Pasir Ris Neighbourhood Guide Singapore 2026: HDB Prices, Condos, Schools and the CRL Opportunity

Quick Answer: Pasir Ris at a Glance

- Location: North-east Singapore, District 18 (Outside Central Region)

- MRT: Pasir Ris EWL station; Cross Island Line (CRL) Pasir Ris Town station by 2032

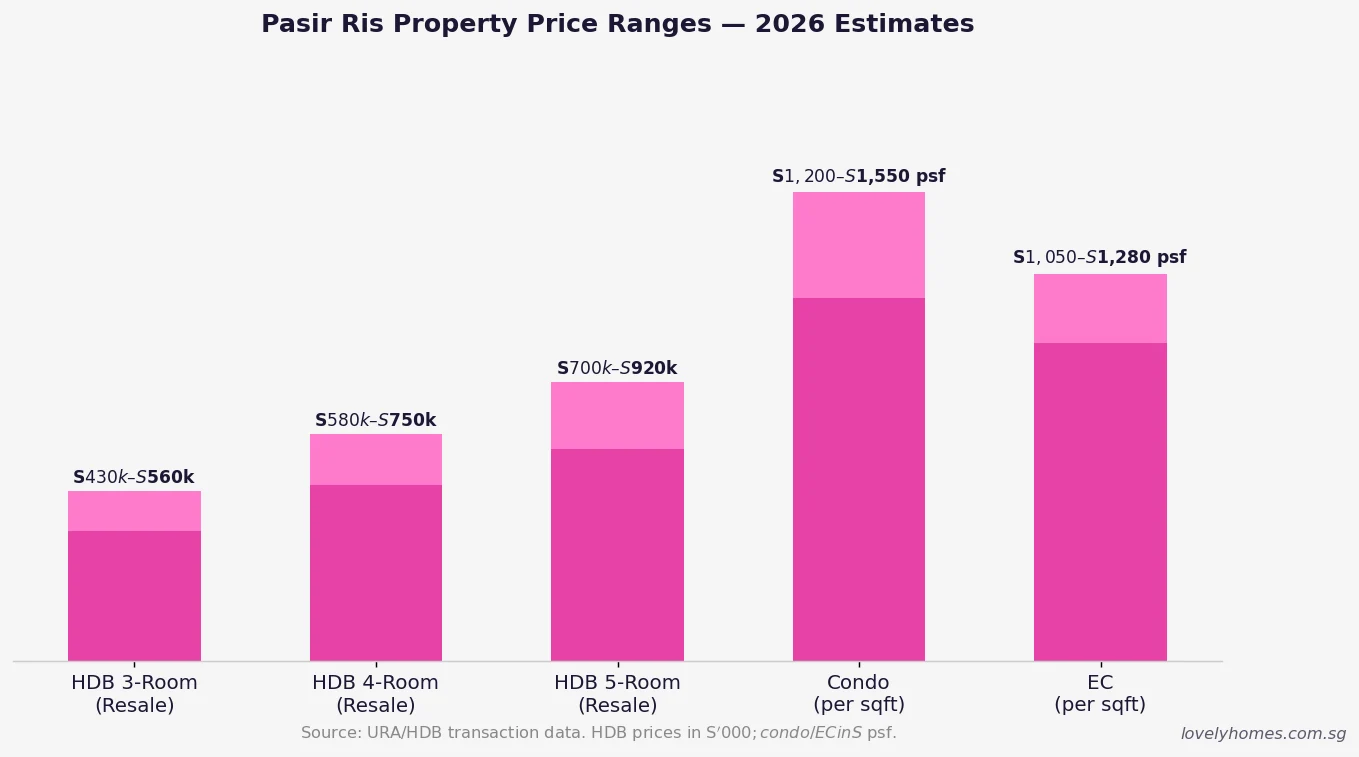

- HDB Resale (2026): 3-room S$430k–S$560k; 4-room S$580k–S$750k; 5-room S$700k–S$920k

