Buyer’s Stamp Duty Singapore 2026: Complete Guide to BSD Rates, Calculation and Remissions

Buyer’s Stamp Duty (BSD) is the foundational property transaction tax that every buyer in Singapore must pay, regardless of nationality, residency status, or how many properties they own. Unlike the Additional Buyer’s Stamp Duty (ABSD) — which targets second-and-subsequent-property buyers and foreigners — BSD is universal. Whether you are a first-time Singapore Citizen buying a public housing flat or a foreign investor acquiring a luxury penthouse, BSD applies equally. Get it wrong in your budget, and you will face an unexpected six-figure bill at the point of signing.

This guide covers everything you need to know about BSD in 2026: the current rates, exactly how the duty is calculated, what is included in the taxable base, how it differs from ABSD, and the complete picture of stamp duty costs for different buyer profiles. All rates reflect the framework introduced on 15 February 2023 for residential property and remain in force as at the date of publication. For official confirmation, always consult the IRAS Stamp Duty for Property page.

Quick Answer — BSD at a Glance

- BSD applies to every buyer — Citizens, PRs, foreigners, companies, and trusts alike.

- Residential rates: 1% → 2% → 3% → 4% → 5% → 6% in progressive tiers (w.e.f. 15 Feb 2023).

- Non-residential rates: 1% → 2% → 3% (simpler three-tier structure, w.e.f. 20 Feb 2018).

- Taxable base is the higher of the purchase price or the property’s open market value.

- BSD must be paid within 14 days of signing the Option to Purchase (OTP) or Sale & Purchase Agreement.

- BSD for a S$1.5 million condo: S$44,600 (effective rate: 2.97%).

- BSD for a S$3 million condo: S$109,600 (effective rate: 3.65%).

- BSD is administered by the Inland Revenue Authority of Singapore (IRAS).

What Is BSD and Why Does It Exist?

Buyer’s Stamp Duty is a documentary tax levied on instruments related to the purchase of property in Singapore. It has existed in Singapore law since the country was a British colony and is codified in the Stamp Duties Act (Cap. 312), administered by IRAS. In contrast to ABSD — which was introduced in December 2011 purely as a demand-management cooling measure — BSD is a revenue instrument: it is part of Singapore’s general tax base and applies to virtually all property acquisitions, not just speculative or investment-driven ones.

BSD was most recently restructured for residential property on 15 February 2023, when the Government added two new upper tiers (5% and 6%) targeting high-value transactions above S$1.5 million and S$3 million respectively. Prior to that, the top residential rate was 4%. The change was targeted at luxury-end transactions and was announced alongside the same cooling-measure package that raised ABSD rates significantly. You can read about the full cooling-measures context in our ABSD Singapore 2026 Complete Guide.

