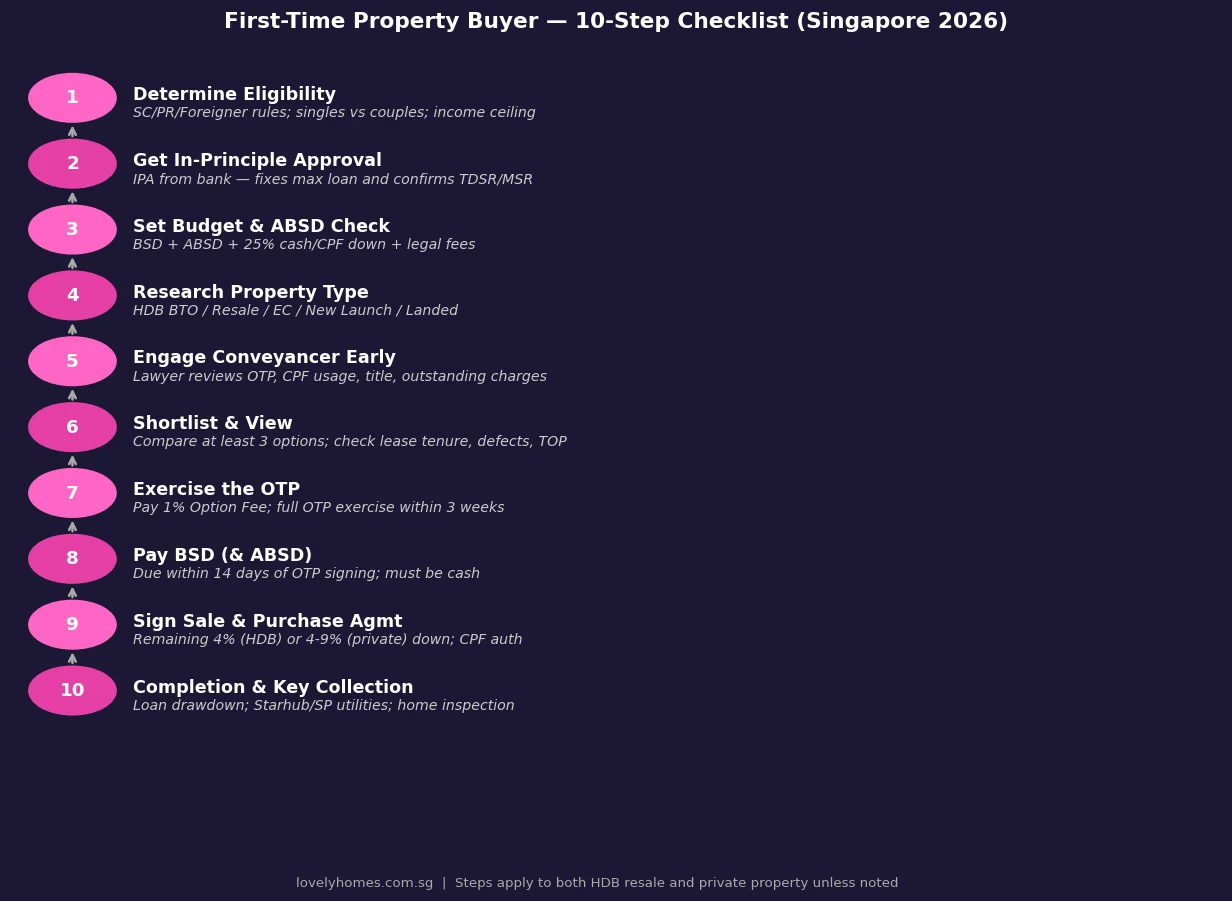

Singapore Home Loan Complete Guide 2026: HDB Loans, Bank Loans, TDSR, MSR and Best Rates Explained

Quick Answer — Singapore Home Loans at a Glance (2026)

- Two main options: HDB Concessionary Loan (2.6% p.a., LTV 80%) and Bank Loan (~3.0–3.7% p.a., LTV 75%).

- MSR caps your HDB or EC loan instalment at 30% of gross income; TDSR caps all debt at 55% of income.

- Bank loans require a minimum 5% cash downpayment; HDB loans require 5% cash on the 20% downpayment portion.

- Floating-rate loans are pegged to SORA (Singapore Overnight Rate Average) — 3M SORA ~2.4% at June 2026.

