Decoupling for Married Couples Singapore 2026: Saving ABSD on a Second Home — Legally and Step-by-Step

Last updated 28 April 2026. Reflects ABSD rates effective 27 April 2023 and Buyer’s Stamp Duty rates effective 14 February 2023.

Quick Answer — 30-second takeaways

- Decoupling is the legal restructuring of a co-owned residential property so that one spouse ends up holding 100% of it. The other spouse is then restored to first-time-buyer status and can buy a second residential property without paying ABSD.

- For a married Singapore Citizen (SC) couple, ABSD on a S$1.5 million second home is 20% (S$300,000). Decoupling typically costs S$50,000–S$70,000 in BSD on the internal transfer plus legal fees.

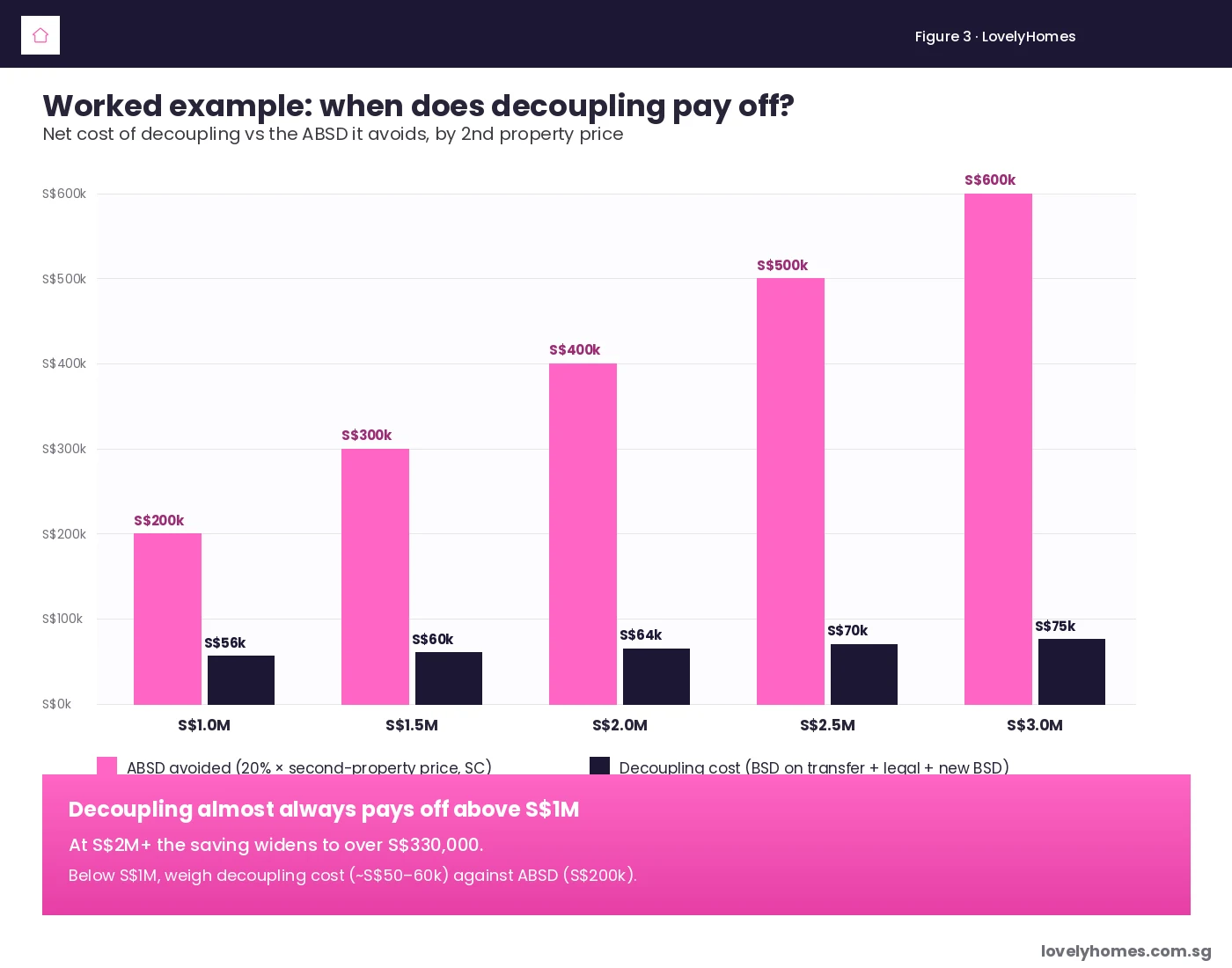

- The maths almost always favours decoupling once the second property is above S$1 million.

