Singapore Property Decoupling Guide 2026: How to Save ABSD by Transferring Ownership

Quick Answer: What Is Property Decoupling in Singapore?

- Decoupling means one co-owner transfers their share of a jointly-owned property to the other, so the transferring party exits as an owner — and can buy a new property as a “first-time buyer” with 0% ABSD.

- The most common use: a married SC couple who jointly own an HDB flat or private property uses decoupling to allow one spouse to buy an investment condo with 0% ABSD instead of 20%.

- Costs include Buyer’s Stamp Duty (BSD) on the transferred share, legal fees (S$3,000–S$6,000 combined), and a fresh bank valuation — typically S$30,000–S$40,000 all-in for a S$1.8M property.

- The decoupled (remaining) owner must pass TDSR at 55% as a sole borrower — this is the most common deal-killer.

- Decoupling an HDB flat is generally not permitted to facilitate a subsequent private property purchase — HDB rules require both owners to occupy the flat; voluntary transfer usually requires HDB approval and income ceiling checks.

- For private property owners, decoupling is a legal tax-planning strategy upheld by IRAS — provided there is genuine consideration and no sham arrangement.

- Timeline: 6–12 weeks from lawyer engagement to SLA registration. Plan ahead before the intended new purchase.

What Is Property Decoupling?

