Singapore Commercial Property Guide 2026: Shophouses, Office, Industrial and the No-ABSD Advantage

- What counts as commercial property: shophouses, strata office units, industrial (B1/B2) space, retail strata units, and commercial land.

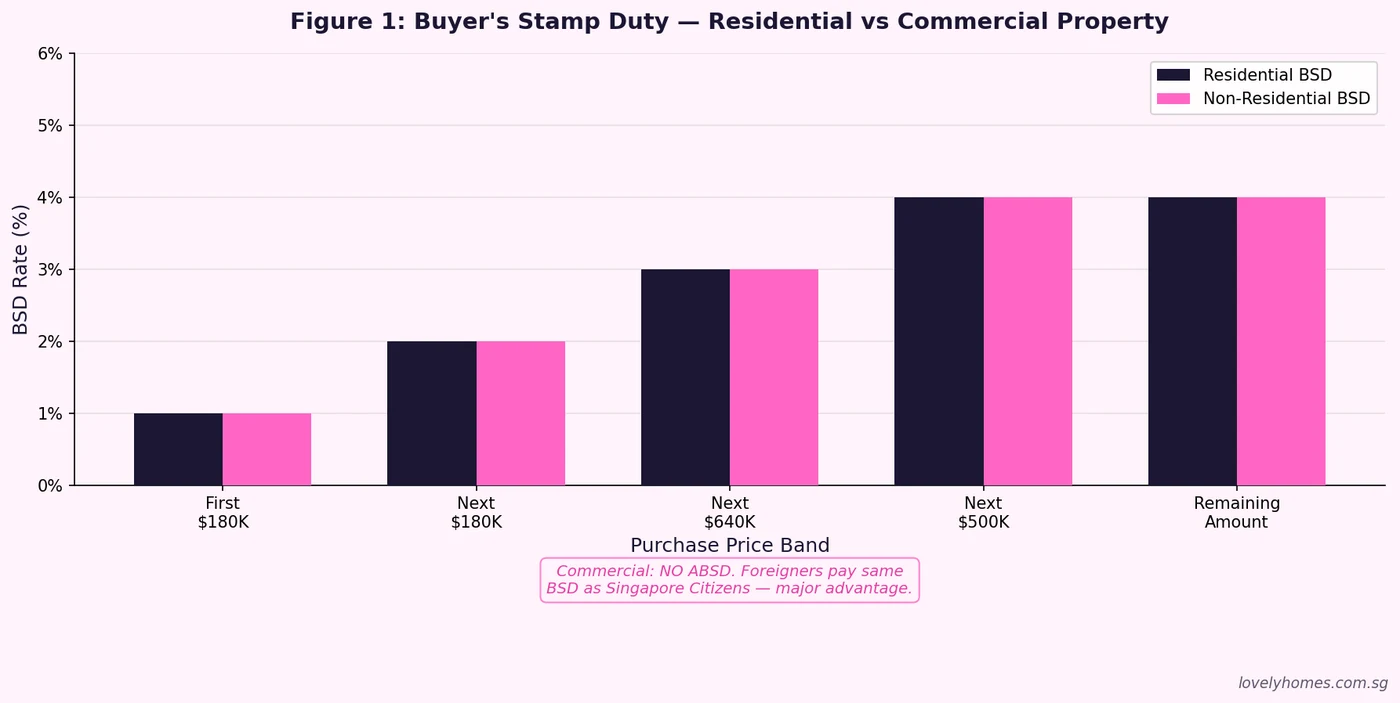

- No ABSD on commercial: Singapore Citizens, Permanent Residents, and foreigners all pay the same Buyer's Stamp Duty only — zero Additional Buyer's Stamp Duty regardless of how many properties you own.

- BSD rates (2026): 1% on first S$180,000; 2% on next S$180,000; 3% on next S$640,000; 4% on next S$500,000; 5% on amounts above S$1.5 million — identical to residential BSD.