- Private Condo psf: S$1,200–S$1,550 psf (Q1 2026 OCR benchmark); EC S$1,050–S$1,280 psf

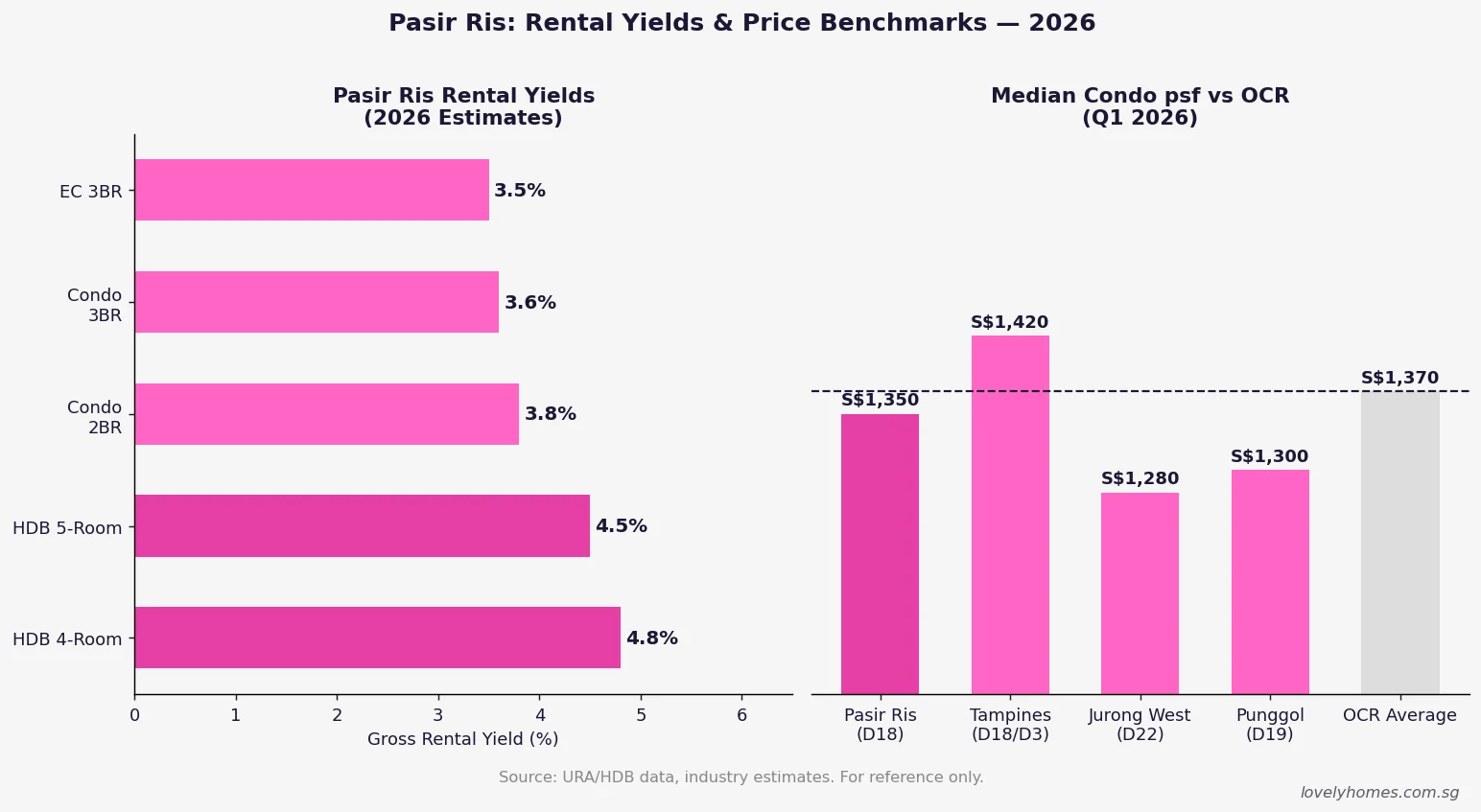

- Gross Rental Yield: HDB 4-room ~4.8%; Condo 2BR ~3.8%; EC 3BR ~3.5%

- Key Lifestyle Draws: Pasir Ris Park (72 ha, mangrove boardwalk), Downtown East, White Sands Mall