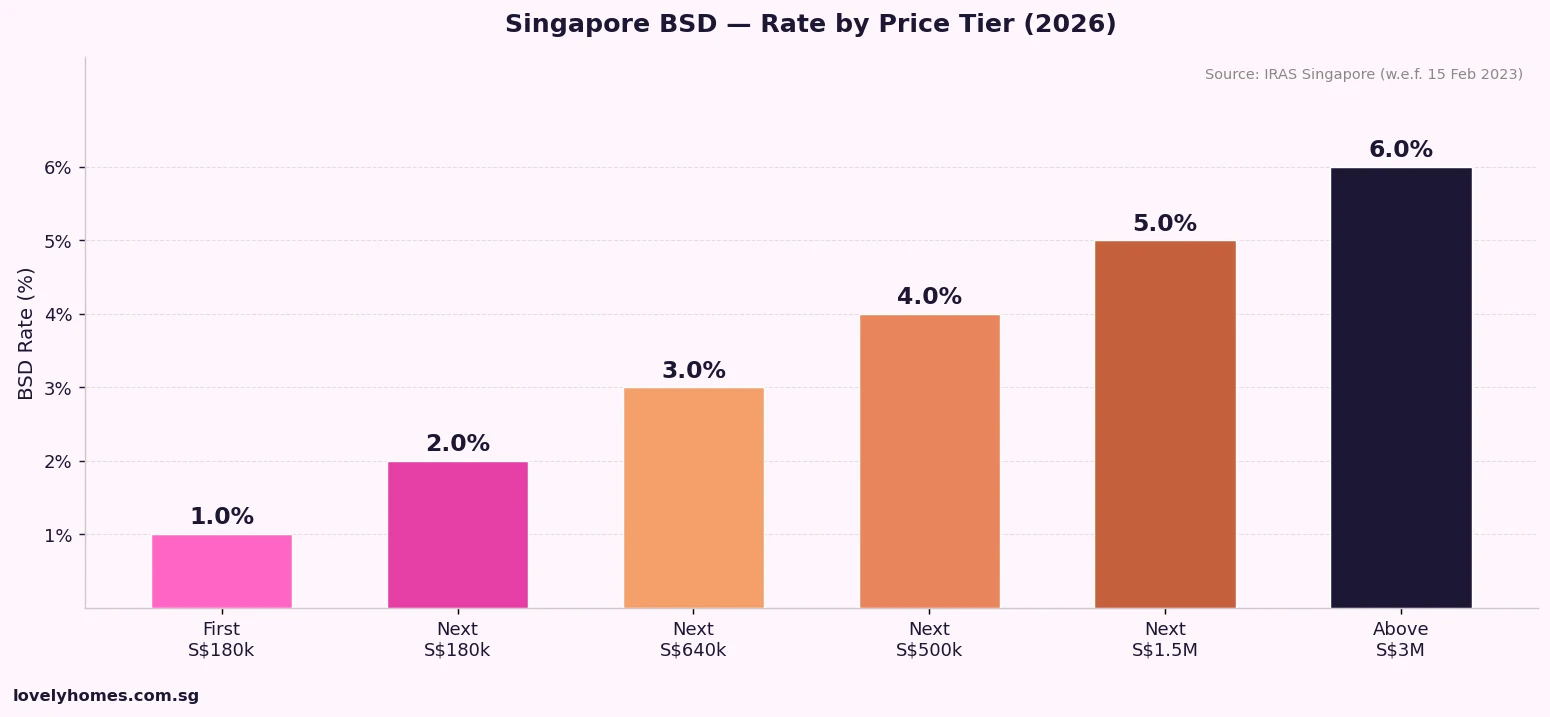

BSD Rates for Residential Property in Singapore (2026)

The current residential BSD rate schedule is progressive, meaning each tier applies only to the portion of the purchase price (or market value, if higher) that falls within that band. The table below sets out the tiers in full.

| Purchase Price (or Market Value) Tier | BSD Rate | Maximum BSD from This Tier |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 | 2% | S$3,600 |

| Next S$640,000 | 3% | S$19,200 |

| Next S$500,000 | 4% | S$20,000 |

| Next S$1,500,000 | 5% | S$75,000 |

| Amount exceeding S$3,000,000 | 6% | Uncapped |

Source: IRAS Singapore. Rates effective 15 February 2023.

