Foreigner Buying Property in Singapore 2026: Complete Guide — ABSD, Eligible Properties and Process

Quick Answer: Can Foreigners Buy Property in Singapore?

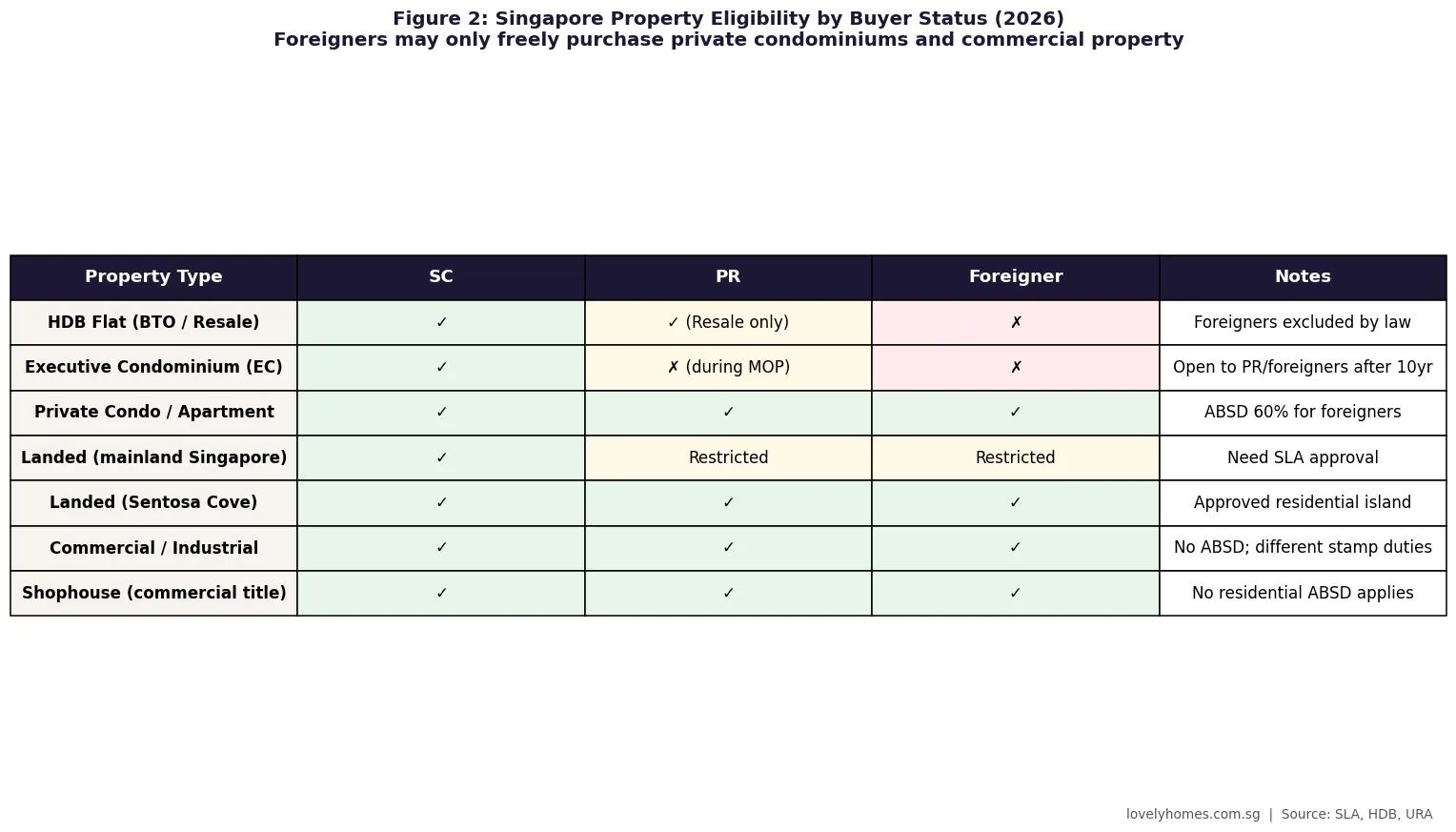

- Foreigners may freely purchase private condominiums and apartments in Singapore — there is no quota or prior approval requirement for these properties.