- Schools: Coral Primary, Loyang Primary, Hai Sing Catholic School, Meridian Junior College

- Coming Up: CRL Phase 2 station by 2032; New Upper Changi Road GLS site (D16, ~1,010 units, tender Sep 2026)

Pasir Ris sits at the easternmost fringe of Singapore’s public housing map — a town of wide roads, generous parks, and a relaxed waterfront atmosphere that has made it a consistent favourite among families and right-sizers for more than three decades. Built up from the late 1980s onward, it lacks the heritage cachet of Tiong Bahru or the hipster draw of Joo Chiat, yet property analysts consistently rank it among the best-value large-family towns in the OCR. With the Cross Island Line bringing a second MRT interchange by 2032 and a major new GLS site in adjacent D16, Pasir Ris is quietly entering a new phase of relevance for both owner-occupiers and investors.

This guide covers everything prospective buyers, tenants, and investors need to know about Pasir Ris in 2026 — from HDB resale prices and private condo benchmarks to schools, connectivity, rental yields, and the key catalysts that could lift values over the coming decade.

Property Prices in Pasir Ris: What You Will Pay in 2026

Pasir Ris sits firmly in the Outside Central Region (OCR), Singapore’s most affordable private residential corridor. HDB dominates the landscape, with roughly 58,000 public flats across 18 neighbourhoods. Private condominiums and executive condominiums (ECs) occupy the western and central fringes, typically closer to the MRT and main expressways.

HDB resale prices have moved steadily higher since the 2022 cooling measures stabilised demand. In Q1 2026, a typical 4-room flat in established Pasir Ris streets — Pasir Ris Drive 1, Pasir Ris Street 11, Pasir Ris Street 21 — transacted between S$580,000 and S$750,000. Five-room flats, especially those on higher floors with unobstructed greenery views, have crossed S$900,000. Million-dollar HDB transactions in Pasir Ris remain rare but are no longer impossible for premium 5-room units in sought-after blocks near the park.

Private condominiums in District 18 trade at S$1,200–S$1,550 per square foot, reflecting a modest premium over deeper OCR towns such as Choa Chu Kang or Jurong West, justified by the proximity to Changi Business Park and the broader East employment corridor. The integrated Pasir Ris 8 development, which sits directly atop the MRT station, commands the top of this range given its lifestyle and transport conveniences. Older freehold condominiums nearby trade closer to S$1,200 psf.

Location and Connectivity: East End Accessibility

Pasir Ris is bounded by Tampines to the west, Loyang to the north, and the Strait of Johor to the north-east. The Pasir Ris MRT station is the eastern terminus of the East West Line (EWL), placing it approximately 44 minutes by train from Raffles Place — manageable rather than fast for CBD commuters, but well-suited to those working in Changi, Tampines Regional Centre, or along the EWL corridor.

By road, residents enjoy direct access to the Tampines Expressway (TPE) and Kallang–Paya Lebar Expressway (KPE), making Changi Airport reachable in under 15 minutes. Tampines Regional Centre — Singapore’s largest regional commercial hub — is one bus stop or a short cycle away.

The transformative upgrade arrives with the Cross Island Line (CRL). Phase 2 of the CRL will include a Pasir Ris Town station (separate from the existing EWL station), creating an interchange that connects residents directly to key growth nodes including Jurong Lake District, Ang Mo Kio, and Tuas. LTA has targeted CRL Phase 2 completion around 2032. Property analysts generally expect this infrastructure upgrade to add 5–10% to local values in the preceding three to four years, mirroring the Tampines price trajectory following the Downtown Line integration in 2017.