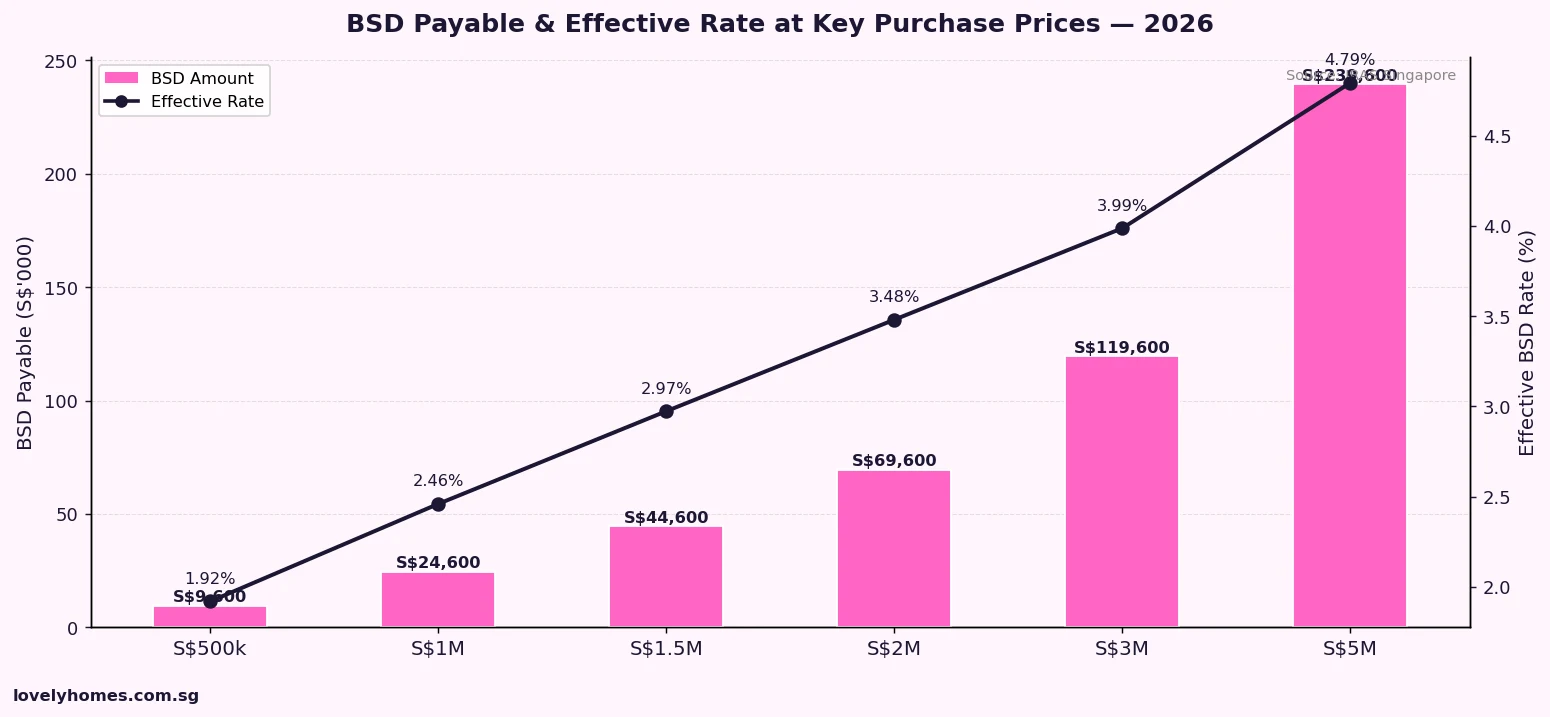

The cumulative BSD cap for a S$3 million property — the last tier before the 6% rate kicks in — is S$109,600. For every dollar above S$3 million, the marginal BSD rate is 6%. A S$5 million property, for instance, attracts BSD of S$109,600 + 6% × S$2,000,000 = S$229,600.

BSD for Non-Residential Property (Industrial, Commercial, Mixed-Use)

Non-residential property — offices, shops, industrial units, mixed-use strata titles, and HDB shophouses — attracts a simpler three-tier BSD structure that has been in place since 20 February 2018.

| Purchase Price Tier | BSD Rate |

|---|---|

| First S$180,000 | 1% |

| Next S$180,000 | 2% |

| Amount exceeding S$360,000 | 3% |

Non-residential BSD is therefore considerably less progressive than its residential counterpart. A S$2 million commercial unit attracts BSD of: 1% × S$180,000 + 2% × S$180,000 + 3% × S$1,640,000 = S$1,800 + S$3,600 + S$49,200 = S$54,600 — compared to S$64,600 for a residential property at the same price. Notably, non-residential property is exempt from ABSD, making it an important consideration for investors who have already consumed their ABSD-free residential quota.