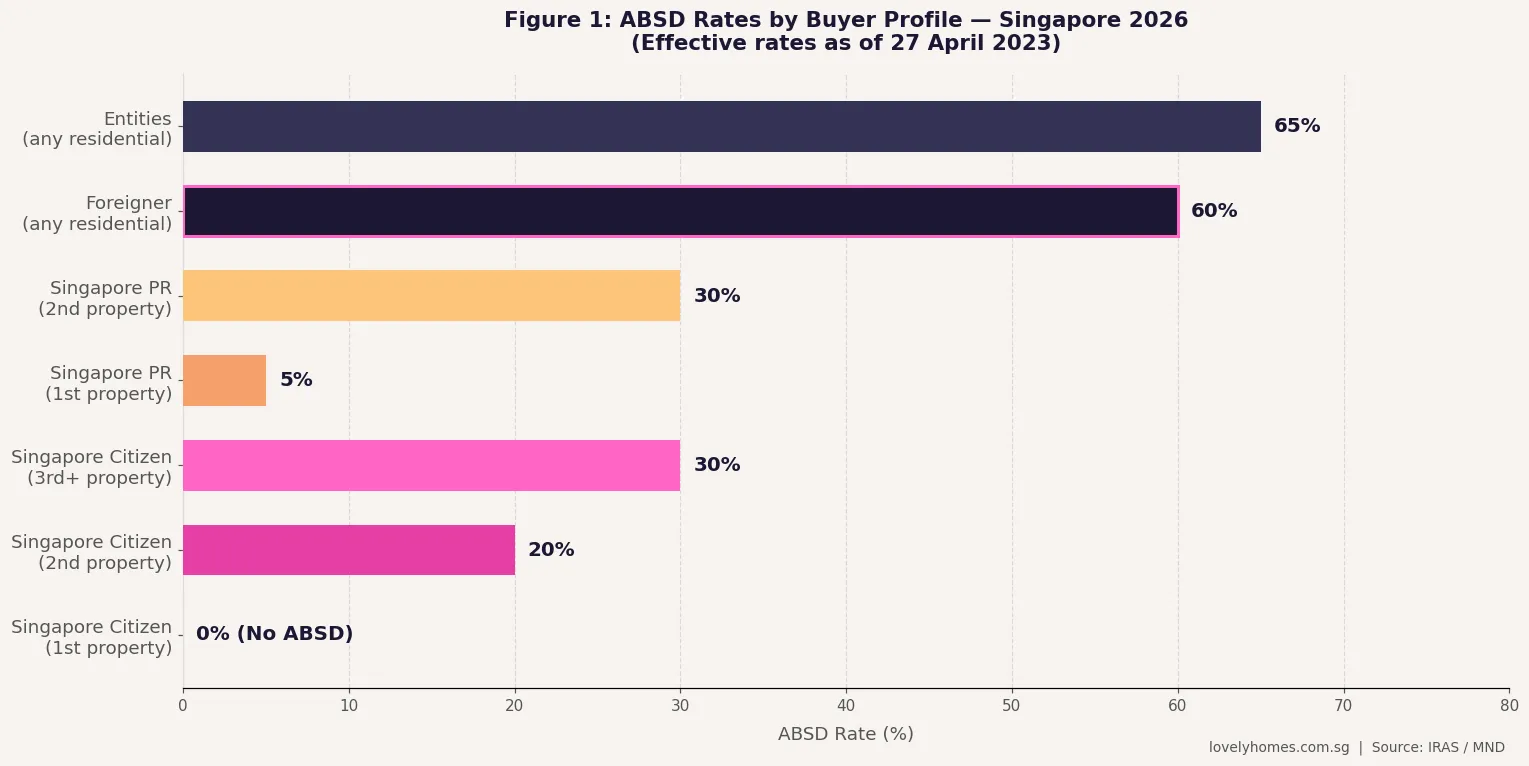

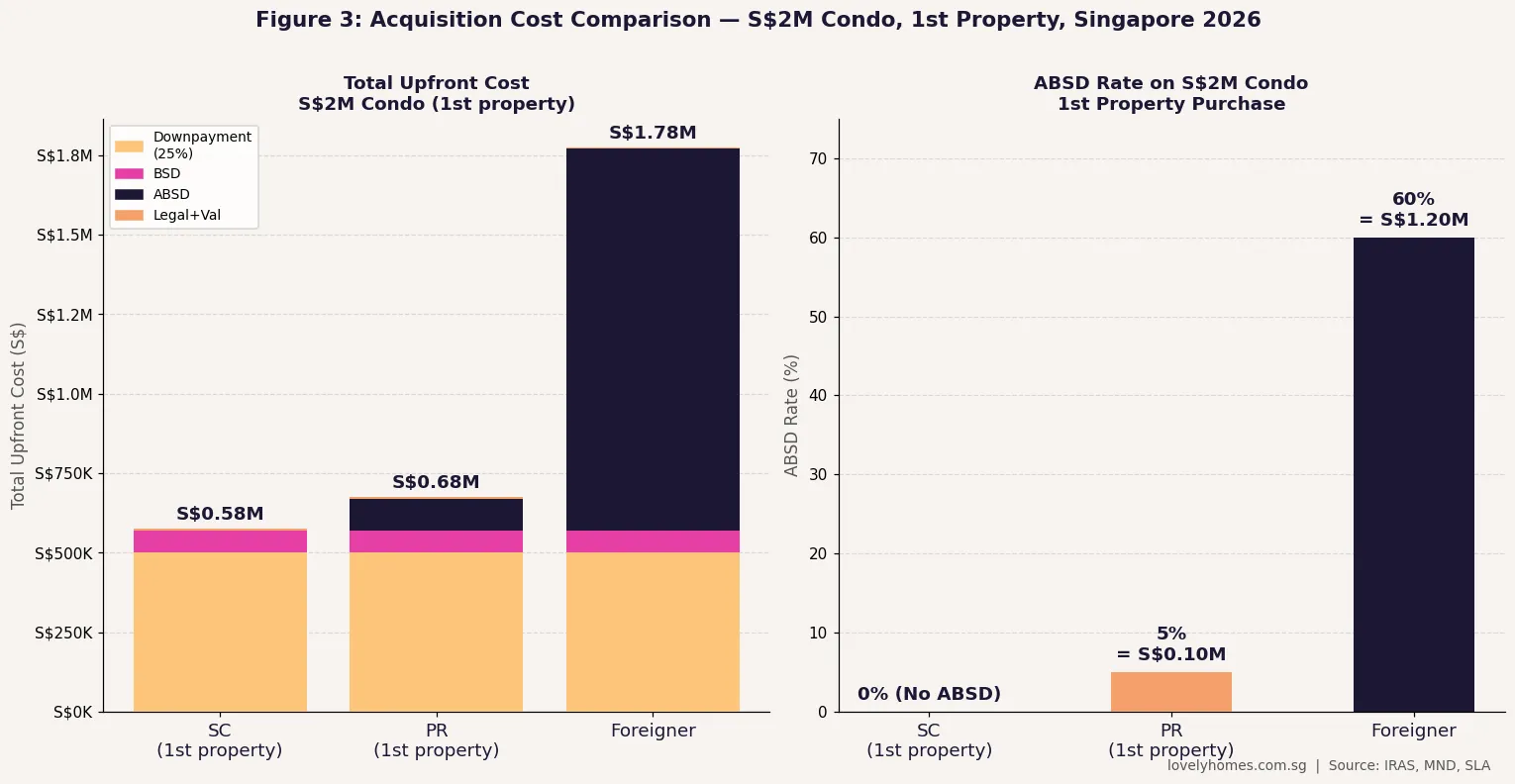

- Additional Buyer’s Stamp Duty (ABSD) of 60% applies to any foreigner buying any Singapore residential property (effective 27 April 2023).

- Foreigners cannot buy HDB flats (public housing) or Executive Condominiums during their 10-year Minimum Occupation Period.

- Foreigners cannot buy mainland Singapore landed property without Singapore Land Authority (SLA) approval; Sentosa Cove is a designated exception.

- Singapore Permanent Residents (PRs) pay 5% ABSD on their first residential property and 30% on subsequent purchases; PRs can buy HDB resale flats but not BTO flats.