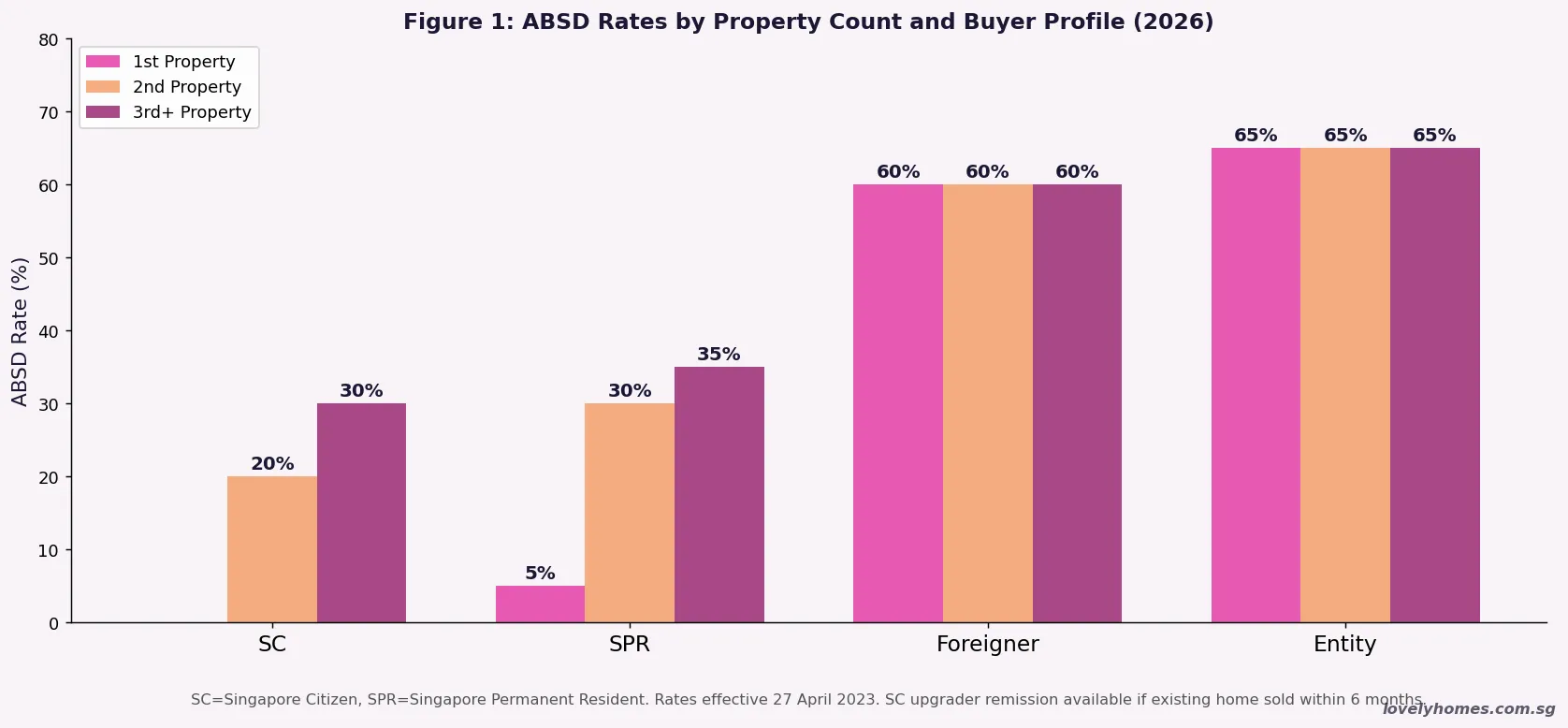

Property decoupling is the process by which one co-owner of a Singapore property transfers their ownership share to the other co-owner. The transferring party is then legally no longer a property owner and — crucially — can buy a new property as a first-time buyer, paying 0% Additional Buyer’s Stamp Duty (ABSD) where they would otherwise have paid 20% (as a Singapore Citizen purchasing a second property) or 30% (as a Singapore Citizen purchasing a third property).

Decoupling is administered under the Land Titles Act (Cap. 157) and is regulated by the Singapore Land Authority (SLA), which updates the property register to reflect the new ownership structure. All stamp duties arising from the transfer are collected by the Inland Revenue Authority of Singapore (IRAS) under the Stamp Duties Act.