How BSD Is Calculated — Step by Step

BSD is calculated on a progressive basis, applying each tier’s rate only to the portion of value that falls within that band. The taxable base is the higher of the agreed purchase price and the property’s open market value as assessed by IRAS. In practice, for arm’s-length transactions, these figures are usually the same. Where a buyer acquires at below market value — for example, from a related party — IRAS will assess BSD on the market value.

The chart above illustrates a key feature of BSD’s progressive structure: the effective rate (total BSD as a percentage of purchase price) rises gradually but never reaches the 6% marginal rate. Even at S$5 million, the effective rate is approximately 4.6%. This distinguishes BSD from ABSD, where — for a foreigner — the entire purchase price is taxed at a flat 60%.

Worked Example — S$1,580,000 Resale Condominium

Mr and Mrs Lim are Singapore Citizens purchasing a resale 3-bedroom condominium in Clementi for S$1,580,000 as their first property. Here is the full BSD calculation:

| Price Tier | Tier Limit | Rate | BSD for This Tier |

|---|---|---|---|

| First | S$180,000 | 1% | S$1,800 |

| Second | S$180,000 | 2% | S$3,600 |

| Third | S$640,000 | 3% | S$19,200 |

| Fourth | S$500,000 | 4% | S$20,000 |

| Fifth | S$80,000 (remaining) | 5% | S$4,000 |

| Total BSD | S$1,580,000 | Effective 3.04% | S$48,600 |

Since this is the Lims’ first residential property and both are Singapore Citizens, their ABSD is S$0. Their total stamp duty outlay is therefore S$48,600. This must be paid within 14 days of exercising the OTP. BSD is typically paid via IRAS’s myTax Portal (e-Stamping). Their lawyer will ordinarily manage this on their behalf as part of the conveyancing process.

If this were instead the Lims’ second residential property, they would also owe ABSD at 20% × S$1,580,000 = S$316,000, bringing total stamp duty to S$364,600. The BSD component is identical regardless of how many properties they own.

BSD vs ABSD — Understanding the Key Difference

BSD and ABSD are two distinct taxes that can apply simultaneously to the same transaction. The confusion between them is understandable — both are calculated as a percentage of the purchase price and both are paid to IRAS — but they serve entirely different purposes and have very different rate structures.

| Feature | Buyer’s Stamp Duty (BSD) | Additional Buyer’s Stamp Duty (ABSD) |

|---|---|---|

| Who pays? | All buyers | Selected profiles only (see ABSD guide) |

| Policy purpose | Revenue instrument (general tax) | Demand-management cooling measure |

| Rate structure | Progressive (1–6%) | Flat rate on full purchase price (0–65%) |

| Maximum rate | 6% (marginal, above S$3M) | 65% (entities & trusts) |

| Remissions available? | Very limited (developer builds only) | Yes — married SC/SPR upgrader, developers, etc. |

| Applies to HDB? | Yes | Yes (but HDB buyers are usually SC 1st-timers at 0%) |

| Non-residential? | Yes (1%/2%/3% structure) | No — ABSD does not apply to non-residential |

The practical upshot: for most Singapore Citizens buying their first property, BSD is the only stamp duty they pay. For all other buyer profiles — PRs, foreigners, second-time and subsequent Singapore Citizen buyers, and entities — both BSD and ABSD apply simultaneously. To model your full stamp duty liability, use our ABSD Complete Guide, which includes full worked scenarios for every buyer profile.

