peaking at S$9.0 billion in 2018 before the government tightened developer remission ABSD conditions in July 2018, which effectively halted the cycle. Activity has been rebuilding since 2022, and 2025 saw an estimated S$5.2 billion in collective sale transactions as developers sought land replenishment amid a tight GLS supply environment.

How Your Payout Is Calculated

The apportionment of sale proceeds is set out in the Collective Sale Agreement and must be approved at a general meeting before the consent exercise begins. Two broad methodologies are used: share value apportionment, which allocates proceeds in proportion to each unit’s share value as registered under the strata title, and strata area apportionment, which allocates by floor area. Hybrid methodologies combining both are also used. In practice, large unit holders (penthouses, commercial units) and small unit holders may disagree strongly over methodology — this is one of the most contentious aspects of the early CSC deliberations.

Summary — Key Legal Requirements

| Item | Requirement | Governed by |

|---|---|---|

| Consent threshold (dev > 10 yr) | 80% share value + 80% strata area | LTSA s.84A |

| Consent threshold (dev ≤ 10 yr) | 90% share value + 90% strata area | LTSA s.84A |

| Consent collection window | 12 months from first signature | LTSA s.84A(4) |

| STB filing deadline | Within 12 months of first signature | LTSA s.84A(2) |

| SSD applicability | Exempt for qualifying en bloc sales | LTSA / IRAS |

| Capital gains tax | Not applicable in Singapore | IRAS (income tax may apply if trading intent) |

| CPF refund | Principal + accrued interest (2.5% p.a.) | CPF Board |

Worked Example: The Rivervale Court Collective Sale

Consider a hypothetical 80-unit development — call it Rivervale Court — with a collective sale price of S$180 million agreed in 2026. Each unit has an identical 1/80th share value under the strata title. Here is how the payout flows from the gross sale price to the individual owner’s net cash in hand.

After deducting agent fees (0.5%), legal and miscellaneous costs (0.3%), and distributing 1/80th of the net proceeds to this particular owner, their gross entitlement is S$2,232,000. They then settle an outstanding mortgage of S$480,000, refund CPF principal plus accrued interest totalling S$162,000, and pay no SSD (held 7 years, and en bloc is SSD-exempt). Their net cash in hand is approximately S$1,590,000 — representing a 77% premium over their original S$900,000 purchase price in 2019. This illustrates why en bloc sales, when they succeed, can be genuinely transformative for long-hold owners.

What This Means for Owners: Supporter vs Dissenter

If you are a supporter of an en bloc sale, your primary responsibilities are to ensure the CSC is well-organised, the marketing agent is reputable, and the reserve price reflects genuine market value. Be alert to any conflict of interest from CSC members who are also agents or advisers. Review the apportionment methodology carefully before signing — once you sign the CSA, you are bound to proceed.

If you are a dissenter, understand that your right to object is not absolute once the threshold is met. The STB will assess whether the transaction price is fair and whether good faith procedures were followed. Valid grounds for objection include: the sale price being below the independent valuation, procedural irregularities in the consent exercise, or evidence of bad faith by the CSC. Engaging a lawyer early is advisable if you intend to resist. STB proceedings can add 6 to 12 months to the timeline, but rarely prevent a properly run collective sale from proceeding.

What Might Come Next for En Bloc Activity

En bloc activity in 2026 is constrained by the same headwinds that have limited broader private residential development: elevated development charges on certain use zones, higher construction costs, and developers’ inventory of unsold units from 2023–2024 launches. That said, several districts — notably D15 (East Coast), D19 (Serangoon), and D21 (Clementi/West Coast) — have ageing leasehold stock that is approaching the 30-to-40-year mark, making these areas prime candidates for the next cycle. The government’s decision to maintain a relatively tight GLS Confirmed List in 1H 2026 (9 sites) also increases developers’ appetite for alternative land-banking routes, including collective sales. Industry observers expect the next peak of en bloc activity to emerge between 2027 and 2029 if interest rates continue their downward path and developer sentiment strengthens.