- Decoupling is only legal for private residential property. HDB flats cannot be decoupled (since 1 April 2016, except in narrow exceptions like divorce, death or financial hardship).

- The receiving spouse must be able to solo-service the loan under TDSR (60%) and refund any CPF used by the outgoing spouse with 2.5% accrued interest.

- Decoupling is administered by IRAS for stamp duty and CPF Board for refund of utilised CPF; conveyancing must be handled by a licensed Singapore lawyer.

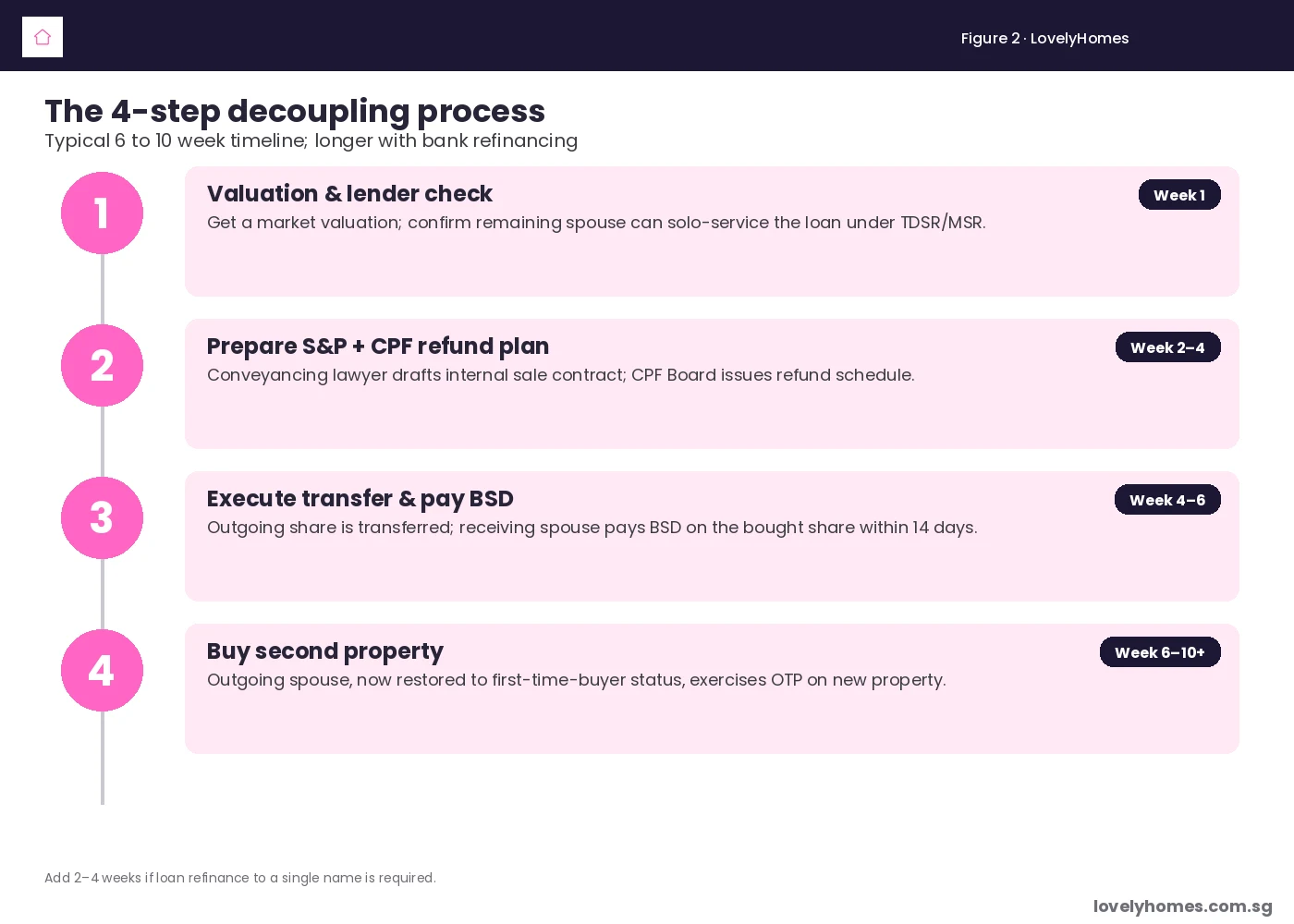

- Allow 6 to 10 weeks end-to-end. Add 2–4 weeks if the loan must be refinanced into one name.

What is decoupling?

“Decoupling” is the informal name for a transaction in which co-owners of a Singapore residential property restructure their ownership so that one party transfers their share to the other. The receiving owner ends up with 100% legal title; the outgoing owner ends up with no residential property in their name.

The reason this is done is rarely sentimental. It is an Additional Buyer’s Stamp Duty (ABSD) avoidance technique — and a perfectly legal one, provided it is structured as an arms-length sale at market value, with stamp duty correctly paid on the transferred share. Once the outgoing spouse no longer owns any residential property, they are restored to “first residential property” status with the Inland Revenue Authority of Singapore (IRAS), and any subsequent purchase falls outside the punitive ABSD net.

The technique was already common before the 27 April 2023 ABSD hike that took the second-property rate for SCs from 17% to 20%. After that hike, decoupling became one of the most-discussed topics on Singapore property forums — and a regular line item in mass-affluent household financial plans.

Why decoupling exists — the ABSD wall

Singapore’s ABSD regime treats any residential property held by either spouse as a household-level holding for stamp duty purposes. Under IRAS rules a married couple is taxed as a single buyer profile: if either spouse has an existing residential property, the next purchase is treated as a second (or third) property and attracts ABSD at the higher band, even if the new property is bought solely in the unencumbered spouse’s name.