- The Loan-to-Value (LTV) limit is 75% for most foreign buyers on their first property from a Singapore-regulated bank — a minimum 5% cash downpayment is required.

- BSD (Buyer’s Stamp Duty) also applies to all buyers; on a S$2M purchase BSD is approximately S$69,600 (effective 3.48%).

Foreigners Buying Property in Singapore: The Full Picture

Singapore has long attracted foreign capital into its property market, offering political stability, rule of law, transparent ownership records, and strong capital preservation. Despite the 60% ABSD surcharge introduced in April 2023, the city-state remains one of Asia’s most liquid and credible real estate markets for overseas investors.

Understanding Singapore’s property restrictions is, however, non-negotiable before committing capital. This guide explains who qualifies as a foreign buyer, what you can and cannot purchase, the full stamp duty liability, the buying process, and what due diligence steps are essential before signing an Option to Purchase (OTP).

The statutory framework governing foreign property ownership in Singapore is primarily the Residential Property Act (Chapter 274), administered by the Singapore Land Authority (SLA), and the Stamp Duties Act, administered by the Inland Revenue Authority of Singapore (IRAS).

Who Is Classified as a Foreign Buyer in Singapore?

For the purposes of Singapore property law and stamp duty, buyers are classified into three main groups:

| Buyer Type | Definition | HDB Resale? | Private Condo? | ABSD (1st Prop.) |

|---|---|---|---|---|

| Singapore Citizen (SC) | Holds Singapore citizenship | ✓ | ✓ | 0% |

| Singapore Permanent Resident (SPR/PR) | Holds Singapore PR (Blue IC) | ✓ (with quota) | ✓ | 5% |

| Foreigner | Neither SC nor PR | ✗ | ✓ | 60% |

| Entity (company/trust) | Any non-individual legal entity | ✗ | ✓ (with caveats) | 65% |

For couples where one partner is an SC and the other is a foreigner, the ABSD rate used depends on the higher-rated buyer — so an SC+foreigner couple purchasing together pays ABSD at the foreigner rate of 60% (or a remission may apply if the SC spouse is purchasing their first property — check with your solicitor). Married couples who are both SC and PR also have specific treatment and should get a stamp duty assessment before exercising an OTP.

What Can Foreigners Buy (and Not Buy) in Singapore?

The Residential Property Act places strict controls on foreign ownership of “restricted residential property”, which covers landed housing on the Singapore mainland. Non-restricted residential property (including all private condominiums and apartments in strata-titled developments) may be purchased freely by foreigners, subject to paying the applicable ABSD.

What Foreigners CAN Buy (Freely)

Private strata-titled condominiums and apartments are the primary vehicle for foreign property investment in Singapore. This includes condominiums in CCR (Core Central Region, Districts 9, 10, 11), RCR (Rest of Central Region), and OCR (Outside Central Region). Foreigners may purchase new launches from developers, resale units on the open market, and serviced apartments under residential titles.

Sentosa Cove landed property is an exception to the landed restriction. The government has designated Sentosa Cove as an approved area where foreigners may purchase bungalows, semi-detached and terrace houses. A Restricted Residential Property Approval is still processed through SLA, but approval is generally granted for bona fide purchasers. Sentosa Cove units attract a Land Betterment Charge (LBC) alongside normal stamp duties.

Commercial and industrial property — shophouses, office units, retail strata units, industrial buildings, and similar non-residential assets — may be purchased by foreigners without ABSD (though BSD and other charges apply). Many investors access Singapore property through shophouses and commercial strata units precisely to avoid the residential ABSD.

What Foreigners CANNOT Buy (Without Approval)