Frequently Asked Questions

Can I be forced to sell my flat in an en bloc?

Yes, once the 80% (or 90%) consent threshold is met and the Strata Titles Board approves the application, all owners — including dissenters — are compelled to sell. This is the core feature of the en bloc mechanism and is explicitly authorised by the Land Titles (Strata) Act. Dissenters retain the right to object to the STB on grounds of good faith, but if the STB or High Court approves the sale, the legal obligation to transfer title is binding on all owners regardless of individual preference.

Is the profit from an en bloc sale taxable?

Singapore does not levy capital gains tax, so the profit from selling your home — including via an en bloc — is generally not taxable. However, IRAS (Inland Revenue Authority of Singapore) applies a facts-and-circumstances test: if you frequently trade properties or if the development was purchased with clear investment intent rather than for owner-occupation, IRAS may treat gains as income subject to income tax. For most long-hold owner-occupiers, the en bloc profit is received tax-free. Seller’s Stamp Duty is also exempt for qualifying en bloc sales.

How is the reserve price determined?

The reserve price is set by the CSC based on an independent valuation from a licensed valuer, the site’s allowable Gross Floor Area under the URA Master Plan, current land values for comparable GLS or collective sale sites, and the development charge that a buyer would need to pay to maximise the plot ratio. The reserve price must be presented to owners before the consent exercise begins and can only be revised upwards (not downwards) without a fresh general meeting and a new consent exercise.

What happens if only 75% of owners agree — just below the 80% threshold?

The collective sale cannot proceed. The CSC may continue seeking signatures up until the 12-month window from the first signature expires. If the threshold is not met within 12 months, the consent exercise lapses. A fresh process — new EOGM, new CSC election, new CSA — would be required to restart. In practice, CSCs with 70–79% support often try to negotiate directly with known holdouts or offer enhanced compensation to incentivise final signatures, within the terms permitted by the LTSA.

Do I need to vacate immediately after the en bloc is approved?

No. The Sales and Purchase Agreement between the CSC and the developer sets out a completion timeline — typically 12 months after the S&P is signed, with options for extension. Owners who are occupying their units are given a defined period (often 3 to 6 months after legal completion) to vacate the property, with the specific terms set out in the CSA and the S&P Agreement. Owners who are landlords with tenants are responsible for managing their existing tenancies in the run-up to completion.

Can I buy another HDB flat after my condo is en-blocced?

Not immediately if you are using the proceeds to buy a subsidised HDB flat. HDB eligibility rules require you to dispose of any private residential property before purchasing a subsidised flat, but the timing windows are governed by HDB’s prevailing policy. If you intend to downgrade to an HDB resale flat, the eligibility criteria, ethnic integration policy, and CPF housing grant conditions all apply as normal. Consulting an HDB officer about the concurrent-ownership rules and the 15-month wait policy (if you have previously owned a private property) is strongly recommended before committing to any replacement purchase.

Related Articles

- ABSD Singapore 2026 — Complete Guide to Additional Buyer’s Stamp Duty

- CPF for Property Purchase Singapore 2026: Withdrawal Limits and Accrued Interest Explained

- Rental Yield vs Capital Gain Singapore 2026: The Property Investor’s Decision Framework

- Singapore Property Market Outlook H2 2026: Supply Wave, Rate Easing and What to Expect

- Foreigners Buying Property in Singapore 2026: ABSD, Eligibility and Full Cost Guide

- Stamp Duty Calculator Singapore 2026: BSD and ABSD for Every Buyer Type

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or property advice. En bloc sale rules are governed by the Land Titles (Strata) Act and are subject to amendment. For advice specific to your development or circumstances, consult a Singapore-qualified lawyer experienced in collective sales. Official resources: Singapore Land Authority, Strata Titles Board, IRAS.