- Financing: Maximum Loan-to-Value (LTV) is 55% for commercial property (versus 75% for a first residential property), and CPF Ordinary Account funds cannot be used for commercial purchases.

- Property tax: Commercial and industrial properties are taxed at 10% of Annual Value — a flat rate, unlike the progressive owner-occupier residential scale.

- Foreigners welcome: Unlike residential property (subject to Residential Property Act restrictions and steep ABSD), foreigners may purchase most commercial properties freely with no SLA approval needed.

- Governing bodies: URA (zoning and planning permission), IRAS (stamp duty and property tax), JTC Corporation (industrial estates).

What Is Commercial Property in Singapore?

Singapore's Urban Redevelopment Authority (URA) classifies land use into three broad categories: residential, commercial, and industrial. When property professionals and investors refer to "commercial property," they typically mean any real estate asset that is not zoned for residential occupation — spanning the entire spectrum from a 1920s Chinatown heritage shophouse to a purpose-built logistics facility in Jurong.

This matters enormously because the legal and tax treatment of commercial real estate differs fundamentally from residential. The Additional Buyer's Stamp Duty (ABSD) regime — which adds up to 65% to the purchase price for foreign buyers of residential property, and 20% for Singapore Citizens purchasing a second home — does not apply to commercial transactions. That single fact reshapes the investment calculus for multiple-property owners, high-net-worth families, and international investors.

The URA Master Plan 2025 designates commercial zones as "Commercial," "Commercial and Residential," "Business 1 (B1)" for clean light industrial, and "Business 2 (B2)" for heavier industrial uses. Each zone carries different permitted activities, plot ratios, and development intensities — all publicly searchable on the URA Space portal.

Types of Commercial Property in Singapore

Singapore's commercial market encompasses several distinct asset classes, each with its own supply dynamics, typical tenants, financing norms, and liquidity profile.