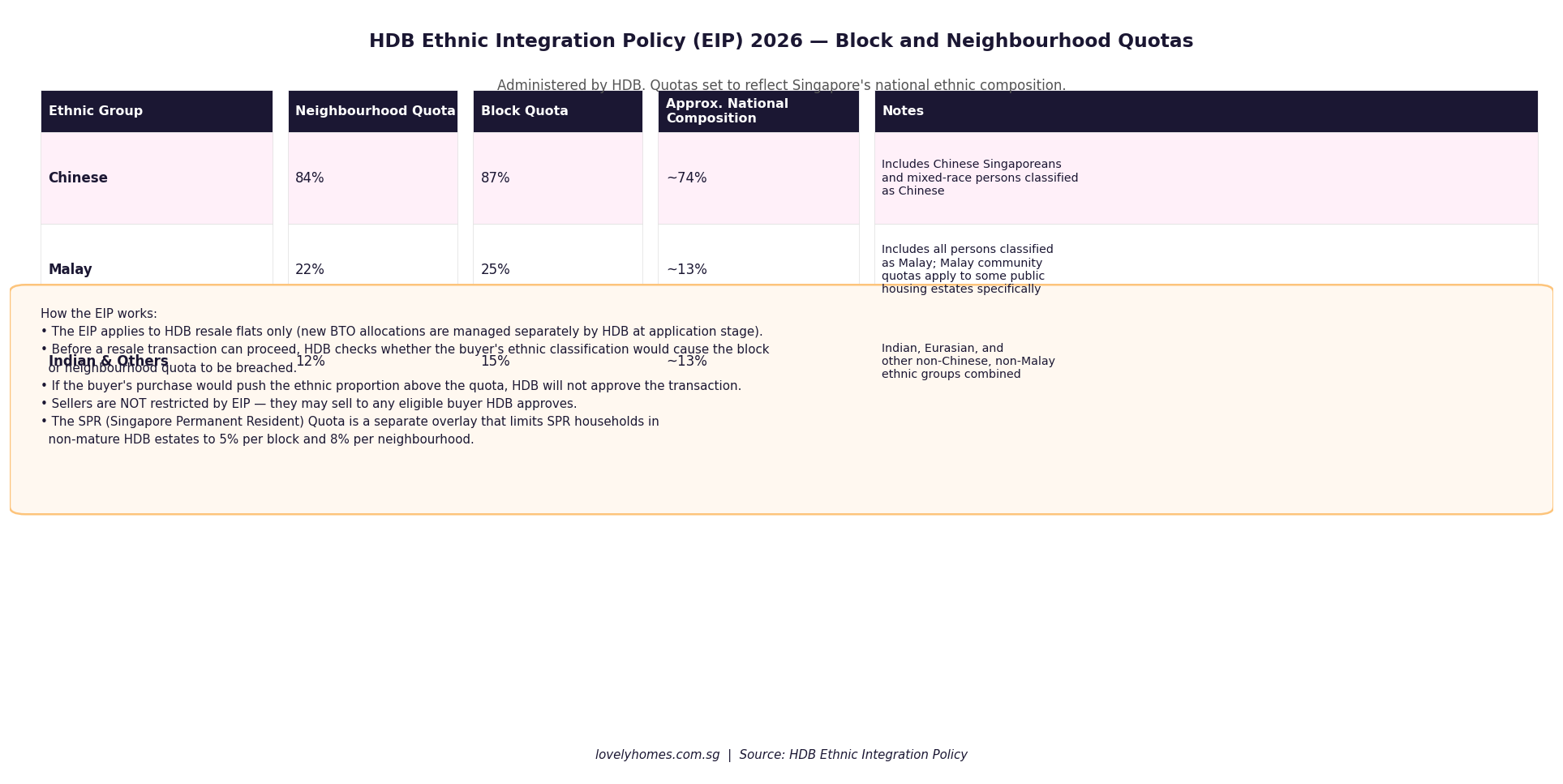

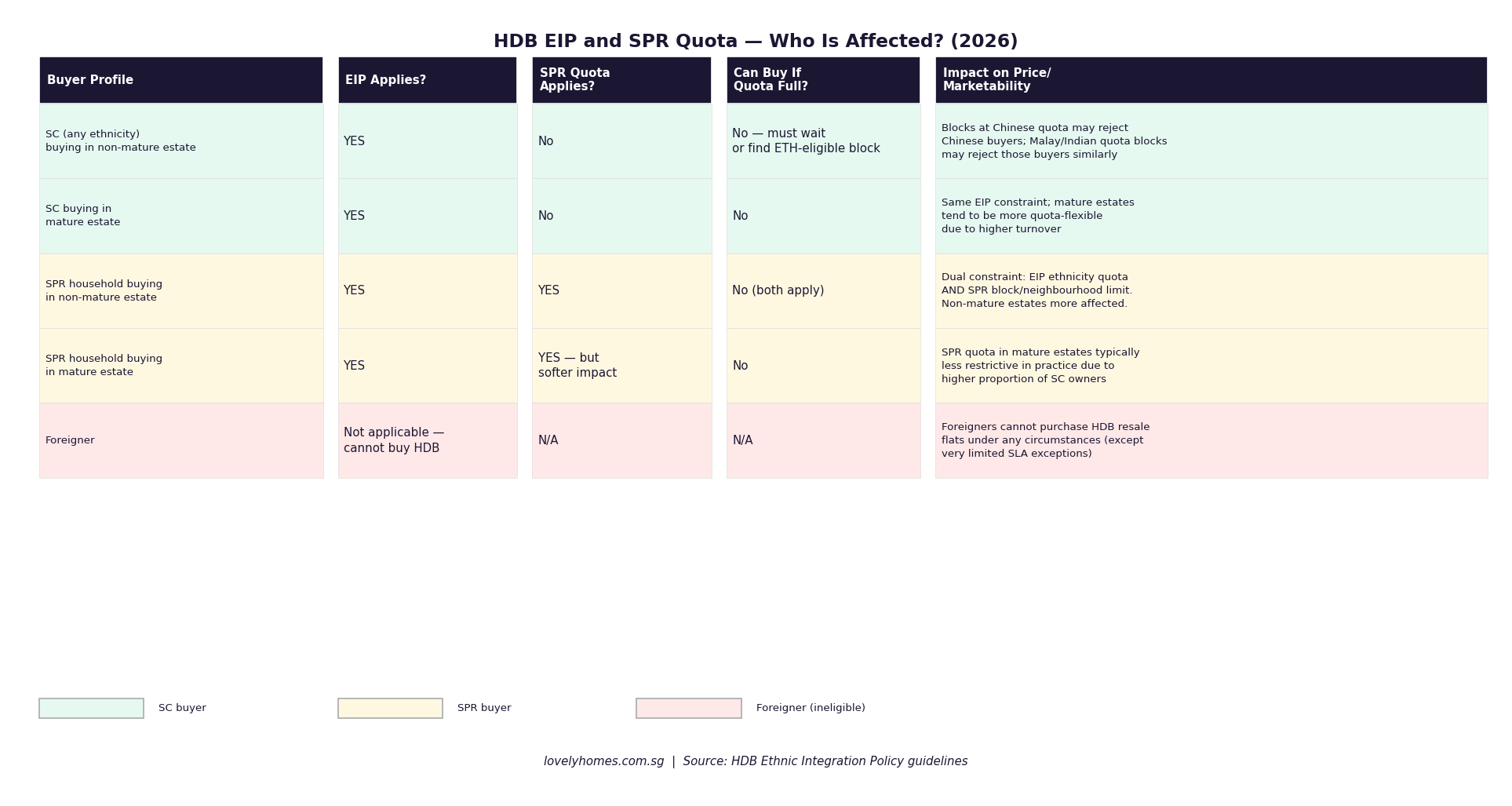

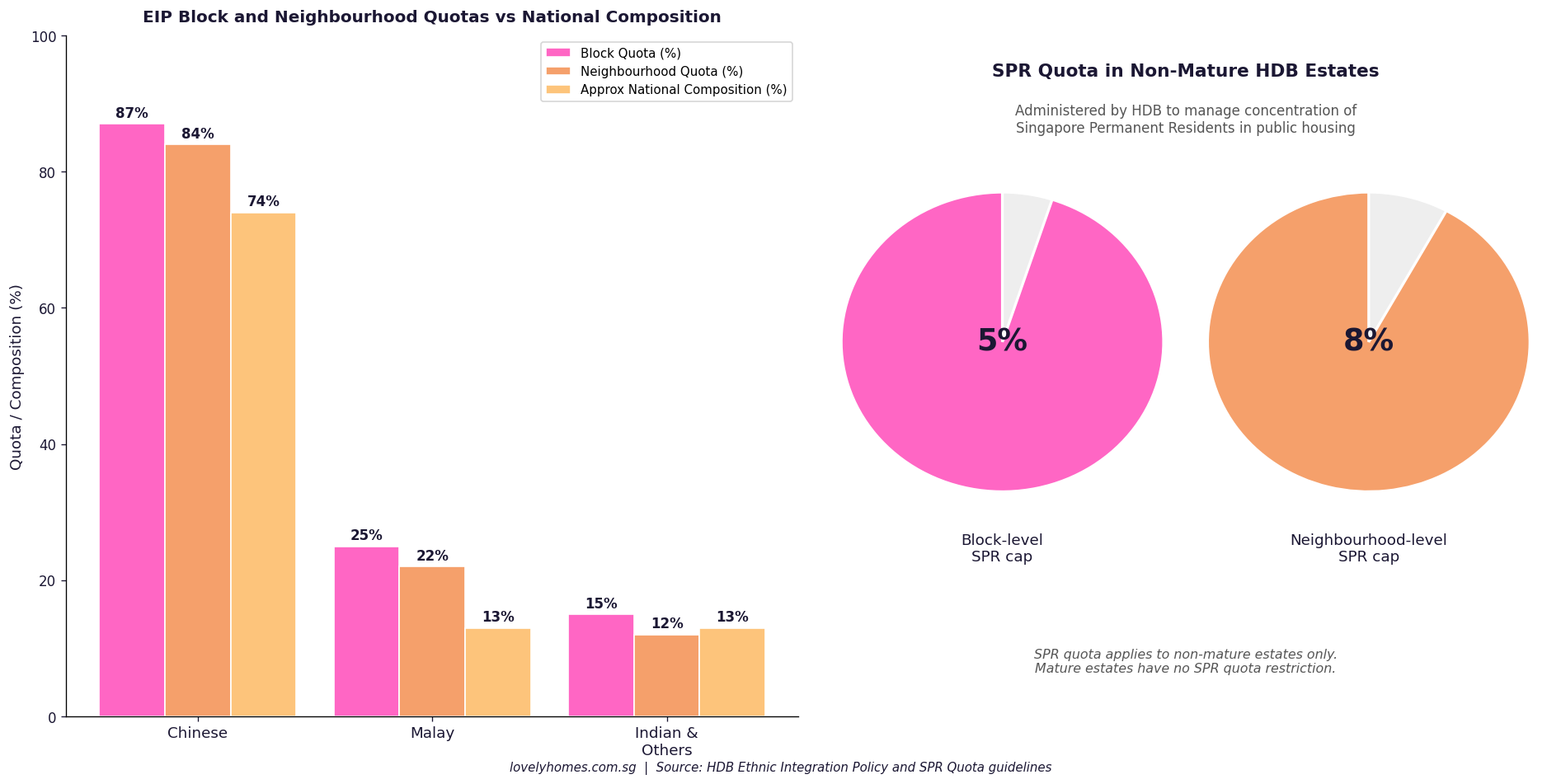

HDB flats (all types: BTO, resale, DBSS) are restricted to Singapore Citizens and Permanent Residents, and even PRs face sub-quotas under the Ethnic Integration Policy. Foreigners have no pathway to HDB ownership.

Executive Condominiums (ECs) are hybrid public-private housing. During the first 10 years (from TOP), ECs cannot be sold to foreigners. After 10 years, ECs are fully privatised and foreigners may purchase them, but ABSD at 60% applies.

Mainland Singapore landed residential property — including detached houses, semi-detached houses, terrace houses, and cluster housing — requires prior SLA approval. In practice, the SLA rarely approves applications from foreigners without substantive economic contribution to Singapore (e.g., Global Investor Programme). Applications that are approved often involve conditions and lengthy processing times.

Additional Buyer’s Stamp Duty (ABSD): The 60% Reality

The 60% ABSD rate for foreigners, introduced on 27 April 2023 under the Stamp Duties (Amendment) Act, doubled the previous rate of 30%. It is assessed on the higher of the purchase price or the market value of the property, and must be paid within 14 days of the exercise of the OTP (or within 30 days for documents executed overseas).

ABSD is administered by the Inland Revenue Authority of Singapore (IRAS). Penalties for late payment are 5% of the ABSD due per annum, and IRAS does not grant extensions except in extraordinary circumstances. Importantly, ABSD cannot be financed through a bank loan — it must be paid entirely in cash from the buyer’s own funds. On a S$2M purchase, that is S$1.2M in cash for ABSD alone, payable within two weeks of exercising the OTP.