HDB Housing: Town Character, Parks, and Flat Types

Pasir Ris was planned as a comprehensive town with its own commercial centre, neighbourhood parks, and a clear separation between residential clusters and industrial uses. The result is one of Singapore’s most liveable HDB towns — wide pavements, cycling paths, and generous inter-block greenery characterise virtually every neighbourhood.

The flagship amenity is Pasir Ris Park, a 72-hectare coastal park that is the largest waterfront park in Singapore’s east. It incorporates a mangrove boardwalk (gazetted as a nature area by URA), bird-watching areas, barbecue pits, cycling paths, and beach volleyball courts. Few HDB towns in Singapore can claim a natural asset of this scale within walking distance of the MRT station.

For everyday convenience, residents rely on White Sands (a mid-sized suburban mall anchored by NTUC FairPrice and Popular Bookstore), Elias Mall, and the Downtown East leisure complex, which houses E!Hub, Wild Wild Wet, and a broad range of food and entertainment options. Downtown East underwent a significant redevelopment and now serves as a regional leisure hub drawing visitors from across the east.

HDB flat types in Pasir Ris range from 3-room (typically 60–68 sqm) to 5-room (approximately 110–122 sqm), with a small stock of executive flats in older blocks. The town was built predominantly in the 1990s and early 2000s, meaning most flats carry 65–75 years of lease remaining — well within CPF and HDB loan thresholds for maximum financing, though buyers in their mid-40s and above should confirm lease adequacy against their own age parameters before committing.

Private Property and the Rental Market

Pasir Ris’s private residential inventory is concentrated along Pasir Ris Grove and Pasir Ris Close, with notable projects including Costa Riá (freehold, 398 units, TOP 2003), Coco Palms EC (944 units, privatised 2021), and the more recent Pasir Ris 8 — a 487-unit mixed-use development integrated with Pasir Ris MRT station and a retail podium. Pasir Ris 8’s psf range sets the benchmark for new-generation OCR integrated projects in the east.

The rental market reflects steady demand from Changi Business Park, Loyang Industrial Estate, and the broader East employment corridor. HDB 4-room units command S$2,800–S$3,800 per month depending on floor level and proximity to amenities. Condo 3-bedroom units typically rent for S$4,200–S$5,500 per month. Gross yields on HDB 4-room flats run approximately 4.5–5.0% at 2026 transaction values; private condo yields range from 3.5–4.2% gross.

Pasir Ris vs OCR Peers: Summary Comparison

| Factor | Pasir Ris (D18) | Tampines (D18) | Punggol (D19) | Jurong West (D22) |

|---|---|---|---|---|

| HDB 4-Room Resale | S$580k–S$750k | S$590k–S$780k | S$550k–S$700k | S$480k–S$620k |

| Private Condo psf | S$1,200–S$1,550 | S$1,300–S$1,600 | S$1,200–S$1,450 | S$1,100–S$1,380 |

| MRT Lines | EWL + CRL (2032) | EWL + DTL | NEL + LRT | EWL + JRL |

| Gross Rental Yield | 3.5%–5.0% | 3.4%–4.8% | 3.6%–5.2% | 3.8%–5.4% |

| Key Catalyst | CRL Phase 2 (2032) | Tampines North EC | Waterway eco-park | JLD + Jurong Rail Corridor |

| Park/Coastal Access | Excellent (72 ha park) | Good (Bedok Reservoir) | Very Good (Waterway) | Good (Jurong Lake) |

Worked Example: First-Timer Buying HDB Resale in Pasir Ris

Mr and Mrs Lim are a Singapore Citizen couple, both aged 34, with a combined gross monthly income of S$10,000. They wish to purchase a 4-room resale HDB flat in Pasir Ris Street 21 for S$680,000 — their first residential property.