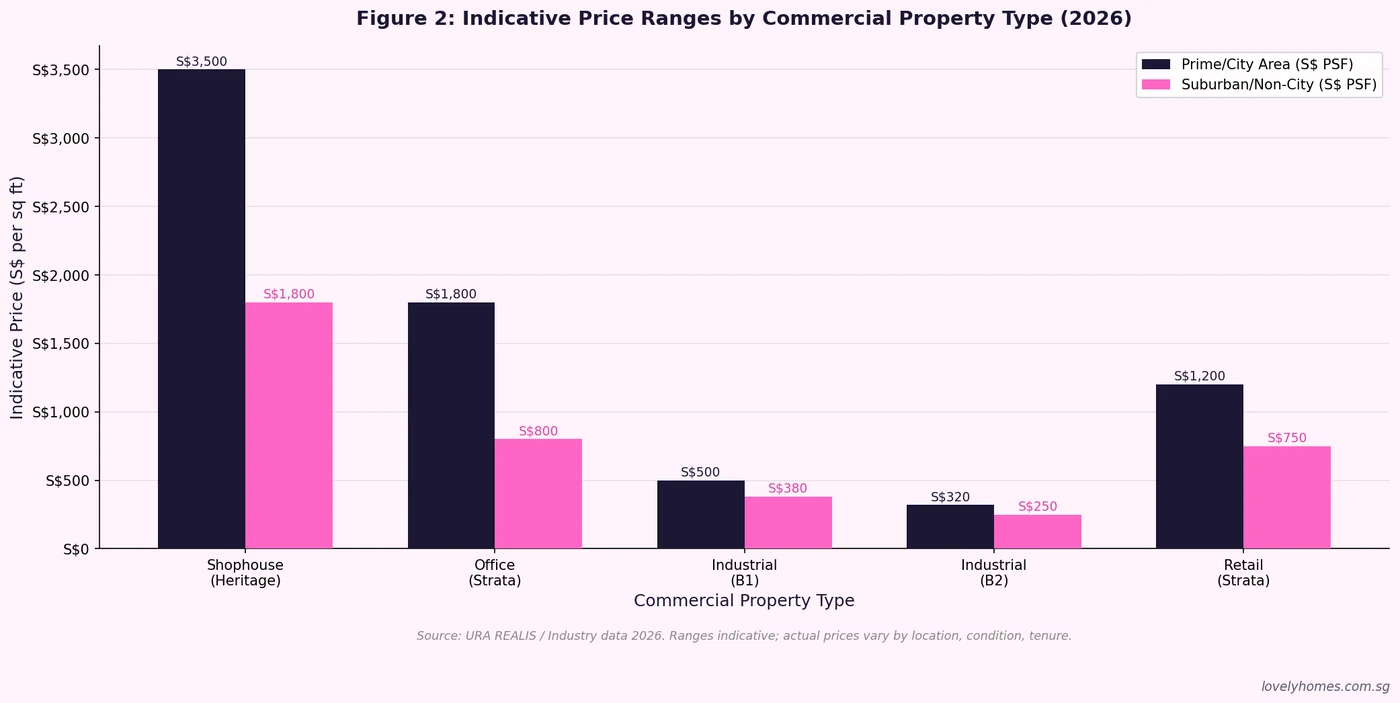

Shophouses are the crown jewel of Singapore's heritage commercial market. Built between roughly 1840 and 1960, they are two-to-four-storey terrace buildings with ground-floor retail or F&B and upper-floor office or residential use. Conservation shophouses in the Civic District, Chinatown, Little India, and Tanjong Pagar trade at premium per-square-foot prices — routinely S$3,000 to S$5,000 per sq ft — because supply is permanently capped: the URA grants no new conservation status. Non-conservation walk-up commercial shophouses in Geylang, Balestier, and Joo Chiat trade at more accessible prices of S$1,500 to S$2,500 per sq ft.

Strata office units are individually owned floors or suites within purpose-built office buildings. The primary supply is concentrated in the Central Business District (CBD) at Marina Bay, Raffles Place, Shenton Way, and Tanjong Pagar. Grade A strata office typically commands S$2,500 to S$3,500 per sq ft; suburban office in Paya Lebar, Jurong East, or Mapletree Business City trades at S$1,000 to S$1,800 per sq ft. Rental yields run at approximately 3% to 4% gross for prime strata office.

Industrial property — comprising B1 (clean light industrial and ancillary office) and B2 (general industrial and logistics) — is the largest commercial property segment by transaction volume. JTC Corporation regulates industrial land use and operates flatted factory clusters, business parks such as one-north and Changi Business Park, and clean-room facilities. B1 industrial units in well-located clusters such as Tai Seng, Ubi, and Geylang Bahru sell for S$300 to S$600 per sq ft, delivering gross rental yields of 5% to 7%. B2 warehouses and logistics facilities in Penjuru, Tuas, and Jurong are typically leasehold and trade at S$150 to S$350 per sq ft.

Retail strata units within suburban malls cater primarily to F&B and service tenants on 2-to-3 year leases. Prices reflect the anchor tenant mix and footfall catchment of the surrounding estate, making due diligence on tenant mix critical before any retail strata purchase.

Buyer's Stamp Duty on Commercial Property

IRAS administers Buyer's Stamp Duty (BSD) on all property purchases in Singapore. Since the February 2023 Budget, BSD rates apply on a tiered basis — identical for both residential and non-residential properties:

| Purchase Price Band | BSD Rate | BSD on That Band |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 | 2% | S$3,600 |

| Next S$640,000 | 3% | S$19,200 |

| Next S$500,000 | 4% | S$20,000 |

| Remaining amount (above S$1.5 million) | 5% | Varies |

On a S$3.5 million shophouse purchase, total BSD = S$1,800 + S$3,600 + S$19,200 + S$20,000 + (S$2,000,000 x 5%) = S$144,600. The same BSD applies whether the buyer is a Singapore Citizen, a Permanent Resident, or a foreign national.