The 2026 ABSD ladder for residential property is:

| Buyer profile | 1st residential | 2nd residential | 3rd & subsequent |

|---|---|---|---|

| Singapore Citizen (SC) | 0% | 20% | 30% |

| Singapore PR | 5% | 30% | 35% |

| Foreigner | 60% | 60% | 60% |

| Entity / Trust | 65% | 65% | 65% |

For a married SC couple, the 20% band on a S$1.5 million purchase is S$300,000 — payable upfront, in cash or CPF, within 14 days of exercising the Option to Purchase. That is the wall decoupling is designed to remove.

Who can decouple — and who cannot

Decoupling is only available for private residential property: condos, executive condominiums (after the privatisation date), and landed homes. It is not available for HDB flats — the Housing and Development Board removed the loophole on 1 April 2016, requiring HDB flats to be held jointly under specified eligibility schemes (Public, Fiance, Joint Singles, etc.) and prohibiting “part-share” transfers between named owners except in narrow circumstances like divorce, death of co-owner, financial hardship or marriage to an existing co-owner.

Within private residential property, decoupling typically works for couples where:

- The property has appreciated enough that BSD on the transferred share is meaningfully smaller than the avoided ABSD;

- The receiving spouse can solo-service the existing mortgage under the 60% Total Debt Servicing Ratio (TDSR);

- Both parties are aligned that the outgoing spouse will end up holding the new property in their sole name (with the implications that brings on inheritance, CPF refund and divorce settlement).

The 4-step decoupling process

Step 1 — Valuation and lender check

The conveyancing lawyer obtains a market valuation. The receiving spouse approaches the existing mortgagee bank (or an alternative bank) to confirm they can solo-service the loan under TDSR — meaning total monthly debt repayments cannot exceed 60% of gross monthly income. The Monetary Authority of Singapore caps the loan tenure at 30 years for private property and the loan-to-value ratio at 75% for the first housing loan.