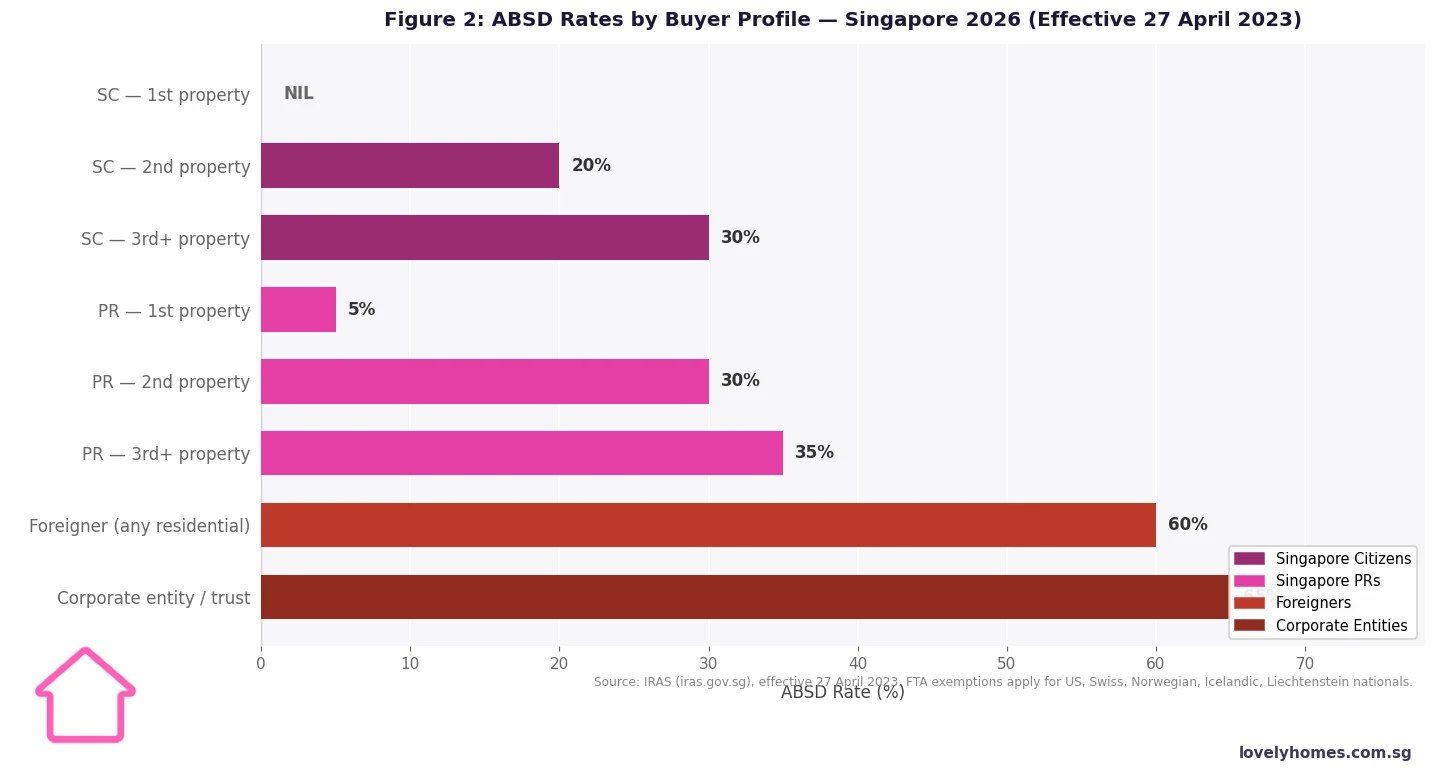

Total Stamp Duty by Buyer Profile — S$1.5 Million Residential Property

| Buyer Profile | BSD | ABSD Rate | ABSD Amount | Total Stamp Duty |

|---|---|---|---|---|

| SC — 1st property | S$44,600 | 0% | S$0 | S$44,600 |

| SC — 2nd property | S$44,600 | 20% | S$300,000 | S$344,600 |

| SC — 3rd+ property | S$44,600 | 30% | S$450,000 | S$494,600 |

| SPR — 1st property | S$44,600 | 5% | S$75,000 | S$119,600 |

| SPR — 2nd+ property | S$44,600 | 30% | S$450,000 | S$494,600 |

| Foreigner — any property | S$44,600 | 60% | S$900,000 | S$944,600 |

| Entity / Trust | S$44,600 | 65% | S$975,000 | S$1,019,600 |

BSD = S$44,600 on S$1.5M (1%×S$180k + 2%×S$180k + 3%×S$640k + 4%×S$500k). ABSD rates: 27 April 2023 framework. SC = Singapore Citizen; SPR = Singapore Permanent Resident.