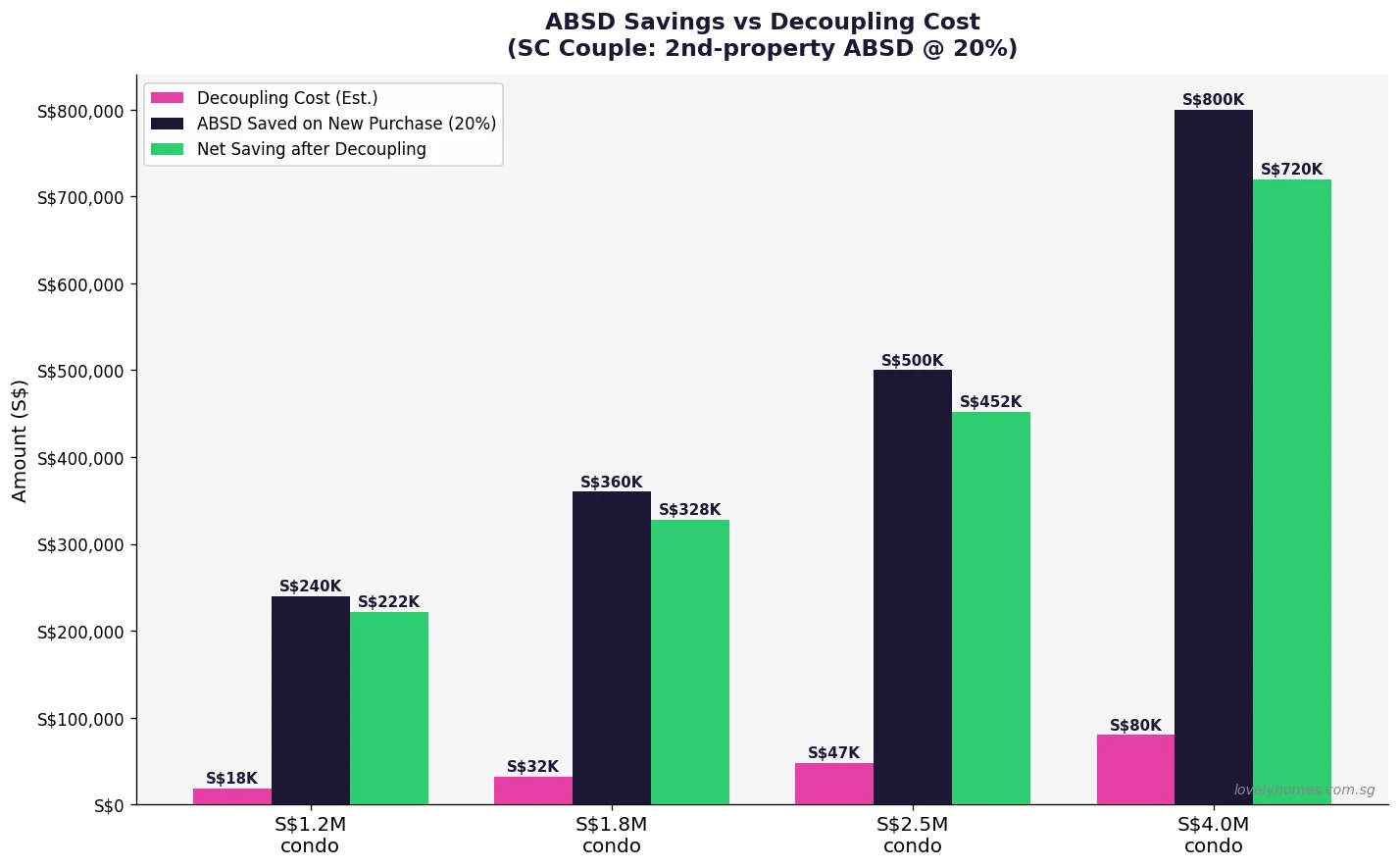

The strategy became widely discussed after successive rounds of ABSD increases — from 7% for Singapore Citizens’ second properties in 2011 to 20% today — made the tax difference between a first and second purchase extremely significant. At a S$1.8M condo, the ABSD delta between a first-time buyer (0%) and a second-time buyer (20%) is S$360,000. A decoupling transaction that costs S$32,000–S$37,000 therefore offers a potential net saving of over S$320,000.

How Decoupling Works: The Mechanics

There are two main ways a co-ownership is structured in Singapore: Joint Tenancy (JT) and Tenancy-in-Common (TiC). In a Joint Tenancy, both owners hold an undivided equal share with right of survivorship — you cannot specify different percentages. In a Tenancy-in-Common, owners hold defined shares (e.g., 60/40) and can sell, will, or transfer their individual share independently.

Decoupling under Joint Tenancy first requires converting the ownership to Tenancy-in-Common (via a unilateral instrument of severance, filed with SLA), then one party transfers their defined share to the other. Under Tenancy-in-Common, the transfer can proceed directly. The receiving party pays Buyer’s Stamp Duty on the value of the acquired share; ABSD may or may not apply depending on how many properties the receiving party will own after the transfer.

Key consideration — CPF: If CPF Ordinary Account funds were used to service the mortgage, the CPF Act requires that when a co-owner transfers their share, the CPF principal plus accrued interest at 2.5% per annum must be refunded to the transferor’s CPF OA. This is not a cash expense but it reduces the seller’s CPF balance available for the next purchase.

Can You Decouple an HDB Flat?

This is one of the most frequently asked questions — and the answer is nuanced. Under HDB rules, the owners of an HDB flat must generally all be listed occupiers and must fulfil the Minimum Occupation Period (MOP) before they can own any private property. Voluntarily transferring a flat interest within a married couple (i.e., removing one spouse as owner) requires HDB approval and the remaining owner must still meet eligibility criteria, income ceiling rules, and the Essential Occupier scheme does not allow the transferring party to immediately buy a private property without potential complications.

IRAS has also scrutinised HDB decoupling arrangements and has in certain cases assessed that ABSD relief was not applicable where the transaction lacked genuine commercial consideration. As a result, HDB decoupling to facilitate immediate private property purchase is generally not a viable strategy — the risk of IRAS anti-avoidance provisions applying is high. Couples who own an HDB flat and wish to invest in private property are better served by completing the MOP, selling the HDB flat, and purchasing the private property — or examining the HDB upgrader ABSD remission scheme.

Private property decoupling, by contrast, has a cleaner legal basis and is widely recognised as a legitimate planning tool by IRAS and the courts, provided it is a genuine arms-length transaction with fair value consideration.