For Singapore Permanent Residents, the ABSD rate on a first residential property is 5% (S$100,000 on a S$2M purchase) and 30% on any subsequent residential property. PRs who hold a joint purchase with an SC spouse buying their first property may apply for an ABSD remission to reduce the effective ABSD to 0% — this requires both parties to be first-time residential property owners.

ABSD remission schemes exist for certain qualifying situations: developers remission (for licensed developers undertaking development), housing upgrader remission (for SCs who sell their HDB/private property within six months of purchasing a new private property), and the joint-purchase SC/PR first-timer remission. None of these apply to typical foreigner purchasers.

Buyer’s Stamp Duty (BSD): Applies to Everyone

Buyer’s Stamp Duty applies to all property purchases regardless of nationality. The progressive rate schedule for residential property is: 1% on the first S$180,000; 2% on the next S$180,000; 3% on the next S$640,000; 4% on the next S$500,000; 5% on the next S$1,500,000; and 6% on the remainder. On a S$2M purchase, BSD amounts to approximately S$69,600 (an effective rate of about 3.48%). BSD must also be paid within the same 14-day window as ABSD.

Financing: LTV Limits, Downpayment and the TDSR

Contrary to some misconceptions, foreigners are not automatically barred from obtaining Singapore bank loans. Singapore-regulated banks (DBS, OCBC, UOB, Standard Chartered, Citibank, HSBC, and others) will assess foreign borrowers on the basis of their income, credit history, Total Debt Servicing Ratio (TDSR), and Loan-to-Value (LTV) limits set by the Monetary Authority of Singapore (MAS).