The No-ABSD Advantage

The ABSD regime was designed by the Ministry of Finance to cool residential speculation and improve housing affordability. It was never intended to dampen commercial investment. For a Singapore Citizen who already owns one residential property, buying a second residential condominium at S$2 million triggers an ABSD charge of 20% = S$400,000, on top of BSD of approximately S$69,600. The total stamp duty bill reaches S$469,600.

The same Singapore Citizen buying a S$2 million strata office unit pays only BSD of S$69,600 — no ABSD, saving S$400,000 in stamp duty. For a foreign national, the arithmetic is even more compelling: a S$2 million residential condo would trigger 65% ABSD = S$1,300,000 plus BSD of S$69,600, whereas a S$2 million commercial unit costs only S$69,600. The saving is S$1,300,000 — equivalent to 65% of the purchase price.

This structural advantage explains consistent institutional and high-net-worth demand for Singapore shophouses and strata office assets even during periods of residential cooling. The URA has confirmed that the ABSD regime has no plans to extend to commercial property as at the time of publication.

Financing Commercial Property in Singapore

The Monetary Authority of Singapore (MAS) does not impose the same Total Debt Servicing Ratio (TDSR) and Loan-to-Value (LTV) regulations on commercial property that it does on residential mortgage loans. However, commercial property loans carry their own constraints.

The maximum LTV for commercial property loans is generally 55% of the property's lower of purchase price or valuation, compared to 75% for a first residential property. In practice, some lenders may offer up to 60% LTV for prime commercial assets with strong tenants, while industrial property in secondary locations may attract only 40-50% LTV. Interest rates for commercial loans typically carry a premium of 0.3% to 0.8% above comparable residential rates.

Crucially, CPF Ordinary Account savings cannot be used to service commercial property loans or meet the purchase downpayment. Commercial buyers must fund the downpayment and loan servicing entirely from cash or investment income. At current commercial lending rates of approximately 3.5% to 4.5% per annum and an LTV of 55%, the monthly interest service on a S$2 million property (S$1.1 million loan) runs at approximately S$3,850 to S$4,950 — which must be covered by rental income with adequate buffer.

Property Tax on Commercial and Industrial Properties

IRAS levies property tax annually on all Singapore properties based on their Annual Value (AV) — the estimated annual rental the property would fetch if rented out. For commercial and industrial properties, the property tax rate is a flat 10% of Annual Value, regardless of whether the property is owner-occupied or investment-held.

This contrasts with the residential owner-occupier scale (0% to 32% progressive on AV) and the non-owner-occupier residential rate (12% to 36% progressive). A CBD strata office unit with a market rental of S$6,000 per month (AV approximately S$72,000) would generate an annual property tax bill of S$7,200 — around 1% of a typical S$700,000 purchase price, or S$600 per month in holding costs.

Risks and Practical Considerations

Commercial property investment in Singapore is not without risk. Vacancy periods can extend to 3 to 6 months between tenancies, particularly for strata office and retail units. Commercial tenants — especially F&B operators — carry elevated insolvency risk compared to residential tenants; a single tenant failure can leave an investor servicing a loan on a vacant unit for months while pursuing re-marketing.

Shophouse liquidity is also more limited than residential. There are far fewer qualified buyers for a S$5 million shophouse than for a S$1.5 million condominium, meaning shophouses should be regarded as 5-to-10-year investment horizons. Industrial assets in JTC estates carry use restrictions — the tenant must operate a qualifying industrial activity, and subleasing without JTC approval is a regulatory breach.

Summary: Commercial vs Residential — Key Differences

| Factor | Commercial Property | Residential Property |

|---|---|---|

| ABSD applicable? | No (zero) | Yes (0%–65% by profile) |

| BSD rate | 1%–5% tiered (same scale) | 1%–5% tiered (same scale) |

| Foreigners allowed? | Yes, freely | Restricted (SLA approval for landed) |

| Max LTV | ~55% | 75% (1st property) |

| CPF usable? | No | Yes (OA for residential) |

| Property tax rate | 10% of AV (flat) | 0%–36% of AV (progressive) |

| Typical gross yield | 3%–7% (by type) | 2%–4% (condo/HDB) |

| Seller's Stamp Duty? | No SSD | SSD 4%–12% within 3 years |

| Governing body | URA / JTC Corporation | URA / HDB |

Worked Example: Mr Rajesh Buys a Chinatown Shophouse

Mr Rajesh is a Singapore Permanent Resident who already owns a 3-bedroom condominium in Bishan. He is comparing a second residential condo versus a conservation shophouse in Chinatown, both priced at approximately S$3.5 million.