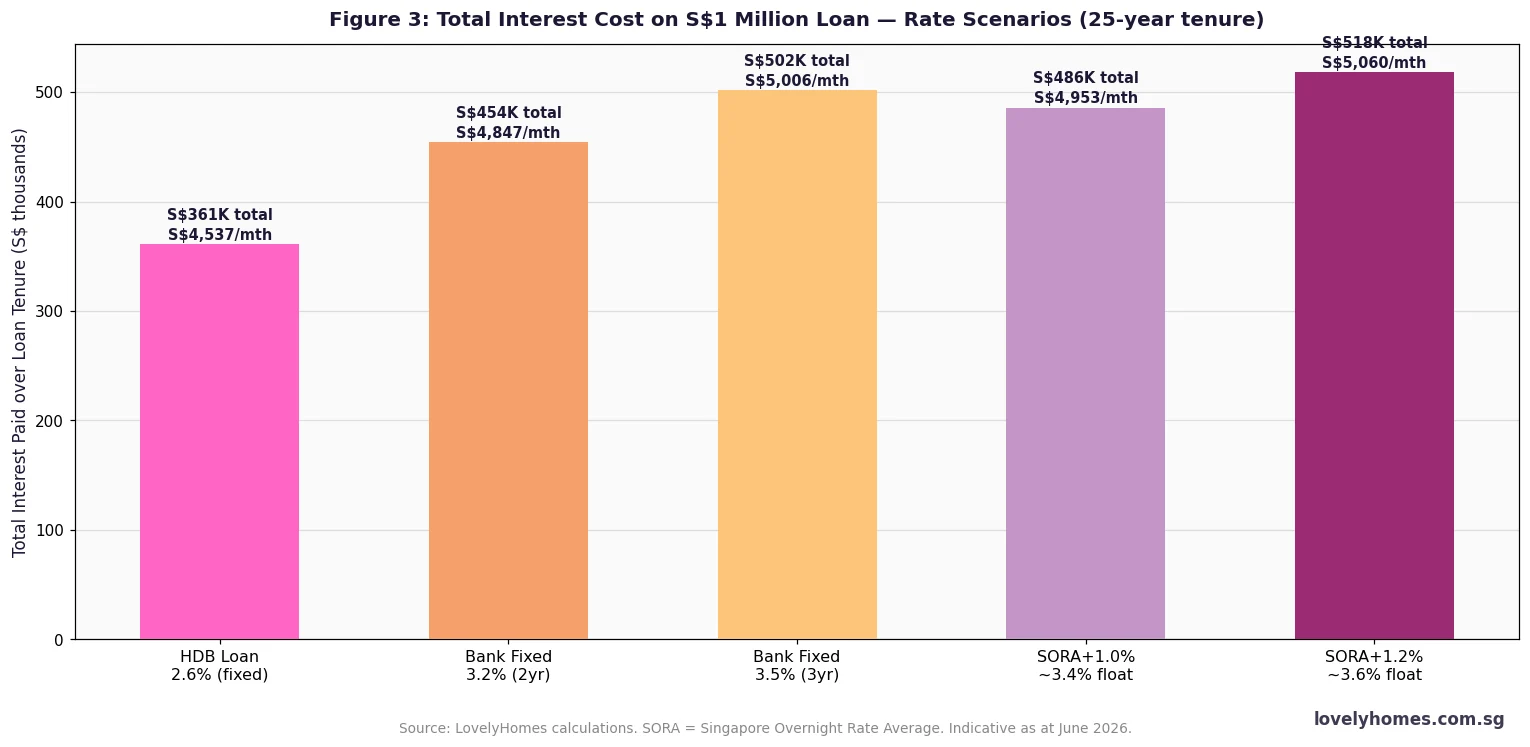

- A S$1 million loan at 3.5% over 25 years costs S$85,000 more in total interest than at 2.6%.

- Lock-in periods of 1–3 years are standard on bank fixed-rate packages; exiting early triggers a clawback of ~1.5% of the outstanding loan.

- Refinancing after the lock-in expires can save tens of thousands; always compare at least 3 banks’ packages.

What Is a Home Loan and Why Does the Structure Matter?

A home loan (or housing loan) is a secured credit facility from a lender — either the Housing and Development Board or a licensed bank — that allows you to finance the purchase of a residential property in Singapore. The property serves as collateral; if you default, the lender can repossess and sell it to recover the outstanding debt.

The structure matters because small differences in interest rate, tenure, and loan-to-value ratio compound dramatically over a 25–30-year horizon. A 0.9 percentage point difference (say, 2.6% vs 3.5%) on a S$600,000 HDB loan over 25 years translates to roughly S$51,000 in additional interest. That is not a minor detail. Beyond the rate, two Monetary Authority of Singapore (MAS) rules govern how much you can borrow: the Mortgage Servicing Ratio (MSR) for HDB and Executive Condominium (EC) purchases, and the Total Debt Servicing Ratio (TDSR) for all property loans.