Step 2 — Prepare S&P agreement and CPF refund schedule

The lawyer drafts an internal sale and purchase agreement at market value. CPF Board issues a refund schedule covering all CPF principal previously used by the outgoing spouse plus 2.5% accrued interest from the date each contribution was used. This is non-negotiable: the CPF refund is a lien on the property and must be settled at completion.

Step 3 — Execute the transfer and pay BSD

On completion, legal title transfers from joint to sole ownership. The receiving spouse pays BSD on the value of the share bought (i.e., 50% of the market valuation in a 50/50 joint tenancy, scaled accordingly for tenancy-in-common). BSD must be paid within 14 days of execution; late payment attracts IRAS penalties.

Step 4 — Buy the second property

The outgoing spouse, now restored to “no residential property” status, exercises the Option to Purchase on the new property and pays standard BSD only — no ABSD. There is no waiting period required between Step 3 and Step 4, but in practice the second OTP is often timed to coincide with the new launch ballot date or resale negotiation.

What decoupling actually costs

Decoupling is not free. The cost stack is dominated by BSD on the share transferred at market value. Other line items include legal fees, valuation, and any bank refinancing/discharge fees if the loan moves to a single name.

| Cost line | Typical range | Notes |

|---|---|---|

| BSD on internal transfer | S$8,000 – S$30,000+ | Calculated on 50% of market value at standard BSD rates |

| Conveyancing legal fees | S$5,000 – S$8,000 | One firm typically acts for both spouses; ask for an itemised quote |

| Bank legal subsidy clawback | up to S$2,000 | If the existing mortgage was taken < 3 years ago |

| Valuation report | S$300 – S$600 | Required by both bank and lawyer |

| Bank early-repayment penalty | 1.50% of outstanding loan | Only if existing loan is within lock-in period; waived if simply refinancing in same name |

| CPF refund (with accrued 2.5% interest) | Varies | Cash flow item, not a sunk cost — money is returned to your CPF account |

When does decoupling pay off?