Option A — Second Residential Condo (SPR buying 2nd residential):

- BSD: S$144,600

- ABSD (SPR 2nd property at 30%): S$1,050,000

- Total stamp duties: S$1,194,600

- Gross rental yield: ~3.5% = S$122,500/year

- Years to recover stamp duties at net yield: ~12 years

Option B — Conservation Shophouse (Commercial, no ABSD):

- BSD: S$144,600

- ABSD: S$0

- Total stamp duties: S$144,600 — saving S$1,050,000 versus Option A

- Gross rental yield: ~2.8% = S$98,000/year

- Loan (LTV 55%): S$1,925,000 at 4.0% pa = S$6,417/month

- Annual property tax (AV ~S$98,000 x 10%): S$9,800

Conclusion: Even at a marginally lower headline yield, the commercial shophouse produces a substantially superior after-stamp-duty return. The ABSD saving of S$1,050,000 effectively reduces the cost base by 30% — demonstrating why Singapore's commercial market consistently attracts investors who have already deployed their first residential purchase.

Why This Matters: Singapore's Commercial Property in a Regional Context

Singapore stands out in Southeast Asia for the clarity of its commercial property regulation. In contrast to markets such as Thailand (where foreign land ownership is prohibited outright), Malaysia (where non-citizens face restrictions on certain property categories), and Indonesia (where foreigners may only acquire nominal use rights), Singapore offers foreigners full freehold strata title to commercial units with no approval process and no repatriation restrictions on proceeds.

This openness, combined with the absence of ABSD on commercial assets, has made Singapore shophouses a preferred safe-haven asset for regional family offices and high-net-worth individuals from across Asia. URA REALIS data confirms that non-Singaporean buyers consistently account for 20 to 35% of shophouse transactions by value in any given year.

The MAS Financial Stability Review (November 2025) noted that the commercial property market remained well supported by strong occupancy fundamentals, with Grade A CBD office vacancy below 5% as at Q4 2025. The review flagged that interest rate normalisation — as SORA resets towards 2.8% from a Q4 2024 peak of 3.7% — should ease financing costs for leveraged commercial investors through 2026.

What Might Come Next

The Jurong Lake District (JLD) White Site, launched under the June 2026 GLS programme, is the single most significant commercial development event in the near term. The JLD master plan envisions a second CBD with 1.6 million sq m of commercial floor space by 2050 — a pipeline that could substantially reshape office market dynamics in the western corridor. The Long Island coastal protection project announced by URA on 30 June 2026 may eventually create new commercial and industrial districts east of Changi, though planning timelines extend well beyond 2040.

There is ongoing policy discussion about whether BSD on very high-value commercial transactions (above S$5 million) should be reviewed in a future Budget. Any BSD increase on commercial property would represent a structural headwind for the shophouse market specifically. LovelyHomes will monitor any IRAS or Ministry of Finance announcements closely and update this guide accordingly.

Frequently Asked Questions

Can a foreigner buy a shophouse in Singapore without government approval?

Yes, in most cases. Foreigners may purchase commercial shophouses without approval from the Singapore Land Authority (SLA). However, if the shophouse has residential upper floors zoned as "residential" under the URA Master Plan, the Residential Property Act (Cap. 274) applies to that component. Buyers should confirm the exact zoning of both the ground and upper floors with a Singapore-qualified property lawyer before exercising any option to purchase a mixed-use shophouse.

Is there a Seller's Stamp Duty (SSD) on commercial property?

