Singapore Private Property Buying Costs 2026: Complete All-In Cost Guide for Every Buyer Profile

- Buying private property in Singapore involves three stamp duties: Buyer’s Stamp Duty (BSD), Additional Buyer’s Stamp Duty (ABSD), and — for resale within 3 years — Seller’s Stamp Duty (SSD, paid by the seller).

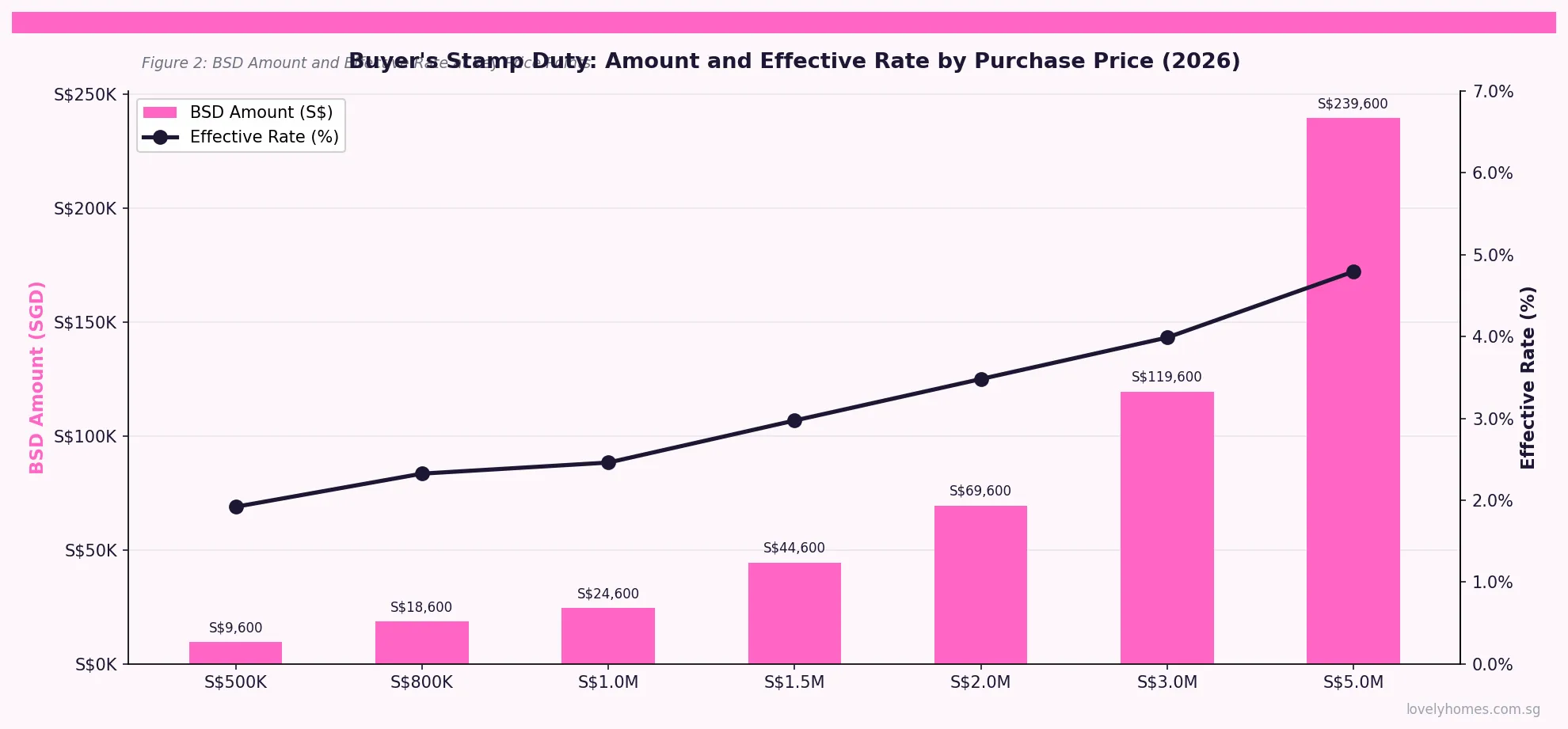

- BSD is payable by every buyer on every property purchase, at progressive rates of 1%–6% on the purchase price or market value, whichever is higher.