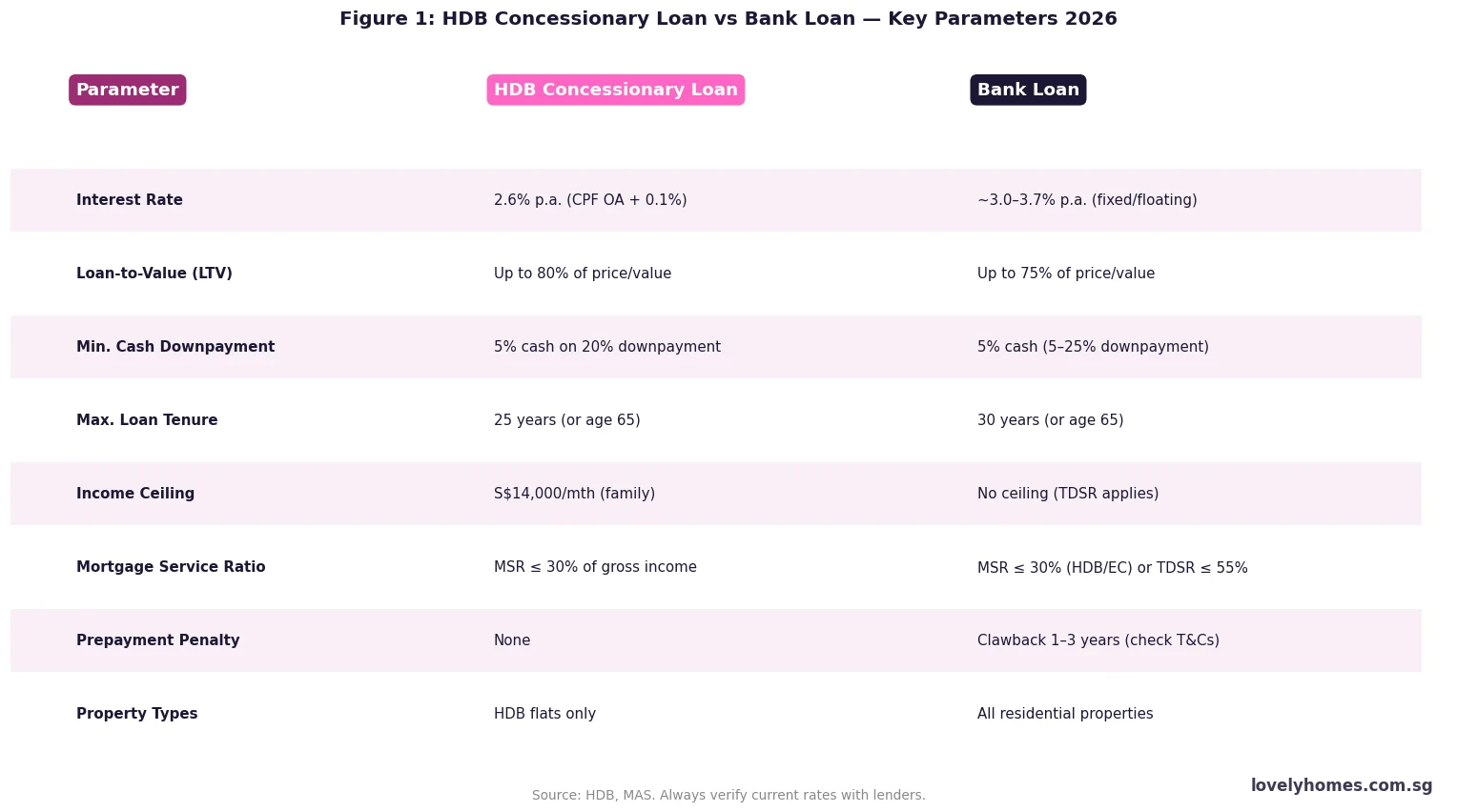

HDB Concessionary Loan vs Bank Loan — The Key Differences

Every Singapore home buyer faces the same first question: HDB loan or bank loan? Each has distinct advantages and constraints. The comparison below sets out the essential differences.

The HDB loan rate of 2.6% p.a. is fixed at 0.1% above the CPF Ordinary Account (OA) rate of 2.5%. It moves only if the CPF OA rate changes — which has not happened since July 1999. Bank loans fluctuate with market rates. At June 2026, the best 2-year fixed bank packages sit at approximately 3.0–3.2% p.a., while SORA-pegged floating packages range from SORA+0.75% to SORA+1.20% (3M SORA ~2.4%, implying ~3.15–3.60% all-in).

HDB Concessionary Loan — Eligibility and Key Rules

To qualify for the HDB loan, at least one buyer must be a Singapore Citizen; the household gross income must not exceed S$14,000 per month (families) or S$7,000 (singles); and no buyer may currently own or have disposed of private property in the 30 months before the flat application. You also need a valid HDB Flat Eligibility (HFE) letter — a mandatory pre-application document from HDB confirming your loan eligibility, CPF grant entitlement and maximum loan quantum (mandatory since May 2023, valid for 9 months).

The maximum loan under the HDB loan is 80% of the lower of the purchase price or valuation. On a S$700,000 flat that is S$560,000. The remaining 20% (S$140,000) is the downpayment — at least 5% (S$35,000) must be cash; the rest may come from CPF OA.