No. Singapore's Seller's Stamp Duty applies only to residential property held for less than three years — at rates of 12%, 8%, or 4% depending on the year of sale. Commercial and industrial property, including shophouses, strata office, and industrial units, carry no SSD regardless of how quickly they are sold after purchase. This makes commercial real estate materially more liquid than residential for short-term hold strategies, though buyers should still account for BSD recovery time and agent fees in any exit model.

Can I use CPF savings to buy commercial property?

No. The CPF Board permits Ordinary Account (OA) savings for residential property purchases and mortgage servicing only. Commercial, industrial, and retail properties are explicitly excluded. Commercial property buyers must fund the downpayment (typically 45% given the 55% LTV cap), all stamp duties, legal fees, and loan instalments entirely from cash. This constraint narrows the accessible buyer pool to investors with sufficiently liquid portfolios.

What is the difference between B1 and B2 industrial zoning?

The URA classifies industrial land as B1 (Business 1) or B2 (Business 2) based on the type of industrial activity and its environmental impact. B1 zones are for clean, light industrial uses compatible with nearby residential areas — such as food production, precision engineering, and high-value manufacturing. B2 zones permit heavier activities including warehousing, logistics, chemical processing, and metal fabrication. Buyers must ensure their intended use (or their tenant's use) is URA-compliant for the zone; non-compliant use can trigger enforcement action from URA and JTC, including lease termination in JTC-managed estates.

How is Annual Value (AV) assessed for commercial property tax purposes?

IRAS assesses Annual Value as the estimated annual rent the property would command in an open market, assuming the tenant pays for repairs and maintenance. For commercial properties, IRAS refers to market rental evidence from comparable transactions in the same street or building. Property owners who believe their AV has been over-assessed may file a formal objection with IRAS within 30 days of receiving the Valuation Notice. Successful objections result in a downward revision of AV and a corresponding reduction in annual property tax.

What stamp duty would a Singapore Citizen pay on a commercial property worth S$5 million?

BSD on a S$5 million commercial property: 1% on S$180,000 = S$1,800; 2% on S$180,000 = S$3,600; 3% on S$640,000 = S$19,200; 4% on S$500,000 = S$20,000; 5% on the remaining S$3,500,000 = S$175,000. Total BSD = S$219,600 (approximately 4.39% of purchase price). No ABSD applies, whether the buyer is a first-time Singapore Citizen or a foreign investor owning ten other properties. BSD must be paid to IRAS within 14 days of exercising the Option to Purchase.

Are there restrictions on subletting commercial property?

For freehold commercial property purchased in the open market, owners have broad freedom to let to any qualifying commercial tenant — subject to URA Master Plan use category compliance. For JTC-managed industrial properties on 30-year or 60-year JTC leases, additional use restrictions apply: the approved use is stated in the JTC lease, and subleasing to non-compliant tenants requires JTC written approval. Breach of use restrictions in JTC estates can result in financial penalties and, in serious cases, JTC exercising its right to re-enter the property.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer's Stamp Duty

- Singapore SSD Guide 2026: Seller's Stamp Duty Rates, History and Exemptions

- En Bloc Sale Singapore 2026: Collective Sales, 80% Consent and Owner Rights

- Singapore Property Succession Guide 2026: Wills, CPF Nominations and Joint Tenancy

- Singapore Housing Loan Guide 2026: HDB Loan, Bank Loan, TDSR and MSR

- Singapore Strata Title and MCST Guide 2026: Management Fees, By-Laws and En Bloc Rights

Disclaimer: This article is published for general educational purposes only and does not constitute legal, tax, or financial advice. Stamp duty rates, BSD tiers, LTV limits, and property tax rates are based on publicly available IRAS, MAS, and URA information as at July 2026 and may change without notice. Readers should consult a Singapore-qualified lawyer, IRAS-registered tax agent, or licensed financial adviser before making any commercial property investment decision. Price and yield data is indicative only and sourced from URA REALIS and JTC Corporation quarterly reports.