- ABSD ranges from 0% (Singapore Citizen first property) to 60% (foreigner) and is computed on the full price from the first dollar — it is not progressive.

- Beyond stamp duties, buyers face legal fees (est. S$2,500–S$5,000), valuation (S$500–S$2,000), and agent commission for resale purchases (typically 1% + 9% GST).

- The minimum cash downpayment for a private property bank loan is 5% of the purchase price; the total downpayment is 25% (5% cash + 20% cash or CPF).

- Ongoing costs after purchase include property tax (administered by IRAS), MCST maintenance fees, mortgage servicing, and insurance.

- All stamp duties must be paid within 14 days of exercising the Option to Purchase (OTP) or signing the Sale and Purchase Agreement (S&P), whichever is earlier.

What Are the Private Property Buying Costs in Singapore?

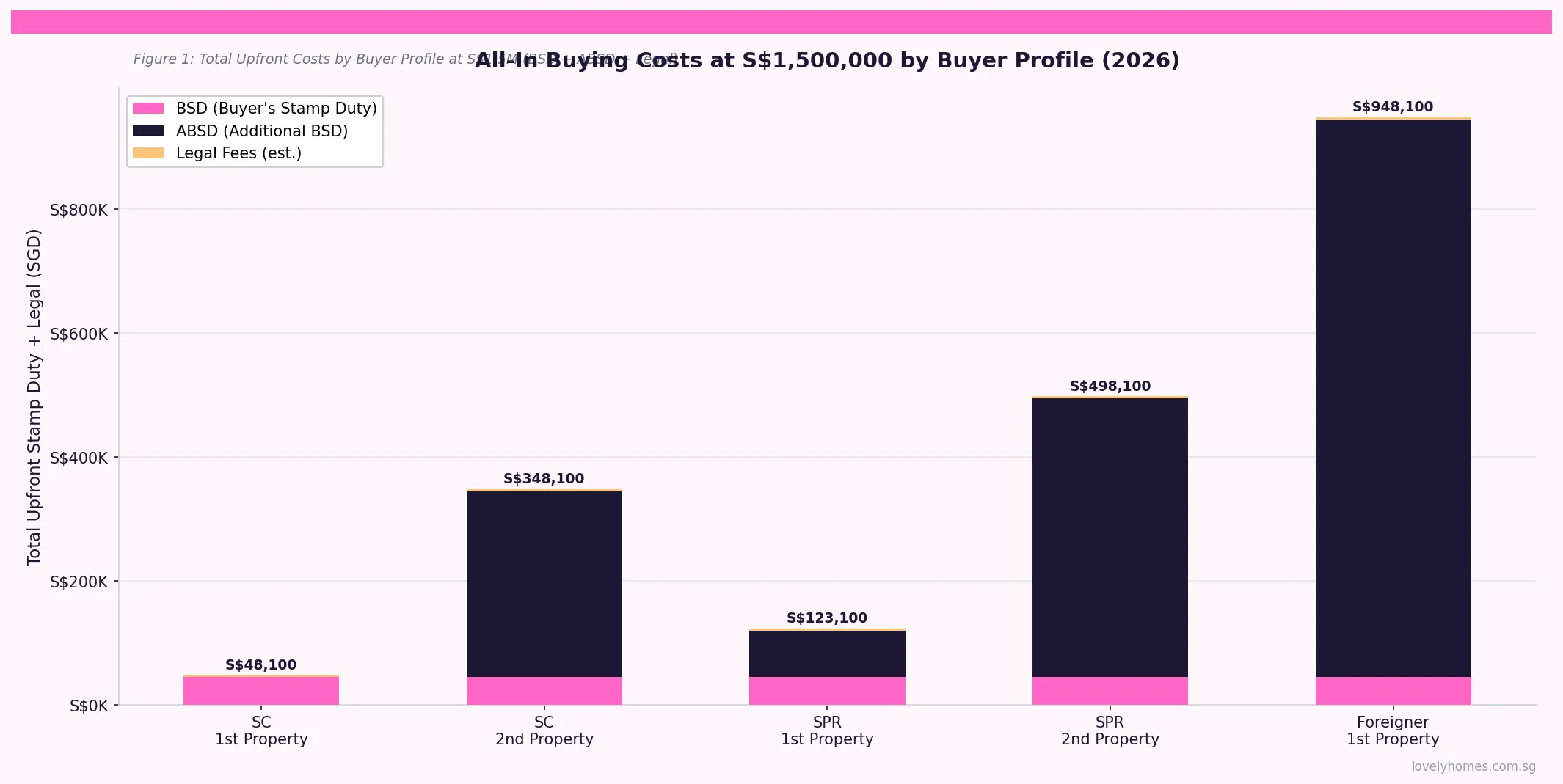

Purchasing private property in Singapore — whether a condominium, apartment, landed house, strata-titled shophouse, or commercial unit — involves a structured set of costs that go well beyond the headline purchase price. The Singapore government, through the Inland Revenue Authority of Singapore (IRAS), administers stamp duties that can represent a significant portion of the total outlay. For a foreigner buying a S$2 million condominium in 2026, the combined BSD and ABSD alone amount to S$1,269,600 — nearly two-thirds of the purchase price again.

This guide covers every material cost a private property buyer incurs in Singapore in 2026: upfront stamp duties, legal and professional fees, mortgage-related costs, and the ongoing holding costs that continue after completion. Costs are broken down for five buyer profiles — Singapore Citizen first property, Singapore Citizen second property, Singapore Permanent Resident (SPR) first property, SPR second property, and foreigner — at representative price points.

Buyer’s Stamp Duty (BSD): What Every Buyer Pays

BSD is a compulsory tax administered by IRAS on every property purchase in Singapore. It applies to all buyers regardless of nationality, residency status, or how many properties they own. It is computed on the higher of the purchase price or the property’s market value as assessed by IRAS.

BSD uses a progressive rate structure. The rates for residential property in 2026 are:

| Portion of Value | BSD Rate | BSD on This Band |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 (S$180K–S$360K) | 2% | S$3,600 |

| Next S$640,000 (S$360K–S$1.0M) | 3% | S$19,200 |

| Next S$500,000 (S$1.0M–S$1.5M) | 4% | S$20,000 |

| Next S$1,500,000 (S$1.5M–S$3.0M) | 5% | S$75,000 |

| Amount exceeding S$3,000,000 | 6% | Varies |

Using the above schedule, BSD on a S$1,500,000 purchase is S$44,600 (effective rate 2.97%); on a S$2,000,000 purchase it is S$69,600 (effective rate 3.48%); on a S$3,000,000 purchase it is S$119,600 (effective rate 3.99%). BSD is due to IRAS within 14 days of the Option to Purchase being exercised (or the date of the contract, whichever is earlier). Late payment attracts a penalty of 5% per annum on the unpaid amount.

BSD can be paid from CPF Ordinary Account (OA) funds, provided the property is residential and the CPF member is eligible. Most buyers use a combination of CPF OA and cash.

Additional Buyer’s Stamp Duty (ABSD): The Nationality and Ownership Surcharge

ABSD is a flat-rate stamp duty levied on top of BSD, applied as a percentage of the full purchase price from the first dollar. Unlike BSD, ABSD is not progressive — the stated rate applies to the entire price. ABSD rates are determined by the buyer’s citizenship status and the number of residential properties they own at the time of purchase. The 2026 ABSD schedule, unchanged since the April 2023 round of cooling measures, is:

| Buyer Profile | 1st Property | 2nd Property | 3rd+ Property |

|---|---|---|---|

| Singapore Citizen | 0% | 20% | 30% |

| Singapore Permanent Resident | 5% | 30% | 30% |

| Foreigner (including most work pass holders) | 60% | 60% | 60% |

| Entity (company, trust, collective investment scheme) | 65% | 65% | 65% |

| Developer (housing developer licence) | 35% (remittable on completion conditions) | — | — |

What counts as “owning” a property for ABSD purposes? IRAS counts every residential property in Singapore in which you hold a legal or beneficial interest — including properties held jointly or as a co-owner, properties held through a trust, and properties inherited (even if you did not pay for them). Overseas property does not count. If you are a SC buying your second property, you will pay 20% ABSD on the full purchase price — S$300,000 on a S$1.5M purchase.