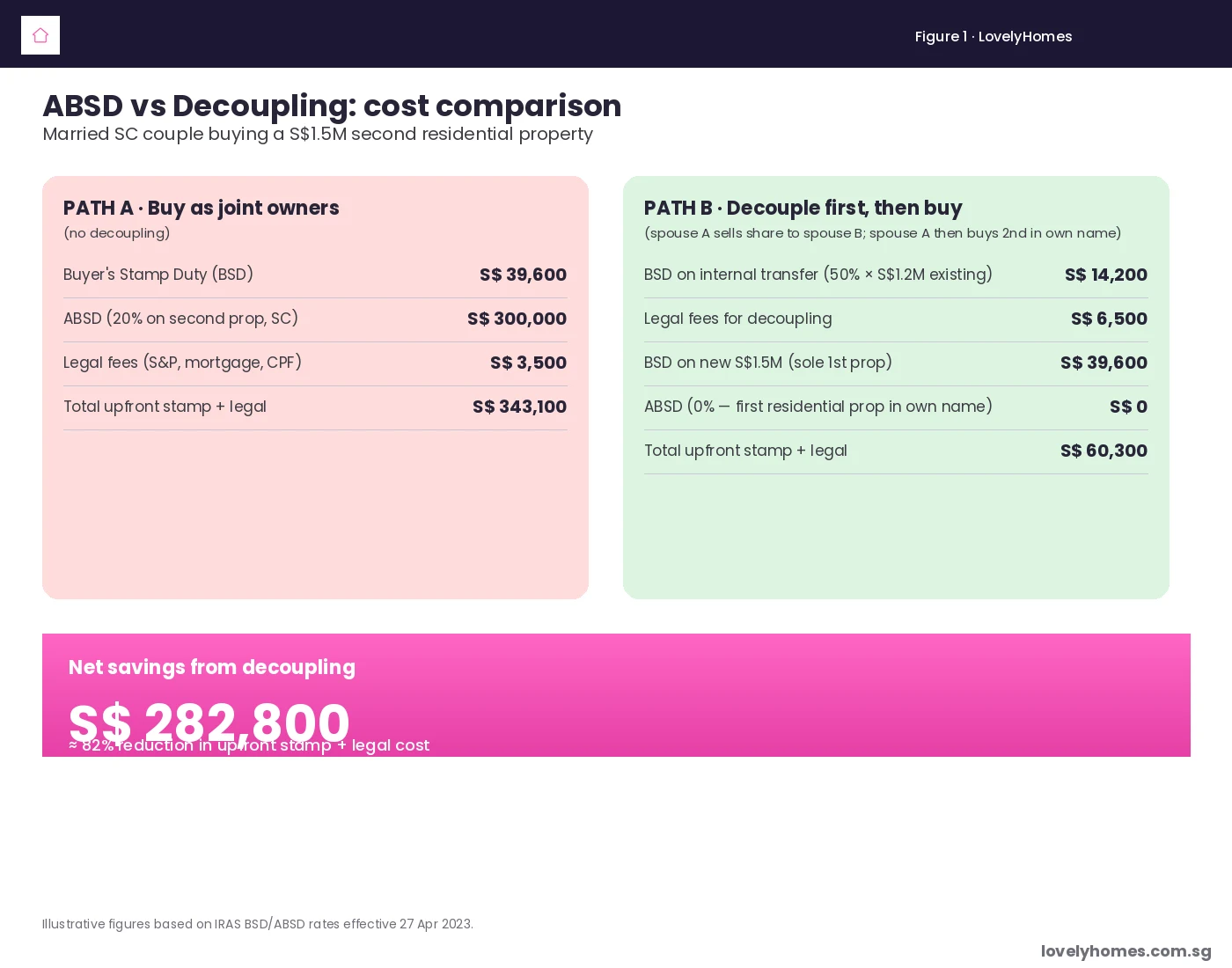

Worked example — Mr and Mrs Tan

Mr and Mrs Tan are both Singapore Citizens. They own a S$1.2 million Outside-Central-Region condo as joint tenants (50/50). They are looking to buy a S$1.5 million Rest-of-Central-Region condo for investment.

Path A — buy as joint owners, no decoupling:

- BSD on S$1.5M = S$39,600

- ABSD at 20% (second residential property, SC) = S$300,000

- Legal fees on the new S&P = S$3,500

- Total upfront: S$343,100

Path B — Mrs Tan sells her 50% share to Mr Tan first; Mr Tan then buys the new property in his sole name:

- BSD on internal transfer of 50% × S$1.2M = S$14,200 (paid by Mr Tan)

- Legal + valuation + bank fees ≈ S$6,500

- Mrs Tan now has no residential property. She buys the S$1.5M ROC condo in her sole name.

- BSD on new S$1.5M = S$39,600

- ABSD = S$0 (first residential property in her name)

- Total upfront: S$60,300

Net saving: S$282,800, or roughly 82% of the original cost. That number is the entire reason decoupling exists as a household financial-planning lever.

The risks people forget to weigh

Decoupling looks like a tax-arbitrage layup. It is — but the structure has consequences that linger long after the BSD is paid.

- Loss of joint protection. Once the property is in one name, the outgoing spouse has no automatic legal interest in it. In divorce, ancillary matrimonial property division still applies — but creditor exposure (e.g. the sole owner’s business debts) shifts.

- Loss of right of survivorship. Joint tenancy carries automatic survivorship: when one spouse dies, the survivor takes the whole property. After decoupling, the property passes via the sole owner’s will (or intestacy rules) — make sure both estate plans are updated immediately.

- CPF cash-flow sting. The accrued-interest refund on CPF used can be substantial — often S$50,000 to S$150,000 in cash that has to be parked back in the outgoing spouse’s CPF account.

- Refinance friction. If TDSR fails on a single income, decoupling cannot proceed. Some couples bridge this by adding a parent or adult child as a co-borrower, but this triggers fresh ABSD considerations.