For a first property purchase, the LTV limit is 75%. The minimum 5% cash downpayment must come from the buyer’s own cash (CPF is only available to Singapore Citizens and PRs). Foreign buyers with no Singapore income need to satisfy the TDSR threshold — monthly total debt obligations must not exceed 55% of gross monthly income. Banks will typically require at least 12 months of salary crediting, employment letters, and often a personal visit to the branch or relationship manager in Singapore.

Foreign buyers should also note that rental income from the property cannot be used to service the TDSR calculation until it is actually received — only documented, existing income is recognised. A pre-approval (Approval-in-Principal) from the bank before exercising the OTP is strongly recommended.

Step-by-Step: How a Foreigner Buys a Singapore Condo

- Engage a Singapore-registered property lawyer before viewing properties. The lawyer will advise on eligibility, stamp duty liability, and contract review. (Note: marketing agents in Singapore are CEA-licensed but are not lawyers — do not rely on agents for legal advice.)

- Identify the property and negotiate the price with the seller or developer. For new launches, register for the sales chart; for resale, negotiate via the seller’s agent or directly.

- Obtain an Approval-in-Principal (AIP) from your chosen bank before committing to an OTP. This confirms your borrowing capacity and avoids the risk of losing your OTP fee if financing falls through.

- Exercise the Option to Purchase (OTP). For resale condos, an OTP fee (typically 1% of the purchase price) is paid to reserve the unit. The buyer then has 14 days to exercise the OTP by paying a further 4% (totalling 5% as initial deposit). For new launches, the process involves an Expression of Interest (EOI), booking fee (typically 5%), and signing the Sale and Purchase (S&P) Agreement.

- Pay ABSD and BSD within 14 days of exercising the OTP (or 30 days for overseas documents). Both must be paid in cash — ABSD cannot be financed.

- Complete legal requisitions. Your solicitor conducts title searches, confirms the title is free of encumbrances, and coordinates with the seller’s solicitor.

- Complete the purchase (typically 8–12 weeks after exercising the OTP for resale; longer for new launches under progressive payment). The balance of the purchase price is funded by the bank loan drawdown and your cash downpayment (after netting off the 5% deposit).

- Register the transfer at the Singapore Land Registry (part of SLA). Your solicitor handles this.

Worked Example: Mr Tanaka — Japanese Expat Buying His First Singapore Condo

Mr Tanaka is a Japanese national on an Employment Pass, working in Singapore in financial services. He earns S$22,000 per month and wants to purchase a 2-bedroom resale condominium in the Tanjong Pagar area (CCR, District 2) priced at S$2,200,000.

Stamp duties: BSD on S$2.2M = S$77,600. ABSD at 60% = S$1,320,000. Total stamp duties = S$1,397,600 (all payable in cash within 14 days of OTP exercise).

Downpayment: LTV 75% → bank loan S$1,650,000. Minimum 5% cash = S$110,000. Total cash for downpayment = S$110,000 (at minimum; remainder to 25% = S$440,000 may come from own funds).

Total cash required at exercise/completion: Stamp duties S$1,397,600 + cash downpayment (25% = S$550,000) + legal fees ~S$5,500 = approximately S$1,953,100 in cash.

Financing: Bank loan S$1,650,000 at 3.2% for 25 years = approx S$7,960/month. TDSR: S$7,960 / S$22,000 = 36.2% — within the 55% threshold. Mr Tanaka qualifies.

Annual property tax (non-owner-occupied, AV ~S$60,000): approximately S$8,100/year at the progressive non-owner-occupied rate.

Mr Tanaka proceeds. His total acquisition cost is S$2,200,000 (purchase) + S$1,397,600 (ABSD+BSD) + S$5,500 (legal) + S$1,200 (valuation) = S$3,604,300 — 63.8% more than the purchase price alone. This underscores why ABSD materially changes the investment economics for foreign buyers.

Permanent Residents (PRs): A Different Calculation

Singapore Permanent Residents occupy a middle ground between citizens and foreigners. PRs may purchase private condominiums and HDB resale flats (subject to EIP quotas). PRs cannot buy HDB BTO flats, HDB SBF flats, or DBSS flats. PRs cannot purchase Executive Condominiums in the open market during the first 5 years from TOP.

ABSD for a PR on a first residential property is 5%. On a S$2M condo, that is S$100,000 — significantly less than the 60% charged to foreigners. A PR who already owns one residential property pays 30% ABSD on any subsequent purchase.

PR couples where one spouse holds SC status buying their first property together may apply for ABSD remission to 0%, provided neither party has previously owned a Singapore residential property. This remission is claimed after purchase and ABSD must first be paid upfront — the refund is processed by IRAS typically within 6–9 months.

Is Singapore Property Still Worth Buying at 60% ABSD?

The 60% ABSD is a deliberate policy tool designed to cool speculative demand from foreign buyers while preserving market access for Singapore residents. For most retail foreign buyers, the financial case for buying residential property is difficult to justify when stamp duties exceed 60% of the purchase price — the break-even point on a 3% annual rental yield, after accounting for stamp duties, legal fees, property tax, and mortgage costs, extends beyond most reasonable investment horizons.

Where foreign buyers continue to transact is typically at the very high end of the market — ultra-high-net-worth individuals purchasing CCR properties as wealth preservation, Singapore-listed family offices, and buyers relocating permanently who intend to apply for PR or citizenship within a few years and factor in the eventual ABSD remission refund.

The data supports this: in the first half of 2026, foreign buyers accounted for approximately 3–5% of private residential transactions, compared to 8–12% before April 2023. That said, Singapore’s fundamentals — rule of law, transparent land registry, liquid resale market, strong SGD, and proximity to Southeast Asian business flows — mean demand endures at the right price point.

Could the 60% ABSD Come Down?

The 60% ABSD rate is not permanent by law but reflects current government policy priorities around housing affordability for Singaporeans. Any relaxation would require the government to be satisfied that the local property market has cooled sufficiently and that the risk of foreign-driven price inflation has abated. As of mid-2026, with private home prices continuing to rise modestly and HDB resale prices experiencing back-to-back quarterly declines, there is no indication the government intends to reduce the 60% rate in the near term. However, targeted remissions — for specific investor visa holders, for instance — are possible as policy instruments.