When and How to Pay BSD

BSD must be paid within 14 days of signing the instrument that triggers the liability. For private residential property, the trigger is typically the Option to Purchase (OTP) or, if no OTP is issued, the Sale and Purchase Agreement (S&P). For HDB flats, the trigger is the signing of the HDB Agreement for Lease.

Payment is made through IRAS’s e-Stamping Portal (accessible via myTax Portal). In practice, your conveyancing lawyer will handle the stamping on your behalf as part of the standard legal process. The stamp certificate is generated electronically and must be produced at completion. Late payment attracts penalties of up to 4× the duty payable under Section 46 of the Stamp Duties Act.

BSD Remissions and Exemptions

Unlike ABSD, BSD has very limited remission provisions. The most relevant situations where BSD may not apply in full are:

Developer remissions for building residential property: Property developers who purchase residential land or existing residential property for the purpose of constructing and selling new residential units may apply to IRAS for BSD remission. This is a specific commercial exception designed to avoid double taxation in the development chain — it does not apply to individual buyers.

Transfers between spouses and immediate family members: The Stamp Duties Act provides for concessionary treatment in limited intra-family transfers, but these are narrow and do not eliminate BSD — they may affect the valuation base or trigger date. Consult a property lawyer before relying on any such arrangement.

HDB Resale Levy and BSD interaction: BSD applies normally to HDB resale flat purchases. There is no interaction between the HDB Resale Levy and BSD — they are entirely separate obligations.

In short: for the vast majority of buyers, there are no BSD remissions. Budget for BSD in full.

What BSD Means for Buyers in 2026

BSD’s restructuring in February 2023 materially increased the cost of high-value acquisitions. A buyer of a S$3 million property now pays S$109,600 in BSD alone — up from S$74,600 under the pre-February 2023 structure, a S$35,000 increase. For S$5 million properties, the increase is S$65,000. These are meaningful sums that affect both the budgeting and the financing of such transactions.

In the broader context of property affordability, BSD at the sub-S$1.5 million residential price range — where most HDB upgraders and first-time private property buyers transact — is relatively modest: S$44,600 on S$1.5 million is 2.97% of the purchase price. The real pinch of Singapore’s stamp duty system comes from ABSD, not BSD. For buyers planning their first property purchase with CPF Housing Grants and a bank loan, BSD is a known, budgetable cost that fits within standard conveyancing estimates.

Singapore’s BSD structure compares favourably with many comparable jurisdictions. Hong Kong charges a flat-rate stamp duty of up to 15% for non-first-time buyers. Australia’s stamp duty is state-based and can reach 5–6% of property value at lower price points. Singapore’s progressive structure, where the 6% rate only applies to the marginal amount above S$3 million, is notably more buyer-friendly at the S$1–2 million range where most transactions occur.

What Might Come Next

BSD rates for residential property have been adjusted three times in the past decade (2018, 2021, and 2023). Each adjustment has moved in one direction: upward, particularly at the high end of the market. If the Government continues its stated objective of moderating luxury segment demand and narrowing the wealth-effects gap between high-end and mass-market property, further BSD increases above S$3 million cannot be ruled out.

Conversely, at the sub-S$1.5 million end — where most owner-occupier transactions occur — there is no political appetite to raise BSD, given the Government’s ongoing commitment to ensuring that public and private housing remains accessible to ordinary Singaporeans. Any future BSD changes are therefore likely to be targeted at the top of the market only. As always, changes to stamp duty rates take effect immediately on the date of announcement and apply to all OTPs granted on or after that date.

Frequently Asked Questions

Does BSD apply to HDB flat purchases?

Yes. BSD applies to all residential property purchases in Singapore, including HDB resale flats, BTO flats (on the Agreement for Lease), and Executive Condominium units. There is no HDB exemption from BSD. For a typical 4-room resale flat at S$550,000, BSD would be: 1%×S$180k + 2%×S$180k + 3%×S$190k = S$1,800 + S$3,600 + S$5,700 = S$11,100.