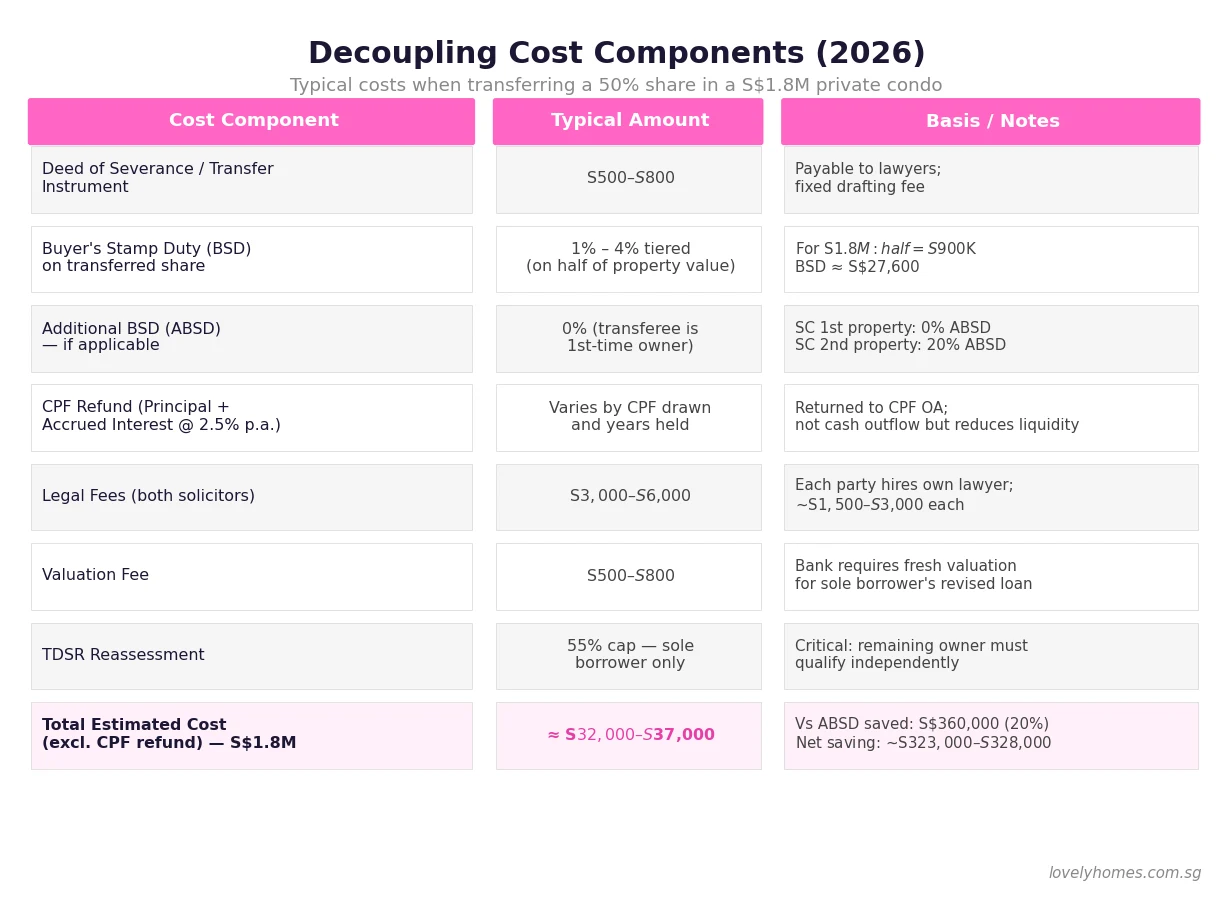

The Stamp Duty Costs of Decoupling

The transferee (receiving party) pays Buyer’s Stamp Duty on the value of the share being acquired. BSD is calculated on the higher of the purchase price and the market value of the share. For a S$1.8M condo where one party acquires the other’s 50% share:

| BSD Tier | Rate | On S$900K share |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 | 2% | S$3,600 |

| Next S$640,000 | 3% | S$19,200 |

| Remaining S$0 (capped at S$900K) | 4% | — |

| Total BSD | — | S$24,600 |

ABSD is payable if the transferee will own more than the number of properties that attracts 0% ABSD after the transfer. If the transferee is a Singapore Citizen and this is their only property after receiving the share, ABSD = 0%. If the transfer results in them owning a second property, 20% ABSD applies on the S$900K share value — S$180,000 in additional stamp duty — which would make decoupling economically unattractive in most cases.