Stamp Duty (BSD): Computed on S$680,000 per IRAS rates: 1% × S$180,000 = S$1,800; 2% × S$180,000 = S$3,600; 3% × S$320,000 = S$9,600. Total BSD: S$15,000. ABSD is nil for Singapore Citizens purchasing their first residential property.

HDB Loan (80% LTV): Maximum loan = S$544,000 at HDB concessionary rate of 2.60% p.a. over 25 years. Estimated monthly instalment: approximately S$2,462/month.

Mortgage Servicing Ratio (MSR): S$2,462 ÷ S$10,000 = 24.6% — PASS (MAS MSR cap is 30% for HDB purchases). TDSR: 24.6% — PASS (cap is 55%, assuming no other debt obligations).

Upfront requirements: 20% cash/CPF downpayment = S$136,000 + BSD S$15,000 = approximately S$151,000. CPF Ordinary Account savings can fund the bulk of this amount, subject to the CPF Withdrawal Limit and Valuation Limit. Budget an additional S$20,000–S$30,000 cash for legal fees, survey, and moving costs.

At 2026 rental market rates, a comparable 4-room flat in the same area rents for approximately S$3,400/month — meaning the Lims’ monthly ownership cost of S$2,462 is materially below the rental equivalent, reinforcing the financial case for purchasing rather than renting.

Why Pasir Ris Matters: The Investment Perspective

Pasir Ris occupies a distinctive position in Singapore’s OCR hierarchy: it is not the cheapest town (that distinction belongs to Woodlands or Jurong West in many flat-type comparisons), nor the most sought-after (Bishan and Clementi command higher psf). What it delivers is a quality-of-life proposition that many more expensive estates cannot match — the 72-hectare park, coastal exposure, uncrowded residential feel, and proximity to Changi Airport and the East employment corridor are structural advantages unlikely to erode regardless of broader market cycles.

The CRL uplift is the single most important medium-term catalyst. Infrastructure upgrades of this nature — new MRT interchanges where a town previously had a single line — have historically preceded 8–15% price appreciation in the two to three years around opening. Investors who position in the 2026–2029 window still have a reasonable opportunity to benefit ahead of the 2032 CRL opening.

What Might Come Next for Pasir Ris

The New Upper Changi Road GLS site (tender closes 1 September 2026) will introduce approximately 1,010 new homes in adjacent D16. This adds medium-term supply but also signals continued government confidence in the Bedok–Pasir Ris east corridor as a residential growth zone. As Pasir Ris 8’s retail podium matures — with more F&B and lifestyle tenants completing fit-out — its pull on surrounding property values should intensify over 2026–2028.

There is also ongoing discussion — nothing confirmed by NParks or URA as at writing — of further enhancements to the Pasir Ris waterfront under Singapore’s Blue Plan framework for coastal recreation. Such upgrades, if they materialise, would reinforce the park’s status as the town’s defining asset.

Frequently Asked Questions

Is Pasir Ris a good place to buy property in 2026?

For owner-occupiers seeking a family-friendly OCR town with strong amenities and an upcoming transport upgrade, Pasir Ris ranks highly. The combination of reasonable HDB resale prices, the 72-hectare park, good schools, and the forthcoming CRL interchange creates a compelling case. Investors should note that rental yields are solid (3.5–5.0% depending on unit type) but the stronger investment thesis rests on capital appreciation via the CRL catalyst rather than current yield alone.

What are the HDB resale prices in Pasir Ris in 2026?

As at Q1 2026, HDB 3-room flats in Pasir Ris transact between S$430,000 and S$560,000; 4-room flats between S$580,000 and S$750,000; and 5-room flats between S$700,000 and S$920,000. Premium blocks near Pasir Ris Park, with high floors and unobstructed views, command the top of these ranges. Prices have held broadly stable since the 2022 cooling measures, with modest upward drift in 2025–2026 as the CRL’s potential becomes more widely understood by the market.