PRs seeking eventual SC status should also note that citizenship typically takes 2–5 years from the grant of PR, and SC buyers receive ABSD remission on their primary residence. Those who purchase property as a PR and subsequently acquire citizenship may apply to IRAS for a partial ABSD refund under the transitional remission framework, subject to specific conditions on timing and property use.

Frequently Asked Questions

Can a foreigner on an Employment Pass buy a Singapore condo?

Yes. Employment Pass or other work visa holders are classified as foreigners for property purchase purposes. They may freely purchase private strata-titled condominiums and apartments in Singapore, subject to paying 60% ABSD plus BSD. There is no minimum residency period, income requirement, or government approval needed — only sufficient funds and a qualifying bank loan assessment.

Does buying Singapore property help with a PR or citizenship application?

Property ownership does not directly count as a contribution for Permanent Residency or citizenship applications, which are assessed by the Immigration and Checkpoints Authority (ICA) based on employment, economic contribution, and community integration. However, property ownership may be a supporting indicator of long-term commitment to Singapore in an immigration file. Investing through the Global Investor Programme (GIP) — which involves minimum fund investments or business set-up — is a more direct pathway to PR for high-net-worth individuals.

Can foreigners buy landed property in Sentosa Cove?

Yes. Sentosa Cove is a designated area under the Residential Property Act where foreigners may purchase landed residential property (bungalows, semi-detached, and terrace houses) subject to SLA approval, which is generally granted for bona fide buyers. The 60% ABSD still applies to the purchase. Sentosa Cove units also attract Land Betterment Charge if the land use intensity is being maximised, and buyers should factor in the annual property tax, MCST fees for island-wide facilities, and the higher-than-average maintenance costs of landed property.

Can a foreigner avoid ABSD by buying through a Singapore company?

No — and attempting to do so is treated as tax avoidance under Singapore law. Entities (companies, trusts, LLPs) pay 65% ABSD on residential property, which is higher than the foreigner rate. The government has also introduced anti-avoidance provisions under the Stamp Duties Act to disregard arrangements that are designed to circumvent ABSD. IRAS has the power to assess ABSD on the underlying beneficial owner in such cases. The correct approach is always to take proper legal and tax advice before structuring any property acquisition.

Can a foreigner rent out a Singapore condo after buying?

Yes, subject to URA rules on short-term versus long-term rental. Private condominiums may be rented on leases of at least three consecutive months under URA’s guidelines (short-term rentals of less than three months require special use authorisation). Rental income is taxable under Singapore income tax; non-residents pay a flat 22% withholding tax on gross rental income unless a tax filing is made to IRAS to claim deductions for mortgage interest and maintenance, which typically reduces the effective tax rate. A tax agent or CPA familiar with Singapore non-resident landlord rules is recommended.

What happens to my property if I leave Singapore?