Bank Loans — LTV, Lock-in and SORA

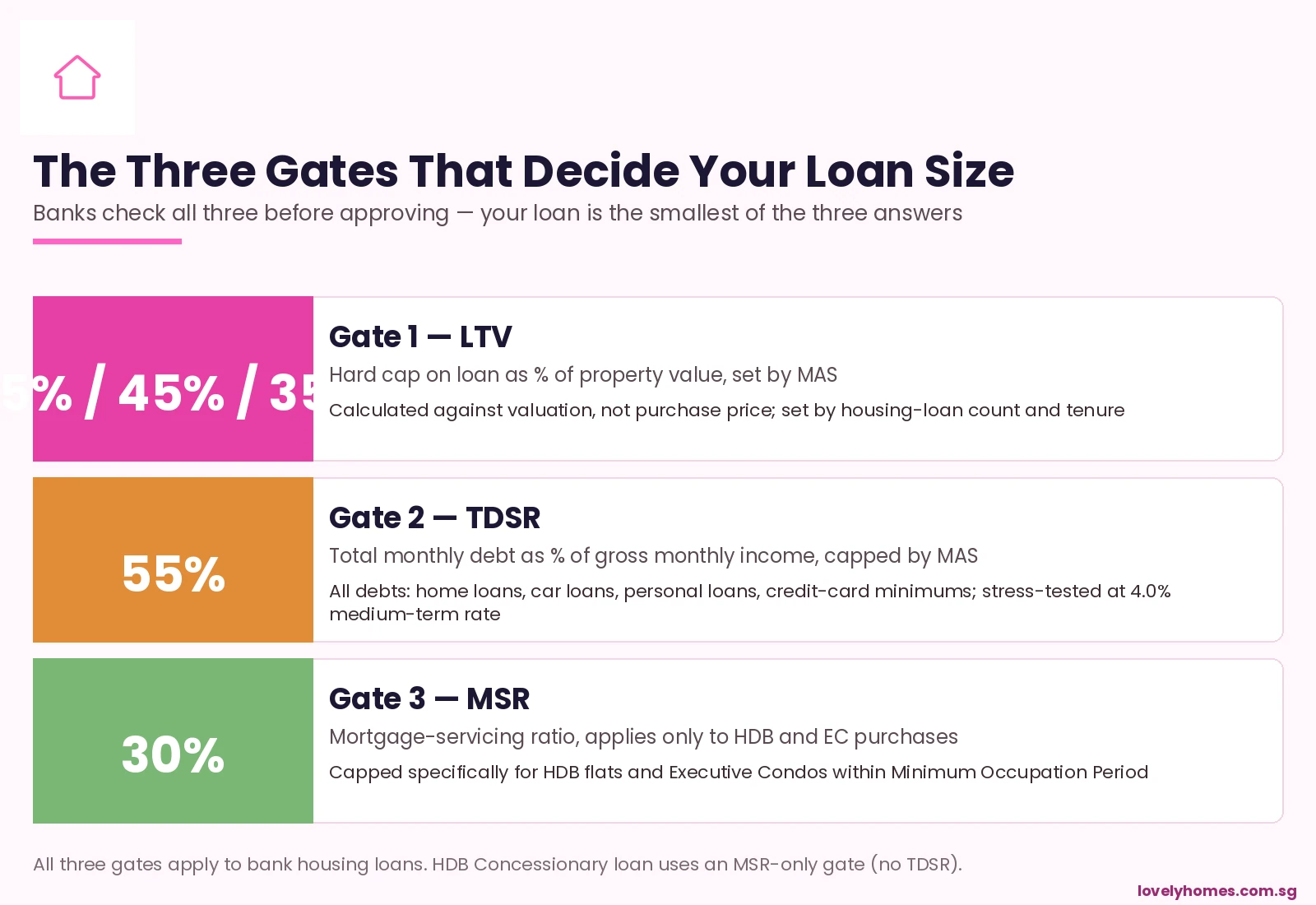

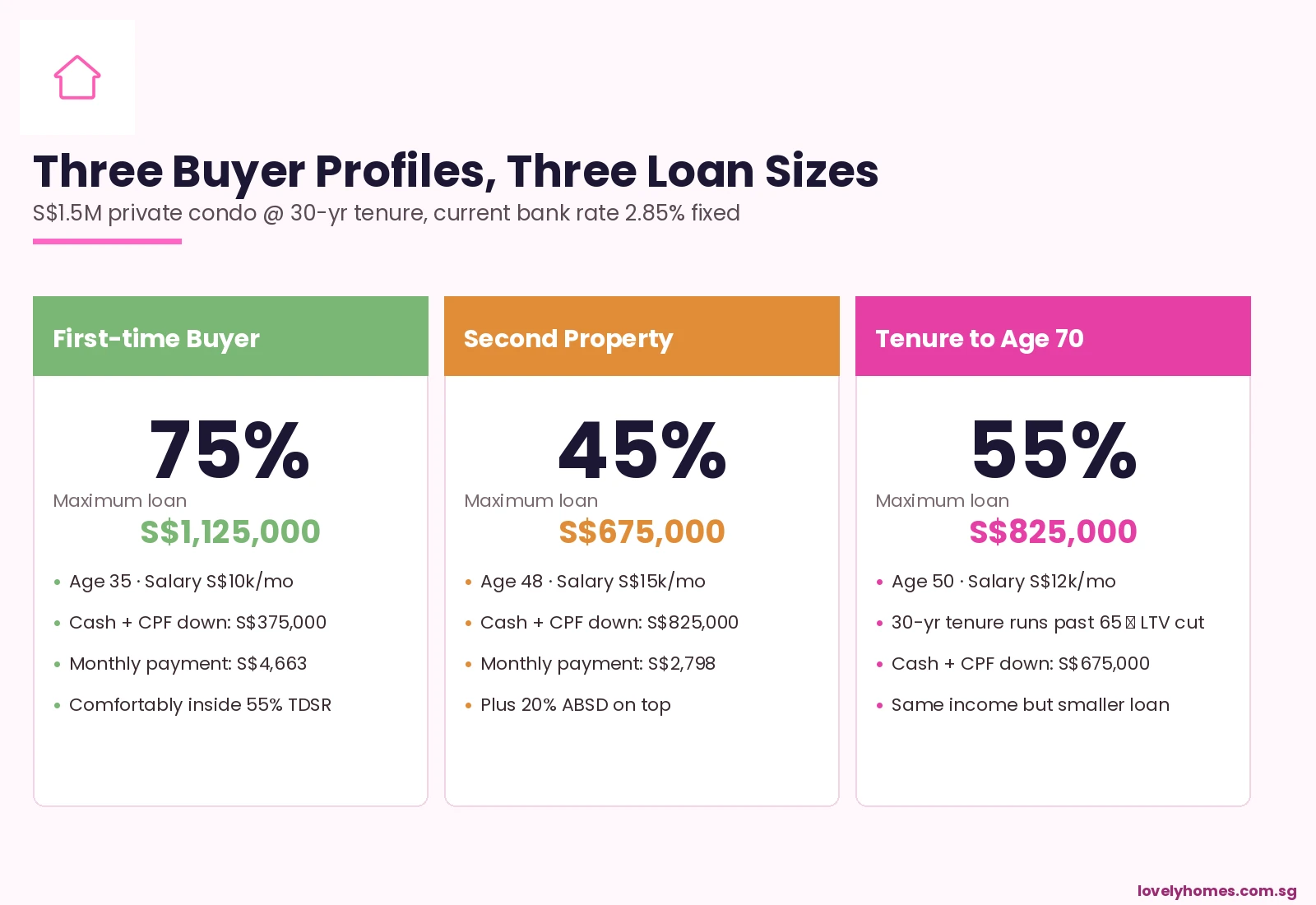

Bank loans allow a longer maximum tenure (30 years vs 25 years), access to all property types, and — potentially — lower rates during low-rate periods. The trade-off is variability and the lock-in period. Most bank fixed rates carry a lock-in of 1–3 years, after which the loan reprices to a floating SORA-pegged rate. The Loan-to-Value (LTV) for a bank loan is 75% if you have no outstanding loans; 45% if you have one; 35% if two or more. SORA replaced SIBOR as the benchmark rate on 1 October 2024 following the MAS phase-out of SIBOR.