TDSR: The Critical Constraint

The Total Debt Servicing Ratio (TDSR) — capped at 55% of gross monthly income by the Monetary Authority of Singapore (MAS) — applies to the remaining owner who takes on the full mortgage as a sole borrower. This is the single most common reason decoupling fails at the planning stage.

To illustrate: if a couple jointly earns S$18,000 per month and has an outstanding mortgage of S$1.2M on their existing condo at 3.0% interest, their joint monthly repayment is approximately S$5,056. Under joint ownership, their combined TDSR is 28.1% — well within the 55% cap. But if one party decouples, the remaining owner must demonstrate that on their own income they can service S$5,056 per month without exceeding TDSR 55%. If the remaining owner earns S$9,000 per month, their solo TDSR is 56.2% — which just exceeds the cap. The bank will require either the loan to be reduced (requiring a partial capital repayment) or the TDSR to be restructured (longer tenure).

Before proceeding with decoupling, both parties should obtain a bank indicative assessment for the sole-borrower scenario. This should be done before signing any transfer documents.

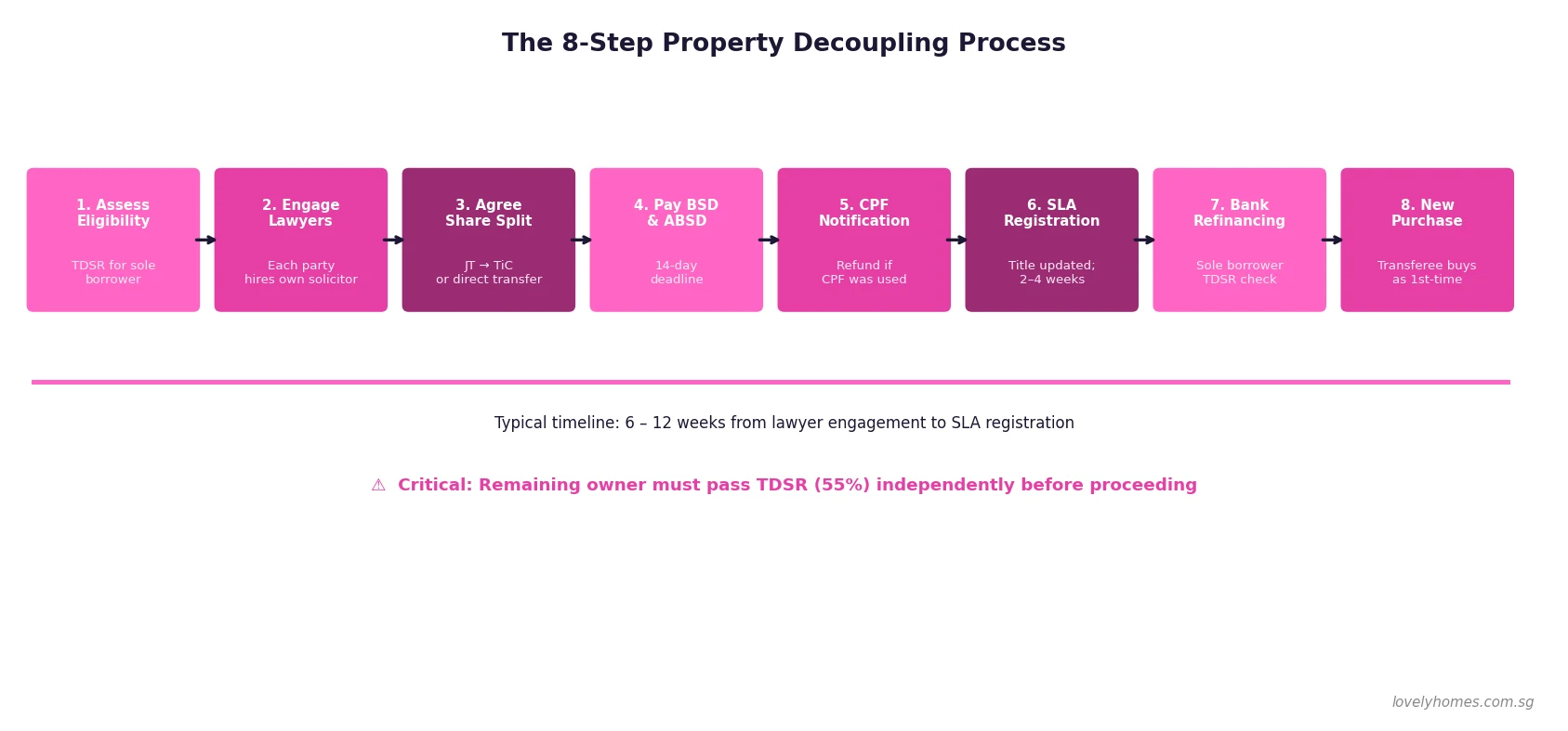

The Step-by-Step Decoupling Process

The decoupling process follows a well-established sequence governed by the Land Titles Act and SLA’s conveyancing procedures. Critically, both the transferor and transferee must engage separate legal counsel — the same firm cannot act for both parties in a transfer.

- TDSR Pre-Assessment — The remaining owner checks with their bank whether they can service the existing mortgage as a sole borrower. The bank will apply the prevailing TDSR stress test (4% p.a. or the contractual rate, whichever is higher). This step is essential before spending on legal fees.

- Engage Two Law Firms — Transferor and transferee each appoint their own conveyancing solicitors. Each firm’s fees range from S$1,500 to S$3,000 depending on complexity.