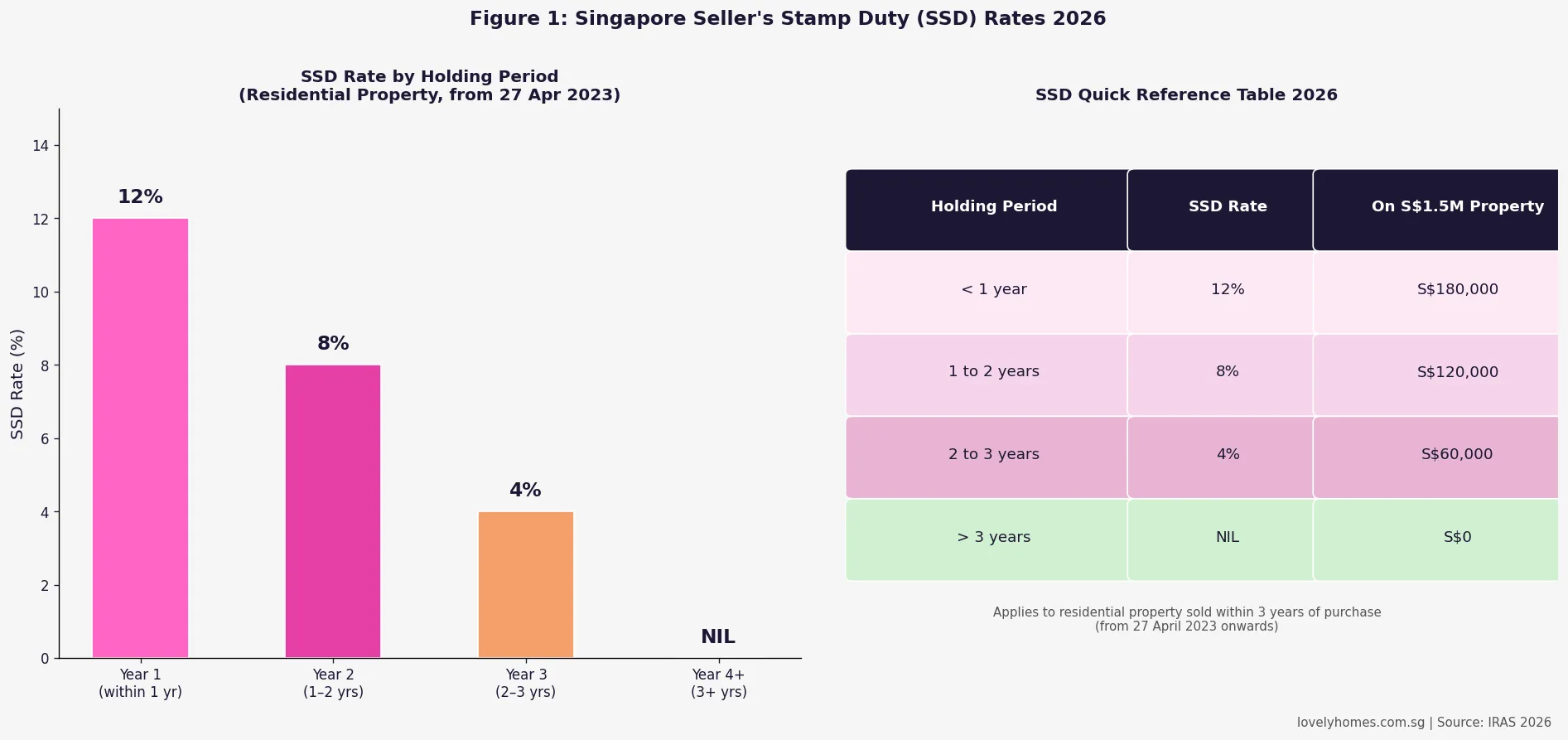

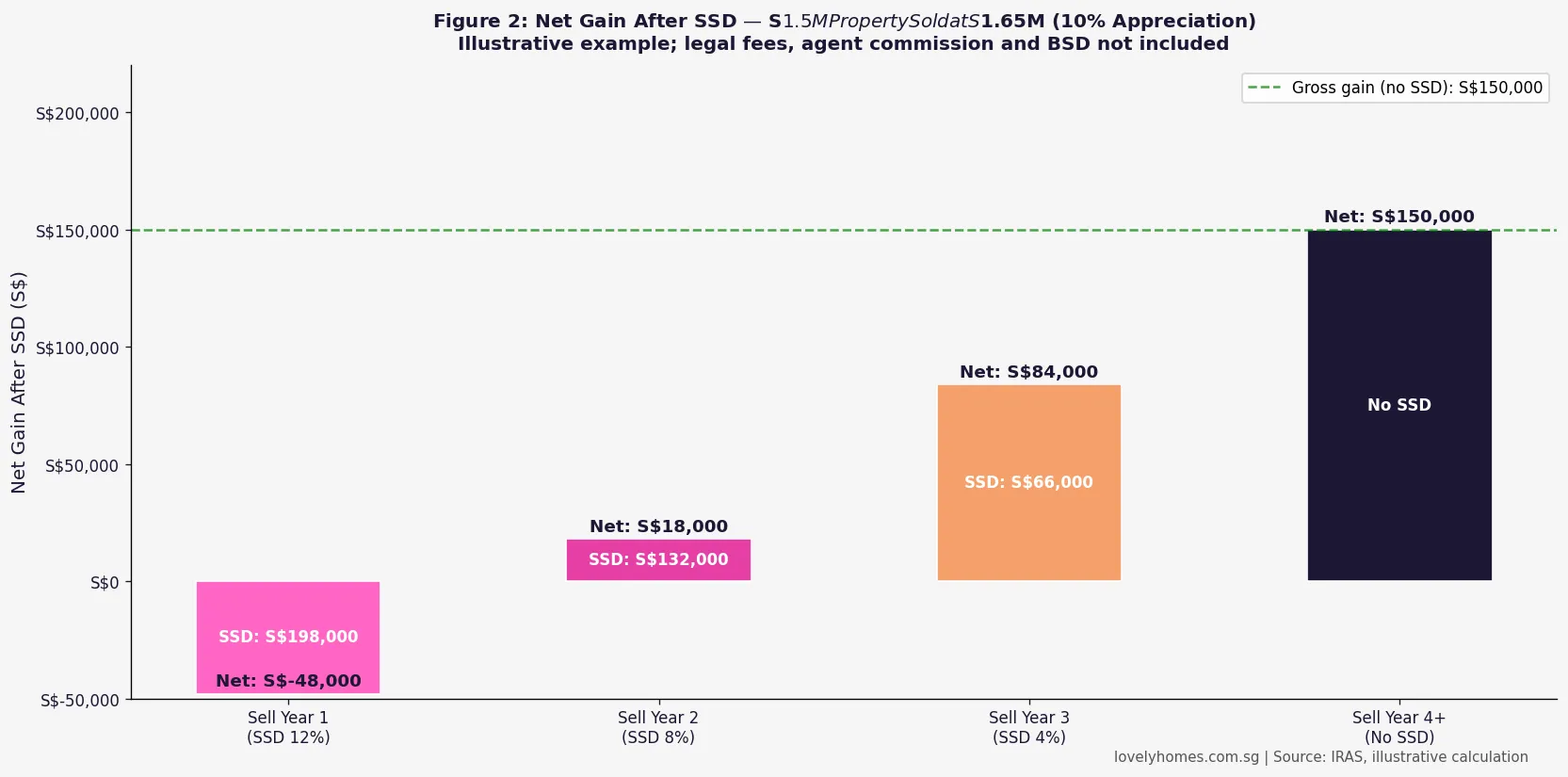

Foreigners may retain ownership of Singapore private property indefinitely regardless of their visa status or residence in Singapore. If you sell within three years of purchase, Seller’s Stamp Duty (SSD) of 12% (Year 1), 8% (Year 2), or 4% (Year 3) applies. There is no restriction on repatriating sale proceeds out of Singapore. Capital gains are not taxed in Singapore (there is no capital gains tax), and gains from the disposal of a property investment are generally treated as capital and not taxable income — though if disposal is frequent enough to constitute a trade, IRAS may take a different view.

What documents does a foreigner need to buy Singapore property?

You will need: a valid passport; evidence of source of funds (bank statements, investment account records, or proof of the sale of another asset); proof of income (payslips, employment contract, and — for business owners — audited accounts and bank statements for your business); an Approval-in-Principal (AIP) from a Singapore bank if financing; and a Singapore Tax Identification Number or NRIC/FIN for IRAS stamp duty payment purposes. Your Singapore property solicitor will guide you through the precise documentation checklist, which varies slightly by bank and by whether you are buying new launch or resale.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty Singapore 2026: BSD Rates and How to Calculate

- Singapore Condo Buying Process 2026: Step-by-Step Guide

- Singapore Home Mortgage Guide 2026: Fixed vs Floating, SORA Rates

- Singapore New Launch Condo Buying Guide 2026

- Singapore Seller’s Stamp Duty (SSD) Guide 2026

Disclaimer

This article provides general information about the rules applicable to foreigners purchasing property in Singapore as of July 2026. It is not legal, financial, or tax advice. The ABSD, BSD, and LTV figures cited reflect the most recently published rates from IRAS and MAS; always verify current rates at iras.gov.sg and mas.gov.sg before transacting. The Residential Property Act and Stamp Duties Act are administered by the SLA and IRAS respectively — consult both official sources and a Singapore-qualified lawyer before making any property purchase decision. Past property performance does not guarantee future returns.

Click anywhere to close