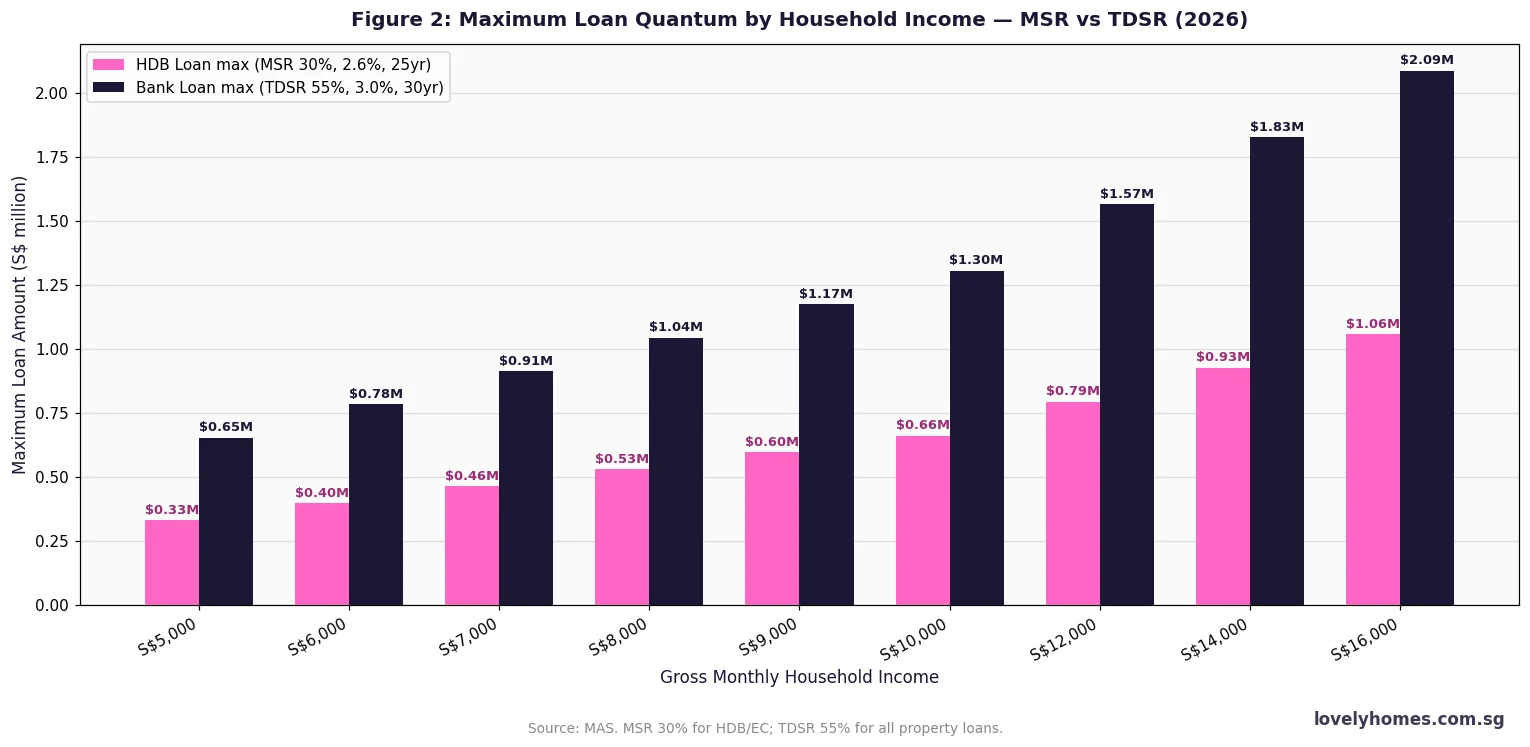

MSR and TDSR — How Much Can You Actually Borrow?

The MAS introduced the TDSR framework in June 2013 and has maintained it as the primary constraint on borrowing. For HDB and EC purchases, the MSR applies as a tighter cap.

- TDSR ≤ 55%: Total monthly debt obligations — home loan plus all other debts — must not exceed 55% of gross monthly income.

- MSR ≤ 30%: For HDB and EC purchases only — the monthly home loan repayment alone must not exceed 30% of gross monthly income.

A household earning S$10,000 per month can borrow up to approximately S$826,000 on an HDB loan (MSR 30% at 2.6% p.a. over 25 years) or up to S$1,514,000 under TDSR on a bank loan for private property (55% at 3.0% p.a. over 30 years). The MSR is the binding constraint for HDB buyers; TDSR is the constraint for private property buyers.

Fixed Rate vs Floating Rate (SORA) — Which Is Better?

Fixed-rate packages offer certainty: the rate is locked for 2–3 years. After the lock-in, the loan reverts to a floating rate and you may reprice or refinance. Breaking the lock-in early triggers a clawback penalty of approximately 1.0–1.75% of the outstanding loan.

Floating-rate packages pegged to 3M compounded SORA move with the market. When rates fall, your instalment falls. When rates rise (as they did sharply in 2022–2023), your instalment rises. Floating packages currently sit at SORA + 0.75%–1.20%.

The chart shows the cost differential starkly. The HDB loan at 2.6% costs approximately S$377,000 in total interest over 25 years on a S$1 million loan. A bank fixed rate at 3.5% costs S$462,000 — a S$85,000 difference. For buyers of private property or ECs using bank financing, the choice between fixed and floating hinges on your rate outlook and risk tolerance.

CPF and Home Loan Financing

Most Singapore buyers use their CPF Ordinary Account (OA) to service instalments and fund the downpayment. The rules are set by the Central Provident Fund Board under the CPF Act (Cap 36). The key constraints are the Valuation Limit (VL) — the lower of price or valuation — and the Withdrawal Limit (WL), which is 120% of the VL. CPF OA can be used freely up to the VL; above the VL up to the WL only if you have set aside the Basic Retirement Sum (S$106,500 in 2026) in your CPF accounts.

A critical point: when you sell the property, you must refund to CPF the total principal withdrawn plus accrued interest at 2.5% p.a. This is not a penalty — it restores your retirement savings — but it reduces net cash proceeds from sale. See our CPF Property Withdrawal Limits 2026 guide for detail.