ABSD must also be paid within 14 days of exercising the OTP (or signing the S&P). Unlike BSD, ABSD cannot be paid from CPF — it must be paid entirely in cash. This is a crucial planning consideration for second-property buyers who may be CPF-rich but cash-light.

One key relief: Singapore Citizen married couples who own one residential property jointly may apply for ABSD remission when they sell the first property within 6 months of buying a new one. This remission restores the SC couple to effectively 0% ABSD on the second purchase. The 6-month clock starts from the completion of the new purchase.

Seller’s Stamp Duty (SSD): A Reminder for Buyers Who May Resell Quickly

Buyers should also be aware of the Seller’s Stamp Duty (SSD), which applies if the property is resold within three years of acquisition. SSD is paid by the seller, but it affects the resale market because sellers typically factor it into their pricing:

- Sold within 1 year: 12% SSD

- Sold within 2 years: 8% SSD

- Sold within 3 years: 4% SSD

- Sold after 3 years: 0% SSD

For buyers who contemplate flipping a property within 3 years, the combined SSD exposure can make the transaction economically unattractive. Planning a minimum 3-year hold eliminates SSD entirely.

Professional and Transaction Fees

Beyond stamp duties, buyers incur a set of professional fees for the conveyancing and mortgage process:

| Fee Item | Typical Range | Who Pays | Notes |

|---|---|---|---|

| Legal fees (conveyancing — buyer’s solicitor) | S$2,500–S$5,000 | Buyer | Higher for complex transactions; covers OTP, S&P, title search, SLA registration |

| Valuation fee | S$500–S$2,000 | Buyer | Required by bank for mortgage; Singapore Institute of Surveyors and Valuers (SISV) accredited valuer |

| Mortgage processing fee | S$0–S$500 | Buyer | Many banks waive this; check with your lender |

| Agent commission (resale purchase) | 1%–2% + 9% GST | Buyer | Not mandatory; buyer’s agent commission is separately negotiated. New launches: 0% (developer pays co-broke) |

| Property tax (pro-rated at completion) | Varies | Shared at completion | Seller reimburses buyer for unused portion of pre-paid property tax |

Downpayment and Loan Structure

For private property financed by a bank loan, MAS mandates a minimum downpayment of 25% of the purchase price (or market value, whichever is lower). The breakdown is:

- 5% must be paid in cash (the Option Exercise Fee of 1% + the balance of 4% at exercise, or 5% at S&P signing for new launches)

- The remaining 20% can be paid from CPF Ordinary Account, cash, or a combination

- 75% maximum LTV (Loan-to-Value) — i.e., the bank loan covers up to 75% of the lower of price or value

For a second property, the LTV ceiling drops to 45%, meaning a downpayment of 55% — with a minimum of 25% in cash. For a third or subsequent property, the LTV is 35%, with a minimum 25% cash downpayment. MAS’s TDSR (Total Debt Servicing Ratio) framework caps total monthly debt obligations (including the new mortgage) at 55% of gross monthly income.

Ongoing Ownership Costs After Completion

The upfront costs are only part of the picture. Once you own the property, several recurring costs apply:

| Ongoing Cost | Typical Annual Amount | Administered By |

|---|---|---|

| Property Tax | S$0–S$20,000+ (depends on AV and usage) | IRAS |

| MCST Maintenance Fees (condo) | S$3,000–S$30,000 (S$250–S$2,500/mth) | MCST (management corporation) |

| Sinking Fund Contributions | Included in MCST fees (10% of maintenance) | MCST |

| Fire Insurance (mandatory for mortgaged property) | S$100–S$400 | Insurer (MAS-regulated) |

| Home Contents Insurance | S$200–S$800 | Optional; insurer |

| Utilities (electricity, water, gas) | S$2,400–S$7,200 (S$200–S$600/mth) | SP Group, PUB |

| Mortgage Servicing | Based on loan amount, tenure, rate | Bank (MAS-regulated) |

Property tax is computed by IRAS on the property’s Annual Value (AV) — a notional figure representing the estimated annual rent the property would fetch unfurnished. Owner-occupied residential properties enjoy concessionary progressive rates starting at 0% on the first S$8,000 of AV. Investment or rented-out properties face higher non-owner-occupier rates. From 2025, IRAS adopted new AV ranges following a property market review.