When will the CRL station at Pasir Ris open?

The Land Transport Authority (LTA) has announced that CRL Phase 2 will include a Pasir Ris Town station — separate from the existing Pasir Ris EWL station — with an indicative completion target around 2032. Exact dates are subject to LTA’s construction milestones and should be verified directly with LTA (lta.gov.sg). The CRL will run from Aviation Park in the east to Jurong Lake District in the west, connecting Pasir Ris to Ang Mo Kio, Clementi, and Tuas without changing trains.

Can foreigners buy property in Pasir Ris?

Foreign nationals (non-Singapore Citizens) cannot purchase HDB flats. They may purchase private condominiums and commercial properties in Pasir Ris. However, Additional Buyer’s Stamp Duty (ABSD) of 60% applies to foreign buyers of all residential properties in Singapore as at 2026, making private condo investment unattractive for most overseas buyers. Singapore Permanent Residents purchasing their first residential property pay 5% ABSD. For full details, see our guide to foreigners buying property in Singapore 2026.

What private condominiums are available in Pasir Ris?

Key private condo projects in District 18 include Pasir Ris 8 (487 units, MRT-integrated, TOP 2023), Costa Riá (398 units, freehold, TOP 2003), Coco Palms EC (944 units, privatised 2021), and Ballota Park Condo (96 units, freehold). Pasir Ris 8 is the premium benchmarker at the top of the D18 psf range; older freehold condos trade closer to S$1,200–S$1,300 psf. The adjacent New Upper Changi Road GLS (tender closes September 2026) will introduce further supply that may influence price formation in the medium term.

What primary schools are within 1 km of Pasir Ris MRT?

Coral Primary School, Loyang Primary School, and Meridian Primary School are among the primary schools within approximately 1–2 km of the Pasir Ris MRT station. Buyers prioritising school proximity for Phase 2A or Phase 2B registration should check the MOE’s official school registration distance lists (moe.gov.sg) when making their shortlist, as exact distances vary by flat block. At the secondary level, Hai Sing Catholic School and Pasir Ris Secondary serve the town.

How does the MSR work, and how does it affect a Pasir Ris HDB purchase?

The Mortgage Servicing Ratio (MSR), set by MAS, caps monthly mortgage instalments on HDB residential property at 30% of the borrower’s gross monthly income for both HDB loans and bank loans used to purchase HDB flats. In the worked example above, the Lim couple’s estimated instalment of S$2,462 on a joint income of S$10,000 equates to 24.6% MSR — comfortably within the cap. The Total Debt Servicing Ratio (TDSR) of 55% covers all debt obligations, including car loans, personal loans, and existing mortgages. Both ratios are assessed by the lender at the point of application.

Related Articles

- Tampines Neighbourhood Guide Singapore 2026

- Punggol Neighbourhood Guide Singapore 2026

- Sengkang Neighbourhood Guide Singapore 2026

- New Upper Changi Road GLS 2026: Site Analysis

- CPF for Property Purchase Singapore 2026

- Singapore Home Loan Interest Rates 2026

- HDB MOP Singapore 2026

- ABSD Singapore 2026: Complete Guide

Disclaimer: All property prices and rental figures cited in this article are estimates based on publicly available transaction data and industry benchmarks as at Q1 2026. They are provided for general information only and do not constitute financial, investment, or legal advice. Individual transactions vary depending on flat condition, floor level, lease remaining, and market conditions at the time of sale. Prospective buyers should obtain independent valuations, consult a licensed property agent registered with the Council for Estate Agencies (CEA), seek advice from a qualified mortgage broker, and read official guidelines published by HDB (hdb.gov.sg), URA (ura.gov.sg), IRAS (iras.gov.sg), CPF Board (cpf.gov.sg), and MAS (mas.gov.sg) before making any property decisions.