Summary Table — Singapore Home Loan Framework 2026

| Parameter | HDB Concessionary Loan | Bank Loan (HDB/EC) | Bank Loan (Private) |

|---|---|---|---|

| Rate (Jun 2026) | 2.6% p.a. fixed | ~3.0–3.7% p.a. | ~3.0–3.7% p.a. |

| Loan-to-Value | 80% | 75% | 75% |

| MSR Cap | ≤ 30% | ≤ 30% | N/A |

| TDSR Cap | ≤ 55% | ≤ 55% | ≤ 55% |

| Max Tenure | 25 years (age 65) | 30 years (age 65) | 30 years (age 65) |

| Min Cash Down | 5% of price | 5% of price | 5% of price |

| Lock-in / Clawback | None | 1–3 yr clawback | 1–3 yr clawback |

| Property Types | HDB flats only | HDB + EC | All types |

Worked Example — Mr & Mrs Wong Buying Bishan 4-Room HDB Resale

Mr & Mrs Wong are a Singapore Citizen couple. Joint gross income: S$9,500 per month. They plan to purchase a 4-room HDB resale flat in Bishan at S$680,000. This is their first property. They hold S$90,000 combined CPF OA. They qualify for an Enhanced Housing Grant (EHG) of S$60,000 (income S$9,001–S$10,000) and a Proximity Housing Grant (PHG) of S$30,000 (parents within 4 km). Total housing grants: S$90,000.

- Purchase price: S$680,000

- HDB Loan (80% LTV): S$544,000

- Downpayment (20%): S$136,000 — CPF OA S$90,000 + cash S$46,000

- Grants applied: S$90,000 (EHG + PHG) — reduces net purchase price

- Monthly instalment (2.6%, 25yr): S$2,468/month

- MSR check: S$2,468 ÷ S$9,500 = 26.0% — PASS (threshold 30%)

- Buyer’s Stamp Duty (BSD): 1% × S$180k + 2% × S$180k + 3% × S$320k = S$15,000

- Legal fees: ~S$2,800 | HDB caveat: S$64.45

- ABSD: Nil (SC first property)

- Total cash outlay: ~S$46,000 (downpayment cash) + S$15,000 (BSD) + S$2,800 (legal) = ~S$63,800

The HDB loan is the clear choice here: the 2.6% fixed rate is materially cheaper than any bank offering in June 2026, the couple meets the S$14,000 income ceiling comfortably, and the S$90,000 grants significantly reduce the net outlay. Total cost of ownership over 25 years at 2.6%: approximately S$680,000 principal + S$200,000 interest + S$63,800 upfront costs = S$943,800 in total expenditure on a flat that, based on OCR HDB price growth of ~10% per year over the past 5 years, may be worth substantially more at resale.

Refinancing and Repricing — When and How

Repricing means switching to a new package with your existing bank; refinancing means moving to a new lender. Refinancing is generally more powerful but involves legal fees of S$1,800–S$3,500 and a valuation fee of S$200–S$500. Most banks offer cashback of S$1,800–S$2,000 to offset these costs. The optimal window to refinance is 3–6 months before your lock-in expires. Never refinance within the lock-in unless savings clearly outweigh the clawback penalty.

What to Watch in H2 2026

3M SORA has been stable at approximately 2.3–2.5% since early 2026 as global central banks paused tightening. The key variable remains the US Federal Reserve: any cut flows through to SORA within weeks. For buyers who value certainty, a 2-year fixed package now locks in June 2026 rates. For buyers expecting rates to fall over the next 12–18 months, a floating SORA package may deliver lower effective payments over the loan lifecycle. The prudent approach regardless: stress-test your affordability at a rate 1.5–2.0 percentage points above your current package rate.

Frequently Asked Questions

Can I switch from an HDB loan to a bank loan after purchasing?

Yes. You can refinance from the HDB loan to a bank loan at any time after the HDB loan is active — there is no lock-in or clawback on the HDB side. You will need a conveyancing lawyer to discharge the HDB mortgage and register the bank mortgage. Bank loans typically cover 75% LTV, so if your outstanding HDB loan balance is below 75% of the current valuation, it can be fully refinanced. Note: once you switch to a bank loan, you cannot switch back to the HDB loan.

What happens if SORA rises sharply on my floating-rate loan?

Floating-rate borrowers bear the full rate risk. A 1 percentage point rise in SORA increases the monthly instalment on a S$600,000 loan (30yr) by approximately S$300. MAS requires banks to stress-test borrowers at a floor of 3.5% or contractual rate plus 1%, whichever is higher — so your loan was approved assuming you can handle a rate rise. Budget a meaningful buffer above your starting instalment.

Can I use CPF to pay stamp duty?

BSD and ABSD must be paid in cash within 14 days of signing the OTP. After payment, you may apply for CPF reimbursement from your OA. The initial cash payment is mandatory. This is a common cash-flow surprise: on a S$680,000 HDB flat, BSD is approximately S$15,000 cash on top of the downpayment.

What is the difference between repricing and refinancing?

Repricing means switching packages with your current lender (processing fee S$0–S$800; limited to that bank’s offerings). Refinancing means moving to a new lender (legal fees S$1,800–S$3,500; access to the full market). Refinancing is generally more effective but involves more paperwork and a 1–3 month processing window. Cashbacks from new lenders typically offset legal costs.

Does my car loan or personal loan reduce how much I can borrow for a home?