- Agree on Consideration and Share Structure — The transfer is at market value (or at least not at gross undervalue) to avoid IRAS anti-avoidance. A fresh bank valuation (S$500–S$800) is typically required.

- Compute and Pay Stamp Duty — IRAS must receive the BSD (and ABSD if applicable) within 14 days of the date of the transfer instrument. Late payment attracts penalties.

- CPF Board Notification — If CPF OA funds were used, the lawyers notify CPF Board. The transferor’s CPF principal plus accrued interest (compounded at 2.5% p.a.) is refunded to their CPF OA from the transfer proceeds.

- SLA Registration — The transfer instrument is lodged with SLA. Title registration updates typically take 2–4 weeks. The property register is updated to reflect the sole owner.

- Bank Refinancing — The bank may require the mortgage to be restructured under the sole borrower’s name. This is the point at which TDSR compliance is formally verified by the lender.

- New Purchase by Transferor — Once the SLA title update is confirmed, the transferor (now holding zero properties) can purchase a new property as a first-time buyer — paying 0% ABSD (for Singapore Citizens).

Worked Example: The Wong Family’s Decoupling Plan

Situation: Mr and Mrs Wong are both Singapore Citizens. They jointly own a 99-year leasehold condo in District 19 purchased in April 2021 for S$1,450,000. Current market value: S$1,800,000. Outstanding mortgage: S$980,000 at 3.0% p.a. (25-year term remaining, monthly repayment S$4,644). Mr Wong earns S$10,000/month; Mrs Wong earns S$9,000/month.

Goal: Mrs Wong to decouple (transfer her 50% share to Mr Wong), then purchase a S$1.5M OCR investment condo in her own name at 0% ABSD.

Step 1 — TDSR Check for Mr Wong as sole borrower:

S$4,644 ÷ S$10,000 = 46.4% — within TDSR 55%. ✓ Bank confirms sole-borrower eligibility.