Worked Example: The Rajan Family’s Private Property Purchase

Scenario: SC Joint Purchase, Second Property at S$2,100,000

Mr Rajan (Singapore Citizen) and Mrs Rajan (Singapore Citizen) currently own a Bishan HDB flat which they plan to sell within 6 months. They are buying a 3-bedroom resale condominium in District 15 (Marine Parade / East Coast) at S$2,100,000. Because they still own the HDB, ABSD at the SC second-property rate of 20% applies upfront; they will apply for ABSD remission after selling the HDB.

| Cost Item | Amount | Notes |

|---|---|---|

| Purchase Price | S$2,100,000 | Market value confirmed S$2,100,000 |

| BSD | S$74,600 | 1%/2%/3%/4%/5% progressive; S$44,600 (on S$1.5M) + S$30,000 (5% × S$600K above S$1.5M) |

| ABSD (20% — SC 2nd property) | S$420,000 | Paid upfront in cash; ABSD remission applied after HDB sold within 6 months |

| ABSD Remission (refund after HDB sale) | -S$420,000 | Applied to IRAS within 6 months of completing new purchase; HDB must be sold first |

| Legal Fees (buyer) | S$3,500 | Conveyancing, SLA registration, title search |

| Valuation Fee | S$800 | Bank-appointed SISV valuer |

| Agent Commission (1% + 9% GST) | S$22,890 | Buyer’s agent for resale purchase |

| Downpayment (25% of S$2.1M) | S$525,000 | 5% cash S$105,000 + 20% CPF/cash S$420,000 |

| Bank Loan (75% LTV) | S$1,575,000 | @3.0% p.a., 30-year tenure, monthly S$6,639 |

| TDSR Check | S$6,639 / S$12,000 = 55.3% | At the TDSR 55% ceiling — couple must clear any other debt obligations before completing |

| Net upfront cash outlay (before ABSD refund) | S$626,790 | BSD + ABSD + legal + val + agent + 5% cash DP |

| Net upfront after ABSD remission | S$206,790 | After S$420,000 ABSD refund once HDB sold within 6 months |

Key risk: Mr and Mrs Rajan must sell the HDB within 6 months of completing the D15 purchase to qualify for ABSD remission. If they miss the window, the S$420,000 ABSD is forfeited. The transaction should be sequenced carefully with both their agent and solicitor to ensure the disposal timeline is locked in before exercising the OTP on the new purchase.

What This Means for Private Property Buyers in 2026

Singapore’s private property buying cost structure is deliberately designed to differentiate between residents buying their home and investors — domestic or foreign — seeking to accumulate property. The ABSD regime effectively creates three distinct cost environments: near-zero cost for SC first-timers; a moderate but significant surcharge for SC second-timers and SPR first-timers; and a prohibitively high 60% surcharge for foreigners.

In a peer-country comparison, Singapore’s residential property stamp duty regime is among the steepest globally for non-resident investors. Hong Kong’s stamp duty for non-permanent residents stands at 15%; Canada’s foreign buyers’ tax varies by province. Singapore’s 60% ABSD, introduced in April 2023, is explicitly designed to insulate the domestic housing market from speculative capital inflows.

For Singaporeans buying their first private property, the cost structure is relatively benign: BSD of 2.97%–3.99% at S$1.5M–S$3M is comparable to transaction costs in other major cities. The MCST fees, property tax, and financing costs are the recurring burden that deserves more careful modelling — a S$4,000/month mortgage, S$800/month MCST, and S$400/month property tax creates an all-in occupancy cost of S$5,200/month before utilities, which must be assessed against the TDSR of the purchasing household.

What Might Come Next

The following is editorial speculation and should not be relied upon for financial decisions.

The current ABSD regime, introduced in April 2023, has been in force for over three years. In that period, private residential transaction volumes involving foreigners have fallen dramatically. Some industry observers have speculated that the government may consider a modest easing of the foreigner rate if volumes remain suppressed to a degree that affects market liquidity in the luxury segment. However, the government has given no signal of any impending change, and Singapore’s housing policy framework has historically prioritised stability over volume. Any adjustment to ABSD would be announced by MND (Ministry of National Development) and MOF (Ministry of Finance) jointly and implemented immediately at announcement — there is no advance notice period.