Yes — under TDSR, all outstanding debt obligations count against your 55% cap. A car loan of S$1,200/month and personal loan of S$500/month on a S$10,000/month income household reduces the permissible home loan instalment to S$3,800/month (55% × S$10k − S$1,700). MAS allows a 30% haircut on variable income (bonuses, commissions) when computing TDSR.

Can a foreigner get a home loan in Singapore?

Yes — foreigners can obtain bank loans for Singapore private residential property. The HDB loan is available only to eligible Singapore Citizens and Permanent Residents buying HDB flats. Note that foreigners purchasing private residential property pay 60% ABSD as at 2026 — see our ABSD guide for the full rate table. Bank loans for foreigners follow the same LTV and TDSR framework, though some banks may apply slightly stricter income documentation requirements for non-residents.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty 2026: BSD, ABSD, SSD and ACD Explained

- CPF Property Withdrawal Limits 2026: Valuation Limit and Accrued Interest Explained

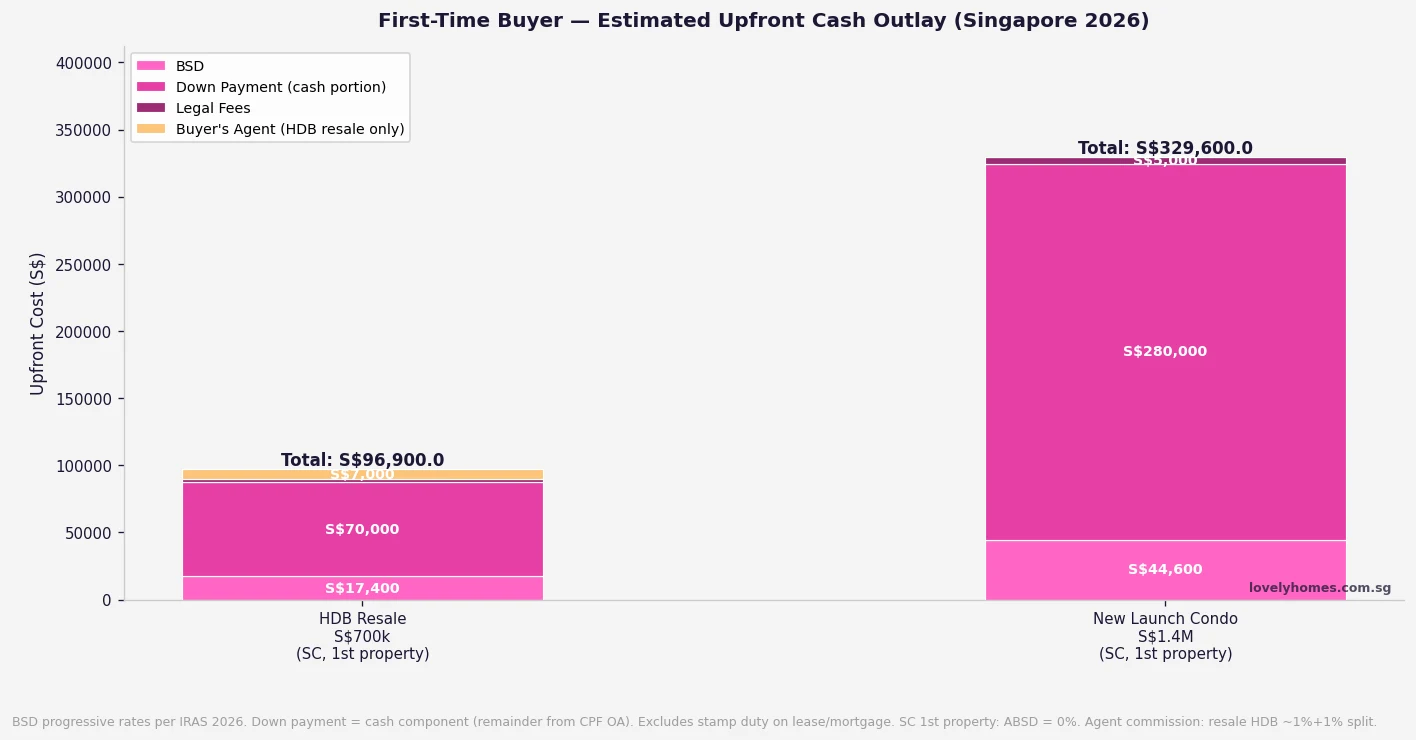

- First-Time Property Buyer Guide Singapore 2026

- Singapore HDB Resale Guide 2026: Complete Buying and Selling Guide

- Singapore Bridging Loan Guide 2026

Disclaimer: This guide is for general information only and does not constitute financial, legal, or mortgage advice. Interest rates, LTV limits, MSR, TDSR, and CPF rules are subject to change. Always verify current rates with your lender or mortgage broker, and consult a licensed financial adviser before making borrowing decisions. Official references: MAS, HDB, CPF Board, IRAS.