Step 2 — Transfer Costs:

Half of market value = S$900,000

BSD on S$900,000: S$1,800 + S$3,600 + S$19,200 = S$24,600

ABSD: 0% (Mr Wong receives 50% share → still 1 property for him)

Legal fees (two firms): ~S$5,500

Valuation: S$700

Total transfer cost: ≈ S$30,800

Step 3 — CPF Refund to Mrs Wong:

CPF used over 5 years: ~S$210,000 principal + S$26,500 accrued interest = S$236,500 returned to Mrs Wong’s CPF OA. This is not a cash cost — it is her retirement savings being restored.

Step 4 — Mrs Wong’s New Purchase (S$1.5M condo, as 1st-time buyer):

BSD: S$1,500 + S$3,000 + S$18,000 = S$22,500 (BSD on first S$1.5M)

Wait — S$1.5M: First S$180K @1% S$1,800 + next S$180K @2% S$3,600 + next S$640K @3% S$19,200 + remaining S$500K @4% S$20,000 = S$44,600 BSD

ABSD: S$0 (first property)

Bank loan: 75% LTV = S$1,125,000 at 3.1% over 30 years → S$4,802/month

TDSR check: S$4,802 ÷ S$9,000 = 53.4% — just within 55%. ✓

Net Benefit:

ABSD that would have been paid (20% on S$1.5M) = S$300,000 saved

Less decoupling cost: S$30,800

Net saving: S$269,200 — a 9× return on the decoupling cost.

Why This Matters: ABSD Rates Make Decoupling Highly Valuable

Singapore’s ABSD rates for Singapore Citizens stand at 20% for second properties and 30% for third properties — among the highest in the Asia-Pacific region. Compared to Hong Kong’s Buyer’s Stamp Duty (eliminated for non-permanent residents in 2024), Malaysia’s RPGT, or Australia’s state-level stamp duties, Singapore’s ABSD is calibrated specifically to discourage speculative multiple-property ownership by residents.

For Singapore Citizens in the income range of S$9,000–S$15,000 per month — the typical HDB upgrader profile — the ABSD on a second condo purchase ranges from S$240,000 (at S$1.2M) to S$500,000 (at S$2.5M). At these magnitudes, the one-time decoupling cost of S$30,000–S$50,000 represents a 6–10× return on the planning investment, making it one of the highest-value legal tax-planning exercises available to Singapore property owners.

IRAS has not indicated any intention to prohibit private property decoupling, though they have tightened scrutiny of sham arrangements and HDB transfers aimed at circumventing ABSD. The key requirement is that the transfer reflects genuine consideration and commercial reality.

What Might Come Next

Decoupling will remain a viable strategy as long as the ABSD gap between first and subsequent properties remains large. There has been periodic speculation that MAS or MOF might introduce new anti-avoidance provisions targeting systematic decoupling — such as a “look-through” rule treating decoupled couples as a single ownership unit. As of June 2026, no such rule has been announced, and the current legislative framework treats each individual’s property count independently.

However, buyers should note that the government regularly reviews ABSD rates at Budget time. Any reduction in the first-to-second property ABSD delta would reduce the economic case for decoupling. Conversely, any further ABSD increase would make decoupling even more valuable.

Summary: Is Decoupling Right for You?

| Factor | Favourable for Decoupling | Works Against Decoupling |

|---|---|---|

| Property type | Private condo / landed | HDB flat (generally not viable) |

| TDSR (remaining owner) | Well below 55% on sole income | Tight or above 55% on sole income |

| CPF usage | Low CPF drawn / paid mostly cash | Heavy CPF use → large refund to OA |

| Property value | Higher value → larger ABSD saving | Low value → smaller saving relative to cost |

| Intended new purchase | Same or higher value condo | No specific next purchase planned |

| Timeline | 3–6+ months before intended purchase | Urgent (6–12 weeks minimum needed) |

Frequently Asked Questions

Does decoupling trigger Seller’s Stamp Duty (SSD)?

SSD applies if the property is sold within 3 years of purchase: 12% in year 1, 8% in year 2, and 4% in year 3. A decoupling transfer is treated as a sale of the transferor’s share for SSD purposes. If the condo was purchased less than 3 years ago, SSD will apply on the value of the transferred share — significantly increasing the cost. For a S$900,000 share transferred in year 1, SSD would be S$108,000. Plan decoupling only after the SSD holding period has passed.