- Future ABSD changes. The outgoing spouse only retains “first residential property” status until they buy. If the new purchase is delayed and ABSD is hiked again, the saving narrows.

Decoupling vs alternatives

Decoupling is one of three structural ways for couples to manage ABSD. The other two are:

- Buying in one spouse’s name from the start. Cheaper than decoupling because there is no internal transfer cost — but only works if you start the journey with this in mind. Most couples don’t.

- Buying through a trust for a child. ABSD at the trust rate (65%) is usually paid upfront and refunded if the trust beneficiary is a citizen child under 21 and meets IRAS conditions. This is a niche structure for high-net-worth families.

For most existing joint-owner couples, decoupling is the most direct route. The “buy from one name” technique is preferable for new couples planning their property ladder before the first purchase.

What might come next

The Ministry of Finance has reviewed the decoupling loophole multiple times since 2017 without closing it for private property. The April 2023 ABSD hike effectively made decoupling more attractive, not less, because the avoided amount grew. If a future cooling-measures package extends the post-2016 HDB anti-decoupling rule to private property — for example, by treating the receiving spouse’s holding as a “household second property” if the divestment was within 3 years — the technique would be neutered overnight. As of April 2026 there is no public signal of such a move, and Singapore’s policy preference has been to raise stamp duty rather than restrict ownership structures. Treat this as policy risk, not a base case.

Frequently asked questions

Can I decouple my HDB flat?

No. Since 1 April 2016, HDB flats can only be held under HDB’s eligibility schemes (Public Scheme, Fiance Scheme, Joint Singles, etc.), and “part-share” transfers between named owners are not permitted except in narrow circumstances: divorce, death of co-owner, financial hardship, marriage of a co-owner, or renunciation of citizenship by a co-owner. The pre-2016 path of selling one party’s share to the other to free up an ABSD slot is closed for HDB.

Will IRAS treat decoupling as tax avoidance?

IRAS has consistently treated genuine decoupling as a legitimate restructuring, provided the transfer is at market value and BSD is correctly paid on the share transferred. The General Anti-Avoidance Provision in section 33 of the Stamp Duties Act has not been used to challenge bona fide decoupling. The risk arises only if the transfer is not at arm’s length or if the receiving spouse subsequently transfers the property back — that pattern would attract scrutiny.

How long does the whole process take?

Six to ten weeks is typical: one to two weeks for valuation and S&P drafting, three to four weeks to the transfer completion and BSD payment, and a further two weeks of buffer for the second property’s OTP timeline. If the loan needs to be refinanced into a single name with a different bank, add another two to four weeks for credit underwriting.

Can I decouple just before retirement?

Yes, but think carefully. The receiving spouse must continue to solo-service any remaining loan; if their income drops in retirement, TDSR may already be tight. Many retirees opt to redeem the loan in full at decoupling, which avoids TDSR issues but pulls cash or CPF out of liquid reserves.

Can I decouple if my property is still within Seller’s Stamp Duty (SSD) holding period?

Yes. SSD only applies on a sale to a third party within the holding period (3 years from purchase for residential property). An internal transfer between spouses is ordinarily exempt from SSD, but check with your conveyancing lawyer because the exemption depends on documentation of the transfer being a transfer of beneficial interest, not a market sale to an unrelated party.

Does CPF need to be refunded immediately?

Yes. The outgoing spouse’s CPF principal plus 2.5% accrued interest must be refunded to their CPF Ordinary Account at completion. The CPF refund is a lien on the property — completion will not proceed without it. The funds can subsequently be used by that spouse for the second property’s downpayment, subject to CPF housing rules.

What if I’m not married — can two siblings or partners decouple?

Decoupling is structurally available to any joint owners, not only married couples. However, the ABSD treatment is different: unmarried co-owners are not aggregated for ABSD by IRAS in the same way spouses are. Two unmarried joint owners who each own only one residential property are already at first-property ABSD on their respective slots. Decoupling for unmarried co-owners is mostly relevant for estate planning, debt segregation, or pre-marriage clean-up rather than ABSD avoidance.