Is BSD the same as ABSD?

No. They are two separate taxes paid to IRAS on the same transaction. BSD is universal (all buyers, all properties) and progressive (1–6%). ABSD is a surcharge that applies only to selected buyer profiles — foreigners, entities, PRs buying a first property, and all buyers from their second property onward — and is charged as a flat rate on the entire purchase price. You always pay BSD; you only pay ABSD if your buyer profile attracts it. See our ABSD Singapore 2026 Guide for the full rate schedule.

Can BSD be paid using CPF?

Yes, BSD can be paid from your CPF Ordinary Account (OA) for HDB flat purchases. For private residential property, CPF OA funds can also be used to pay BSD, but only after meeting the CPF Minimum Sum requirements and subject to CPF withdrawal limits. In practice, many buyers use cash for stamp duties to preserve their CPF balance for the monthly mortgage servicing — consult your financial planner or mortgage adviser on the optimal approach.

What happens if BSD is paid late?

Under Section 46 of the Stamp Duties Act, late payment penalties are substantial. The penalty is a multiple of the duty payable, depending on the length of the delay: one to three times the duty for delays up to six months, and up to four times for longer delays. In extreme cases, IRAS has the power to seek a court order to enforce payment. In practice, your conveyancing lawyer will ensure that BSD is stamped within the 14-day window. Late stamping almost always results from buyers attempting to handle the stamping themselves without legal assistance.

Does BSD apply to the purchase of a share in a property?

Yes. Where a buyer acquires a fractional share in a property — for example, a 50% interest in a jointly owned private property — BSD is calculated on the proportionate market value of the property that corresponds to the share being acquired. The progressive BSD tiers apply to the full market value of the underlying property first, and the resulting duty is then apportioned to the share acquired. This means the effective BSD rate on a 50% share of a S$2 million property is calculated as if the full S$2 million were the taxable base, then halved — not calculated on S$1 million at a lower tier. IRAS guidance on this is set out in their e-Stamping FAQ.

Is BSD refundable if the sale falls through?

BSD that has been paid on a stamped instrument is generally not refundable if the sale subsequently fails to complete. However, if the instrument itself is rescinded before it takes legal effect — for example, if the OTP lapses without exercise — and the buyer can demonstrate to IRAS that no property changed hands, a refund application under Section 22 of the Stamp Duties Act may be possible. The application must be made within six months of the date of the instrument. IRAS assesses each case on its facts. Always take legal advice before assuming a refund is available.

Do foreign buyers in Singapore pay more BSD than locals?

No. BSD rates are identical for all buyers regardless of nationality or residency status. A Singapore Citizen and a foreign national buying the same S$2 million property both pay exactly the same BSD — S$64,600. The difference in overall stamp duty cost arises entirely from ABSD, which for a foreigner is 60% of the purchase price (S$1,200,000 on a S$2M purchase) versus 0% for a Singapore Citizen buying their first home. This is why total stamp duty for a foreigner buying a S$2 million property (S$1,264,600) is dramatically higher than for a first-time SC buyer (S$64,600).

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Home Loan Complete Guide 2026: Rates, TDSR, MSR and How to Choose

- HDB CPF Housing Grant Guide 2026: EHG, Family Grant, Step-Up, PHG and Singles Grant Explained

- HDB Resale Levy Singapore 2026: Complete Guide for Second-Timer Buyers

- Singapore Property Investment Guide 2026: Strategies, Yields and Market Outlook

- Singapore HDB Resale Guide 2026: How to Buy, Price, and Negotiate

Disclaimer: This article is for general informational purposes only and does not constitute tax, legal, or financial advice. BSD rates and payment rules are governed by the Stamp Duties Act and IRAS administrative guidelines, which may be amended at any time. Always refer to the IRAS official website for the most current rates and verify your stamp duty liability with a licensed conveyancing lawyer or property tax adviser before transacting. LovelyHomes is not a licensed tax or legal advisory firm.