Can we use CPF to pay for the BSD and costs of decoupling?

Yes, the transferee (receiving party) may use their CPF OA to pay the BSD on the transferred share, provided the property is already within the approved CPF usage framework (e.g., remaining lease covers at least 30 years). The transferor cannot use CPF for costs; however, if their CPF was used in the original mortgage, they will receive a CPF refund which is credited back to their OA — this can then fund the downpayment for their new purchase.

Can a Singapore Citizen decouple with a Permanent Resident spouse?

Yes, but the ABSD implications are more complex. If the SC spouse is the transferee (receives the share), their property count determines the ABSD rate — 0% if it becomes their first or only property. If the SPR spouse is the transferee, they would pay ABSD at 5% (SPR first property) on the received share. Given that SPR ABSD rates are higher than SC rates, it is typically more efficient for the SC spouse to remain as sole owner post-transfer. However, IRAS anti-avoidance provisions require commercial justification — consult a tax lawyer before proceeding.

Does my bank need to approve the decoupling?

Yes. If there is an outstanding mortgage on the property, the bank is a secured creditor with a registered charge. The bank must consent to the transfer of ownership and will typically require the remaining borrower (sole owner post-transfer) to pass a new creditworthiness assessment, including TDSR at 55%. Some banks may require partial repayment to reduce the loan balance before approving the sole-borrower structure. Engage your bank early — before signing the transfer instrument.

Is there a risk that IRAS disallows the ABSD saving?

IRAS has broad anti-avoidance powers under section 33A of the Stamp Duties Act, which allows IRAS to disregard or vary any arrangement that has the effect of reducing stamp duty liability if the arrangement has no commercial substance. For private property decoupling between genuine co-owners at market value, the risk is low provided: (a) the transfer is at full market value supported by a bank valuation; (b) there is genuine consideration passing between parties (not a gift at zero value); (c) the parties are not transferring back within a short period. Sham decouplings — paper transfers with no actual cash or CPF refund — carry serious legal risk.

After decoupling, when can the transferor buy a new property?

As soon as the SLA register is updated to remove the transferor as an owner, they are legally a first-time buyer for ABSD purposes. There is no mandatory waiting period post-registration. However, practically, the buyer should obtain the SLA title search confirming the updated ownership before signing any Option to Purchase (OTP) for the new property — ABSD is assessed on the buyer’s ownership status at the time of OTP exercise.

Can we reverse a decoupling if plans change?

A reversal (transferring the share back) is legally possible but would incur fresh BSD on the re-transfer, and potentially ABSD if the re-acquiring party now holds a second property. The SSD clock also restarts from the date of the original purchase in most interpretations. Reversals are expensive and should be avoided. Decoupling should only be executed when there is a firm plan to proceed with the new purchase.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Joint Property Ownership Guide 2026: Joint Tenancy, Tenancy-in-Common, ABSD and CPF Rules

- Singapore Property Portfolio Guide 2026: ABSD, Yields and Strategy

- Singapore Private Property Buying Costs 2026: Complete All-In Cost Guide

- Singapore Property Mortgage Guide 2026: SORA, Fixed vs Floating, LTV and Refinancing

- Singapore Home Loan Refinancing Guide 2026: When to Switch, What It Costs and How Much You Save

Disclaimer: The information in this article is provided for general educational purposes only. Stamp duty rates, CPF rules, and TDSR regulations cited are based on IRAS, MAS, and CPF Board guidelines current as at June 2026 and are subject to change. LovelyHomes does not provide legal, tax, or financial advice. Before executing any property transfer or decoupling arrangement, consult a licensed conveyancing solicitor, a tax specialist registered with IRAS, and a bank or MAS-licensed mortgage adviser. Authoritative sources: IRAS (iras.gov.sg), SLA (sla.gov.sg), MAS (mas.gov.sg), CPF Board (cpf.gov.sg).