Frequently Asked Questions

Can I pay ABSD using CPF Ordinary Account funds?

No. ABSD must be paid entirely in cash. Unlike BSD, which can be paid from your CPF OA for a residential property purchase, ABSD is not an allowable CPF withdrawal purpose. This makes ABSD a significant liquidity consideration for buyers who are CPF-rich but cash-light — for example, a Singapore Citizen buying a second property at S$1.5M would need S$300,000 in cash for ABSD alone, on top of the 5% cash downpayment of S$75,000, totalling S$375,000 in cash before legal fees.

What is the 14-day stamp duty deadline and what happens if I miss it?

BSD and ABSD must be paid to IRAS within 14 calendar days of the date you exercise the Option to Purchase (OTP) or sign the Sale and Purchase Agreement (S&P), whichever is earlier. For new launches, it is typically 14 days from the date of the S&P. If you miss this deadline, IRAS charges a penalty of 5% per annum on the unpaid stamp duty, accruing daily. For large ABSD amounts, even a few days’ delay can cost thousands of dollars in penalties. Your solicitor should be engaged well before the OTP exercise date to ensure the stamping is completed in time.

I am a foreigner but my spouse is a Singapore Citizen. Do we still pay 60% ABSD?

Yes and no. If you and your Singapore Citizen spouse are purchasing the property jointly, ABSD is charged at the rate applicable to the buyer with the highest ABSD liability — which in this case would be 60% for the foreigner. However, since 16 February 2023, there is no longer an ABSD remission for married couples with mixed citizenship (one SC and one foreigner) purchasing their first jointly-owned residential property. The full 60% ABSD applies. One common planning approach is for the SC spouse to purchase the property solely in their own name, in which case no ABSD applies (for their first property). This creates financing and ownership planning considerations that should be discussed with a solicitor.

Is valuation mandatory for all private property purchases?

Valuation is not required by law for every purchase, but it is effectively mandatory whenever you take a bank loan — the bank will appoint its own panel valuer to determine the market value before approving the LTV ratio. If the bank valuation comes in below the purchase price, the LTV is calculated on the lower valuation figure, meaning you must make up the difference in cash. For cash purchases, valuation is optional but advisable for ABSD calculation purposes (ABSD is charged on the higher of price or market value). IRAS can independently assess market value and charge ABSD accordingly.

Can I avoid paying agent commission as a buyer?

For new launch condominiums, developers typically pay the buyer’s agent commission through their co-broke arrangement; buyers pay no direct commission. For resale private properties, a buyer’s agent commission is customary (typically 1% + 9% GST) but not legally mandated. You may choose to transact without a buyer’s agent and negotiate directly with the seller’s agent; however, the seller’s agent represents the seller’s interests, not yours. CEA (Council for Estate Agencies) guidelines distinguish clearly between representing one or both parties. Using a buyer’s agent generally costs 1% but provides representation, market data, and negotiation support.

What ongoing property tax will I pay on a S$2M condominium?

Property tax is based on the Annual Value (AV) — IRAS’s estimate of the annual market rent the property could command, unfurnished. For a S$2M condominium, the AV might be approximately S$48,000–S$60,000 per annum depending on location and unit size. For owner-occupiers, the 2026 progressive rate yields approximately S$2,400–S$4,000/year at those AV levels. For non-owner-occupiers (renting out the unit), the non-OO rates apply and the annual property tax can be S$8,000–S$14,000 on the same AV. Check the IRAS property tax calculator at iras.gov.sg for an accurate estimate for your specific property.

For a new launch, when exactly do I pay BSD and ABSD?

For a new private residential launch, you typically pay a 5% booking fee to the developer upon selecting your unit (this secures the unit). BSD and ABSD are due within 14 days of signing the Sale and Purchase Agreement (S&P), which is typically issued 8 to 12 weeks after the booking date. This means you have roughly 2–3 months from booking to arrange the stamp duty cash — but do not leave it late. Your solicitor will handle the stamping electronically via IRAS e-Stamping and will liaise directly with IRAS on the calculation.